Book 4. Liquidity and Treasury Risk

FRM Part 2

LTR 2. Liquidity and Leverage

Presented by: Sudhanshu

Module 1. Sources of Liquidity Risk, Liquidity Transformation and Systematic Funding

Module 2. Collateral Market and Leverage

Module 3. Funding and Transactions, Liquidity Risk and Transactions Cost

Module 1. Sources of Liquidity Risk, Liquidity Transformation and Systematic Funding

Topic 1. Sources of Liquidity Risk

Topic 2. Liquidity Transformation by Banks

Topic 3. Structured Credit Products and Off-Balance Sheet Vehicles

Topic 4. Systematic Funding Liquidity Risk

Topic 1. Sources of Liquidity Risk

-

Liquidity for asset and market:

-

An asset is liquid if it can be sold quickly and cheaply without a significant price decrease.

-

A market is liquid if positions can be unwound quickly and at a low transaction cost, without an "undue price deterioration".

-

- Transactions vs. Funding Liquidity: Transactions liquidity deals with financial assets and financial markets. Funding liquidity is related to an individual’s or firm’s creditworthiness.

- Transactions (or Market) Liquidity Risk: Buying or selling an asset will cause an adverse price movement.

-

Funding Liquidity (or Balance Sheet) Risk: A borrower's creditworthiness is deteriorating or is perceived to be deteriorating by the market. It also occurs when the market as a whole deteriorates.

-

As a result, creditors withdraw credit or change credit terms (increase collateral) and the position may become unprofitable or need to be unwound.

-

Maturity Mismatch: This occurs when a borrower funds longer-term assets with shorter-term liabilities. It is often profitable because short-term debt has a lower required rate of return.

-

The incentive is even greater when the yield curve is upward sloping.

-

-

-

Funding Liquidity Risk (...continued):

-

Rollover Risk (aka cliff risk): The risk that short-term debt cannot be refinanced or can only be refinanced at escalating rates.

-

-

Systemic Risk: The entire financial system is impaired due to severe financial stress, which can lead to a breakdown in credit allocation.

Topic 1. Sources of Liquidity Risk

-

Interrelated Risk Amplification: Liquidity risks are interconnected and can compound problems.

- For example, increased collateral requirements can force early position unwinding at a loss, where increased funding liquidity risk amplifies transactions liquidity risk.

- Leverage as Critical Link: Leverage connects funding and transactions liquidity; investors forced to sell assets due to funding constraints reduce the pool of potential buyers, lowering asset valuations and potentially creating a debt-deflation crisis through rapid deleveraging.

- Portfolio Liquidity Dilemma: When facing redemptions, asset managers must choose between selling liquid assets or selling illiquid assets.

- Procyclical Liquidity Constraints: Economy-wide liquidity directly impacts systemic risk; market deterioration constrains liquidity precisely when investors need it most, as severe financial stress affects all participants simultaneously

- Systemic Contagion Risk: Liquidity risk events can become systemic through disruptions in payment, clearing, and settlement systems, with the illiquidity or insolvency of one counterparty creating a domino effect throughout the financial system.

Topic 2. Interconnected Liquidity Risks

Practice Questions: Q1

Q1. Jackson Grimes, a trader for Glenn Funds, works on the repurchase agreement (repo) desk at his firm. Markets have been highly volatile but Glenn Funds has a large capital base and is sound. Grimes reports to the CEO that in the last month, the firm Glenn Funds borrows from has been consistently increasing collateral requirements to roll over repos. From the perspective of Glenn Funds, this represents:

A. systematic risk.

B. transactions liquidity risk.

C. balance sheet risk.

D. maturity transformation risk.

Practice Questions: Q1 Answer

Explanation: C is correct.

Funding liquidity risk or balance sheet risk results when a borrower's credit position is either deteriorating or is perceived by market participants to be deteriorating. It also occurs when the market as a whole deteriorates. Under these conditions, creditors may withdraw credit or change the terms of credit. In this case, the lender is increasing the haircut and is thus changing the terms of credit. Glenn Fund's creditworthiness does not actually have to decline for a lender to withdraw credit or change the terms of credit.

