Andreas Park PRO

Professor of Finance at UofT

by Andreas Park

Research Presentation

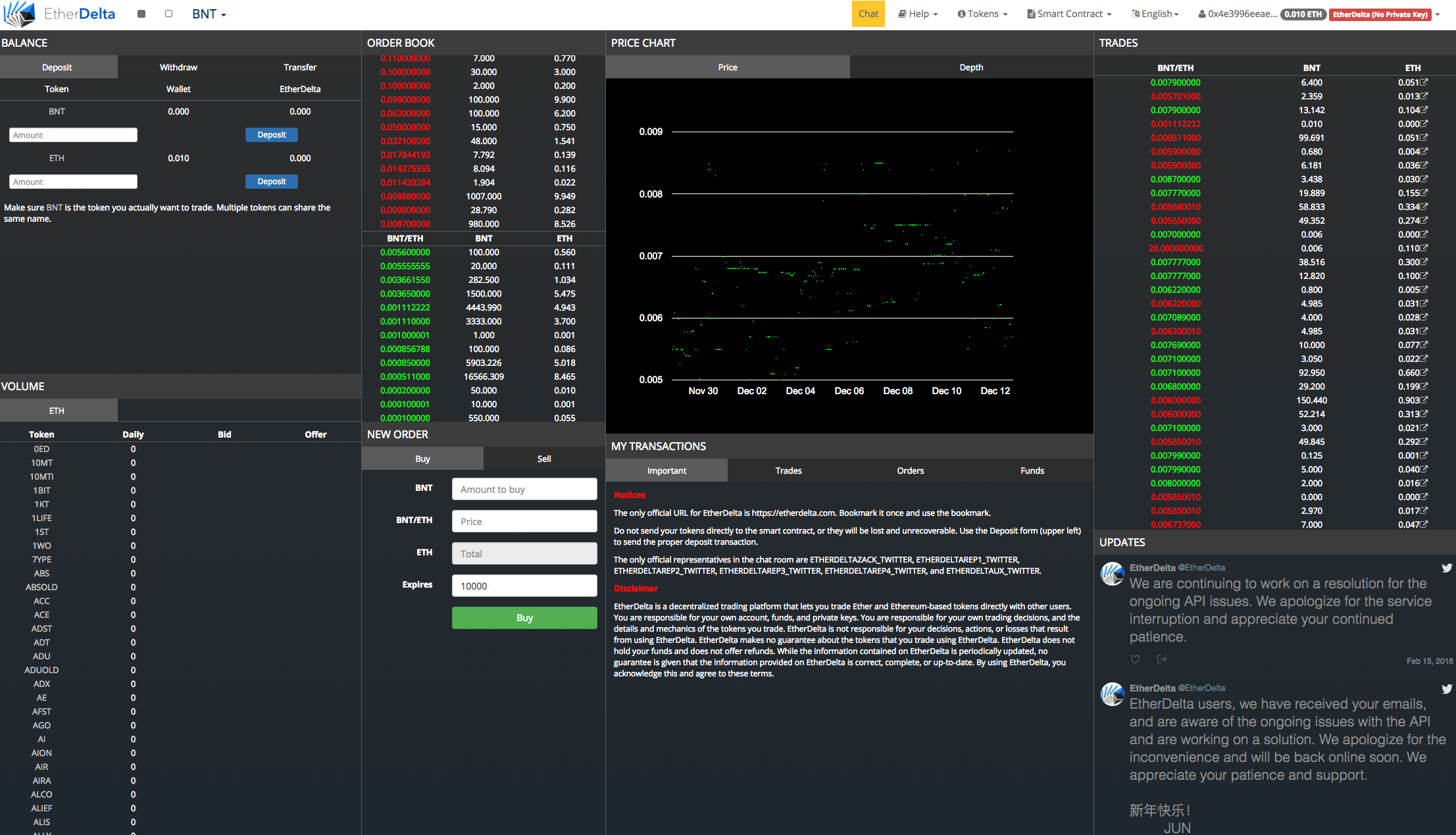

How do you set the price?

