Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park & Zissis Poulos

2021

MakerDAO

borrowing/lending

on-chain ability to exchange arbitrary value

(last class)

Idea:

Sidebar: what is a DAO?

4 ETH

(1 ETH = $375)

(Oct 15, 2020)

\(\approx\) $1,500

\(\vdots\)

1,500 DAI

(1 DAI = $1)

formally: this smart contract is a collateralized debt position (CDP)

fractional collateral \(\to\) collateralization factor \(=\) 150%

total collateral = $1,500

maximum loan = $1000

overcollateralization = $500

actual loan (example) = $500

buffer = $500

ETH \(\nearrow\) $500

value of ETH collateral = $2,000

maximum loan = $2,000/150%=$1,333

total collateral = $2,000

maximum loan = $1,333

overcollateralization = $667

actual loan (example) = $500

buffer = $500

overcollateralization = $667

new loan capacity= $333

ETH \(\searrow\) $187.5

value of ETH collateral = $750

maximum loan = $750/150%=$500

total collateral = $750

maximum loan = $500

overcollateralization = $250

actual loan (example) = $500

buffer = $0

for reference: former value of collateral

ETH \(\searrow\) $150

value of ETH collateral = $600

maximum loan = $600/150%=$400

total collateral = $600

maximum loan = $400

required overcollateralization = $200

actual loan (example) = $500

buffer = -$100

for reference: former value of collateral

\(\Rightarrow\) triggering of liquidation auction by "keeper"

sell 3.33 ETH=$500=500 DAI

repay $500=500 DAI loan

retain incentive

return remainding ETH to vault owner

\(\Rightarrow\) all relies on behavioral assumptions

\(\Rightarrow\) But: there are also real incentives & mechanisms

borrowers of DAI need to pay interest \(\to\) stability fee

DSR paid on "locked" DAI

total amount of debt (or DAI) outstanding is limited

Sidebar: how is this decided?

