Book 4. Liquidity and Treasury Risk

FRM Part 2

LTR 17. Risk Management for Changing Interest Rates: Asset-Liability Management and Duration Techniques

Presented by: Sudhanshu

Module 1. Interest-Sensitive Gap Management

Module 2. Duration Gap Management

Module 1. Interest-Sensitive Gap Management

Topic 1. Asset-Liability Management Strategies

Topic 2. Managing Interest Rate Risk

Topic 3. Net Interest Margin and Gap Management

Topic 1. Asset-Liability Management Strategies

-

Bank Management Focus

- Primary concerns include net interest income (NII), equity (assets minus liabilities), and risk exposure.

- Net income equals interest earned on assets minus interest costs on liabilities (excludes credit risk considerations).

-

Asset-Liability Management (ALM)

- Integrated approach treating both sides of the balance sheet as a unified whole for profitability and risk management.

- Overseen by the Asset-Liability Committee (ALCO), composed of senior management from various departments.

-

Funds management, as part of the ALM process, refers to:

-

Decisions regarding the volume, mix, and interest rates of both assets and liabilities.

-

Policies regarding assets and liabilities, which must be consistent with each other.

-

Managing the revenues and costs generated from both assets and liabilities to both increase interest income and control costs.

-

Practice Questions: Q1

Q1. An integrated approach to managing balance sheet interest rate risk is called:

A. asset management.

B. liability management.

C. asset-liability management (ALM).

D. asset-liability and owners’ equity management.

Practice Questions: Q1 Answer

Explanation: C is correct.

Financial institutions take an integrated approach to balance sheet management, called ALM. The two sides of the balance sheet are seen as an integrated whole. Banks do engage in capital planning and management, but it is not called asset- liability and owners’ equity management.

Topic 2. Managing Interest Rate Risk

-

Interest Rate Risk: As market interest rates change, both the yield on the bank's earning assets (loans and securities) and the cost of its funds (borrowing from depositors and lenders) also change. This impacts the bank's interest income and interest expense.

-

Reinvestment Risk: An additional form of interest rate risk is reinvestment risk. This is the uncertainty about the future interest rate the bank can earn by reinvesting its interest income in interest-bearing assets.

-

Price Risk (Market Risk): This refers to the uncertainty about the value of a bank's assets (like securities and loans) due to changes in market interest rates. When interest rates rise, the value of fixed-income securities and fixed-payment loans typically falls.

-

-

Hedging with ALM Strategies

-

Managing Risks: Banks use asset-liability strategies to manage both price risk and reinvestment risk.

-

Balance Sheet Adjustments: This can involve adjusting the mix, maturities, and amounts of assets and liabilities to lessen the impact of interest rate changes on net income.

-

Off-Balance-Sheet Solutions: Financial institutions can also use off-balance-sheet instruments like futures and swap contracts to hedge against the risk to net income caused by interest rate changes.

-

Topic 3. Net Interest Margin and Gap Management

-

Net Interest Margin (NIM): NIM is a key metric for bank performance.

-

NIM is calculated as: NIM = NII/Earning Assets

-

NII: Net interest income (NII) is calculated as: NII = Interest Income - Interest Expense

-

Earning Assets: Earning assets are the bank's assets that generate income, such as loans and securities.

-

-

Example: For Gray Sky Bank with $45 billion in earning assets, $4 billion in interest income, and $2.2 billion in interest expense, the NIM is ($4−$2.2)/$45=4.00%.

-

-

Interest-Sensitive (IS) Gap: The IS gap is a measure of interest rate risk.

-

IS Gap is calculated as: IS Gap = IS assets - IS liabilities

-

Asset vs. Liability Sensitive:

-

Positive IS gap: The bank has more interest-sensitive assets than liabilities and is considered asset sensitive.

-

Negative IS gap: The bank has more interest-sensitive liabilities than assets and is considered liability sensitive.

-

-

-

Steps to Estimate IS Gap:

-

Select Maturity Buckets: Define time periods (e.g., a day, a week, a year) based on when assets and liabilities will reprice (interest rates change to current market rates).

