Book 2. Credit Risk

FRM Part 2

CR 7. Credit Scoring and Retail Credit Risk Management

Presented by: Sudhanshu

Module 1. Credit Risk

Module 2. Creditwothiness

Module 1. Credit Risk

Topic 1. Retail Banking Risks

Topic 2. Retail Vs. Corporate Credit Risk

Topic 3. Downside of Retail Credit Risk

Topic 4. Lending Standards

Topic 4. Credit Risk Scoring Models

Topic 1. Retail Banking Risks

-

Credit Risk in Retail Banking: It is the potential for financial loss when a customer fails to repay a loan. Credit risk is the primary risk in retail banking.

-

Examples: Credit risk is associated with products like home mortgages, home equity lines of credit (HELOCs), installment loans (auto loans, credit cards, etc) and small business loans (SBLs).

-

Management: Banks manage credit risk by assessing a borrower's creditworthiness, setting appropriate credit limits, and using strategies like diversification and collateralization.

-

-

Risky lending practices: In the five years before the 2007 subprime crisis, banks offered mortgages to borrowers who could not afford them and were exposed to excessive risk.

-

High leverage and weak credit: Lending featured very high loan-to-value (LTV) ratios and extended mortgages to borrowers with weaker credit profiles.

-

Crisis outcome: When housing prices collapsed, mortgage balances frequently exceeded property values, amplifying losses and defaults.

-

Other Risks in Retail Banking

-

Operational Risk: The risk of losses due to failed internal processes, systems, people, or external events. This includes risks like fraud, system failures, and human error.

-

Business Risk: Strategic risk associated with new products or trends and volume risks associated with measures like mortgage volume when rates change.

-

Reputation Risk: This is the potential for damage to the bank's reputation, which can be present throughout the organization.

-

Interest Rate Risk: The potential for a bank's earnings to be affected by changes in interest rates. This arises from mismatches in the timing of rate changes and cash flows.

-

Asset Valuation Risk: A form of market risk associated with the valuation of assets, liabilities, and collateral classes. An example includes prepayment risk associated with mortgages in decreasing rate environments. Valuation risk also exists in situations when car dealers assume a residual value for a vehicle at the end of the life of a lease.

-

Topic 1. Retail Banking Risks

Practice Questions: Q1

Q1. Which of the following statements is most accurate regarding risks incurred by retail lenders?

A. Reputation risk is more of a concern for the borrower rather than the lender.

B. Business risk relates to the day-to-day operational risks of the business.

C. Credit risk relates to the potential for a lender to default on their obligation.

D. Refinancing a mortgage when rates decrease is an example of asset valuation risk.

Practice Questions: Q1 Answer

Explanation: D is correct.

Refinancing a mortgage is considered a prepayment risk to the lender, which is a component of asset valuation risk. When rates decrease, borrowers are more

likely to refinance their existing (higher rate) mortgage into a lower rate

obligation. The lender then earns less in interest on the debt obligation than they would have previously.

Reputation risk is primarily a concern for the lender.

Business risk relates to strategic risks tied to new products and volume, while

credit risk is the risk that the borrower (rather than the lender) will default.

Topic 2. Retail Vs. Corporate Credit Risk

-

Retail Credit Risk

-

Consists of small individual exposures within large, diversified portfolios

-

Default of a single customer does not materially threaten the lending institution

-

Highly diversified, allowing expected defaults to be treated as a normal cost of doing business

-

Losses are priced into products through interest rates and fees

-

Early warning signals from customer behavior often allow preemptive actions, such as:

-

Targeting lower-risk customers

-

Increasing rates for higher-risk customers

-

-

-

Corporate Credit Risk

-

Characterized by large, concentrated exposures to individual firms

-

Defaults can have a significant impact on the bank, the industry, and even the broader economy

-

Losses may exceed expected levels, posing a potentially crippling risk to the bank

-

Limited early warning signals, as financial distress may become visible too late for corrective action

-

Topic 3. Downside of Retail Credit Risk

-

"Dark Side" of Retail Credit Risk: While individual defaults are small, a systematic event can influence the behavior of a large number of retail credits at once. Primary causes:

- Limited loss history: Insufficient historical loss data for newer products makes risk estimation unreliable.