Practice Questions: Q2

Q2. Chris Clayton, an analyst for a private equity fund, noticed that merger arbitrage strategies at several hedge funds experienced large losses in late 2007 to early 2008. These losses were likely due to:

A. abandoned merger plans due to a lack of available financing.

B. target prices falling precipitously due to stock market corrections.

C. acquirers filing for bankruptcy as the subprime mortgage crisis unfolded.

D. idiosyncratic risks surrounding the merger arbitrage strategy.

Practice Questions: Q2 Answer

Explanation: A is correct.

Systematic funding risks were apparent in many market sectors during the subprime mortgage crisis. Hedge funds engaged in merger arbitrage experienced losses in the early stages of the subprime mortgage crisis. After a merger is announced, the target's stock price typically increases and the acquirer's price sometimes declines due to increased debt. The merger arbitrage strategy exploits the difference between the current and announced acquisition prices. Hedge funds experienced large losses as mergers were abandoned when financing dried up.

Topic 2. Liquidity Transformation by Banks

-

Commercial bank assets are typically longer-term and less liquid than bank liabilities (e.g., deposits).

-

Wholesale funding (i.e., non-deposit sources of funding like commercial paper, bonds) is generally longer term but deposits are “sticky.”

-

Depositors generally change banks only in extraordinary circumstances. Deposits make up approximately 65% of bank liabilities in the U.S.

-

Fractional-Reserve Bank: Banks only expect a fraction of deposits and other liabilities to be redeemed at any point in time. As a result, they do not hold all the deposits in liquid assets, but make loans with deposits instead.

-

Asset-Liability Management (ALM): Using deposits to finance loans is called ALM.

-

Fractional Reserves: Banks don't hold all deposits in liquid assets because they only expect a fraction of deposits to be redeemed at any given time. They lend out the rest. This is the basis of a fractional-reserve bank.

-

Suspension of Convertibility: If withdrawals exceed a bank's reserves, the bank will not be convert deposits immediately to cash.

-

Bank Runs: An extreme case where depositors, concerned about a bank's liquidity, rush to withdraw their money before depositors and lenders.

Topic 2. Liquidity Transformation by Banks

-

Rollover Risk: Similar to bank runs but less extreme. Rollover risk on other short-term financing can increase a bank's fragility. Higher capital reduces bank fragility.

-

Role of Regulators: The Lehman Brothers failure illustrated the fragility of bank funding, with commercial paper markets freezing up.

-

In response, the Federal Reserve created facilities like the Commercial Paper Funding Facility (CPFF) and the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) to provide liquidity.

-

Topic 3. Structured Credit Products and Off-Balance Sheet Vehicles

-

Structured Credit and Liquidity Risk

-

Structured credit products like asset-based securities (ABSs) and mortgage-backed securities (MBSs) match investor funding needs with pooled assets.

-

ABSs and MBSs are maturity-matched and not subject to funding liquidity issues.

-

Liquidity risk arises when investors in these products use short-term financing to fund their investments. This was a major driver of the 2007-2009 subprime crisis.

-

Two types of short-term financing include:

-

Securities leading (i.e., applying structured credit products as collateral to short-term loans), and

-

Off-balance sheet vehicles.

-

-

-

Off-Balance Sheet Vehicles

-

Special-purpose vehicles (SPVs) act as off-balance sheet vehicles by issuing secured debt in the form of asset-backed commercial paper (ABCP).

-

ABCP conduits finance purchases of assets, such as securities and loans, with ABCP. They receive liquidity and credit support via credit guarantees.

-

Structured investment vehicles (SIVs) are similar to ABCP conduits but do not receive the same level of liquidity and credit support.

-

-

ABCP conduits and SIVs profited from the spread between funding costs and asset yields before subprime crisis.

-

Assets held by ABCP conduits and SIVs typically had longer maturities than the ABCP that fund the assets.