\(\to\) special "governance" token MKR

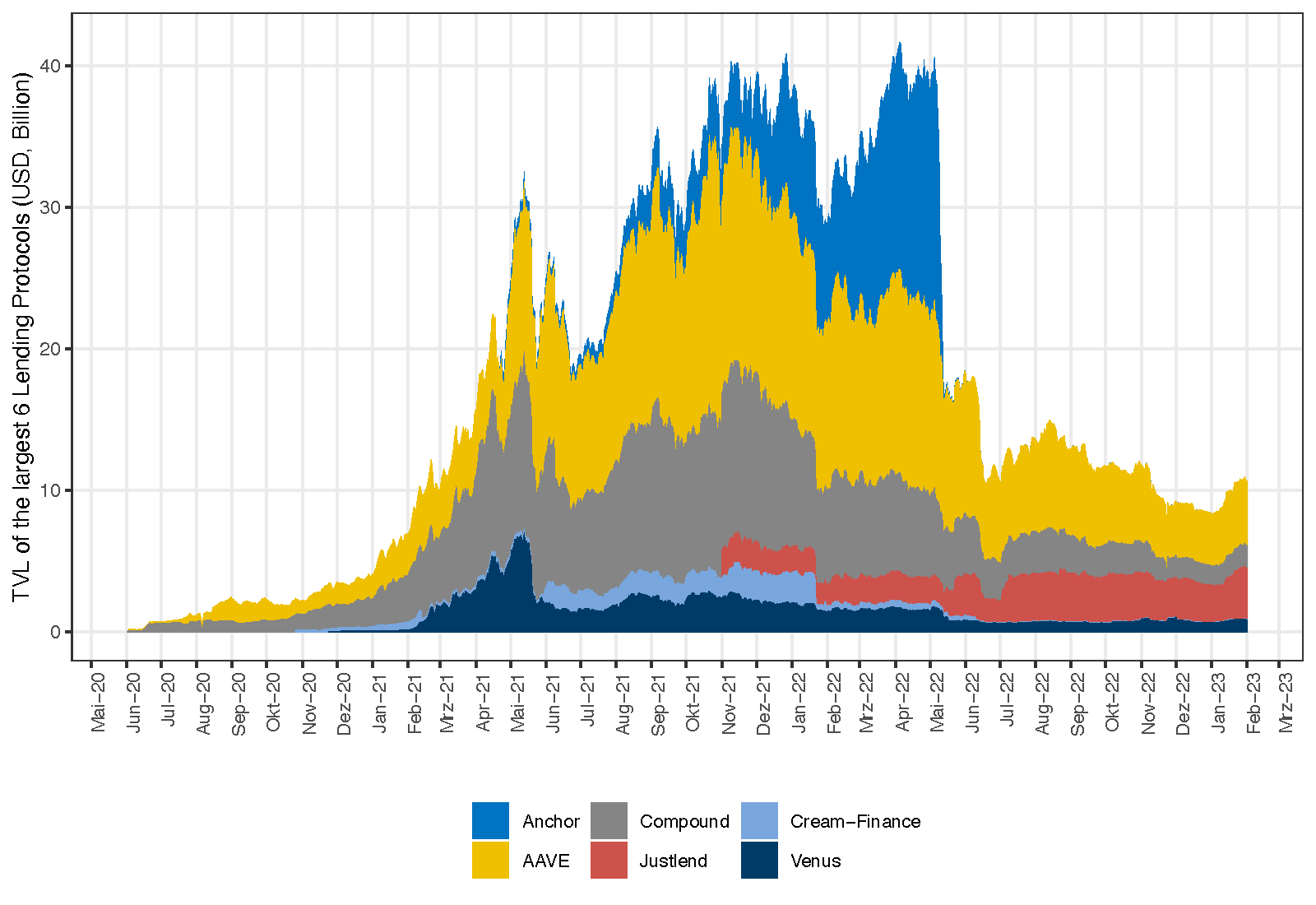

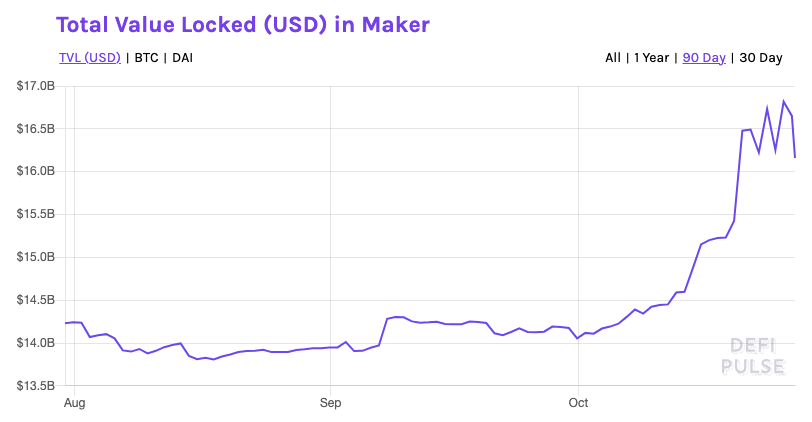

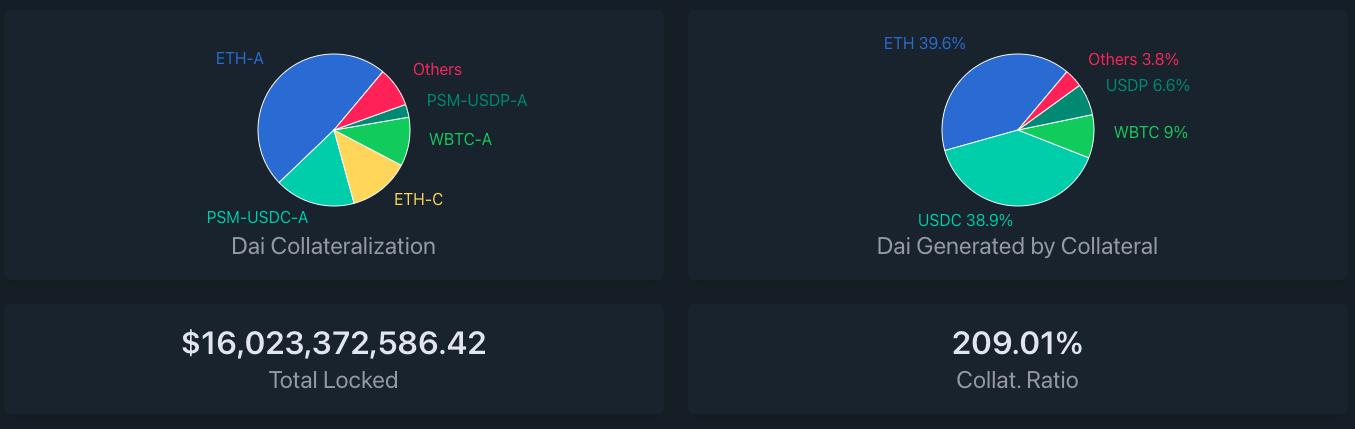

Source: daistats.com (Oct 27, 2021)

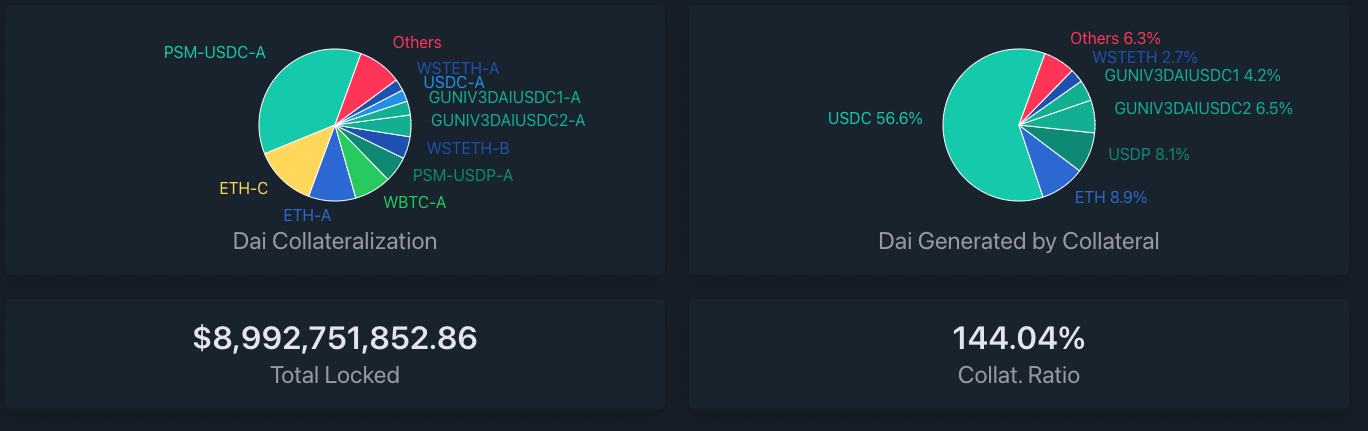

Source: daistats.com (Oct 26, 2022)

