Applied

Microeconomics

Lecture 9

BE 300

Plan for Today

Finish price ceiling/price floor

Sugar imports case

NOTE: Quiz opens at 9:00am tomorrow, closes 8:00am Monday. Open book/open note but no communication with other students.

Plan for Today

Case due Thursday (Sugar Import Quotas)

Review session for perfect competition: Wednesday 5:30-6:30 w/ Professor Feldman, W 2760

Quiz Friday -- Online, open Friday and available over the weekend -- Open book/note, but you can not confer with other classmates.

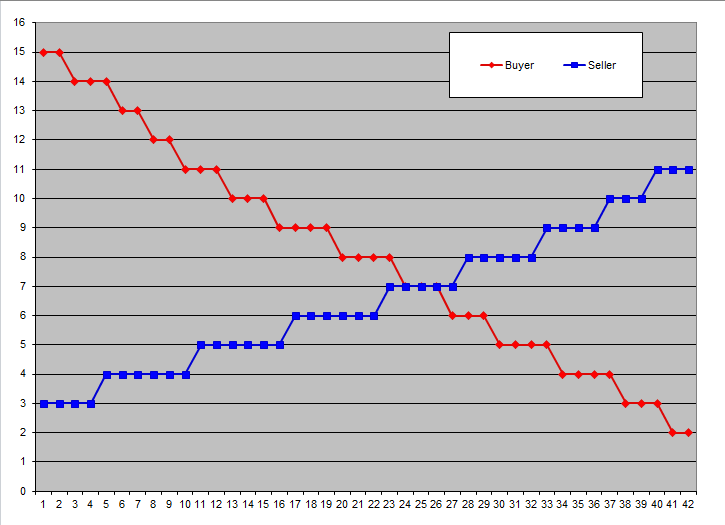

Market Simulation

Supply & demand curves from simulation

Market Simulation

[spreadsheet]

Market Simulation

Overall takeaways:

You were able to achieve most of the surplus, even though many could not make trades:

- Low cost producers found a way to sell

- Buyers with high value of the good found a way to buy

- This is where market efficiency comes from

Free trade made buyers better off--domestic sellers worse off. Whose surplus are we forgetting to count?

Practice Exercise

A firm in a perfectly competitive market has the following total cost curve:

TC = 400 + 2q + q^2

TC=400+2q+q2

where q is in thousands. The current price of the good is $30 per thousand units (i.e., $0.03 per unit).

- Assume other firms in the industry have similar cost curves. Does the price of $30 per 1000 units represent a long run equilibrium? Why or why not?

- If the demand in the total market (again, where Q is in thousands of units) is Qd = 900 - 3P, how many firms to you expect to be in this industry in the long run (round your answer)?

Summary of Long v. Short Run

In both long & short run:

Firms maximize profits by setting MC=P.

Price occurs where market demand=market supply

In short run:

Profits can be >0 or <0

Firms not necessarily producing at min of ATC

In long run:

Profits=0

Firms produce at min of ATC

Short Run Supply & Demand

When a doctor prescribes a drug, the prescription may be filled with either the brand name drug or its generic equivalent. Suppose a disruption in supply leads to an increase in brand name drug prices. How will this affect total consumer expenditures on brand name drugs and generic drugs? Expenditures would:

- increase for both brand name drugs and generics

- decrease for brand name drugs and increase for generics

- increase for generics, but might increase or decrease for brand name drugs

- increase for brand name drugs, but might increase or decrease for generics

Competition vs. Monopoly

Monopoly: A market with only one seller.

What are some reasons that a monopoly may arise?

Patent

Legal barriers to entry

Other barriers to entry (e.g. non-transferrable technical expertise or skill)

Competition vs. Monopoly

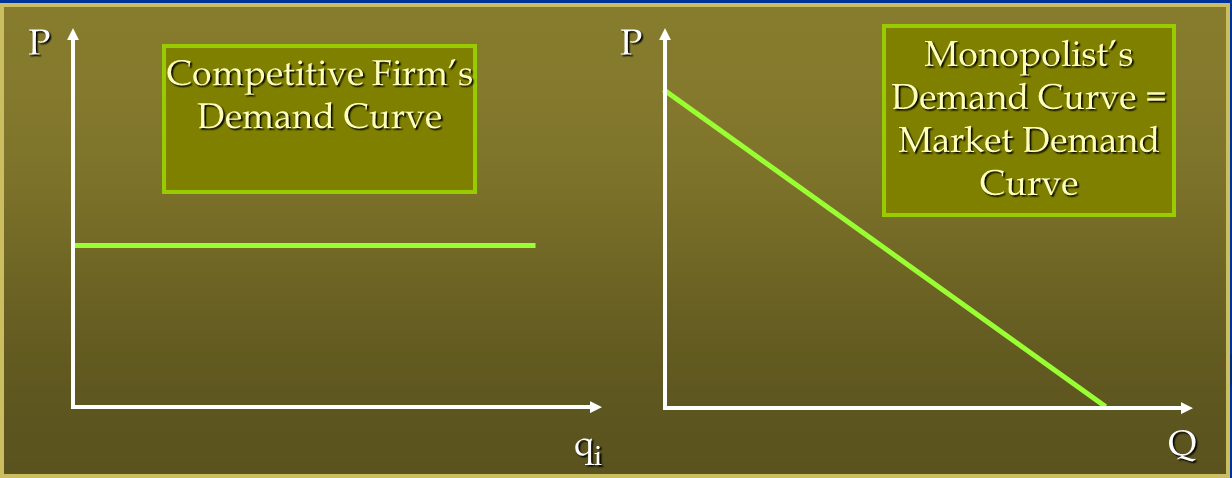

Since a monopolist is the only seller in the market, it faces the whole market demand.

Competitive market firm can produce as much as it wants and sell it at the market price. What does the monopolist have to do if she wants to sell more?