-

Add Assets and Liabilities: Place the dollar amounts of assets and liabilities that will reprice into the appropriate buckets.

-

Calculate IS Gap for Each Bucket: Determine the IS gap for each bucket (time period).

-

Estimate NII/NIM Changes: Use the bucket IS gaps to estimate NII and NIM for an assumed change in interest rates.

-

Topic 3. Net Interest Margin and Gap Management

-

An asset or liability is rate sensitive over a given time horizon if:

- It matures

- It is a variable-rate instrument

-

Prepayments or withdrawals are expected but uncertain.

-

Determination of Repricing period

- Easier for fixed-maturity securities, variable rates with specified reset schedules, and instruments with significant prepayment or withdrawal penalties.

- More difficult when prepayment timing is uncertain or when assets/liabilities have no specified maturity dates.

- Non-interest-bearing demand deposits (e.g., checking accounts) don't directly respond to rate changes but exhibit indirect sensitivity.

- Account balances fluctuate as interest rates on alternatives like money market accounts change, causing customers to shift funds.

- Cumulative Gap: It can be calculated by summing the IS gaps across some or all repricing periods (buckets).

- Relative Gap: Relative Gap = IS Gap/Total Assets

-

Interest Sensitivity Ratio (ISR): ISR = IS Assets/IS Liabilities

-

The relationship between the bank's IS Gap and its NII is

-

Change in NII = (Change in Rate) × IS Gap

-

Topic 3. Net Interest Margin and Gap Management

-

This equation is accurate when interest rates on all assets and liabilities change by the same amount, but this is an unlikely outcome. The relationships between the bank’s IS gap and its NII and NIM are:

- IS gap=0: NII and NIM are not affected by interest rate changes.

- IS gap>0: An increase in rates will increase NII and NIM, while a decrease will decrease them.

- IS gap<0: An increase in rates will decrease NII and NIM, while a decrease will increase them.

-

Limitations of IS Gap Management

-

If we relax the assumption that all interest rates at all horizons change in lock step, the weights in each bucket will affect the change in NII so that a simple average IS gap across all time periods will not suffice.

-

Also, the signs of interest rate changes at the various horizons, the rates of change in interest rates at various horizons, and the rates of change for interest rates on assets and liabilities could all differ as well.

-

- Most banks use computer modeling to estimate interest rate sensitivity due to these complexities.

- Management must set target net interest margin (NIM) goals and determine the appropriate asset/liability volume and mix to achieve them.

Topic 3. Net Interest Margin and Gap Management

-

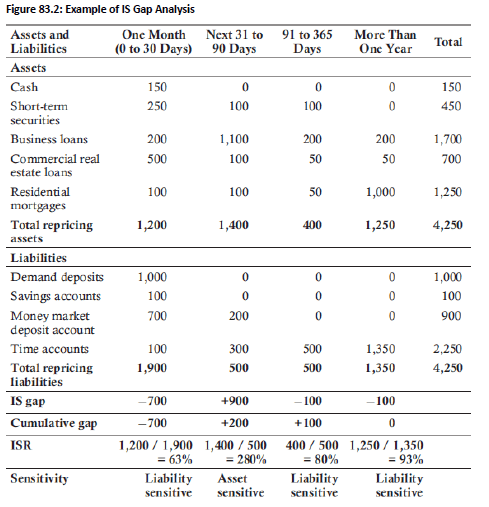

Fig 83.2 illustrates IS gap analysis and the effect of IS gap on NII and NIM in a simple case.

-

Assumptions:

-

Avg yield on IS assets: 6%

-

Avg cost of funds on IS liabilities: 3%

-

Avg yield on fixed-rate assets: 7%

-

Avg cost of fixed-rate liabilities: 4%

-

Avg earning assets: $4,250.

-

Under these assumptions,

-

NIM is as shown in Fig 83.3

-

-

Topic 4. Example of IS Gap Analysis

-

From Fig 83.2, we can see that the IS gaps for the four buckets are −700 for 0–30 days, 900 for 31–90 days, −100 for 91–365 days, and −100 for over 365 days.

