Book 2. Credit Risk

FRM Part 2

CR 23. An Introduction to Securitization

Presented by: Sudhanshu

Module 1. Securitization Process

Module 2. Cash Waterfall, SPV Structures, Securitization Benefits and Performance Analysis Tools

Module 3. Securitized Structure Ratios

Module 4. Prepayment Forecasting

Module 1. Securitization Process

Topic 1. Securitization

Topic 2. Participants In Securitization Process

Topic 3. Overview Of Securitization Process

Topic 1. Securitization Process

- Securitization Definition: Process of transforming illiquid assets into ABSs or MBSs through packaging, credit enhancements, liquidity enhancements, and structuring; represents an off-balance-sheet transaction when sold without recourse

- Securitizable Assets: Wide range including mortgages, credit card receivables, and auto loans; common feature is that underlying assets generate cash flows

- Key Participants - Originator and Issuer:

- Originator: Entity converting credit-sensitive assets into cash and transferring credit risk away

- Issuer: Third-party SPV that buys assets from originator; must be legally distinct for a "true sale" with no recourse

- Special Purpose Vehicle (SPV/SPE): Separate legal trust or company established specifically for securitization that:

- Separates underlying asset pool from originator's other assets

- Protects securitized assets from originator's insolvency

- Provides credit enhancement through guaranteeing credit quality

- Often incorporated in offshore locations (Cayman Islands, Dublin, Netherlands) for tax purposes

- SPV Structures: May be designated as corporation or trust; in the US, trust structure is most common for accounting purposes; in Europe, corporate structure is permitted under accounting regulations

- SPV Applications: Cash flow securitization (most common), currency conversion through swaps, credit-linked notes issuance, and converting illiquid assets to liquid assets

Topic 2. Participants In Securitization Process

- Structuring Agent: De facto advisor responsible for security design (maturity, credit rating, credit enhancement) and forecasting interest and principal cash flows; may also serve as sponsor

- Trustee: Holds fiduciary responsibility to safeguard investor interests, monitors assets based on pre-specified conditions (minimum credit quality, delinquency ratios)

- Financial Guarantor: Insurance company that "wraps" deals by guaranteeing financial support if SPV defaults; more common in master trust arrangements

- Custodian: Evolved from safeguarding physical securities to collecting and distributing cash flows from assets like equities and bonds

- Credit Rating Agencies: Provide formal credit ratings, quantify originator's corporate credit quality, and analyze competitors, industry, regulatory issues, SPV legal structure, and cash flows; may trigger restructuring if ratings are too low

Topic 3. Overview Of Securitization Process

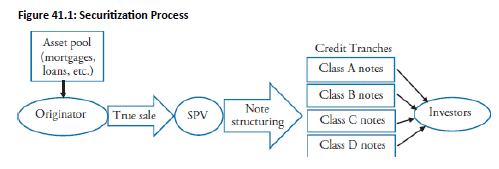

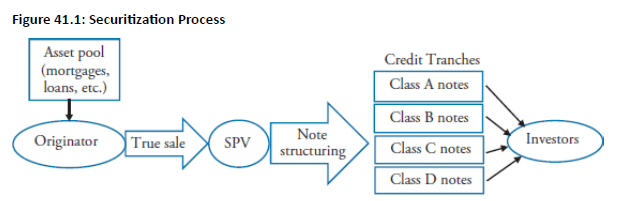

- Process Overview (Fig 41.1): SPV purchases assets from originator, funds purchase by issuing notes to investors, with structure customized via tranches to meet investor credit quality needs; allows originator to remove credit risk and assets from balance sheet

Practice Questions: Q1

Q1. Which of the following statements most accurately describes the effect of selling a loan without recourse?

A. The bank that sells the loan retains a contingent liability.

B. The bank that sells the loan bears a specified percentage of the credit risk.

C. The loan is removed from the balance sheet of the bank that sells the loan.

D. The purchaser has the right to sell the loan back to the bank that originated the loan.

Practice Questions: Q1 Answer

Explanation: C is correct.

When a bank originates a loan and then sells it without recourse, the loan is removed from the bank’s balance sheet, and the purchaser bears all of the credit risk.

