Andreas Park PRO

Professor of Finance at UofT

Discussion of Identifying High Frequency Trading activity without proprietary data

Paper by Bidisha Chakrabarty, Carole Comerton-Forde, and

Roberto Pascual

Discussion by Andreas Park

Northern Finance Association Meeting, September 2021

How computed as HFT-specific?

Charles Jones: "All good papers have the key results in table III"

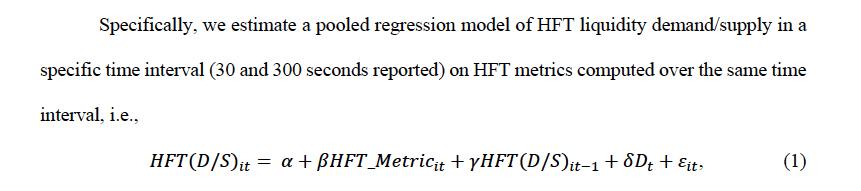

Three correlations of interest

statistical pre-requisite: standardization, including intra-day seasonality

all between 40-80%

all previous measures are somewhat order-submission based,

so should (and do) catch message-intensive strategies

HFTs have many strategies

what captures these?

seems like correlation to me ... how's that identified?

Literature:

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park