Competition vs. Monopoly

Competition vs. Monopoly

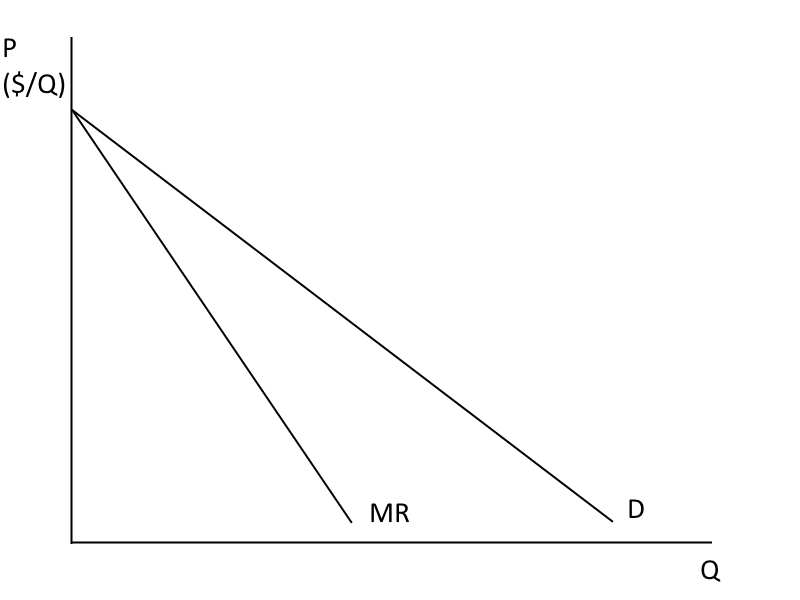

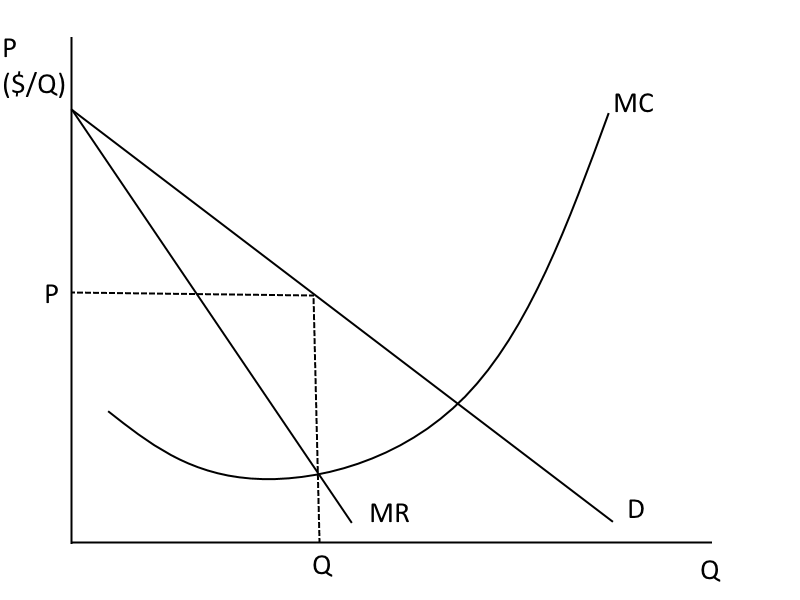

So, like all firms, a monopolist maximizes its profits by choosing Q such that MR=MC.

It sells this quantity at the price that the market is willing to pay, which we find on the demand curve.

Note: Just because there is only one firm does not mean there is no market discipline--the monopolist cannot charge a higher price than the demand curve will support.

Competition vs. Monopoly

At what quantity and price will the monopolist produce?

Competition vs. Monopoly

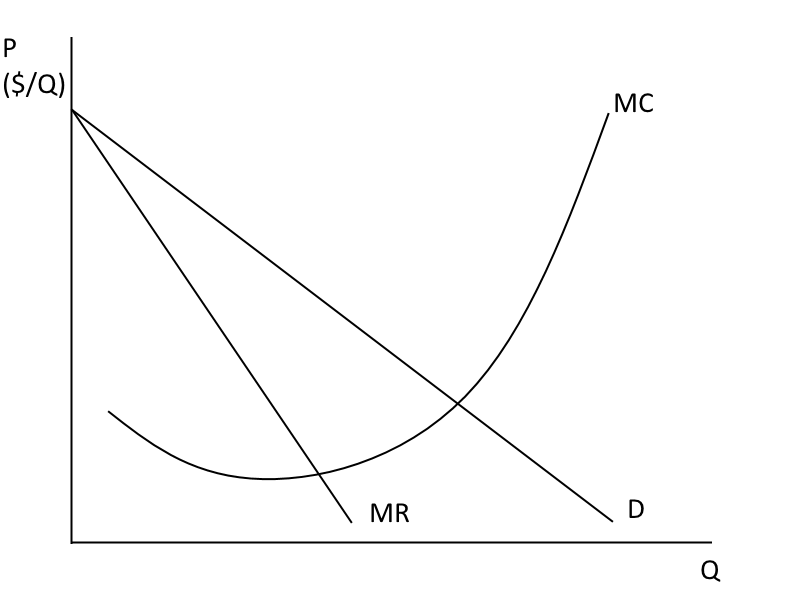

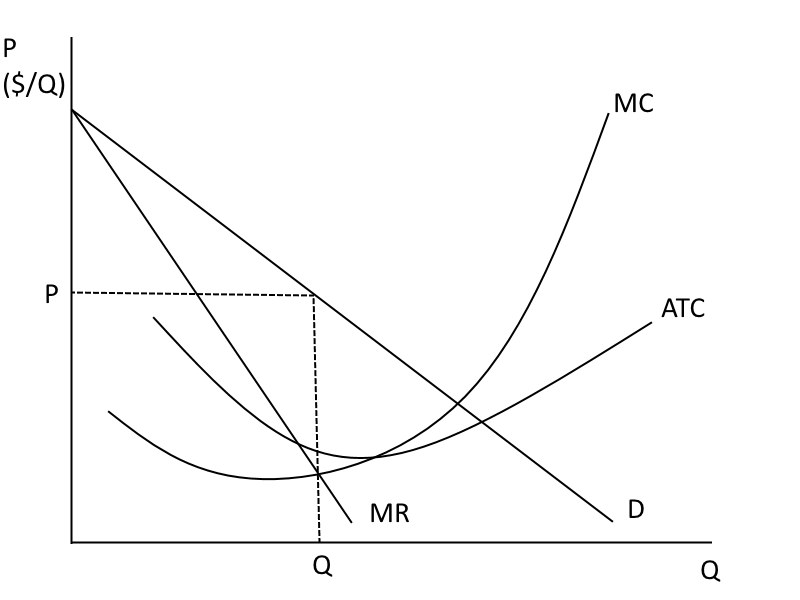

For the last unit sold, how much did it cost to produce? What was the "value" (WTP) of the good to the consumer?)

Competition vs. Monopoly

Price will always be greater than MC for a monopolist ("mark up"). In perfect competition, how much is mark up?

- One way regulators measure market power is by how much mark up there is.

Competition vs. Monopoly

Is the firm producing at the "efficient scale"?

Why or why not?

Competition vs. Monopoly

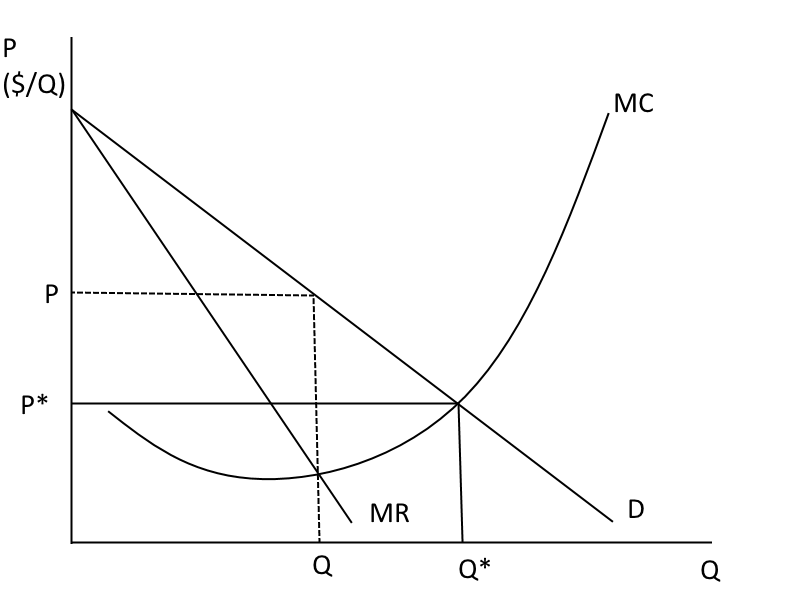

Where are profits in the graph? Do you think these are short or long run profits?

