Book 4. Liquidity and Treasury Risk

FRM Part 2

LTR 7. Monitoring Liquidity

Presented by: Sudhanshu

Module 1. Cash Flow Types and Liquidity Options

Module 2. Liquidity Risks, Cash Flows and Capacity

Module 3. Managing Assets for Liquidity

Module 1. Cash Flow Types and Liquidity Options

Topic 1. Deterministic and Stochastic Cash Flows

Topic 2. Liquidity Options

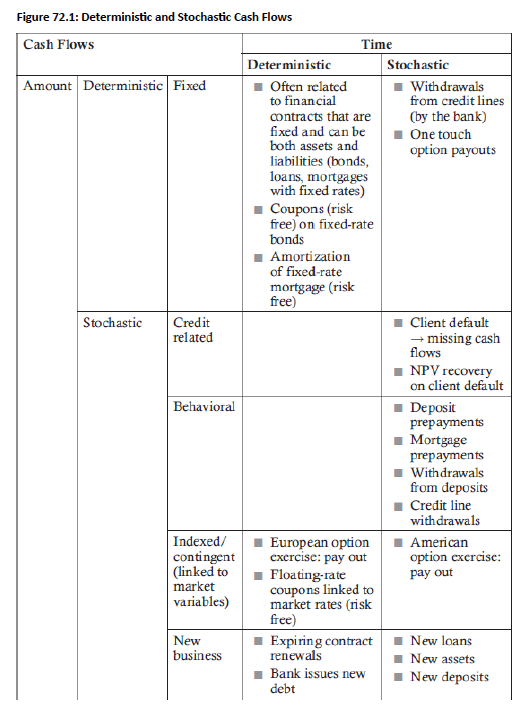

Topic 1. Deterministic and Stochastic Cash Flows

-

Cash flows characterized by two dimensions: time and amount.

-

Time dimension:

-

Deterministic: occur at known times.

-

Stochastic: occur randomly.

-

-

Amount dimension:

-

Deterministic (fixed): amounts known in advance.

-

Stochastic (unknown): fall into four categories:

-

Credit-related: uncertainty from credit events.

-

Behavioral: driven by counterparties’/clients’ decisions.

-

Indexed/contingent: depend on market variables.

-

New business: from new contracts.

-

-

Topic 1. Deterministic and Stochastic Cash Flows

Practice Questions: Q1

Q1. Each of the following cash fows is stochastic in timing and amount except:

A. new debt issued by a bank.

B. a bank’s recovery on a client default.

C. the payout on an American-style call option.

D. mortgage prepayments due to interest rate declines.

Practice Questions: Q1 Answer

Explanation: A is correct.

Cash flows at a point in time can be identified based on two dimensions: time and amount. Cash flows that occur randomly and have unknown amounts are

stochastic across both dimensions. A new bond issuance is time deterministic and amount stochastic. Each of the other choices (recovery on client default, American option payouts, and mortgage prepayments) are all time and amount stochastic.

Topic 2. Liquidity Options

- Definition: A liquidity option is the right held by a party to either give cash to or receive cash from a bank at specific times and terms. The exercise of this option is often driven by a need for a surplus of liquidity.

-

Standard financial options are exercised when profitable, with post-exercise cash flows typically positive and independent of the exercise decision. Liquidity options are exercised based on post-exercise cash flows, which may not align with financial profitability.

-

Examples of Liquidity Options: Banks are often on the selling side of liquidity options, meaning they must provide cash to the option holder if the option is exercised.

-

Customer Credit Lines: A customer with a line of credit has the right to withdraw funds whenever they want. This can be particularly beneficial for the customer if their credit spread widens and borrowing new funds would be more expensive.

-

Savings Account Withdrawals: A customer's ability to withdraw funds from their savings account with little to no notice is another example of a liquidity option offered by a bank.

-

Mortgage Prepayments: When interest rates decline, a customer may choose to prepay their mortgage. While this provides the bank with early liquidity, it's often at the cost of having to replace the asset with a new one at a lower, less advantageous rate.

-

-

Liquidity option exercise affects a bank in two ways:

-

Balance sheet impact: based on amount repaid or withdrawn.

-

Financial impact: gain or loss from differences in contract rates, spreads, and market values at exercise.

