Andreas Park PRO

Professor of Finance at UofT

Decentralized Futures and Options Markets

Instructor: Andreas Park

Content

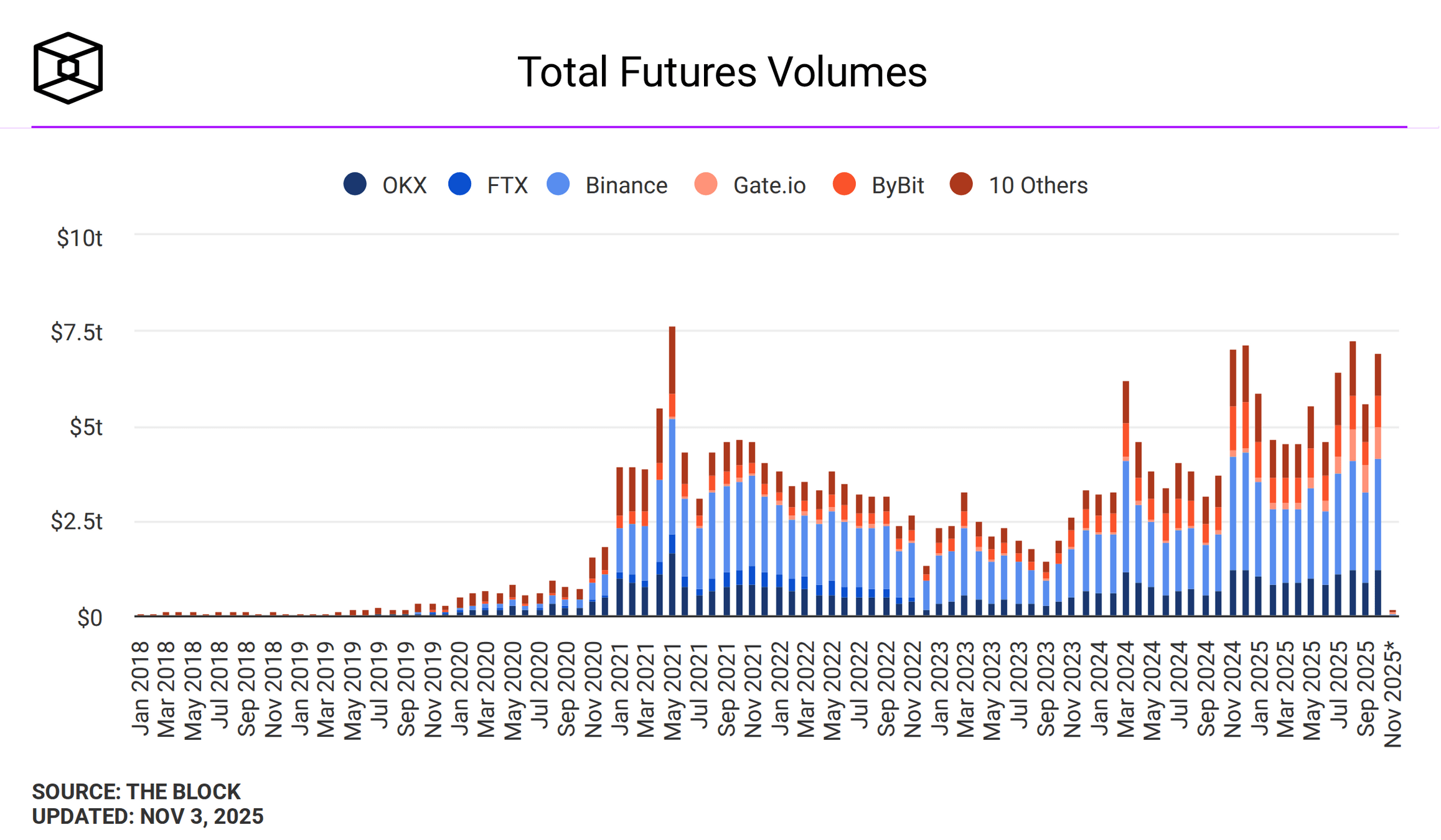

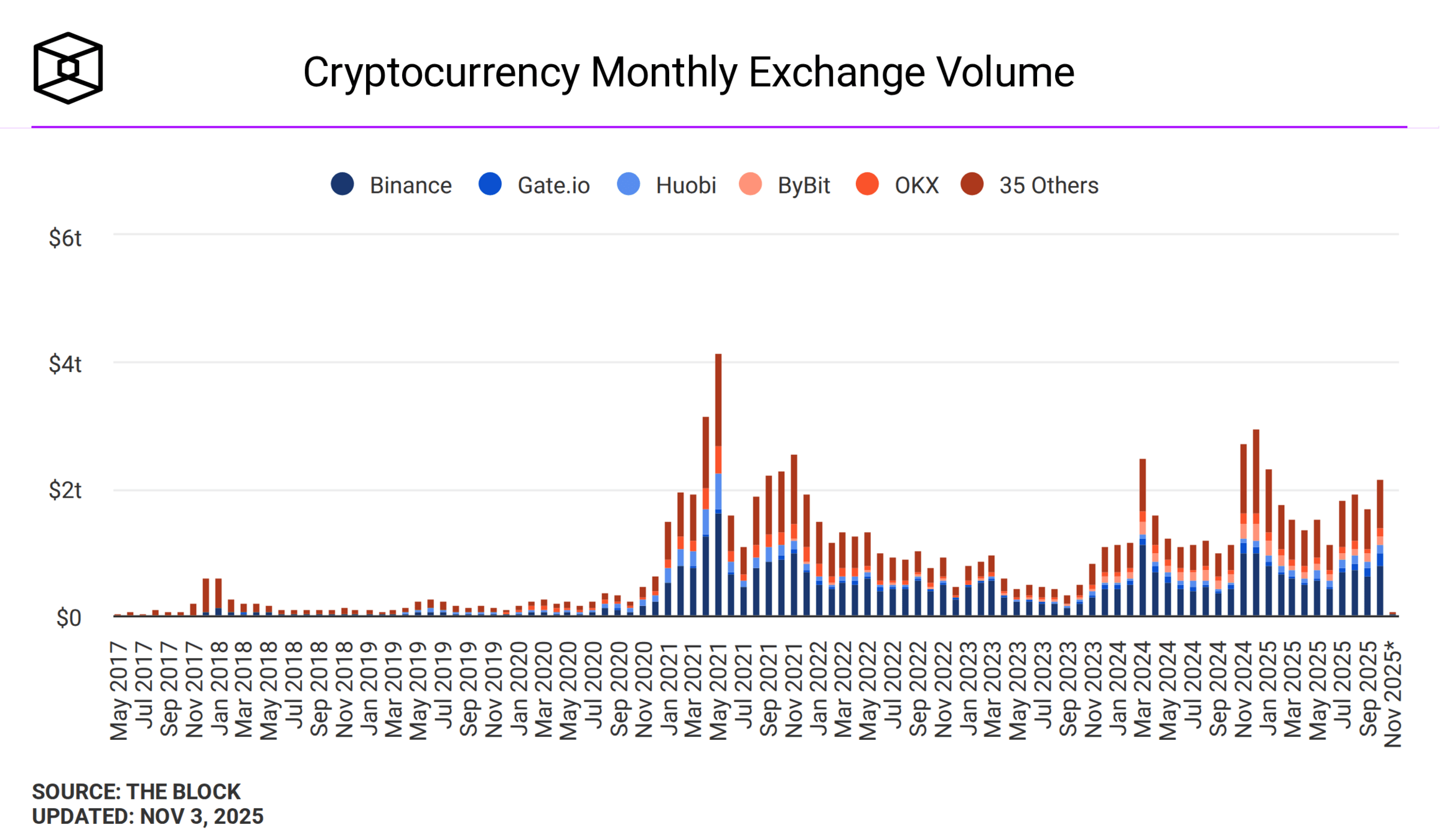

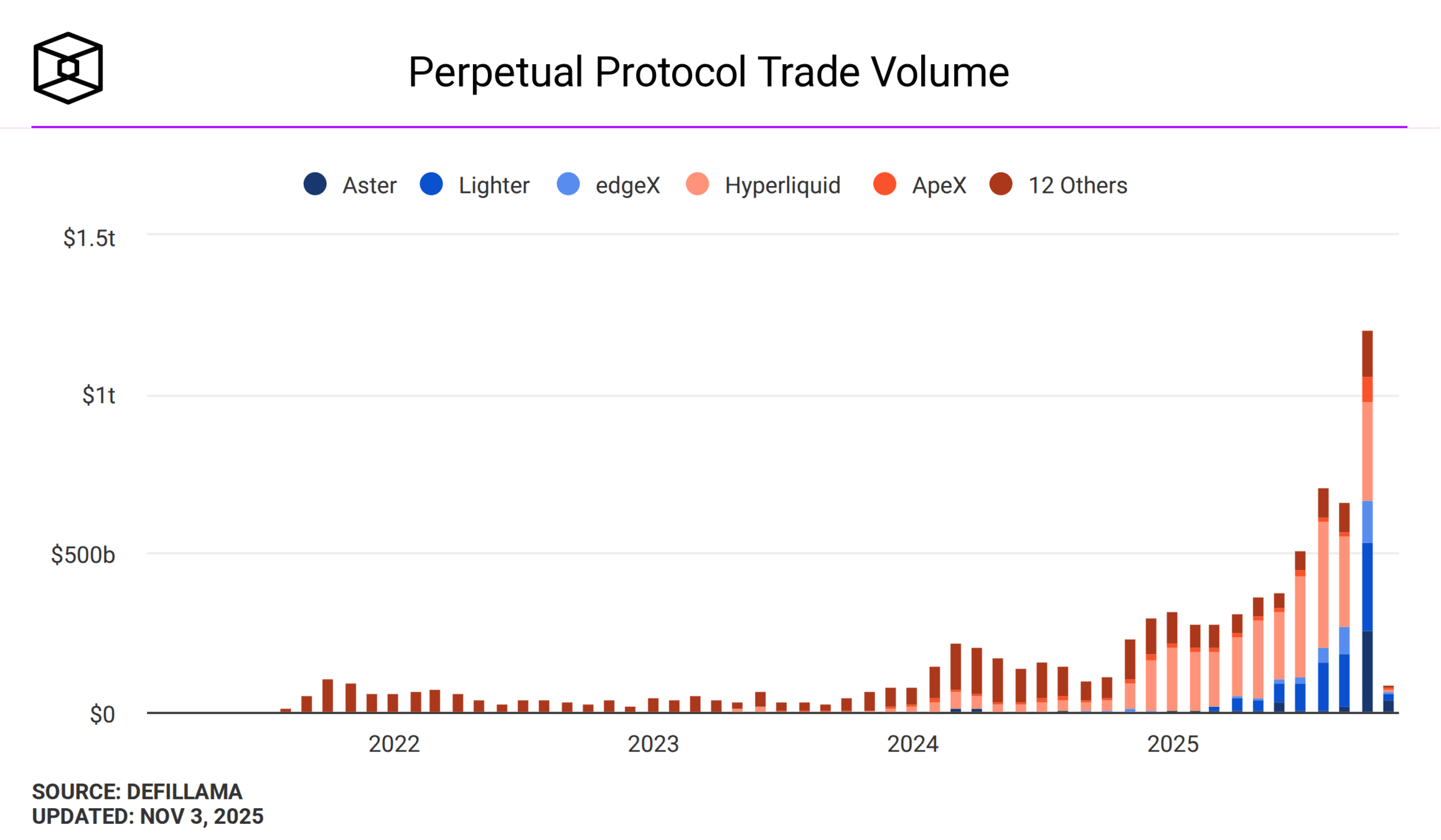

Some Data

Perpetual Futures:

