Book 1. Market Risk

FRM Part 2

MR 18. Fundamental Review of the Trading Book

Presented by: Sudhanshu

Module 1. Fundamental Review of the Trading Book

Module 1. Fundamental Review of the Trading Book

Topic 1. Fundamental Review of the Trading Book

Topic 2. FRTB: From VaR to Expected Shortfall

Topic 3. Market Risk Capital Calculation: Example

Topic 4. Liquidity Horizons under FRTB

Topic 5. Allocation of Risk Factors to Liquidity Horizons

Topic 6. FRTB Liquidity Horizon Methodology

Topic 7. Internal Models Approach (IMA)

Topic 8. Proposed Modifications to Basel Regulations: Trading Book Vs Banking Book

Topic 9. Proposed Modifications to Basel Regulations: Backtesting and Profit/Loss Attribution

Topic 10. Proposed Modifications to Basel Regulations: Credit Risk and Securitizations

Topic 1. Fundamental Review of the Trading Book

-

Timeline & Development

- May 2012: Basel Committee initiated next round of market risk capital changes, process known as Fundamental Review of the Trading Book (FRTB).

- December 2014: Rules refined after public comments and formal study results

- Critical: Risk managers must understand proposed changes and new methodology

-

Previous Requirements: Basel I

- Metric: 10-day VaR at 99% confidence level

- Advantage: Very current result using recent 1-4 year time period

-

Previous Requirements: Basel II.5

- Addition: Stressed VaR measure added to standard 10-day VaR

- Stressed VaR: Captures market variable behavior during 250-day stressed period

- Bank requirement: Self-select 250-day historical window that would stress current portfolio

-

VaR Limitation

- Question answered: "How bad can things get?" with confidence threshold

- Example flaw: 99% VaR of $25M ignores potential $700M catastrophic loss in the 1% tail

- Weakness: Only provides loss threshold, not magnitude of extreme losses

-

Expected Shortfall (ES) Advantage

- Question answered: "If things get bad, what is the estimated loss?"

- Captures: Actual P&L impact for shocks of varying severity beyond the confidence threshold

- FRTB proposal: Replace 10-day 99% VaR with ES to better measure bank's true risk exposure

Topic 2. FRTB: From VaR to Expected Shortfall

-

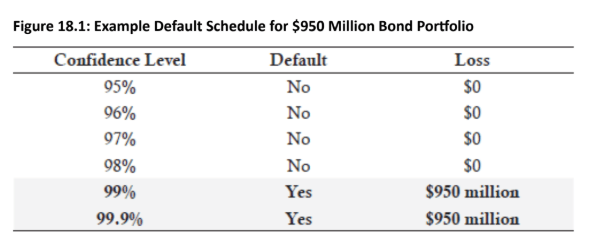

Consider the following example where a bank has a $950 million bond portfolio with a 2% probability of default. The default schedule appears in Figure 18.1.

-

VaR and ES calculations at 95% confidence level

- 95% VaR: Shows $0 ES

- 95% ES: Accounts for conditional losses beyond VaR threshold

- Calculation: 40% of tail scenarios result in total $950M loss → ES = $380M (40% × $950M)

- Insight: Reveals materially different risk perspective than VaR alone

-

FRTB Proposal

- Shift: From 10-day 99% VaR to 97.5% ES

- Normal distribution: Both measures approximately equivalent (99% VaR = μ + 2.326σ; 97.5% ES = μ + 2.338σ)

- Fat-tailed distributions: ES can differ considerably from VaR, capturing extreme tail risk more effectively

Topic 3. Market Risk Capital Calculation: Example

Practice Questions: Q1

Q1. Which of the following statements regarding the differences between Basel I, Basel II.5, and the Fundamental Review of the Trading Book (FRTB) for market risk capital calculations is incorrect?

A. Both Basel I and Basel II.5 require calculation of VaR with a 99% confidence level.

B. FRTB requires the calculation of expected shortfall with a 97.5% confidence level.

C. FRTB requires adding a stressed VaR measure to complement the expected shortfall calculation.

D. The 10-day time horizon for market risk capital proposed under Basel I incorporates a recent period of time, which typically ranges from one to four years.

Practice Questions: Q1 Answer

Explanation: C is correct.

Basel I and Basel II.5 use VaR with a 99% confidence level and the FRTB uses the expected shortfall with a 97.5% confidence level. Basel I market risk capital requirements produced a very current result because the 10-day horizon incorporated a recent period of time. The FRTB does not require adding a stressed VaR to the expected shortfall calculation. It was Basel II.5 that required the addition of a stressed VaR.

Practice Questions: Q2

Q2. What is the difference between using a 95% value at risk (VaR) and a 95% expected shortfall (ES) for a bond portfolio with $825 million in assets and a probability of default of 3%?

