Book 3. Operational Risk

FRM Part 2

OR 17. Stress Testing Banks

Presented by: Sudhanshu

Module 1. Stress Testing

Module 2. Challenges in Modeling Losses and Revenues

Module 1. Stress Testing

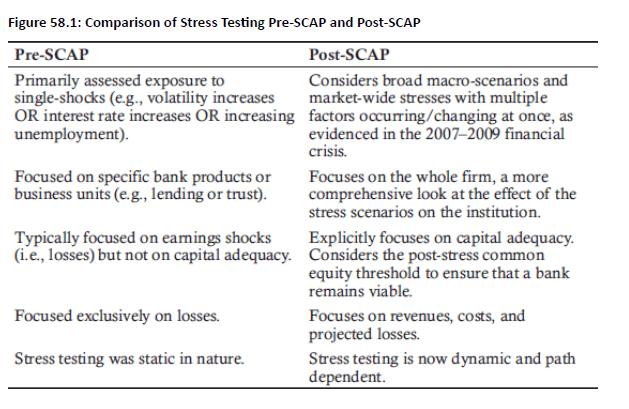

Topic 1. Stress Testing Evolution

Topic 2. Supervisory Capital Assessment Program (SCAP)

Topic 3. Challenges in Designing Stress Tests

Topic 1. Stress Testing Evolution

- Post-Crisis Banking Assessment: Following the 2008 financial crisis, regulators implemented the 2009 Supervisory Capital Assessment Program (SCAP) to assess U.S. banking system capital strength and identify gaps between required and available capital.

- Macro vs. Micro-Prudential Focus: SCAP represented the first macro-prudential stress test post-crisis, focusing on systematic risks and overall banking system soundness rather than individual institution safety.

- Government Capital Backstop: The federal government planned to infuse equity capital into undercapitalized banks through the Treasury's Capital Assistance Program (CAP), with Treasury borrowing funds to downstream as bank equity.

- Investor Dilution Mechanism: Banks unable to convince private investors to fill capital gaps would face dilution through government equity investment, creating incentives for private capital raising.

- Successful Private Capital Raising: The 19 SCAP banks were required to raise $75 billion within six months and successfully raised $77 billion in Tier 1 common equity without needing CAP funds.

Topic 2. Supervisory Capital Assessment Program (SCAP)

-

Launched: 2009 – First macro-prudential U.S. stress test after the crisis.

-

Purpose: Assess capital shortfall and restore market confidence.

-

Outcome:

-

19 banks were required to raise $75 billion; raised $77 billion instead.

-

No need to use government funds via the Capital Assistance Program (CAP).

-

-

Key Feature: Introduced macro-prudential regulation, focusing on systemic risk.

-

Impact:

-

Marked shift from simple pre-crisis testing to robust, systematic evaluation.

-

Triggered evolution to more complex frameworks like CCAR and EBA.

-

Topic 2. Supervisory Capital Assessment Program (SCAP)

Practice Questions: Q1

Q1. Which of the following changes in stress testing was not the result of the 2009 Supervisory Capital Assessment Program (SCAP)?

A. Banks are now required to provide the results of their own scenario stress tests.

B. Stress scenarios are now broader in nature.

C. Stress testing now focuses on the whole firm.

D. Stress testing now focuses on revenues, costs, and projected losses.

Practice Questions: Q1 Answer

Explanation: A is correct.

The 2009 U.S. bank stress test, known as the Supervisory Capital Assessment Program (SCAP), was the first macro-prudential stress test after the 2007–2009 financial crisis.

Topic 3. Challenges in Designing StressTests

- Coherence Challenge: Stress test scenarios must be extreme yet reasonable and possible, requiring careful balance between severity and plausibility to ensure meaningful results.

- Multi-Factor Risk Dependencies: Problems are inherently interconnected (e.g., increased volatility freezing credit markets, high unemployment correlating with falling equity prices), making it insufficient to test single risk factors in isolation.

- Joint Risk Factor Specification: Supervisors must specify coherent joint outcomes across all relevant risk factors rather than treating them as independent variables.

- Balanced Market Dynamics: Not everything deteriorates simultaneously - if some currencies depreciate, others must appreciate; "flight to quality" scenarios require identifying which assets serve as safe havens in the stress environment.