Centralized (Derebit/BitMEX/Binance) and Decentralized (Hyperliquid)

Forward (OTC)

Futures (Exchange-Traded)

| Spot Move | Leverage | Change in Futures P&L on Margin | Comment |

|---|---|---|---|

| +5 % | 1× | +5 % | Same as spot |

| +5 % | 5× | +25 % | Gains magnified |

| +5 % | 10× | +50 % | Gains amplified further |

| –5 % | 10× | –50 % | Same magnification on losses |

| –10 % | 10× | –100 % | Position wiped out (liquidation) |

Positive basis (futures > spot) → market in contango.

Negative basis (futures < spot) → market in backwardation.

Funding

Setup

Price + 2 % → $10 200

Price – 2 % → $9 800

Isolated Margin

Cross Margin

| Collateral | Margin Currency | Volatility Impact |

|---|---|---|

| USDC | Stable | Margin value fixed |

| ETH | Volatile | Margin value fluctuates; can fall as ETH price drops |

Scenario:

Trader A long 1 BTC (cross) with USDC collateral.

Trader B long 1 BTC (isolated) with ETH collateral.

Index = $10 000, Initial = 10 %.

| Case | A (USDC, Cross) | B (ETH, Isolated) |

|---|---|---|

| ETH – 10 % | Margin still $1 000 | Margin falls ≈ $900 (ETH value drop) |

| BTC – 5 % | Equity = $500 loss, covered by other balances | Equity = $500 loss → may liquidate (isolated) |

| Combined shock | Cross uses all balance; Isolated liquidates this position only |

