Book 2. Credit Risk

FRM Part 2

CR 16. Netting, Close-Out and Related Aspects

Presented by: Sudhanshu

Module 1. Netting and Close-Out Procedures

Module 2. Termination Provisions and Trade Compression

Module 1. Netting and Close-Out Procedures

Topic 1. ISDA Master Agreement

Topic 2. Netting Between Two Counterparties

Topic 3. Close-Out Between Two Counterparties

Topic 4. Netting and Close-Out Between Multiple Counterparties

Topic 5. Netting Effectiveness

Topic 1. ISDA Master Agreement

- Purpose and Function: Standardizes OTC agreements to reduce legal uncertainty and mitigate credit risk by creating a framework that specifies terms and conditions related to collateral, netting, and termination events

- Comprehensive Coverage: Forms a single legal contract with an indefinite term that can cover multiple transactions between counterparties

Topic 2. Netting Between Two Counterparties

-

Netting Concepts:

-

Payment Netting: Combining cash flows from different contracts with a counterparty into a single net amount; reduces settlement risk and enhances operational efficiency

- Close-Out Netting: Netting of contract values with a counterparty in the event of default; incorporates two key rights: (1) unilateral contract termination under certain conditions and (2) offsetting amounts due at termination into a single sum

- Impact on Exposure: Without netting, exposure equals the sum of positive mark-to-market values (e.g., two equal and opposite trades of +10 and -10 create exposure of +10); with netting, exposures offset significantly reducing overall risk

-

-

Advantages and Disadvantages of Netting:

- Exposure Reduction: Offsetting exposures reduces risk and improves operational efficiency by managing net positions only

- Disadvantage: Netted exposures can be volatile, making exposure control difficult

- Unwinding Positions: Executing reverse positions with the initial counterparty removes both market and counterparty risk

- Disadvantage: Initial counterparty may impose less favorable terms knowing the entity wants to exit

- Multiple Positions: Trading multiple positions with the same counterparty reduces counterparty risk, obtains favorable terms, and reduces collateral requirements

- Stability: Netting reduces motivation to cease trading with troubled counterparties, making agreements more achievable and preventing exacerbation of financial distress

- Exposure Reduction: Offsetting exposures reduces risk and improves operational efficiency by managing net positions only

Topic 2. Netting Between Two Counterparties

-

Legal Framework and Agreements:

- ISDA Master Agreement: Governs netting agreements (specifically close-out netting) effective upon counterparty bankruptcy; eliminates legal uncertainties under a single universal contract with indefinite term and has obtained legal opinions in most jurisdictions

- Bilateral Netting Coverage: Applies to OTC derivatives, repo transactions, balance sheet loans, and deposits

- Additive Exposures: When no legal netting agreement exists, exposures do not offset and are considered additive

Practice Questions: Q1

Q1. Riggs Resources, LLC, (Riggs) is a commodity trading firm. Riggs has numerous trades outstanding with several counterparties; however, it is concerned with presettlement risk. In order to reduce presettlement risk (the risk that Riggs’s counterparties would default before settlement), it would be most beneficial for Riggs to:

A. have payment netting.

B. have close-out netting.

C. analyze potential losses as the sum of exposures.

D. have netting but not set-off.

Practice Questions: Q1 Answer

Explanation: B is correct.

To minimize presettlement risk, Riggs should have close-out netting. Under closeout, contracts between solvent and insolvent counterparties are terminated and netted. Payment netting would reduce settlement and operational risk, but not presettlement risk. Netting also means individual positive exposures are nonadditive. The terms netting and set-off are synonymous.

Practice Questions: Q2

Q2. Entity XYZ is netting its trades with Entity ABC. Which of the following techniques best describe this type of netting arrangement?

A. Multilateral netting.

B. Bilateral netting.

C. Close-out netting.

D. Additive exposure netting.

Practice Questions: Q2 Answer

Explanation: B is correct.

Bilateral netting is a netting arrangement between two entities and is limited to two entities. Trades with multiple counterparties is known as multilateral netting. Close-out netting refers to netting contract values with a counterparty if the counterparty defaults.

