Book 2. Credit Risk

FRM Part 2

CR 17. Margin (Collateral) and Settlement

Presented by: Sudhanshu

Module 1. Collateral

Module 2. Collateral Agreements

Module 1. Collateral

Topic 1. Collateral Management

Topic 2. ISDA Documentation and CSA

Topic 3. Valuation Agents

Topic 4. Collateral Agreements and Types of Collateral

Topic 5. Collateral Coverage

Topic 6. Collateral Disputes and Resolutions

Topic 1. Collateral Management

- Basic Concept: In OTC trades (forwards, swaps), the party with negative mark-to-market (MtM) exposure posts collateral (cash or securities) to the party with positive MtM exposure; collateral legally supports risk in an enforceable manner

- Bilateral Management: Collateral management is often bilateral, requiring either side to post or return collateral to whichever party holds positive exposure at any given time

- Credit Risk Mitigation Approaches: Firms manage exposures by limiting notional trade values with counterparties or offsetting trades through netting arrangements

- Four Key Motivations for Collateral Management:

- Reduce credit exposure to enable increased trading volume

- Enable trading with counterparties when credit rating restrictions prevent uncollateralized transactions

- Reduce regulatory capital requirements

- Allow more competitive pricing of counterparty risk

Practice Questions: Q1

Q1. Which of the following features is least likely a benefit of collateralization?

A. Reduces capital requirements.

B. Allows for more competitive pricing of counterparty risk.

C. Reduces market, operational, and liquidity risk.

D. Reduces credit exposure.

Practice Questions: Q1 Answer

Explanation: C is correct.

Collateralizing trades reduces credit exposure (credit risk) and capital

requirements, and allows for more competitive pricing of counterparty risk. However, collateralization also creates other risks including market risk (negative equity leaving exposures partially or fully uncollateralized), operational risk (legal obstacles to take possession of collateral), and liquidity risk (difficulty in selling collateral at a fair market value).

Topic 2. ISDA Documentation and CSA

- Evolution of Standards: Collateral management evolved from having no legal standards to highly standardized through ISDA documentation introduced in 1994

- CSA Purpose: Credit Support Annex incorporated into ISDA Master Agreement enables parties to mitigate credit risk through structured collateral posting

- CSA Governance Areas: Defines collateral eligibility, interest rate payments, transfer timing and mechanics, collateral calculations, haircuts, substitutions, valuation methods and timing, collateral reuse, dispute handling, and event-triggered changes

- Key CSA Parameters:

- Threshold: MtM exposure level that triggers collateral posting requirement

- Initial Margin (Independent Amount): Extra collateral required regardless of exposure level

- Minimum Transfer Amount: Smallest collateral amount that can be called at one time

- Rounding: Standardizes collateral calls/returns to specific sizes for operational convenience

- Haircut: Reduces collateral value to account for potential price decline between calls and default

- Credit Quality: Declining counterparty credit quality increases collateral importance

- Credit Support Amount: Total collateral that either counterparty may call at a given point in time

Practice Questions: Q2

Q2. Which of the following statements is least accurate regarding a credit support annex (CSA) and/or an ISDA Master Agreement?

A. ISDA Master Agreements help standardize collateral management.

B. CSAs must define all collateralization parameters in order to work as intended.

C. Compared to the ISDA Master Agreement, CSAs were first to establish collateral standards.

D. CSAs are incorporated into an ISDA Master Agreement.

Practice Questions: Q2 Answer

Explanation: C is correct.

The purpose of a credit support annex (CSA) incorporated into an ISDA Master Agreement is to allow the parties to the agreement to mitigate credit risk through the posting of collateral. A CSA is created to govern issues such as collateral eligibility, interest rate payments, timing and mechanics associated with transfers, posted collateral calculations, haircuts to collateral securities (if applicable), substitutions of collateral, timing and methods for valuation, reuse of collateral, handling disputes, and collateral changes that may be triggered by various events.

In order to work as they are intended to work, CSAs must define all collateralization parameters and account for any scenarios that may impact both the counterparties and the collateral they are posting.