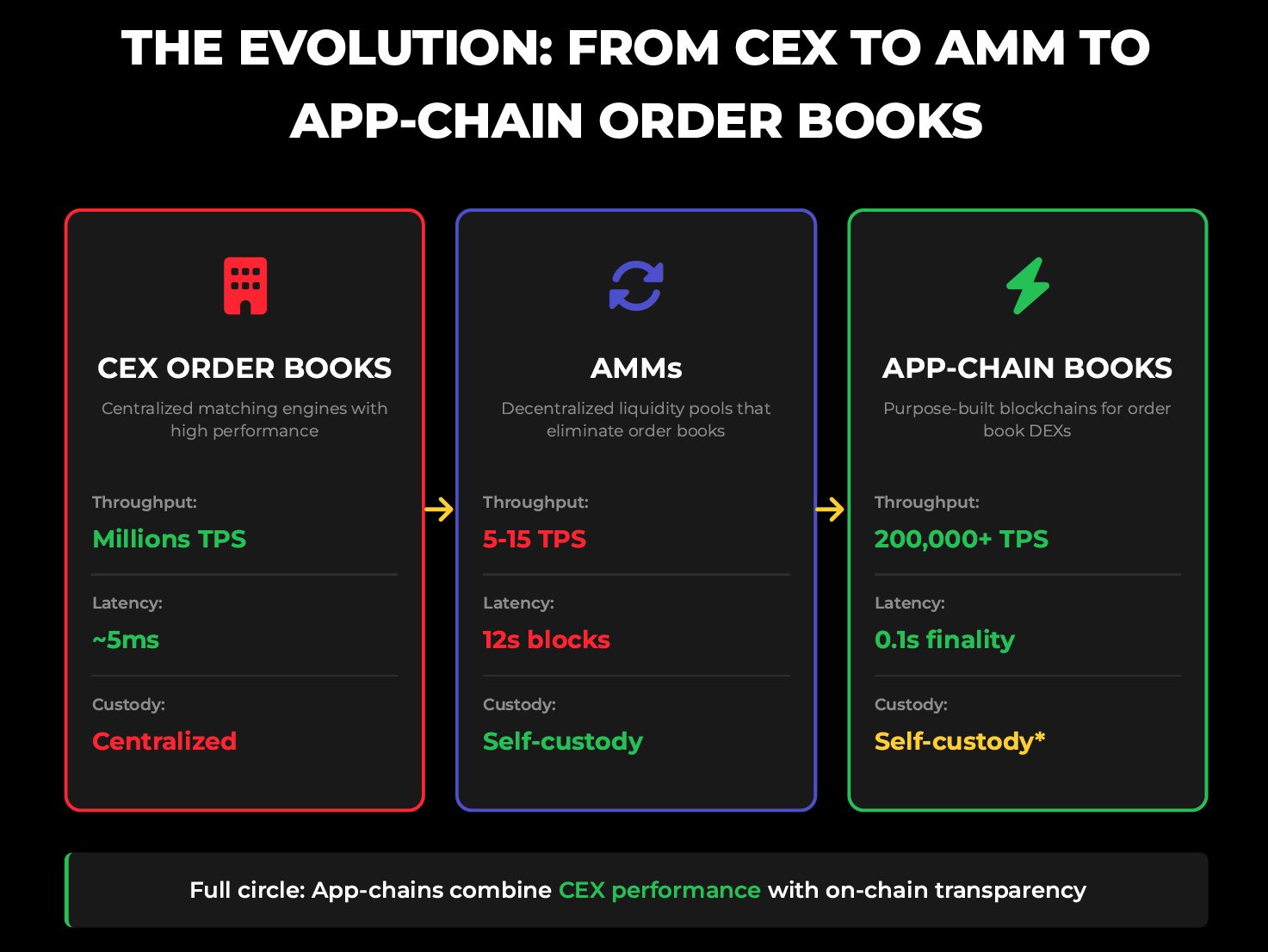

| Feature | Binance (Centralized) | Hyperliquid (On-Chain) |

|---|---|---|

| Matching | Central server engine | Smart-contract order book |

| Custody | Exchange holds collateral | User retains custody on-chain |

| Counterparty | Exchange is CCP | Protocol smart contract as clearing layer |

| Funding | Exchange computes & nets | On-chain funding redistributes automatically |

| Liquidation | Managed by exchange engine | Triggered by contract logic; backed by protocol insurance |

| Margin modes | Cross / Isolated | Cross / Isolated |

| Funding interval | 8 h (1 h if capped) | 1 h default |

Key takeaway: even with an on-chain order book, funding and liquidation remain pooled, not bilateral.

Decentralized Options: Aevo/Lyra

Assume:

| ETH at Expiry | Option Payout | Vault P&L | Final Vault Value |

|---|---|---|---|

| 2 200 USDC | 2 000 | –1 000 | 9 000 |

| 1 800 USDC | 0 | +1 000 | 11 000 |

LP withdraws collateral proportionally after expiry.

GreekSymbolMeaningInterpretation

| Delta | \( \Delta\) | ∂Price/∂Underlying | change in option price for a $1 move in the underlying |

| Gamma | \(\Gamma \) | ∂Δ/∂Underlying | curvature; how Delta changes with price |

| Vega | \( \nu \) | ∂Price/∂Volatility | sensitivity to implied volatility |

| Theta | \( \Theta\) | ∂Price/∂Time | time decay; loss of value as expiry nears |

| Feature | OCC (Traditional) | Aevo / Lyra (On-Chain) |

|---|---|---|

| Collateral Basis | Partial — margin equals estimated portfolio risk (SPAN) | Full — 100 % collateralization of notional exposure |

| Offsets / Netting | Allowed across related positions | None; each vault independent |

| Leverage | Moderate; efficient use of capital | None; fully funded |

| Counterparty Risk | Mutualized through clearinghouse fund | Virtually none (smart-contract enforcement) |

| Capital Efficiency | High — lower margin requirements | Low — higher locked capital |

| Residual Risk | Credit and operational (clearing members) | Protocol, oracle, and contract risk |

| Collateral Type | Cash, Treasuries, or approved securities | Stablecoins (e.g., USDC) held on-chain |