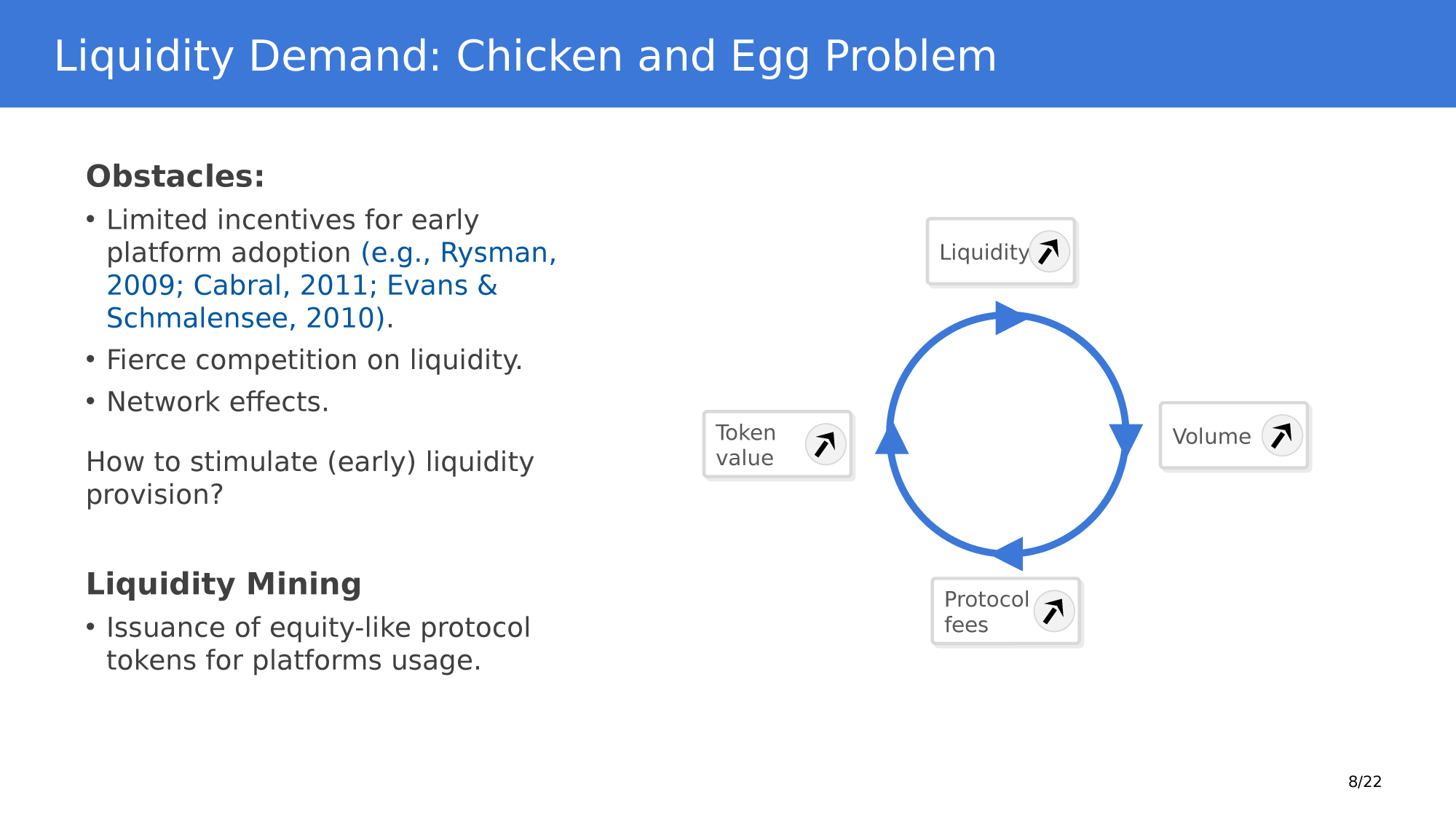

The Problem:

The Solution:

Note: In May 2021, ETH prices dropped again by >30% but no drama in DAI

Interest rates influenced by the FED, access to loan products controlled by regulation and institutional policies

MakerDAO platform is openly controlled by the MKR holders.

Difficulty of obtaining loans for large majority of population

Open ability to take out DAI liquidity against an overcollateralized position in any supported ERC20 token. Access to a competitive USD denominated return in DSR.

Costs of time and money to acquire a loan

Instant liquidity with minimal transaction costs.

Can't seamlessly use the same USD across many platforms

Issuance of DAI, a permissionless USD-tracking stablecoin backed by cryptocurrency. DAI can be used in any smart contract or DeFi application.

interoperability

inefficiency

centralized control

limited access

opacity

Unclear collateralization of lending institutions.

