Andreas Park PRO

Professor of Finance at UofT

many facets

many facets

Source: Schmall & Wolkowitz (2016), Center for Financial Services Innovation (2016) "Financially Underserved Market Size Study"

Source: Schmall & Wolkowitz (2016), Center for Financial Services Innovation (2016) "Financially Underserved Market Size Study"

Source: Schmall & Wolkowitz (2016), Center for Financial Services Innovation (2016) "Financially Underserved Market Size Study"

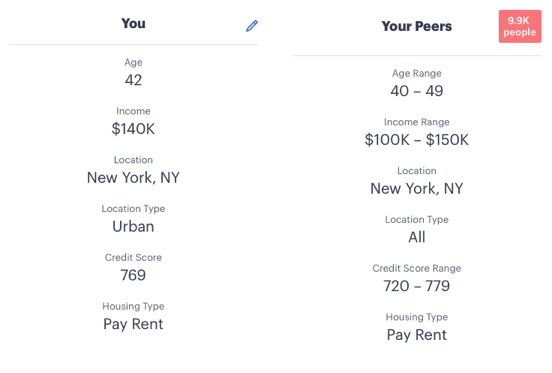

elicits characteristics of customers

uses US representative micro-data on transactions

shows customers the spending profile of similar group

assesses the reaction of customers (transaction level)