-

The 0–30 day bucket has an IS gap of −700, making it liability sensitive; a 1% rate increase decreases NII by $7.00 (from $134.50 to $127.50).

- The 31–90 day bucket has an IS gap of +900, making it asset sensitive; a 1% rate increase increases NII by $9.00 (from $118.50 to $127.50).

- Cumulative IS gap across all horizons equals zero, implying that uniform rate changes across all maturities leave NII unaffected.

- Non-uniform rate changes at different horizons will impact NII even with a zero cumulative gap.

- Banks can manage IS gaps by adjusting asset/liability composition in each bucket or using derivative contracts (futures, swaps) to hedge interest rate risk.

- Banks confident in their rate forecasts may intentionally shift IS gaps toward asset or liability sensitivity to profit from expected rate movements.

Topic 4. Example of IS Gap Analysis

Practice Questions: Q2

Q2. A bank has a portfolio of short-term bonds. Holding the bank’s earning assets and cost of funds constant, in a rising interest rate environment, the bank’s:

A. NII and NIM will remain steady.

B. NII and NIM will decline.

C. NII and NIM will increase.

D. NII will decrease and NIM will increase.

Practice Questions: Q2 Answer

Explanation: C is correct.

The short-term bonds (assets) will reprice while the cost of funds holds steady, increasing NII and NIM.

Practice Questions: Q3

Q3. A mortgage bank has the major part of its assets in 30-year, fixed-rate mortgages. The bank has a small amount of core deposits but is mostly funded with repurchase agreements and one-quarter negotiable certificates of deposit (CDs). The bank’s 91-day interest-sensitive (IS) gap is most likely:

A. positive.

B. negative.

C. zero.

D. equal to its duration gap.

Practice Questions: Q3 Answer

Explanation: B is correct.

This bank likely has a negative IS gap because assets are not likely to reprice over the next 91 days (or at least only a very small portion will) but all of the negotiable CDs will reprice each quarter.

Practice Questions: Q4

Q4. The net interest margin (NIM) of a bank with a positive interest-sensitive (IS) gap will:

A. increase as interest rates increase.

B. increase as interest rates decrease.

C. decrease as interest rates increase.

D. any of these might happen.

Practice Questions: Q4 Answer

Explanation: A is correct.

The NIM of a bank with a positive IS gap will increase as interest rates increase. The bank is asset sensitive, meaning that assets will reprice faster than labilities, increasing net interest income (NII) and NIM.

Practice Questions: Q5

Q5. Paul Saunders, a risk manager and member of the asset-liability committee (ALCO) at National Bank and Trust, is considering strategies to hedge the bank’s net interest margin (NIM) against expected increasing interest rates. The bank currently has negative cumulative interest-sensitive (IS) gap positions over the one-month, one-quarter, and one-year maturity buckets. Which would be the

least effective strategy?

A. Selling long-term Treasury bonds and purchasing short-term Treasury bonds.

B. Shifting from a focus on making fixed-rate mortgages to a focus on making variable-rate mortgages.

C. Increasing the volume of overnight funding from the fed funds market and relying less on long- term funding from the Federal Home Loan Bank.

D. Shifting funding from overnight repurchase agreements to five-year retail certificates of deposit.

Practice Questions: Q5 Answer

Explanation: C is correct.

The bank needs to shift toward a zero or positive IS gap position from a negative gap position. The bank will see NIM squeezed in a rising rate environment as the cost of funds increases faster than the yield on earning assets. Any strategy that makes assets more rate sensitive or liabilities less rate sensitive will accomplish Saunders’ goal. Thus, the least effective would be shifting into shorter-term

funding (which will get more expensive in a rising rate environment) and out of longer-term funding. The least effective strategy would be to increase overnight funding from the fed funds market and shrink longer-term funding from the Federal Home Loan Bank.