- Safe Haven Evolution: Models must account for scenarios where traditional safe assets (like U.S. Treasury debt) lose their status and identify alternative "risk-free" assets where capital would flee.

- Trading Portfolio Complexity: Marked-to-market portfolios present greater challenges with hundreds of thousands of positions mapped to thousands of risk factors, making coherent outcomes difficult in complex, multi-dimensional universes.

- SCAP Simplicity vs. Coherence: The 2009 SCAP used three simple variables (GDP growth, unemployment, house price index) with historical market risk scenarios, achieving coherence despite not testing novel conditions.

- Evolution to Bank-Specific Scenarios: Post-2011 CCAR moved beyond one-size-fits-all approach, requiring banks to submit their own stress scenarios alongside supervisory scenarios to reveal bank-specific vulnerabilities and improve both micro- and macro-prudential supervision.

Module 2. Challenges in Modeling Losses and Revenues

Topic 1. Modeling Bank Losses, Revenues and Balance Sheet– Key Challenges

Topic 2. Modeling Balance Sheet Over Stress Horizon

Topic 3. Summary – Benefits and Costs of Stress Testing

Topic 4. CCAR Disclosure and International Comparison

Topic 5. Comparison of Macro-Prudential Stress Tests

Topic 6. Stress Test Disclosure: Benefits, Costs and Disclosure

Topic 1. Modeling Bank Losses, Revenues and Balance Sheet – Key Challenges

- Macro-to-Micro Translation: Stress tests struggle to translate broad macro-scenarios (unemployment, GDP, HPI) into specific bank outcomes for different products and geographic areas.

- Geographic Risk Variations: Regional economic differences create dramatically different loss patterns, making uniform stress testing approaches less effective across diverse markets.

- Asset-Specific Risk Responses: Different asset classes respond uniquely to economic stress, with varying default rates and loss given default patterns across product types.

- Industry Cycle Misalignment: Different industries experience recession impacts at varying times, creating collateral liquidity issues when banks hold sector-specific assets during downturns.

- Revenue Modeling Gaps: Revenue modeling over stress horizons remains underdeveloped compared to loss modeling, with limited guidance on stress-period revenue calculations.

- Interest Income Challenges: While yield curves can estimate interest income, the direct impact of changing rates on bank profitability remains unclear and difficult to model.

- Noninterest Income Complexity: Modeling noninterest income (fees, service charges) proves challenging despite its growing importance for U.S. bank profitability.

Practice Questions: Q2

Q2. Piper Hook, a bank examiner, is trying to make sense of stress tests done by one of the banks she examines. The stress tests are multi-factored and complex. The bank is using multiple extreme scenarios to test capital adequacy, making it difficult for Hook to interpret the results. One of the key stress test design challenges that Hook must deal with in her examination of stress tests is:

A. multiplicity.

B. efficiency.

C. coherence.

D. efficacy.

Practice Questions: Q2 Answer

Explanation: C is correct.

One of the challenges of designing useful stress tests is coherence. The sensitivities and scenarios must be extreme but must also be reasonable or possible (i.e., coherent). Problems are inherently multi-factored, making it more difficult to design a coherent stress test. Hook is dealing with the possibly incoherent results of the bank’s stress tests.

Topic 2. Challenges in Modeling the Balance Sheet

- Two-Year Modeling Horizon: Typical stress tests span two years, requiring modeling of both income statement and balance sheet to determine post-stress capital adequacy, with capital generally measured as a ratio of common equity to risk-weighted assets.

- Risk-Weighted Asset Calculations: RWAs are computed using Basel II risk weight definitions, where different asset types receive varying risk weights (e.g., agency securities have lower risk weights than credit card loans).

- Quarter-by-Quarter Progression: Stress models begin with the initial balance sheet to generate first quarter income and loss under stressed scenarios, which then determines the quarter-end balance sheet for subsequent modeling periods.

- Complex Balance Sheet Decisions: Modelers must consider numerous variables including asset sales or originations, capital depletion from acquisitions, capital conservation from spin-offs, dividend payment changes, and share repurchases or issuances.

- Static vs. Dynamic Modeling Challenges: Balance sheet modeling complexities exist under both static and dynamic assumptions, with stress models unable to determine optimal timing for strategic decisions like subsidiary sales or dividend reductions.