Competition vs. Monopoly

For a given market demand, a competitive outcome is where P=MC, or where demand = MC. Here, the marginal cost of producing the good is equal to the marginal value of that good by consumers.

No surplus is left on the table

Competition vs. Monopoly

"Competitive" outcome--demand (P)=MC

Competition vs. Monopoly

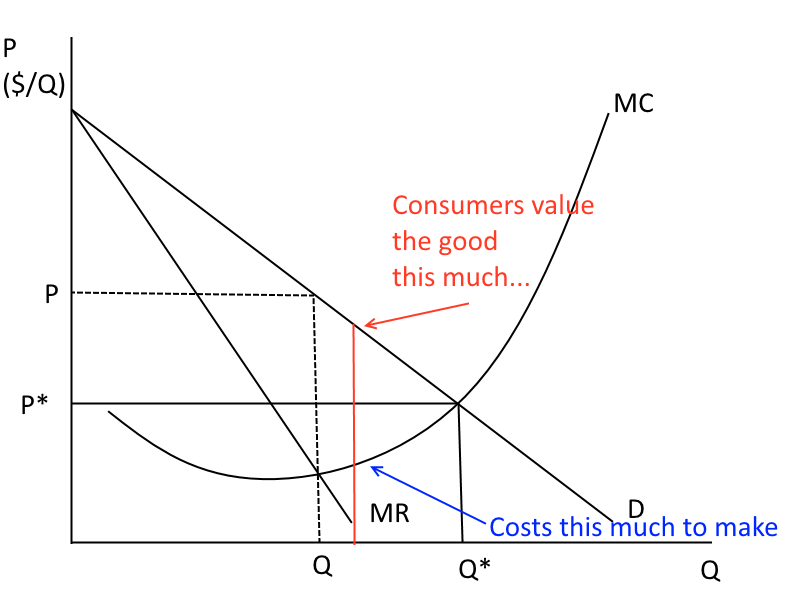

In a competitive environment, goods get produced as long as the value to consumers is greater than the cost to produce that good.

Is that true with monopoly?

Competition vs. Monopoly

Competition vs. Monopoly

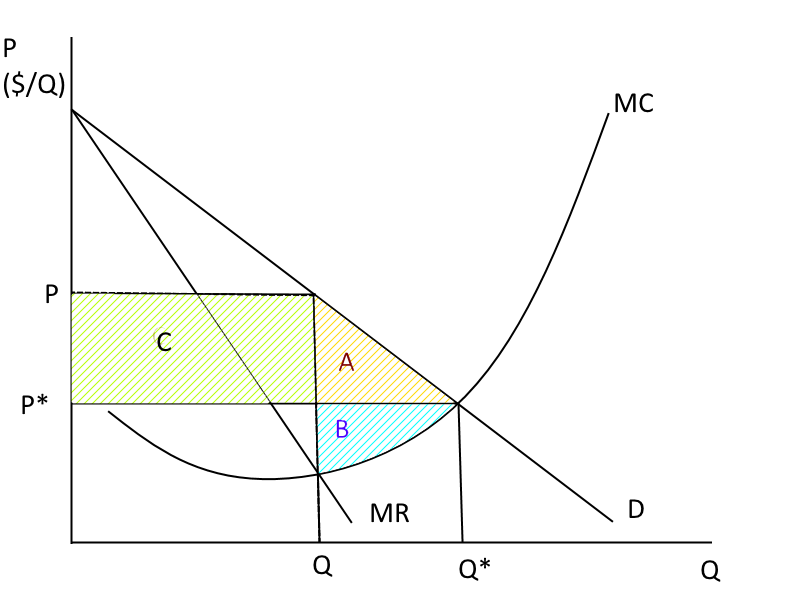

How would you characterize areas A, B, and C?

Competition vs. Monopoly

Because the monopolist knows increasing Q comes at the cost of lowering P, he or she will always want to produce less than the competitive outcome to drive up the price. This creates deadweight loss.

Competition vs. Monopoly

Suppose a brand name drug manufacturer faces

a demand curve of

Q_d= 250-.1P

Qd=250−.1P

or

P=2500-10 Q_d

P=2500−10Qd

where Q is in thousands of doses. Assume that the marginal cost of producing a thousand doses is constant, at 200.

- What are the competitive market price and quantity?

- Competitive market outcome is where Demand=MC

- What are the monopoly price and quantity?

- Monopoly outcome is where MR=MC

- MR for monopolist has same intercept as demand curve but 2x slope

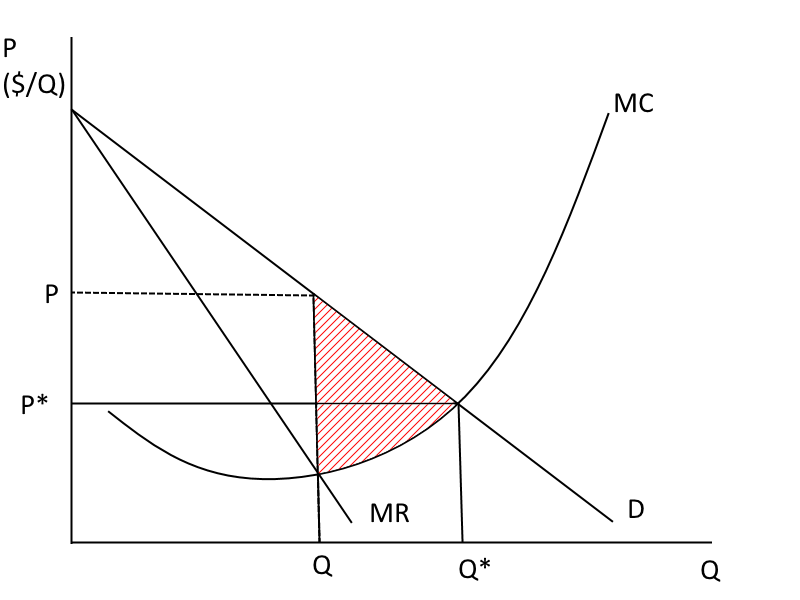

- What is the monopoly deadweight loss?

(Note this is a special case, with a constant or flat MC, so that MC also = AC.)

Competition vs. Monopoly

Monopolists are not disciplined by competition.

- They do not produce at the bottom of the AC curve, and need not even produce with the best technology.