A. Both measures will show the same result.

B. The VaR shows a loss of $495 million while the expected shortfall shows no loss.

C. The VaR shows no loss while the expected shortfall shows a $495 million loss.

D. The VaR shows no loss while the expected shortfall shows a $395 million loss.

Practice Questions: Q2 Answer

Explanation: C is correct.

The VaR measure would show a $0 loss because the probability of default is less than 5%. Having a 3% probability means that three out of five times, in the tail, the portfolio will experience a total loss. The potential loss is $495 million (= 3/5× $825 million).

Topic 4. Liquidity Horizons under FRTB

-

Definition & Rationale

- Liquidity Horizon: Time required to exit exposure to a risk factor without moving hedging instrument prices in stressed conditions

- Change: Standard 10-day LH insufficient due to actual liquidity variations across instruments

-

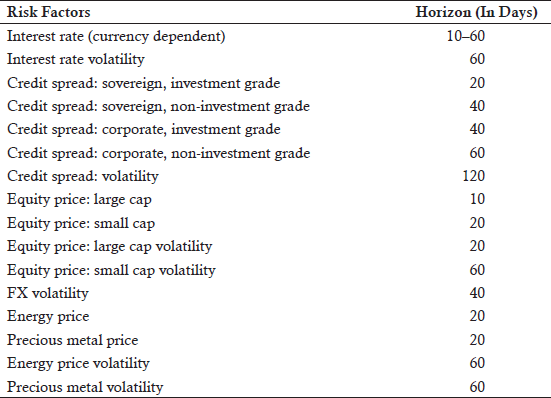

Five-Tier Framework

- Horizons: 10, 20, 40, 60, and 120 days

- Purpose: Regulatory capital protects banks during required time to recover from price volatility

- Example: 60-day horizon = three months of trading days

-

Risk Factor Assignment

- Investment grade sovereign spreads: 20-day horizon

- Non-investment grade corporate spreads: 60-day horizon

- Application: Each risk factor assigned specific LH for capital calculations

Topic 5. Allocation of Risk Factors to Liquidity Horizons

Topic 6. FRTB Liquidity Horizon Methodology

-

Original Proposal: Overlapping Periods

- Concept: Scale smaller time periods to longer periods using multiple trials

- Example: 10-day large-cap equity vs. 60-day non-investment grade spread

- Trial process: Day 0-10 and Day 0-60 (Trial 1); Day 1-11 and Day 1-61 (Trial 2); continues through Day 249-259 and Day 249-309

- ES calculation: Average loss in lower 2.5% tail across 250 trials

-

Revised Approach, December 2014:

- It is also known as Internal Models Approach (IMA)

- Five categories: 10, 20, 40, 60, and 120-day horizons

- Rationale: Reduce implementation costs while maintaining risk sensitivity

- Key advantage: Accounts for potential lack of correlation in risk factor shocks across different liquidity horizons

-

Nested Pairing Scheme (Waterfall): The 10-day ES is measured through five successive shocks in a nested pairing scheme (ES1 through ES5).

-

ES1: 10-day shock in all categories (1–5) with intense volatility

-

ES2: 10-day shock in categories 2-5 only, holding categories 1 constant

-

ES3: 10-day shock in categories 3-5 only, holding categories 1–2 constant

-

ES4: 10-day shock in categories 4-5 only, holding categories 1–3 constant

-

ES5: 10-day shock in category 5 only, holding categories 1–4 constant

-

-

Liquidity-Adjusted ES Formula: The overall ES is scaled to the square root of the difference in the horizon lengths of the nested risk factors, yielding the liquidity-adjusted ES formula:

-

-

Simplified example: With only Categories 1 and 2, assumes 10-day behavior of all risk factors is independent from future 10-day behavior of Category 2 factors

-

E S=\sqrt{E S_1^2+\sum_{j=2}^5\left(E S_j \sqrt{\frac{L H_j-L H_{j-1}}{10}}\right)^2}

Topic 7. Internal Models Approach (IMA)

E S=\sqrt{ES_1^2+ES_2^2}

Practice Questions: Q3

Q3. Which of the following statements best describe how the internal models-based approach (IMA) incorporates various liquidity horizons into the expected shortfall calculation?

A. A rolling 10-day approach is used over a 250-day window of time.

B. Smaller time periods are used to extrapolate into larger time periods.

C. A series of weights are applied to the various liquidity horizons along with a correlation factor determined by the Basel Committee.

D. The expected shortfall is based on a waterfall of the liquidity horizon categories and is then scaled to the square root of the difference in the horizon lengths of the nested risk factors.

Practice Questions: Q3 Answer

Explanation: D is correct.

The expected shortfall is based on a waterfall of the liquidity horizon categories and is then scaled to the square root of the difference in the horizon lengths of the nested risk factors.

