Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park & Zissis Poulos

Rotman – MBA

A tumultuous 12 months

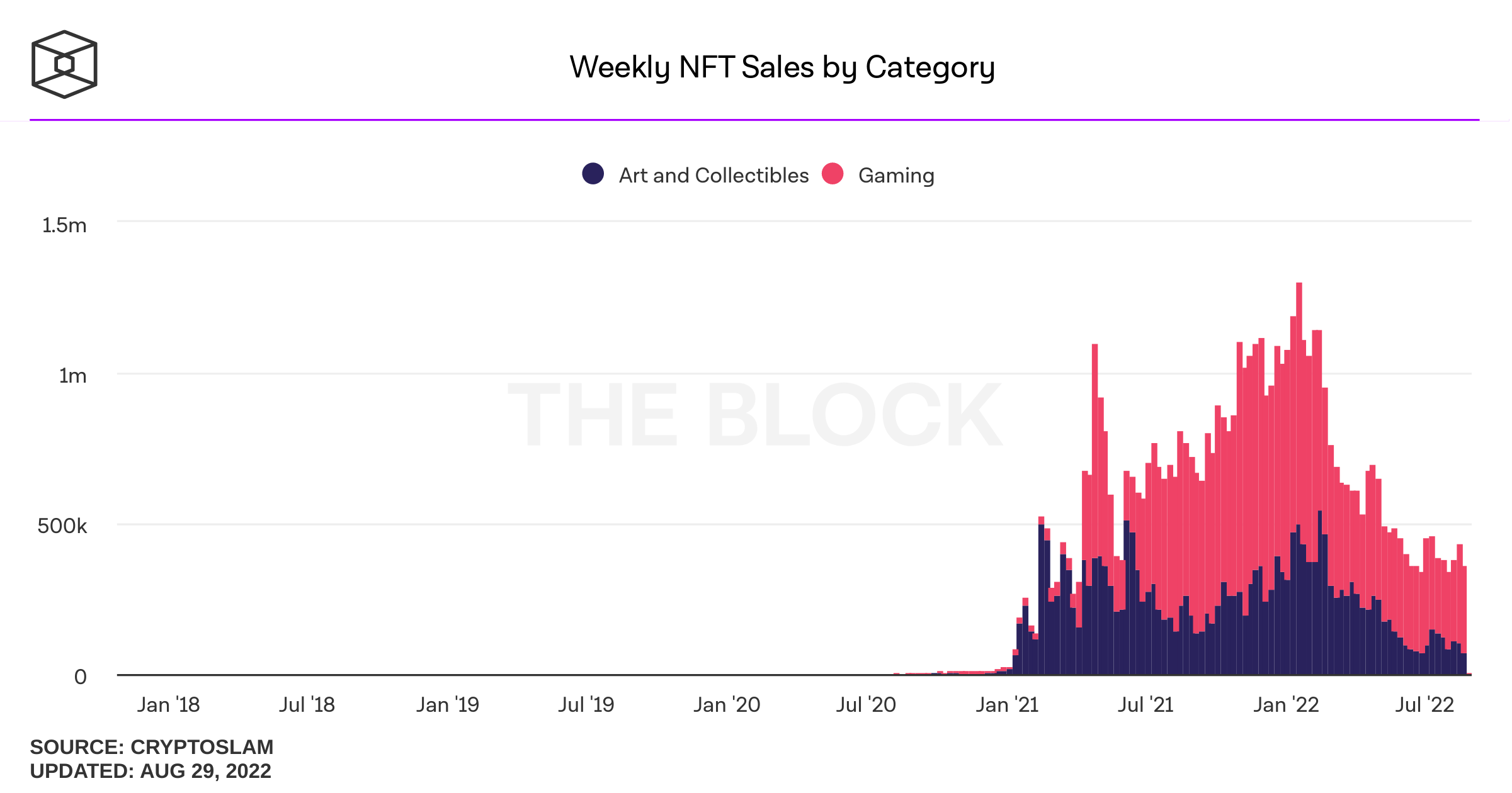

The NFT Boom

The NFT Boom & Crash

The Terra Implosion

UST Stablecoin

LUNA (cryptocurrency of the TERRA network)

A timeline

May 7: selling pressure on UST from Curve withdrawals

May 12: LUNA and UST at $0.01

June 27: Three Arrows Capital ordered to liquidate

June 12: Celsius Network suspends withdrawals

July 13: Celsius files for Chapter 11

July 6: Voyager Digital files for Chapter 11

July 4: Vault suspends withdrawals

Three Arrows Capital lost >60% of value and faces numerous margin calls that they did not react to

The Aftermath:

is crypto dead or dying?

Cryptomarket Crash

bitcoin

ETH

-70%

-60%

Consequences of the Crash?