-

In addition to maturity transformation, these vehicles also provided liquidity transformation.

-

This is done by creating ABCP that was more liquid and had shorter terms than the assets held in the conduit and SIV.

-

They engaged in maturity and liquidity transformation by creating shorter-term, more liquid ABCP to fund longer-term assets.

-

Despite being off-balance sheet, which permitted firms to hold less capital, these vehicles did not entirely transfer risk.

-

As a result, they still contributed to the leverage issues and fragility of the financial system during the subprime crisis.

Topic 3. Structured Credit Products and Off-Balance Sheet Vehicles

Topic 4. Systematic Funding Liquidity Risk

-

Systematic funding risks affect both borrowers and lenders at the same time, particularly when loans become shorter term.

-

These "soft risks" are difficult to link to a specific series of asset returns. Analysts must examine data on credit and liquidity spreads, as well as the availability of credit, to understand the probability of a liquidity freeze.

-

Examples from the 2007-2009 Crisis

-

Leveraged Buyouts (LBOs): During the crisis, funding for LBOs dried up, causing deals to fall apart and banks to incur significant losses on "hung loans" that couldn't be distributed to investors.

-

Merger Arbitrage Hedge Funds: These funds, which exploit the price difference between a target company's stock and the acquisition price, experienced large losses when mergers were abandoned due to a lack of financing.

-

Convertible Arbitrage Hedge Funds: These funds rely on leverage from broker-dealers. When financing became unavailable during the crisis, convertible bond values dropped sharply. This funding liquidity problem was compounded by redemptions, a market liquidity problem.

-

-

Money Market Mutual Funds (MMMFs)

- MMMFs are like banks in that they are obligated to repay investors on demand, even though their liabilities are more liquid than their underlying investments.

- Amortized Cost Method: Under SEC Rule 2a-7, MMMFs are not required to mark their assets to market daily, unlike other mutual funds.

- Breaking the Buck: While MMMFs' assets are typically high-credit, short-term instruments valued at a notional $1.00 per share, credit write-downs can cause the net asset value (NAV) to fall below this value.

- Runs on MMMFs: Similar to banks, MMMFs are subject to runs. If many investors try to redeem shares during adverse market conditions, the fund may be forced to sell assets at a loss, potentially resulting in write-downs and "breaking the buck".

Topic 4. Systematic Funding Liquidity Risk

Practice Questions: Q3

Q3. With respect to the valuation of money market mutual fund (MMMF) assets, funds:

A. are not required to mark-to-market the underlying assets daily.

B. must reflect changes in the values of underlying assets that are the result of changes in credit risks but may ignore value changes that are the result of changes in interest rates.

C. will set the notional values of each of the underlying assets equal to $1.00.

D. are not allowed to invest in any asset with a rating below AAA because asset values must not fluctuate outside of a 10% range around the historical value in order to keep the notional value equal to $1.00.

Practice Questions: Q3 Answer

Explanation: A is correct.

MMMFs use a form of accounting called the amortized cost method, under the Securities and Exchange Commission's (SEC) Rule 2a-7. This means that MMMF assets do not have to be marked-to-market each day, as required for other types of mutual funds. However, the values of the underlying assets in the fund, despite their relative safety, are subject to change. As such, redemptions may be limited if asset values fall.

Module 2. Collateral Market And Leverage

Topic 1. Economics of the Collateral Market

Topic 2. Leverage Ratio and Leverage Effect

Topic 3. Margin Loans and Leverage

Topic 4. Short Positions and Leverage

Topic 5. Derivatives and Leverage

Topic 1. Economics of the Collateral Market

-

Collateral Markets: Markets where assets (securities) are pledged to secure a loan.

-

Two Primary Purposes:

-

Enhance Borrowing:

-

Enable Short Positions

-

-

Key Risk: Collateral values fluctuate, necessitating regular adjustments.

-

Haircut: The difference between the collateral market value and loan lent against it.

-

Remargining: The process of adjusting posted collateral as its value fluctuates, requiring additional funds to restore the required margin level.