-

-

Hedging requires cash reserves, liquid assets, or credit line access.

Practice Questions: Q2

Q2. Which of the following statements comparing liquidity to financial options is most accurate?

A. Financial options typically produce negative cash fows.

B. Financial options align the cash fow decision with profitability.

C. Both options are typically only exercised when they are in the money.

D. Liquidity options may or may not be financially profitable upon exercise.

Practice Questions: Q2 Answer

Explanation: D is correct.

The decision to exercise a liquidity option is based on a need for liquidity, as opposed to financial options that are exercised when they are profitable (in the money). This implies that liquidity options may or may not be profitable upon exercise. Financial options typically produce positive cash flows after exercise, although that is not the intent of exercise. For financial options, the cash flow

decision is independent of the profitability situation.

Module 2. Liquidity Risks, Cash Flows and Capacity

Topic 1. Term Structure of Cash Flows

Topic 2. TSECF and TSECCF

Topic 3. TSCCF and TSECCF Example

Topic 4. Key Elements to Consider

Topic 5. Liquidity Risks & Funding Cost Risk

Topic 6. Liquidity Generation Capacity (LGC)

Topic 7. TSLGC and TSCLGC

Topic 8. Term Structure of Expected Liquidity

Topic 9. cfaR, TSCF and TSLaR

Topic 1. Term Structure of Cash Flows

-

Banks must monitor expected future net cash flows to manage quantitative liquidity risk.

-

Liquidity risk arises from existing and forecasted contracts in normal business activities.

-

Sources of liquidity generate positive cash flows to manage and hedge liquidity risk.

-

Cumulative expected cash flows include both inflows and outflows from a given point in time.

-

For a series of contracts/securities , expected positive and negative cash flows (expected at time from reference time ) are derived using the following formulas:

-

-

At reference time , cumulative cash flows from date to time are calculated as:

-

C F\left(t_0, t_a, t_b\right)=\sum_{i=a}^b\left(c f_e^{+}\left(t_0, t_i\right)+c f_e^{-}\left(t_0, t_i\right)\right)

(d_1, d_2, \ldots)

t_1

t_0

\begin{aligned}

& \mathrm{cf}_{\mathrm{e}}^{+}\left(\mathrm{t}_0, \mathrm{t}_1\right)=\mathrm{E}\left[\sum_{j=1}^{\mathrm{N}} \mathrm{cf}^{+}\left(\mathrm{t}_0, \mathrm{t}_1 ; \mathrm{d}_j\right)\right] \\

& \mathrm{cf}_{\mathrm{e}}^{-}\left(\mathrm{t}_0, \mathrm{t}_1\right)=\mathrm{E}\left[\sum_{j=1}^{\mathrm{N}} \mathrm{cf}^{-}\left(\mathrm{t}_0, \mathrm{t}_1 ; \mathrm{d}_j\right)\right]

\end{aligned}

t_0

t_b

t_a

Topic 2. TSECF and TSECCF

-

Term Structure of Expected Cash Flows (TSECF): The TSECF, or "maturity ladder," is a collection of a bank's expected positive and negative expected cash flows, organized by date, up until the expiration of the contract with the longest maturity

-

-

Term Structure of Expected Cumulated cash Flows (TSECCF): TSECCF is the collection of cumulative expected cash flows in date order:

-

-

Banks use TSECCF to monitor both daily cash flow balance and cumulative cash position over time.

-

While net cash flows may be negative on specific dates, positive balances from prior inflows can offset these deficits.

-

The critical metric is the bank's total cumulative cash available at any given time.

(t_b)

\operatorname{TSECF}\left(t_0, t_b\right)= \left\{c f_e^{+}\left(t_0, t_0\right), c f_e^{-}\left(t_0, t_0\right), c f_e^{+}\left(t_0, t_1\right), c f_e^{-}\left(t_0, t_1\right), \ldots, c f_e^{+}\left(t_0, t_b\right), c f_e^{-}\left(t_0, t_b\right)\right\}

\operatorname{TSECCF}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)=\left\{\operatorname{CF}\left(\mathrm{t}_0, \mathrm{t}_0, \mathrm{t}_1\right), \operatorname{CF}\left(\mathrm{t}_0, \mathrm{t}_0, \mathrm{t}_2\right), \ldots, \operatorname{CF}\left(\mathrm{t}_0, \mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)\right\}

Topic 3. TSCCF and TSECCF Example

-

To calculate TSECF and TSECCF for a bank, start with a balance sheet of assets, liabilities, and equity. Assuming no deposit liquidity options and no asset default risk, expiring assets generate positive cash flows while expiring liabilities create negative outflows. Order items by expiration date and include interest payments from both assets and liabilities.