-

Systemic risk shifts: Broad-based economic shocks can cause retail credit products to behave differently than expected.

-

Social and legal changes: Evolving social or legal frameworks may unintentionally increase incentives to default.

-

Operational flaws: Semi-automated credit processes can contain operational flaws that lead to lending to higher-risk individuals.

-

Consumer Financial Protection Act (CFPA) requiremts: CFPA requires credit originators to evaluate qualified mortgages and ability to repay.

-

Repayment capacity assumption: Borrowers with a qualified mortgage are presumed to have the ability to repay, subject to limits on income allocated to debt service (e.g., debt-to-income ratio below 45%).

-

Product restrictions: Qualified mortgages cannot include excessive upfront fees or points, balloon or interest-only features, terms longer than 30 years, or negative amortization.

-

Topic 4. Lending Standards

-

Lending Standards: the following underwriting standards must be considered while evaluating a customer's "ability to replay":

-

Credit history

-

Current income and assets

-

Current employment status

-

Mortgage monthly payments

-

Monthly payments onmortgage-related items such as insurance and property taxes

-

Monthly payments on other associated property loans

-

Additional debt obligations of the borrower

-

The monthly debt-to-income ratio resulting from the mortgage

-

-

Lower capital needs for retail credit: As retail credit is relatively predictable and safer, banks are required to hold less risk capital compared with corporate loan exposures.

-

Regulatory reporting requirements: Banks must report segment-level credit risk metrics to regulators, including PD, EAD and LGD.

Practice Questions: Q2

Q2. The dark side of retail credit risk is perpetuated by all of the following factors except:

A. capital set aside to protect a bank in the event of default.

B. process flaws resulting in high risk applicants receiving credit.

C. new products which do not have suffcient historical loss data.

D. a social acceptance of bankruptcy and borrowers “walking away” from their obligations.

Practice Questions: Q2 Answer

Explanation: A is correct.

Capital must be set aside to protect banks in the event of default, but this is a response to the dark side of retail credit risk rather than a perpetuating factor. A process flaw which grants credit to high risk individuals, a new product which doesn’t have historical loss data, and the social “acceptance” of failing to meet debt payments are all considered perpetuating factors of retail credit risk.

-

Purpose: Credit risk scoring models convert applicant information into a numerical score to assess risk, where higher scores indicate a higher probability of repayment and lower overall credit risk, enabling automated evaluation of large data volumes.

-

Working: Credit scorecards collect data from applications and credit bureau reports, assign attributes to borrower characteristics (e.g., years with current employer), and weight each attribute based on historical performance and repayment probabilities.

-

Types of consumer credit scoring models:

-

Credit bureau scores: Standardized scores (e.g., FICO ranging from 300 to 850) that are fast, low-cost, and widely used, with higher scores implying lower lender risk and lower borrower interest rates.

-

Pooled models: Developed by third parties, more expensive than bureau scores but flexible and adaptable to specific industries.

-

Custom models: Built internally by lenders using proprietary application data, allowing tailored evaluation for the lender’s specific products.

-

Topic 5. Credit Risk Scoring Models

-

Every individual with a credit history will have credit files with following details:

-

Personal (identifying) information which doesn’t factor into scoringmodels.

-

Records of credit inquiries when a file is accessed. Requests for new credit will be visible to credit grantors.

-

Data on collections, reported by entities that provide credit or agencies that collect outstanding debts.

-

Legal (public) records on bankruptcies, tax liens, and judgments.

-

Account and trade line information gathered from receivables information sent to credit bureaus by grantors.

-

Topic 5. Credit Risk Scoring Models

Practice Questions: Q3

Q3. Which of the following statements is correct regarding credit risk scoring models?

A. A pooled model will result in scores ranging from 300 to 850.

B. A custom model is cheaper to implement than credit bureau scores.

C. Multiple requests for new credit will reduce an applicant’s credit score.

D. An example of a characteristic in a scoring model is the applicant’s current gross salary of $50,000.

Practice Questions: Q3 Answer

Explanation: C is correct.

An individual’s credit file will show a history of credit requests, with multiple requests causing an applicant’s credit score to decline. A credit bureau score model (rather than pooled model) will result in scores ranging from 300 to 850. A custom model is more expensive to implement than credit bureau scores. “Gross salary with current employer” is an example of a characteristic, with the actual

salary number itself representing an attribute.