- Inadequate managerial motivation to be efficient => waste of resources

- e.g., When Israel’s phone monopoly was deregulated, the cost per call went from $3 to $0.30 in a matter of months

Competition vs. Monopoly

“Rent-seeking”: Firms expend resources to obtain or maintain monopoly profits.

E.g., brand-name drug companies try to stall generics.

Lobbying for patent extensions.

Getting multiple patents on a drug, even for such things as the shape of the pill.

Raising questions about the safety of the generic version.

Paying generic drug companies to drop patent challenges.

(Challenged by the US Federal Trade Commission as illegal conduct)

Competition vs. Monopoly

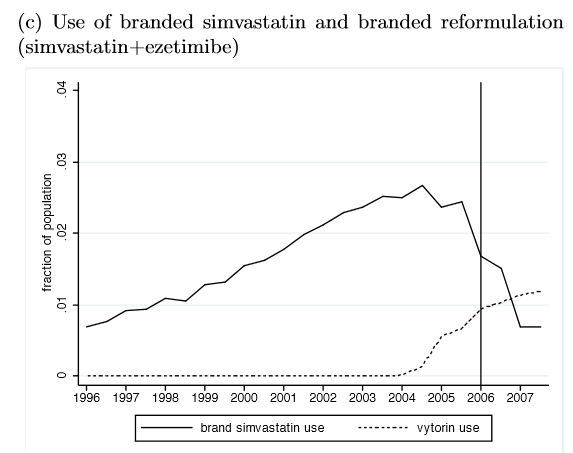

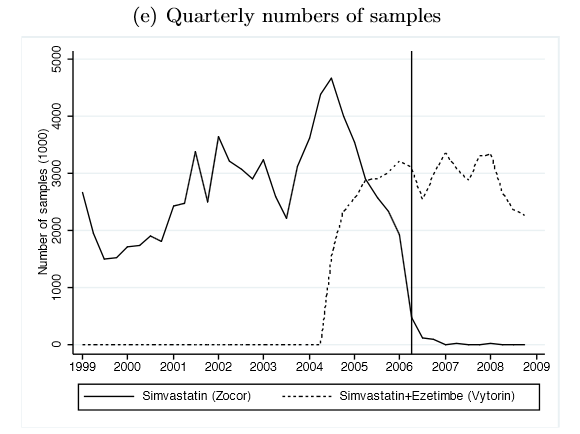

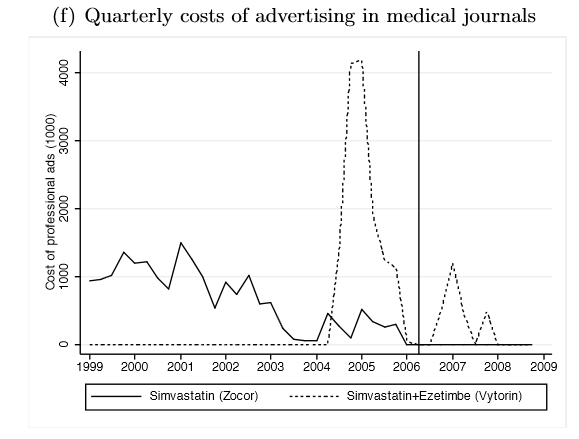

Ex: Zocor patent expiration (from Huckfeldt and Knittel NBER 2011)

Even though the price of the branded drug dropped when it went generic--utilization still went down

Competition vs. Monopoly

Huckfeldt and Knittel NBER 2011

Competition vs. Monopoly

Huckfeldt and Knittel NBER 2011

Competition vs. Monopoly

However, there's a counter argument: Dynamic v. Static Efficiency

- Does market power lead to more or less innovation?

Schumpeter’s claim (1943): The perfectly competitive system, though efficient in the static sense, may be inferior over the long-run because it produces less innovation.

Others argue monopolists rest on their laurels and do not produce enough innovation (quiet life argument)

Analysis of Competitive Markets

Market Analysis

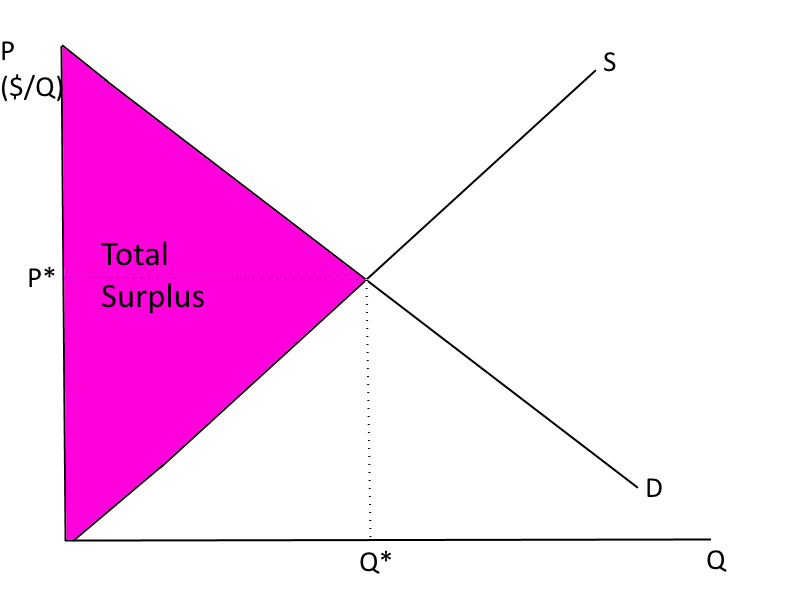

As we saw earlier: in equilibrium, perfectly competitive markets maximize total surplus in the economy. This is how economists think of the total value or total welfare created by this market.

Market Analysis

Also, in the long-run, all firms in competitive industries produce at the lowest cost possible:

- They all end up at the bottom of their ATC curve

- They all have to use efficient technology

- So goods are produced using the least amount of resources

- Further, they are produced in combinations that match what consumers are willing to pay for them

Welfare is maximized.

Market Analysis

But... there are important assumptions:

Income Distribution: A competitive market maximizes the total surplus given the initial distribution of income.

Consumer Sovereignty: Consumers are the best judge of what is good for them.

No Externalities: Producers bear all of the costs of production, and purchasers receive all of the benefits of consumption.

If society is concerned about the initial income distribution, or the other two assumptions fail, there can be an economic rationale for government intervention

Market Analysis

Spend a little time talking about government intervention in competitive markets and public policy issues

- Broaden our view

- Your business might suffer or benefit from government regulation – it is important to understand the basis for, and anticipate market reactions to, such regulation

Market Analysis

Our benchmark for doing policy analysis is the outcomes that would occur in an unconstrained competitive market.

Why?

Productive Efficiency

Allocative Efficiency

Market Analysis

Another way to say this is:

Competitive markets maximize the sum of consumer and producer surplus, so no one can be made better off without making someone else worse off.

This is called Pareto Efficiency.