Some Questions

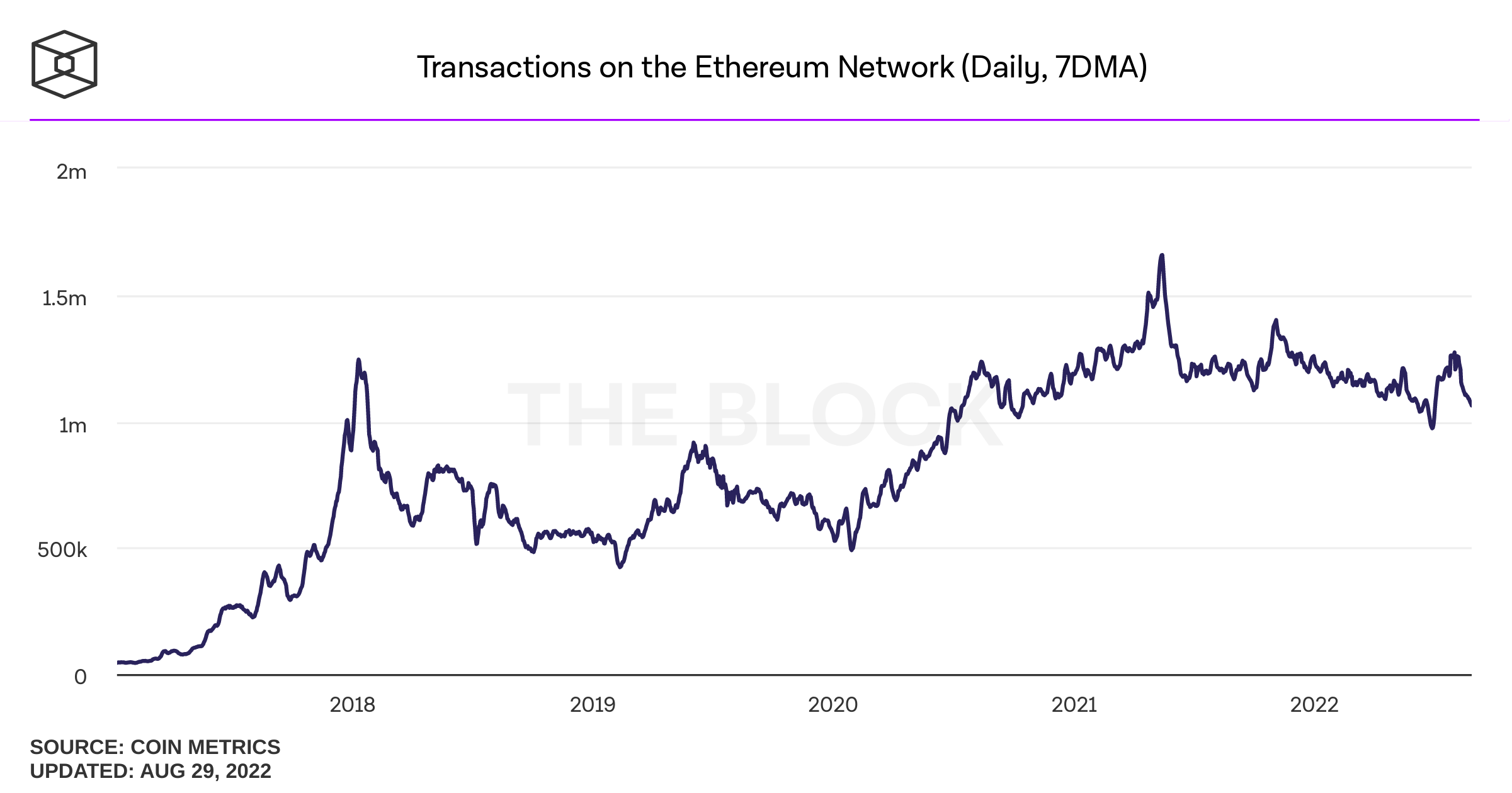

Are blockchains no longer used?

transactions on Ethereum flat

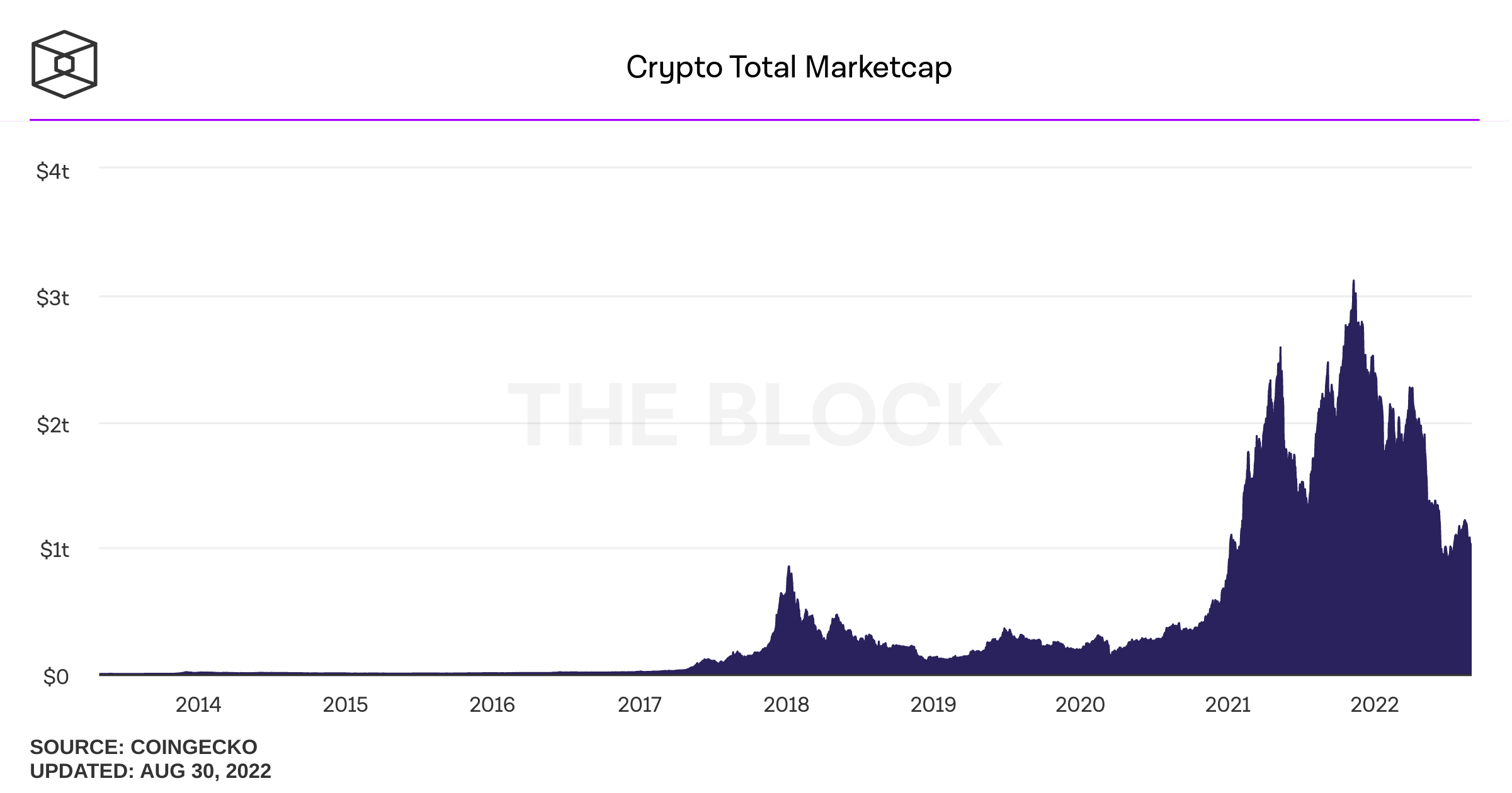

Is crypto-investing dead?

