Book 4. Liquidity and Treasury Risk

FRM Part 2

LTR 4. The Investment Function in Financial Services Management

Presented by: Sudhanshu

Module 1. Money Market and Capital Market Instruments

Module 2. Investment Security Selection and Risks

Module 3. Investment Maturity Strategies and Maturity Management Tools

Module 1. Money Market and Capital Market Instruments

Topic 1. Money Market and Capital Market Investments

Topic 2. Money Market Investments

Topic 3. Capital Market Investments

Topic 4. More Recently Developed Investment Instruments

Topic 1. Money Market and Capital Market Investments

-

Investment securities help in income stabilization, hedging, diversification, liquidity, tax benefits.

-

Investments can also be referred to as the crossroads account because they stand in between borrowing and lending.

-

Securities can be classified based on maturity as:

-

Money market instruments: Maturity less than or equal to 1 year, low risk and low yield.

-

Capital market instruments: Maturity greater than to 1 year, high risk and high yield

-

Topic 1. Money Market Investments

-

Money Market Investments:

-

Treasury Bills (T-bills): Zero-coupon securities that are issued at discount by U.S. federal government through weekly and monthly auctions. T-bills mature at par with ≤ 1 year of maturity. T-bills have low risk and low yield. T-bills can be used as collateral and their primary advantage is safety, liquidity, and use as collateral.

-

Treasury notes (T-notes) and Treasury bonds (T-bonds): Coupon-bearing securities issued by the U.S. federal government. T-notes at issuance have maturities ≤ 10 years and T-bonds have maturities > 10 years. The primary advantages of T-notes and T-bonds are safety, secondary market liquidity and use as collateral. However, their returns are typically more than T-bills and they also offer capital gains.

-

Federal agency securities: Issued by agencies that are owned or sponsored by the U.S. federal government. They include the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), the Farm Credit System, and the Federal Land Banks. Interest income on these securities is typically fully taxable.

-

Certificates of deposit (CDs): Issued by banks for fixed terms. CDs have low risk and low initial investment (as low as $500) and they offer a higher yield than T-bills. They also benefit from federal insurance up to $250,000. Consumer-oriented CDs are typically issued in smaller denominations of $500 to $100,000, while business-oriented CDs are issued with denominations over $100,000.

-

Topic 1. Money Market Investments

-

Money Market Investments:

-

International Eurocurrency deposits: Uninsured time deposits with a maturity of 30, 60, or 90 days. They are issued by large banks but the market is concentrated in London. They are low-risk and offer better yield than time deposits. Their disadvantage include interest rate volatility and taxability in income.

-

Bankers’ acceptances: Short-term investments used in trade credit (also called trade finance) transactions. Here, a bank guarantees the payment of a customer for an export/import transaction. The bank receives a fee for the guarantee and becomes the primary obligor for the transaction. Bankers’ acceptances are issued at a discount and mature at par value. They have an active secondary market. They offer higher yields than T-bills but lower than Eurocurrency deposits. Their disadvantages are lack of availability for certain maturities and taxability in income.

-

Commercial paper: Issued by large corporations for short-term maturities—typically ≤ 90-days in the U.S. They are issued at a discount and mature at par value. Their income is taxable. They are attractive to money market funds, and both small and large firms (mainly in Europe and Japan).

-

Short-term municipal obligations: Two common types include tax-anticipation notes (TANs) and revenue-anticipation notes (RANs). Interest earned is exempt from U.S. federal income tax.

-

Practice Questions: Q1

Q1. Which of the following characteristics is not an advantage of Treasury bills?

A. They have stable market prices.

B. They can serve as collateral for borrowers.

C. They have higher yields than agency securities.

D. They are backed by the taxing power of the federal government.

Practice Questions: Q1 Answer

Explanation: C is correct.

Treasury bills are very liquid short-term instruments backed by the taxing power of the federal government. They are liquid with stable prices and can be used as collateral for borrowing. They are considered safer investments than agency securities, and therefore have lower yields.

Practice Questions: Q2

Q2. Which of the following instruments is most common in trade finance transactions?

A. Commercial paper.

B. Bankers’ acceptances.

C. Tax-anticipation notes.

D. Certificates of deposit.

Practice Questions: Q2 Answer

Explanation: B is correct.