Interpretation

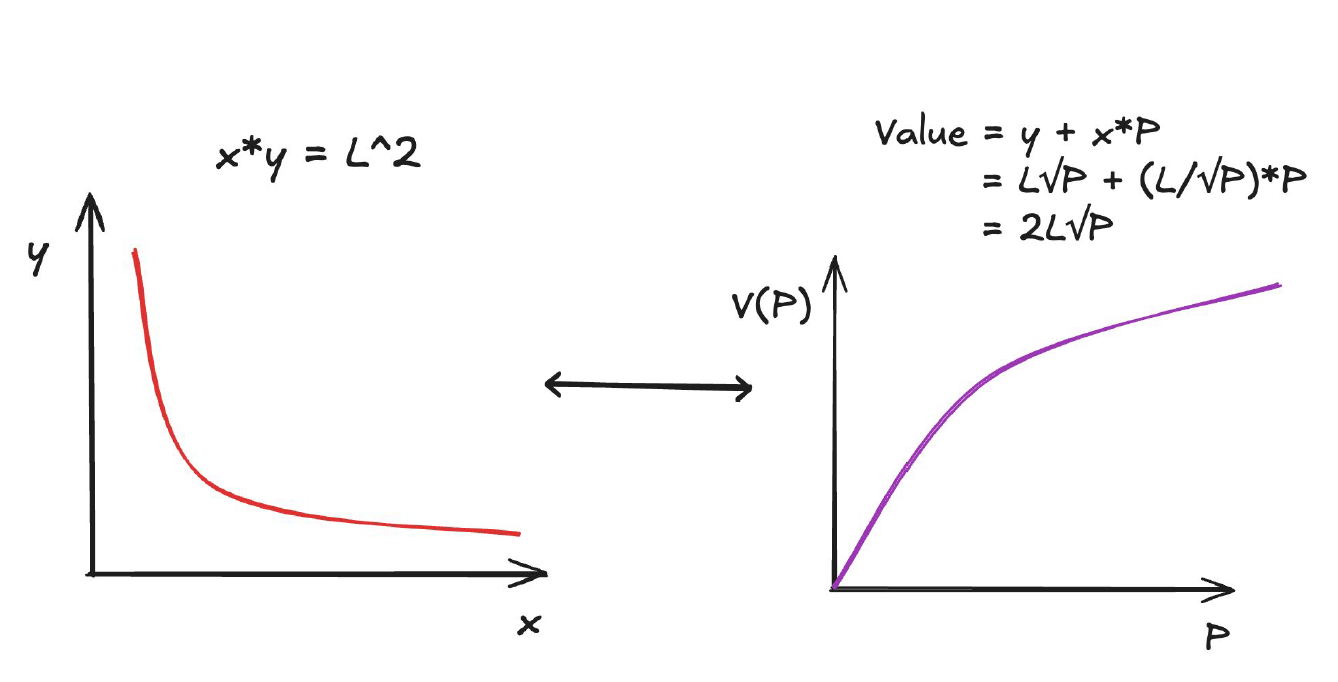

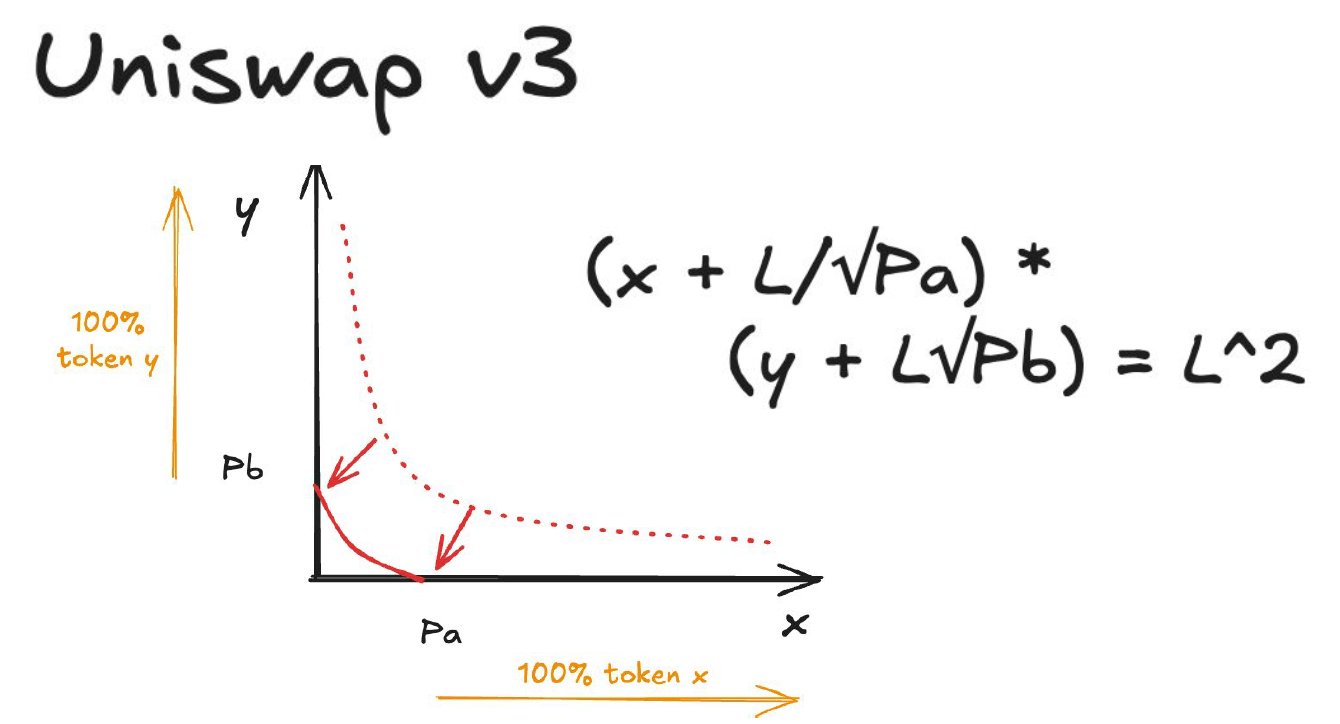

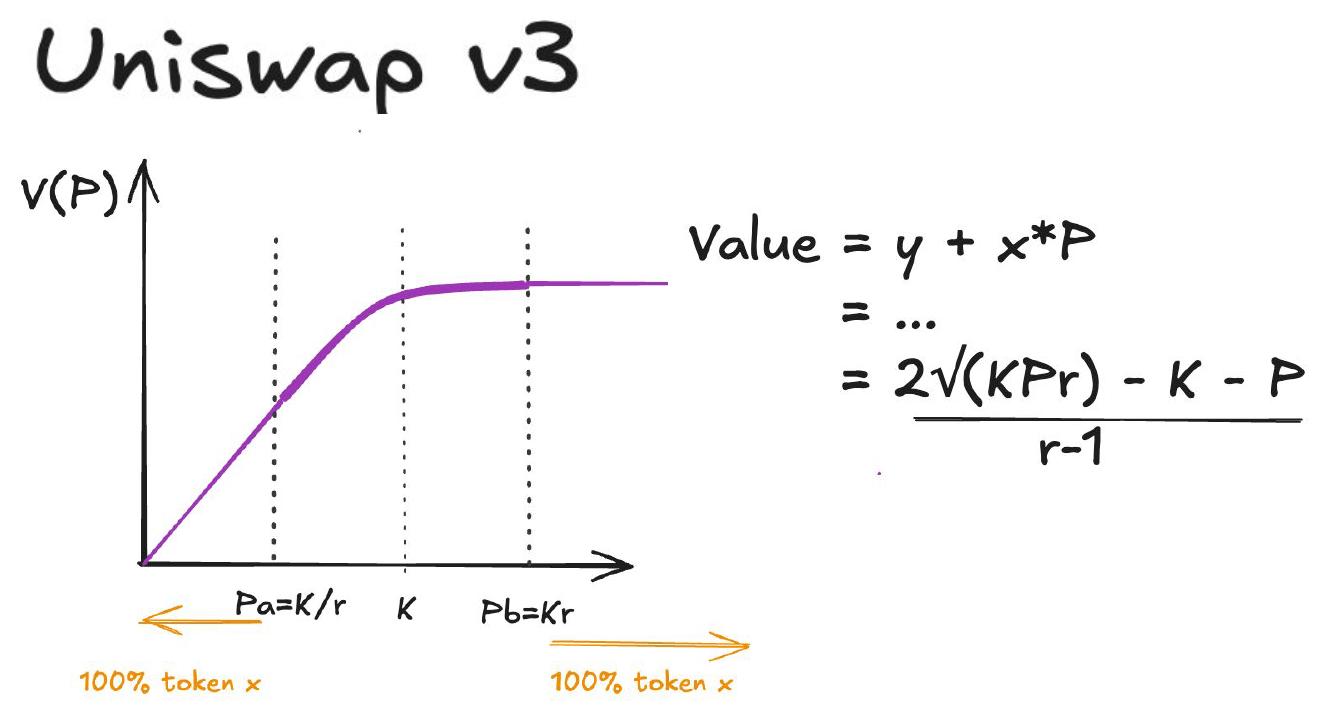

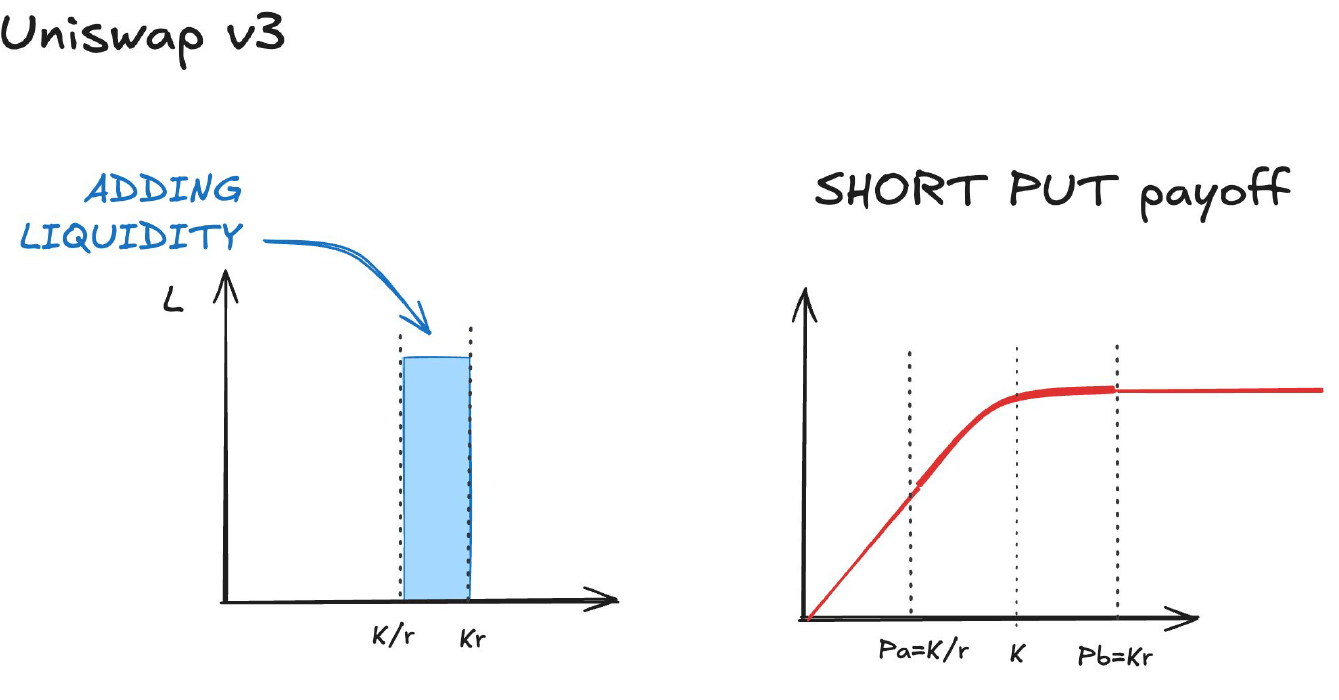

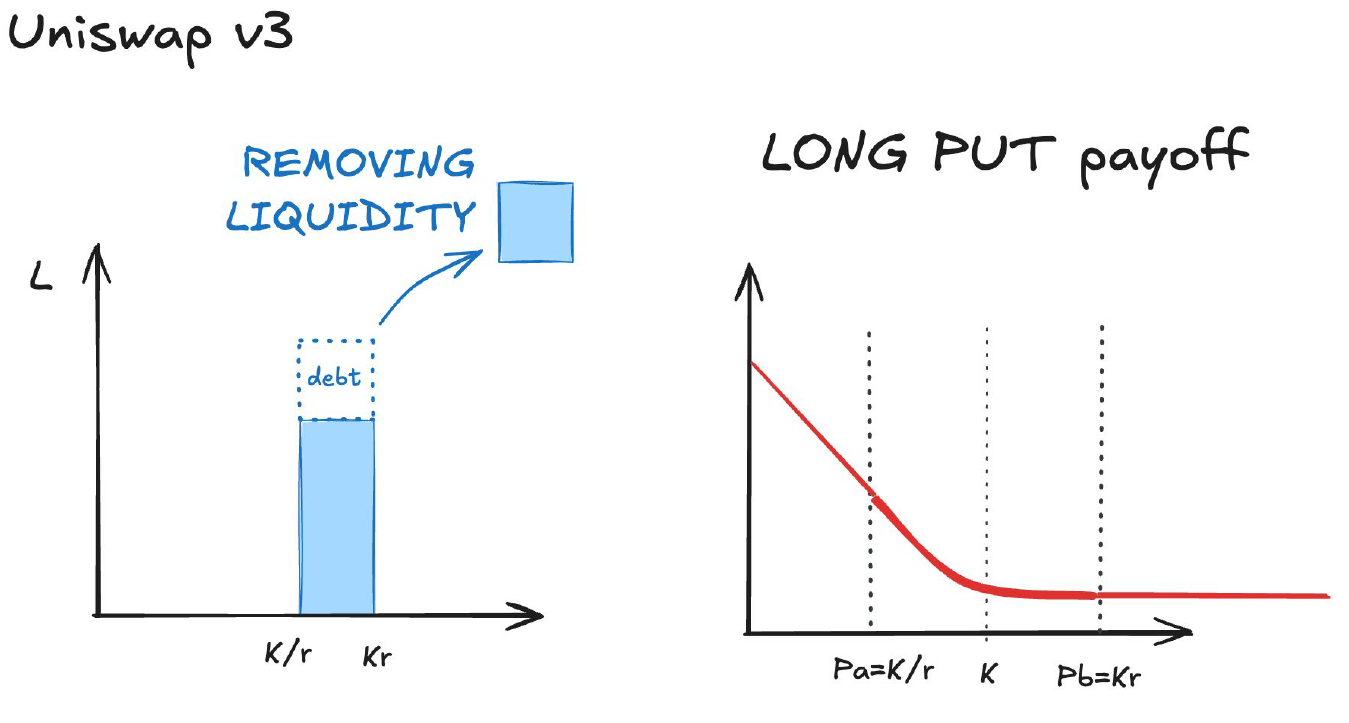

Decentralized Options: Panoptic