-

The TSECCF each period is the cumulative balance of cash flows from the expiration of the assets and liabilities themselves, as well as the associated interest impact.

-

Example (TSECCF): At the start of Year 1, King Bank’s balance sheet reflects the following balances:

-

Assets: $125 million

-

Liability: $75 million

-

Equity: $50 million

-

At the end of Year 1, assets expire that are worth $25 million. At the end of Year 2, liabilities expire that are worth $15 million. Assuming assets earn an interest rate of 6.00% and liabilities bear an interest rate of 5.00%, calculate TSECCF for Years 1 and 2.

-

TSECCF (Year 1): $25 million (the expiring asset) +$7.5 million (6.00% interest earned on $125 million) - $3.75 million (5.00% interest paid on $75 million) = $28.75 million

-

TSECCF (Year 2): $28.75 million (from Year 1) + $6.0 million (6.00% interest earned on $100 million) - $15 million (the expiring liability) - $3.75 million (5.00% interest paid on $75 million)=$16.00 million

-

Topic 4. Key Elements to Consider

-

Key elements of the model to consider include the following:

-

Cash flows are often stochastic due to their linkage to market indices.

-

Credit models need to consider default risk and correlations that inevitably exist between bank counterparties.

-

Behavioral models can be used to adjust cash flows for liquidity options.

-

New business cash flows should also be considered, as well as rollovers of maturing liabilities and new bond issuances to fund asset increases.

-

-

Treasury monitors TSECF (Treasury Single Expected Cash Flow) and TSECCF (Treasury Single Expected Cumulative Cash Flow).

-

TSECCF should remain positive, meaning positive inflows cover outflows.

-

Both metrics capture expected (not actual) cash flows.

-

Timing mismatches in asset/liability maturities can cause temporary negative cash flows.

-

Negative TSECCF may signal potential insolvency or bankruptcy, making it critical to maintain positivity.

Practice Questions: Q1

Q2. Which of the following statements is least accurate regarding TSECF and TSECCF calculations and the models used to estimate them?

A. Rollovers of maturing liabilities should be included.

B. Behavioral components are often adjusted for liquidity options.

C. Default risk and correlations between bank counterparties need to be captured.

D. Only deterministic cash flows are counted, with stochastic cash flows captured in other models.

Practice Questions: Q1 Answer

Explanation: D is correct.

Stochastic cash flows are regularly captured in TSECF and TSECCF models, as a significant percentage of expected cash flows are stochastic. Rollovers of maturing liabilities, behavioral components adjusted for liquidity options, and default risk and correlations are also regularly captured in these models.

Topic 5. Liquidity Risks & Funding Cost Risk

-

Risk & Uncertainty: Risk is tied to future uncertainty (positive or negative), but risk management focuses on adverse outcomes.

-

Quantitative Liquidity Risk: Occurs when future cash inflows are lower than expected, creating challenges in meeting obligations. It covers both market liquidity risk and funding cost risk.

-

Market Liquidity Risk: Assets cannot be sold quickly at fair prices, leading to reduced cash inflows.

-

Funding Cost Risk: Banks may need to borrow at higher-than-expected costs over the risk-free rate to access liquidity.

-

-

Pre-2007 Context: Low spreads and minimal default concerns made liability rollover low risk.

-

Post-2007 Crisis: Spreads widened, volatility rose, funding declined, and intervention became necessary.

-

Liquidity Risk (Overall): Economic losses occur when actual vs. expected cash flows and funding availability diverge. It includes both the quantitative and cost dimentions.

-

Quantitative Dimension: Inability to secure funds, forcing asset sales at below fair value.

-

Cost Dimension: Ability to raise funds, but at higher-than-expected costs (e.g., high interest rates).