-

Variation Margin: Extra funds requested to cover losses and ensure the margin requirement remains adequate as market values change.

-

Rehypothecation: Collateral received in a secured transaction is reused or pledged again to finance other assets or trades, allowing the same collateral to circulate through multiple transactions.

Topic 1. Economics of the Collateral Market

-

Forms of Collateral Market Transactions

- Margin Loans: Collateralized by the purchased security, typically provided by the broker.

-

Street Name Accounts: Securities are registered in the broker's name, making it easier to seize and sell them to meet margin calls.

-

Regulation T: Sets the initial margin requirement at 50% for securities purchases.

-

Cross-margin agreements are used to establish the net margin position of investors with portfolios of long and short positions.

-

-

Repurchase Agreements (Repos): Collateralized short-term loans. The interest is implied from the difference between the spot sale price and the forward repurchase price.

-

Securities Lending: Loan of securities (often to short-sellers) in exchange for cash collateral and a fee (rebate). The lender continues to receive dividends and interest.

-

Total Return Swaps (TRS): One party pays a fixed fee for the total return (income + capital gains) of a reference asset, gaining synthetic ownership without the balance sheet implications. The party providing the return is short the asset.

- Margin Loans: Collateralized by the purchased security, typically provided by the broker.

Topic 2. Leverage Ratio and Leverage Effect

-

Leverage Ratio (L): The ratio of a firm's assets (A) to its equity (E)

-

-

-

Lowest value is 1.0 (all-equity financed).

-

-

As debt increases, the leverage ratio (i.e.,multiplier) increases. For example, a firm with $100 of assets financed with $50 debt and $50 equity has a leverage ratio equal to 2.0 (= $100/$50).

-

Leverage Effect: The principle that Return on Equity ( ) is magnified by leverage, provided the Return on Assets ( ) exceeds the Cost of Debt ( ).

-

Return on Equity ( ) Formula:

-

Where:

-

= Return on Assets

-

= Cost of Debt

-

L = Leverage Ratio

-

(L - 1) = The multiplier for the cost of debt, which represents the proportion of the balance sheet financed with debt.

-

-

- The cost of debt is multiplied by the factor (L-1). For L=4, (L-1)=3 => debt costs are multiplied by 3 because 3/4 of the balance sheet is financed with debt.

r_E

r_E

r_A

r_A

r_D

r_D

L = \frac{A}{E} = \frac{E + D}{E} = 1 + \frac{D}{E}

r_{E} = L r_{A} - (L - 1) r_{D}

-

Impact of Changing Leverage

-

Change in ROE ( ) due to Change in Leverage ( ):

-

-

Key Insight: ROE increases when leverage increases, but only if the firm's assets generate a return greater than the cost of the borrowed funds used to finance them.

-

Double-Edged Sword: Leverage amplifies both gains and losses.

-

\partial r_E

\partial L

\frac{\partial r_{E}}{\partial L} = r_{A} - r_{D}

Topic 2. Leverage Ratio and Leverage Effect

Practice Questions: Q1

Q1. Charleston Funds intends to use leverage to increase the returns on a convertible arbitrage strategy. The return on assets (ROA) of the strategy is 8%. The fund has $1,000 invested in the strategy and will finance the investment with 75% borrowed funds. The cost of borrowing is 4 %. The return on equity (ROE) is closest to:

A. 4 %.

B. 32%.

C. 20%.

D. 12%.

Practice Questions: Q1 Answer

Explanation: C is correct.

\begin{aligned}

\text {Debt }&=\$ 1,000 \times 0.75=\$ 750 \\

\text {Leverage Ratio }&=\text { Total Assets} / \text {Equity } = \$ 1,000 / \$ 250=4 \\

r_E&=\operatorname{Lr}_A-(L-1) r_D \\

\text {Return on Equity }&=4(8 \%)-[(4-1)(4 \%)]=32 \%-12 \%=20 \%

\end{aligned}

Topic 3. Margin Loans and Leverage

-

Explicit Leverage: Directly using borrowed funds to finance assets (e.g., issuing bonds, purchasing stock on margin).