Transparent collateralization ratios of vaults visible to entire ecosystem

legacy finance

MakerDAO

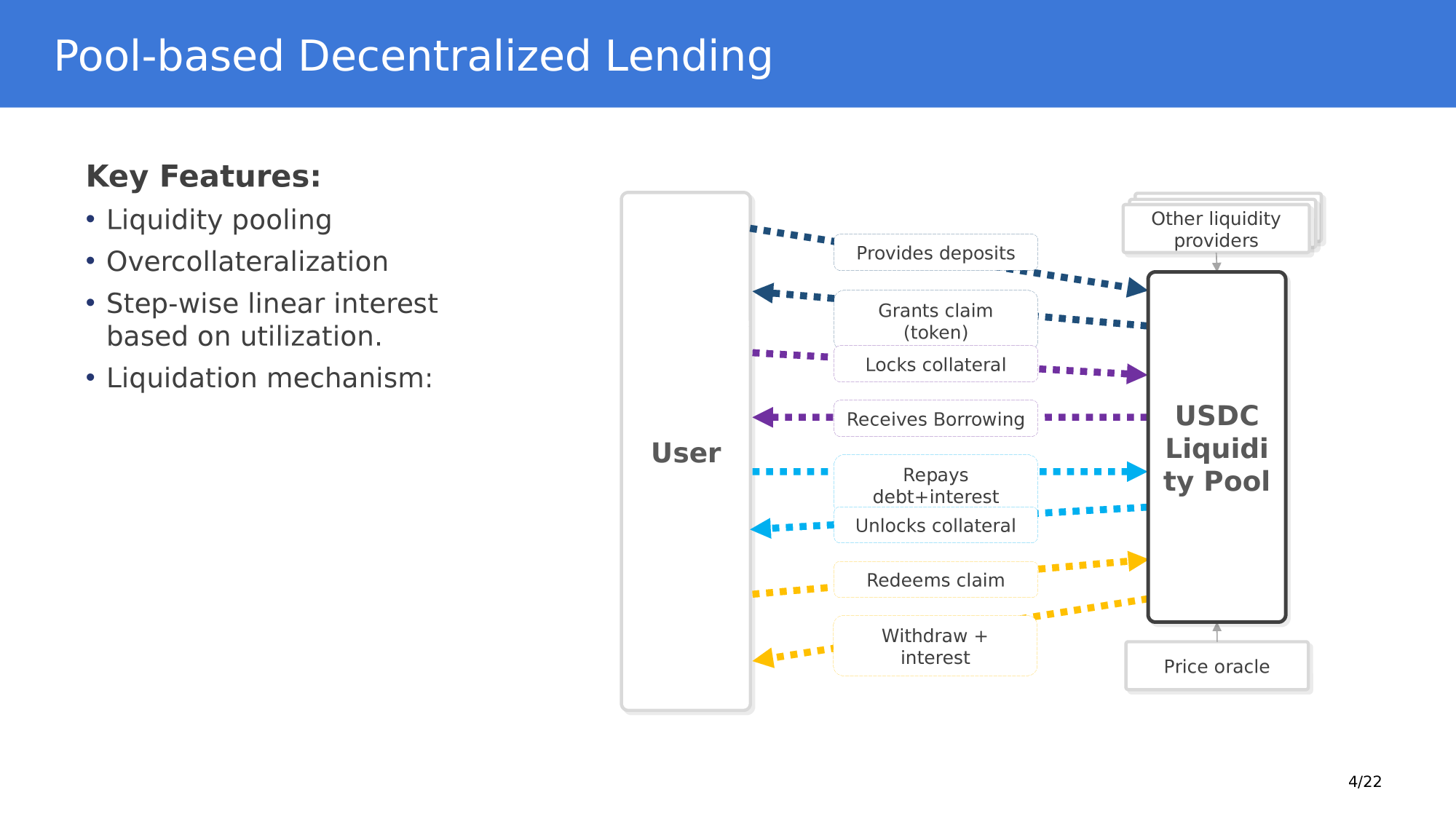

Pool-based lending principles

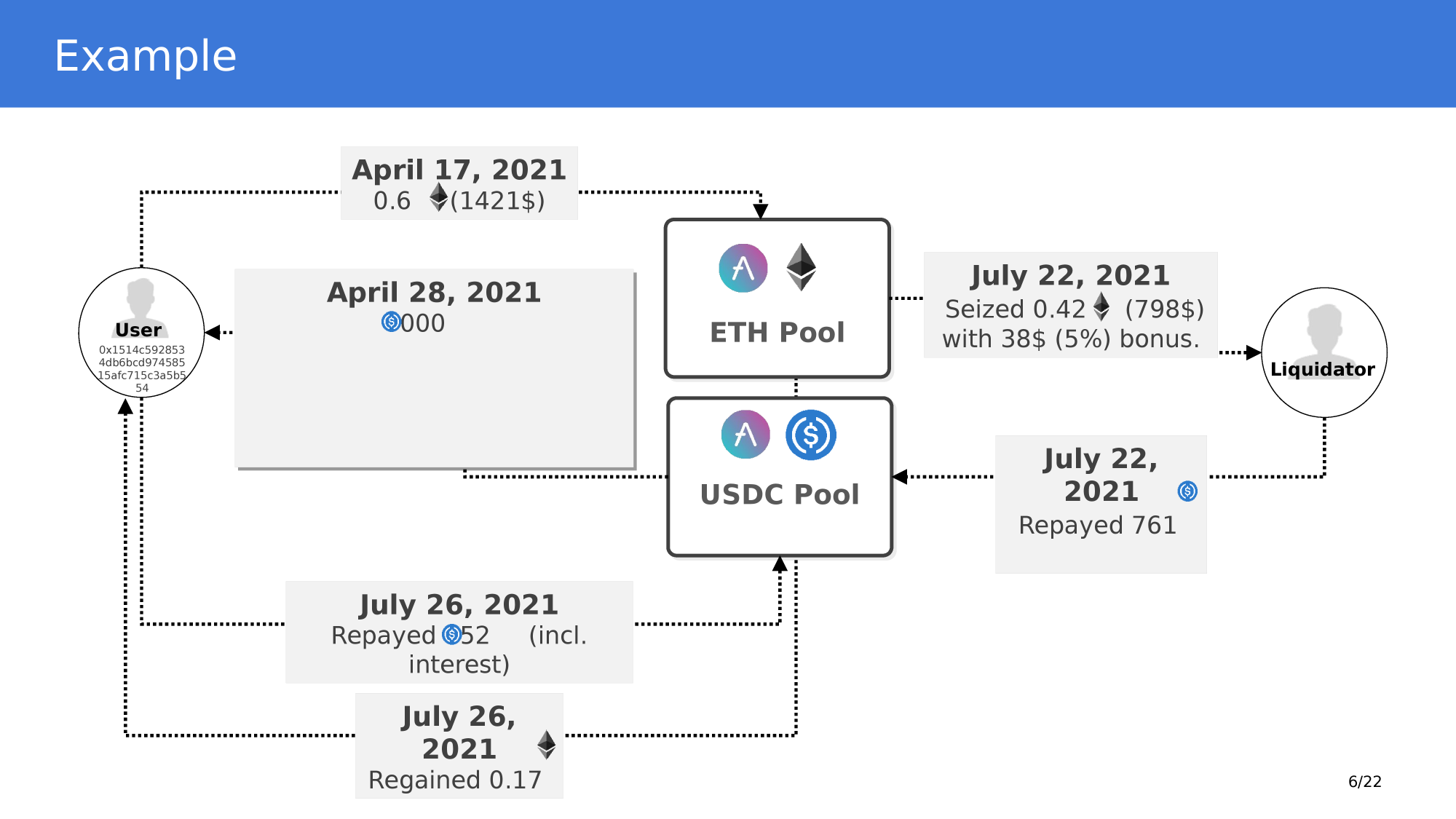

Example 1