-

- Opportunity Cost: Excess liquidity may only be invested at lower-than-expected returns.

Practice Questions: Q1

Q1. If a bank manager is concerned about a high cost of liquidity risk, she is most likely concerned about:

A. selling assets quickly at fair market prices.

B. receiving lower than expected cash infows in the future.

C. generating positive cash fows from its sources of liquidity.

D. a high interest rate for borrowing relative to the risk-free rate.

Practice Questions: Q1 Answer

Explanation: D is correct.

Funding cost risk (the cost of liquidity risk) is the risk that when a bank needs to access sources of liquidity, there will be a wide spread between the interest rate paid and the risk-free rate. The ability to sell assets quickly at fair market prices is market liquidity risk. Receiving lower than expected cash inflows in the future is overall quantitative liquidity risk. Generating positive cash flows from liquidity sources is the liquidity generation capacity (LGC).

Topic 6. Liquidity Generation Capacity (LGC)

-

Liquidity Generation Capacity (LGC): Measures a bank’s ability to generate positive cash flows beyond contractual inflows; key for managing negative expected cash flow positions.

-

Sources of LGC:

-

Balance sheet expansion - via new bond issuance, credit line withdrawals, or increased deposits; influenced by external parties (clients, institutions). External factors (clients, institutional counterparties) play a significant role in balance sheet expansion. Liquidity other than balance sheet liquidity comes from balance sheet expansion.

-

Balance sheet shrinkage – via asset sales (liquid or less liquid securities); not influenced by external parties. External factors do not play a role in balance sheet shrinkage or balance sheet neutral transactions such as repo transactions. Balance sheet liquidity (BSL) comes from existing assets on the balance sheet and is directly linked to balance sheet shrinkage

-

-

LGC Types:

-

Security-linked (BSL): Secured debt issuance, secured credit line withdrawals, asset sales, repo sales.

-

Security-unlinked: Unsecured bond issuance, new client deposits, unsecured credit line withdrawals.

-

-

Three Primary Liquidity Sources: asset sales (AS), secured funding via repos/collateralized borrowing (RP) and unsecured funding via credit lines & interbank deposits (USF)

-

Balance Sheet Impact: AS and RP transactions will reduce the balance sheet, or at best keep it constant. USF transactions expand the balance sheet.

Topic 7. TSLGC and TSCLGC

-

TSLGC: TSLGC is the collection of liquidity at a given time that can be generated by sources of liquidity up to a terminal time

-

-

-

TSCLGC: The term structure of cumulated LGC, known as TSCLGC, is the cumulative liquidity that can be generated by sources of liquidity up to a terminal time

-

-

-

-

The TSLGC sources of liquidity come from either the banking or trading books.

-

Banking Book Sources:

-

AFS bonds and eligible assets → can be repoed or sold.

-

Repos = collateralized loans (sell asset, buy back later); easier than unsecured funding. For repos and collateralized loans, banks need to consider the size of the haircut.

-

Haircuts = reduction in collateral value; depend on bond volatility & issuer default risk.

-

- Committed credit lines → counted, but become liabilities once drawn.

-

Unsecured funding via interbank deposits also provides liquidity.

-

-

Trading Book Sources: Bonds, stocks, and other unencumbered assets available as liquidity.

t_b

\operatorname{TSLGC}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)=\left\{\operatorname{AS}\left(\mathrm{t}_0, \mathrm{t}_1\right), \operatorname{RP}\left(\mathrm{t}_0, \mathrm{t}_1\right), \operatorname{USF}\left(\mathrm{t}_0, \mathrm{t}_1\right), \ldots, \operatorname{AS}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right), \operatorname{RP}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right), \operatorname{USF}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)\right\}

t_b

\operatorname{TSCLGC}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)=\left\{\sum_{i=0}^1 \operatorname{TSLGC}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{i}}\right), \sum_{i=0}^2 \operatorname{TSLGC}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{i}}\right), \ldots \sum_{\mathrm{i}=0}^{\mathrm{b}} \operatorname{TSLGC}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{i}}\right)\right\}

-

Term Structure of Expected Liquidity (TSLe): This measures a bank's ability to cover negative cumulative cash flows at a future point in time. To be solvent, a bank must maintain a positive TSL.

