Book 2. Credit Risk

FRM Part 2

CR 14. Derivatives

Presented by: Sudhanshu

Module 1. Types of Derivatives and Derivatives Markets

Module 2. Central Clearing of Derivatives and Modeling Derivatives Risks

Module 1. Types of Derivatives and Derivatives Markets

Topic 1. Introduction to Derivatives

Topic 2. Derivatives Markets

Topic 3. Clearing Derivatives Transactions

Topic 4. Participants in Derivatives Markets

Topic 5. Collateralization in Derivatives Markets

Topic 1. Introduction to Derivatives

- Definition and Characteristics: Contractual agreements between two parties to buy/sell an underlying security or make future payments; varying maturities from short-term (few weeks for futures) to long-term (several years for swaps); value changes over contract life, though many are valued at zero at inception

- Historical Context and Hedging Applications:

- Derivatives have existed for centuries as risk management tools

- Hedge interest rate risk (interest rate forwards/swaps), foreign exchange risk (FX forwards), and commodity price risk (commodity futures/swaps)

- Enable entities to gain or reduce exposure to underlying securities

- Example: Farmer hedges wheat price decline by selling wheat futures to lock in future price

- Market Participants and Structure: Used by corporations, wealth managers, banks, insurance companies, governments, and central banks; some derivatives are standardized (futures) while others are customized (forwards and swaps); markets often dominated by large systemically important banks as derivatives dealers

- Counterparty Credit Risk:

- Derivatives create their own risk despite being hedging tools

- Counterparty credit risk combines market and credit risk

- Risk that the counterparty fails to meet contractual obligations as contract value changes with market conditions

- Managed either bilaterally (each party manages own risk) or centrally via a central counterparty (CCP)

-

Exchange-Traded Derivatives: Standardized contracts created and traded on exchanges with terms specified by the exchange

- Include specific prices, expiry dates, and notional values of underlying securities

- Cannot be altered once established

- Facilitate clearing, settlement, transparency, and accessibility through standardization

- Generally very liquid markets

-

Over-the-Counter (OTC) Derivatives: Customized, private contracts traded informally through global dealer networks between two counterparties

- Enable precise risk transfer and greater flexibility

- Example: Computer manufacturer needing exactly 1,241 ounces of copper in 133 days can create custom contract

- Main disadvantage: Unwinding positions is very difficult or only possible at unfavorable terms

- Dealers cannot simultaneously buy and sell at better prices

- Novation (assignment to another party) typically requires original counterparty permission

- Liquidity varies significantly by market; some OTC markets (like FX) are very liquid while others are illiquid

- Enable precise risk transfer and greater flexibility

Topic 2. Derivatives Markets

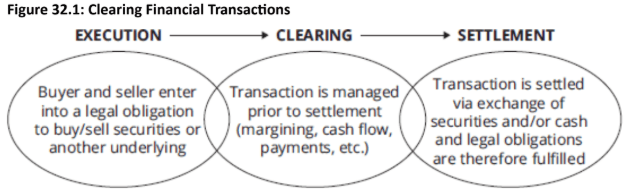

- Clearing: Process before settlement that records counterparties' identities, computes and facilitates margin and payment obligations; represents the period between executing and settling a transaction

- Settlement: Related process of facilitating payment and transferring money from one counterparty to the other when the contract is closed out to satisfy legal obligations

- Counterparty Credit Risk Management: Both clearing and settlement are critical for managing the risk of failure in contractual obligations (nonpayment or non-delivery of assets); particularly important for derivatives with long time horizons

- Bilateral Market Structure: Original counterparty remains unchanged for the contract's duration; each counterparty manages its own risk independently

- Centrally Cleared Market Structure: Central Counterparty (CCP) replaces the original counterparty, steps into the middle of the transaction, becomes the new counterparty to each side, and performs risk management functions

- OTC Central Clearing Trends: While OTC markets have historically been primarily bilaterally cleared, central OTC clearing is gaining prominence; however, central clearing requires standardization and is not feasible for all OTC derivatives

Topic 3. Clearing Derivatives Transactions

Practice Questions: Q1

Q1. The process under which margin transactions are facilitated and computed is best referred to as:

A. clearing.

B. settlement.

C. execution.

D. collateralization.

Practice Questions: Q1 Answer

Explanation: A is correct.

Clearing is the process of recording counterparties’ identities and calculating

margin and payment obligations. Settlement is the process of facilitating payment and transferring money when the contract is closed out. Execution is the initial step of entering into a derivatives contract. Collateralization is the process of posting assets as security to minimize credit risk.