-

Implicit Leverage: Embedded in transactions that offer large exposure with a small capital outlay (e.g., short sales, derivatives such as options and swaps).

-

Margin Loan Mechanics

-

The stock purchased with margin loan is collateral for the loan.

-

The haircut (h) is the borrower's equity contribution.

-

1 − h is loaned against the market value of the collateral.

- Leverage is calculated as 1/h.

-

The Federal Reserve requires that an investor put up a minimum of 50% equity (i.e., h = 50%) in a stock purchase using borrowed funds

-

-

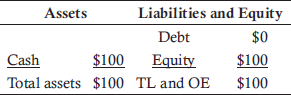

Scenario: First, assume that a firm has $100 cash invested by the owners (i.e., no borrowed funds). The balance sheet in this case is:

-

-

-

-

-

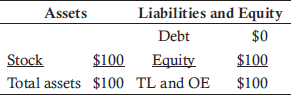

If the firm uses the cash to purchase stock, the balance sheet is:

-

-

-

-

Thus, the leverage ratio is equal to 1 (i.e., $100/$100 or 1.0/1.0).

-

-

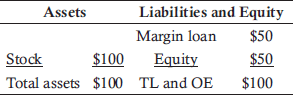

Now, assume that the firm uses 50% borrowed funds and invests 50% (i.e., h = 50%) equity to buy shares of stock. Immediately after the trade, the margin account balance sheet has 50% equity and a $50 margin loan from the broker:

-

-

-

-

-

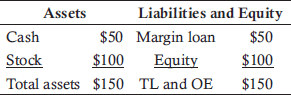

The full economic balance sheet due to borrowed funds (remember, owners put in $100 of equity initially so the firm now has $100 of stock and $50 of cash) is:

-

-

-

-

-

Thus, the leverage ratio has increased to 1.5 (i.e., $150/$100 or 1/0.667). Note that the broker retains custody of the stock to use as collateral for the loan

Topic 3. Margin Loans and Leverage

Topic 4. Short Positions and Leverage

-

Process: An investor borrows shares of a security and sells them.

-

Liability: The obligation to return the borrowed shares (Short Position).

-

Asset: The cash proceeds from the sale cannot be used for other investments and are held in a short account.

-

Margin Account: If the stock price increases, the firm need to add funds in a margin account.

-

Balance Sheet Impact: The transaction lengthens the balance sheet because both the cash proceeds and the obligation to return the securities appear.

-

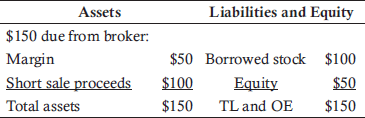

Transaction: Short sale of $100 of stock, short account has $50 equity and the margin account has a $50 margin loan from the broker.

-

-

The firm’s full economic balance sheet given the short sale is:

-

-

-

-

-

Thus, the leverage ratio has increased to 2.0 (i.e., $200/$100 or 1/0.50).

-

The leverage is higher in this case because the full value of the stock is borrowed in a short transaction.

-

Leverage in Short Vs Long Position:

-

Leverage is inherent in the short position but is a choice in the long position.

-

The firm only borrows 50% of the balance of the stock in the long position.

-

-

Hedging using Short Position: If the short position plays a hedging role in the portfolio, the position will reduce market risk.

-

Leverage impact on Risk: Leverage will overstate the overall risk because it ignores the potential risk reducing benefits of the short positions. As such, a distinction must be made between gross and net leverage.

-

Gross Leverage: The value of all the assets, including cash generated by short sales, divided by capital.

-

Net leverage: The ratio of the difference between the long and short positions divided by capital.

Topic 4. Short Positions and Leverage

Practice Questions: Q2

Q2. Assume a broker provides a margin loan to a U.S. hedge fund that puts up the minimum equity amount required by the Federal Reserve. If the hedge fund wants to take a $250,000 equity position, determine the margin loan amount and the leverage ratio of this position.