Example 2

Example 3

borrowing and lending rates compounded per block

Token Accounting:

tracking ownership

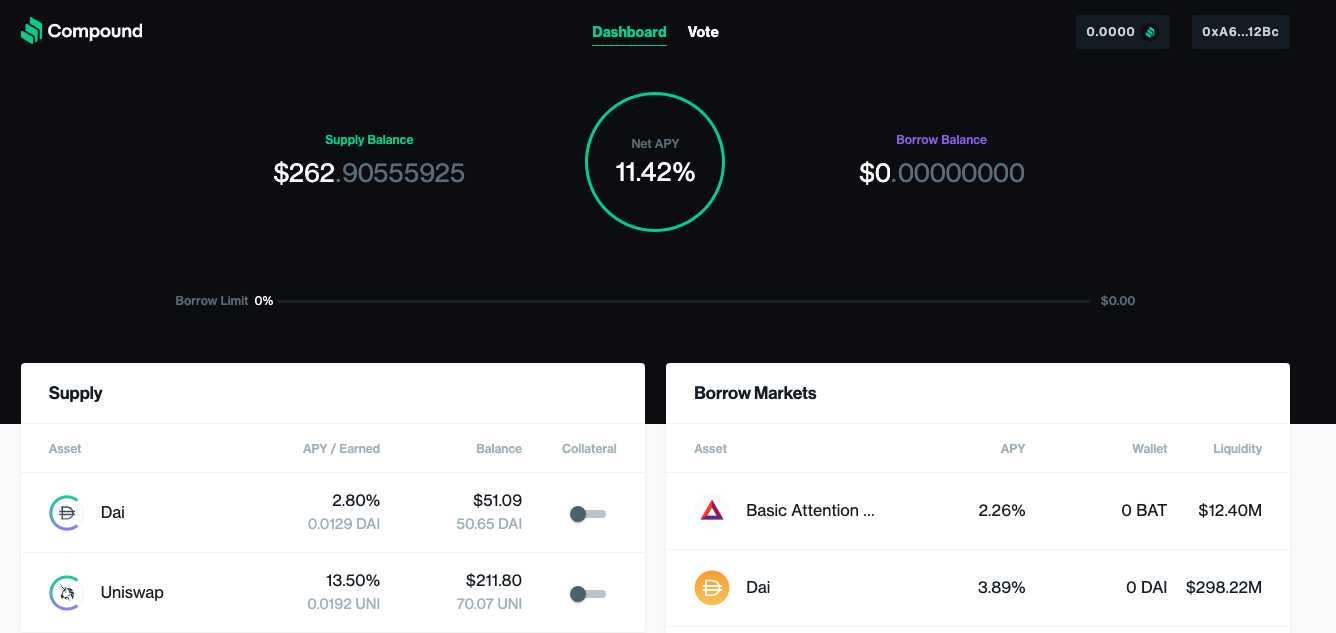

Compound

AAVE

Token Accounting: TWO Types

Fundamentally, what does a bank do?