-

The TSL will include all possible expected cash flows from ordinary business activity, from new business, and from the policies and measures undertaken to manage negative cumulated cash flows.

-

The TSL is a combination of the TSECCF and TSCLGC.

-

-

-

Example (Term Structure of LGC): Given the TSECF and TSCLGC amounts for Years 1–5 for Leland Bank. Assuming 0 for each measure in Year 0, calculate the TSECCF and TSL for Years 1–5.

-

TSECCF = cumulative TSECF amounts

-

TSL = TSECCF + TSCLGC

-

Year 1: TSECCF= 3.9; TSL = 3.9+0=3.9

-

Year 2: TSECCF= 9.7; TSL = 9.7+2.0=11.7

-

Year 3: TSECCF= 27.9: TSL = 27.9+2.0=29.9

-

Year 4: TSECCF= 21.0: TSL = 21.0+4.8=25.8

-

Year 5: TSECCF= 23.5: TSL = 23.5+4.8=28.3

-

TSL_e\left(t_0, t_b\right)=\left\{T S E C C F\left(t_0, t_0\right), \operatorname{TSECCF}\left(t_0, t_1\right)+\right.TSCLGC\left(t_0, t_1\right), \ldots, \left. \operatorname{TSECCF}\left(t_0, t_b\right)+\operatorname{TSCLGC}\left(t_0, t_b\right)\right\}\\

Topic 8. Term Structure of Expected Liquidity

(TSL_e)

\begin{array}{|c|c|c|}

\hline \text { Years } & \text { TSECF } & \text { TSCLGC } \\

\hline 1 & 3.9 & 0 \\

2 & 5.8 & 2.0 \\

3 & 18.2 & 2.0 \\

4 & -6.9 & 4.8 \\

5 & 2.5 & 4.8 \\

\hline

\end{array}

-

Cash Flow at Risk (cfaR): Since most cash flows are stochastic, modeling should take into account both expected values and volatility associated with those values.

-

Extreme values for both positive and negative cash flows are measured.

-

Positive cash flow at risk:

-

Negative cash flow at risk:

-

-

Here, x reflects the risk factors such as credit, behavioral, and market variables.

-

The term structure of unexpected cash flows for positive and negative amounts:

-

The formulas represent upper and lower bounds for the TSCFs, with an expected value equal to TSECF.

-

Redefining the term structure of liquidity (TSL) with maximum and minimum cash flows at confidence levels α and 1 − α, respectively:

-

-

Term Structure of Liquidity-at-Risk (TSLaR): TSLaR is the collection of unexpected cash flows at each date for a given period, representing the difference between the avg and minimum levels of cash flows.

-

cfaR_{\alpha}^+(t_0,t_i)=cf_{\alpha}^+(t_0,t_i;x)-cf_e(t_0,t_i;x)

cfaR_{1-\alpha}^-(t_0,t_i)=cf_{1-\alpha}^-(t_0,t_i;x)-cf_e(t_0,t_i;x)

Topic 9. cfaR, TSCF and TSLaR

\begin{aligned}

& \operatorname{TSCF}_\alpha^{+}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)=\left\{\mathrm{cfaR}_\alpha^{+}\left(\mathrm{t}_0, \mathrm{t}_0\right), \mathrm{cfaR}_\alpha^{+}\left(\mathrm{t}_0, \mathrm{t}_1\right), \ldots, \mathrm{cfaR}_\alpha^{+}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)\right\} \\

& \operatorname{TSCF}_{1-\alpha}^{-}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)=\left\{\mathrm{cfaR}_{1-\alpha}^{-}\left(\mathrm{t}_0, \mathrm{t}_0\right), \mathrm{cfaR}_{1-\alpha}^{-}\left(\mathrm{t}_0, \mathrm{t}_1\right), \ldots, \mathrm{cfaR}_{1-\alpha}^{-}\left(\mathrm{t}_0, \mathrm{t}_{\mathrm{b}}\right)\right\}

\end{aligned}

\begin{aligned}

& \operatorname{TSL}_\alpha\left(t_0, t_b\right)=\left\{\mathrm{cf}_\alpha\left(t_0, t_1\right), \ldots, \mathrm{cf}_\alpha\left(t_0, t_b\right)\right\} \\