Topic 4. Participants in Derivatives Markets

-

Market Participants for derivatives fall into three major groups:

-

Large Players: Large global banks with significant derivatives portfolios and high trading volumes

- Trade most derivative types: FX, interest rate, equities, commodities, and credit

- Provide significant market liquidity as members of most exchanges and CCPs

- Participate as dealers in OTC markets, controlling approximately 80% of notional value of OTC trades

- Medium-Sized Players: Usually small banks and financial institutions with moderate OTC trading activity

- Execute fair amount of OTC trades across various derivative types

- Members of exchanges and CCPs (local or regional banks hedging IR/FX exposures)

- Trade limited derivative spectrum, typically excluding credit derivatives, commodities, or exotic derivatives

- End Users: Small financial institutions, large corporations, and sovereign governments with specific hedging needs

- Relatively small or specialized derivatives requirements, often hedging single exposure types

- Transact with limited number of counterparties and tend to avoid frequent collateral posting or post illiquid collateral

- Examples: pension funds using interest rate swaps for floating rate exposure, mining companies using commodity forwards for price hedging

- High-quality entities (large regional/sovereign governments, supranationals) can negotiate favorable terms including one-way collateral posting and advantageous rating triggers

-

-

Derivatives can also be classified based on the way they are transacted and collateralized, and fall into four groups:

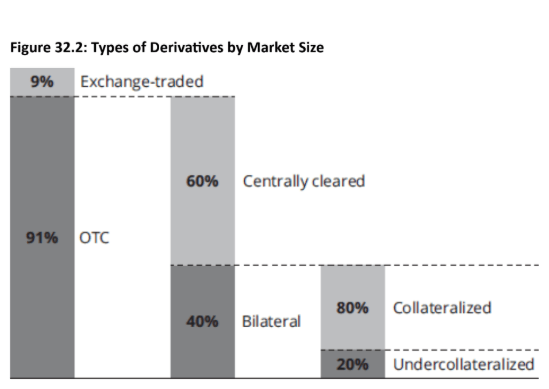

- Exchange-Traded Derivatives: Represent less than 10% of the market; simple, short-dated, and highly liquid instruments that are centrally cleared and collateralized with daily margin posting and mark-to-market settlement, greatly minimizing counterparty credit risk

- OTC Centrally Cleared: Include more complex and less liquid OTC derivatives unsuited for exchange trading; centrally cleared and collateralized with daily variation margin to reduce counterparty risk

- OTC Collateralized: Bilateral OTC trades where counterparties post cash or security collateral to reduce counterparty credit risk, introducing legal and operational risk plus funding costs

- OTC Uncollateralized: Bilateral OTC trades without collateral, typically because counterparties cannot or will not lock up cash or securities; represent the riskiest derivatives markets due to full counterparty credit exposure

- Market Composition: OTC derivatives represent the bulk of the market and are usually not settled daily, though many are centrally cleared and collateralized; collateral posting reduces counterparty risk but introduces legal, operational, and funding cost considerations

Topic 5. Collateralization in Derivatives Markets

Topic 5. Collateralization in Derivatives Markets

Module 2. Central Clearing of Derivatives and Modeling Derivatives Risks

Topic 1. ISDA Master Agreement

Topic 2. Credit Derivatives

Topic 3. Central Counterparties (CCPs)

Topic 4. Margin Requirements for Derivatives

Topic 5. Counterparty Risk Intermediaries

Topic 6. Modeling Derivatives Risk

Topic 1. ISDA Master Agreement

- Overview: Industry standard legal documentation for OTC derivatives developed by the International Swaps and Derivatives Association; introduced in 1985 and widely used since 1992 to govern general terms of privately negotiated contracts

- Risk Reduction: Standardizes terms and reduces counterparty risk through four key provisions:

- Contractual terms for posting collateral

- Events of default and termination definitions

- Netting of obligations

- Closeout process specifications

- Agreement Structure: Main agreement is standardized with an adjustable schedule for customizable terms; typically governed by English or New York law, though negotiation can be time-consuming

- Events of Default: Trigger agreement termination and initiate closeout process; most common include:

- Failure to pay or deliver (most common)

- Breach of agreement

- Credit support default

- Misrepresentation

- Default under a specified transaction

- Cross-default (default on another obligation of the same counterparty)

- Bankruptcy (most common)

- Merger without assumption

Topic 2. Credit Derivatives

- Definition and Purpose: Credit derivatives are instruments designed to hedge exposure to credit risk, providing an efficient mechanism for transferring credit risk between parties

- Common Types:

- Credit Default Swap (CDS) - most common

- Total Return Swaps

- Credit Spread Options

- Market Evolution: Speculation in credit derivatives markets (particularly before the global financial crisis) introduced significant systemic risk, resulting in slower market growth in recent years

- CDS Structure: Involves a credit protection buyer (seeking protection against third-party default) and a credit protection seller