Bankers’ acceptances are short-term investments in which a financial firm like a bank guarantees the payment of a customer for an export/import transaction. These transactions are primarily used in trade credit (also called trade finance) deals.

Topic 3. Capital Market Investments

-

Capital Market Investments:

-

T-notes and T-bonds: Coupon-bearing securities issued by the U.S. federal government. T-notes have maturities up to 10 years and T-bonds have maturities over 10 years. Their advantages include safety, secondary market liquidity, and use as collateral. The main disadvantages are price risk from higher volatility and liquidity risk for less liquid secondary trading.

-

Municipal notes and bonds: Issued by state and local governments. Interest is exempt from U.S. federal income taxes. They are less liquid and are subject to capital gains taxes. Investors can purchase these instruments through bidding or from investment dealers. There are two main types of municipal bonds:

-

General obligation (GO) bonds: Backed by the full faith of the issuing government and paid from general revenues, such as taxes.

-

Revenue bonds: Issued to finance revenue-generating projects, with repayment coming from the project's revenues (eg. tolls from a toll road).

-

- Corporate notes and bonds: These are debt securities issued by corporations. Corporate notes have maturity ≤ 5 years, while corporate bonds have maturity > 5 years. Varieties of these securities include debentures and debt secured by mortgages. Insurance companies and pension funds find them appealing for their higher yields compared to government-issued debt. This higher yield implies higher risk, and yields tend to widen during economic downturns.

-

Topic 4. Recently Developed Investment Instruments

-

Over the last few decades, new investment securities have been created, including structured notes, securitized assets, and stripped securities.

-

Structured notes: Created by dealers from federal agency security pools with yields resetting based on reference rates, featuring optional cap rate and floor rate. Coupons can adjust when rates change, or there can be a step-up provision based for additional coupon yield. These notes are complex with a high loss potential

-

Stripped securities: These are hybrid investments created when dealers "strip" a bond's cash flows into separate principal-only (PO) and interest-only (IO) securities.

- They are zero-coupon securities issued at a discount and maturing at par. They are used by investors to hedge against interest rate changes.

- Common stripped securities include U.S. Treasury notes and bonds and mortgage-backed securities.

- IOs are less sensitive to changes in interest rates than regular bonds, whereas POs are more sensitive.

-

Securitized assets: Created from uniform loan pools (mortgages, credit cards, govt insured home loans) with higher yields, strong liquidity, and potential government/private guarantees. Their popularity declined after 2007-2009 crisis exposed structural weaknesses

-

Pass-through securities: Issuing entity pools mortgages with trustee, passing principal and interest payments directly to investors, with potential payment guarantees from federal agencies like Fannie Mae and Ginnie Mae for a fee.

-

Collateralized mortgage obligations (CMOs): Developed by Freddie Mac, CMOs are pass-through securities that are divided into segments called tranches, each with a different level of risk and coupon rate. CMOs can be created either from securitizing mortgage loans or pass-through securities.

-

Real estate mortgage conduits (REMICs): Segment mortgage cash flows into multiple maturity classes to reduce uncertainty, with primary risk being early mortgage prepayment by borrowers.

-

Mortgage-backed bonds (MBBs): Created from a pool of unerlying mortgages. Unlike pass-throughs and CMOs, the underlying mortgages for MBBs remain on the issuer's balance sheet, though they are segregated from other assets. A trustee ensures adequate tracking of loans and verifies that loan values exceed bond values.

-

Topic 4. Recently Developed Investment Instruments

Module 2. Investment Security Selection And Risks

Topic 1. Investment Security Selection

Topic 2. Expected Rate of Return

Topic 3. Tax Exposure

Topic 4. Interest Rate Risk

Topic 5. Credit Risk

Topic 6. Business Risk

Topic 7. Liquidity Risk

Topic 8. Call Risk

Topic 9. Prepayment Risk

Topic 10. Inflation Risk

Topic 11. Pledging Requirements

Topic 1. Investment Security Selection

-

Investment securities account for roughly 20% of total bank assets, though the share varies by bank size. Smaller banks generally hold a higher proportion of investments than larger banks.

-

Bank investments are concentrated in a limited set of security types. U.S. government and agency-guaranteed debt, especially MBS, dominate holdings and make up over half of total bank investments.