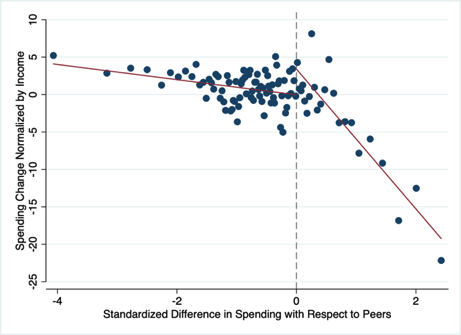

Source: D’Acunto, Rossi, and Weber: Crowdsourcing Financial Information, 2019

Source: D’Acunto, Rossi, and Weber: Crowdsourcing Financial Information, 2019

"over-spenders" reduced spending

most people reduced spending

Why we should be skeptical of untethered AI

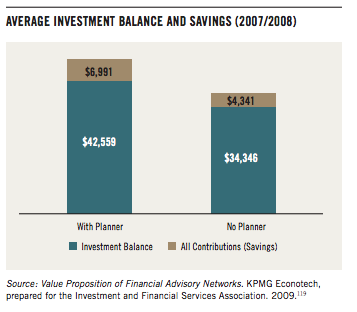

https://assets.dynamic.ca/content/dam/klick/Article-Reprints/SUFA_sareport.pdf

several developments in recent years

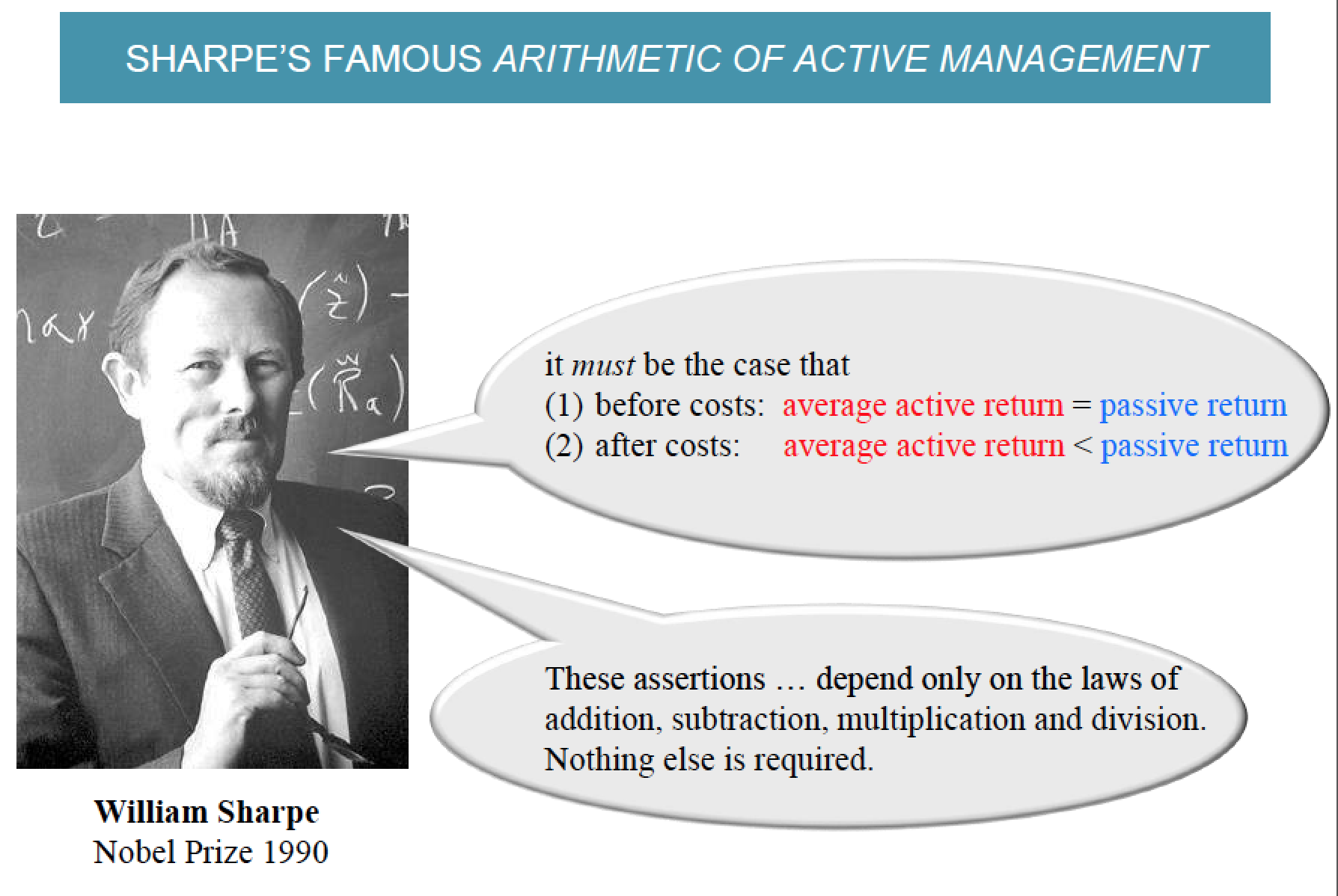

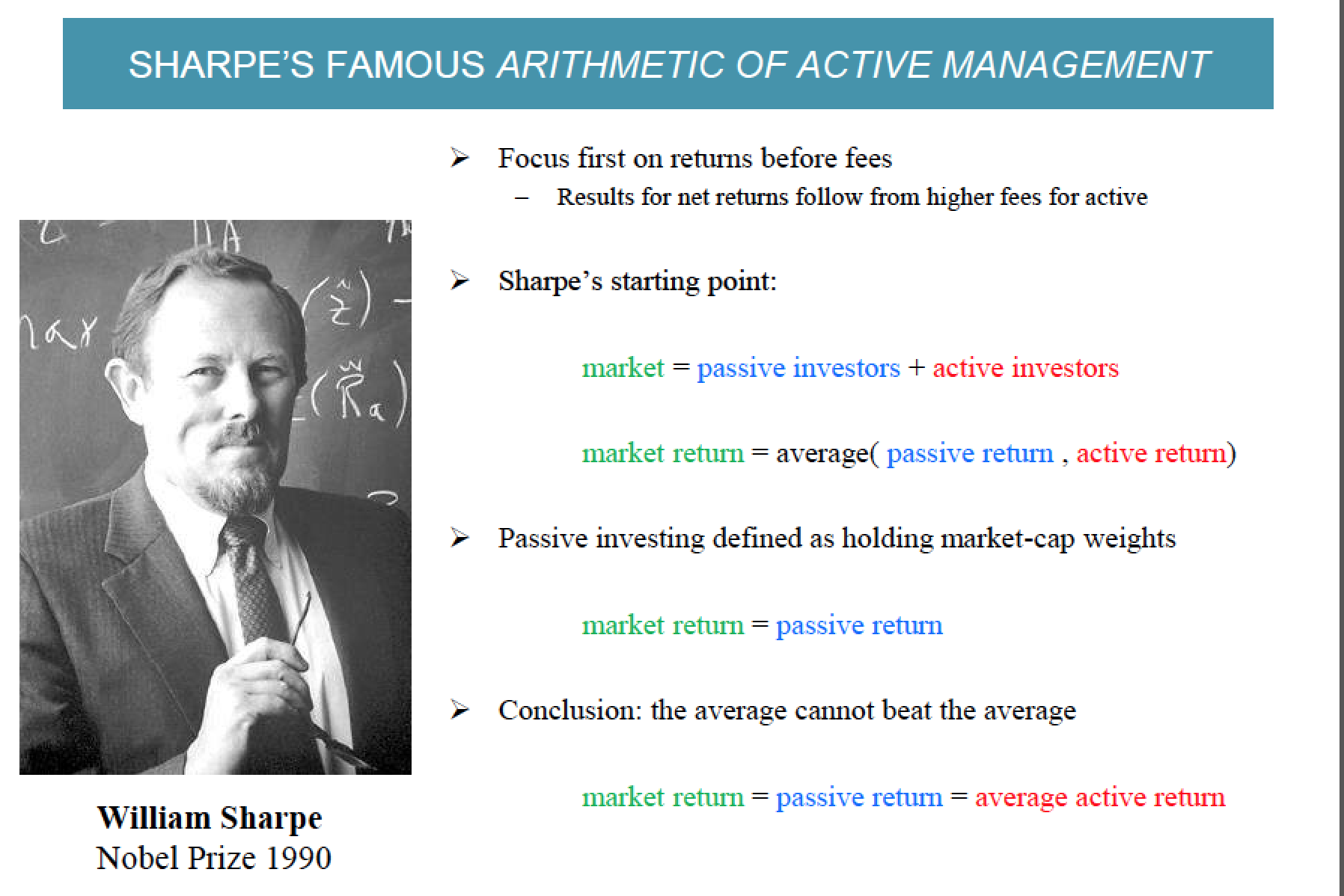

The founding father of portfolio optimization is still with us, his name is Harry Markowitz

Won the Nobel prize in 1990 for work he did in the 1950s

His insight is the engine of robo-advising

How to take the least risk for the expected return

Want higher expected return, lower risk

For a given expected return, want the lowest risk

For a given risk, want the highest expected return

Industry terminology is "efficient portfolio"

Portfolio with the minimum risk, for its expected return

Efficient in the sense of bearing only the risk necessary for the expected return