And how is this done?

on blockchain

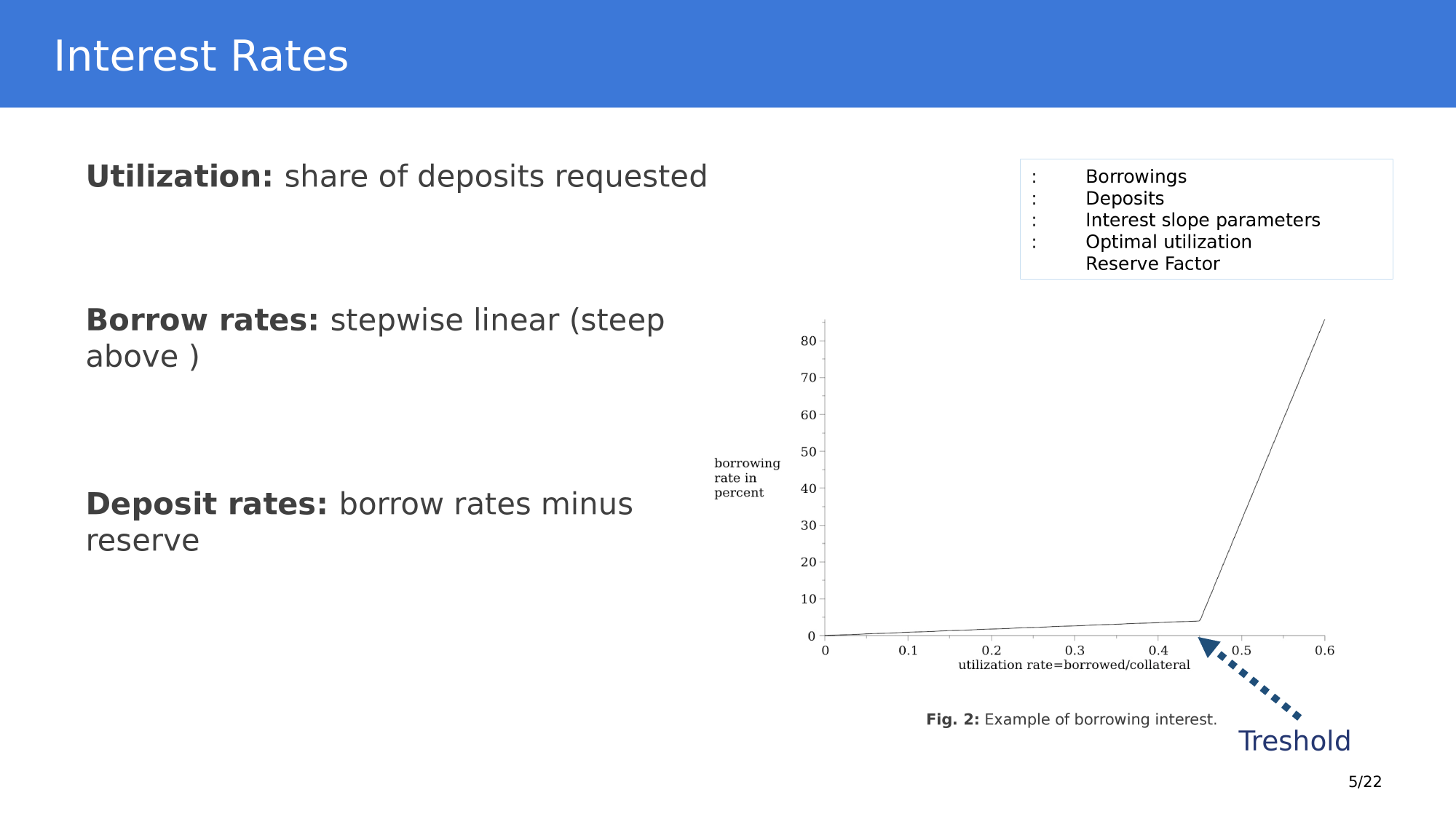

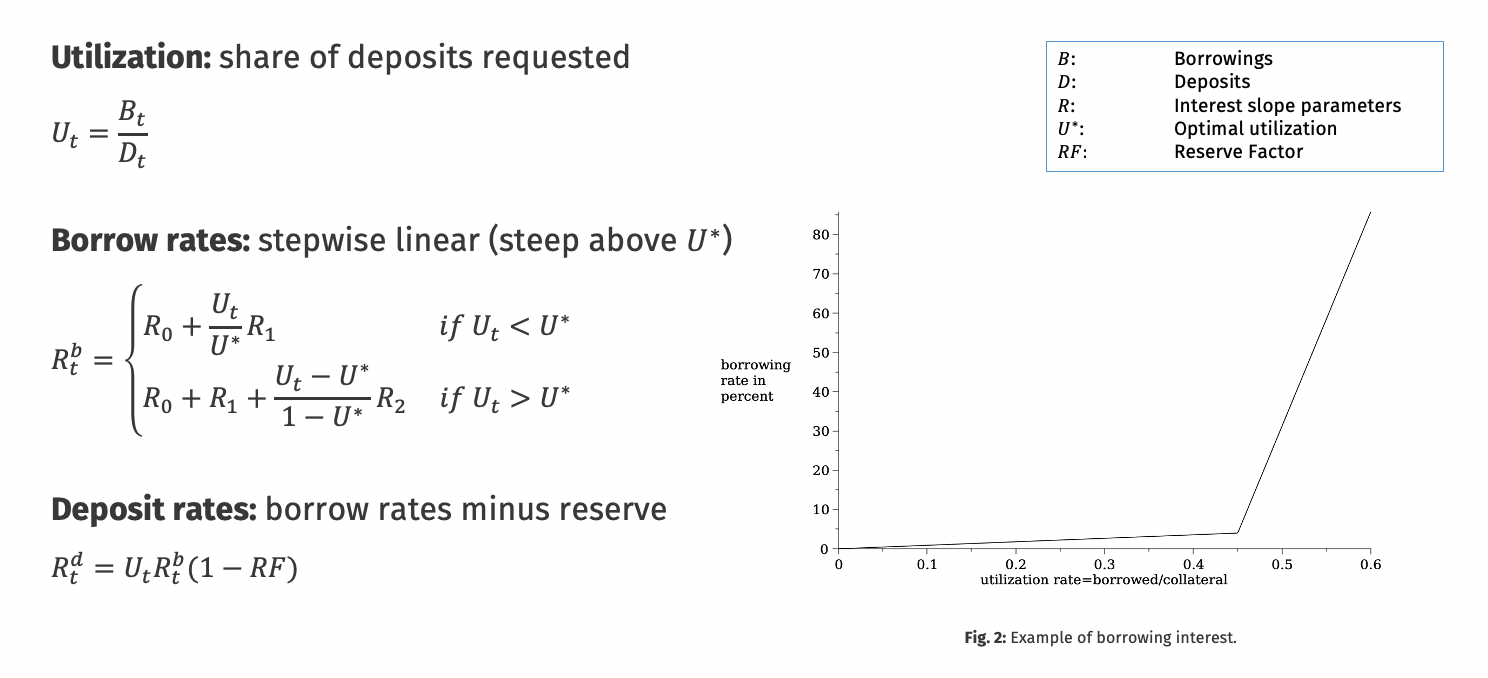

100%

fraction of supplied that's been borrowed

base rate

borrow rate

In Compound

translated

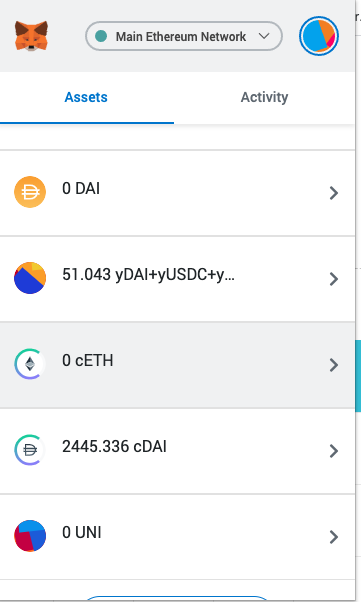

new deposit

1,000 DAI

100 cDAI

500 DAI

add 50 new cDAI

In Compound

translated

new deposit

1,000 DAI

150 cDAI

500 DAI

1 year later: 10% interest on compound

150 DAI

(same cDAI, ownership shares don't change, just each cDAI is worth more)

(accrues per block per deposit)

AAVE

Liquidity Mining

Flash Loans

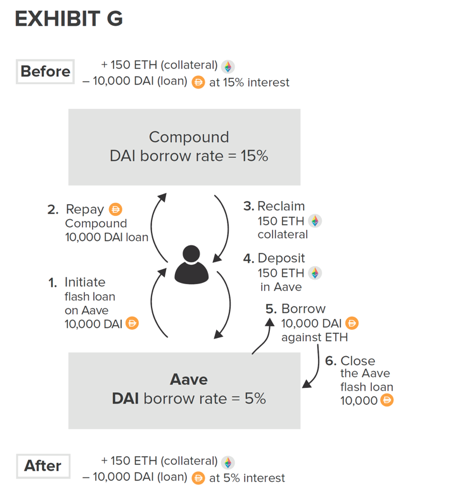

common theme in DeFi: jumping between dApps

Source: Harvey, Ramachandran, and Santoro (2020)

1. flash-borrow DAI

5. repay DAI

3. receive ETH

4. convert ETH to DAI

2. liquidate ETH loan with DAI

Loan liquidation opportunity

Commercial Paper/T-Bill like securities

1 ETH = 150 DAI

collateralization ratio 125%

seller

buyer

supplies 1 ETH collateral today

mints (=borrows) 100 yDAI to be repaid in 1 year

y

receives 92 DAI today

pays 92 DAI today

y

receives 100 yDAI

repays loan with 100 DAI

deposits yDAI and receives 100 DAI

seller

buyer

Scenario 1: ETH \(\ge\)125 DAI

deposits 100 yDAI

withdraws 100 DAI

receives balance of 1 ETH - 100 DAI

What does the seller own (ignore keeper fee)?

seller

buyer

Scenario 2: ETH falls to <125 DAI

keeper

closes undercollateralized position \(\to\) sells 0.8 ETH for 100 DAI

receives 100 DAI early

receives balance

of 0.2 ETH

disclaimer: an incomplete list

Bitcoin,

stablecoins, etc.