-

Other key holdings include state and local government debt and non-government asset-backed securities.

-

Private sector securities (corporate bonds, commercial paper, equities) form a relatively smaller share.

-

Banks hold investment securities mainly for resale to fund investments, support lending, or meet customer withdrawals, and therefore typically classify them as trading securities.

-

Small banks offset high-risk loans by holding low-risk government securities. Large banks with higher risk tolerance, invest more in riskier assets such as foreign securities, private debt and equity to achieve higher yields.

-

A bank's choice for investment security depends on its expected rate of return, tax exposure, interest rate risk, credit risk, business risk, liquidity risk, call risk, prepayment risk, inflation risk, and pledging requirements.

Topic 2. Expected Rate of Return

-

Yield to maturity (YTM):

-

YTM is the best measure of expected return for most investment securities, except equities.

-

YTM factors in principal and interest payments, and any capital gains or losses.

-

The YTM of a security should be compared to other investment securities to determine investment opportunities.

-

-

Holding period yield (HPY):

-

For securities sold before maturity or those without a maturity date, the HPY is a more suitable measure.

-

The HPY calculates the return that equates the purchase price with the expected cash flows until the security is sold.

-

Topic 3. Tax Exposure

-

For tax exempt institutions like credit unions and mutual funds, before-tax returns are more important.

-

Banks often focus on the after-tax returns of investments rather than before-tax returns due to their high tax exposure.

-

Banks in the highest tax brackets often favor tax-exempt state and municipal bonds and notes.

-

Taxable vs. tax-exempt bonds: As municipal bonds are tax exempt, their returns are compared on an after-tax basis. Banks can also use the tax-equivalent yield (TEY) to compare investments on a before-tax gross basis.

-

Example: A bank with a 35% marginal tax rate is considering a corporate bond with a 6% YTM or a municipal bond with a 4.4% YTM.

-

Corporate bond after-tax YTM: 6%×(1−0.35)=3.9%

-

Municipal bond after-tax YTM: 4.4%×(1−0)=4.4% (since it's tax-exempt)

-

Conclusion: The municipal bond is more attractive due to its higher after-tax yield.

-

-

Tax-Equivalent Yield (TEY): For the municipal bond, the TEY would be 4.4%/(1−0.35)=6.8%.

-

Topic 3. Tax Exposure

-

Tax reforms and bank-qualified bonds: Since the Tax Reform Act of 1986, banks have significantly decreased their holdings of municipal debt given:

-

(1) lower tax advantages, (2) lower corporate tax rates, and (3) a decline in available tax-exempt bonds.

-

Bank-qualified bonds: These bonds qualify for a tax advantage, where a bank can deduct 80% of the interest incurred to fund the bond purchase. These bond must be issued by smaller municipalities issuing ≤ $10 M annually in public securities.

-

The highest corporate tax bracket has declined from 46% prior to the tax reform to 35% for mid/larger corporations and 34% for the rest.

-

After-tax return on municipal bonds by calculating the additional return generated by the tax advantage:

-

net after-tax return = (nominal after-tax municipal bond return) - (interest expense incurred to buy the bond) + (tax advantage)

-

tax advantage = (marginal bank tax rate) × (ratio of interest expense that qualifies for a tax deduction) x (interest expense incurred to fund the bond purchase)

-

-

Example: Suppose that a bank purchases a municipal bond with a 6% gross nominal rate of return. The bank’s borrowing cost to purchase the bond is 5%, and the bank is in the top income tax bracket of 35%. The bond is a bank-qualified bond, and 80% of the interest expense is tax deductible. Calculate the net after-tax return on the bond.

- Net after-tax return = 6% − 5%+(0.35 × 0.80 × 5%) = 2.4%

-

Topic 3. Tax Exposure

-

Tax-Swapping: Allows lender to to sell lower-yielding investment securities at a loss to reduce current taxable income, and simultaneously purchase new higher-yielding securities to generate higher future income.

-

It is used by lending institutions during periods of high loan revenues.

-

The strategy is most attractive for institutions in the highest tax brackets with strong loan revenues.

-

Its use is limited by factors such as the availability and utilization of tax-exempt income.