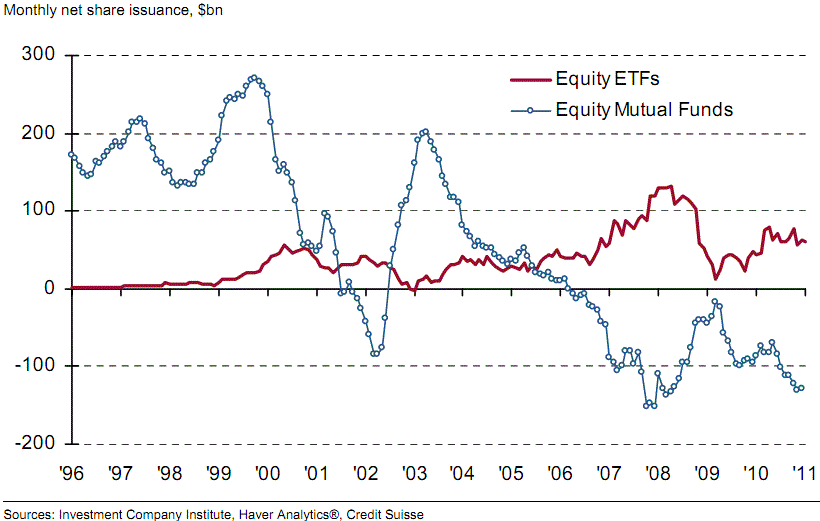

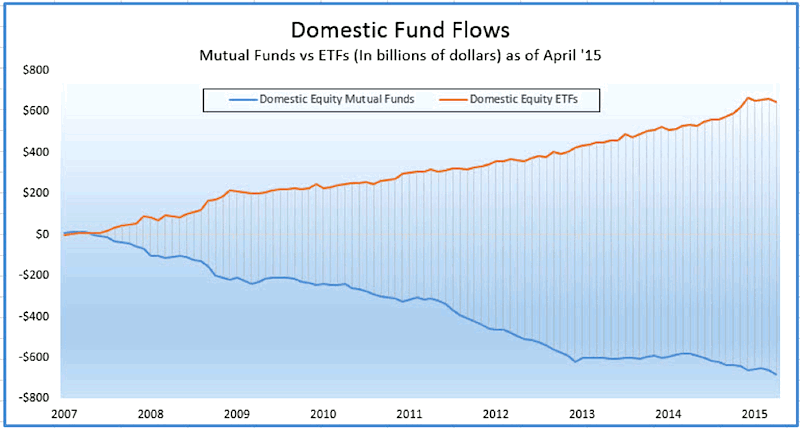

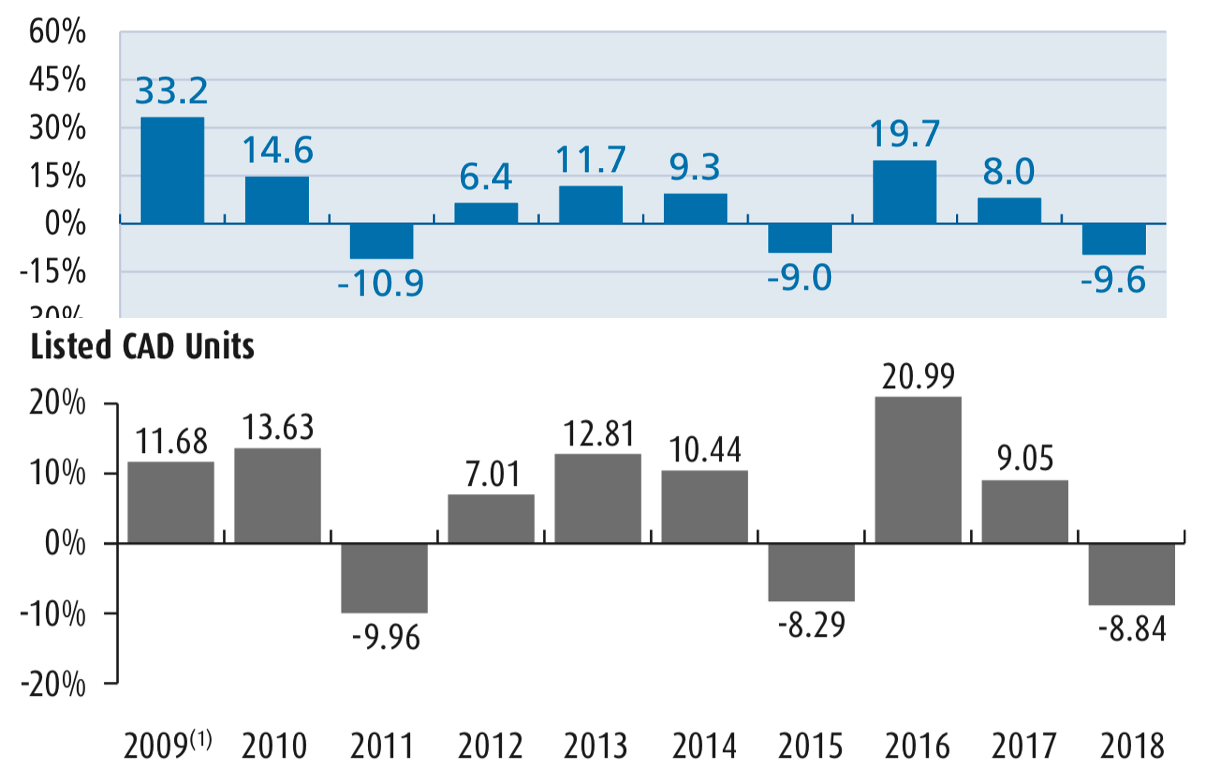

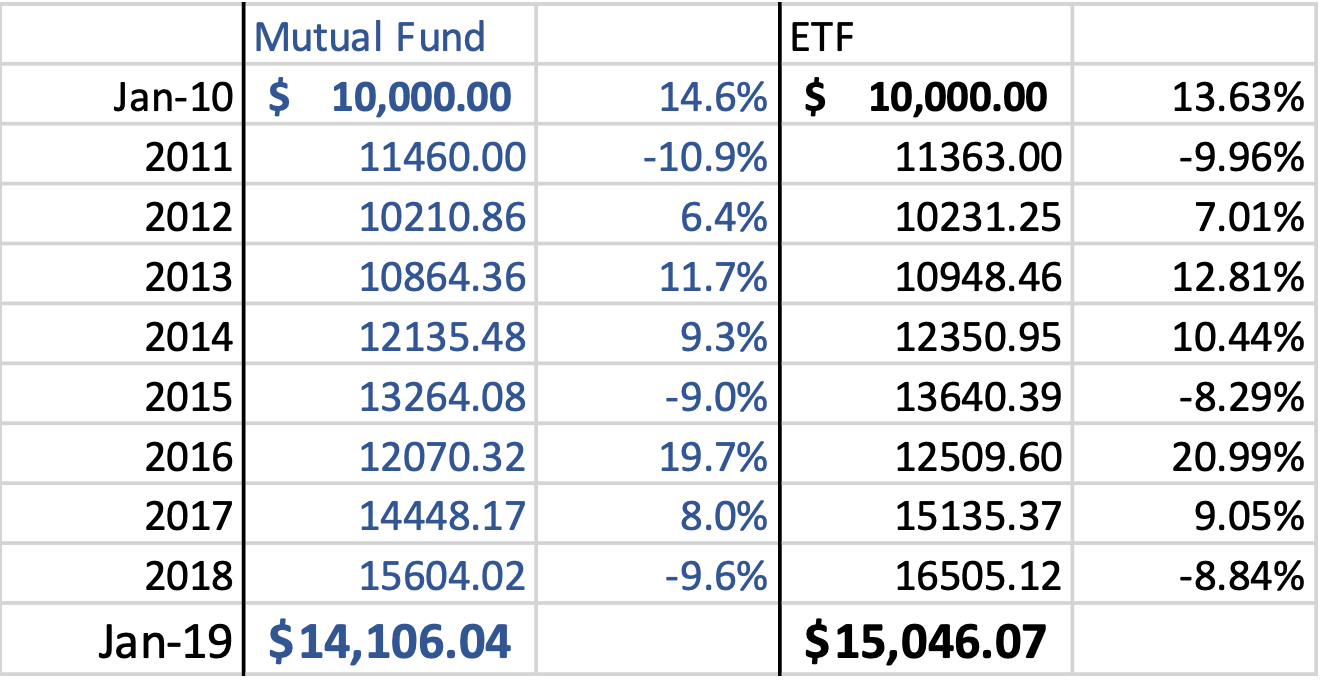

US data: https://www.seeitmarket.com/what-are-etf-and-mutual-fund-flows-trends-telling-investors-now-14449/