crypto market follows traditional market

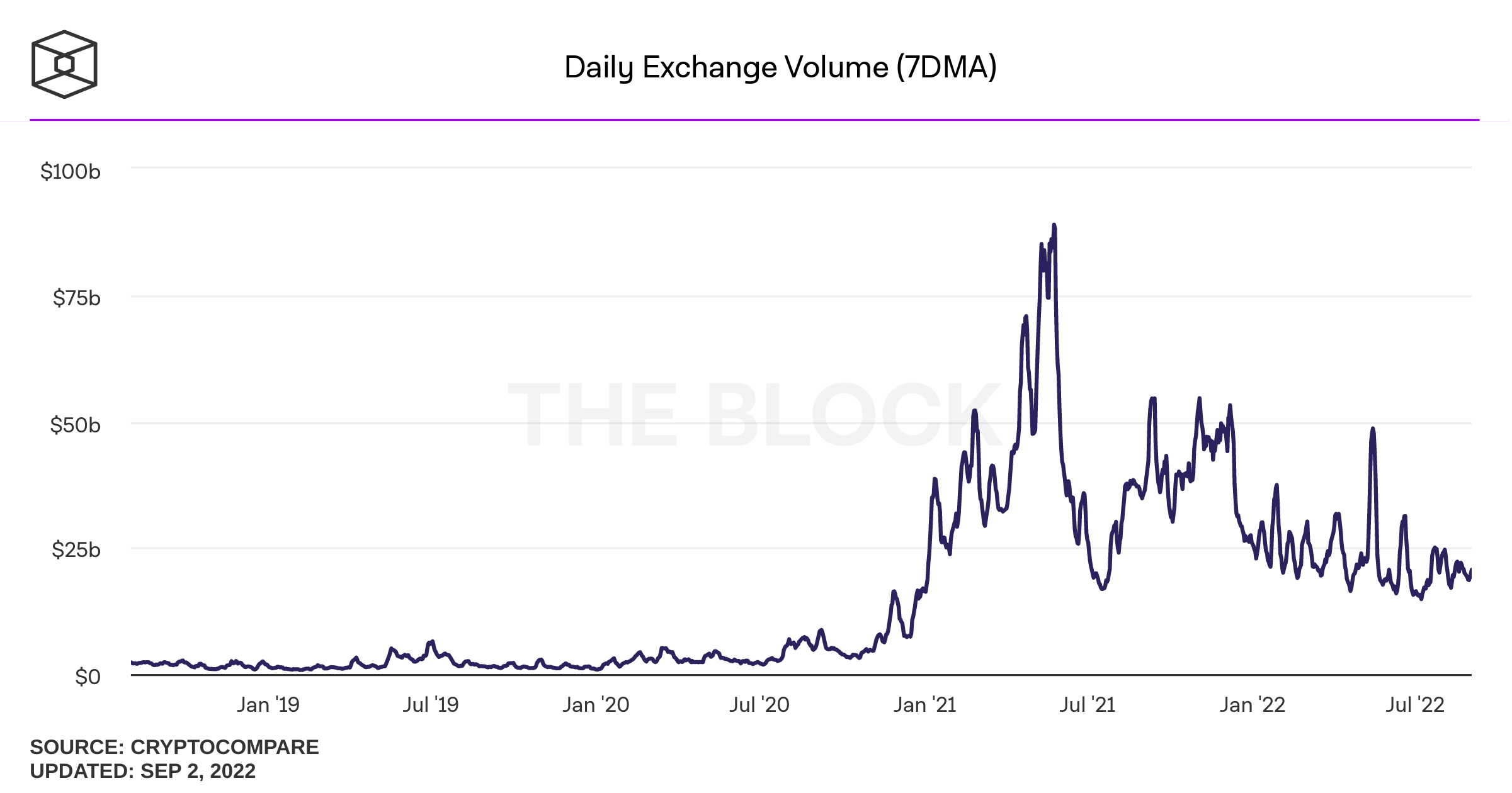

Is crypto trading dead?

trading volume on exchanges lower but steady

Are markets dead?

