Book 3. Operational Risk

FRM Part 2

OR 24. Basel III: Finalising Post-Crisis Reforms

Presented by: Sudhanshu

Module 1. Basel III: Post-Crisis Reforms

Module 1. Basel III: Post-Crisis Reforms

Topic 1. Standardized Approach

Topic 2. Topic 2. ILDC, SC and FC Calculation

Topic 3. Internal Loss Multiplier

Topic 4. Standardized Approach Capital Requirement

Topic 5. Standardized Approach vs. Earlier Approaches

Topic 6. Identification, Collection and Treatment of Operational Loss Data: General Criteria

Topic 7. Identification, Collection and Treatment of Operational Loss Data: Specific Criteria

Topic 1. Standardized Approach

-

Definition: A combination of three key elements:

- Business Indicator (BI): A financial statement operational risk exposure proxy.

- Business Indicator Component (BIC): Product of a regulatory marginal coefficient and the BI.

- Internal Loss Multiplier (ILM): Reflects operational loss data specific to an individual bank.

-

Business Indicator (BI) Calculation

-

Formula:

-

Calculated as the most recent three-year average for each component.

-

-

Components:

-

ILDC: Interest, Lease, Dividend Component

- SC: Services Component

- FC: Financial Component

-

-

BI=ILDC_{avg}+SC_{avg}+FC_{avg}

-

ILDC Component

- Where: II = interest income, IE = interest expenses, IEA = interest earning assets, DI = dividend income.

-

Services Component (SC):

-

-

Where: OOI = other operating income, OOE = other operating expenses, FI = fee income, FE = fee expenses.

-

-

Financial Component (FC):

-

FC = abs(net P<Bavg)+abs(net P&LBBavg)

-

Where: P&L = profit & loss, TB = trading book, BB = banking book.

-

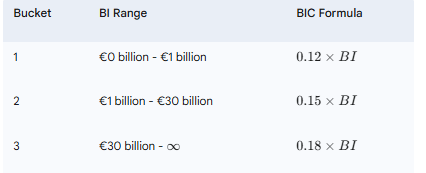

- Banks are divided into three buckets based on their BI size for BIC calculation:

- Example: If BI = €40 billion, BIC = (0.12×1)+[0.15×(30−1)]+[0.18×(40−30)]=€6.27 billion.

SC=max(OOI_{vg}; OOE_{avg})+max(FI_{abg};FE_{avg})

Topic 2. ILDC, SC and FC Calculation

ILDC = min[abs(II_{avg}-IE_{avg});0.0225 \times IEA_{avg}]+DI_{avg}

Practice Questions: Q1

Q1. The business indicator (BI) component in the standardized approach calculation for a bank with a BI of €13 billion will be closest to:

A. €1.43 billion.

B. €1.92 billion.

C. €2.43 billion.

D. €13.00 billion.

Practice Questions: Q1 Answer

Explanation: B is correct.

A bank with a BI of €13 million will fall into bucket 2, which covers a BI range of €1 billion to €30 billion. With the BI component formula of 0.15 × BI for bucket 2 banks, the BI component for this bank will be equal to 0.12 × 1 + 0.15 × (13 – 1) = €1.92 billion.

Practice Questions: Q2

Q2. Which of the following components within the BI calculation takes into account a bank’s trading and banking book P&L results?

A. Loss component.

B. Services component.

C. Financial component.

D. Interest, lease, dividend component.

Practice Questions: Q2 Answer

Explanation: C is correct.

The formula for the financial component of the BI calculation is equal to abs(net P<Bavg) + abs(net P&LBBavg), with TB representing the trading book and BB representing the banking book.

- Purpose: Factors internal losses into the Standardized Approach, making it more risk-sensitive.

-

Formula:

-

- Loss Component: 15× average annual operational risk loss over the last 10 years.

-

Impact:

- If Loss Component = BIC (average exposure), then ILM = 1.

-

If Loss Component > BIC (greater loss experience), then ILM > 1.

-

If Loss Component < BIC (less loss experience), then ILM < 1.

- Data Requirement: Ideally 10 years of quality data. Minimum 5 years during transition. If less than 5 years, only BIC is used.

I L M=\ln \left[e^1-1+\left(\frac{\text { loss component }}{B I C}\right)^{0.8}\right]

Topic 3. Internal Loss Multiplier

-

The standardized approach is used to determine the operational risk capital requirement and is calculated as follows:

- For BI Bucket 1 banks: Operational Risk Capital = BIC

-

For BI Bucket 2 and 3 banks: Operational Risk Capital = BIC×ILM

-

Consolidated Entities: Calculations incorporate fully consolidated BI amounts (netting intragroup income/expenses).

-

At sub-consolidated and subsidiary levels, specific BI amounts are used.

-

If a subsidiary in buckets 2/3 does not meet qualitative standards for loss component, 100% of BIC is used.

-

Topic 4. Standardized Approach Capital Requirement

Topic 5. Standardized Approach vs. Earlier Approaches

-

Before the development of the standardized approach, some banks were using the advanced measurement approach (AMA) to assess operational risk.