- Continuous Capital Ratio Maintenance: Banks must maintain required capital and liquidity ratios during all quarters throughout the stress test horizon, not just at the end point.

- Extended Reserve Requirements: Two-year stress tests effectively become three-year tests, as banks must estimate reserves needed to cover loan and lease losses for the year following the stress horizon (T+1 year requirements for T-year tests).

Topic 3. Stress Test Comparisons

- 2009 SCAP Comprehensive Disclosure: SCAP disclosed projected losses for all 19 participating banks across eight asset classes, plus loss-absorbing resources like pre-provision net revenue and reserve releases, creating unprecedented transparency.

- Market Assessment Capability: High disclosure levels allowed investors and markets to independently verify stress test severity and understand outcomes at individual bank levels, marking a shift from reporting only realized losses to forecasted stress scenario losses.

- 2011 CCAR Limited Disclosure: CCAR required only macro-scenario results publication without bank-level details, forcing market participants to infer pass/fail status through indirect signals like dividend increases.

- 2012 CCAR Return to Transparency: CCAR disclosure returned to 2009 SCAP levels, providing detailed bank-level loss rates and losses by major asset classes for comprehensive market assessment.

-

Six Regulatory Asset Classes: Stress tests evaluate losses across

- First and second lien mortgages,

- Commercial and industrial loans,

- Commercial real estate loans,

- Credit card lending,

- Other consumer loans, and

- Other loans.

- Bank Scenario Submission Requirement: CCAR 2011 and 2012 required banks to submit results from their own baseline and stress scenarios in addition to supervisory stress test results, expanding beyond previous testing frameworks.

- Detailed Trading Portfolio Analysis: Fed reported dollar amounts for pre-provision net revenue, gains/losses on available-for-sale and held-to-maturity securities, plus trading and counterparty losses for the six largest trading portfolio institutions.

- Supervisory vs. Bank Estimates: Trading book stress test results represented supervisory estimates of losses under stress scenarios, not bank-generated estimates, ensuring regulatory consistency.

- European Banking Authority Comprehensive Disclosure: 2011 EBA Irish and Europe-wide stress tests provided extensive detail in electronic, downloadable format, including comparisons of bank versus third-party loss estimates.

- Credibility Recovery Through Transparency: Ireland required detailed disclosure after failing CEBS stress test in July 2010 and needing aid four months later, highlighting the importance of market confidence in stress testing.

- Granular European Data Requirements: EBA disclosure included bank-by-bank, asset-class, country, and maturity bucket breakdowns to enable independent market risk assessment and restore faith in European supervisors.

Topic 4. CCAR Disclosure and International Comparison

| Stress Test | Methodologies | Disclosure | Findings |

|---|---|---|---|

| SCAP (2009). All banks with $100 billion or more in assets as of 2008 year end were included. | Tested simple scenarios with three dimensions, GDP growth, unemployment, and the house price index (HPI). Historical experience was used for the market risk scenario (i.e., the financial crisis-a period of "flight to safety," the failure of Lehman, and higher risk premiums). A "one-size-fits-all" approach. | First to provide bank level projected losses and asset/product level loss rates. | 19 SCAP banks were required to raise $75 billion within six months. The under-capitalized banks actually raised $77 billion of Tier 1 common equity and none of the banks were forced to use the Treasury's Capital Assistance Program funds. |

| CCAR (2011) | In recognition of "one-size-fits-all" stress testing, CCAR asked banks to submit results from their own baseline and stress scenarios. | Only macro-scenario results were published. | |

| CCAR (2012) | Banks were again asked to submit their own baseline and stress test results. | Similar in detail to SCAP 2009-bank level and asset/ product level loss rates disclosed. | |

| EBA Irish (2011) | Similar in design to EBA Europe 2011 | Comparison of bank and third party projected losses; comparison of exposures by asset class and geography. Data is electronic and downloadable. | After passing the 2010 stress tests, 2011 stress tests revealed Irish banks needed €24 billion. Greater disclosure in 2011 resulted in tightening credit spreads on Irish sovereign and individual bank debt. |

| EBA Europe (2011). [formerly the Committee of European Bank Supervisors (CEBS)] 90 European banks were stress tested. | Specified eight macro-factors (GDP growth, inflation, unemployment, commercial and residential real estate price indices, short and long-term government rates, and stock prices) for each of 21 countries. Specified over 70 risk factors for the trading book. It also imposed sovereign haircuts across seven maturity buckets. | Bank level projected losses. Comparisons of exposures by asset class and geography. Data is electronic and downloadable. | Eight banks were required to raise €2.5 billion |

Topic 5. Comparison Of Macro-Prudential Stress Tests

- Transparency During Crisis: Greater disclosure provides crucial transparency, particularly valuable during periods of financial distress when market confidence and clarity are essential.