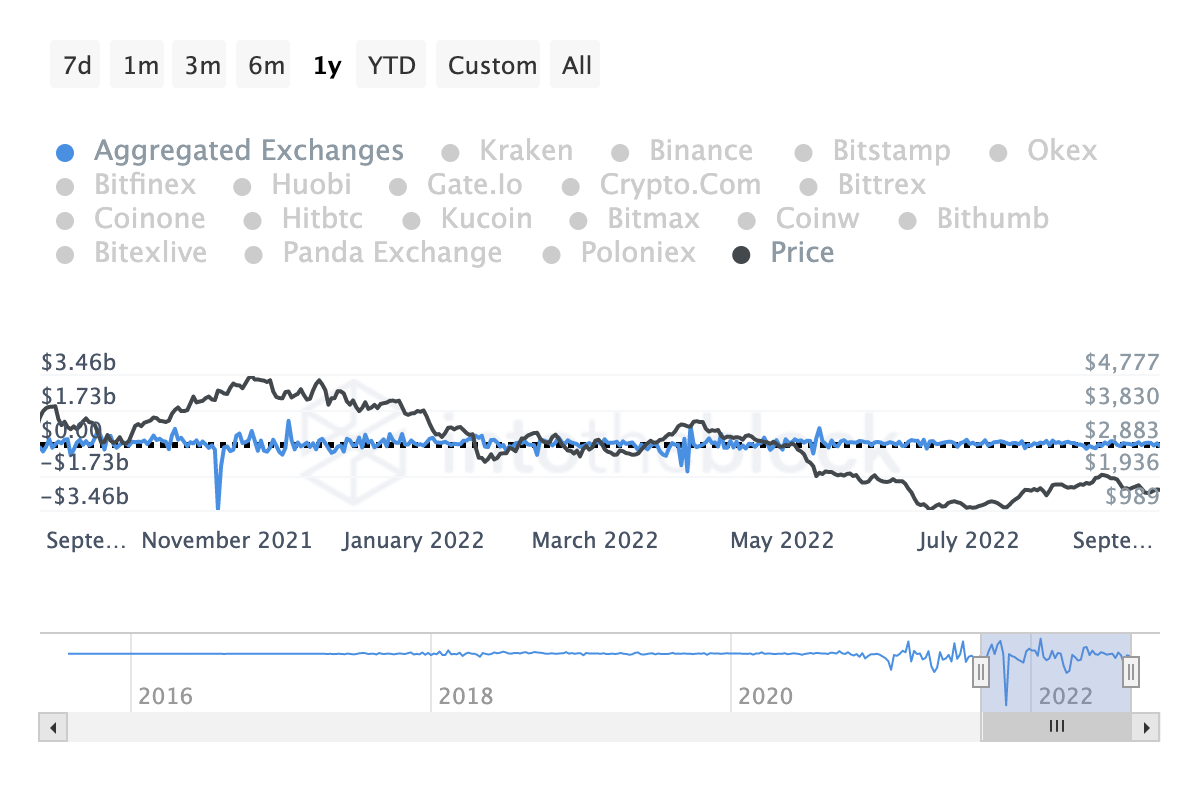

no meaningful net outflows from exchanges

Other consequences?

