Andreas Park PRO

Professor of Finance at UofT

Andreas Park

July 31, 2025: "today I am announcing the launch of “Project Crypto”—a Commission-wide initiative to modernize the securities rules and regulations to enable America’s financial markets to move on-chain."

What's interesting about Defi Lending?

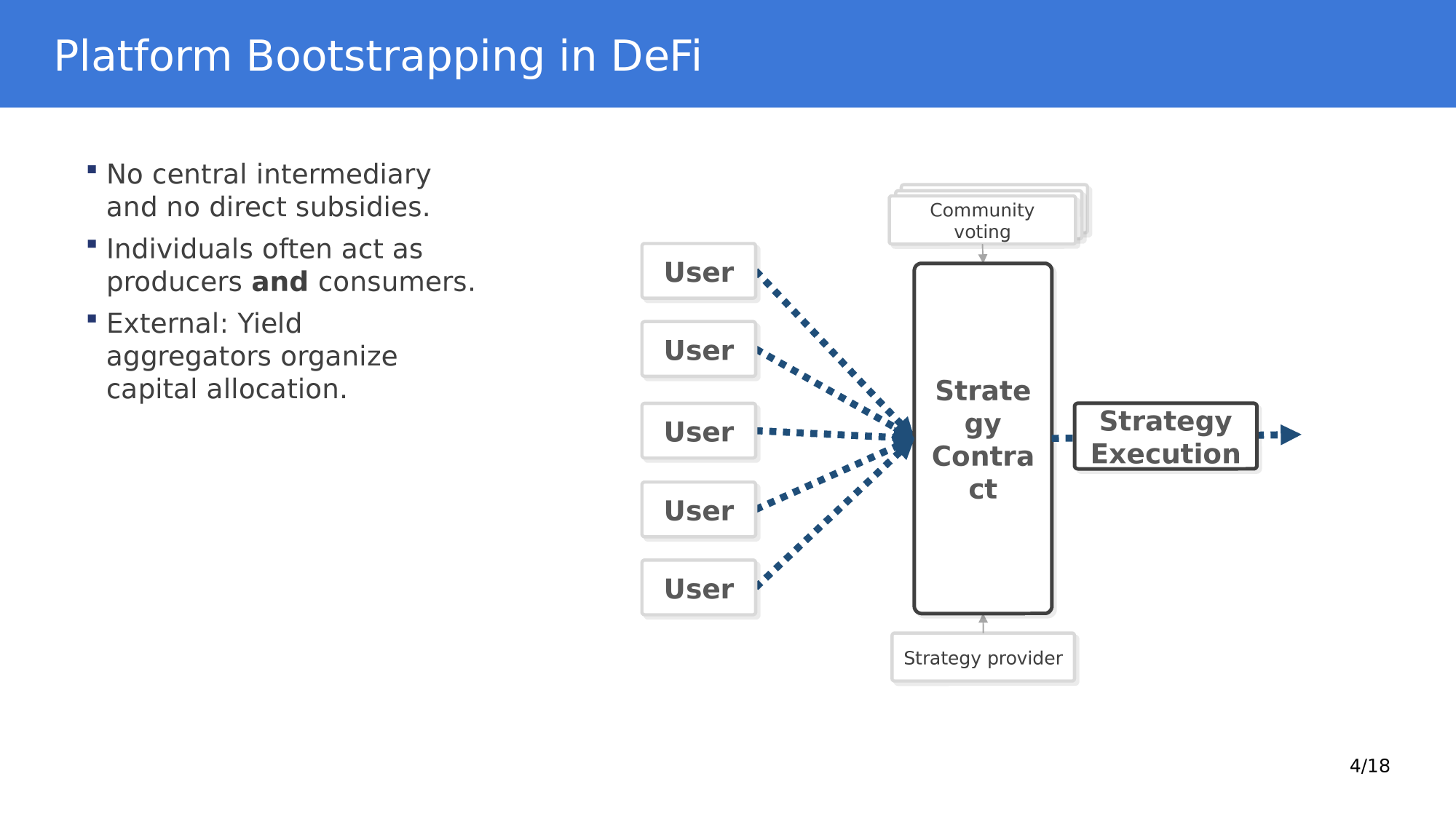

What are the core functions that a DeFi Ecosystem must cover?

What are the core functions that a DeFi Ecosystem must cover?

Liquidity transformation

Credit

Comparative advantage

MakerDAO/Sky

very hard without identity

this talk:

AAVE/Compound

the empirical part will focus on this episode

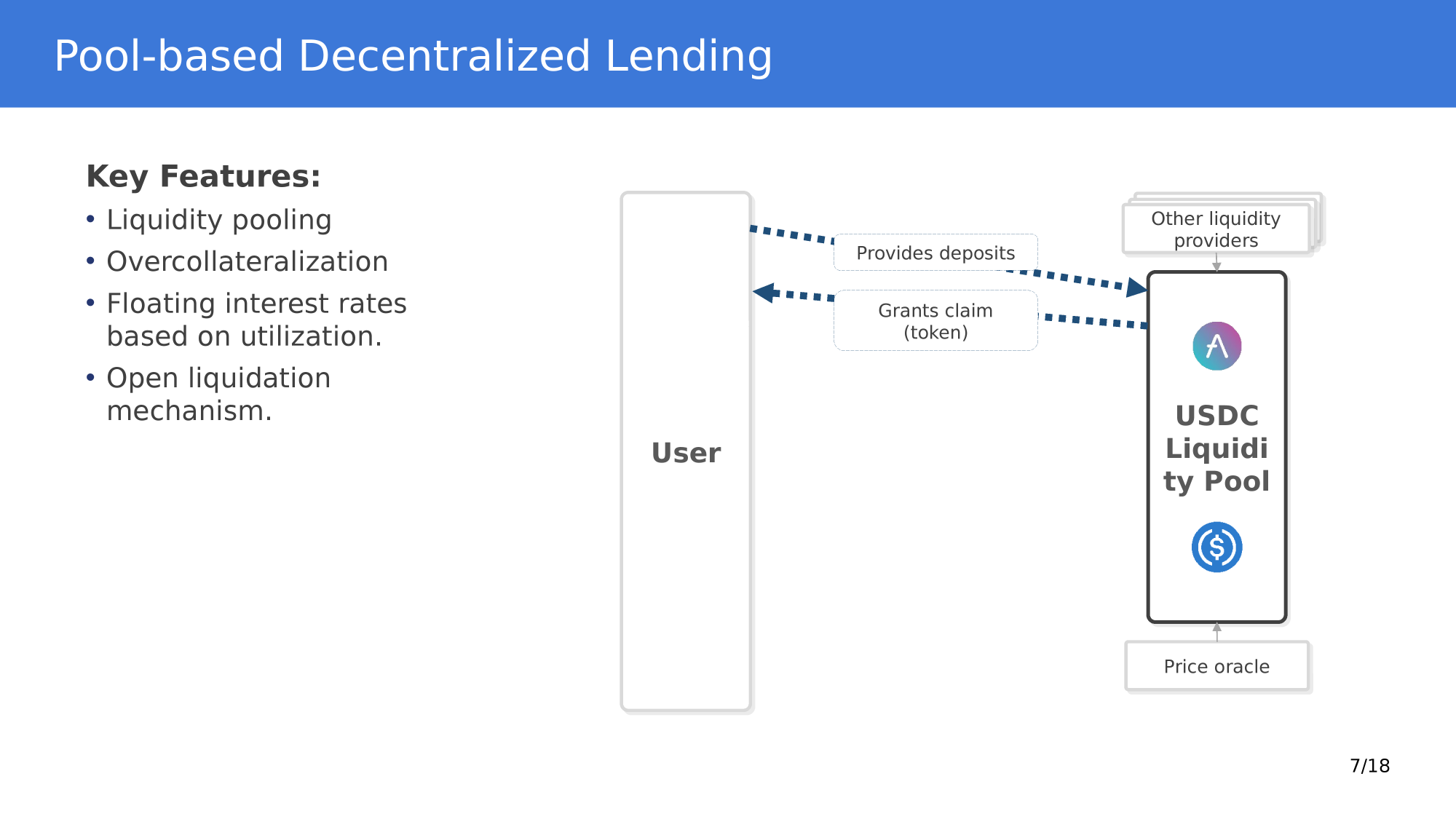

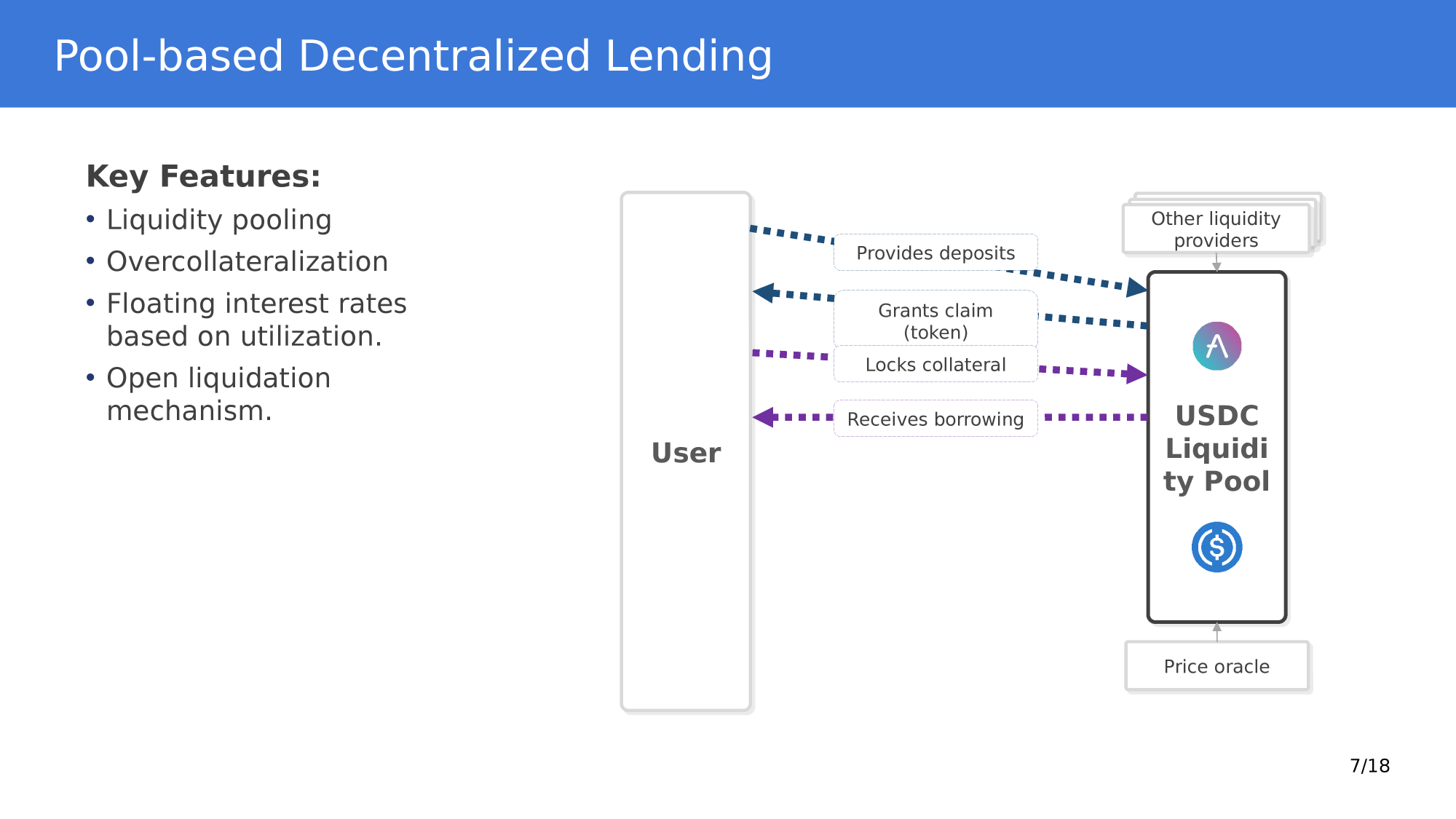

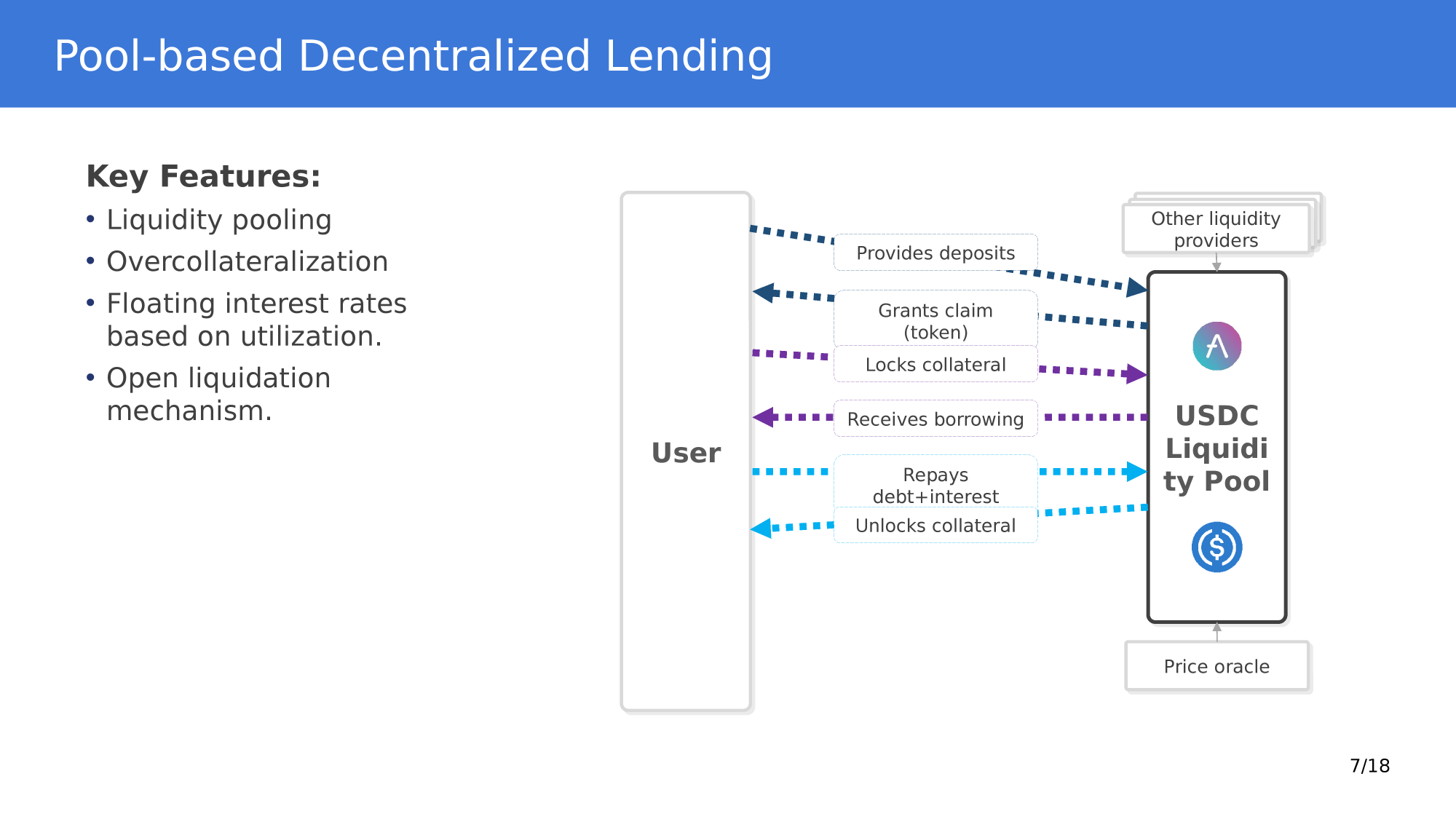

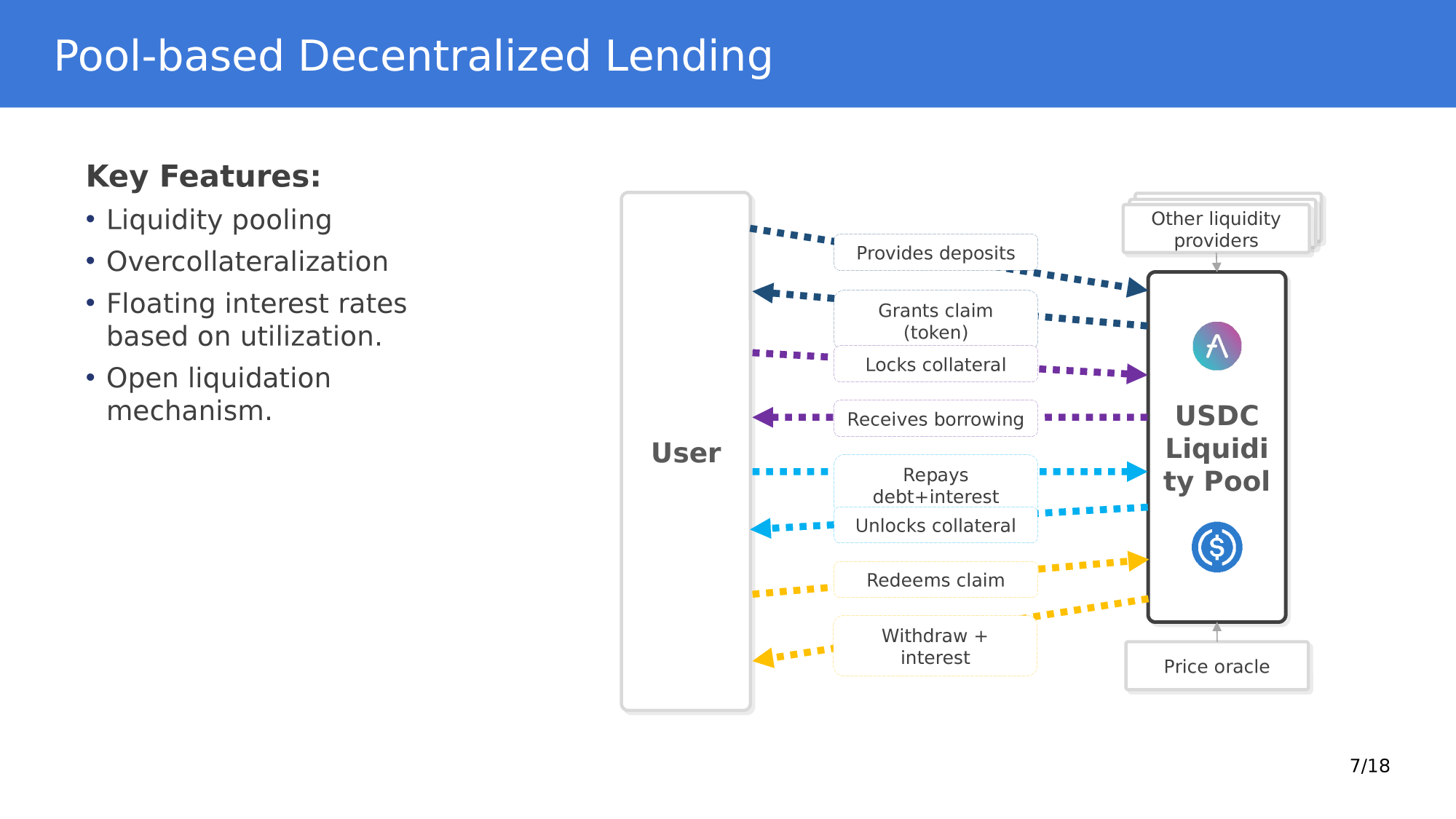

: mechanical functions

: mechanical functions

: mechanical functions

: mechanical functions

: mechanical functions

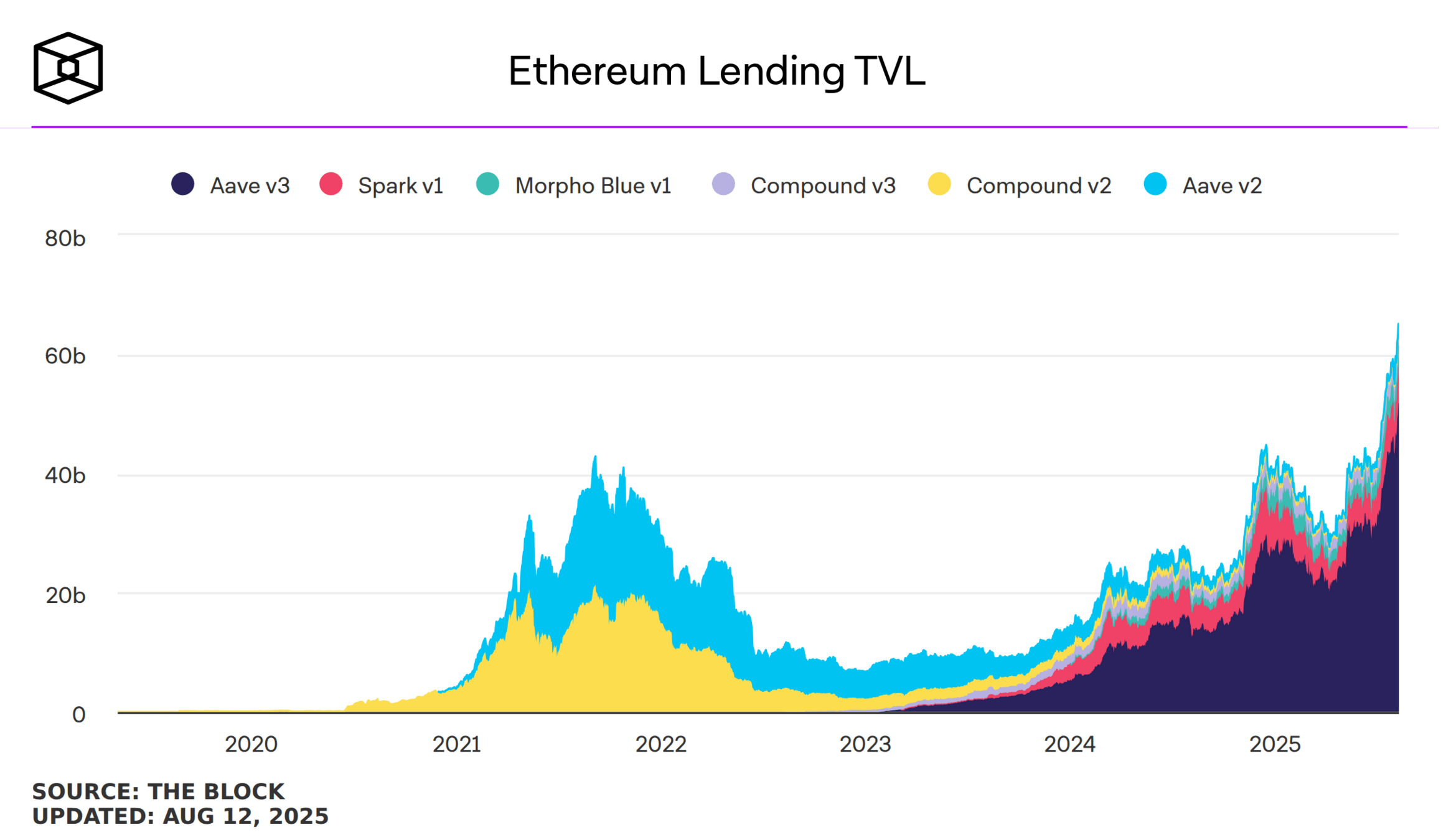