Module 2. Creditworthiness

Topic 1. Mortgage Credit Assessment

Topic 2. Cutoff Scores

Topic 3. Scorecard Perfomance

Topic 4. Creditworthiness Vs. Profitability

Topic 5. Risk-Based Pricing

Topic 1. Mortgage Credit Assessment

-

In assessing an application for mortgage credit, the key variables include:

-

FICO Score: A numerical score serving as a measure of default risk tied to the borrower’s credit history.

-

Loan-to-value (LTV) Ratio: The amount of the mortgage divided by the associated property’s total appraised value.

-

Debt-to-income (DTI) Ratio: The ratio of monthly debt payments (mortgage, auto, etc.) to the monthly gross income of the borrower.

-

Payment (Pmt) Type: The type of mortgage (adjustable rate, fixed, etc.).

-

Documentation (doc) types:

-

Full doc: A loan which requires evidence of assets and income

-

Stated income: Employment is verified but borrower income is not

-

No ratio: Similar to stated income, employment is documented but income is not. The debt-to-income ratio is not calculated

-

No income/no asset: Income and assets are provided on the loan application but are not lender verified (other than the source of income)

-

No doc: No documentation of income or assets is provided

-

-

Practice Questions: Q1

Q1. In assessing the key variables associated with a potential mortgage loan, a bank will charge a higher interest rate if the borrower has a relatively:

A. high FICO score.

B. high loan-to-value ratio.

C. low debt-to-assets ratio.

D. low debt-to-income ratio.

Practice Questions: Q1 Answer

Explanation: B is correct.

The loan-to-value ratio represents the amount of the mortgage versus the appraised value of the property. The higher this ratio is for a property and an associated borrower, the more risk there is to the lender. In order to protect their position, a lender will charge a higher interest rate. Each of the other scenarios will result in a lower interest rate.

Topic 2. Cutoff Scores

-

Definition: Cutoff scores represent thresholds where lenders determine whether they will or will not lend money (and the terms of the loan) to a particular borrower.

-

Cutoff score trade-off: A cutoff set too low increases default risk, while a cutoff set too high can exclude low-risk borrowers and reduce profitable lending opportunities.

-

Cutoff score calibration: Once a cutoff score is set, banks use historical data to estimate profitability and loss rates for a product line and may adjust the cutoff over longer horizons to balance risk and profitability across economic cycles.

-

Basel portfolio segmentation: Under the Basel Accord, banks must segment portfolios into risk-homogeneous subgroups using score bands and estimate PD and LGD for each group.

-

Implied PD calculation: The PD can be inferred from historical loss rates and LGD; for example, a 3% loss rate with a 75% LGD implies a PD of 4% (3% ÷ 75%).

Topic 3. Scorecard Perfomance

-

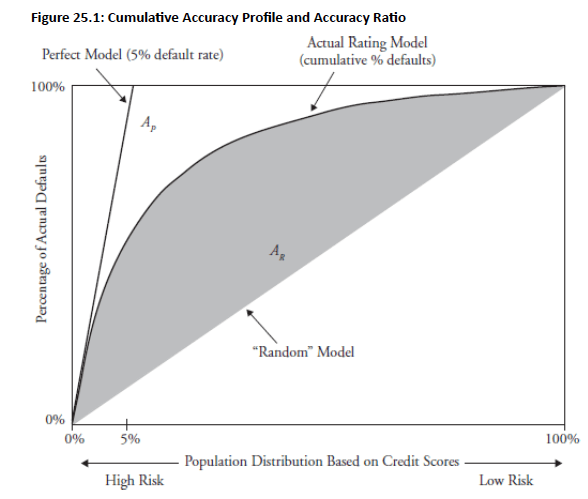

Evaluation: The performance of a scorecard is assessed using CAP and AR.

- Cumulative Accuracy Profile (CAP): The CAP shows the population distribution based on credit scores vs. the percentage of actual defaults.

- Lines plotted on the graph include the perfect model line, random model line and observed cumulative default percentage line.