Topic 2. The Securitization Process

-

Step 1: Origination. The originator (e.g., a bank) creates a pool of credit-sensitive assets, such as residential mortgages, auto loans, or credit card receivables.

-

Step 2: True Sale. The assets are sold to a legally distinct SPV to separate them from the originator's financial state. This "true sale" is crucial because it ensures the assets are not considered part of the originator's bankruptcy estate.

-

Step 3: Structuring & Issuance. The SPV structures the assets into tranches and issues securities to investors, using careful packaging, credit enhancements, and liquidity enhancements.

-

Step 4: Cash Flows. The payments from the underlying assets are collected and distributed to investors in a predetermined order, a process known as the "cash waterfall."

Topic 3. Roles of Participants

-

Originator: The entity that creates the assets and sells them. This could be a bank, finance company, or other corporation. Their primary role is to pool the assets and sell them to the SPV.

-

Issuer (SPV/SPE): The separate legal entity that buys the assets and issues the securities. The SPV is created solely for this purpose and is designed to be "bankruptcy-remote," meaning its financial condition is separate from the originator.

-

Structuring Agent: Typically an investment bank, this agent designs the securities and determines the structure of the deal, including forecasting the cash flows from the underlying assets and arranging the different tranches.

-

Trustee: A third party, often a commercial bank, responsible for safeguarding the investors' interests. The trustee ensures the SPV adheres to the terms of the legal agreement and oversees the distribution of cash flows according to the waterfall.

-

Financial Guarantor: An insurance company that may provide a financial guarantee against losses, covering the loss of principal in the collateral pool. This reduces the risk for investors and can help the securities achieve a higher credit rating.

-

Credit Rating Agencies: Organizations like Moody's or S&P that provide formal credit ratings for the different tranches of the securities to help investors assess the risk and determine the appropriate pricing.

Module 2. Cash Waterfall, SPV Structures, Securitization Benefits and Performance Analysis Tools

Topic 1. Cash Waterfall Process

Topic 2. SPV Structures

Topic 3. Securitization Benefits to Financial Firms

Topic 4. Securitization Benefits to Investors

Topic 5. Credit Enhancements

Topic 6. Performance Measures for Securitized Structures

Topic 1. Cash Waterfall Process

- Tranche Structure: Securitization pools assets into different classes (tranches) designed to meet specific investor needs with varying credit quality and risk levels

- Overcollateralization: Method to enhance credit quality of lowest-rated assets by issuing notes with principal value less than the underlying asset pool

- Example: 101 mortgages backing 100 mortgage notes provides one-mortgage cushion against default before investors suffer losses

- First-Loss Piece (Equity Tranche): Lowest credit quality class where losses are first absorbed in default events

- Often retained by the originator, hence called "equity piece"

- Typically non-rated and absorbs initial losses before senior tranches are affected

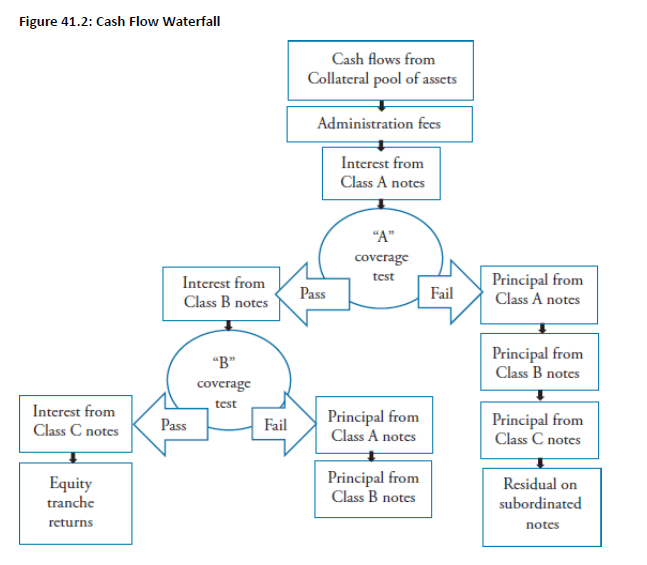

- Cash Waterfall Process: Defines the order in which payments from the asset pool are distributed to investors

