Book 1. Foundations of Risk Management

FRM Part 1

FRM 2. How Do Firms Manage Financial Risk?

Presented by: Sudhanshu

Module 1. Corporate Risk Management

Module 2. Risk Management Methods and Instruments

Module 1. Corporate Risk Management

Topic 1. Strategies for Risk Management

Topic 2. Risk Appetite Relative to Risk Decision-Making

Topic 3. Role of the Board of Directors

Topic 4. Risk Mapping

Topic 5. Hedging Risk Exposures

Topic 6. Hedging Advantages (In Practice)

Topic 7. Hedging Disadvantages (In Theory)

Topic 8. Hedging Disadvantages (In Practice)

Topic 9. Challenges Involved with Hedging Strategies

Topic 1. Strategies for Risk Management

-

Risk Management Strategies:

-

Accept Risk: When risk is immaterial, manageable, or desirable (e.g., gold miner wanting gold exposure).

-

Avoid Risk: Exit or avoid risky business units or markets.

-

Mitigate Risk: Take steps to reduce the likelihood or severity (e.g., automation to reduce labor risk).

-

Transfer Risk: Use insurance or derivatives; introduces counterparty risk.

-

-

Best Practice: Cost-benefit analysis of each option before decision.

Practice Questions: Q1

Q1. Bank Y has decided to use currency futures and forward to offset its entire estimated foreign sales exposure. Which high-level risk mitigation strategy does this description represent?

A. Retain risk.

B. Avoid risk.

C. Mitigate risk.

D. Transfer risk.

Practice Questions: Q1 Answer

Explanation: D is correct.

Since Bank Y has decided to take a formal action, they have not chosen to either retain or avoid the risk. Mitigation would involve taking some internal action without using a financial asset. In using futures and forward contracts, Bank Y has chosen to transfer their foreign currency risk to a third party.

Topic 2. Risk Appetite Relative to Risk Decision-Making

-

Risk Appetite = Risk willingness + Risk ability.

-

Willingness: Based on business goals.

-

Ability: Constrained by internal controls or regulations (e.g., leverage caps).

-

-

Process:

-

Identify appetite

-

Map risks

-

Operationalize

-

Implement

-

Monitor & adjust

-

-

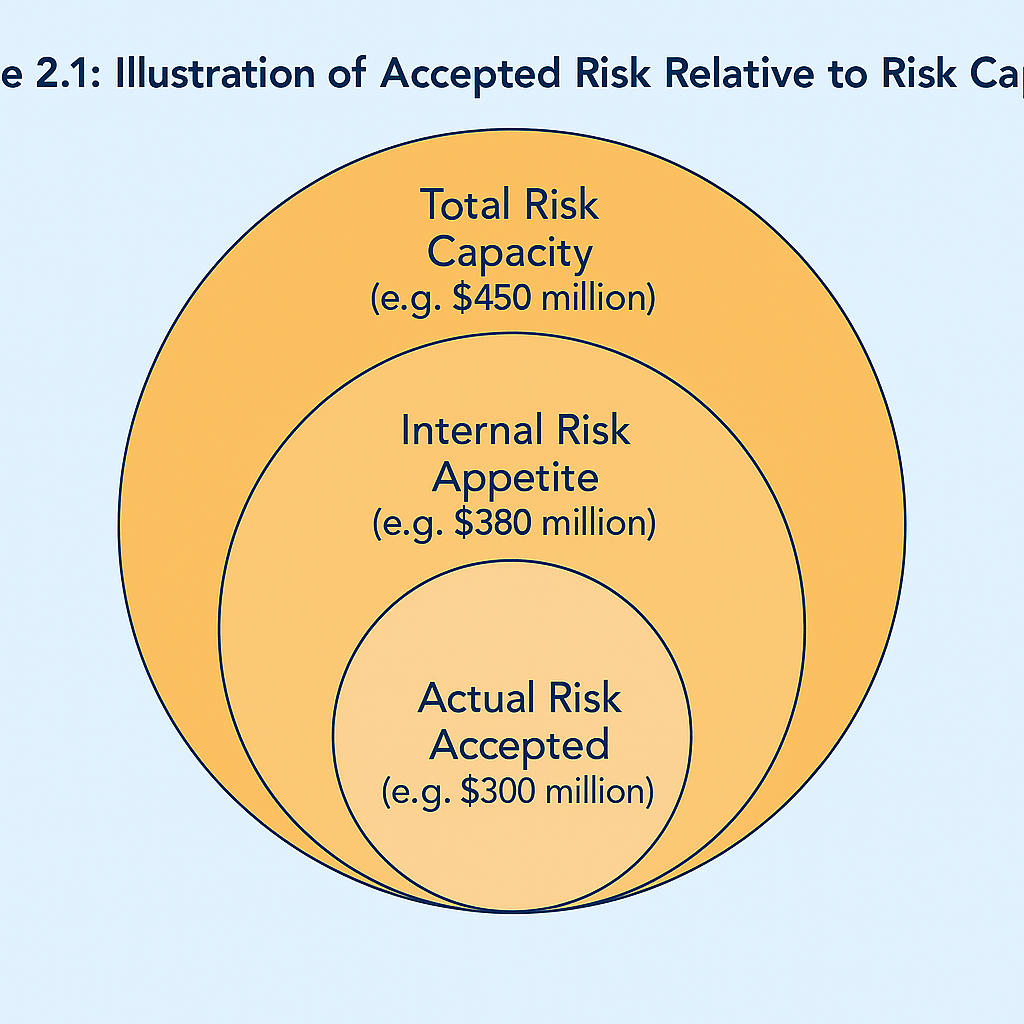

Set below capacity to create margin for model error.

Topic 2. Risk Appetite Relative to Risk Decision-Making

Accepted Risk Relative To Risk Capacity

Topic 3. Role of the Board of Directors

-

Define and communicate risk appetite qualitatively and quantitatively.

-

Resolve debtholder vs. shareholder conflicts:

-

Debtholders → minimize risk.

-

Shareholders → accept calculated risk.

-

-

Considerations:

-

Risk correlations, reputational impacts, tolerance bands.

-

Unity across risk types (credit, market, operational).

-

Metrics like VaR, stress testing, notional limits.

-

Practice Questions: Q2

Q2. The involvement of the board of directors is important within the context of a firm’s decision to hedge specific risk factors. Which of the following statements regarding the setting of risk appetite is correct?

I. Risk appetite may be conveyed strictly in a qualitative manner.

II. Debtholders and shareholders are both likely to desire minimizing the firm’s risk appetite.

A. I only.

B. II only.

C. Both I and II.

D. Neither I nor II.

Practice Questions: Q2 Answer

Explanation: A is correct.

Risk appetite may be conveyed in a qualitative and/or quantitative manner, therefore, qualitative alone may be acceptable. Debtholders would likely be more concerned about minimizing all risks because their upside potential is generally limited to the rate of interest charged. In contrast, shareholders may be willing for the firm to accept a large but unlikely risk to increase equity prices.

Topic 4. Risk Mapping

-

Systematic inventory of all known risks:

-

Market, credit, liquidity, legal, strategic, operational, reputation.

-

-

Evaluate: Magnitude, timing, location of exposure.

-

Factor in:

-

Netting benefits (e.g., offsetting currency inflows/outflows).

-

Forecasted vs. actual exposure.

-

Geographic and currency complexity.

-

Topic 5. Hedging Risk Exposures

-

Hedging Goal: Improve financial stability, reduce distress risk.

-

Not all risks should be hedged:

-

Some risks are part of the firm’s value proposition.

-

Some are too expensive to hedge.

-

Topic 6. Hedging Advantages (In Practice)

-

Reduces earnings volatility → lower cost of capital.

-

Enhances planning and cash flow predictability.

-

Increases borrowing capacity (debt covenants).

-

Can reduce tax burden via smoother earnings.

-

Signals sound risk management to stakeholders.

-

May result in profitable derivative positions.

Topic 7. Hedging Disadvantages (In Theory)

-

Modigliani-Miller Theorem: In perfect markets, hedging has no firm value impact.

-

CAPM (Sharpe): Only systematic risk matters.

-

Hedging may shift earnings between periods (zero-sum assumption).

-

Doesn’t consider real-world frictions like bankruptcy cost.

Topic 8. Hedging Disadvantages (In Practice)

-

Derivative complexity may shift risk unexpectedly.

-

High compliance and audit costs.

-

Management distraction from core business.

-

Risk of revealing strategic information.

-

Ill-suited hedge → unexpected losses (e.g., MGRM case).

-

Human capital constraints (expertise gap).

Practice Questions: Q3

Q3. Melody Li is a junior risk analyst who recently prepared a report on the advantages and disadvantages of hedging risk exposures. An excerpt from her report contains four statements. Which of Li’s statements is correct?