-

-

Portfolio shifting: Allows banks to sell securities at a loss to offset high loan income and reduce tax liability.

-

Institutions may also replace older, low-yield securities with new, higher-yield securities.

-

This strategy can lead to short-term losses, but may produce long-term gains.

-

Practice Questions: Q1

Q1. A bank recently purchased a municipal bond with a 5.5% nominal rate of return. To finance the purchase, the bank borrowed funds at a cost of 4.7%. The bank’s marginal income tax rate is 34%.

The bond is a bank-qualified bond, and 80% of the interest expense is tax deductible. The net after-tax return on the bond is closest to:

A. 0.80%.

B. 2.08%.

C. 2.40%.

D. 4.56%.

Practice Questions: Q1 Answer

Explanation: B is correct.

The after-tax return on municipal bonds can be calculated as:

\begin{aligned}\text{Net After-Tax Return }&= \text{(Nominal After-Tax Municipal Bond Return) - (Interest }\\

&\text{Expense Incurred to Buy the Bond) + (Tax Advantage)}\\

\text{Tax Advantage}& =\text{ (Marginal Bank Tax Rate) }\times \text{(Ratio of Interest Expense that}\\

& \text{qualifies for a Tax Deduction) }\times \text{(Interest Expense incurred}\\

&\text{to fund the Bond Purchase)}\\

\text{Net After-Tax Return }&=(5.5 \%-4.7 \%)+(0.34 \times 0.80 \times 4.7 \%)=2.08 \% \end{aligned}

Practice Questions: Q2

Q2. An investment firm that is prohibited from holding speculative grade securities would have to sell a security when its rating changes from:

A. AAA to AA.

B. BBB to BB.

C. BB to B.

D. B to CCC.

Practice Questions: Q2 Answer

Explanation: B is correct.

Investment firms like pension funds may be prohibited from holding speculative (noninvestment grade) securities. These securities are rated BB or below (Ba on a Moody’s scale). Firms can only hold securities rated BBB or above (Baa on a Moody’s scale).

The choices BB to B and B to CCC are incorrect because the investment firm would be prohibited from holding securities that are rated BB or B, so even if these securities’ ratings deteriorate further, they are ineligible investments. If a security’s rating drops from AAA to AA, it is still eligible for investment by the firm.

Topic 4. Interest Rate Risk

-

Interest rate risk refers to changes in investment or portfolio value and returns due to interest rate movements.

-

Institutions commonly hedge interest rate risk using derivatives such as interest rate swaps.

-

Changes in interest rates affect both portfolio values and demand for loanable funds.

-

Rising interest rates increase borrowing demand from institutions.

-

Falling interest rates increase borrowing demand from consumers.

Topic 5. Credit Risk

-

Credit risk is the risk that an entity will be unable to make scheduled principal or interest payments or may default on its obligations.

-

Credit rating agencies assign credit ratings to measure the relative credit quality of entities.

-

Institutional investors, such as pension funds, are often restricted to holding only investment grade securities, which have a credit rating of BBB, Baa or higher.

-

If a security's rating drops below this threshold (eg. to BB- or Ba), institutions can no longer hold it.

-

Rating agencies use modifiers within letter grades, such as + / − or 1, 2, and 3, where + or 1 denotes the higher end of a rating category.

-

The 2007–2009 financial crisis revealed widespread defaults among investment-grade entities, exposing rating agencies to significant legal and reputational risks.

-

Lending institutions manage default risk mainly using credit derivatives, such as credit swaps and credit options, to protect investment yields.

-

Credit options provide a payoff to the buyer if the bond issuer defaults.

Topic 6. Business Risk

-

Definition: The risk associated with general economic downturns or specific challenges within the issuer's industry (e.g., auto manufacturing, energy).

-

Mitigation: Firms often protect against business risk through geographical diversification of their portfolio.

-

For example, a firm serving the western U.S.market may include bonds issued by entities located outside the western market.

-

Topic 7. Liquidity Risk

- Liquidity risk is the risk that a security cannot be sold quickly and at a reasonable price, which could lead to potential losses.

- The depth and breadth of a security's resale market are crucial factors in a bank's purchase decision.

- There is often a trade-off between liquidity and yield.

- For instance, T-bills, T-bonds, and T-notes have superior liquidity but offer the lowest yields, which can lower a portfolio's overall return.