- Senior tranches receive payments before junior tranches

- Third-party administrator runs coverage tests to ensure sufficient cash flows for outstanding liabilities

- Coverage Test Mechanics (Figure 41.2):

- If coverage test passes: Interest payments made to subordinate tranche levels

- If coverage test fails: Principal repayment begins with most senior tranche first

Topic 1. Cash Waterfall Process

Practice Questions: Q1

Q1. A major benefit of securitization for a financial institution is the ability to remove assets from the balance sheet, which lowers risk and the required regulatory capital. While a large portion of the risk is removed from the balance sheet the originating financial institution often maintains a portion of the risk. Which of the following terms best identifies the risk that is maintained by the originator?

A. Correlation.

B. Excess spread.

C. First-loss piece.

D. Guarantor of collateral value.

Practice Questions: Q1 Answer

Explanation: C is correct.

The originator often maintains ownership of the first-loss piece, which is the class of assets with the lowest credit quality and is the most junior level where losses are first absorbed in the event of a default.

Topic 2. SPV Structures

-

Three Main SPV Structures: Amortizing, revolving, and master trust structures are used based on how payments are received over the ABS's life

-

Amortizing Structure:

-

Payment Mechanism: Principal and interest payments made on an amortizing schedule; operates as a pass-through structure where payments are made as coupons are received

- Common Applications: Residential mortgages, commercial mortgages, and consumer loans with defined amortization schedules

- Valuation: Based on expected maturity and weighted-average life (WAL)

- WAL measures the time-weighted period assets remain outstanding

- Must include prepayment assumptions due to borrowers' early payoff options

-

-

Revolving Structure:

- Payment Characteristics: Principal repaid in large lump sums rather than pre-specified amortization schedules; used for products with short time horizons and high prepayment rates

- Common Applications: Credit card debt and auto loans

- Operational Process: Principal payments used to purchase new receivables with similar criteria; investors repaid through controlled amortization or soft bullet payments (single lump sums)

Topic 2. SPV Structures

-

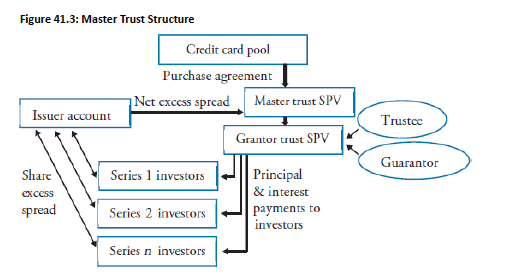

Master Trustee Structure:

- Purpose: Enables SPVs to make frequent issues or multiple securitizations from a single asset pool

- Common Applications: Mortgages and credit card debt securitization

- Structure (Fig 41.3): Two-tier SPV arrangement with master trust (SPV 1) and grantor trust (SPV 2)

- Originator sells assets to master trust for cash

- Master trust deposits assets in grantor trust and receives beneficial interest

- Claims backed by beneficial interest rather than assets directly

- Excess Spread: High-yield debt less ABS issuance costs creates excess spread (difference between cash inflows from assets and interest payment outflows)

- Remaining spread after administration expenses held in reserve account for future losses

- Unused excess spread returned to originator

- Credit Enhancement: Financial guarantors used for uncollateralized debt (e.g., credit cards); excess spread shared across multiple series to cover defaults

- Key Differentiator: Multiple series investors share excess spreads, distinguishing master trusts from amortizing and revolving structures

Topic 2. SPV Structures

-

Fig 41.3 shows a master trustee structure.

Practice Questions: Q2

Q2. Securitized products are often customized to meet the needs of the investor as well as the originator. What type of asset-backed securities (ABSs) typically uses a revolving structure?

A. Residential mortgage.

B. Credit card debt.

C. Commercial mortgage.

D. Commercial paper.

Practice Questions: Q2 Answer

Explanation: B is correct.

Revolving structures are used with products that are paid back on a revolving basis, such as credit card debt or auto loans. Credit card debt does not have a pre specified amortization schedule; therefore the principal paid back to investors is in large lump sums rather than amortizing schedules.