- Counterparty Risk Issue: While CDS protects against third-party credit risk, it introduces credit risk between the two CDS counterparties themselves

- Regulatory Response: Counterparty credit risk in CDS transactions is a key driver behind the push toward central clearing of over-the-counter (OTC) derivatives

Topic 3. Central Counterparties (CCPs)

-

Post-Crisis Importance

-

Following the 2007-2009 financial crisis, central clearing of derivatives and CCPs became critical for systemic risk mitigation

- CCPs provide clearing services for financial transactions between member firms, standing between counterparties as the buyer for every seller and seller for every buyer

-

-

Major CCP Functions:

- Setting standards and rules for clearing members

- Closing out positions of defaulting clearing members

- Requiring initial margin, variation margin, and default fund contributions to mutualize losses

- Establishing extreme event plans (e.g., default fund top-ups or variation margin haircuts)

Topic 3. Central Counterparties (CCPs)

-

Benefits of CCPs

- Credit Risk Transformation: Changes traditional bilateral counterparty risk landscape; CCP becomes the new counterparty for all trades, eliminating direct counterparty credit risk

- Multilateral Netting: CCPs remain market neutral by netting buy-side and sell-side transactions; reduces theoretical system risk through mark-to-market collateralization

- Default Management: In member defaults, CCP replaces nonperforming transactions by substituting defaulted member with another clearing member rather than closing out positions

- Loss Mutualization: Counterparty losses are spread across all clearing members; closeout process facilitated through auctions with netting to minimize position value and volatility

-

Shortfalls of CCPs:

- Systemic Risk Concentration: CCPs must maintain extremely strong credit quality; CCP failure could trigger systemic shock

- Creditor Hierarchy Issues: Credit risk reduction may come at the expense of other market participants like bondholders, as derivatives counterparties are prioritized

- Regulatory Complexity: Cross-border activities require navigation of conflicting legal frameworks and regulations across jurisdictions

-

Advantages:

-

Significant reduction of counterparty credit risk: By stepping in as the new counterparty, the CCP effectively eliminates the original counterparty risk.

-

Improved operational efficiency: The standardized process reduces the complexity of managing multiple bilateral trades.

-

Reduced systemic risk: By mutualizing losses and managing defaults, CCPs prevent a single failure from triggering a cascade of failures across the financial system.

-

-

Shortfalls: A CCP failure could cause a systemic shock. Furthermore, because CCPs prioritize derivatives counterparties, this could be at the expense of other market participants like bondholders.

Topic 3. Central Counterparties (CCPs)

Practice Questions: Q1

Q1. Which of the following statements is not an improvement that centrally cleared markets offer relative to bilateral markets? Centrally cleared markets:

A. remain market neutral by netting trades.

B. offer more flexibility in contract selection.

C. formalize the default closeout process by mutualizing losses.

D. improve counterparty risk by replacing the original counterparty with a series of new counterparties.

Practice Questions: Q1 Answer

Explanation: B is correct.

Bilateral markets permit any type of customized financial contract and customized collateral that is freely negotiated between the two bilateral parties. In a centrally cleared market, flexibility is reduced because contracts must be standardized, and collateral rules are fixed and nonnegotiable.

Practice Questions: Q2

Q2. Which of the following actions is not an advantage of the central counterparty (CCP) in the centralized clearing process?

A. Loss mutualization.

B. Eliminate counterparty risk.

C. Improve operational efficiency.

D. Risk reduction through multilateral nettng.

Practice Questions: Q2 Answer

Explanation: B is correct.

The centralized clearing process used by a CCP does not fully eliminate counterparty risk, but it significantly reduces or minimizes this risk relative to bilateral transactions.

Topic 4. Margin Requirements for Derivatives

- Centrally Cleared Derivatives: Clearing members must post initial margin and variation margin, plus contribute to a default fund to cover losses from defaulting members

- Initial margin required on all trades

- Variation margin covers market value changes in derivatives

- Bilateral (Non-Centrally Cleared) Derivatives: Historically had no or limited margin requirements; regulators globally now introducing similar margin requirements as central clearing to mitigate systemic risk

Topic 5. Counterparty Risk Intermediaries

-

Special Purpose Vehicles (SPVs)/ Special Purpose Entities (SPEs): Off-balance sheet, bankruptcy-remote entity separate from its sponsor created to reduce counterparty risk; SPV investors have creditor priority through flip provisions

- Credit Profile: Receive high credit ratings due to bankruptcy remoteness and typically low leverage; transforms counterparty risk into legal risk

- Legal Risk Concerns:

- Bankruptcy courts may consolidate SPV assets with sponsor in default, negating isolation benefits

- U.S. courts have history of consolidation rulings; U.K. courts generally avoid consolidation unless fraud involved