Module 2. Duration Gap Management

Topic 1. Duration Gap Management to Protect Bank's Net Worth

Topic 2. Portfolio Duration and Change in Assets

Topic 3. Leverage-Adjusted Duration Gap

Topic 4. Limitations of Interest-Sensitive Gap Management

Topic 4. Limitations of Duration Gap Management

Topic 1. Duration Gap Management to Protect Bank's Net Worth

- Risk to Net Worth: While the interest-sensitive (IS) gap addresses risk to net investment income (NII), a bank's net worth (assets minus liabilities) is still exposed to interest rate risk.

- Approximating Change in Value: The effect of an interest rate change on the value of a bank's assets and liabilities can be approximated using duration.

- Duration: The duration of a bond is the time-weighted average of the present value of its expected cash flows, as a percentage of its current value

-

Percentage Change in Value: The approximate percentage change in a bond's value (ΔP/P) is calculated as:

-

-

-

Where

-

D is the duration,

-

i is the bond's current yield and

-

Δi is the change in the interest rate.

-

-

\frac{\Delta P}{P} \approx -D \times \frac{\Delta i}{1+i}

- Portfolio Duration: The duration of a portfolio of securities is a weighted average of the durations of the individual securities within that portfolio. The weights are the market values of each instrument.

-

Example: A bank has total assets of $250 million, including residential mortgages ($120 million, 7.4 years duration), commercial loans ($40 million, 0.8 years duration), Treasury securities ($60 million, 6.5 years duration), and consumer loans ($30 million, 1.4 years duration). Estimate the change in the market value of total assets for an increase in the appropriate discount rate from 2.5% to 3%.

-

The portfolio duration is calculated as:

-

-

For a 0.5% interest rate increase (from 2.5% to 3%), the estimated percentage change in asset value is:

-

-

The change in the value of total assets is approximately:

-

\frac{(120 \times 7.4)+(40 \times 0.8)+(60 \times 6.5)+(30 \times 1.4)}{250}=5.41 \text { years }

\frac{\Delta P}{P}=-5.41 \times \frac{0.005}{1.025} \approx-0.0264

Topic 2. Portfolio Duration and Change in Assets

\Delta P = -0.0264 \times \$ 250 \text { million }=-\$ 6.6 \text { million }

- Equal Duration is Not Enough: Simply matching the duration of assets to the duration of liabilities is insufficient to minimize the effect of interest rate changes on net worth, especially since a bank typically has positive net worth (assets > liabilities).

-

Leverage-Adjusted Duration Gap: It accounts for the initial values of assets and liabilities to ensure that the dollar value changes in response to IT changes are approximately equal.

-

-

Managing the Gap: To protect net worth from interest rate changes, a bank must manage its asset and liability durations so that the leverage-adjusted duration gap is equal to zero.

-

- Convexity Impact: A duration-based estimate of the change in security value is only an approximation. In practice, our estimate would be improved by also including the effect of convexity on the change in security value.

\text{Leverage-Adjusted Duration Gap}=D_A-D_L \times \frac{\text{Total Liabilities}}{\text{Total Assets}}

Topic 3. Leverage-Adjusted Duration Gap

\implies D_A =D_L \times \frac{\text{Total Liabilities}}{\text{Total Assets}}

-

To summarize, in order to hedge net worth against rate increases, banks should examine the duration of each of the bank’s assets and liabilities. The ALCO should:

-

Calculate the duration of loans, securities deposits, money market funding, etc.

-

Weight each of the durations by the market values of each instrument.

-

Sum the weighted durations to determine the duration of the asset and liability portfolios.

-

Calculate the duration gap.

-

-

The effect of the leverage-adjusted duration gap on the market (price) risk of assets and liabilities is:

-

Zero duration gap: The effect of interest rate changes on net worth is minimized.

-

Positive gap: Assets have more dollar market risk than liabilities. Net worth has interest rate risk, increases in rates will decrease net worth, and asset value will decrease more than liability value.

-

Negative gap: Liability value will fall more than asset value. Net worth has interest rate risk and increases in rates will increase net worth.