Market Analysis

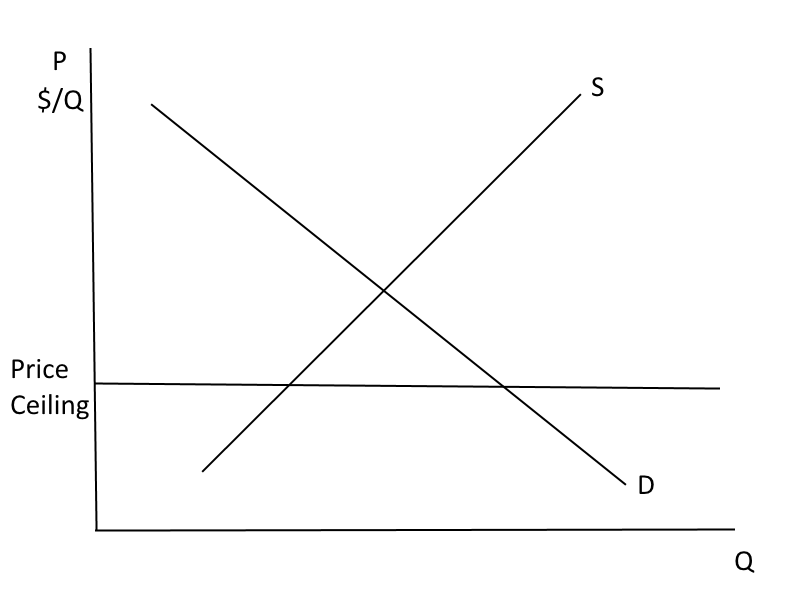

Price Ceiling: When the price of a good is not allowed to go above a certain level.

Can you think of an example of a price ceiling?

Market Analysis

With Venezuelan Food Shortages, Some Blame Price Controls

(NYT 2012)

"By 6:30 a.m., a full hour and a half before the store would open, about two dozen people were already in line. They waited patiently, not for the latest iPhone, but for something far more basic: groceries

Market Analysis

NYT 2012 (cont.)

"The shortages affect both the poor and the well-off, in surprising ways. A supermarket in the upscale La Castellana neighborhood recently had plenty of chicken and cheese — even quail eggs — but not a single roll of toilet paper. Only a few bags of coffee remained on a bottom shelf."

"...At the heart of the debate is President Hugo Chávez’s socialist-inspired government, which imposes strict price controls that are intended to make a range of foods and other goods more affordable for the poor. They are often the very products that are the hardest to find.

Market Analysis

How would a price control affect a firm's decision making about production?

How would it effect demand?

The goal of the policy was to make consumers better off.

Was it successful in that regard?

Are any consumers made better off?

Market Analysis

“[M]any economists call it a classic case of a government causing a problem rather than solving it. Prices are set so low, they say, that companies and producers cannot make a profit. So farmers grow less food, manufacturers cut back production and retailers stock less inventory."

Market Analysis

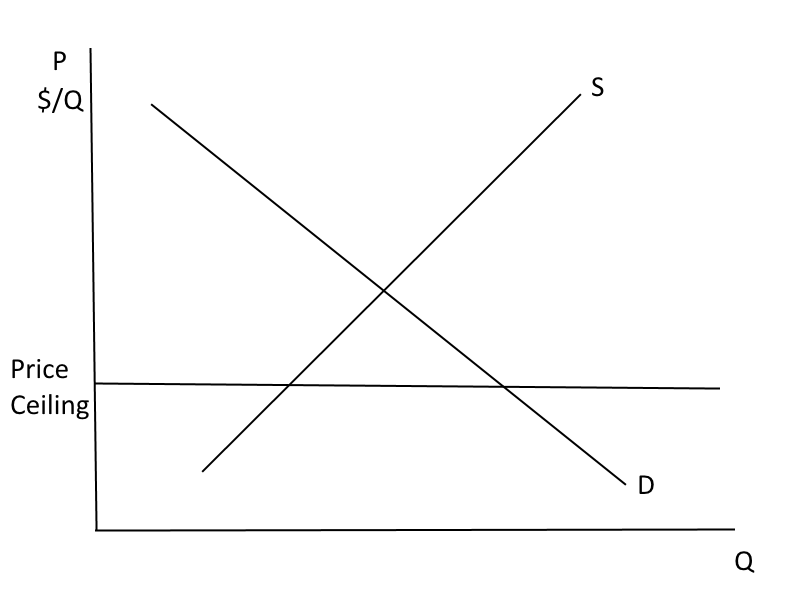

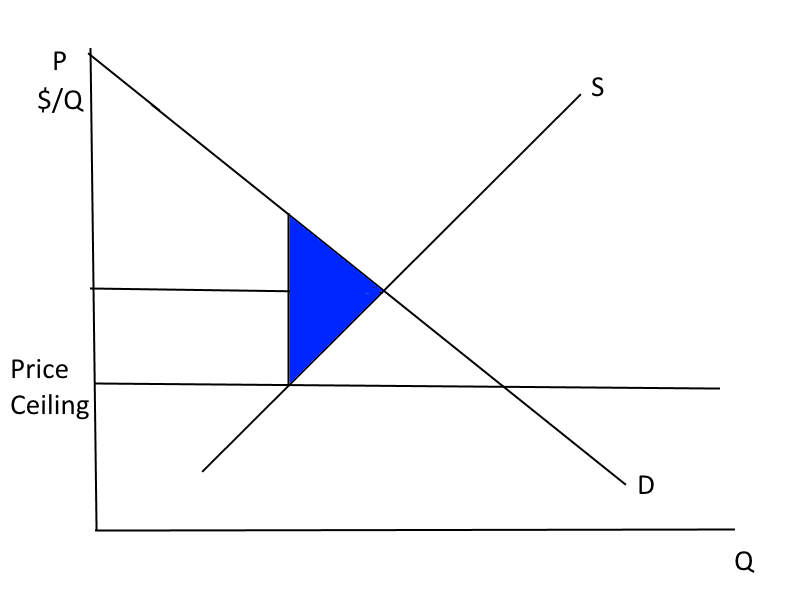

Without a price ceiling, what would be the price and the quantity in the market?

Market Analysis

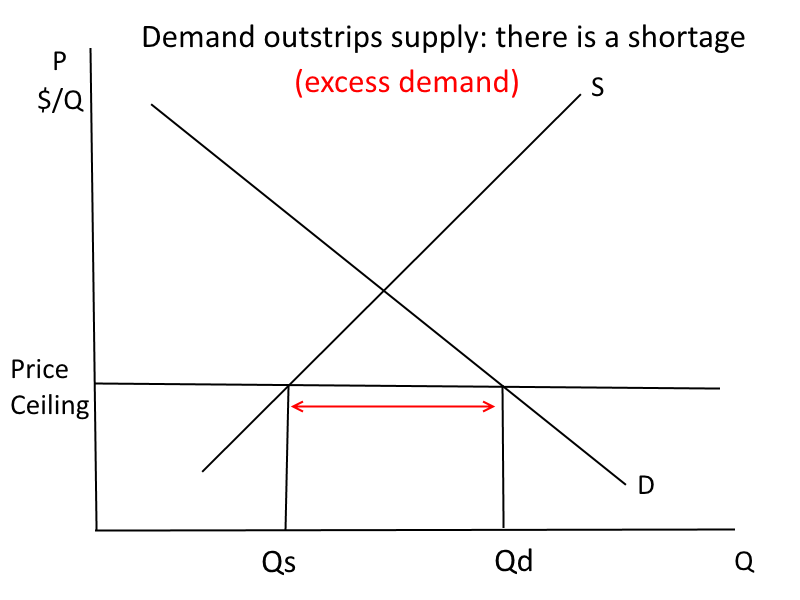

With a price ceiling, how much is demanded? How much is supplied? What do we call this situation?