Topic 3. Securitization Benefits to Financial Firms

- Funding Assets: Securitization provides funding that supports growth, diversifies the funding mix, and reduces maturity mismatches

- Diversified funding mix reduces risk and cost of funding

- Originators separate assets from balance sheet through SPV

- Enhanced Credit Ratings and Cost Savings: ABS issued by SPVs often carry higher credit ratings than bonds issued directly by originators, lowering debt issuance costs despite ABS markets being less liquid than bond markets; Cost savings from securitization create cash surplus for originator

- Duration Matching: Securitization allows SPV-issued notes to match the time horizon of underlying assets

- Addresses common maturity mismatch where short-term liabilities (savings/checking accounts) fund long-term assets (mortgages)

- Removes duration mismatch risk from originator's balance sheet

- Capital Management and Regulatory Relief: Basel I capital requirements (e.g., 8% of total asset value) incentivize banks to securitize assets

- SPVs are not subject to bank capital requirements and selling assets to SPVs reduces regulatory capital requirements (though originators often retain first-loss piece)

- Reduced capital requirements increase return on equity (ROE), a key investor metric

- Risk Management: Removes NPAs from balance sheet along with associated credit risk and negative sentiment; Originator may still receive surplus profit from SPV if non-performing assets generate future cash flows

Topic 4. Securitization Benefits to Investors

- Access to New Asset Classes: Investors gain access to previously unavailable liquid assets, enabling different risk-reward profiles and sector diversification

- Enhanced Risk-Reward: Securitized notes often provide higher risk-reward than corporate bonds with equivalent credit ratings

- Improved performance results from originator retaining equity tranche

- Diversified risk exposure through pooled assets in SPV versus single corporate entity

- Market Efficiency: Securitization broadens markets through diversification and customization of new liquid products

- Increased liquidity reduces transaction costs for both borrowers and investors

Topic 5. Credit Enhancements

-

Purpose: Improve credit ratings for ABS/MBS tranches by absorbing losses or controlling cash flows, with greatest benefits for lowest-rated assets

-

Collateral Loss Absorption Enhancements

- Overcollateralization: Principal value of issued notes is less than principal value of underlying assets; additional collateral absorbs initial losses with no investor impact, commonly used for lowest-rated note classes

- Pool Insurance: Composite insurance company provides coverage for principal losses in the collateral pool in the event of SPV default

-

Cash Flow Control Enhancements

- Subordinating Note Classes: Tranching creates senior-subordinate structure where:

- Junior (Class B) notes are subordinate to senior (Class A) notes

- Class B investors receive no principal payments until Class A notes are fully redeemed or rating agency requirements are met

- Collateral pool must pass performance tests before making subordinate principal payments

- Margin Step-Up: Coupon rate increases after a call date, providing investor incentive while giving issuer refinancing option if increased coupons exceed market rates

- Excess Spread: Difference between cash inflows from underlying assets and cash outflows for interest payments on ABS issues:

- Structured so SPV liabilities (issued notes) have lower cost than SPV assets (receivables)

- Remaining spread after administration expenses held in reserve account for future losses

- Excess returned to originator if no future losses occur

- Subordinating Note Classes: Tranching creates senior-subordinate structure where:

Practice Questions: Q3

Q3. Which of the following statements regarding credit enhancements in the process of structuring a securitization through a special purpose vehicle (SPV) is correct?

A. The securitization process is structured such that the asset side of the SPV has a lower cost than the liability side of the SPV.

B. Credit enhancements are typically only associated with mortgage-backed securities (MBSs) and are not used in other types of asset-backed securities (ABSs).

C. The most senior class of notes is often overcollateralized in order to reduce the risk of the asset backed security (ABS).

D. A margin step-up is sometimes used by an asset-backed securities (ABSs) where the coupon structure increases after a call date.

Practice Questions: Q3 Answer

Explanation: D is correct.

ABS issues may use a margin step-up that increases the coupon structure after a call date. Credit enhancements play an important role in the securitization process for both the asset-backed security (ABS) and mortgage-backed security (MBS) issues. The liability side of the SPV has a lower cost than the asset side of the SPV to create an excess spread prior to administration costs. The lowest class of notes are often overcollateralized where the principal value of the notes issued are valued less than the principal value of the original underlying assets.