- Lehman Brothers bankruptcy: U.S. courts ruled flip provisions unenforceable while U.K. courts upheld them

Topic 5. Counterparty Risk Intermediaries

-

Derivatives Product Companies (DPCs): Set up by financial institutions with separate capitalization from parent to obtain very high (typically AAA) credit rating and provide enhanced counterparty protection

- Credit Rating Determinants:

- Minimizing market risk through market-neutral positioning with offsetting contracts

- Parent support via pre-arranged transfer to strong institution or orderly unwinding upon parent failure

- Internal credit risk management with daily mark-to-market and collateral posting

- Crisis Performance: Lehman Brothers and Bear Stearns failures revealed DPCs did not unwind orderly; Lehman DPCs filed Chapter 11 while Bear Stearns DPCs were wound down by JPMorgan, exposing legal, market, and operational risks

- Credit Rating Determinants:

Topic 5. Counterparty Risk Intermediaries

-

Monoline Insurance Companies: Highly leveraged insurance companies with single business line insuring bond repayments through credit wraps to enhance bond ratings; provide credit enhancements often as CDSs for structured credit products

- Normal Operations: Do not post collateral under normal conditions while maintaining very high (usually AAA) credit ratings

- Crisis Failure: During 2007-2009 financial crisis, mounting valuation losses led to rating downgrades, forced collateral posting coinciding with increased insured losses, resulting in multiple monoline failures

- Credit Derivatives Product Companies (CDPCs): Similar to DPCs but with monoline-style business models to provide credit derivative protection for profit

- Risk Profile: Highly leveraged with significant market risk due to lack of offsetting positions; do not post collateral under normal conditions while maintaining AAA ratings

- Crisis Outcome: Many CDPCs failed during or shortly after the global financial crisis, similar to monolines

Practice Questions: Q3

Q3. Which of the following statements is an enhancement offered by the central counterparty (CCP) structure relative to the special purpose vehicle (SPV), the derivative product company (DPC), and the monoline insurance models? The CCP structure:

A. enables financial institutions to remove assets from their balance sheets.

B. enables counterparty risk to be outsourced, but in a non diversified format.

C. spreads losses over a group of counterparties to minimize potential systemic risk.

D. enables a counterparty transaction originator to fail and not affect the other member firms.

Practice Questions: Q3 Answer

Explanation: C is correct.

Through the collateralization and loss mutualization processes, a CCP spreads losses over a group of counterparties—and, in the process, reduces potential systemic risk. SPVs and DPCs are entities that remove assets from a financial institution’s balance sheet. Mono lines enable counterparty risk outsourcing in a non diversified format. In the event that a member fails in the CCP structure, all other member firms are impacted through loss mutualization. It is the DPC that protects itself from the failure of the transaction originator.

Topic 6. Modeling Derivatives Risk

- Value at Risk (VaR): Measures the worst loss over a specified period (typically short-term) at a given confidence level

- Example: one-month VaR of $100,000 at 99% confidence means 99% probability the maximum loss is $100,000

- Advantage: Summarizes risk in a single number, distribution-shape independent

- Limitations: Does not reveal losses beyond the confidence level; may not be subadditive (portfolio risk may not equal sum of individual risks)

- Potential Future Exposure (PFE): Credit risk equivalent of VaR with a long time horizon (often years); measures counterparty credit exposure due to potential gains in derivative positions

- Expected Shortfall (ES): Modification of VaR that measures the average loss beyond VaR; captures the expected loss given that the loss exceeds the VaR threshold

- Model Implementation: VaR and ES typically use historical simulation with real data, recalculating outcomes under different scenarios and backtesting ex post to validate predictive power

- Integrated Risk Modeling: Financial institutions combine VaR and ES with complex quantitative models incorporating correlation, volatility, and dependence factors; model effectiveness depends not on the model itself but on how institutions use them

- Correlation and Dependence Challenges: Historical correlations are poor predictors of future outcomes; correlations change significantly during volatility and stress periods; codependence of risk factors (credit, market, collateral) becomes critical and varies over time

Practice Questions: Q4

Q4. A risk manager at MAB Funds estimates that the fund’s one-week value at risk (VaR) is $1 million using a 95% probability. The fund can, therefore, be expected to lose:

A. an average of $1 million in a week 5% of the time.

B. an average of $1 million in a week 95% of the time.

C. no more than $1 million in a week 5% of the time.

D. no more than $1 million in a week 95% of the time.

Practice Questions: Q4 Answer

Explanation: D is correct.

VaR measures the worst loss over a specified short period using a given confidence level. As a result, the risk manager expects that the fund will lose no more than $1 million in a week 95% of the time (or, it will lose at least $1million 5% of the time).

Copy of CR 14. Derivatives

By Prateek Yadav