Challenges

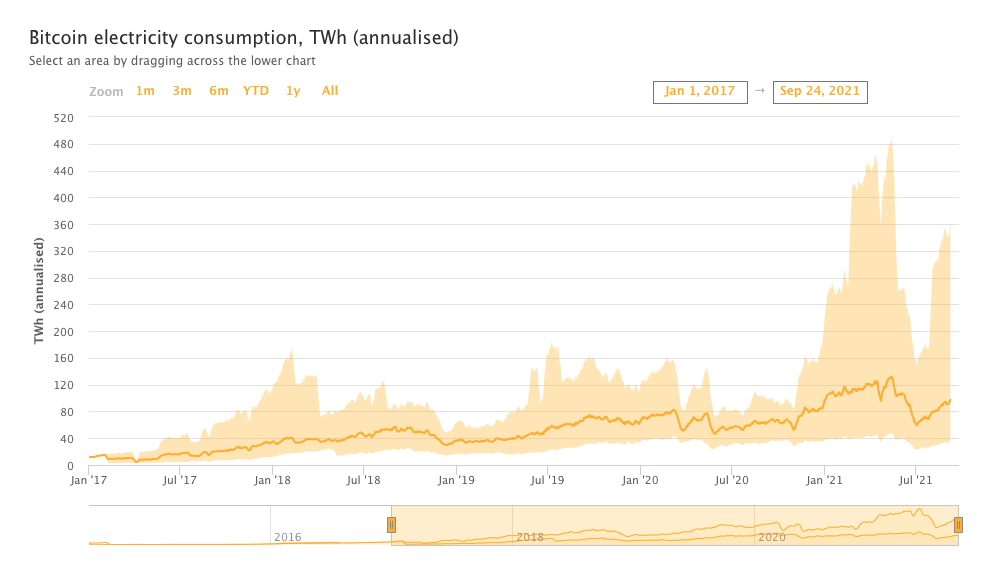

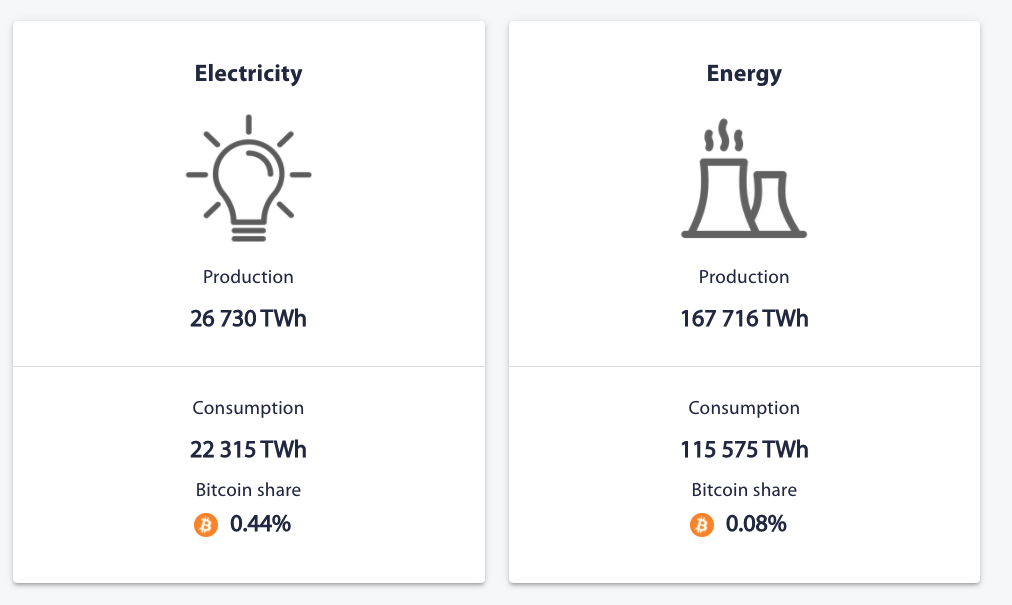

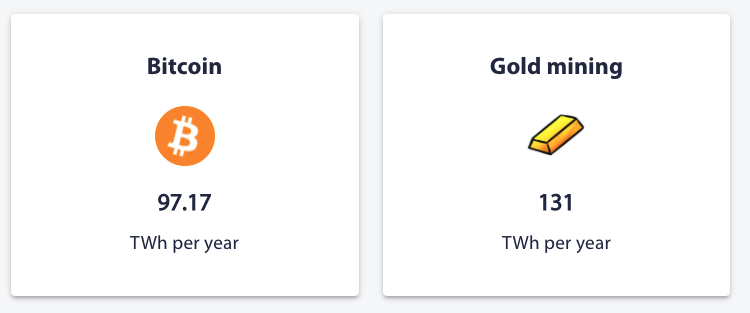

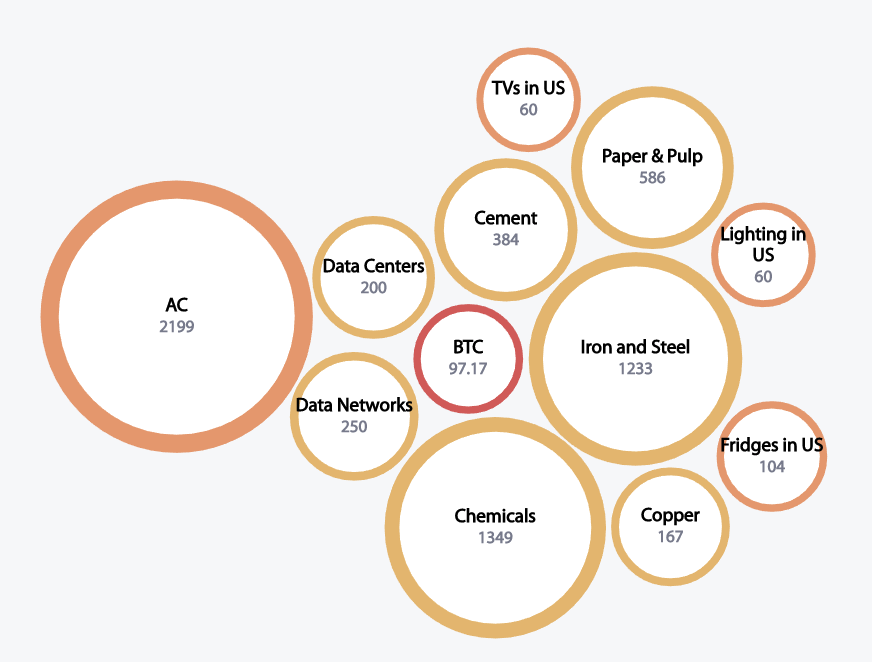

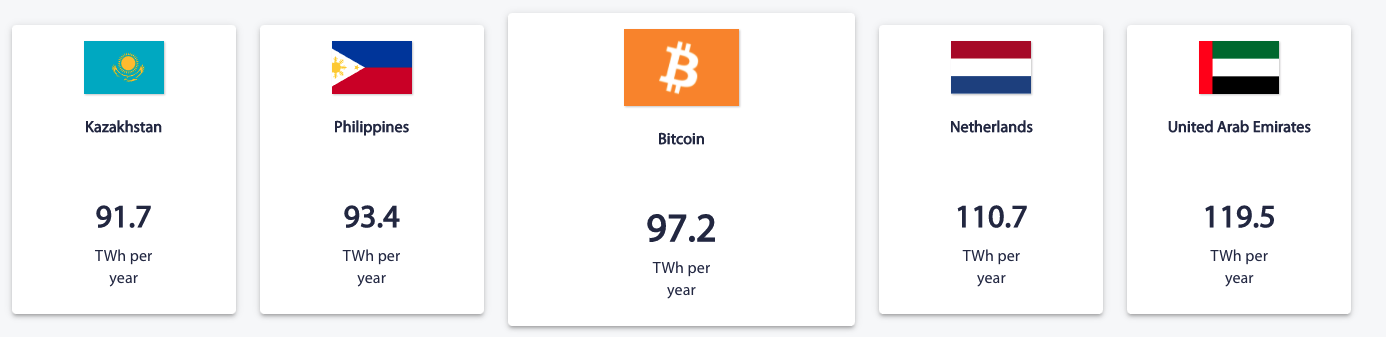

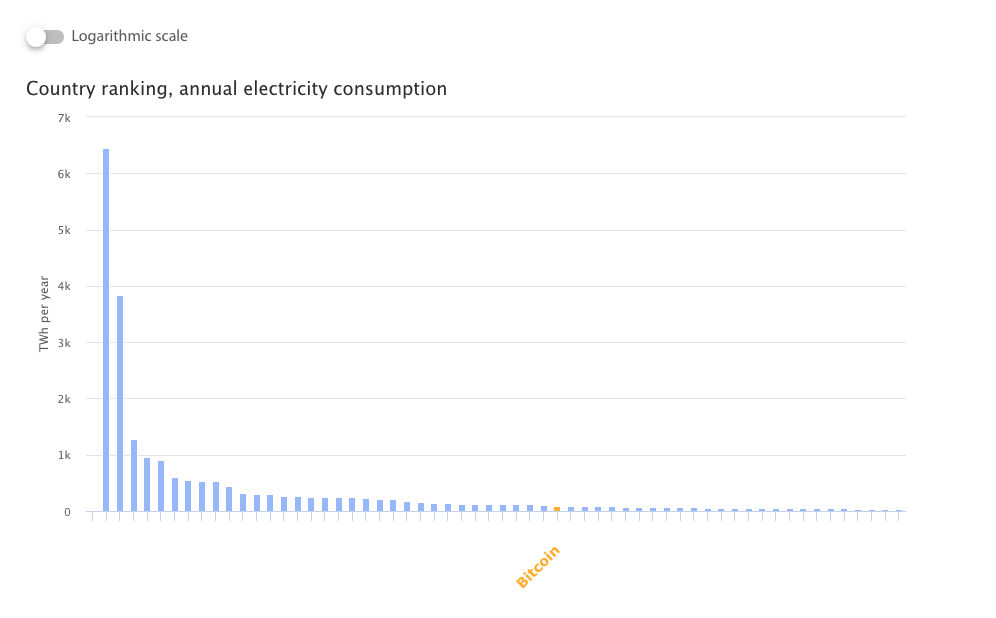

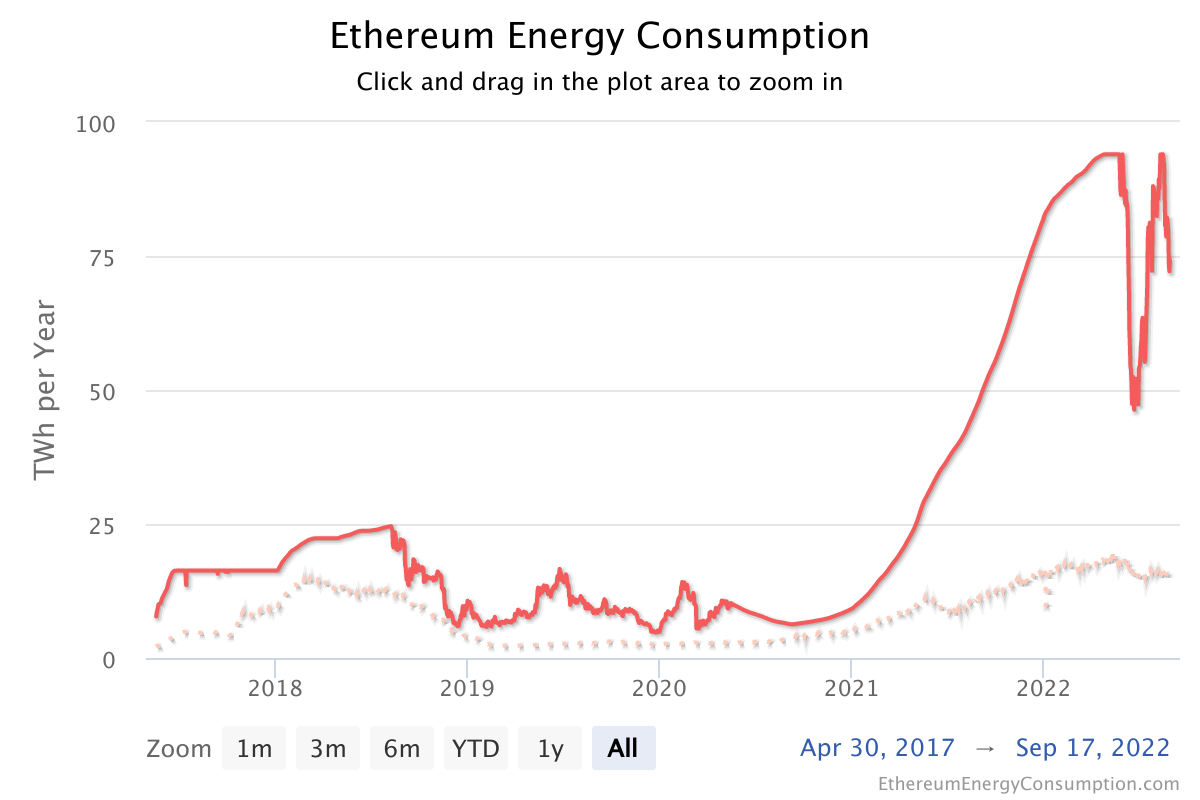

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

Usage

| Network | DApps | Dollarvolume |

|---|---|---|

| Ethereum | 3,500 | $40-50B |

| Solana | 100 | $2.5B |

| Binance Smart Chain | 250 | $3B |

| Avalanche | 400 | <$.5B |

| EOS | 300 | <$100M |

| Algorand | 12 | <$20M |

Ethereum Challenge 1: Environment

| transactions per second | T per 12 hours (business day) | |

|---|---|---|

| Bitcoin | 7 | 302,400 |

| Ethereum | 30 | 1,296,000 |

| Algorand | 2000 | 86,400,000 |

| Conflux | 4000 | 172,800,000 |

| Athereum | 5000 | 216,000,000 |

| Payments Canada ACSS | 648 | 28,000,000 |

| US retail | 7639 | 330,000,000 |

| Canada number of equity trades | 46 | 2,000,000 |

| Orders on Canadian equity markets | 3588 | 155,000,000 |

Tweaks: lighting network (BTC) or side chains, SegWit, blocksize possible, but there are limits

microtransactions, IoT, and other smart contract use cases place very high demands