Topic 6. Performance Measures for Securitized Structures

-

Overview:

-

MBS Origins: Created to provide cheaper residential home financing through pass-through securities; investors gained a new liquid asset class while lenders removed interest rate risk from balance sheets, with early issues backed by government-sponsored entities ("Ginnie Mae")

- ABS Growth Period: Auto loans and credit card ABS became popular during 2002–2007 low interest rate environment, offering diversification benefits and higher returns than corporate bonds

- Performance Dependency: Portfolio performance depends on individuals' ability to repay consumer debt and mortgages; performance measures serve as triggers to accelerate amortization with reserve accounts protecting against interest shortfalls

- CDO vs. ABS Structural Difference: CDO portfolios typically contain fewer than 200 loans, while ABS/MBS structures have much greater diversity with thousands of obligors

-

Topic 6. Performance Measures for Securitized Structures

-

Auto Loan Performance Tools:

- Favorable Investor Features: Auto loans are collateralized with highly liquid assets in default scenarios and have short 3-5 year horizons, resulting in stable prepayment risk and relatively low losses

- Loss Curve: Shows expected cumulative loss for the collateral pool's life; actual losses are compared to expected losses

- Prime loan originators typically have evenly distributed losses

- Subprime/non-prime originators have higher initial losses with steeper curves

- All loan types typically show declining losses in later years

- Absolute Prepayment Speed (APS): Indicates expected maturity of issued ABS by measuring actual period payments as a percentage of total collateral pool balance; used to determine the value of the ABS's implicit call option at any time

Topic 6. Performance Measures for Securitized Structures

-

Credit Card Performance Tools:

- Unique Characteristics: Credit card debt has no predetermined term for outstanding balances (differentiating it from other ABS), though most debt is repaid within six months; repayment speed controlled by scheduled amortization or revolving period under master trust framework

- Three Key Performance Ratios (serve as triggers for early amortization):

- Delinquency Ratio: Value of credit card receivables 90+ days past due ÷ total credit card receivables pool; provides early indication of overall collateral pool quality

- Default Ratio: Amount of written-off credit card receivables ÷ total credit card receivables pool

- Monthly Payment Rate (MPR): Monthly principal and interest payments ÷ total credit card receivables pool; rating agencies require minimum MPR as trigger for early amortization in all non-amortizing ABS

Module 3. Securitized Structure Ratios

Topic 1. Early Amortization Signals

Topic 2. MBS Performance Tools

Topic 3. Debt Service Coverage Ratio (DSCR)

Topic 4. Weighted Average Coupon (WAC)

Topic 5. Weighted Average Maturity (WAM)

Topic 6. Weighted Average Life (WAL)

Topic 1. Early Amortization Signals

-

Overview: The delinquency ratio, default ratio and monthly payment rate (MPR) serve as triggers to signal early amortization of the receivables pool for an ABS.

-

Example: Suppose an ABS has a total outstanding balance of credit card receivables of $57,800,000. $49,900,000 of the total receivables are current, $5,750,000 of the receivables are over 30 days past due, $1,270,000 of the receivables are over 60 days past due, and $880,000 are over 90 days past due. In addition, $1,100,000 of receivables were written off. Total monthly principal and interest payments per month are $1,560,000. Calculate the delinquency ratio, default ratio, and monthly payment rate for this ABS.

-

Answer:

-

Delinquency ratio: Delinquency ratio = (value of credit card receivables over 90 days past due)/(total credit card receivables pool) = $880,000/$57,800,000 = 1.522%.

-

Default ratio: Default ratio = (amount of written off credit card receivables)/(total credit card receivables pool) = $1,100,000/$57,800,000 = 1.903%.

-

Monthly payment rate (MPR): MPR = (percentage of monthly principal and interest payments)/(total credit card receivables pool) = $1,560,000/$57,800,000 = 2.699%.

-

Topic 2. MBS Performance Tools

-

Overview: These are specific metrics used to analyze the performance of mortgage-backed securities, which are heavily influenced by prepayment risk.

-

Prepayment Risk: The risk that a mortgage borrower will pay off their loan before the scheduled maturity date, typically when interest rates fall.