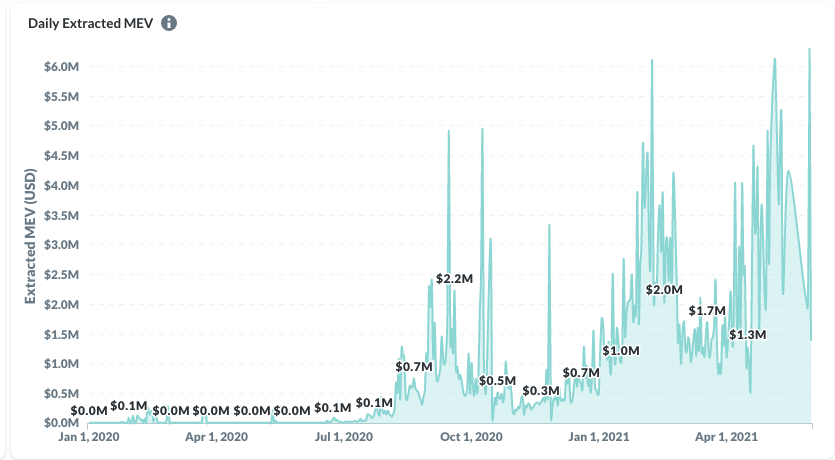

But there is a dark side: miner extractable value

a

b

c

d

e

f

g

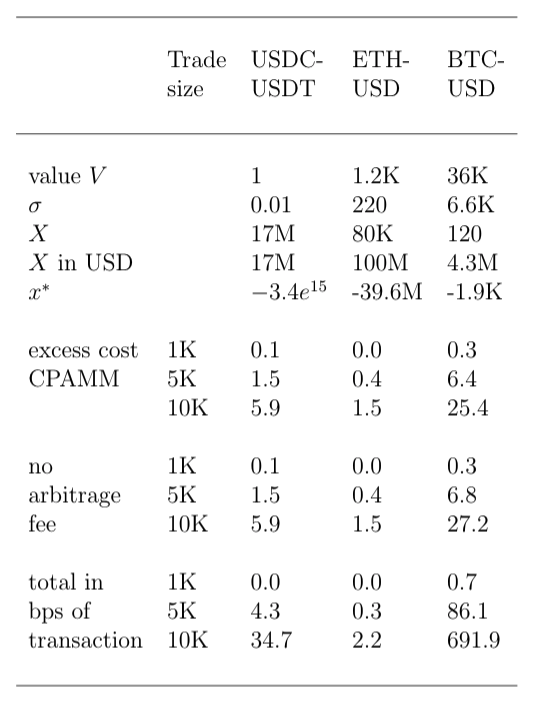

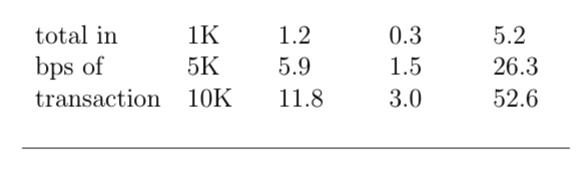

However: although front-running is annoying, it is only a concern if it is intrinsically profitable.

My paper:

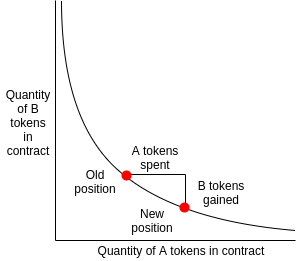

Price mechanism:

Prices

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

\(X\)

\(Y\)

\(Y-y'\)

\(X+x\)

\(Y-y'-y''\)

\(X+2x\)

\(y'=y''~\Rightarrow\)

front-running is not intrinsically profitable

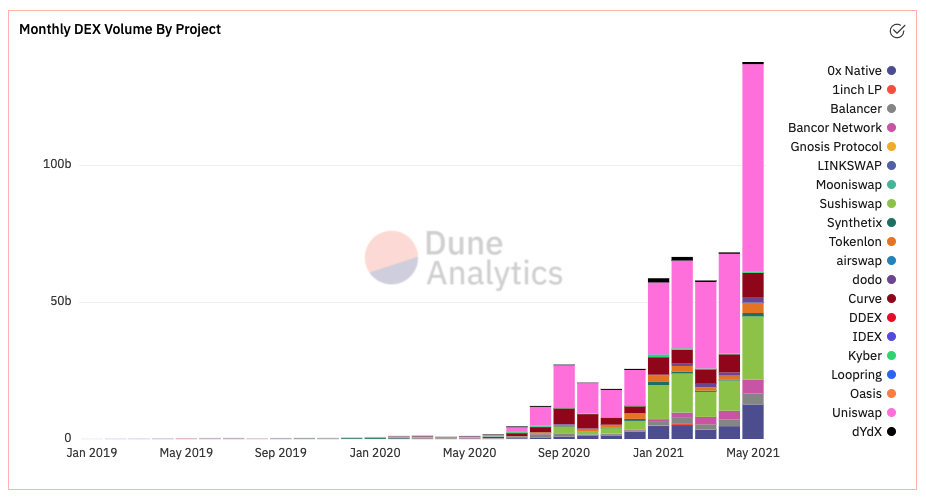

CPAMM

canonical

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park