-

Area under the curves: APA_PAP represents the area between the perfect model and the random model, while ARA_RAR represents the area between the observed cumulative default percentage curve and the random model.

-

Accuracy Ratio (AR): Defined as AR/APA_R / A_PAR/AP, where values closer to 1 indicate a more accurate credit risk model.

-

Example: In a perfect model, if the bank predicts 5% of its accounts will default over a specific period, 100% of those defaults will come from the riskiest 5% of the population.

-

A random model will assume 5% of the defaults will come from the riskiest 5%, 20%will come from the riskiest 20%, etc.

-

The observed cumulative default line represents the actual defaults observed by the bank.

Topic 4. Creditworthiness Vs. Profitability

-

Creditwothiness vs profitability trade-off: Lenders must assess not only credit risk but also customer and product profitability when extending credit.

-

High vs low credit scores: Customers with very high FICO scores may generate little interest income if they pay balances in full, while low FICO score customers offer higher potential returns but carry greater default risk.

-

Profitability scoring: Beyond credit scoring, lenders use product- and customer-level profitability scores to evaluate expected returns from specific products and customers.

-

Expanded scorecard use: Beyond credit bureau (FICO) scores, lenders use additional scorecards to assess both customer creditworthiness and profitability, including the following types.

-

Customer relationship cycle: Encompasses marketing products and services, screening customer applications, managing ongoing accounts, and cross-selling additional products.

-

Marketing and screening: Marketing focuses on acquiring new customers or tailoring products for existing ones, while applicant screening uses scorecards to approve or reject applications and set appropriate pricing.

-

Account management: Involves product pricing, credit line approvals, modifications, renewals, and collection of principal and interest.

-

Cross-selling: Targets existing customers with additional lender products to meet evolving financial needs.

Topic 4. Creditworthiness Vs. Profitability

-

Expanded scorecard use: Beyond credit bureau (FICO) scores, lenders use additional scorecards to assess both customer creditworthiness and profitability, including the following types.

-

Revenue Scores: Used to evaluate existing customers on potential profitability

-

Application Scores: Used to support the decision to extend credit to a new applicant

-

Response Scores: Assign a probability to whether a customer is likely to respond to an offer

-

Insurance Scores: Assign a probability to potential claims by the insured

-

Behavior Scores: Assess existing customer credit usage and historical delinquencies

-

Tax Authority Scores: Predict where potential audits may be needed for revenue collection

-

Attrition Scores: Assign a probability to the reduction or elimination of outstanding debt by existing customers

-

-

Motivation: Charging a single price to all customers can lead to adverse selection, attracting higher-risk borrowers and discouraging lower-risk ones.

-

Risk-based pricing (RBP): RBP sets different prices for customers based on their individual risk profiles rather than a uniform rate.

-

Current adoption: Although still evolving in retail banking, RBP is more commonly applied in credit cards, home mortgages, and auto loans.

-

Key external and internal factors which account for risk and play into the interest rates and prices charged by lenders include:

-

The probability of take-up (i.e., acceptance by the customer of the offered product)

- PD, LGD and EAD

- The cost of equity capital to the lender

- Capital allocated to the transaction

- Operating expenses of the lender

-

-

Tiered risk-based pricing: Prices are set using score bands that classify borrowers from high to low risk tier, with each risk tier linked to metrics such as profit/loss, revenue, market share, and risk-adjusted return.

-

Strategic trade-off evaluation: Effective use of risk-based pricing helps management balance profitability, market share, and risk to support long-term shareholder value.

Topic 5. Risk-Based Pricing

Practice Questions: Q2

Q2. By implementing risk-based pricing on its mortgage products, a bank will likely charge a:

A. higher interest rate to a customer with a higher FICO score.

B. lower interest rate to a customer with a lower credit bureau score.

C. higher interest rate to a customer with a higher probability of default.

D. lower interest rate to a customer positioned on a lower relative score band.

Practice Questions: Q2 Answer

Explanation: C is correct.

The more likely it is that a customer will default, the higher the interest rate the bank will charge. A customer with a higher (lower) FICO/credit bureau score will be offered a lower (higher) interest rate. A customer positioned on a lower relative score band will be offered a higher interest rate.

CR 7. Credit Scoring and Retail Credit Risk Management

By Prateek Yadav