- Normal Times Cost-Benefit Trade-off: During stable periods, disclosure costs may outweigh benefits as banks may engage in portfolio "window dressing" and make poor long-term investment decisions to pass tests.

- Market Information Distortion: Public stress test disclosure may cause traders to over-rely on disclosed information while reducing incentives to generate private intelligence about financial institutions.

- Price Discovery Impairment: Reduced private information generation harms market price information content, making prices less useful for regulators making policy decisions.

- One-Size-Fits-All Problem: Pre-2011 CCAR supervisory stress tests applied identical scenarios to all banks, failing to capture institution-specific risk profiles and vulnerabilities.

- Bank-Specific Scenario Innovation: 2011 and 2012 CCAR required banks to submit results from their own scenarios alongside supervisory scenarios, attempting to reveal unique institutional vulnerabilities.

Topic 6. Stress Test Disclosure: Benefits, Costs and Evolution

Practice Questions: Q3

Q3. Greg Nugent, a regulator with the Office of the Comptroller of the Currency, is presenting research on stress tests to a group of regulators. He is explaining that macro-variable stress testing can be

misleading for some banks because of geographical differences in macro risk factors. He gives the example of the wide range of unemployment rates across the United States following the 2007–

2009 financial crisis. Which type of loan did Nugent most likely identify as having losses tied to unemployment rates?

A. Residential real estate loans.

B. Credit card loans.

C. Commercial real estate loans.

D. Industrial term loans.

Practice Questions: Q3 Answer

Explanation: B is correct.

Credit card losses are particularly sensitive to unemployment figures. For example, unemployment was 12.9% in Nevada in July 2011, 3.3% in North Dakota, and the national unemployment rate was 9.1%. Credit card loss rates varied dramatically from region to region during this period. Residential mortgages are affected by unemployment as well but people are generally more likely to quit

paying credit card bills before mortgages.

Practice Questions: Q4

Q4. A risk modeler has to make assumptions about acquisitions and spinoffs, if dividend payments will change, and if the bank will buy back stock or issue stock options to employees. These factors make

it especially challenging to:

A. get a CAMELS rating of 2 or better.

B. determine if the bank has enough liquidity to meet its obligations.

C. meet the Tier 1 equity capital to risk-weighted assets ratio.

D. model a bank’s balance sheet over a stress test horizon.

Practice Questions: Q4 Answer

Explanation: D is correct.

In a stress model, the starting balance sheet generates the first quarter’s income and loss from the stressed scenario, which in turn determines the quarter-end balance sheet. At that point, the person modeling the risk must consider if any assets will be sold or originated, if capital is depleted due to other actions such as

acquisitions or conserved as the result of a spin-off, if there are changes made to dividend payments, if shares will be repurchased or issued (e.g., employee stock or stock option programs), and so on. This makes it challenging to model the balance sheet over the stress horizon.

Practice Questions: Q5

Q5. One of the key differences between the 2011 CCAR stress test and the 2011 EBA Irish stress test is that the:

A. CCAR did not require banks to provide results from their own stress scenarios.

B. EBA Irish did not and any banks in violation of capital adequacy requirements.

C. CCAR required disclosure of macro-level, not bank level, scenario results.

D. EBA Irish allowed for 1-year stress horizons.

Practice Questions: Q5 Answer

Explanation: C is correct.

The 2011 CCAR required banks to provide results from their own stress scenarios but the EBA Irish did not. After the 2011 EBA Irish tests, €24 billion was required to increase the capital of several banks. The 2011 CCAR, unlike the SCAP and the 2012 CCAR, only required the disclosure of macro-level scenario results. The EBA Irish did not change the stress horizon from two years to one year.

Copy of OR 17. Stress Testing Banks

By Prateek Yadav