& \operatorname{TSL}_{1-\alpha}\left(t_0, t_b\right)=\left\{\mathrm{cf}_{1-\alpha}\left(t_0, t_1\right), \ldots, \mathrm{cf}_{1-\alpha}\left(t_0, t_b\right)\right\}

\end{aligned}

\operatorname{TSLaR}_{1-\alpha}\left(t_0, t_b\right)=\left\{\begin{array}{l}

\operatorname{cf}_{1-\alpha}\left(t_0, t_1\right)-\operatorname{TSECCF}\left(t_0, t_1\right)-\operatorname{TSCLGC}\left(t_0, t_1\right), \ldots, \\

\operatorname{cf}_{1-\alpha}\left(t_0, t_b\right)-\operatorname{TSECCF}\left(t_0, t_b\right)-\operatorname{TSCLGC}\left(t_0, t_b\right)

\end{array}\right\}

Module 3. Managing Assets For Liquidity

Topic 1. Term Structure of Available Assets (TSAA): Overview

Topic 2. Transactions that Increase TSAA

Topic 3. Transactions that Decrease TSAA

Topic 4. TSAA Mathematical Expression

Topic 5. Impact of Different Transactions on TSAA, TSECF/TSECCF and TSCLGC

Topic 1. Term Structure of Available Assets (TSAA): Overview

-

Term Structure of Available Assets (TSAA): TSAA is used by banks to monitor their LGC. It shows the extent to which an asset can be used to create liquidity.

-

When a bank purchases a bond, the cash position reflects an outflow for the purchase and subsequent inflows for interest and the principal paid back at maturity.

-

Since these cash flows relate to a contract, they are included in both the TSECF and TSECCF calculations after accounting for default probabilities.

-

TSAA is also impacted by other types of purchases (which increase the TSAA) and asset expirations (which decrease the TSAA).

-

Repo transactions and sales impact asset availability and the TSAA calculation.

-

- Note: Possession, rather than ownership, drives availability for liquidity purposes.

Topic 2. Transactions that Increase TSAA

-

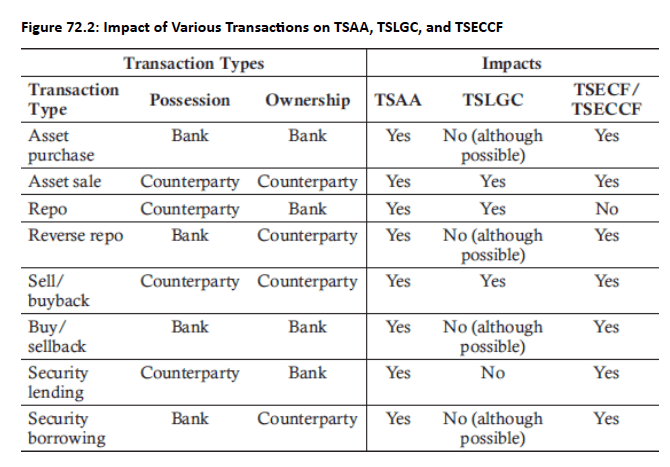

Reverse repo transactions: The bank pays cash equal to the asset price less the haircut in exchange for receiving the asset. The counterparty owns the asset (implying that asset payments are not included in TSECF and TSECCF calculations), but the bank has possession and can therefore use it as collateral for other transactions. The TSAA increases by the repo’s notional amount, while TSLGC is not impacted (unless the asset is repoed).

-

Buy/sellback transactions: Cash and assets are exchanged, but unlike with reverse repos ownership and possession of the asset both pass to the bank at the start of the contract. Asset payments before the sellback go to the bank, which means that they, along with purchase and sale cash fllows, are included in TSECF and TSECCF calculations. The TSAA increases by the notional amount of the agreement, while the TSLGC amount is not impacted (unless the asset is repoed).

-

Security borrowing: While similar to the buy/sellback, possession passes to the

bank and no cash is paid by the bank to the counterparty. The counterparty

receives payments for the asset. The only impact to TSECF and TSECCF is the

interest payment made by the bank at the expiration of the contract. The TSAA

increases by the notional amount of the borrowing, as the bank can use the

borrowed security as collateral. The TSLGC is not impacted, although the asset can produce liquidity.