Topic 3. Valuation Agents

- Primary Responsibilities: The valuation agent calls for collateral delivery and handles all calculations including credit exposure, market values, credit support amounts, and collateral delivery or return

- Appointment Dynamics:

- Larger entities typically insist on being valuation agents when dealing with smaller counterparties

- When counterparties are similar in size, both may serve as valuation agents, though this can lead to disputes and processing delays

- Third-Party Solution: Independent third-party valuation agents can handle the collateral process, process substitutions, resolve disputes, and produce daily valuation reports to avoid conflicts

Topic 4. Collateral Agreements and Types of Collateral

- Legal Framework and Documentation: Collateral agreements establish terms and conditions through legal documents that specify key parameters including currency, agreement type (one-way or two-way), eligible collateral, delivery timing, margin call frequency, and interest rates for cash collateral

- Mark-to-Market Process: Trades are marked-to-market on an ongoing basis (typically daily) with valuations including netting; the party with negative MtM exposure delivers collateral to the counterparty, and collateral positions are continuously updated

- Types of Collateral by Risk Level: Various collateral types are used depending on credit exposure riskiness

- Cash (most common), government and government agency securities, mortgage-backed securities, corporate bonds and commercial paper, letters of credit, and equity

- Collateral Considerations and Challenges:

- Cash supply can become limited during extreme market events

- Agency securities are preferred for liquidity but recent events have raised questions about their true riskiness

- Non-cash collateral creates potential rehypothecation issues and price uncertainty

Topic 5. Collateral Coverage

- Trade Inclusion Strategy: Generally preferred to include maximum number of trades in collateral agreements, but single hard-to-value trades can complicate collateral calls and trigger disputes

- Exclusion Considerations:

- Exclude potentially problematic assets that are complex (exotic options) or illiquid (credit derivatives)

- Focus on subset of trades representing majority of credit exposure

- Handle geographically problematic regions separately if they constitute small portion of trades

- Leave uncollateralized trades that counterparties may struggle to value, avoiding frequent disputes

- Collateralization Benefits: Agreements requiring immediate transfer of undisputed amounts make it generally advantageous to collateralize majority of products

- Common Dispute Sources: Trade population disagreements, trade valuation differences, netting rule interpretations, market data and closing time discrepancies, and valuation of previously posted collateral

Topic 6. Collateral Disputes and Resolutions

- Dispute Resolution Process:

- Disputing party notifies counterparty by end of day following collateral call

- All undisputed amounts transferred immediately; reason for dispute identified

- For unresolved disputes, parties request quotes from multiple market makers (typically four) for mark-to-market value

- Small disputed amounts may be resolved by splitting the difference; larger differences remain uncollateralized until resolved

- Dispute Prevention: Regular trade reconciliation minimizes disputes; dummy reconciliations before trading and periodic reconciliations (weekly/monthly) during trading help preempt future conflicts

Module 2. Collateral Agreements

Topic 1. Collateral Agreement Features

Topic 2. Collateral Aspects

Topic 3. CSA Agreements

Topic 4. CSA Calculations

Topic 5. Collateral Agreement Risks

Topic 6. Regulatory Requirements

Topic 1. Collateral Agreement Features

- Collateral Agreement Terms and Features

- Agreement Timing and Updates: Collateral agreements are negotiated prior to trading and updated before increasing trading activity; parameters must be clearly defined, balancing operational workload with risk mitigation benefits

- Credit Quality Linkage: Terms are often linked to counterparty credit quality to minimize operational burden while maintaining flexibility to tighten terms when credit deteriorates

- Traditional approach links terms to credit rating changes (e.g., downgrades below investment grade)

- Rating-based triggers can create "death spiral" by requiring collateral posting during credit stress

- Alternative metrics include credit spreads, market value of equity, or net asset values

- Margin Call Frequency: Should occur at least daily; repos and swaps cleared via central counterparties often have intraday margining; daily margining has become market standard despite higher operational workload

Topic 1. Collateral Agreement Features

- Collateral Agreement Terms and Features

- Threshold: Level of exposure below which collateral will not be called; represents uncollateralized exposure with only incremental amounts above threshold collateralized

- Reduces operational burden of frequent small collateral calls

- Zero threshold means all exposure is collateralized; infinite threshold means no collateralization

- Typically linked to credit ratings in tiered manner (lower ratings = lower/zero thresholds)