Topic 8. Call Risk

-

Definition: The risk that a bond issuer will redeem a bond before its scheduled maturity date (calling the bond).

-

When it Occurs: Issuers call bonds when market interest rates fall, allowing them to reissue debt at a lower cost.

-

Investor Impact: The investor (the bank) loses a high-yielding investment and must reinvest the principal at a lower, prevailing market interest rate. This is an adverse form of reinvestment risk.

-

Mitigation Strategy: Investors can mitigate this risk by avoiding callable bonds or by purchasing callable bonds with longer call protection (deferment) periods.

Topic 9. Prepayment Risk

-

Definition: The risk that the investors will not receive all of the expected cash flows on investments.

-

Cash flows from MBSs come from principal and interest payments. When interest rates fall, borrowers refinance mortgage loans, forcing investors to reinvest at lower yields.

-

Borrower defaults can further reduce or disrupt expected cash flows.

-

The speed at which mortgages or loans are prepaid depends on the yield curve shape, economic conditions, age of loans, and seasonal factors.

-

Public Securities Association (PSA) prepayment model: Investment officers aim to predict prepayments using models such as the PSA model.

-

The model assumes mortgage prepayments start at 0.2% in month 1, increase by 0.2% per month for the first 30 months, and then level off at 6%.

-

A mortgage portfolio with 100% PSA is assumed to follow this exact prepayment pattern.

-

- Although prepayments during falling interest rates are typically unfavorable due to reinvestment at lower rates, they can be beneficial if early cash flows are redeployed into more profitable opportunities.

Topic 10. Inflation Risk

-

Definition: The risk that inflation will erode the purchasing power of the income and principal received from an investment.

-

TIPS: Treasury Inflation-Protected Securities (TIPS) are bonds whose principal value is adjusted based on changes in the Consumer Price Index (CPI), directly protecting the investor from unexpected inflation.

- TIPS are issued by the U.S. Treasury Department and they exist in maturities of 5, 10, and 30 years.

Topic 11. Pledging Risk

-

Mandate: Depository institutions in the U.S. cannot accept federal, state, or local governments' deposits without posting acceptable collateral.

-

Eligible Securities: Acceptable collateral must be of sufficiently high credit quality, typically limited to Federal and Municipal Securities.

-

Usage in repos: Pledging securities for collateral is also used to secure borrowing via repurchase agreements (repos).

Module 3. Investment Maturity Strategies and Maturity Management Tools

Topic 1. Investment Maturity Strategies

Topic 2. Maturity Management using Yield Curve

Topic 3. Maturity Management using Duration

Topic 1. Investment Maturity Strategies

-

Institutions look at duration (long-term vs short-term) and distribution of investment maturities.

-

A key factor in this decision is expectations of future interest rate levels

-

Three Primary Strategies: Banks generally adopt one of three strategies: the Laddered Strategy, the Front-Loaded (or Short-Term) Strategy, or the Back-Loaded (or Long-Term) Strategy.

-

Laddered (Spaced-Maturity) Strategy: The strategy allocates equal investments across each maturity bucket up to a chosen maximum maturity.

-

For example, with a five-year maximum maturity, 20% is invested in each of the 1–5 year maturities.

-

While it does not maximize returns, the approach is simple and widely used by smaller institutions.

-

As securities mature, they release cash that can be reinvested in new opportunities.

-

-

Front-End Load Maturity Approach: Investment firms may allocate excess funds (which are not needed for loans or reserves) to short-term investments.

-

For example, a firm can invest 100% of its available funds in securities with maturities of two years or less

-

This strategy provides high liquidity.

-

-

Back-End Load Maturity Approach: Investment firms may allocate excess funds to long-term investments.

- For example, a firm can invest 100% of its available funds in securities with maturities in the 7-years to to-years range

-

This strategy may require significant borrowing to meet short-term

liquidity requirements.

-

Barbell Strategy: A combination of the front-end and back-end load strategies and is favored by smaller institutions.

-

Institutions allocate most funds to short- and long-maturity portfolios, with limited exposure to intermediate maturities.

-

The short-term portfolio generates liquidity, while the long-term portfolio produces higher returns.

