Buying the Hype:

Understanding Equity

and Stock Offers

slides.com/verythorough/buying-the-hype

Jessica Parsons

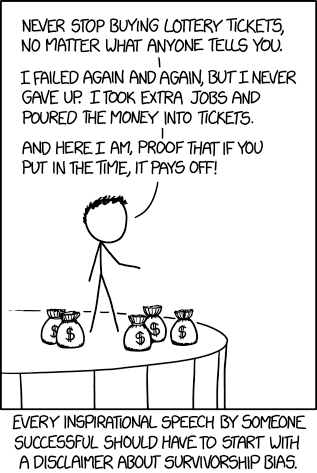

The Dream

The Reality

source: xkcd

The Basics

Defining Terms

Stock Options: An option to buy a certain amount of stock at a certain price

Grant

Legally binding agreement of terms for your options

Vesting

Gradually gives you access to your options

Exercise

The act of purchasing your actual stock

Sale

The act of selling your stock

Important Grant Info

Grant date: date when your grant begins

Post-termination period: window when you can still buy after you leave (usually 90 days, more for death, etc.)

Expiration date: date when you can no longer buy your options (usually 10 years after grant date)

Strike/exercise price: the price you pay for your shares (usually 'fair market value' on the grant date)

Quantity: number of shares you can buy when fully vested

Vesting Schedule

"Four-year monthly vesting with a one-year cliff"

Vested options

Vesting Schedule

"... and a ten-year expiration"

Vested options

Exercise Terms

# of shares x strike price = cost basis

# of shares x (current fair market value - strike price) =

1000 x $0.10 = $100

1000 x ( $1.00 - $0.10 ) =

Spread

$900

Sale Terms

# of shares x current market price = gross proceeds

gross proceeds - cost basis = net proceeds

1000 x $2.00 = $2000

$2000 - $100 = $1900*

* $900 of this is the spread

Types of Equity

Restricted stock award: actual stock granted to you, with no purchase required (granted and transferred all at once, but control is usually vested)

ISOs (incentive stock options): options with special tax benefits (only available to employees)

NSOs (nonstatutory stock options): options where the spread is taxed as ordinary income at exercise (usually used for contractors)

RSUs (restricted stock units): "units" of stock (or cash value of stock) given to you over a vesting schedule

On the Market

Public Company Options

Same-day exercise & sell

1000 shares Strike price $0.10 Market price $2

Cost basis = 1000 x $0.10 = $100

Spread = 1000 x ($2 - $0.10) = $1900

Gross proceeds = 1000 x $2 = $2000

Net proceeds = $2000 - $100 = $1900

Net proceeds = Spread = $1900 ordinary income

Public Company Options

Buy & hold

1000 shares Strike price $0.10 Value at exercise $1 Sale price $2

Cost basis = 1000 x $0.10 = $100

Spread = 1000 x ($1 - $0.10) = $900

Gross proceeds = 1000 x $2 = $2000

Net proceeds = $2000 - $100 = $1900

Tax calculations depend on how long you hold

Public Company Options

Taxes: How long did you hold?

Net proceeds = $1900 Spread = $900

Hold for less than 1 year

Spread = $900 taxable as income

Net proceeds - Spread = $1000 short-term capital gains*

*taxed at the same rate as ordinary income

Hold for more than 1 year

Spread = $900 taxable as income

Net proceeds - Spread = $1000 long-term capital gains

If your total income is high enough, Net Investment Income Tax may also apply.

Public Company Options

Taxes: How long did you hold?

Net proceeds = $1900 Spread = $900

Special to ISOs:

ALL net proceeds = $1900 long-term capital gains

Hold for more than 1 year

... and 2 years after grant

AMT

Alternative Minimum Tax

Counts the bargain element as income

at exercise

It varies widely by situation! You can use calculators to estimate, but talk to an expert before making a move.

The Startup

Private Company Options

Buy & hold for ... ever?

1000 shares Strike price $0.10 Exercise price $1

Cost basis = 1000 x $0.10 = $100

Spread = 1000 x ($1 - $0.10) = $900

Can't sell until there's an exit:

Lots of upfront cost that may never pay off

acquisition ~ or ~ IPO

Private Company ISOs

AMT can be huge

10,000 shares Strike price $0.10 Exercise price $5

Cost basis = 10,000 x $0.10 = $1000

Spread = 10,000 x ($5 - $0.10) =

$49,000

taxable "income"

...but again, it's complicated,

so talk to an expert!