-

Advanced Measurement Approaches (AMA):

-

Introduced in Basel II (2006).

-

Allowed internal modeling for regulatory capital estimation.

-

Principles-based framework with significant flexibility.

-

Challenges: Lack of comparability among banks due to diverse modeling practices, overly complex calculations.

-

-

Standardized Approach (SA):

-

Goal: Greater comparability and less complexity.

-

Methodology: Single, non-model-based method.

-

Combines financial statement information with bank-specific internal loss experience.

-

Key Difference: SA is less flexible and aims for greater consistency across banks compared to the highly flexible, model-based AMA.

-

Practice Questions: Q3

Q3. Which of the following statements best describe a difference between the standardized approach and older operational risk capital approaches?

A. The advanced measurement approach (AMA) was introduced as part of the Basel III revisions.

B. The AMA was more flexible in its application than the standardized approach.

C. The standardized approach accounts for internal loss experiences that were not factored into the AMA.

D. The standardized approach uses a model-based methodology, while the AMA was more flexible and principle-based.

Practice Questions: Q3 Answer

Explanation: B is correct.

Because banks were able to use a wide range of models for calculating the AMA, there was more flexibility to these approaches than under the newer standardized approach. The AMA was introduced as part of the Basel II framework in 2006. AMA did account for internal losses. The standardized approach is nonmodel

based, whereas the AMA did incorporate bank-specific models.

Topic 6. Identification, Collection and Treatment of Operational Loss Data: General Criteria

-

Documented Processes and procedures

-

Information Maintenance: For each operational risk event, maintain:

-

Gross loss amounts; Date of occurrence, discovery, and accounting; Gross loss amount recoveries; Drivers of the loss event.

-

- Loss data Accuracy

-

Operational risk losses tied to credit risk-weighted assets are excluded and market risk losses are included.

-

Loss Allocation: Document criteria for allocating losses to specific event types and categorize historical data into Basel II Accord Level 1 supervisory categories.

-

Observation Period: 10 years for internal loss data calculations. Minimum 5 years during transition for new adopters.

-

Comprehensiveness & Thresholds:

-

Internal loss data must be comprehensive, capturing all material exposures across locations/subsystems.

-

Initial gross loss threshold: €20,000. Can increase to €100,000 for Bucket 2 and 3 banks later.

-

-

Policy for Inclusion: Each bank needs a policy defining criteria for including operational risk events/losses in the standardized approach loss data set.

- Identification of Loss Amounts: Specifically identify gross loss amounts, insurance recoveries, and non-insurance recoveries. Standardized approach loss data should include losses net of insurance recoveries.

-

Included in Gross Loss Calculation:

-

External expenses (legal, advisor, vendor fees) directly tied to the event.

-

Settlements, impairments, write-downs, direct charges to income statement.

-

Repair/replacement costs to restore the bank's position.

-

Reserves or provisions tied to potential operational loss impact and booked to income statement.

-

Pending losses (definitive financial impact, in transition/suspense accounts, materiality dictates inclusion).

-

Timing losses from legal risk crossing financial accounting periods.

-

- Excluded from Gross Loss Calculation: Costs of improvements, upgrades, and risk assessment enhancements incurred after the event; Insurance premiums; Costs associated with general maintenance contracts on property, plant, and equipment (PP&E).

-

Date for Loss Data Set: Only the date of accounting can be used. For legal loss events, the date the legal reserve is booked is the latest.

-

Loss Allocation over Time: Losses related to a common operational risk event, or related events over time but posted to accounts over many years, should be allocated to the given year of the loss.

Topic 7. Identification, Collection and Treatment of Operational Loss Data: Specific Criteria

Practice Questions: Q4

Q4. Which of the following items from the profit & loss (P&L) statement should be included in the BI component calculation?

A. Administrative expenses.

B. Insurance premiums paid.

C. Depreciation related to capitalized equipment.

D. Provision reversals related to operational loss events.

Practice Questions: Q4 Answer

Explanation: D is correct.

A provision reversal would normally be excluded except when it relates to operational loss events. Each of the other three choices represents a P&L item that should be excluded from the BI component calculation.

Practice Questions: Q5

Q5. In deriving the standardized approach loss data set for an individual bank, each of the following items will most likely be included in the gross loss calculation except:

A. legal fees of €900,000 associated with an unusual risk event.

B. a €2 million settlement tied to a recent operational risk event.

C. a €1.4 million reserve booked to the income statement to cover a potential operational loss.

D. €1.75 million spent on maintenance contracts tied to the bank’s property, plant, and equipment.

Practice Questions: Q5 Answer

Explanation: D is correct.

The costs associated with maintenance contracts for PP&E are outlined in the specifiic criteria for collecting operational loss data as excluded for the purposes of calculating the gross loss for the SMA loss data set.

Copy of OR 24. Basel III- Finalising Post-Crisis Reforms

By Prateek Yadav