A. Margin loan = $125,000; leverage ratio = 1.0.

B. Margin loan = $125,000; leverage ratio = 2.0.

C. Margin loan =$ 250,000; leverage ratio =0.0.

D. Margin loan=$250,000; leverage ratio =1.0.

Practice Questions: Q2 Answer

Explanation: B is correct.

The Federal Reserve requires an initial margin of 50 % (i.e., haircut is 50%). Therefore, the margin loan will be . The leverage ratio is equal to total assets divided by equity. Therefore, the hedge fund's leverage ratio is 2.0 (=$ 250,000/$125,000).

\$ 125,000(=\$ 250,000 \times 50 \%)

Topic 5. Derivatives and Leverage

Derivatives provide exposure to an underlying asset's price movement without actually buying or selling the asset.

Derivatives also allows investors to increase leverage.

Derivatives are generally off-balance sheet but they should be included on the economic balance sheet as they affect an investor’s returns.

Derivatives are synthetic long and short positions.

We need to find the cash-equivalent market value for each type of derivative to estimate the economic balance sheet.

-

Major derivatives include:

Futures, forward contracts, and swap contracts: Linear and symmetric to the underlying asset price. The amount of the underlying instrument is set at the initiation to represent the values on the economic balance sheet by the market value of the underlying asset. These contracts have zero (NPVs) at initiation.

Option contracts: Non-linear relationship to the underlying asset price. The amount of the underlying represented by the option changes over time. The value can be fixed at any single point in time by the option delta. Thus, on the economic balance sheet, the cash equivalent market values can be represented by the delta equivalents rather than the market values of the underlying assets. These contracts do not have zero NPVs at initiation because the value is decomposed into an intrinsic value (which may be zero) and a time value (which is likely not zero).

Topic 5. Derivatives and Leverage

-

In this example, the counterparty is assumed to be the prime broker or broker-dealer executing the positions. This means that margin will be assessed by a single broker on a portfolio basis.

-

First, assume the firm enters a 1-month currency forward contract and is short $100 against the euro and the 1-month forward exchange rate is $1.25 per euro. The balance sheet is:

-

-

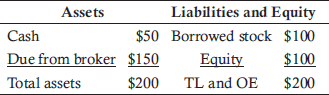

Now, assume the firm buys a 3-month ATM call option on a stock index with an underlying index value of $100. The call’s delta is currently 50%. The transaction is equivalent to using a $50 broker loan to buy $50 of the stock index.

-

-

Next, assume the firm enters a short equity position via a total return swap (TRS). The firm pays the total return on $100 of ABC stock and the cost of borrowing the ABC stock (i.e., the short rebate). This is equivalent to taking a short position in ABC. Assuming the market price of ABC is $100, we have:

-

Topic 5. Derivatives and Leverage

-

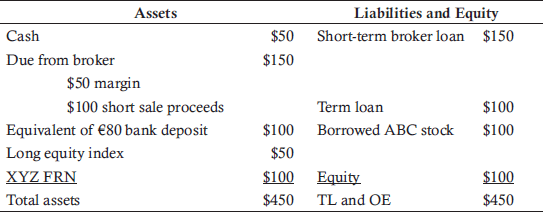

Finally, assume the firm adds short protection on company XYZ via a 5-year CDS with a notional value of $100. This position is equivalent to a long position in a par-value 5-year floating rate note (FRN) financed with a term loan.

-

The firm’s combined economic balance sheet that includes all of the derivatives positions is:

-

-

The firm has increased its leverage to 3.5 in its long positions. The long positions combined with the short position (the ABC TRS) means the firm has gained exposure to securities valued at $450 using $50 of cash.

-

Computing leverage is complex when derivatives are used.

-

Correctly interpreting leverage is important since risk may be mitigated if short positions are used to hedge. Example: FX and IR risk can be hedged accurately but the positions must be of the same magnitude as the underlying assets.

-

If the positions are carried on the economic balance sheet, leverage will be overstated and other material risks in the portfolio may be ignored.