A. “Purchasing an insurance policy is an example of hedging.”

B. “In practice, hedging with derivatives may not be a zero-sum game.”

C. “The existence of significant costs of financial distress and bankruptcy is a natural consideration by perfect capital markets.”

D. “Hedging with derivatives is advantageous in the sense that there is often the ability to avoid numerous disclosure requirements compared with other financial instruments.”

Practice Questions: Q3 Answer

Explanation: B is correct.

The complexity of derivatives pricing means that the pricing may not always be as accurate as possible, so it will not always reflect all of the relevant risk factors. As a result, in practice, hedging with derivatives may not be a zero-sum game of transferring risk between periods or between participants.

Hedging involves the use of financial derivatives, and insuring involves the use of insurance policies; an insurance policy is not considered a financial instrument in the same sense as a derivatives instrument.

The existence of significant costs of financial distress and bankruptcy is contrary to the assumption of perfect capital markets. Hedging with derivatives will require disclosure, including some operational information that the firm may otherwise prefer to keep private.

Topic 9. Challenges Involved With Hedging Strategies

-

Misidentified or misestimated risks.

-

Changing market conditions alter risk profile.

-

Communication failures (internal/external).

-

Dynamic hedging needs real-time monitoring.

-

Cultural barriers to enterprise-wide risk awareness.

Module 2. Risk Management Methods and Instruments

Topic 1. Hedging Operational and Financial Risks

Topic 2. Pricing Risk

Topic 3. Foreign Currency Risk

Topic 4. Interest Rate Risk

Topic 5. Static and Dynamic Hedging Strategies

Topic 6. Additional Hedging Considerations

Topic 7. The Impact of Risk Management Tools

Topic 8. Derivatives Contracts As Risk Management Tools

Topic 9. Advantages and Disadvantages of Derivatives

Topic 10. Impact of Risk Management Tools

Topic 11. Risk Limits

Topic 1. Hedging Operational and Financial Risks

-

Operational Risks: Revenue & expense volatility (e.g., cost of raw materials).

-

Financial Risks: Balance sheet exposures (assets, liabilities).

Topic 2. Pricing Risk

-

Input cost volatility: E.g., cork for wine production.

-

Use forward/futures contracts to lock in prices.

Topic 3. Foreign Currency Risk

-

Arises from foreign revenues and investments.

-

Tools:

-

Currency put options (limit downside).

-

Forward contracts (lock in FX rate).

-

Natural hedging via liabilities (e.g., FX debt offsets FX assets).

-

Topic 4. Interest Rate Risk

-

Arises from floating-rate borrowing or fixed-rate investing.

-

Tools:

-

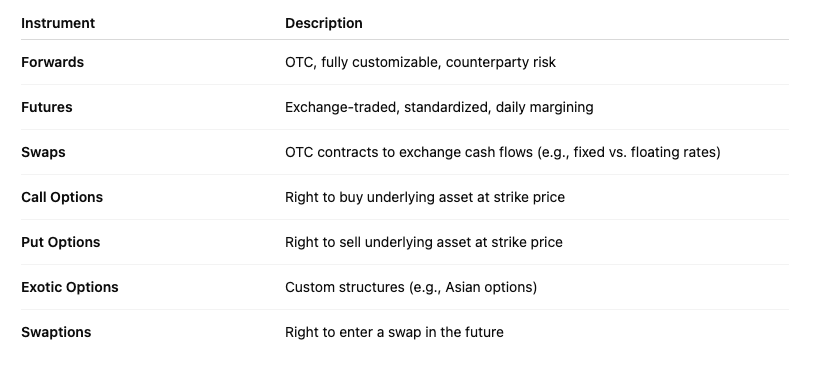

Interest rate swaps, swaptions.

-

-

Hedge both asset and liability sides.

Practice Questions: Q4

Q4. Jasmine Cellars is a U.S. wine producer that purchases a significant amount of cork (from Asia) for its wine bottles. Eighty percent of their sales are to customers in North America. Based on these two broad transactions, which of the following risks does Cellars most likely face?

A. Financial position risk and operational risk.

B. Operational risk and pricing risk.

C. Pricing risk only.

D. Financial position risk, operational risk, and pricing risk.

Practice Questions: Q4 Answer

Explanation: B is correct.

Operational risk could cover activities pertaining to Jasmine Cellars’s input products (i.e., cork) and products exported to foreign countries (i.e., bottles of wine). In addition, there would be pricing risk for both the inputs and outputs. For example, the cost of the cork may have a significant impact on Cellars’s ability to conduct business in a competitive manner.