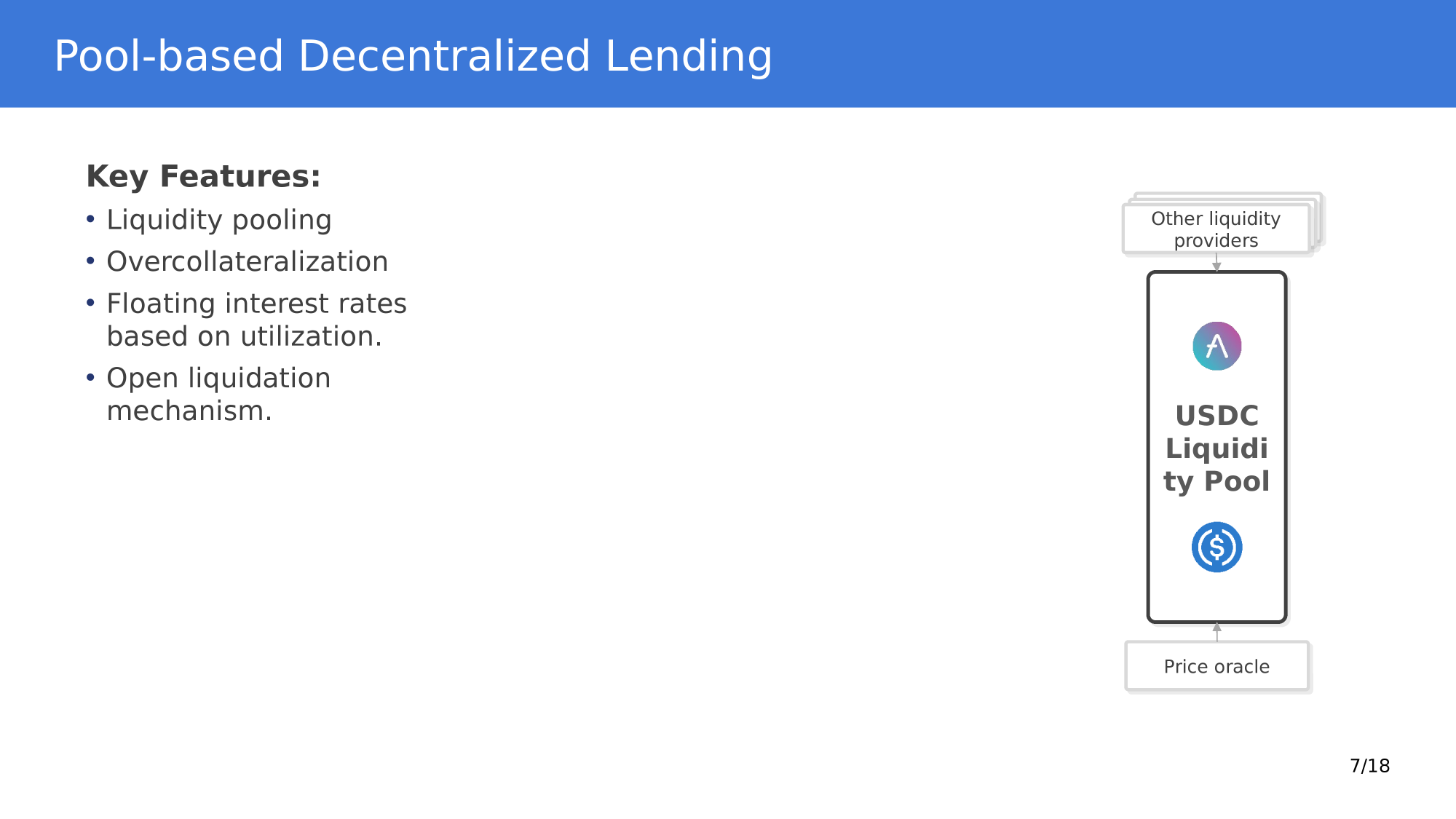

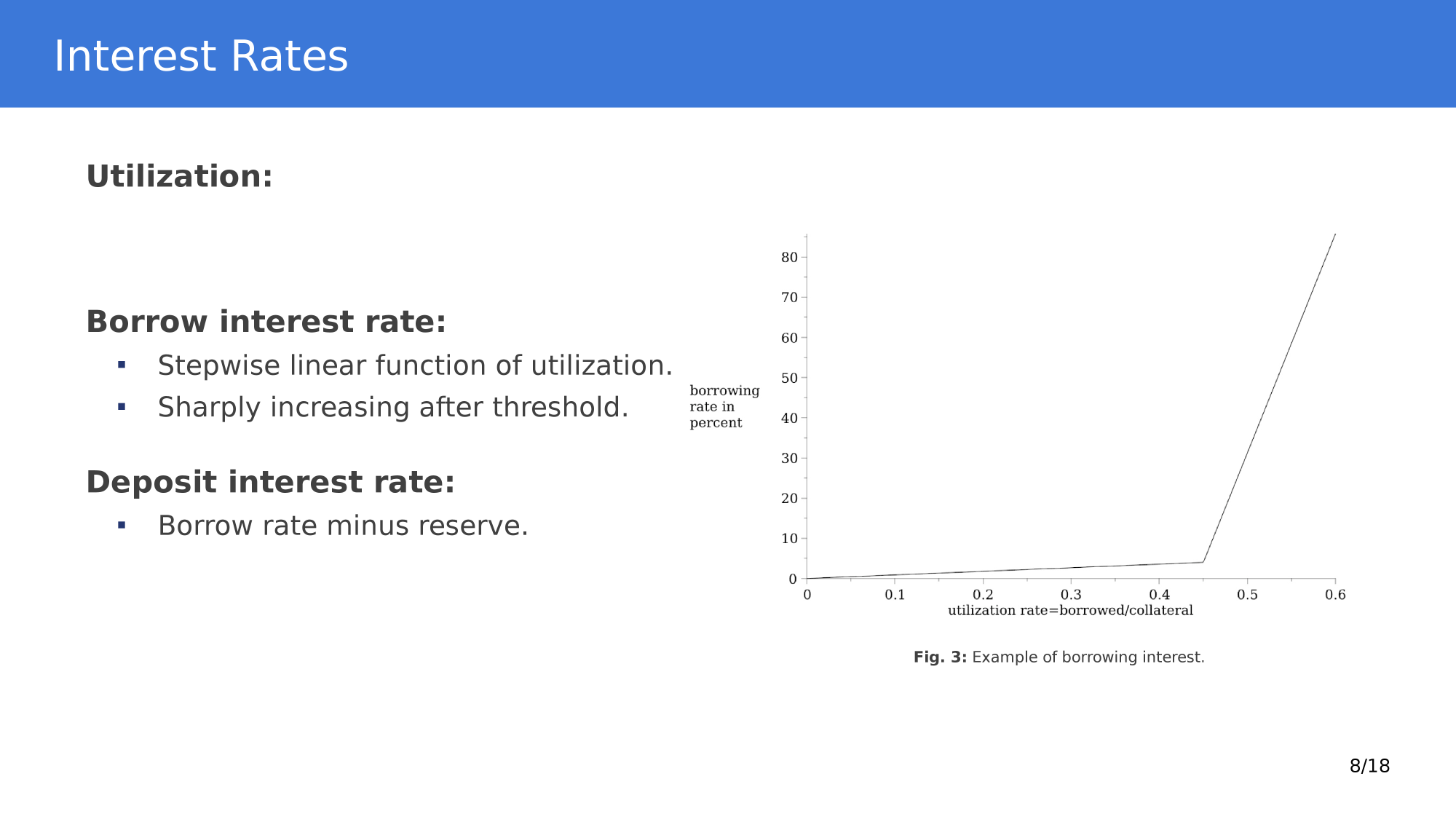

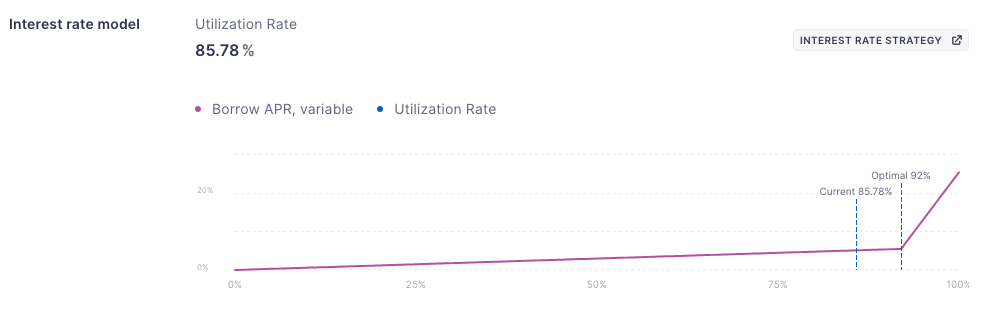

Pool-based Decentralized Lending: economic function = the price

\[U=\frac{\text{amount borrowed}}{\text{amount available}}\]

AAVE (Aug 12) for USDC

Pool-based Decentralized Lending: economic function = the price

Economists have two immediate questions

Riviera, Saleh, Vanderweyer (2025)

Stinner & Park (2025)

Pool-based Defi Lending Theory

Riviera, Saleh, Vanderweyer (2025)

Pool-based Decentralized Lending: economic function = the price

Riviera, Saleh, Vanderweyer: Results

Without uncertainty over how many people may enter the market, welfare can be made arbitrarily close to competitive equilibrium welfare.

For any admissible borrower interest rate function, there exists a unique stationary equilibrium in utilization

With uncertainty users worry about excessive rates (borrowers) or low income (lenders) => they "internalize and use the lending protocol less"

no uncertainty: Users’ informed actions reveal the market state via utilization; DLP can set rates close to competitive levels.