Topic 3. Close-Out Between Two Counterparties

-

Close-Out Mechanisms:

- Close-Out vs. Acceleration: Close-out allows termination of all contracts and creates a claim for compensation; acceleration clauses make future payments immediately due given a credit event (e.g., ratings downgrade)

- Treatment of Exposures:

- Negative mark-to-market: Solvent entity makes full payment to insolvent entity

- Positive mark-to-market: Solvent entity becomes creditor and can terminate/replace contracts

- Court Stays: Courts may impose temporary suspension on agreements to provide "time out" while maintaining validity of termination clauses, as both acceleration and close-out can accelerate financial distress

- Benefits of Close-Out Clauses:

- Reduced Uncertainty: Limits uncertainty in position value with insolvent counterparty; allows solvent entity to fully re-hedge transactions while awaiting claim recovery

- Exposure Freezing: Known, non-fluctuating exposure amounts enable better hedging by the solvent entity, minimizing market risk and trading uncertainty

Topic 4. Netting and Close-Out Between Multiple Counterparties

- Bilateral Netting Limitations: Netting arrangements between only two entities; effective for reducing credit exposure but limited in scope when multiple counterparties are involved

- Multilateral Netting Structure: Involves netting arrangements across multiple counterparties to mitigate counterparty and operational risk

- Example: Entity A has exposure to B, B to C, and C back to A, creating interconnected exposure chains where default of any entity raises loss allocation questions

- Typically achieved through a central entity (exchange or clearinghouse) handling valuation, settlement, and collateralization

- Disadvantages of Multilateral Netting:

- Mutualizes counterparty risk, reducing incentives for entities to monitor each other's credit quality

- Enables accumulation of redundant trading positions, increasing operational costs (mitigated by algorithmic detection systems)

- Requires trading disclosure, potentially exposing proprietary information that firms prefer to keep confidential

Practice Questions: Q3

Q3. Assume the following current MtM values for five different transactions for Entity ABC: +5, −4, +2, +3, and −6. What is the total exposure with and without netting, respectively?

A. 0, 10.

B. 20, 10.

C. 10, 0.

D. 10, 20.

Practice Questions: Q3 Answer

Explanation: A is correct.

The total exposure with netting is 0 (5 − 4 + 2 + 3 − 6 = 0), and the total exposure without netting is 10 (5 + 2 + 3 = 10).

Topic 5. Netting Effectiveness

- Netting Impact on Exposure: Netting can either reduce counterparty exposure or have no effect, but can never increase it; the effectiveness depends on the instrument's ability to carry negative mark-to-market values

- Beneficial Netting Instruments: Trading instruments with potential negative MtM values during their life provide greater netting benefits and exposure reduction

- Limited Netting Benefit Instruments:

- Instruments with only positive MtM: Options with up-front premiums (equity options, swaptions, caps/floors, FX options)

- Instruments with mostly positive MtM: Long options without up-front premiums, certain interest rate swaps, certain FX forwards, cross-currency swaps, off-market instruments, wrong-way instruments

- Rationale for Including Positive MtM Instruments in Netting Agreements:

- Future trades with negative MtM could offset current positive MtM positions

- Inclusion of all trades necessary for effective collateralization

- Ensures no residual counterparty risk when unwinding positions through offsetting mirror trades

Practice Questions: Q4

Q4. Which of the following trading instruments would have the most beneficial effect on netting?

A. Options with up-front premiums.

B. Equity options.

C. FX options.

D. Futures.

Practice Questions: Q4 Answer

Explanation: D is correct.

A trading instrument will have a beneficial effect on netting if it can have a negative mark-to-market (MtM) value during its life. For instruments whose MtM value can only be positive during their life, the effect on netting will not be as beneficial. Instruments with only positive MtM values include options with upfront premiums such as equity options, as well as swaptions, caps and floors, and FX options. Futures can have negative MtM values.