-

Topic 3. Leverage-Adjusted Duration Gap

Practice Questions: Q1

Q1. A bank has the major part of its assets in 30-year fixed-rate mortgages. The bank has a small amount of core deposits but is mostly funded with repurchase agreements and negotiable certificates of deposit (CDs). Assuming the bank’s assets are approximately 10% greater than its liabilities, the bank’s leverage-adjusted duration gap is most likely:

A. positive.

B. negative.

C. zero.

D. equal to its duration gap.

Practice Questions: Q1 Answer

Explanation: A is correct.

Given the large difference between the average maturity of its assets and its liabilities, the leverage-adjusted duration gap will be positive. This bank has long maturity (duration) assets funded with short maturity (duration) labilities. This means the bank's duration gap will be positive, while its IS gap is likely negative (with a positively sloped yield curve).

Practice Questions: Q2

Q2. Frank Bloomfield, a risk manager and asset-liability committee (ALCO) member at Bloomfield Bank, makes two statements to investors regarding the impact on the bank’s capital and profitability. The bank has a positive leverage-adjusted duration gap and negative interest-sensitive (IS) gap. Bloomfield states the following:

- Statement 1: Our bank has a positive leverage-adjusted duration gap, so the expected increasing interest rate environment will improve our bank's capital position.

- Statement 2: Our bank has a negative IS gap, so the expected increasing interest rate environment will improve our bank's NIM.

Which of the following is most correct?

A. Both statements made by Bloomfield are correct.

B. Both statements made by Bloomfield are incorrect.

C. Statement 1 is correct; Statement 2 is incorrect.

D. Statement 1 is incorrect; Statement 2 is correct.

Practice Questions: Q2 Answer

Explanation: B is correct.

Both statements made by Bloomfield are incorrect. If the bank has a positive duration gap, capital will decline as interest rates increase. Asset values will fall more than liability values, reducing capital. If the bank has a negative IS gap, the cost of funds will increase faster than the yield on earning assets in an increasing rate environment, shrinking the bank's NIM.

Topic 4. Limitations of Interest-Sensitive Gap Management

- Non-Uniform Rate Changes: The IS gap assumes that rates on all assets and liabilities move together, which is often not the case. Banks might change loan rates quickly but be slower to adjust savings rates.

- Weighted IS Gap: To address this, banks can use a weighted IS gap measure, which applies different weights to asset and liability rates based on their sensitivity to market changes. This provides a better reflection of the risk to NII.

- Difficulty in Identifying Repricing: It's often difficult to pinpoint the exact moment when assets and liabilities will reprice. The repricing of some variable-rate loans might be scheduled annually, while the short-term funds financing them reprice daily. This can lead to NII volatility even with a cumulative IS gap of zero.

-

Difficult to Define Cash Flows: It can be challenging to define the cash flow patterns for instruments like demand deposits and savings accounts, making their duration difficult to calculate. Prepayments on loans can also introduce uncertainty.

- Inaccuracy for Large Rate Changes: Duration is a more accurate measure of price sensitivity for small changes in interest rates. For larger changes, it is less accurate due to the convexity of the relationship between security values and their yields.

- Parallel Yield Curve Assumption: Duration analysis is based on the assumption that all interest rates on the yield curve change by the same amount, which is often not the case in reality. Short-term rates, for example, may change differently and at a different speed than longer-term rates

- Utility as a Tool: Despite these limitations, duration gap analysis remains a valuable tool for estimating the effect of interest rate changes on a bank's capital position.

Topic 5. Limitations of Duration Gap Management

Practice Questions: Q3

Q3. Which of the following is a limitation associated with duration gap?

A. Rates on assets and liabilities may not move together.

B. Rates may change at different speeds within a maturity bucket.

C. The point at which assets and liabilities reprice is not easy to identify.

D. It may be difficult to define the pattern of cash flows for instruments such as demand deposits.

Practice Questions: Q3 Answer

Explanation: D is correct.

It is difficult to calculate the duration of an asset or liability if the cash flow pattern is difficult to define. Rates on assets and liabilities moving out of sync and changing at different speeds within a maturity bucket are limitations associated with an IS gap. Also, the difficulty identifying the point at which assets and liabilities reprice is also a problem associated with an IS gap.

LTR 17. Risk Management for Changing Interest Rates- ALM and Duration Techniques

By Prateek Yadav