-

Topic 1. Investment Maturity Strategies

-

Rate Expectations Approach: Investment decisions depend heavily on interest rate and economic forecasts, making this approach more suitable for larger institutions with advanced forecasting capabilities.

-

Since bond prices move inversely to interest rates, expected rate increases prompt a shift toward shorter maturities, while expected rate declines encourage longer maturities.

-

Adjusting portfolio maturities requires significant trading, potentially generating taxable gains or losses.

-

Managers typically trade when tax efficiency improves returns, higher yields can be locked in, asset quality is enhanced, and returns are not compromised.

-

Topic 1. Investment Maturity Strategies

Practice Questions: Q1

Q1. Which of the following investment maturity strategies would most likely reduce income fluctuation in the medium and long term, while generating sufficient ongoing liquidity for potential investment opportunities?

A. Ladder.

B. Barbell.

C. Back-end load.

D. Front-end load.

Practice Questions: Q1 Answer

Explanation: A is correct.

The ladder strategy involves investing an equal portion of securities in each maturity segment up until the maximum maturity desired. As investments in each interval mature, they free up cash which can then be used to take advantage of potential investment opportunities.

The other strategies either don’t provide ongoing liquidity or do not reduce income fluctuation in the medium or long term.

Topic 2. Maturity Management using Yield Curve

-

The two primary maturity management tools are the yield curve and duration.

-

Yield-Curve: We will discuss following aspects related to a yield curve: interest rate forecasts, risk-return trade-offs, carry trade and riding the yield curve.

-

Interest rate forecasts: The yield curve shows yields of securities at a point in time, differing only by maturity.

-

An upward-sloping curve indicates higher yields for longer maturities.

-

A downward-sloping curve implies lower yields for longer maturities, while a flat curve indicates equal yields across maturities.

-

Investment officers use the yield curve to predict future interest rate movements.

-

A downward-sloping curve signals expectations of falling short-term rates, making long-term investments attractive for capital gains.

-

The yield curve also serves as a trading signal:

-

Yield below the curve → overpriced → sell signal

-

Yield above the curve → underpriced → buy signal

-

-

Topic 2. Maturity Management using Yield Curve

-

Risk-Return Trade-Offs: The yield curve reflects a trade-off between higher returns and higher risk.

-

Investors can earn higher yields by extending maturity, especially under an upward-sloping yield curve.

-

Example: moving from a 3-year bond (3%) to a 7-year bond (3.8%) adds 80 bps of yield.

-

This higher return comes with greater risk, including increased sensitivity to interest rate rises and potential capital losses.

-

-

Carry Trade: A carry trade involves borrowing at low short-term rates to invest in higher-yielding long-term securities.

-

If the investment return (after taxes and fees) exceeds the borrowing cost, the investor earns a positive carry return.

-

-

Riding the Yield Curve: A steeply upward-sloping yield curve can cause bond prices to rise as maturity approaches.

-

Investors can sell bonds before maturity to realize gains and reinvest in longer-term securities.

-

This approach, known as riding the yield curve, generates positive returns as long as the yield curve shape remains unchanged.

-

-

Limitations of Yield Curve: Yield curve strategies have limitations such as:

-

Changes in the shape, slope, or steepness of the yield curve can negatively impact portfolio values.

-

The yield curve provides no insight about timing or size of future cash flows.

-

-

Duration: Duration represents the present value–weighted maturity of a security or portfolio.

-

It can also be interpreted as the average time to receive all expected cash flows.

-

Duration addresses the limitations of yield curve by measuring an investment’s interest rate sensitivity.

-

-

-

Portfolio Immunization: Protects portfolio returns from interest rate movements by matching the portfolio duration with the investment horizon.

-

It balances price risk and reinvestment risk: Rising rates lower prices but increase reinvestment returns; falling rates raise prices but reduce reinvestment returns.

-

By offsetting these effects, immunization stabilizes total portfolio returns against interest rate changes.

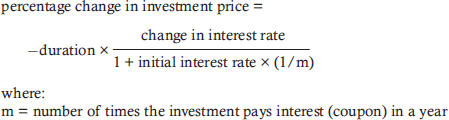

Topic 3. Maturity Management using Duration

LTR 4. The Investment Function in Financial-Services Management

By Prateek Yadav