Module 2. Termination Provisions and Trade Compression

Topic 1. Termination Provisions

Topic 2. Walkaway Clauses

Topic 3. Trade Compression

Topic 1. Termination Provisions

-

Termination Events: Allow institutions to terminate trades before counterparties become bankrupt, providing early exit mechanisms

- Reset Agreements: Readjust parameters for heavily ITM trades by resetting them to ATM status

- Reset dates typically linked to payment dates or triggered when certain market values are breached

- Example: Resettable cross-currency swaps exchange MtM value at each reset date and reset the FX rate to current spot, changing the notional amount for one swap leg

-

Additional Termination Events (ATEs)/ Break Clauses: Allow institutions to terminate trades if counterparty creditworthiness declines toward bankruptcy; also called liquidity puts or early termination options

-

Three Trigger Categories:

- Mandatory: Transaction automatically terminates at the break clause date

- Optional: One or both counterparties have the option to terminate at pre-specified dates

- Trigger-based: Requires a specific trigger event (e.g., ratings downgrade) before the clause can be exercised

- Limited Adoption Reasons:

- Break clauses represent discrete collateralization, while continuous collateral posting is more effective

- "Banker's paradox: Clauses are most useful when exercised early, but entities avoid early exercise to preserve counterparty relationships

-

Practice Questions: Q1

Q1. Leverage, Inc., an investment bank, has numerous credit default swaps with XYZ Corp. Leverage has established a break clause with XYZ Corp. to reduce risk. The break clause is trigger-based and may be exercised once the trigger is satisfied. The CEO of Leverage is concerned about a banker’s paradox. Which of the following statements best describe the CEO’s concern?

A. To be effective, the break clause option should not be used too early.

B. The weak firm often recovers after the use of the break clause.

C. The break clause option is used too late, and the weak firm gets weaker.

D. The break clause option is used too early, and is unlikely to avoid systemic risk issues.

Practice Questions: Q1 Answer

Explanation: C is correct.

A break clause (also called a liquidity put or early termination option) allows a party to terminate a transaction at specified future dates at its replacement value. Despite their advantages, break clauses have not been highly popular. One explanation is known as banker’s paradox, which implies that for a break clause to be truly useful, it should be exercised early on, prior to the substantial decline in a counterparty’s credit quality. Entities, however, typically avoid early exercise to preserve their good relationships with counterparties.

Topic 2. Walkaway Clauses

- Mechanism: Allow an entity to avoid net liabilities to a defaulting counterparty while still claiming positive mark-to-market exposure

- Current Status and Criticisms: Popular before 1992 but less common since the 1992 ISDA Master Agreement

- Create additional costs for counterparties in default events

- Generate moral hazard

- Hide transaction risks by pricing the walkaway feature into transactions

- Should be avoided due to these drawbacks

Topic 3. Trade Compression

- Multilateral Netting Process: Achieved through a central entity (exchange or clearinghouse) that handles valuation, settlement, and collateralization for multiple counterparties

- Trade Compression Overview: An approach to multilateral netting without requiring membership in a central organization; reduces gross notional amount and number of trades by eliminating portfolio redundancies across multiple counterparties

- Reduces net exposure without changing the institution's overall risk profile

- Commonly used for OTC derivatives transactions

- Trade Compression Mechanics: Participants submit applicable trades with desired risk tolerance; submitted trades are matched to each counterparty and netted into a single contract

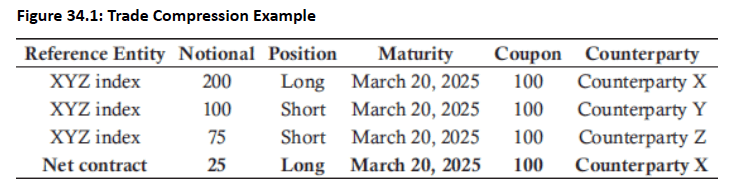

- Example: Three CDS contracts for the same reference entity and maturity with different counterparties can be compressed into one net contract

- Net contract uses weighted average of the three contract coupons as the new coupon rate

Topic 3. Trade Compression

- Trade Compression Benefits: Services like TriOptima help reduce OTC derivatives exposures across various products including interest rates, commodities, and credit derivatives

- CDS market standardization (standard coupons and maturity dates) enhances compression benefits

- Example: Counterparty X holds net contract position with notional exposure of 25 after compression

Copy of CR 16. Netting, Close-Out and Related Aspects

By Prateek Yadav