"higher layer"

lending

payments processing

financial

advice

trading

services

funding

services

prop trading to manage risks

too early, but projects are underway

as it turns out, these items are often directly related

interoperability

inefficiency

centralized control

limited access

opacity

interchange (=VISA) fees, settlement times, microtransactions, physical infrastructure

between-institution or transfers, reconciliation process, international remittances, various securities custody and trading systems

information for users, health of deposit taker, what-happens-behind-the-scenes, counterparty risk

local monopolies/switching costs, central banking, deposit concentration, control vs. competition

1.7B unbanked in the world, 24M in the US, many services or products not available based on location etc, lack of SME support, inability to collateralize

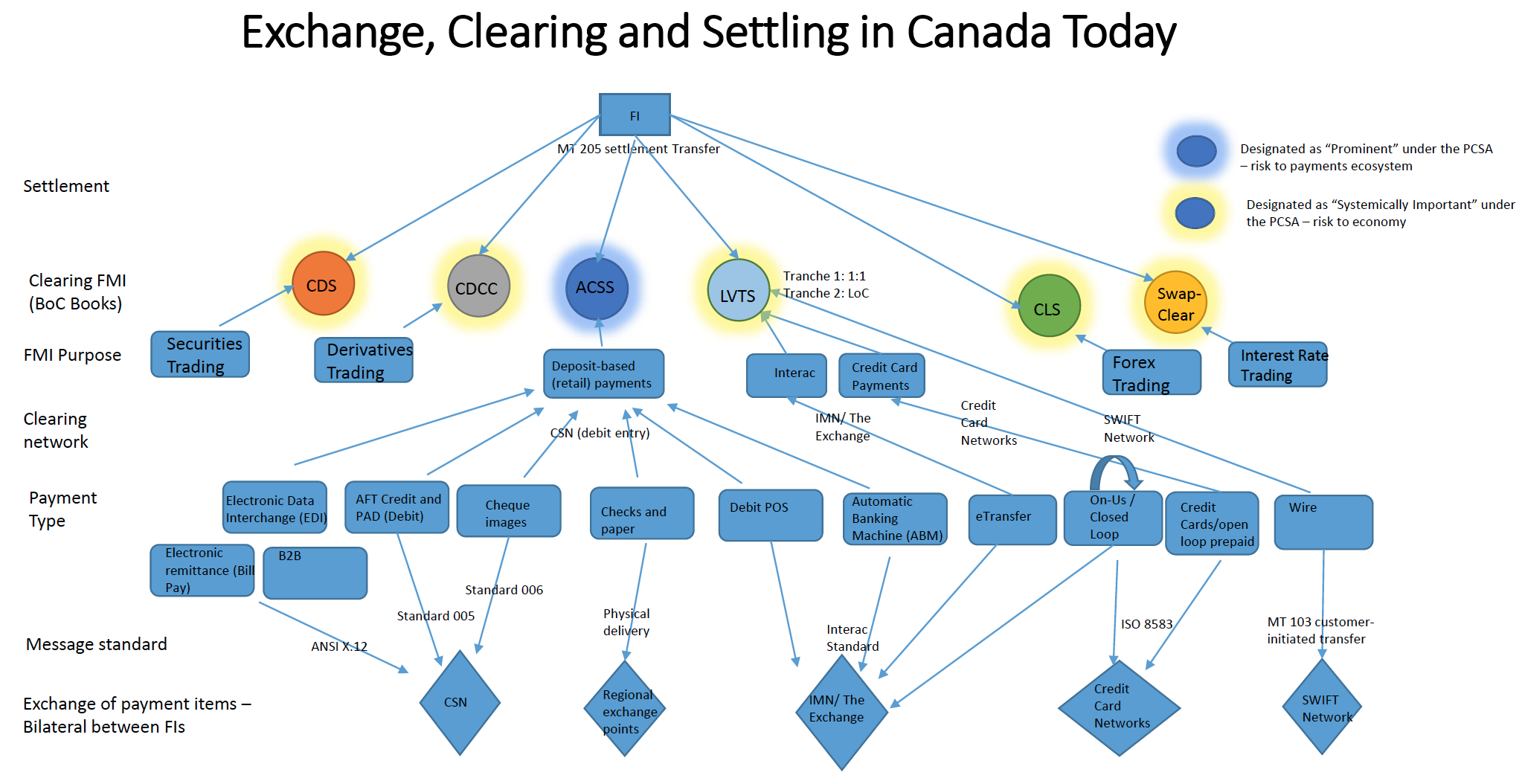

Source: Wendy Rotenberg's Payments lecture

CDS

ACSS

LVTS

Cheques

Debit at POS

e-transfer

Credit Card/

open loop

ATMs

Wire

Interac

Credit

Card

deposit based retail

Interac standard

credit card network

SWIFT

CSN

Settlement

Clearing process

Underlying network

Type of payment

Financial market infrastructure purpose

Securities Trading

e-transfer

Wire

deposit based retail

CDS

Securities Trading

derivatives

swaps

property registry

interoperability

inefficiency

centralized control

limited access

opacity

siloed legacy system

is interoperable by design

reduces frictions and separates service from "commodity"

decentralized control and common operation

fewer barriers\(\to\) broad access

is/can be highly transparent

common infrastructure system

interoperability

inefficiency

centralized control

limited access

opacity

payments

lending

trading

services

funding

services

prop trading

manage risks

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

This slide deck provides an overview of DeFi protocols. It draws insights from Harvey, Ramachandran, and Santoro (2020) "DeFi and the Future of Finance"