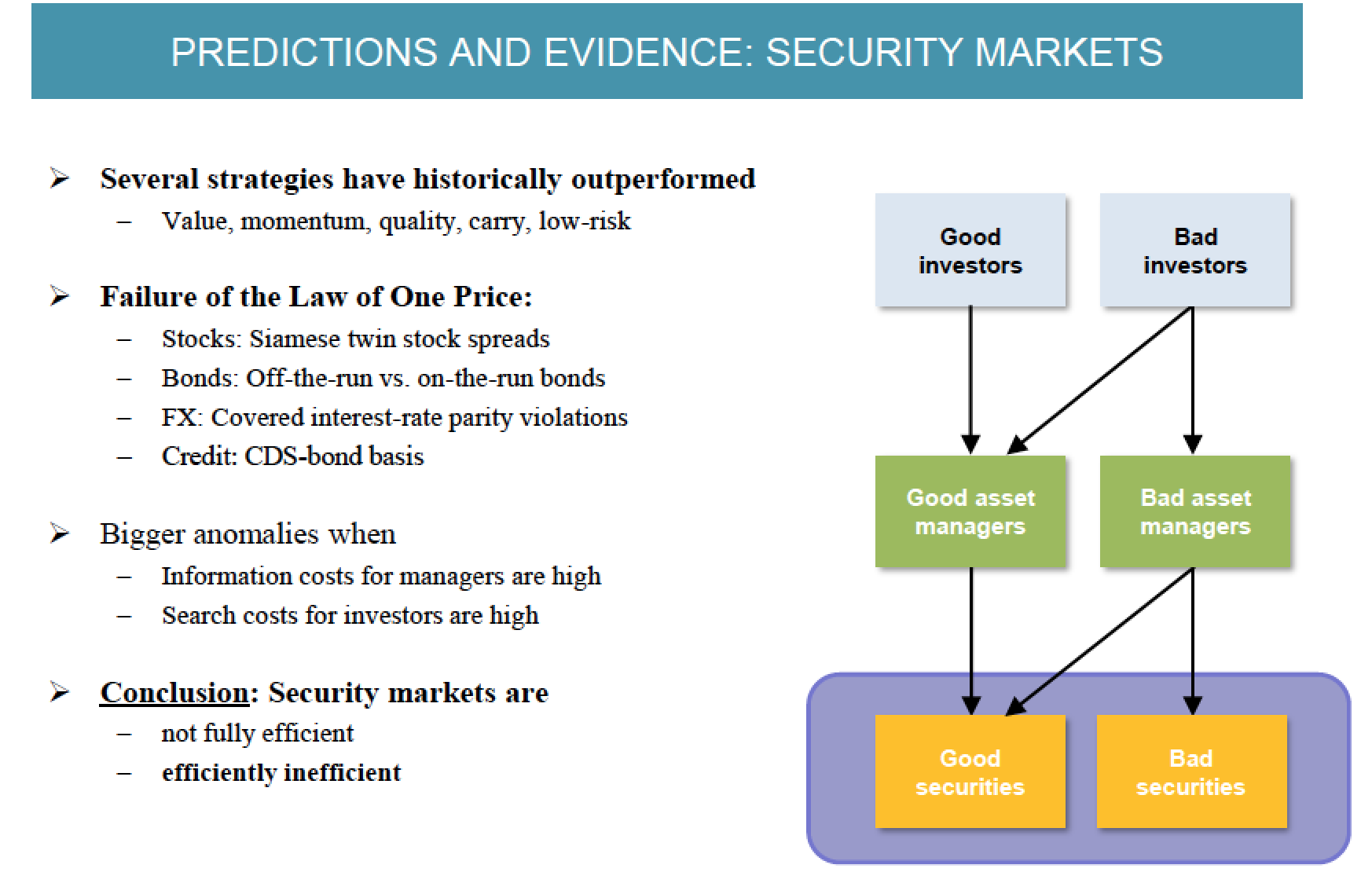

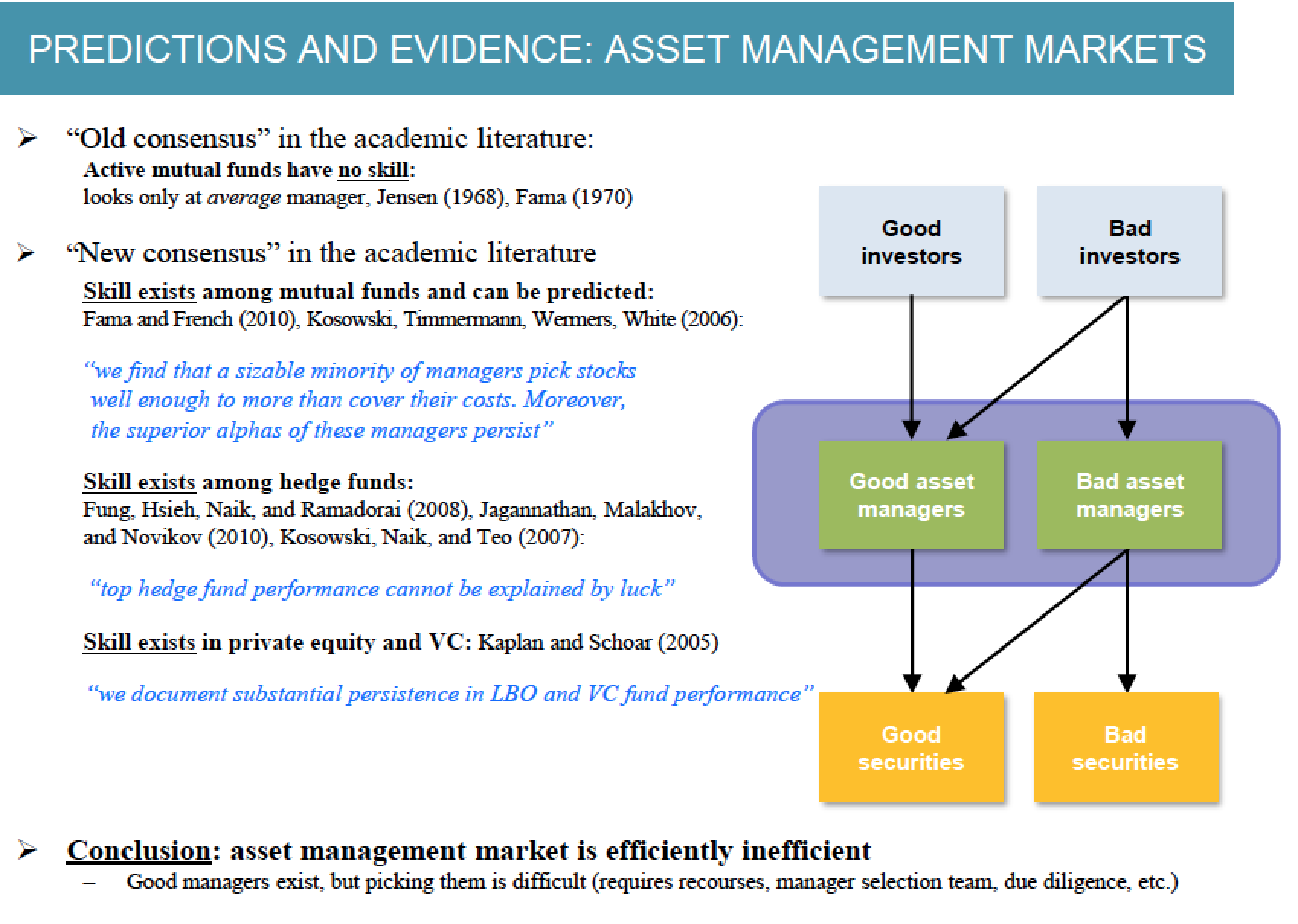

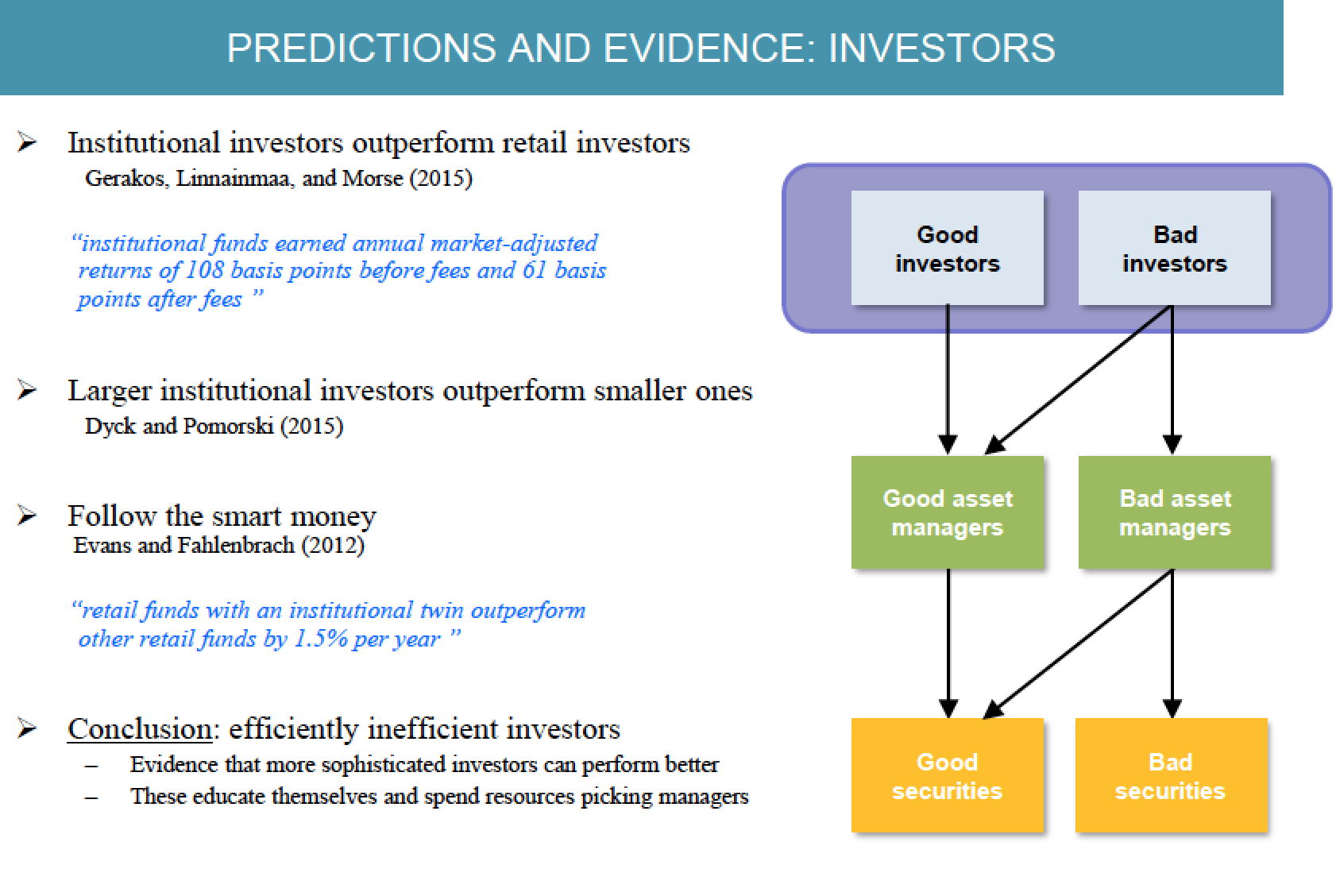

Based on

Capital Asset Pricing Model