Market Analysis

Excess Demand (Shortage) = Qd-Qs

Market Analysis

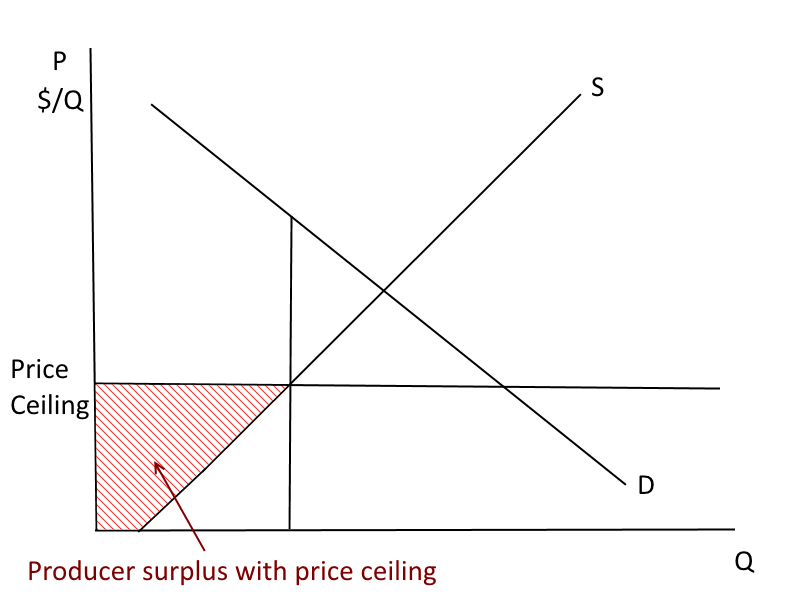

Where on the figure is producer surplus?

Market Analysis

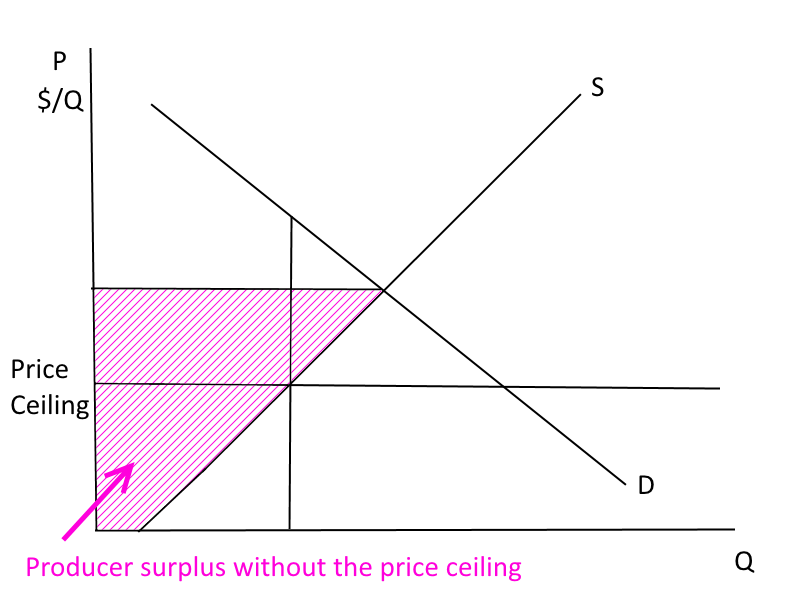

Where would producer surplus be without a price ceiling?

Market Analysis

Market Analysis

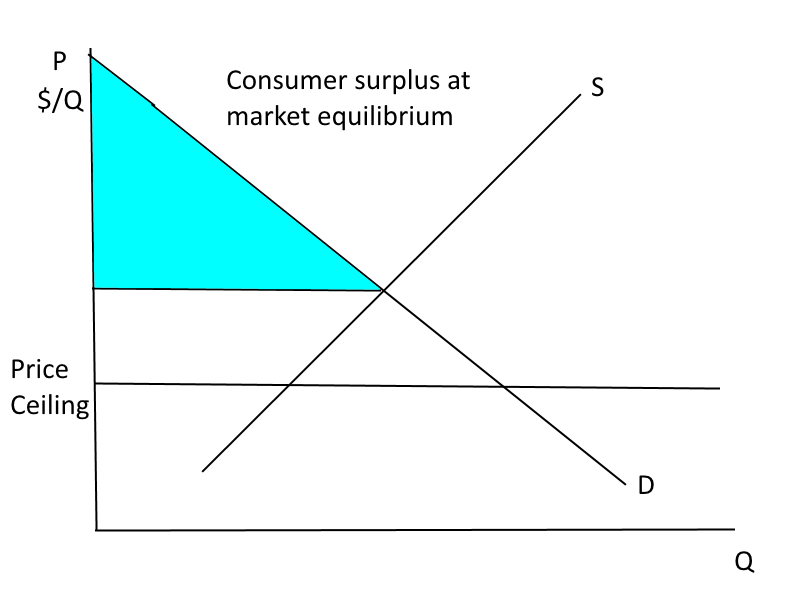

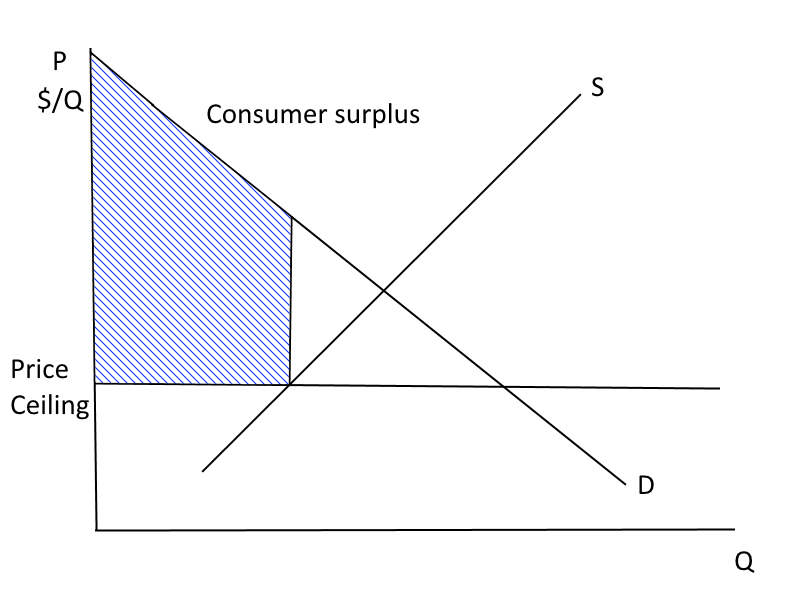

Where would consumer surplus be in the absence of a price ceiling?