Ethereum Challenge 2: Throughput

Ethereum Challenge 2: Throughput

Source: Etherscan w re-scaling

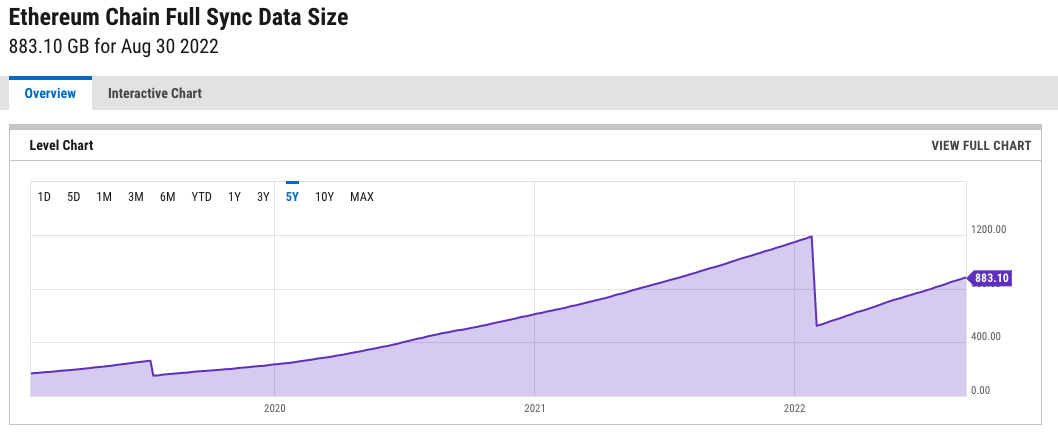

Ethereum Challenge 3: State Size

Source: Ycharts

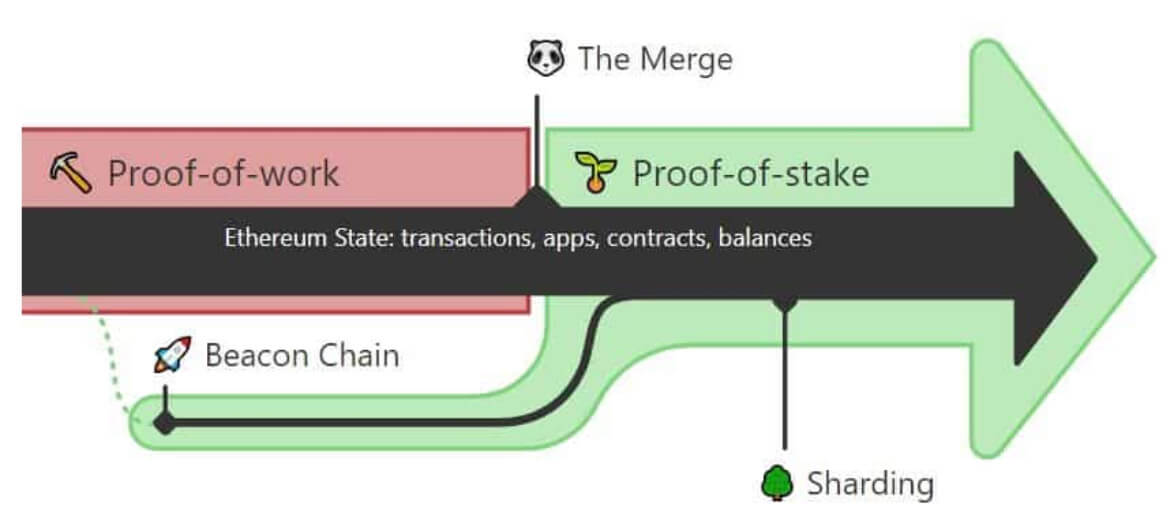

Major Ethereum Tech Upgrade: The Merge

scheduled date: September 13

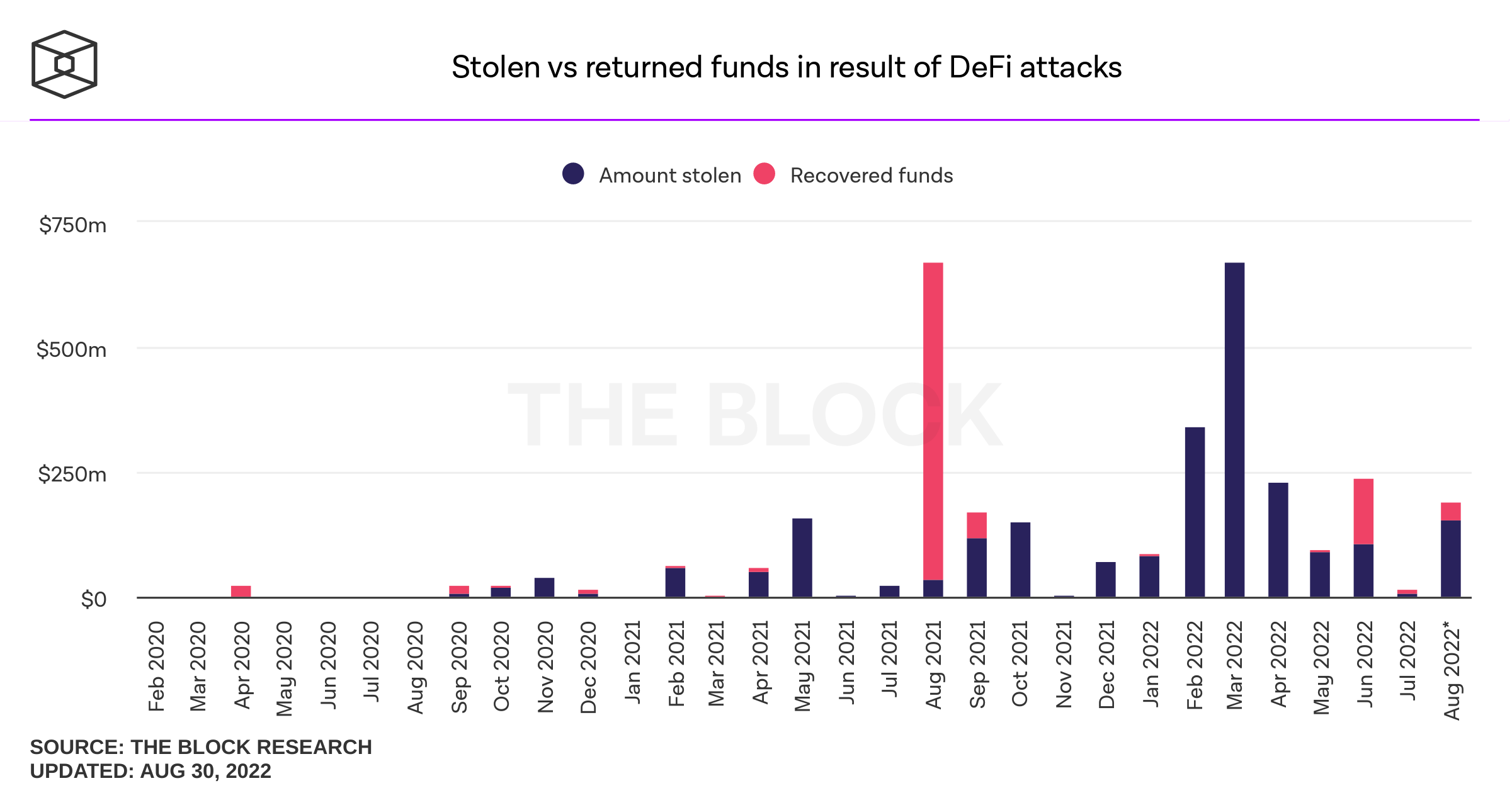

Hacks, Thefts, and Exploits

Common Reasons: hacks, faulty code, tricking a protocol

5-minute version:

What is a blockchain?

blockchain=

an infrastructure for digital resource transfers

5-minute version:

What is a cryptocurrency?

cryptocurrency =

internal payment mechanism to pay for operation of a blockchain

Evolution

vs

"Let me just say how impressed I am with Ethereum...If Bitcoin is email ––a one-trick pony, so to speak, but obviously revolutionary–– Ethereum goes far beyond that; it's more like the Internet...The whole idea of DeFi really is, number one, it’s obviously revolutionary, and I think at the end of the day could lead to a massive disintermediation of the financial system and the traditional players."

Heath P. Tarbert, CFTC Chairman, October 2020

5-minute version:

What is Decentralized Finance?

decentralized finance =

provision of financial services without the necessary involvement of a traditional financial intermediary based on blockchain technology

in practice: new financial infrastructure that will be a common resource

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

\(\vdots\)

Source: Harvey, Ramachandran, and Santoro (2020)

What can it for finance, what are problems and obstacles?

moving value (remittances)

digital money: real-time settlement, reduced reserves

tokenization of assets

automization of contract payments

securitization

systems and infrastructure reorganization

digital identity

new forms of financial contracts, assets, and forms of financing

Private Sector Solutions

Who gets to update?

Can a higher body prevent

transactions?