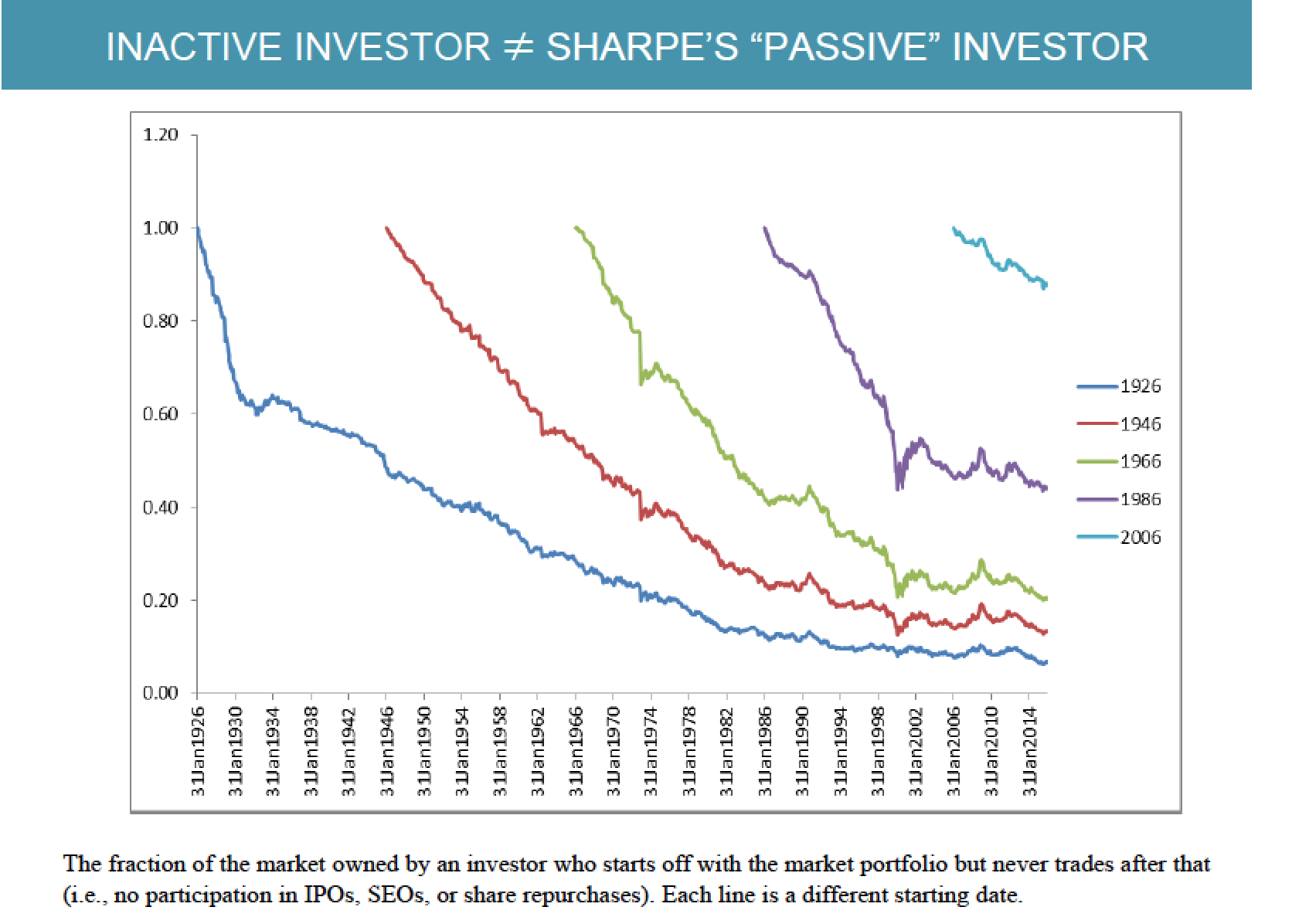

When passive trade, they are typically uninformed and lose money to the informed (hence, the latter can make money!)