Market Analysis

Where would consumer surplus be in the absence of a price ceiling?

Market Analysis

Are consumers better or worse off with the price ceiling?

Market Analysis

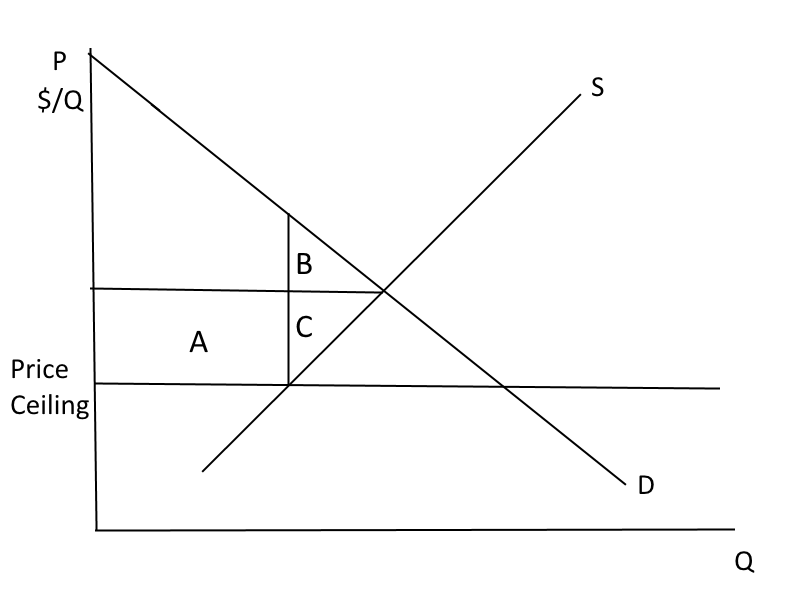

A is a transfer from producers to consumers.

B was part of consumer surplus, but is no longer, because fewer units are produced. C was part of producer surplus.

Market Analysis

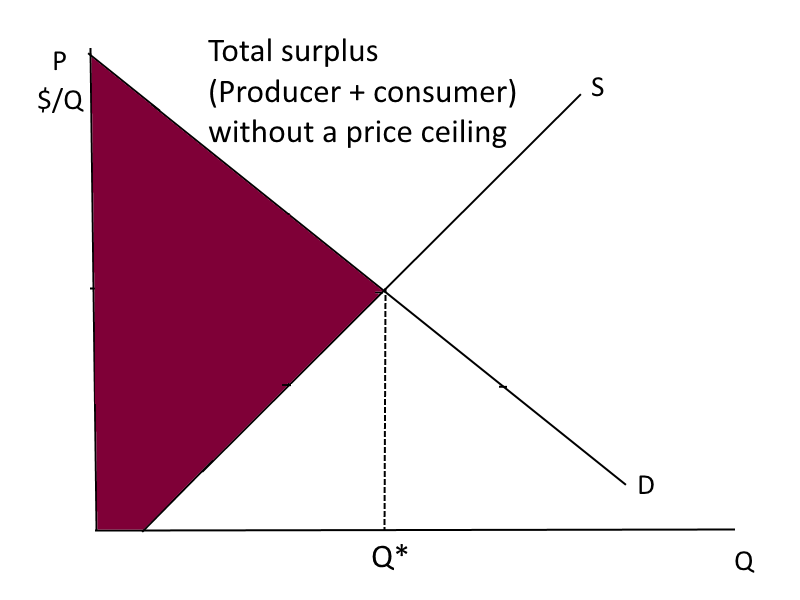

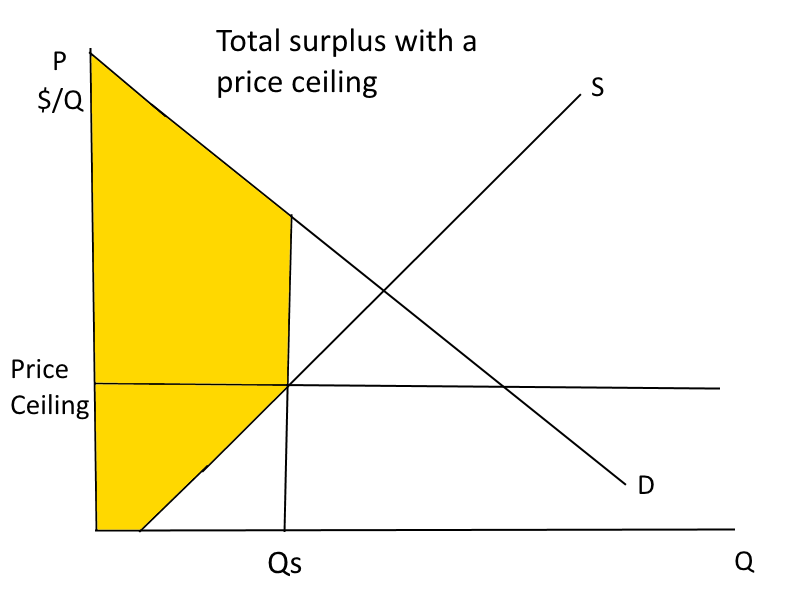

Is total surplus higher or lower with a price ceiling?

Market Analysis

Market Analysis

Surplus is smaller because fewer units are produced. Those units would be valued by consumers by more than they cost producers to make -- but they aren't produced because the policy makes it unprofitable for firms

Market Analysis

The difference between the surplus with a price ceiling and the maximum possible surplus is called deadweight loss

Market Analysis

A rent control policy setting $1500 per month rent on apartments in San Francisco is being considered. Assume apartments are all the same, with the demand for apartments given by

P=3600-Q_d

P=3600−Qd

And supply is

P = 400 + Q

P=400+Q

What is the deadweight loss created by the rent control policy?

Market Analysis

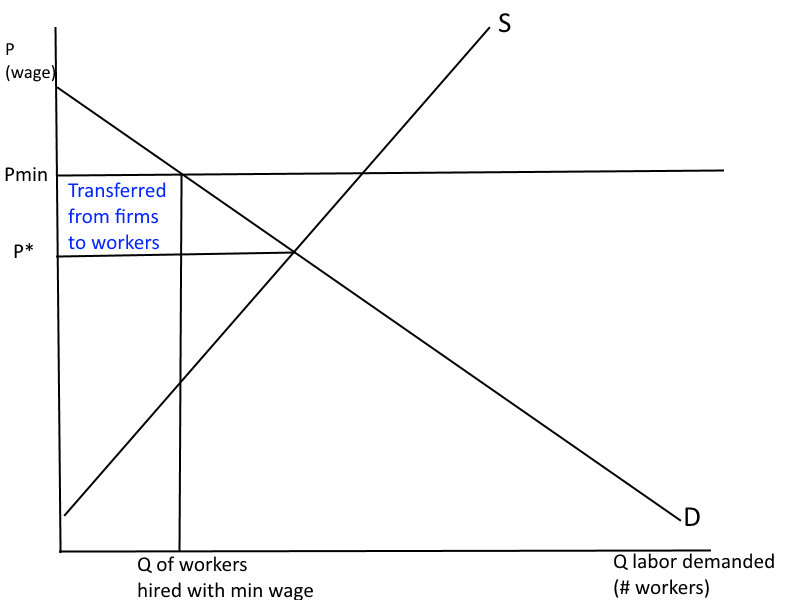

Another type of price control is a price floor.