Also consider that Cellars has sales to customers in foreign countries (with payment in the foreign currency) where there is the risk of the devaluation of the foreign currency in the future. Financial position risk refers to the balance sheet of a firm. Neither the purchases nor the sales impact Cellars’s balance sheet.

Topic 5. Static and Dynamic Hedging Strategies

-

Static Hedging:

-

One-time setup.

-

Lower cost, less responsive.

-

-

Dynamic Hedging:

-

Adjust hedge as underlying changes.

-

Higher cost, but better tracking of risk.

-

Topic 6. Additional Hedging Considerations

-

Align hedge horizon with performance evaluation.

-

Consider accounting and tax implications.

-

Derivatives mismatches may create reported gains/losses.

-

Tax law complexity varies by jurisdiction.

Topic 7. The Impact of Risk Management Tools

-

Determine if RM is a cost center or profit center.

-

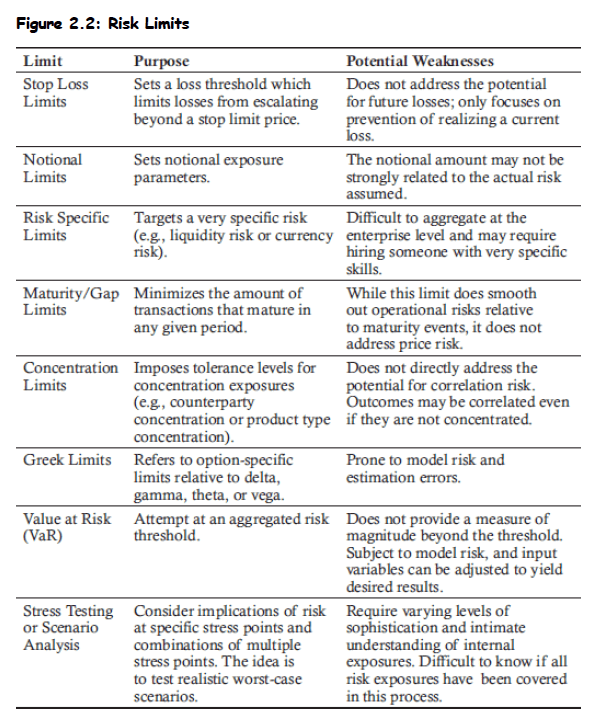

Establish risk limits:

-

Liquidity limits

-

Counterparty limits

-

Market exposure caps

-

-

Rightsize the program:

-

Strategic or tactical use?

-

Centralized vs. business-level hedging costs?

-

Topic 8. Derivatives Contracts As Risk Management Tools

Practice Questions: Q5

Q5. You have just been hired as the vice president of risk management at Johnson Controllers. Your new employer is domiciled in the United States, but 35% of their sales are in Brazil. The highest priority task is to hedge the firm’s exposure to the Brazilian real (their currency).

You want to use a product that minimizes basis risk and can accommodate the firm’s dynamic and sometimes unique cash flow patterns. Which tool would you least likely recommend?

A. Futures contracts.

B. Forward contracts.

C. Swap contracts.

D. Call option contracts.

Practice Questions: Q5 Answer

Explanation: A is correct.

A futures contract does not provide customization. The firm wants to reduce basis risk and provide for a complex and dynamic cash flow pattern.

Topic 9. Advantages and Disadvantages of Derivatives

-

Advantages:

-

Enable tailored hedging.

-

Add value via price stability.

-

Exchange-traded = high liquidity and low credit risk.

-

OTC = customization.

-

-

Disadvantages:

-

OTC derivatives carry counterparty risk.

-

Basis risk if contract doesn’t perfectly match exposure.

-

Complexity increases operational and disclosure burden.

-

Example: Airlines hedging jet fuel with crude oil = basis risk.

-

Topic 10. Impact of Risk Management Tools

-

Strategic Alignment: Firms must decide whether hedging is a one-time fix or part of a broader enterprise-wide risk management program—a process known as rightsizing.

-

Dynamic Markets: Financial markets evolve rapidly. A long-term, integrated strategy requires:

-

Investment in complex infrastructure

-

Hiring of experienced traders and risk professionals

-

-

Risk Limit Framework: Risk mapping helps identify exposures, after which appropriate risk limits should be set and monitored.

Topic 11. Risk Limits

Copy of FRM 2. How Do Firms Manage Financial Risk

By Prateek Yadav