- Initial Margin: Upfront collateral posted independent of subsequent collateralization to mitigate credit spread widening or equity value declines

- Required by stronger credit quality counterparties or those with likely positive exposures

- Represents overcollateralization level, converting counterparty risk into gap risk

- Increases with lower credit ratings (opposite of threshold structure)

- Should be large enough to cover value movements if risky counterparty defaults

- Minimum Transfer Amount: Smallest collateral amount that can be transferred to reduce operational workload

- Additive with threshold (exposure must exceed both combined before collateral call)

- Tied to credit ratings (higher ratings = higher minimum amounts)

- Rounding: Collateral amounts typically rounded (e.g., nearest thousand) to avoid transferring very small amounts

- Threshold: Level of exposure below which collateral will not be called; represents uncollateralized exposure with only incremental amounts above threshold collateralized

-

Haircuts and Collateral Valuation:

- Haircut Definition: Discount applied to posted collateral value; x% haircut means only (1-x)% credit is given

- Valuation percentage is the complement of haircut

- Example: 2% haircut requires posting $102,041 to satisfy $100,000 call ($100,000 / 0.98)

- Haircut Hierarchy by Risk: Cash (0%) < high-quality government bonds < AAA-rated corporate bonds < structured products < equities and commodities

- Key factors: liquidation time, underlying market volatility, default risk, maturity, and liquidity

- Assessed using sophisticated VaR calculations based on current market conditions

- Interest and Cash Flows: Entities pay interest, coupons, dividends, and other cash flows to counterparties posting collateral (unless in default)

- Interest on cash collateral paid at overnight market rate

- During high volatility/illiquid markets, entities may pay above-market rates to incentivize cash collateral posting

- Haircut Definition: Discount applied to posted collateral value; x% haircut means only (1-x)% credit is given

Topic 1. Collateral Agreement Features

Practice Questions: Q3

Q3. Assume a sovereign bond has a haircut of 5% and is used for a collateral call of $100,000. What amount is credited if a $100,000 bond is submitted, and what amount of bond is needed for $100,000 to be credited, respectively?

A. $100,000; $106,263.

B. $95,000; $100,000.

C. $95,000; $105,263.

D. $105,263; $95,000.

Practice Questions: Q3 Answer

Explanation: C is correct.

A haircut is essentially a discount to the value of posted collateral. In other words, a haircut of x% means that for every unit of collateral posted, only (1−x)% of credit will be given. This credit is also referred to as valuation percentage.

If a particular sovereign bond has a haircut of 5% and a collateral call of $100,000 is made, only 95% of the collateral’s value is credited for collateral purposes. That is, in order to satisfy a $100,000 collateral call, $105,263 (= $100,000/0.95) of the sovereign bond must be posted.

Topic 2. Collateral Aspects

- Collateral Substitution: Counterparties can request return of original posted collateral by providing equivalent value of other eligible collateral to meet delivery commitments; substitution requests cannot be refused if replacement collateral meets all eligibility criteria

- Collateral Reuse: Noncash collateral may be sold, used in repo transactions, or rehypothecated to other parties

- Rehypothecation: Transfer of posted collateral to other counterparties as collateral for separate transactions

- Risks: If Party A pledges collateral to Party B, and Party B rehypothecates to Party C, Party B faces both loss from Party C's default and liability to return collateral to Party A

- Market trend: Widespread pre-2007-2009 crisis but significantly less popular post-crisis; parties now increasingly prefer cash collateral

- Segregation of Collateral: Legally protects posted collateral in the event of counterparty insolvency by establishing legal actions to return all non-required collateral

- Works contrary to rehypothecation by reducing counterparty risk through legal protection

- Trade-off: May create funding problems when replacing collateral that could otherwise have been rehypothecated

Practice Questions: Q1

Q1. Collateral agreements could potentially create multiple risks, including liquidity and liquidation risks. Which of the following is most accurate regarding liquidity and liquidation risk?

A. Liquidation risk occurs when the amount of a security sold is large relative to its outstanding volume, which may affect the price of that security.

B. Liquidity risk must be hedged in spot and forward markets.

C. Liquidation risk embodies a transaction cost when collateral is liquidated in accordance with initial margin.

D. Liquidity risk occurs when there are potential pitfalls in the handling of collateral, including human error.

Practice Questions: Q1 Answer

Explanation: A is correct.