With uncertainty: Random shocks to credit market conditions create rate volatility; risk-averse users reduce borrowing/lending ex-ante to avoid bad outcomes, lowering utilization.

Riviera, Saleh, Vanderweyer: Translating Econ-Speak to Practice: what do we learn?

Design: Interest rate functions should heavily penalize utilization near 100% and set low rates when far below it.

Limits: No interest rate function can fully remove inefficiency if users face uncertainty.

Oracle problem: Overrated in this context — user uncertainty is the real constraint.

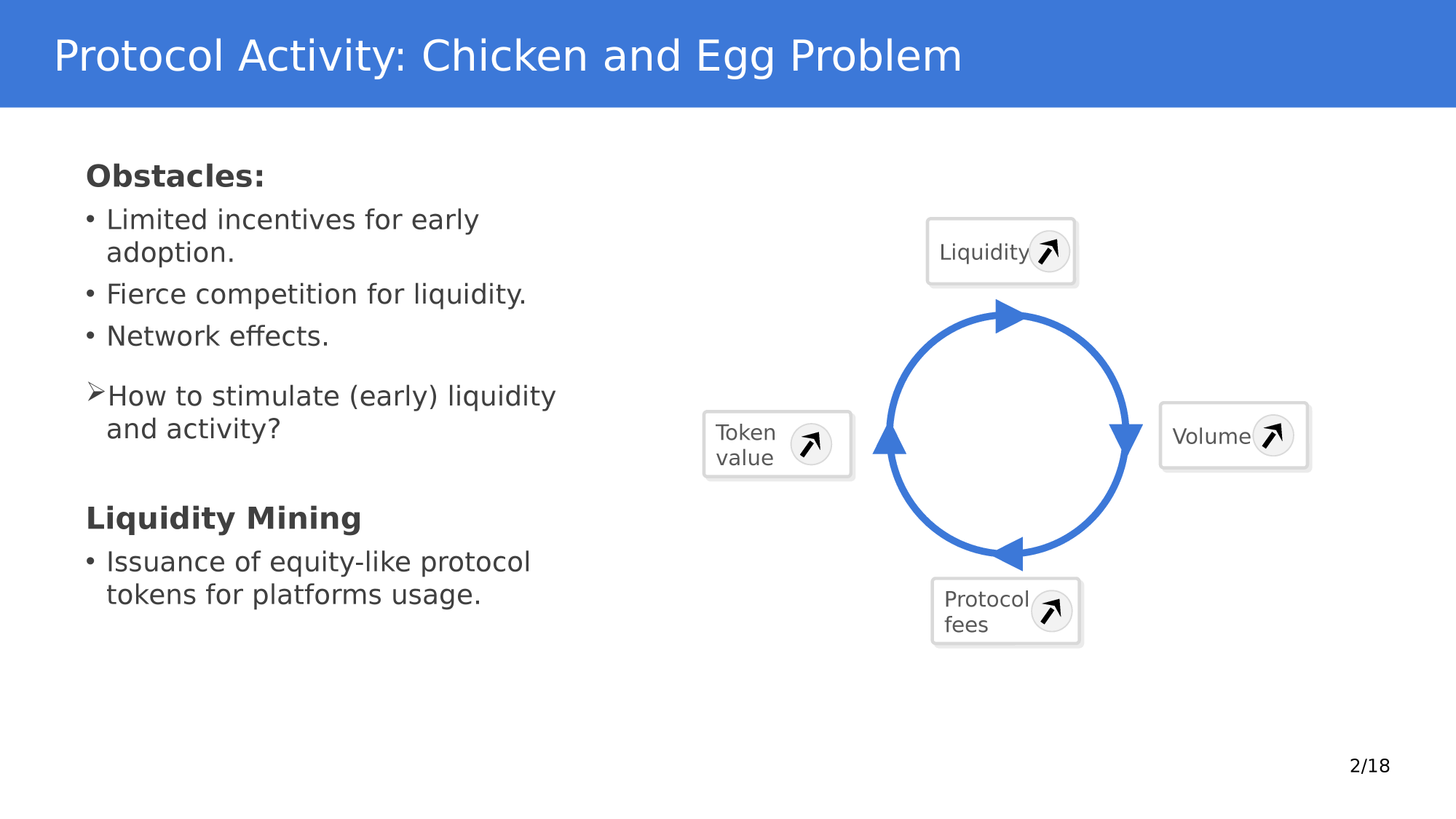

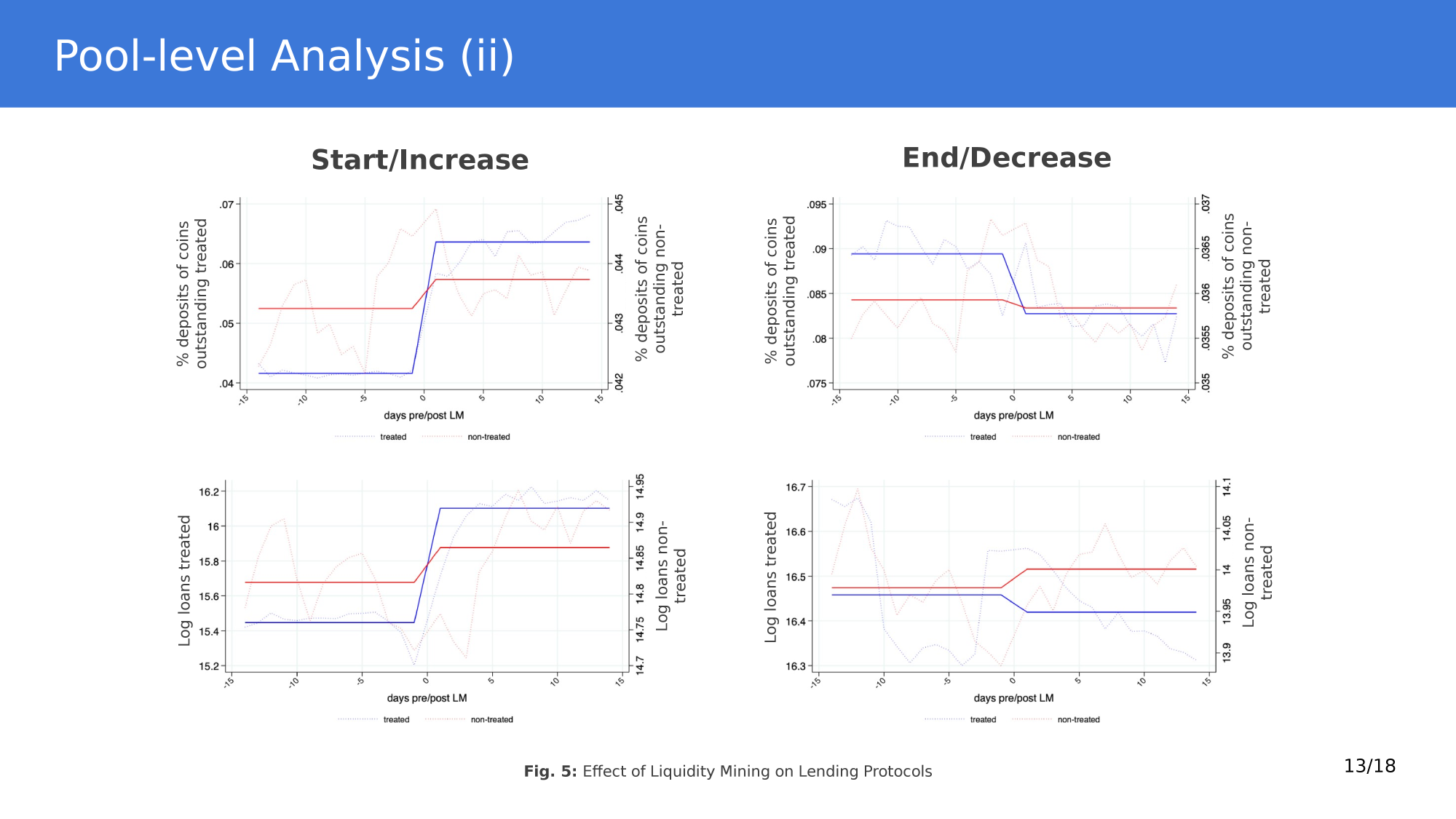

Park & Stinner (2025): Solving the Chicken and Egg Problem: Liquidity and Activity Incentives