Module 3. Funding And Transactions, Liquidity Risk, And Transactions Cost

Topic 1. Sources of Transactions Liquidity Risk

Topic 2. Transactions Cost

Topic 3. Adjusting VaR for Position Liquidity

Topic 4. Measuring Market Liquidity

Topic 5. Funding Liquidity Risk Management

Topic 1. Sources of Transactions Liquidity Risk

-

Transactions (Market) Liquidity Risk: Risk that buying or selling an asset will result in an unfavorable price change. It is related to costs associated with finding the counterparty.

-

Market microstructure fundamentals help in understanding transactions liquidity risk:

-

Trade processing costs: Trade's processing, clearing and settlement costs.

-

Inventory management: Dealers hold long or short inventories of assets and compensated by price concessions. This risk is a volatility exposure.

-

Adverse selection: Dealers must differentiate between liquidity or informed and information traders. Dealers do not know which of the two are attempting to trade and must be compensated for this lemons risk through the bid-ask spread. The spread is wider if the dealer believes he is trading with someone who knows more than he does. However, the dealer does have more information about the flow of trading activity (i.e., is there a surge in either buy or sell orders).

-

Differences of opinion: It is more difficult to find a counterparty when market participants agree (e.g., the GFC) than when they disagree. Investors generally disagree about the correct or true price on an asset.

-

Topic 1. Sources of Transactions Liquidity Risk

-

Market microstructure fundamentals differ across different types of market organizations. For example:

-

In a quote-driven system (common in OTC markets), market makers are expected to publicly post 2-way prices or quotes and to buy or sell at those prices within identified transaction size limits.

-

In contrast, order-driven systems (common in organized exchanges) are more similar to competitive auction models.

-

Typically the best bids and offers are matched throughout the trading session.

-

-

Liquidity risks are introduced when bid-ask spreads fluctuate through:

- Adverse price impact: The trader’s actions impact the equilibrium price of the asset

-

Slippage: The price of an asset falls in the time it takes to settle a trade

-

Regulators have focused more on credit and market risks and less on liquidity risk.

-

Liquidity risk is difficult to measure. However, since the GFC, more attention is being paid to measuring liquidity risks in a firm.

Practice Questions: Q1

Q1. Brett Doninger recently placed an order to sell a stock when the market price was $42.12. The market was volatile and, by the time Doninger’s broker sold the stock, the price had fallen to $41.88. In the market, this phenomenon is known as:

A. adverse selection.

B. transactional imbalance.

C. slippage.

D. the spread risk factor.

Practice Questions: Q1 Answer

Explanation: C is correct.

Liquidity risks are introduced when bid-ask spreads fluctuate, when the trader’s own actions impact the equilibrium price of the asset (called adverse price impact), and when the price of an asset deteriorates in the time it takes a trade to get done. When the price deteriorates in the time it takes to get a trade done, it is called slippage.

Topic 2. Transactions Cost

-

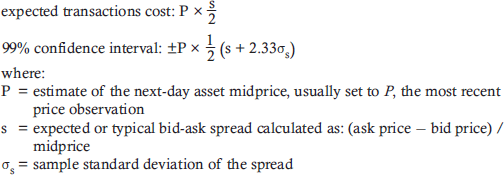

Expected transactions cost and confidence interval: Assuming that daily changes in the bid-ask spread are normally distributed, the expected transactions cost (known as the half-spread) and the 99% confidence interval on the transactions cost in dollars are computed as:

-

-

component is called as 99% spread risk factor.

-

Example: Brieton, Inc., recently traded at an ask price of $100 and a bid price of $99. The sample standard deviation of the spread is 0.0002. Calculate the expected transactions cost and the 99% spread risk factor for a transaction.