-

-

Importance: MBS investors rely on the steady stream of cash flows from the underlying mortgages. Prepayments disrupt these cash flows and can reduce the investor's return. MBS performance tools are essential for forecasting cash flows and managing investor expectations by providing a standardized way to measure prepayment speeds and other key characteristics of the collateral pool.

-

Major MBS Performance Tools: The major MBS performance tools include:

-

Debt Service Coverage Ratio (DSCR)

-

Weighted Average Coupon (WAC)

-

Weighted Average Maturity (WAM)

-

Weighted Average Life (WAL)

-

Topic 3. Debt Service Coverage Ratio (DSCR)

- Formula: DSCR = Net Operating Income (NOI) / Total Debt Payments

- Net Operating Income Definition: Income or cash flows remaining after all operating expenses have been paid

- Purpose: Performance tool measuring a borrower's ability to repay outstanding debt associated with commercial mortgages

- Interpretation: DSCR less than 1.0 indicates the underlying commercial mortgage asset pool generates insufficient cash flows to cover total debt payments

- Total Debt Service Components: All costs related to servicing debt, including:

- Interest payments

- Principal payments

- Other debt obligations

- Investor Confidence Relationship: As investor confidence in the securitization increases, required DSCR decreases, and vice versa

- Typical Ranges:

- Residential mortgages: 2.5 to 3.0

- Riskier receivables: Higher DSCRs needed when receivable values are heavily discounted in default scenarios

Topic 3. Debt Service Coverage Ratio (DSCR)

- Example: Suppose an MBS has net operating income from commercial mortgaged properties equal to $89,572,500. The total debt payments for notes issued against these mortgages is equal to $87,958,000. Calculate the debt service coverage ratio (DSCR).

- Answer: The DSCR is equal to 1.02, calculated as $89,572,500 / $87,958,000. A DSCR greater than one implies that there is sufficient cash flows generated from the underlying mortgage pool to meet debt payments. However, this is a very low DSCR for mortgages.

Topic 4. Weighted Average Coupon (WAC)

- Purpose: Measures the weighted coupon rate of the entire mortgage pool

- Calculation Formula: WAC is calculated by multiplying the mortgage rate for each loan pool by its loan balance, then dividing by the total outstanding loan balance for all pools

- Use in Analysis: WAC is compared to the net coupon payable to investors to assess the mortgage pool's ability to make payments over the outstanding life of the MBS

- Example: Suppose anMBS is composed of three different pools of mortgages: $6million of mortgages that yield 7.8%, $10 million of mortgages that yield 6.0%, and $4 million of mortgages that yield 5%. Calculate the weighted average coupon (WAC).

- Answer: The WAC is calculated as follows:

-

-

-

-

-

-

For example, if notes issued by the SPV are for 5.5%, then an excess spread will be generated if there are no defaults on the original mortgages.

\begin{aligned}

\text { WAC } &= \frac{{[0.078(6 \text { million })+0.06(10 \text { million })} +0.05(4 \text { million })}{(6 \text { million }+10 \text { million }+4 \text { million })} ] \\

&= (0.468 \text { million }+0.6 \text { million }+0.2 \text { million }) / 20 \text { million } \\

&= 1.268 \text { million } / 20 \text { million } \\

&= 0.0634 \text { or } 6.34 \%

\end{aligned}

Topic 5. Weighted Average Maturity (WAM)

- WAM Definition: The weighted average months remaining to maturity for the pool of mortgages in a mortgage-backed security (MBS)

- WAM Calculation: Multiply the weight of each MBS pool by its time until maturity, then sum all values

- Weight = (Total value of pool for one maturity) ÷ (Total value of all loans)

- Volatility Relationship: MBS volatility is directly related to the length of maturity of the underlying securities

- Two WAM Calculation Approaches:

- Stated Maturity Dates: Captures liquidity risk of all mortgage securities by using actual maturity dates

- Reset Dates: Captures the effect of prepayments on loan maturity

- Example: Suppose an MBS is composed of three different pools of mortgages: $6 million of mortgages that have a maturity of 180 days, $10 million of mortgages that have a maturity of 360 days, and $4 million of mortgages that have a maturity of 90 days. Calculate the weighted average maturity (WAM).