Waiting for an exit

Schedule limitations

Termination (voluntary or involuntary)

Quit/fire/layoff is usually 90 days

(but some are offering much longer)

Death or disability may have a longer window

(like 12-18 months)

Expiration

10 years after grant date

Waiting for an exit

Possible shortcuts

Tender offer ('buy back')

Company may offer an event allowing

shareholders to sell a potion of their shares

Secondary 'sale' services

Third-party companies offer loan-like instruments

for buying and selling options

Examples (not endorsements!): ESO Fund, EquityZen, Equitybee

Weighing

the Options

Evaluating an Offer

General Considerations

- Are you taking a cut in salary?

- How much?

- When will you reach market value?

- If you made the higher salary, would you save it?

- Do you need for this to pay out big?

- What stage is the company in?

- How are its prospects?

- What type of equity is offered?

Evaluating an Offer

Questions to ask the company

- How many shares are being offered?

- What % of the company do the shares represent?

- What is the total current share pool?

- What is the current 409a valuation?

- What is the vesting schedule?

- (Mostly for RSUs) Are there any other vesting triggers?

- Performance milestones

- Company exit

- How long after termination can options be exercised?

Evaluating an Offer

How does your percentage compare?

- Check rough estimates based on position or hire #

- Check Wellfound (formerly AngelList) for similar positions at similar companies.

- Send your offer info to Carta (web form or email) to get custom benchmark information.

(Be aware that this may also vary widely,

especially in early stage companies)

Calculating Possible Exits

Dilution and Preferred Shares

Dilution

Your option/share count stays the same, but your percentage will decrease as more investors join

This can mean that if the company sells for $100M

but raised $100M, your shares are worth $0

Preferred Shares

Investors typically have preferred shares, which usually includes liquidation preference, which means investors get back what they put in, first.

Calculating Possible Exits

See what info you can get from the company

- Can I see a waterfall table of different exit scenarios? (unlikely, but possible)

-

What is the liquidation overhang?

- How much has the company raised?

- Is all of that preferred with liquidation preference?

- Do any investors have multipliers or participation rights? (This amplifies the liquidation overhang.)

- Do you plan to raise more? What are your long-term goals?

Calculating Possible Exits

Generate possible minimums

- How much would the company have to 'sell' for before your stock is worth anything?

- How much before you get back your lost salary?

- How much before it really gets interesting?

How likely is this to happen? How long will it take?

(Be sure to consider future funding in your calculations.)

Find similar companies to compare.

Asking for More

Negotiation Points

Minimize upfront costs

Early exercise

Buy shares before vesting to eliminate the bargain element

10,000 shares Strike price $0.10 Exercise price $0.10

Cost basis = 10,000 x $0.10 = $1000

Spread = 10,000 x ($0.10 - $0.10) = $0

Restricted Stock Award (not RSUs!)

Similar benefits, except there's no purchase price - you're given the stock outright (and taxed as income)

(In both cases, you'll lose unvested shares if you leave early)

may also get Qualified Small Business Stock benefits

archival photo, Silicon Valley circa 2017

but don't forget ...

Negotiation Points

Keep your options on the table

Extended exercise period

Keep your options for years after you leave, so you can wait for an exit. Some may scoff, but companies are doing it.

Follow-on stock grants

See if the company has a policy for granting more stock over time, to curb dilution and get options with later expiration.

Accelerated vesting on acquisition

Avoid losing unvested options if the company is acquired (single-trigger) and lays you off (double-trigger).

The Follow-Up

After Accepting

Gotchas to watch out for

Get your grant

This is not your offer letter! It may be months before you get it, especially in a new startup. Try to ensure you get it before the company's valuation goes up.

Look before you leap

Before exercising options (especially buy & hold), make sure you know the tax implications. Get professional help!

Check for take-backs

Ask if the company has the right to repurchase vested shares. This can hurt (or sometimes help) you.

After Accepting

Reality Check

Money isn't everything

And stock options may never be money! Remember there are many reasons to join a company.

Satisfaction is perception

Wondering if you could have negotiated a better deal will not bring you more money or happiness. Celebrate what you achieved and move on!

(and new funding rounds are a great time to renegotiate!)

Buying the Hype: Evaluating Equity and Stock Offers

By Jessica Parsons

Buying the Hype: Evaluating Equity and Stock Offers

Companies often justify lower salaries with promises of huge stock returns, but the laws and options are complex, and values are difficult to evaluate against an uncertain future. How do you evaluate the potential and comparability of the offer you've received? What options do you have for negotiating an offer to your advantage, and how can you make the most of it? I'll help you wade through the sea of terms, options, and outcomes so you'll feel prepared to make these choices for yourself when you receive your next equity offer, or in leveraging options you already have. Presented at Write/Speak/Code 2017 and Google IWD SF 2018.