In RSV, people show up as per model

In practice: liquidity must come first only if expect borrowers

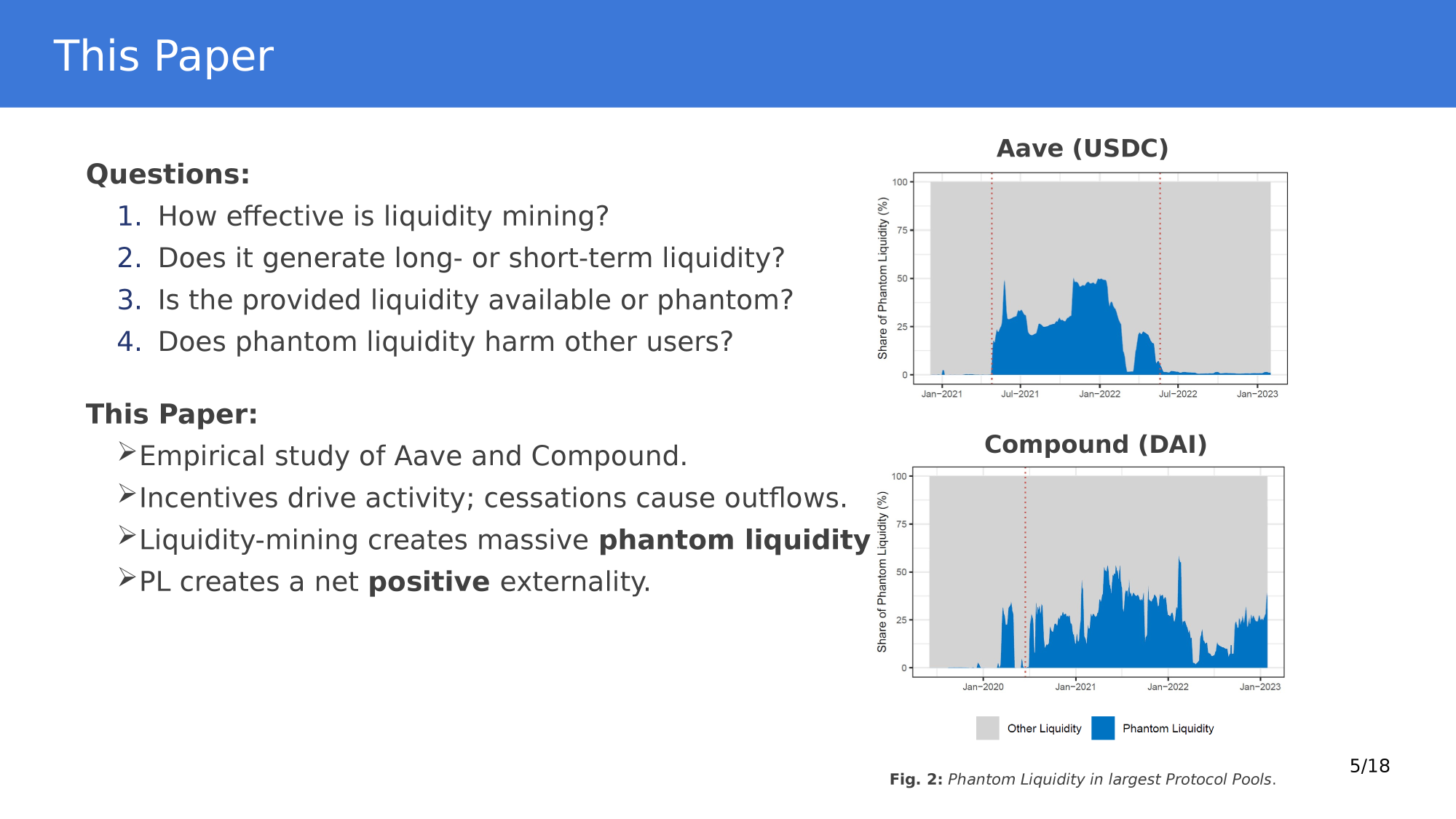

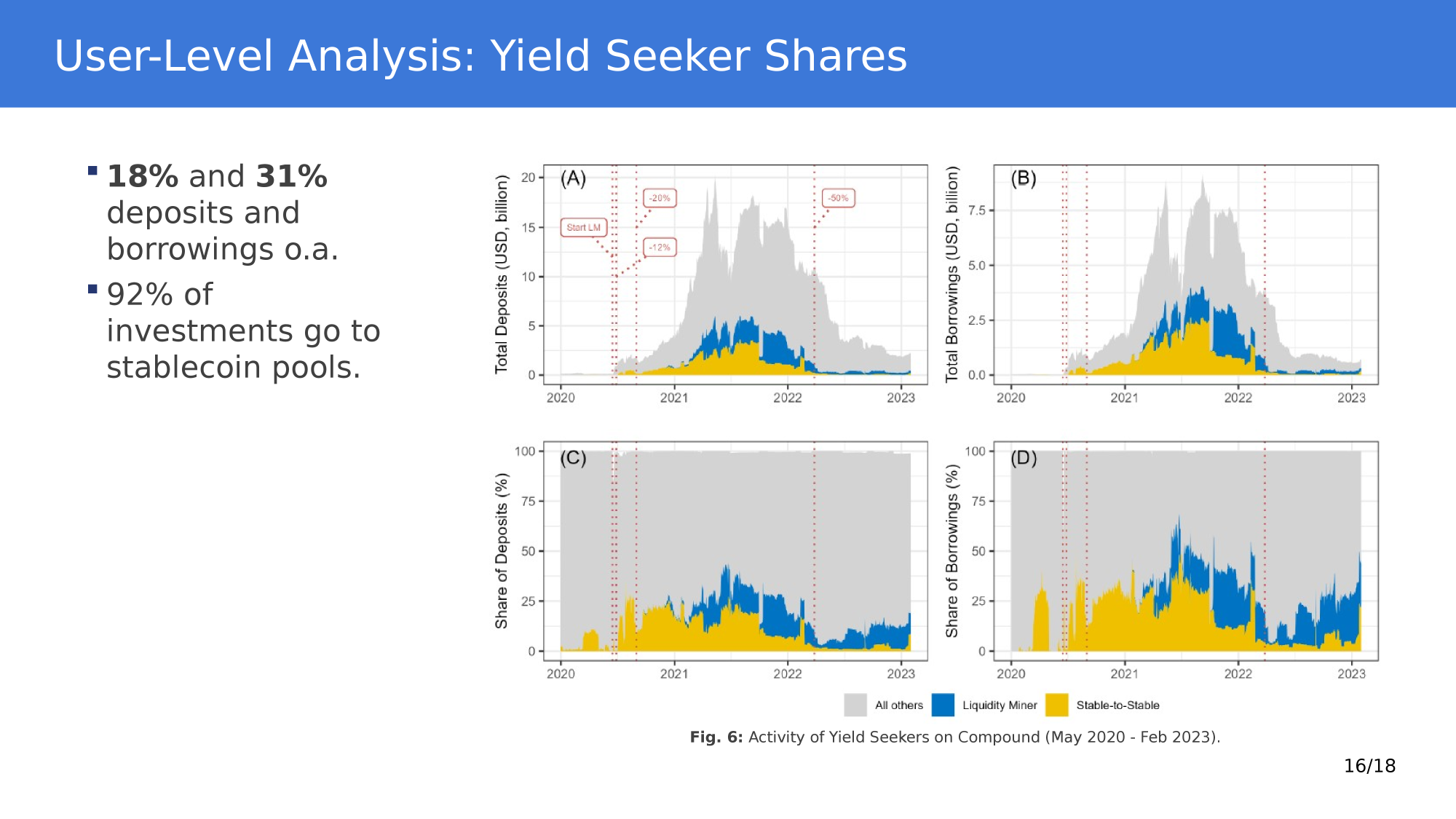

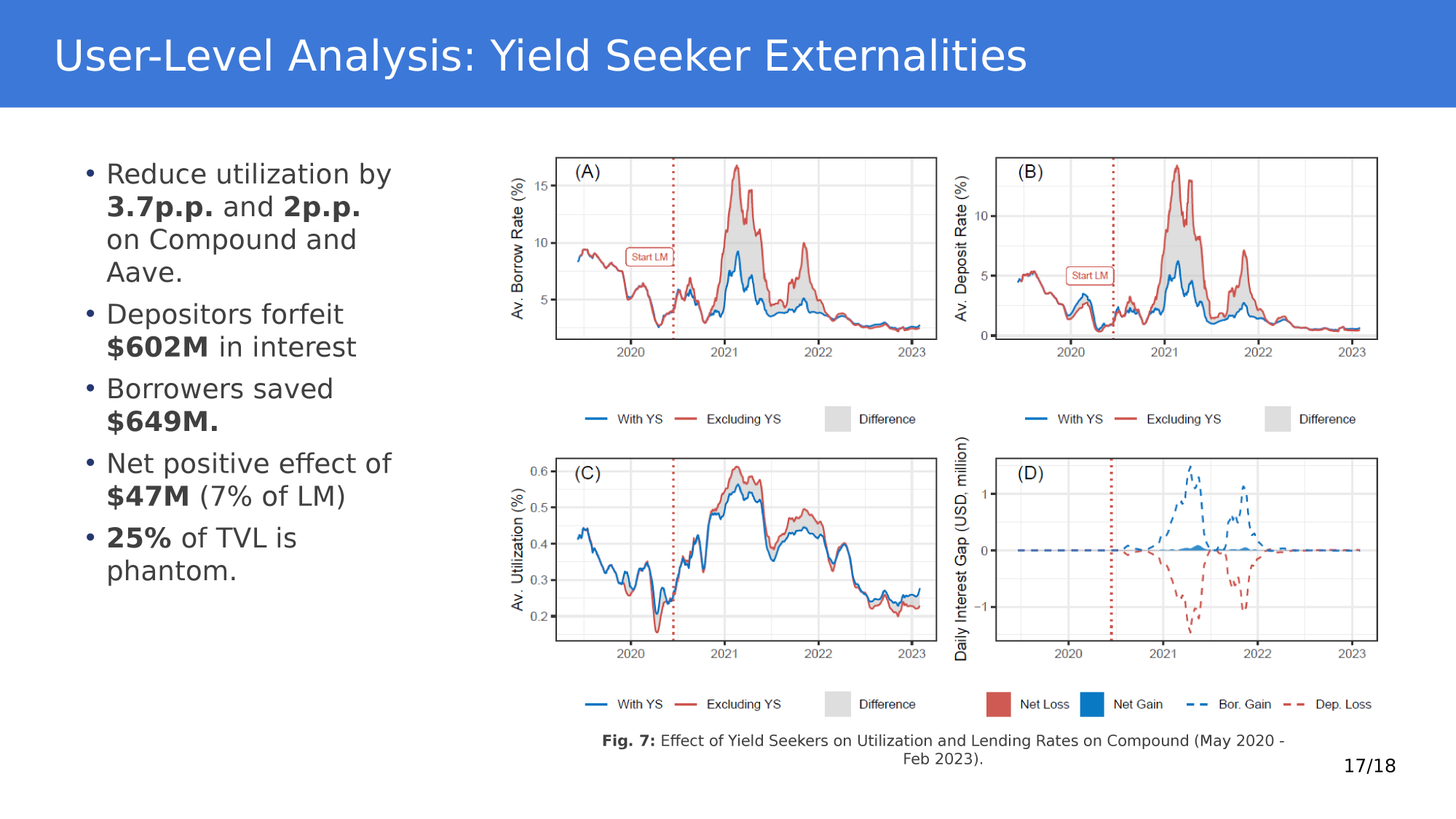

Phantom Liquidity and Externalities

\(\to\) distortion in utilization - tricky to use as "efficiency" measures as in RSV

To compare to RSV: without PLP, utilization would be higher ceteris paribus

Why economic research for defi markets matters

Why does this work matter?

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park