-

Answer: Midprice = (100+99)/2=99.5; s=(100-99)/99.5=0.01005

-

Expected transactions cost = 99.50*0.01005/2=$0.5

-

Spread risk factor = 1/2[0.01005+2.33(0.0002)]=0.005258

-

1 / 2\left(s+2.33 \sigma_s\right)

Topic 3. Adjusting VaR for Position Liquidity

-

Liquidity-adjusted value at risk (LVaR): Measures the risk of adverse price impact.

-

Traders liquidate a position over a period of days to ensure an orderly liquidation.

-

Adjusting VaR for liquidity requires an estimate of the number of days it will take to liquidate a position. The number of trading days is typically denoted T.

-

Assuming the position can be divided into equal parts across T days and liquidated at the end of each trading day, a trader would face a:

-

1-day holding period on the entire position,

-

2-day holding period on a fraction (T − 1)/T of the position,

-

3-day holding period on a fraction (T − 2)/T of the position, and so on.

-

-

The 1-day position VaR adjusted by the square root of time is estimated as:

-

-

-

This formula overstates VaR for positions that are liquidated over time because it assumes that the whole position is held for T days.

-

To adjust for the fact that the position could be liquidated over a period of days, the following formula can be used:

-

-

-

VaR_t \times \sqrt{T}

VaR_t \times \sqrt{\frac{(1+T)(1+2T)}{6T}}

Topic 3. Adjusting VaR for Position Liquidity

-

Example: If the position can be liquidated in four trading days (T = 4), the adjustment to the overnight VaR of the position is 1.3693, which means we should increase VaR by 37%.

-

This is greater than the initial 1-day VaR, but less than the 1-day VaR adjusted by the square root of T

Topic 4. Measuring Market Liquidity

-

Market liquidity is measured using tightness, depth, and resiliency.

-

Tightness (width): Cost of a round-trip transaction, measured by the

bid-ask spread and brokers’ commissions. The narrower the spread, the tighter it is. The tighter it is, the greater the liquidity.

-

Depth: This relates to the size of a position that a market can absorb without a significant price impact. Compared to an individual investor, an institution is more likely to have an adverse impact on the market with a transaction.

-

Resiliency: This describes how quickly prices return to their long-run equilibrium after a random, uninformative shock.

-

-

Both depth and resiliency affect how quickly a market participant can execute a transaction.

Topic 5. Funding Liquidity Risk Management

-

Redemption requests may require hedge fund managers to unwind positions rapidly, exposing the fund to transactions liquidity risk.

-

Fire sales may happen if this happens to many funds at once. Hedge funds manage liquidity via:

-

Cash: Cash can be held in money market accounts or Treasury bills. However, cash also has some risk because money market funds may suspend redemptions in times of stress or crisis, and broker balances are at risk if the broker fails.

-

Unpledged assets: Unpledged assets, also called assets in the box, are assets not currently being used as collateral. They are often held with a broker. Only Treasury bills can be used as collateral during a crisis. Unpledged assets can be sold, rather than pledged, to generate liquidity.

-

Unused borrowing capacity: This liquidity source is limited, as counterparties can revoke unused borrowing capacity by increasing haircuts or refusing collateral at rollover. These loans are very short term and credit can disappear quickly (as it did during the GFC).

-

-

During the GFC crisis, hedge funds that had not experienced large losses still faced a liquidity crisis as investors issued redemption requests.

-

Off-Balance Sheet Vehicles: Structured investment vehicles (SIVs) and asset-backed commercial paper (ABCP) conduits provided both liquidity and maturity transformation. They created ABCP with shorter terms and greater liquidity than the assets they held. Despite being off-balance sheet, which allowed firms to hold less capital, these vehicles still contributed to the fragility and leverage issues of the financial system during the subprime crisis.

-

Money Market Mutual Funds (MMMFs): Like banks, MMMFs are obligated to repay investors on demand. Their liabilities are more liquid than their investments. They are also subject to runs. If a large number of investors try to redeem shares during adverse market conditions, the fund may be forced to sell assets at a loss, potentially causing the Net Asset Value (NAV) to fall below $1.00, which is known as "breaking the buck".

Copy of LTR 2. Liquidity and Leverage

By Prateek Yadav