Topic 8. Proposed Modifications to Basel Regulations: Trading Book Vs Banking Book

-

Historical Distinction & Arbitrage Issue

- Trading book: Assets intended for trading, marked-to-market, subject to market risk capital rules

- Banking book: Hold-to-maturity assets at cost, subject to stricter credit risk capital rules

- Problem: Banks exploited different rules by placing credit-dependent assets in trading book to reduce capital requirements

-

New Trading Book Criteria

- Dual requirements: (1) Ability to trade the asset AND (2) physically manage associated risks on trading desk

- Additional condition: Day-to-day price fluctuations must affect bank's equity and pose solvency risk

- Purpose: Prove actual trading activity, not just intent

-

Reclassification Restrictions

- General rule: Once assigned, assets cannot be reclassified except under extraordinary circumstances

- Extraordinary examples: Firm-wide accounting practice changes

- Capital requirement protection: Any benefit from post-reclassification category is disallowed; original method's capital requirement must be retained

- Goal: Prevent opportunistic category switching based on capital calculation advantages

Practice Questions: Q4

Q4. Which of the following statements represents a criteria for classifying an asset into the trading book?

I. The bank must be able to physically trade the asset.

II. The risk of the asset must be managed by the bank’s trading desk.

A. I only.

B. II only.

C. Both I and II.

D. Neither I nor II.

Practice Questions: Q4 Answer

Explanation: C is correct.

The criteria for classification as a trading book asset are (1) the bank must be able to physically trade the asset, and (2) the bank must manage the associated risks on the trading desk.

-

Backtesting: Stressed ES measures are not backtested under FRTB due to the difficulty of backtesting extreme values that may not recur frequently. Also, backtesting VaR is easier than backtesting ES.

-

For VaR backtesting, FRTB suggests a one-day horizon and the latest 12 months of data, using either a 99% or 97.5% confidence level.

-

If there are more than 12 exceptions at the 99% level or more than 30 exceptions at the 97.5% level, the standardized approach for capital computation must be used.

-

-

Profit/Loss Attribution: Banks can use two measures to compare actual and model-predicted profit/loss figures:

-

-

- D represents the difference between the actual and model profit/loss on a given day, and A represents the actual profit/loss on a given day.

-

Measure 1 should be within ±10%, and Measure 2 should be less than 20%.

-

If these measures are outside the requirements on four or more occasions within a 12-month period, the standardized approach for capital computation must be used.

-

Topic 9. Proposed Modifications to Basel Regulations: Backtesting and Profit/Loss Attribution

\text{Measure 1}=\frac{\text { mean of } \mathrm{D}}{\text { standard deviation of } \mathrm{A}};\text{ and }

\text{Measure 2}=\frac{\text { variance of } D}{\text { variance of } A}

-

Credit Risk: Basel II.5 introduced the incremental risk charge (IRC) which recognizes credit spread risk and jump-to-default risk for credit-dependent assets

-

Credit Spread Risk: The risk of a credit risk asset's credit spread changing, affecting its MTM value. This can be addressed by ES calculation. Basel II.5 allowed the assumption of constant risk, where deteriorating positions are replaced with other risk assets.

- FRTB Change: FRTB proposes incremental marking to market without assuming replacement.

-

Jump-to-Default Risk: The risk of immediate and significant loss due to the default of an issuing company. This is subject to an Incremental Default Risk (IDR) charge.

- IDR Calculation: Applies to all default-susceptible risk assets (including equities) and is calculated based on a 99.9% VaR with a one-year time horizon.

-

Credit Spread Risk: The risk of a credit risk asset's credit spread changing, affecting its MTM value. This can be addressed by ES calculation. Basel II.5 allowed the assumption of constant risk, where deteriorating positions are replaced with other risk assets.

-

Securitizations

- Comprehensive Risk Measure (CRM): Introduced in Basel II.5 to address risks from securitized products (e.g., ABSs and CDOs).

- FRTB Change: Under CRM, banks could use their own internal models, leading to significant capital charge variations. Therefore, FRTB recommends using the standardized approach for securitizations.

Topic 10. Proposed Modifications to Basel Regulations: Credit Risk and Securitizations

Practice Questions: Q5

Q5. Which of the following risks is specifically recognized by the incremental risk charge (IRC)?

A. Expected shortfall risk, because it is important to understand the amount of loss potential in the tail.

B. Jump-to-default risk, as measured by 99% VaR, because a default could cause a significant loss for the bank.

C. Equity price risk, because a change in market prices could materially impact mark-to-market accounting for risk.

D. Interest rate risk, as measured by 97.5% expected shortfall, because an increase in interest rates could cause a significant loss for the bank.

Practice Questions: Q5 Answer

Explanation: B is correct.

The two types of risk recognized by the incremental risk charge are (1) credit

spread risk and (2) jump-to-default risk. Jump-to-default risk is measured by 99% VaR and not 97.5% expected shortfall.

Copy of MR 18. Fundamental Review of Trading Book

By Prateek Yadav