Can the past be altered?

consensus

immutability

censorship resistence

open to anyone

no one can be excluded

past cannot be changed

high visibility of transactions

open-access eco-system

slow governance

privacy only at a cost

joint control and governance

straightforward KYC and AML

tech support

transaction secrecy simpler

rely on corporate development

compliance with law (reversion)

can keep competition out

Enter BigTech

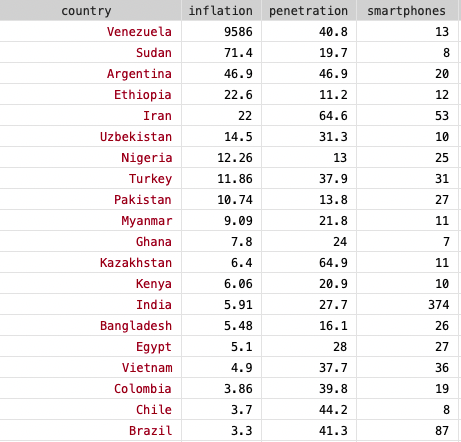

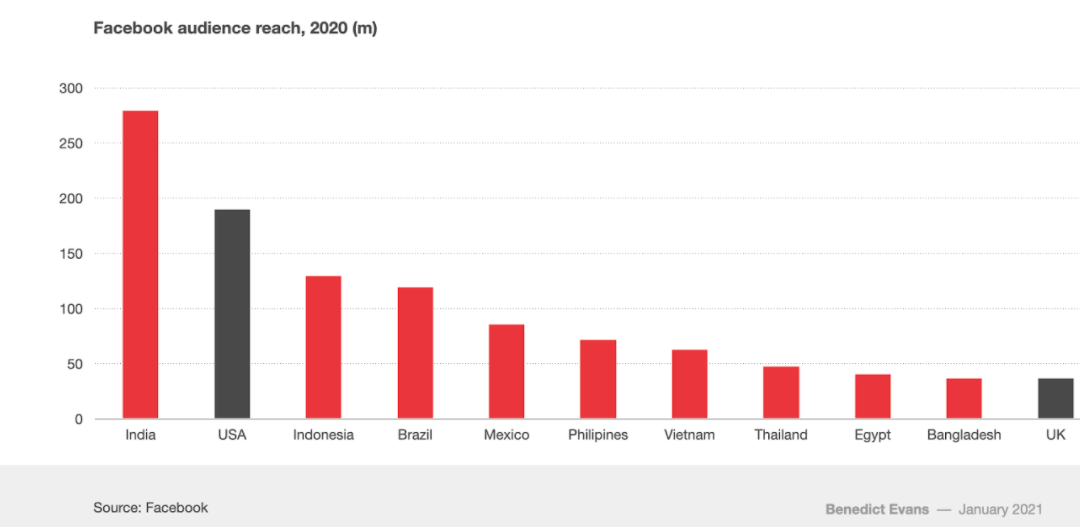

cellphone data from 2018 (NewZoo), inflation from 2020 (World Population Review)

Evolution

DIEM = "new financial infrastructure"

They have ZERO interest in becoming a financial institution/bank

\(\rightarrow\) no expertise

\(\rightarrow\) competitive market

\(\rightarrow\) one of the most regulated business environments

They are trying to deal with frictions that impede their business

They aim to collect data which will vastly improve their business

Lay the groundwork for the next step of the digital evolution: the "Metaverse"

Technology

Legal/Regulation

Economic functions

interoperability

cybersecurity and privacy

functionality

scalability

smart contract features and verification

space constraints

interoperability

scalability

space constraints:

Does the law have to change to accommodate new tech? If so, how? What's dated, what's not?

Legal setup of a platform: what rules can, should, and must a platform establish? What regulations are necessary?

How can token design and the law be married?

What is the economic impact of "tokenizing everything"?

How will it affect investments and investment banking?

Which business opportunities will it enable?

What do tokens and "alternative money" mean for payments?

Future of Crypto: Regulators

United States

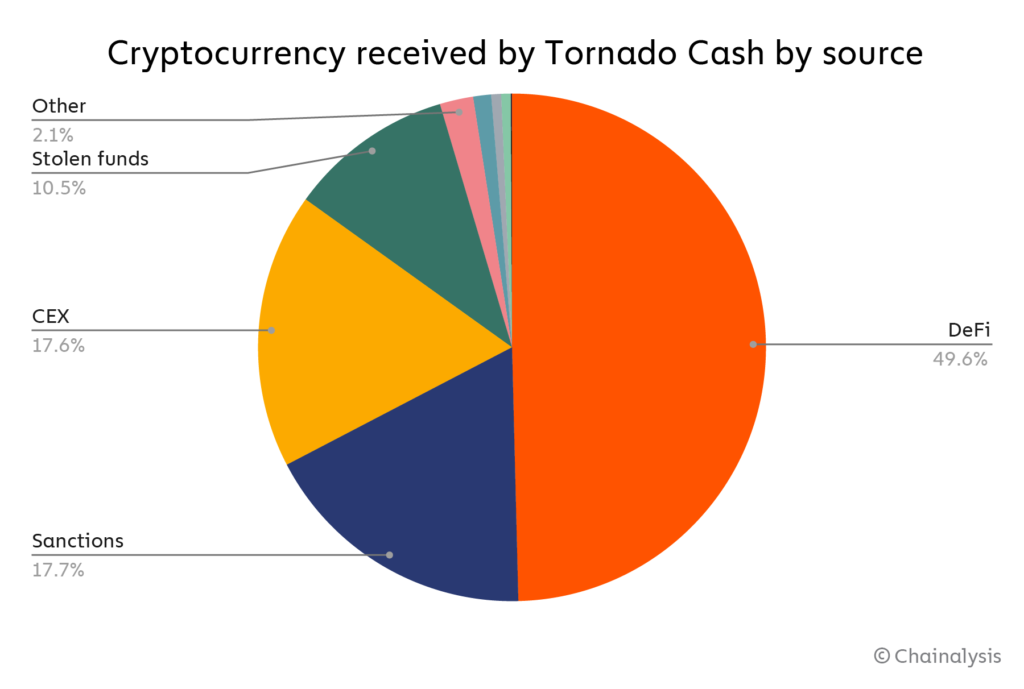

Most relevant case for FIs: Tornado Cash

Need for Regulation

FinTech

DeFi

innovation vs. salesmanship

main focus

blockchain is a transformative technology, but won't be used in practice overnight

many conceptual and technological challenges remain, but there are already various areas of application

legal, regulatory, and competitive changes are needed and then the opportunities are endless ...

it will open up the banking world further, foster international competition, and change how we pay and exchange value

My view: business development will happen in private/semi-public space; strong increase in recent activity; no more testing but re-engineering of processes.

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

This is the slide deck that I use for a quick introduction to the Decentralized Finance class.