Topic 3. Transactions that Decrease TSAA

-

Repo transactions: The bank receives cash equal to the asset price less the haircut in exchange for delivering the asset to the counterparty.While the bank owns the assets, the counterparty has possession, which means they are not available for the bank’s liquidity purposes. Asset payments during the life of the repo belong to the bank, which means TSECF and TSECCF are not impacted by those payments. The TSAA declines by the notional amount of the repo, while the TSLGC is impacted by both the cash received at the start and the negative cash flow at the end.

-

Sell/buyback transactions: Cash and assets are exchanged, but unlike with repo transactions, ownership and possession passes to the counterparty at the start of the contract. Asset payments prior to the buyback belong to the counterparty, which results in the removal of cash flows from the TSECF and TSECCF calculations. The TSAA decreases by the notional amount of the agreement, while the TSLGC is impacted in a similar fashion to repo transactions.

-

Security lending: While similar to the sell/buyback, only possession passes to the counterparty; no cash is paid by the counterparty to the bank. The bank receives fee payments for the asset along with interest from the counterparty at contract expiration, which positively impacts TSECF and TSECCF. The TSAA decreases by the notional amount of the lending arrangement, while the TSLGC is not impacted as the asset cannot generate liquidity until the end of the contract.

Topic 4. TSAA Mathematical Expression

-

For assets such as stocks that don’t have expiration dates, the only contract cash flows that impact TSECF and TSECCF are the initial outflow for the purchase and the inflows for dividends received.

-

For a single asset , where is the asset quantity in the bank’s possession, the TSAA is expressed as:

-

For a set of M securities held by the bank, the total TSAA for all assets is equal to:

-

Figure 72.2 summarizes the impacts that the transaction types have on the various liquidity measures

A_1

A(t_i)

\operatorname{TSAA}^{A_1}\left(t_0, t_b\right)=\left\{A_1^P\left(t_0\right), A_1^P\left(t_1\right), \ldots, A_1^P\left(t_b\right)\right\}

\operatorname{TSAA}\left(t_0, t_b\right)=\left\{\sum_{m=1}^M A_m^P\left(t_0\right), \sum_{m=1}^M A_m^P\left(t_1\right), \ldots, \sum_{m=1}^M A_m^P\left(t_b\right)\right\}

Topic 5. Impact of Different Transactions on TSAA, TSECF/TSECCF and TSCLGC

- Bond Purchase: Creates cash outflow (purchase price) and increases TSAA (maturity value). Coupon payments increase TSECF/TSECCF. At maturity, TSAA drops to zero with final coupon and principal inflows. Partial sales reduce TSAA, lower future cash flows, and increase TSCLGC.

- Repo Transactions: Reduce TSAA by notional amount, increase TSCLGC by repo price minus haircut. At repo end, TSAA returns to previous level and TSCLGC returns to zero.

- Reverse Repos: Increase TSAA by notional amount with cash outflow (bond price minus haircut) reducing TSECF/TSECCF. At contract end, interest earned creates positive cash inflow.

- Buy/Sellback: Purchase creates cash outflow, increases TSAA, decreases TSECF/TSECCF. Sellback reduces TSAA but increases TSECF/TSECCF.

- Sell/Buyback: Sale decreases TSAA, increases TSCLGC. Buyback increases TSAA, decreases TSCLGC.

- Asset Lending: Reduces TSAA when lent, increases when returned. Only cash impact is positive fee received at contract end.

- Asset Borrowing: Only cash impact is negative interest payment at contract end affecting TSECF/TSECCF.

Practice Questions: Q1

Q1. Gerard Bank enters into a reverse repo transaction for six months. Which of the following

statements is most accurate regarding the impact of the transaction?

A. TSLGC will not be impacted.

B. Both TSAA and TSECCF are impacted.

C. TSECF is impacted, but TSECCF will not be impacted.

D. Possession and ownership of the asset belong to the counterparty.

Practice Questions: Q1 Answer

Explanation: B is correct.

For a reverse repo transaction, both TSAA and TSECCF (and TSECF) are impacted. TSLGC may or may not be impacted. Ownership belongs to the counterparty, but possession is with the bank.

Copy of LTR 7. Monitoring Liquidity

By Prateek Yadav