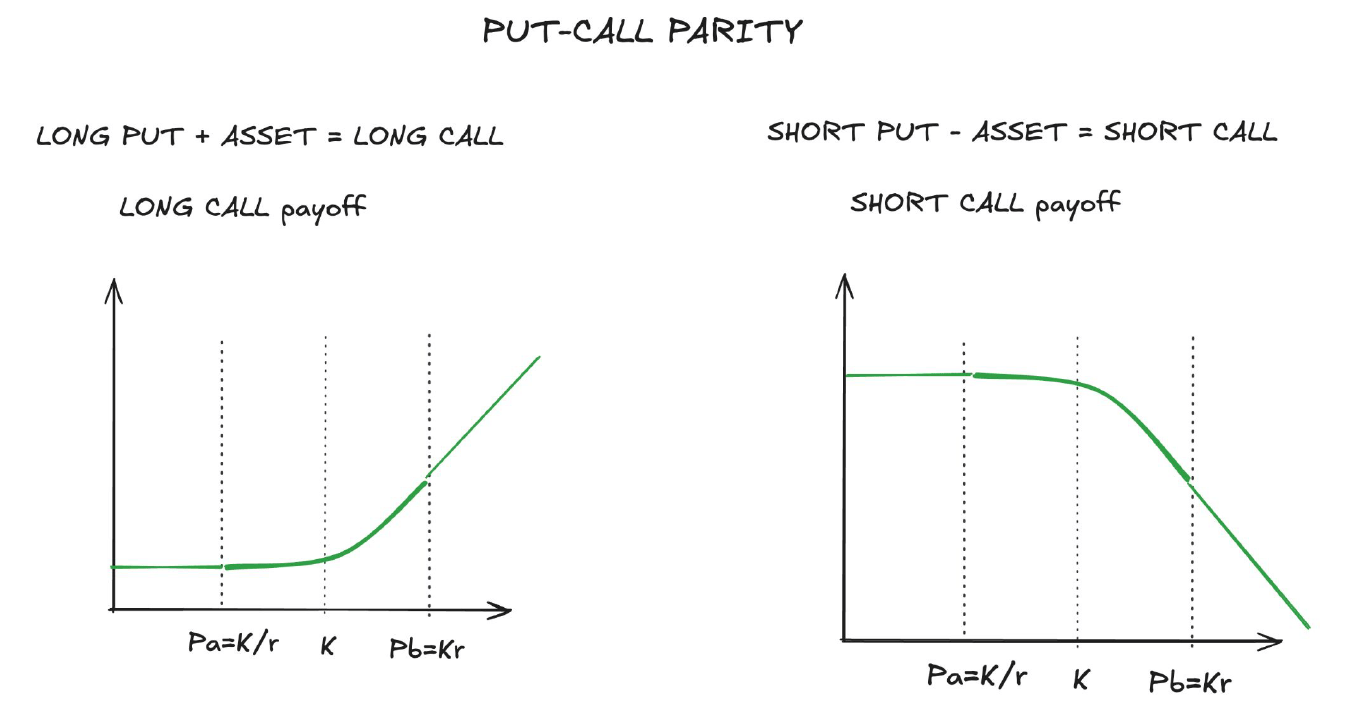

short put = short call + asset = covered call

-long call = - long put - asset = covered put

Price RegionToken CompositionOption AnalogueExposure Type

| Below lower bound \(P_a\) | All base token, no quote token | Covered Put | You hold the asset; limited downside |

| Within range \([P_a, P_b]\) | Mix of both tokens | Short Straddle / Short Put (locally) | Short volatility — concave payoff |

| Above upper bound \(P_b\) | All quote token, no base token | Covered Call | Sold upside; capped gain |