Price Floor: When the price of a good is not allowed to go below a certain level

What is an example of a price floor?

Market Analysis

In this scenario, who are the demanders?

Who are the suppliers?

Market Analysis

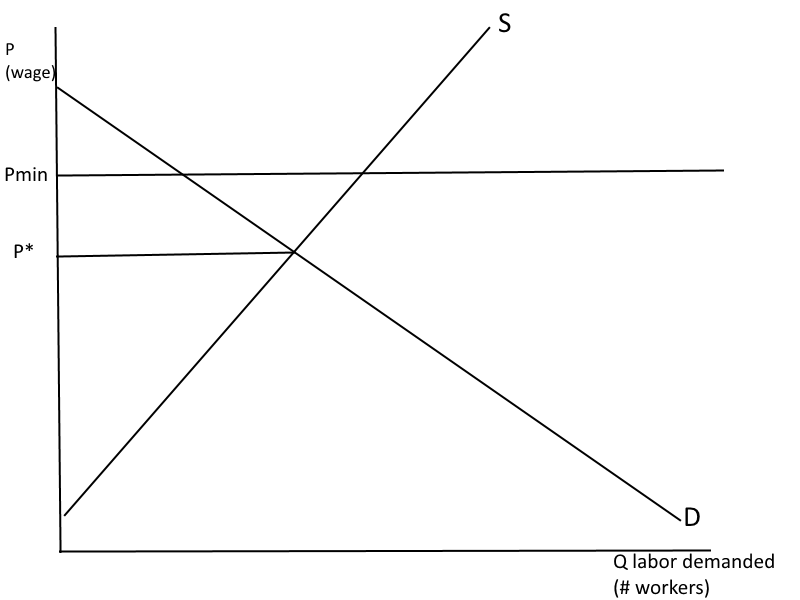

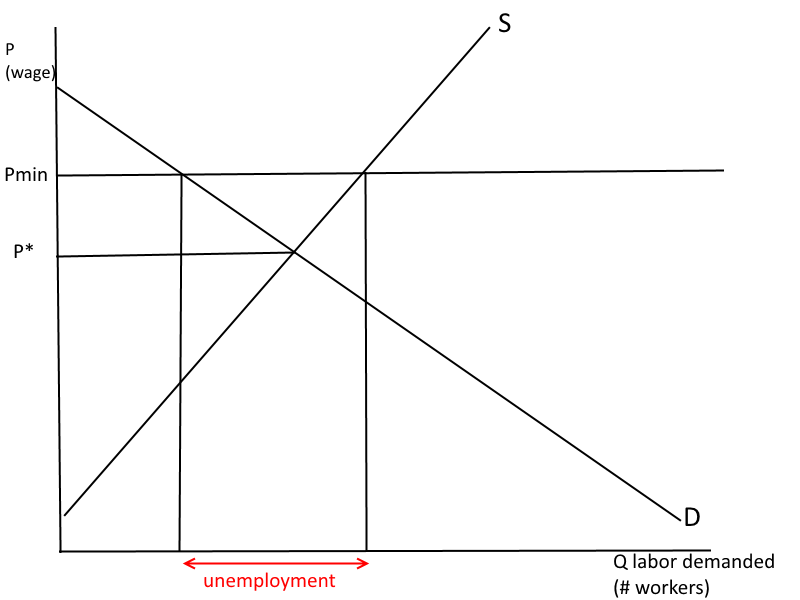

How much labor is demanded by firms? How many workers are willing to supply their labor? What do we call this difference?

Market Analysis

What has happened to the consumer surplus of the firm? What has happened to the producer surplus of the workers?

Market Analysis

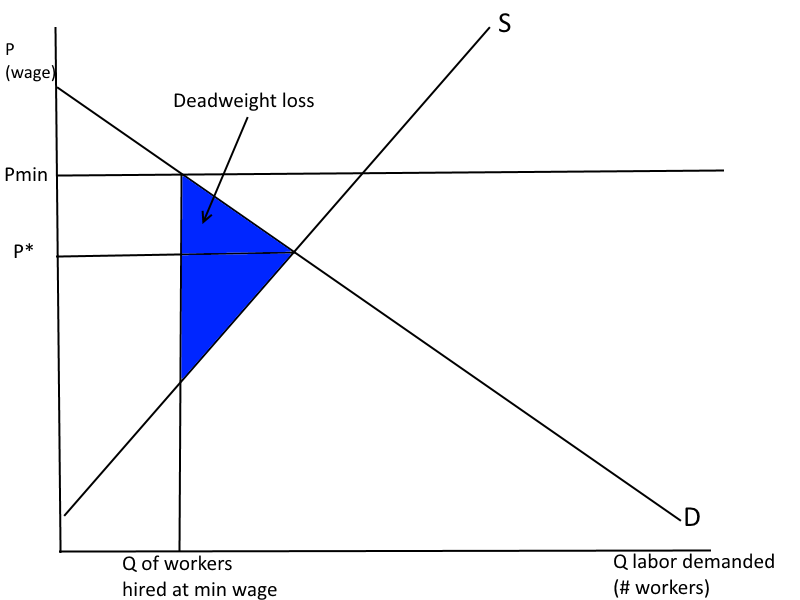

Where is deadweight loss?

What causes deadweight loss in this scenario?

Market Analysis

Market Analysis

Slate (Feb 24, 2014):

"Today the Congressional Budget Office put out a report on the economic impact of raising the minimum wage to $10.10, and it found that doing so would probably reduce the total number of people employed but also raise the incomes of low-income families.

The White House has struck back citing contrary research, and in my experience the empirical evidence on this question has never persuaded anyone."

Market Analysis

Slate (Feb 24, 2014):

"So let me make another point. If the White House genuinely believes that a hike to $10.10 would have zero negative impact on job creation, then the White House is probably proposing too low a number. The outcome that the CBO is forecasting—an outcome where you get a small amount of disemployment that's vastly outweighed by the increase in income among low-wage families writ large—is the outcome that you want. If $10.10 an hour would raise incomes and cost zero jobs, then why not go up to $11 and raise incomes even more at the cost of a little bit of disemployment?"

Market Analysis

If the supply of labor is at least somewhat elastic, is it possible that a minimum wage can raise incomes but have no effect on the total number of jobs available to low income workers?

Do you think all of our model's assumptions apply to the labor market for those making the minimum wage? Why or why not?

Lecture 9

By umich