\(\to\) most people need or look for help

\(\to\) investment advisor

Advice given fifty years ago

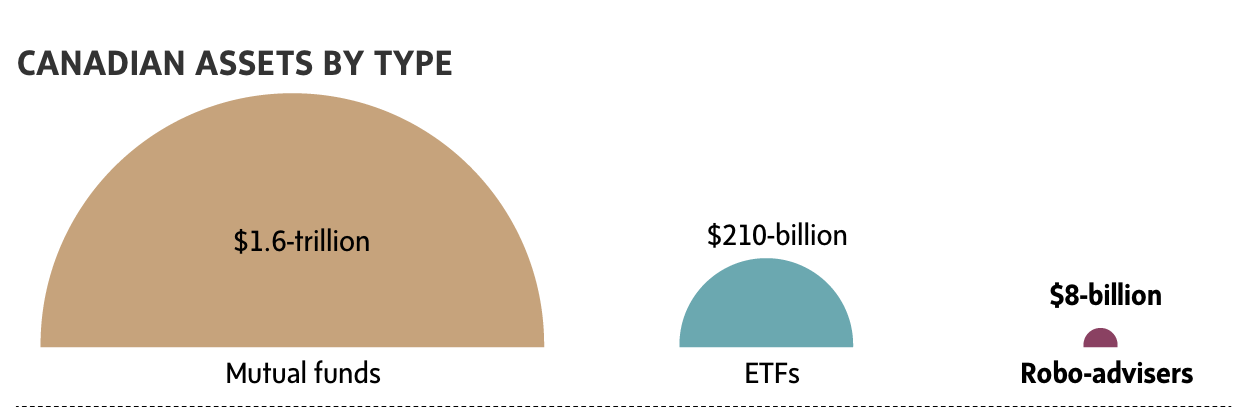

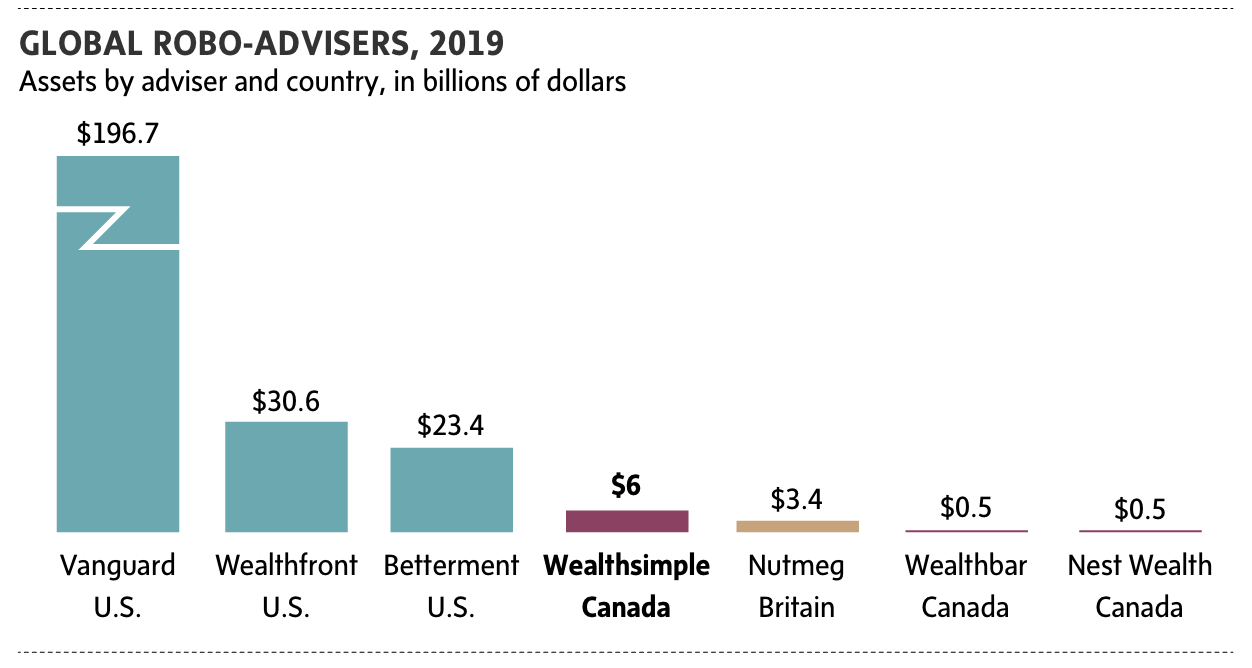

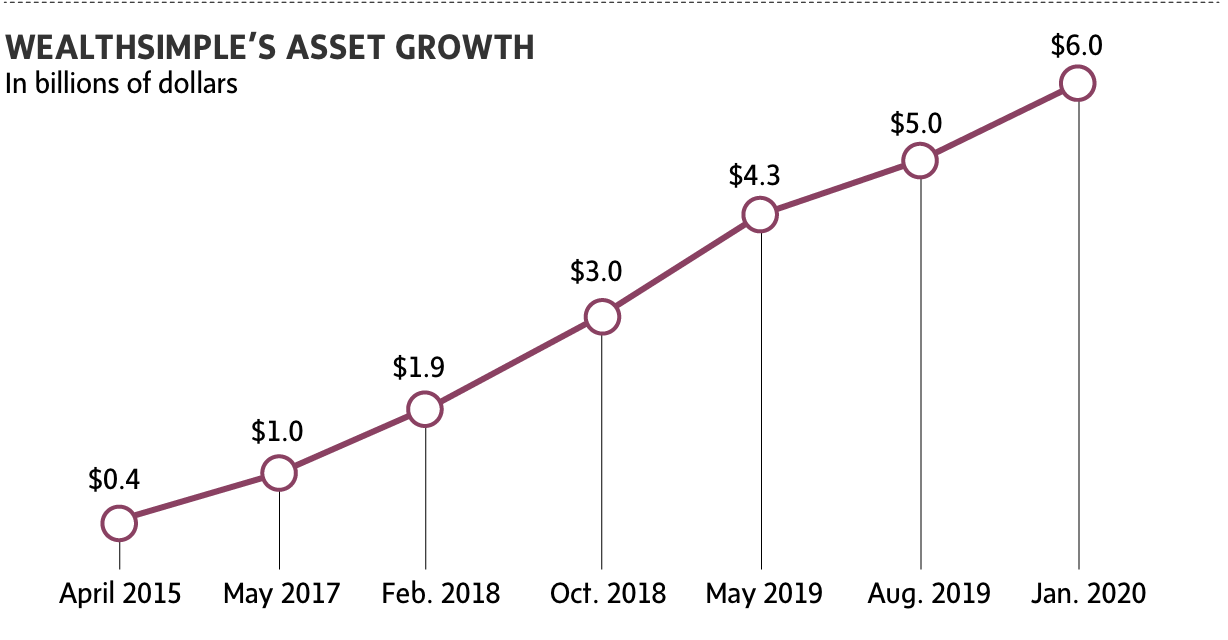

Globe and Mail Feb 2020

Recent development:

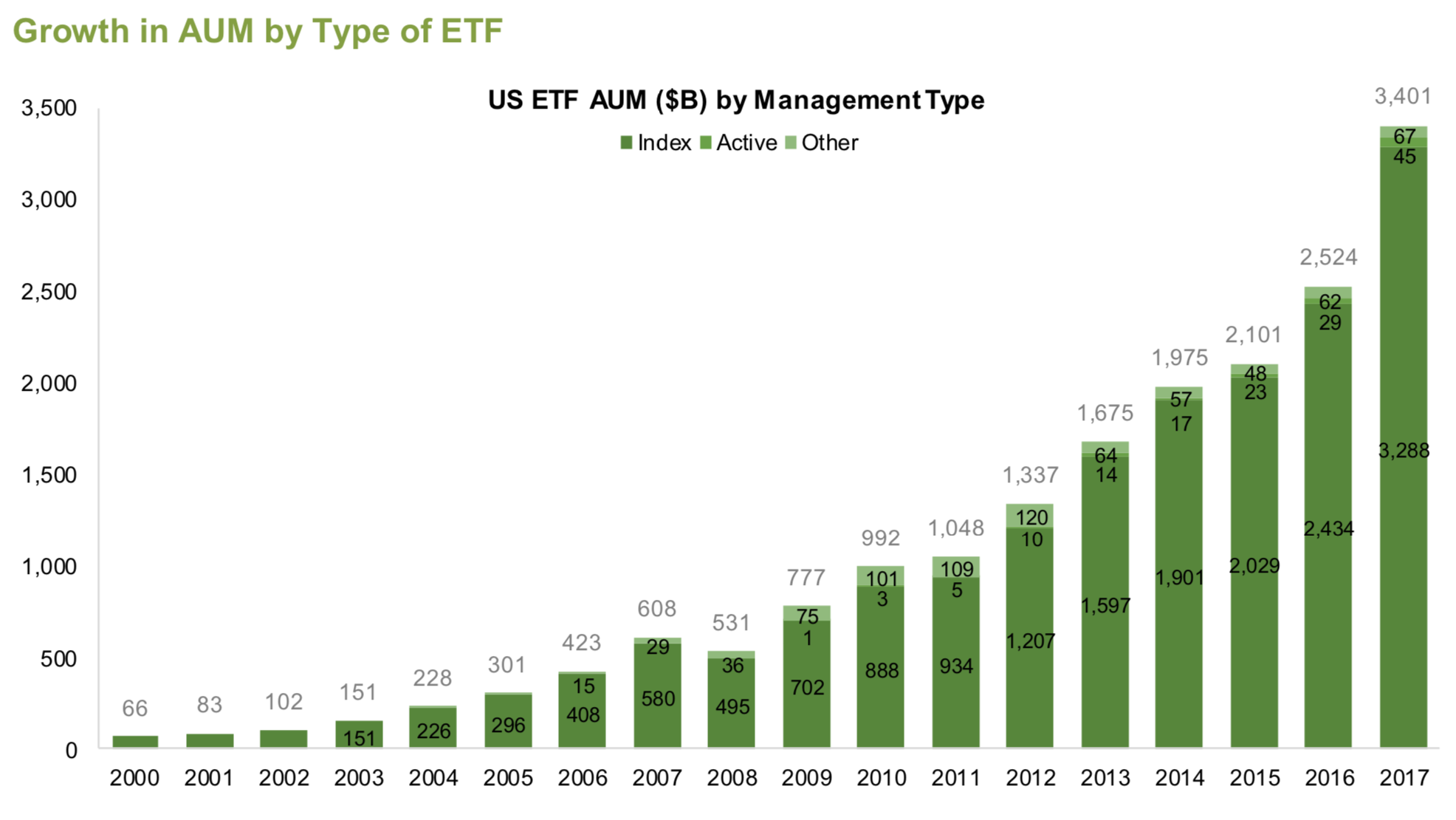

"active" ETFs with the usual fees

BUT: this all means 100,000 middle class jobs are at risk ...

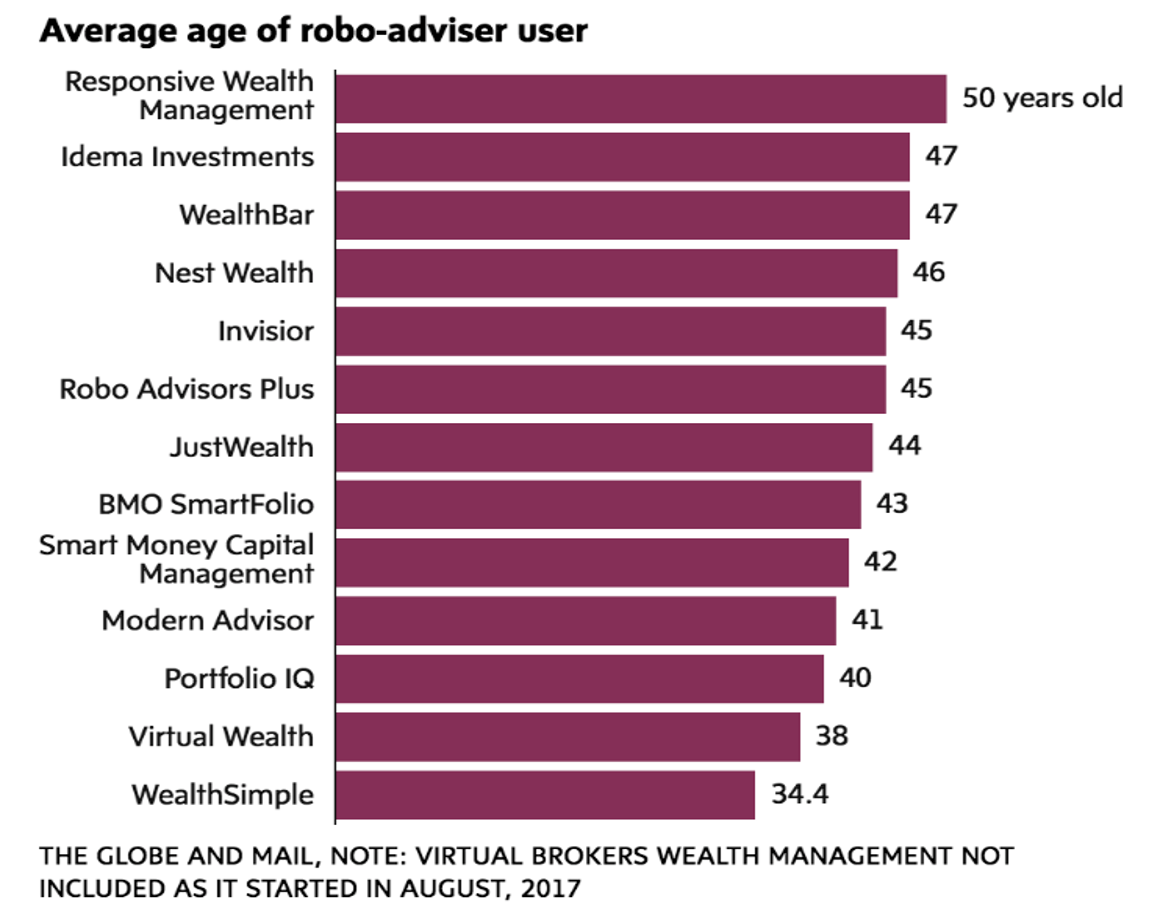

Gen X

Millenials

partnering with the wealth-management industry to license online technology to those investment firms who want to bring robo-adviser capabilities in-house for their financial advisers to use directly with clients

Source: D’Acunto, Prabhala, and Rossi: The Promises and Pitfalls of Robo-advising, RFS 2018

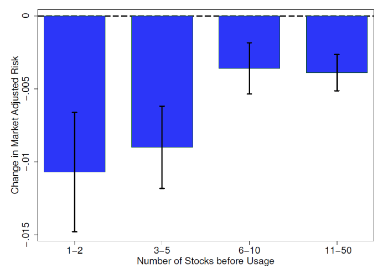

\(\to\) reduction in risk/better diversification

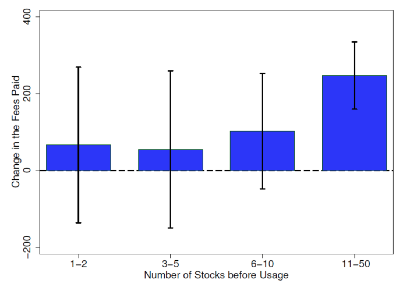

\(\to\) people with diversified portfolio trade much more

Source: Rossi & Utkus (2019) Who Benefits from Robo-advising? Evidence from Machine Learning

Source: Rossi & Utkus (2019) Who Benefits from Robo-advising? Evidence from Machine Learning

\(\to\) evidence clearly points to robo-advice being a positive development

By Andreas Park

This deck of slides is on WealthTech