Liquidating a security in an amount that is large relative to its typical trading volume may negatively impact its price, leading to a substantial loss.

Topic 3. CSA Agreements

- No CSA Situations: Institutions may avoid CSAs when their credit quality significantly exceeds their counterparty's, or when they cannot meet the operational and liquidity requirements of maintaining collateral commitments

- Two-Way CSAs: Established between relatively similar counterparties as both parties benefit from mutual collateral posting

- Key parameters (threshold, initial margin) may differ based on respective risk levels despite mutual arrangement

- One-Way CSAs: Only one counterparty posts collateral, either immediately or after specific triggering events such as ratings downgrades

- Beneficial to collateral receiver but presents additional risk to the posting party

- Typically used when counterparties differ significantly in size, credit quality, or risk levels

- Credit Quality Linkage: Collateral agreement terms are commonly tied to counterparty credit quality measures

- Minimizes operational workload when counterparty credit is strong

- Enables enforcement of collateralization when credit quality deteriorates

- Quality Metrics: Credit ratings most commonly used, but alternatives include market value of equity, net asset value, and traded credit spreads

- Trade-offs: Benefits of credit rating linkages must be weighed against costs and liquidity demands triggered by ratings downgrades

Practice Questions: Q2

Q2. When dealing with a hedge fund, a bank would most likely negotiate a:

A. one-way agreement in the bank’s favor given the bank’s stronger credit rating.

B. one-way agreement in the bank’s favor agreeing to post collateral to the hedge fund.

C. two-way agreement given the relatively small difference in credit quality between the two entities.

D. two-way agreement where both parties agree to post collateral.

Practice Questions: Q2 Answer

Explanation: A is correct.

The bank would most likely negotiate a one-way agreement in its own favor given the higher credit quality of the bank. This type of negotiation is typical when there are large differences in credit quality between two entities.

Topic 4. CSA Calculations

- ISDA Documentation: Specifies that, at any point in time, the credit support amount is equal to the amount of the requested margin.

- CSA amount is not equal to the portfolio value due to parameters such as thresholds, initial margins, and minimum transfer amounts.

- Single Counterparty Calculation (receiving margin only): Assume a counterparty is only receiving the margin amount. In this case, the credit support amount (margin) calculation when only considering the threshold and initial margin is:

- where

- Thresholds and initial margins work in opposite directions

- When initial margins are present, threshold is typically set to zero

\text{Variation Margin}=\max \left(\text { value }-\mathrm{K}_{\mathrm{A}}, 0\right)+\mathrm{IM}_{\mathrm{A}}\\

\begin{aligned}

\text {value }&=\text { current value of applicable transactions }\\

\mathrm{K}_{\mathrm{A}}&=\text { threshold (fixed amount) }\\

\mathrm{IM}_{\mathrm{A}}&=\text { initial margin (dynamic amount) }

\end{aligned}

Topic 4. CSA Calculations

- Bilateral Margin Calculation: When considering both counterparties, the equation for computing the credit support amount (for variation margin) is:

- where

- Margin Call/Posting Logic:

- Positive result: margin can be called

- Negative result: margin must be posted

- Conditions apply only if margin amount exceeds minimum transfer amount

- Initial Margin Treatment

- Independent Amount: Initial margin is computed separately from variation margin (credit support amount) and is often called the "independent amount"

- No Netting: When both counterparties post initial margin, amounts are not netted and are paid separately

\text{Variation Margin}= \max \left(\text { value }-K_A, 0\right)-\max \left(- \text { value }-K_B, 0\right)-C S B

\begin{aligned}

& K_B=\text { threshold for the counterparty generating the margin calculation } \\

& C S B=\text { credit support balance (margin previously held) }

\end{aligned}

Topic 4. CSA Calculations

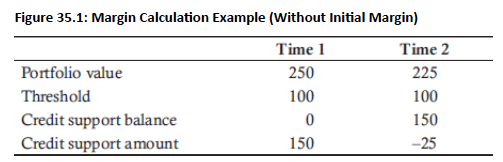

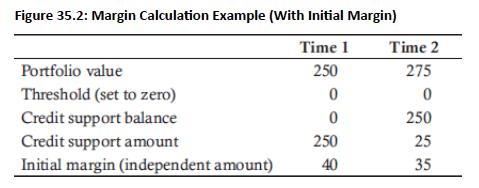

- Example Margin Calculation (With and Without Initial Margin): Fig. 35.1 and 35.2 show margin calculations without and with initial margins, respectively.