- Answer: The WAM is calculated as follows:

-

\begin{aligned}

\text { WAC } &= \frac{{[180(6 \text { million })+360(10 \text { million })} +90(4 \text { million })}{(6 \text { million }+10 \text { million }+4 \text { million })} ] \\

&= (1,080 \text { million }+3,600 \text { million }+360 \text { million }) / 20 \text { million } \\

&= 5040 \text { million } / 20 \text { million } \\

&= 252 \text { days }

\end{aligned}

Practice Questions: Q1

Q1. Assume an MBS is composed of the following four different pools of mortgages:

- $2 million of mortgages that have a maturity of 90 days.

- $3 million of mortgages that have a maturity of 180 days.

- $5 million of mortgages that have a maturity of 270 days.

- $10 million of mortgages that have a maturity of 360 days.

What is the weighted average maturity (WAM) of these mortgage pools?

A. 167 days.

B. 225 days.

C. 252 days.

D. 284 days.

Practice Questions: Q1 Answer

Explanation: D is correct.

The WAM is calculated as follows:

WAC= [90(2 million)+180(3 million)+270(5 million)+360(10 million)/(2 million+3 million+5 million+10 million)

= (180 million +540 million +1,350 million+3,600 million)/20 million

= 5,670 million/20 million

= 284 days

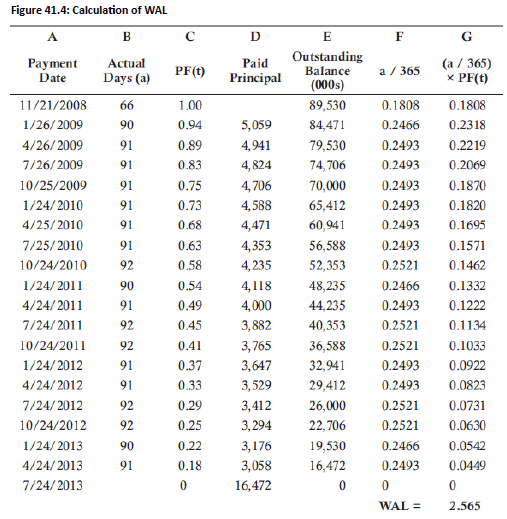

Topic 6. Weighted Average Life (WAL)

-

Definition: The weighted average of the time until each dollar of principal is repaid, taking into account expected prepayments.

-

Relationship to WAM: Unlike WAM, which only considers the stated maturity of the loans, the WAL is a more accurate measure because it accounts for the impact of both scheduled amortization and prepayments.

-

Influencing Factors: The WAL is highly sensitive to the level of prepayments. If prepayment speeds increase, the WAL will decrease because the principal is being returned to investors more quickly. Conversely, if prepayments slow down, the WAL will lengthen.

-

Importance: This metric is crucial for bond investors as it helps them estimate the true expected term of the investment and understand the impact of prepayment risk. A shorter WAL can be a negative for investors who desire a longer-term, predictable income stream.

-

WAL Formula:

-

where

-

'a' represents actual days until next payment

-

PF(t) is the pool factor (outstanding notional value adjusted by repayment weighting).

-

-

\mathrm{WAL}=\sum(\mathrm{a} / 365) \times \mathrm{PF}(\mathrm{t})

Topic 6. Weighted Average Life (WAL)

-

Calculation Steps (per Fig 41.4):

- Start with initial outstanding balance for entire pool (example: $89,530,000)

- Column B: Actual days until next payment

- Column F: Time to maturity = Column B ÷ 365

- Column G: Individual note's weighted life = Column F × Column C (pool factor)

- Final WAL = Sum of all values in Column G

Module 4. Prepayment Forecasting

Topic 1. Prepayment Forecasting

Topic 2. Performance Tools for ABS and MBS

Topic 1. Prepayment Forecasting

- Common Methodologies: Common methodologies used to estimate prepayments for MBS or ABS collateralized by mortgages or student loans include:

- Constant Prepayment Rate (CPR) method

- Public Securities Association (PSA) method

- Prepayment Impact: Prepayment assumptions are required to estimate MBS cash flows

- Prepayments reduce MBS yield assuming principal payments remain unchanged

- CPR Calculation:

- Formula:

- SMM = Single Monthly Mortality (single-month proportional prepayment)

- Influencing factors: market environment, underlying mortgage pool characteristics, outstanding pool balance

- Example: Suppose an ABS has an SMM of 1.5%. This implies that the approximate prepayment for the month is equal to 1.5% of the remaining mortgage balance for the month less the scheduled principal repayment. Calculate the CPR for this MBS.

