Book 2. Credit Risk

FRM Part 2

CR 1. Fundamentals of Credit Risk

Presented by: Sudhanshu

Module 1. Credit Risk Definition and Transaction Types

Module 2. Credit Risk Exposure

Module 1. Credit Risk Definition and Transaction Types

Topic 1. Credit Risk

Topic 2. Insolvency vs. Default vs. Bankruptcy

Topic 3. Transactions that Generate Credit Risk

Topic 1. Credit Risk

-

Definition: Credit risk is the probability that one party (a creditor or lender) will lose money if a counterparty (a borrower or obligor) fails to honor its financial obligation.

-

How it Arises: Credit risk can arise due to an inability, unwillingness, or nontimeliness of payment.

-

Inability to Repay: This is the most common reason. It could be due to a company's product becoming obsolete, capital expansion failure, or unanticipated events like macroeconomic shocks (e.g., the COVID-19 pandemic).

-

Unwillingness to Repay: A deliberate refusal to pay, often due to a dispute over the original contract.

-

Example: A sovereign state defaulting on its international debt, or forcing a conversion of its foreign currency debt obligations into domestic currency.

-

-

Nontimeliness of Obligation: Even a delay in payment can create credit risk for the creditor by contributing to lost interest or investment income.

-

- General Principle: The longer the term of a contract, the greater the credit risk.

-

Credit risk is assessed using:

- the amount of credit risk

- the probability of counterparty default

- the recovery amount and the timing of payment receipt

Practice Questions: Q1

Q1. Which of the following set of factors is most critical in helping creditors assess credit risk?

A. Amount of credit risk, probability of counterparty default, recovery amount/timing.

B. Foreign currency exposure, amount of credit risk, amount of illiquid counterparty assets.

C. Probability of counterparty default, counterparty management strength, recovery amount.

D. Recovery amount/timing, amount of uninsured assets, probability of counterparty insolvency.

Practice Questions: Q1 Answer

Explanation: A is correct.

While all factors listed are helpful in assessing credit risk, the three most important factors creditors want to assess are:

- the amount of credit risk,

- the probability of counterparty default, and

- the recovery amount and timing of payment receipt.

Topic 2. Insolvency vs. Default vs. Bankruptcy

-

A counterparty’s inability to pay its financial obligations can be due to insolvency, default, or bankruptcy.

-

Insolvency: An entity's liabilities (L) exceed its total assets (A), resulting in a negative equity (L > A).

-

Insolvent entities are not necessarily bankrupt.

-

-

Default: A counterparty fails to meet its contractual obligations.

-

A common reason for default is the inability or unwillingness to pay when

an obligation is due.

-

-

Bankruptcy: A legal procedure where an entity, typically in default, seeks legal protection through a court.

-

In a bankruptcy process, the court negotiates with the entity’s management, creditors, and other stakeholders.

-

The two forms of bankruptcy are dissolution/liquidation (Chapter 7 in the U.S.) and restructuring/reorganization (Chapter 11 in the U.S.).

-

Practice Questions: Q2

Q2. Acquaria Corporation’s year-end balance sheet shows $280 million in assets and $320 million in debt to creditors. Acquaria’s management estimates that it will continue to be able to meet its upcoming payment obligations. The company is best characterized as being:

A. bankrupt.

B. insolvent.

C. in default.

D. nonperforming.

Practice Questions: Q2 Answer

Explanation: B is correct.

Acquaria is best described as being insolvent, meaning its liabilities exceed the value of its assets. Acquaria continues to perform on its contractual obligations.

Default occurs when an entity fails to meet its contractual obligations. Bankruptcy occurs when an entity seeks legal protection through a court.

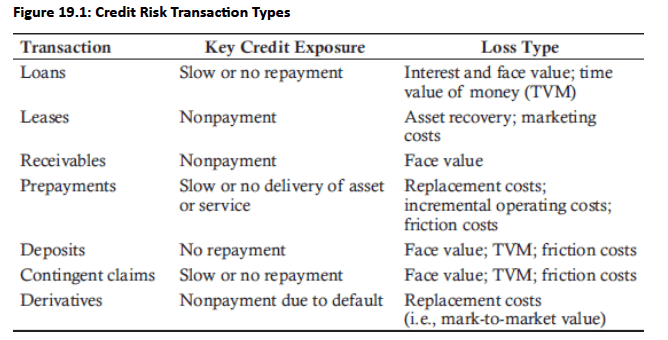

Topic 3. Transactions that Generate Credit Risk

-

Credit risk can arise out of many complex activities, including trade transactions involving future payments, derivatives transactions, claims on collateral, and contingent liabilities.