- Without Initial Margin:

- Time 1: Portfolio not fully collateralized

- Time 2: Portfolio uncollateralized by 75 (225 - 150), but credit support amount is -25, requiring margin posting up to threshold of 100

- With Initial Margin:

- Time 1: Portfolio is overcollateralized due to initial margin

- Time 2: Portfolio value increase creates 25 margin deficit within initial margin cushion; variation margin increase does not affect independent initial margin amount

Topic 5. Collateral Agreement Risks

-

Overview: Collateralization improves asset recovery in counterparty default but should supplement, not replace, ongoing due diligence. If managed poorly, it creates additional risks.

-

Market Risk: Relates to market movements occurring between collateral postings; relatively small compared to uncollateralized risk but challenging to hedge and quantify

-

Residual risk remains due to minimum transfer amounts, thresholds, and margin period of risk (delay between collateral call and receipt)

-

-

Operational Risk: Can arise from missed collateral calls, failed deliveries, computer/human error, and fraud

- Required Controls: Accurate enforceable legal agreements, robust automated IT systems, timely collateral valuation, and current information on initial margins and transfer requirements

-

Liquidity and Liquidation Risk: Transaction costs (bid-ask spreads, selling costs) arise when liquidating collateral to mitigate counterparty risk

- Large liquidations relative to typical trading volume negatively impact price; slow liquidation exposes counterparty to market volatility

- Key considerations:

- Market capitalization of collateral issue

- Wrong-Way Risk (WWR): Link between collateral value and counterparty credit quality

- Impact of counterparty default on collateral liquidity

Topic 5. Collateral Agreement Risks

-

Funding Liquidity Risk:

-

Refers to institution's ability to settle obligations quickly when due, stemming from CSA funding needs

- Risk is small when markets are liquid and funding costs are low, but escalates significantly when markets become illiquid and funding costs rise sharply

- Counterparties without operational capacity or liquidity for frequent collateral calls face vulnerability

-

-

Default Risk

-

Default of posted security lowers collateral value, potentially beyond haircut coverage

- Cash or high-quality fixed-income securities are preferred collateral types

- Collateral failing to meet specified credit rating must be replaced; poor collateral fails to mitigate counterparty risk

-

-

Foreign Exchange Risk

-

Occurs when counterparties operate in different currencies

- Can be hedged in spot and forward markets, but requires careful management due to dynamic and changing collateral values

-

Topic 6. Regulatory Requirements

- Capital and Regulatory Framework: Non-clearable OTC transactions require higher bank capital compared to standardized OTC transactions; G20 established bilateral collateral requirements in 2011 covering variation and initial margins to minimize systemic risk and reduce regulatory arbitrage

- Market Impact: Additional collateralization forces banks to find new funding sources or exit the OTC derivatives market; funding liquidity risk likely increases during stressed market conditions

- Covered Entities: Financial and systemically important non-financial entities must exchange both variation and initial margin

- Variation Margin Requirements:

- Must be exchanged frequently with full collateral

- Cannot exceed $650,000 threshold

- Must be posted in entirety for post-implementation transactions

- Initial Margin Requirements:

- Must be highly liquid and exchanged without netting

- Must be bankruptcy-protected

- Based on extreme but plausible portfolio movements using 10-day time horizon

- Calculated using regulatory tables or internal models

- Subject to phased-in implementation

Topic 6. Regulatory Requirements

- Operational Requirements: Variation and initial margin must be segregated with strong dispute resolution mechanisms in place

- Credit Support Annexes (CSAs): Covered counterparties establish new or updated CSAs addressing thresholds, minimum transfer amounts, collateral eligibility, haircuts, initial margin calculations, delivery schedules, dispute resolution, and segregation approaches

CR 17. Margin (Collateral) and Settlement

By Prateek Yadav