- Answer: The CPR for this MBS equals 16.59%, calculated as:

-

C P R=1-(1-S M M)^{12}

C P R=1-(1-S M M)^{12} = 1 - (1-0.015)^{12}= 0.1659

Topic 1. Prepayment Forecasting

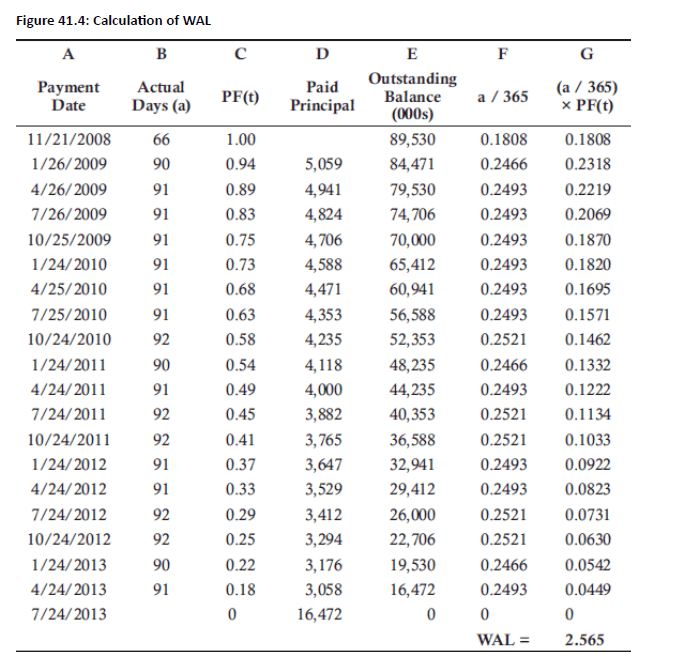

- PSA Method Characteristics:

- Assumes prepayments increase as pool approaches maturity

- 100% PSA benchmark: CPR starts at 0 and increases 0.2% each month for first 30 months, then remains constant at 6% until maturity

- Fig 41.5 shows CPR trajectory as ABS approaches maturity

- PSA Scenario Variations (Fig 41.5):

- 50% PSA (bottom line): Prepayments increase 0.1% monthly for first 30 months, then constant 3%

- 100% PSA (middle line): Prepayments increase 0.2% monthly for first 30 months, then constant 6%

- 150% PSA (top line): Prepayments increase 0.3% monthly for first 30 months, then constant 9%

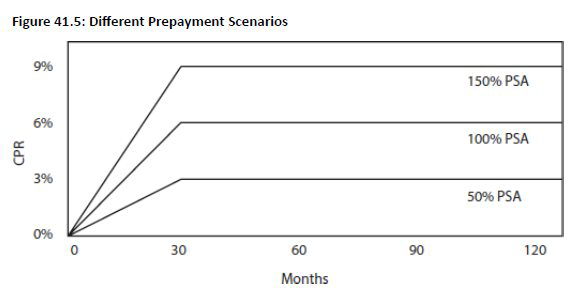

Topic 2. Performance Tools for ABS and MBS

-

Fig 41.6 summarizes performance tools based on the type of ABS or MBS.

Practice Questions: Q1

Q1. Which of the following measures are most likely to be used by a securitized product backed by student loans?

A. Single monthly mortality (SMM), constant prepayment rate (CPR), and Public Securities Association (PSA).

B. Loss curves and absolute prepayment speed (APS).

C. Weighted average life (WAL), weighted average maturity (WAM), and weighted average coupon (WAC).

D. Debt service coverage ratio (DSCR) and monthly payment rate (MPR).

Practice Questions: Q1 Answer

Explanation: A is correct.

The constant prepayment rate (CPR) and the Public Securities Association (PSA) method are common methodologies used to estimate prepayments for student loans and mortgages.

CR 23. An Introduction to Securitization

By Prateek Yadav