-

In the U.S., corporate obligations constitute the largest source of credit exposure, concentrated in domestic financial companies.

-

Globally, the largest source of credit exposure by notional value is from derivatives, estimated at $600 trillion in June 2020, with most from interest rate derivatives.

Topic 3. Transactions that Generate Credit Risk

-

The main transaction types that generate credit risk are as follows:

-

Lending: When funds are lent, the lender faces the risk that the borrower may fail to repay principal or interest in the future.

-

Leases: Lessors are exposed to credit risk if lessees fail to make scheduled lease payments over the lease term.

-

Receivables: Sellers who allow delayed payment for goods or services face the risk of non-payment by the buyer.

-

Prepayments: Entities that pay in advance for goods or services face the risk that delivery may not occur, such as in the event of the supplier’s bankruptcy.

-

Deposits: Customers are exposed to credit risk if banks fail to provide timely access to deposits, with large corporates typically managing this risk through due diligence.

-

Contingent claims: Credit risk arises when future payments depend on events, such as insurers failing to honor claims or pension sponsors lacking sufficient assets.

-

Derivatives: Derivatives create ongoing counterparty credit risk because future payments may be required over the life of contracts such as forwards, swaps, repos, and options.

-

Module 2. Credit Risk Exposure

Topic 1. Enitities Exposed to Credit Risk

Topic 2. Banks

Topic 3. Asset Managers

Topic 4. Hedge Funds

Topic 5. Insurance Companies

Topic 6. Pension Funds

Topic 6. Corporations

Topic 8. Individuals

Topic 9. Managing Credit Risk

Topic 1. Enitities Exposed to Credit Risk

-

Credit risk is a natural byproduct: Exposure to credit risk is not inherently negative and commonly arises from routine activities of corporations, governments, and individuals.

-

Everyday examples: Prepaid rent or selling goods on credit exposes landlords and businesses to credit risk.

-

Sector concentration: In the U.S., the financial sector holds the largest credit exposure, mainly through depository institutions and mutual funds, followed by insurers, pension plans, and finance companies.

Topic 2. Banks

-

Sources of credit risk: Banks face significant credit risk from retail and corporate lending, as well as from derivatives activities and counterparty exposures.

-

Risk management sophistication: Banks are among the most advanced institutions in managing credit risk, although overall risk appetite in the sector has declined in recent years.

-

Collateralized lending risk: Repo and other secured lending expose banks to counterparty default risk, partially mitigated by collateral.

-

Residual collateral risk: In fast-moving markets, collateral values can fall rapidly and may become insufficient to fully cover outstanding obligations.

-

Derivatives counterparty exposure: Banks also face counterparty credit risk through derivatives used for hedging and trading portfolios.

-

Scale of exposure: Large institutions can have extremely high derivatives receivable exposures, such as JPMorgan Chase reporting over $700 billion in 2020.

Practice Questions: Q1

Q1. A bank has entered into a $25 million, 6-month repurchase agreement with an investment grade corporate client, collateralized by $26 million notional value, 10-year state bonds. The bank has:

A. no credit risk because the repurchase agreement matures before the bonds.

B. no credit risk because the client is rated investment grade; therefore, counterparty default is unlikely.

C. no credit risk because the notional value of the bonds exceeds the value of the repurchase agreement.

D. credit risk because if the client defaults, the bank may not be able to sell the bonds to cover the full amount of the repurchase agreement.

Practice Questions: Q1 Answer

Explanation: D is correct.

The repurchase agreement exposes the bank to the risk that the client will not repay its obligation or will default. Although the collateral mitigates this risk, in a stressed or unfavorable market, the collateral value may decline and no longer sufficiently cover the amount owed to the bank under the repurchase agreement.

Topic 3. Asset Managers

-

Investment and risk objectives: Asset managers invest client funds across a spectrum of return and risk objectives, exposing portfolios to varying levels of credit risk.

-

Role of risk management: Risk management teams provide independent assessment and oversight of fund managers’ investment decisions.

-

Credit risk focus: A core risk management objective is to mitigate credit risk by evaluating the creditworthiness of corporate and government issuers of bonds, equities, and other securities.