\(\Rightarrow\) they become an options clearing house

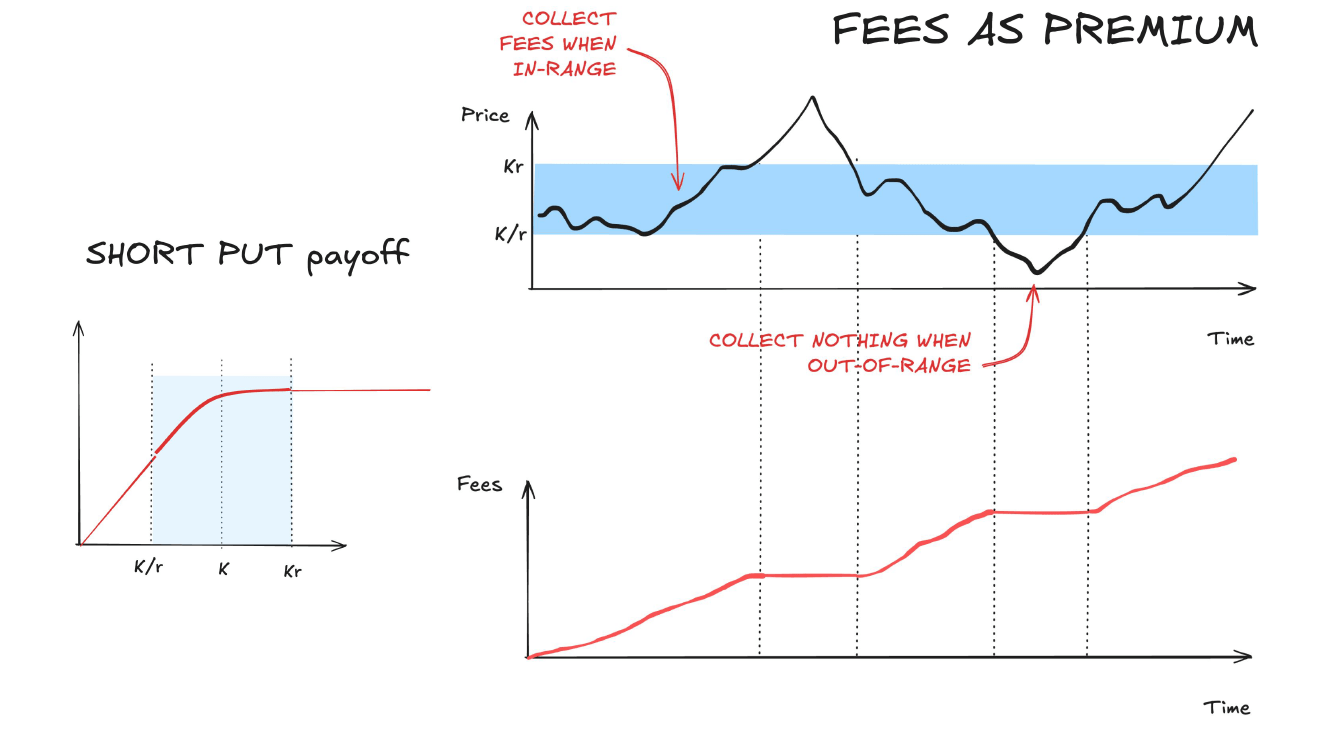

LPs in Panoptic earn two income streams:

\[ \text{Total Yield} = \text{Uniswap Swap Fees} + \text{Panoptic Option Premiums} - \text{Hedging Costs}. \]

This dual-income model compensates LPs both as market-makers and as option writers.

| Feature | Aevo (ex-Lyra) | Panoptic |

|---|---|---|

| Market Type | Discrete-expiry options (European style) | Perpetual options (no expiry) |

| Underlying Mechanism | AMM-based options backed by Market Maker Vaults (MMVs) and delta-hedged via perps | Built directly on Uniswap v3 liquidity ranges (CLAMMs) |

| Collateral Model | Fully collateralized MMVs (100 % backing, no leverage) | Uses Uniswap LP collateral plus trader margin on-chain |

| Hedging | Dedicated delta pool trades underlying assets externally | Continuous rebalancing within the AMM (automatic) |

| Income to LPs | Option premiums + hedging profits (via AMM) | Uniswap swap fees + option premiums from Panoptic traders |

| Exposure Type | LPs short Vega and Delta (managed by hedging pool) | LPs short Gamma (volatility); traders can buy convexity |

| Settlement | Expiry-based exercise and settlement | Continuous mark-to-market; perpetual funding mechanism |

| Capital Efficiency | Lower (full collateral) | Higher (shared AMM liquidity) |

| Main Analogy | OCC-style clearinghouse with on-chain automation | On-chain options clearinghouse embedded in Uniswap v3 |

Summary

Spot paths at day 30 (illustrative, no fees outside range):

| (S_{30}) | Inside range? | LP inventory effect (short-gamma) | Net (qualitative) |

|---|---|---|---|

| 1,900 | Yes | Bought ETH as it fell (adverse) | Fees + premium vs inventory loss; sign depends on realized vol |

| 2,000 | Yes | Minimal inventory change | Fees + premium dominate → positive |

| 2,300 | No (above (P_b)) | All quote; upside capped | Keep fees + premium; no further upside |

Payout intuition at day 30 (ignoring path costs):

Numerical sketch (example, marking to range convexity):

| (S_{30}) | Move | Long-option convex P&L (example) | Premium | Net |

|---|---|---|---|---|

| 1,900 | –5% | +400 | –300 | +100 |

| 2,000 | 0% | ~0 | –300 | –300 |

| 2,300 | +15% (out of range) | +700 | –300 | +400 |

Numbers illustrate the idea: the long option benefits when realized volatility is high; the LP (short option) benefits when price stays within the range and fee + premium exceed inventory losses.

By Andreas Park

The deck covers crypto futures and options markets