Topic 4. Hedge Funds

-

Higher risk appetite: Hedge funds typically operate with higher risk tolerance and aggressive mandates, investing in risky instruments such as private equity, private debt, alternatives, and distressed securities, and may sell credit protection.

-

Default as opportunity: Unlike traditional asset managers, hedge fund managers may view default or financial distress as an investment opportunity rather than a risk to hedge or avoid, using both direct positions and derivatives like CDSs.

-

Short-selling and downside risk: Strategies such as short selling distressed debt or equity can generate high returns but expose funds to significant losses if prices move sharply against expectations.

-

Example: Melvin Capital’s 2021 short position in GameStop led to massive losses when the share price surged unexpectedly, requiring a bailout to avoid default.

Topic 5. Insurance Companies

-

Multiple sources of credit exposure: Insurance companies face credit risk across underwriting, investment activities, and reinsurance arrangements.

-

Underwriting risk: Insurers collect premiums, invest them, and later pay claims, requiring a balance between generating returns for shareholders and minimizing risk to policyholders.

-

Investment-related risk: Assets managed in separate accounts do not affect shareholders directly if losses occur, but significant losses can damage the insurer’s reputation and future business prospects.

-

Reinsurance credit risk: Credit exposure arises from the time lag between claim submission and reimbursement by reinsurers, with large or long-dated claims (e.g., catastrophe losses) creating substantial reinsurance recoverables and long-term credit risk.

-

Topic 6. Pension Funds

-

Role of pension funds: Pension funds invest assets on behalf of plan members, similar to how asset managers invest on behalf of clients.

-

Exposure to credit risk: Investments in credit-risky securities can create significant credit risk for pension plan members.

-

Regulatory guardrails: Tighter regulation of public and private pension funds has introduced strong risk management requirements to protect plan members.

Topic 7. Corporations

-

Sources of corporate credit risk: Corporations face credit risk from customer behavior, market disruptions (e.g., pandemics, shifts to online demand), and counterparties across operations and investments.

-

Accounts receivable: Credit risk arises when customers receive goods before payment and later default. Assessing credit quality is easier for large firms and harder for small firms or individuals due to limited data.

-

Mitigation methods include receivables insurance, factoring, and documentary credit for foreign transactions.

-

-

Short-term investments and bank deposits: Credit risk arises when issuers or banks fail to meet interest, principal, or deposit obligations, and is commonly mitigated by diversifying deposits across multiple banks.

-

Derivatives exposure: Exchange-traded futures pose low credit risk due to margining and clearinghouse guarantees but TC forwards and swaps create bilateral counterparty risk that can force costly market replacement.

-

Firms with large derivatives exposure typically use advanced risk management practices.

-

-

Vendor financing: Firms offering financing or leasing face credit risk from defaults or nonpayment.

-

Supply chain credit risk: Reliance on single or critical suppliers exposes firms to losses from supplier default or delivery failures as upply disruptions (e.g., Suez Canal blockage) can lead to significant operational and financial losses.

Practice Questions: Q2

Q2. Which of the following options would a corporation least likely select to mitigate its receivables credit risk?

A. Factoring.

B. Insurance.

C. Derivatives.

D. Documentary credit.

Practice Questions: Q2 Answer

Explanation: C is correct.

Corporations typically mitigate receivables credit risk in one of following three ways:

- Buying insurance on their account receivables

- Selling their receivables to another company (i.e., factoring)

- Securing foreign transactions through documentary credit

Topic 8. Individuals

-

Prepayment risk: Individuals face credit risk when they prepay for goods or services, as losses may occur if delivery does not happen.

-

Bank deposit risk: Deposits expose individuals to the credit risk of bank failures.

-

Investment counterparty risk: Individuals are also exposed to credit risk through investments held with asset managers.

-

Risk mitigation via insurance: In some countries (e.g., the US and Canada), federal deposit insurance reduces the risk of losses on bank deposits.

-

Successful companies maintain sufficient equity to absorb both expected and unexpected losses while supporting survival, profitability, and ROE.

-

Survival: Managing credit risk ensures that companies avoid large losses, and therefore, do not face bankruptcy.

-

Profitability: Managing credit exposure and avoiding losses will help increase profitability.

-

Return on equity: Successful companies find the right balance between debt and equity to maximize their return on equity.

-

Topic 9. Managing Credit Risk

CR 1. Fundamentals of Credit Risk

By Prateek Yadav