Andreas Park PRO

Professor of Finance at UofT

Instructor: Andreas Park

Rotman – Master in Financial Risk Management

Financial Innovation

What's the relationship of payments and monetary policy?

A

B

\(-\)

0

+

A

B

0

+

\(-\)

Option 1: borrow from BoC

lending rate:

deposit rate:

target rate

target rate\(+\)25bps

target rate\(-\)25bps

A

B

0

+

\(-\)

Option 2: borrow from another bank

target rate

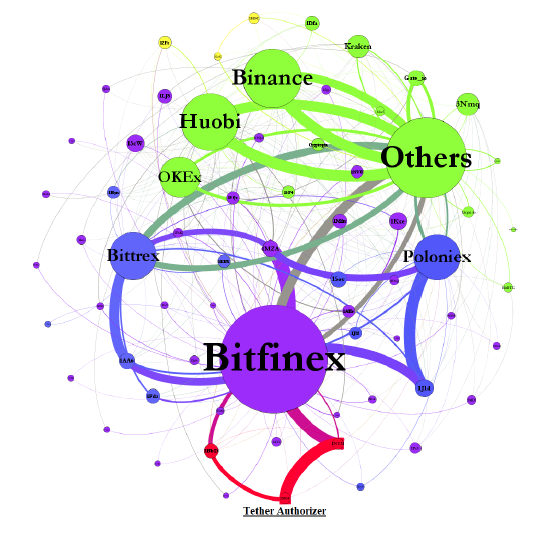

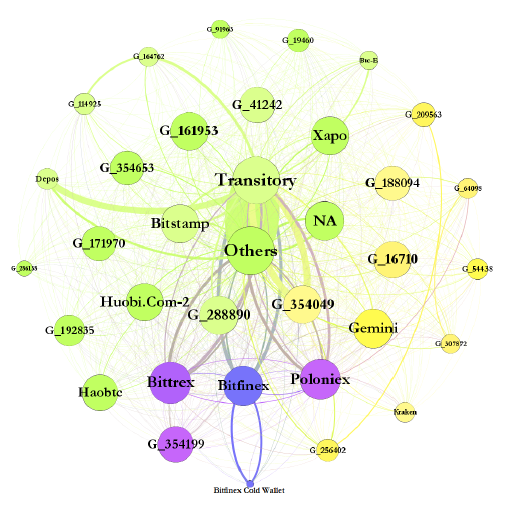

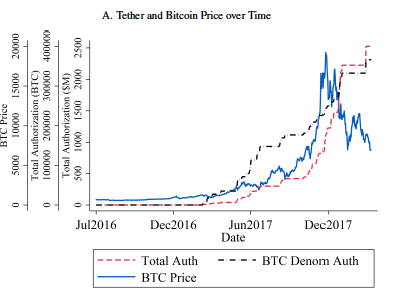

Why should we worry about private money? The Case of Tether

Historically: “Tether Platform currencies are 100% backed by actual fiat currency

assets in our reserve account.”

Text

Today: "The Tether Platform is fully reserved when the sum of all tethers in circulation is less than or equal to the value of our reserves."

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

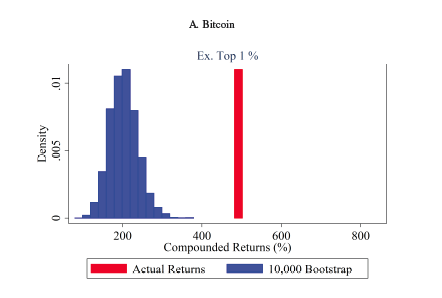

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

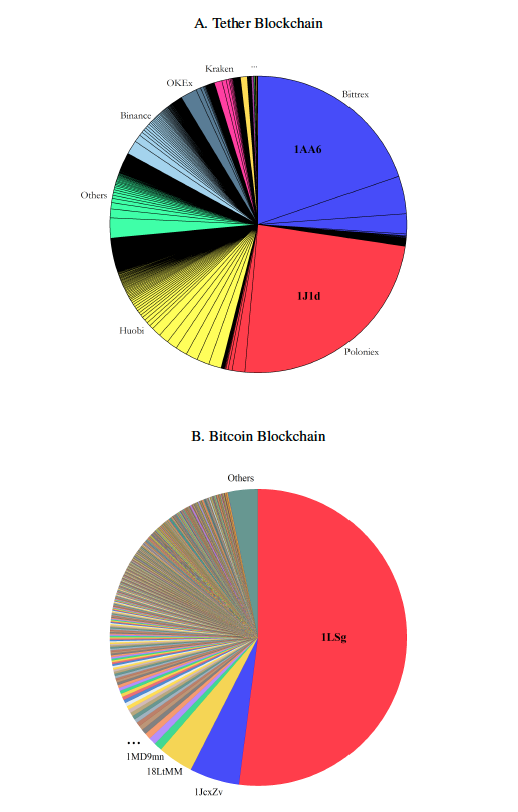

Figure 1. Aggregate Flow of Tether between Major Addresses

Figure 3. Aggregate Flow of Bitcoin between Major Addresses.

Top Accounts Associated with the Flow of Tether from and Bitcoin to Bitfinex

the 1% of hours with the strongest lagged Tether flow are associated with 58.8% of the Bitcoin buy-and-hold return over the period.

the "normal-times" returns

Related Development: Libra

Partnerships

"new financial infrastructure"

My prediction: Libra Network will go live in the Spring of 2021

issued by a consortium of firms (e.g., Facebook, Stripe, Lyft) and not-for-profits (Creative Destruction Lab)

two types of coin: single-currency stablecoins and multi-currency stablecoin, fully backed by reserves

idea is conceptually similar to IMF Special Drawing Rights (pegged to USD, EUR, YEN, GBP, YUAN)

in Libra, this coin is a composite, not separate asset

not "pegged", but will fluctuate relative to any other currency (a bit like an ETF)

eventually transition to a permissionless system.

Problem: perimeter control - can unknown participants take control of the system and remove key compliance provisions?

\(\to\) not happening

Modeled after mutually owned stock exchanges

Expanding membership with competition for slots

hope: replicate key economic properties of a permissionless system through an open, transparent, and competitive market for network services and governance.

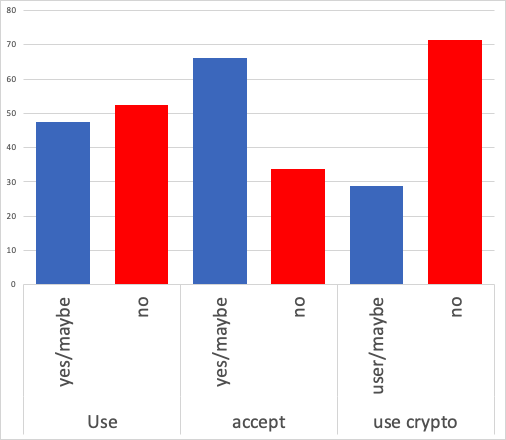

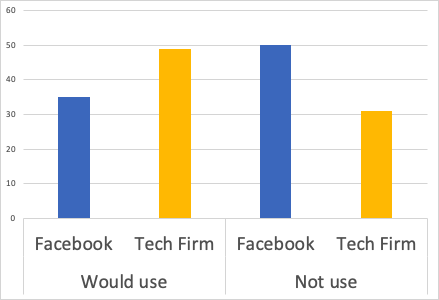

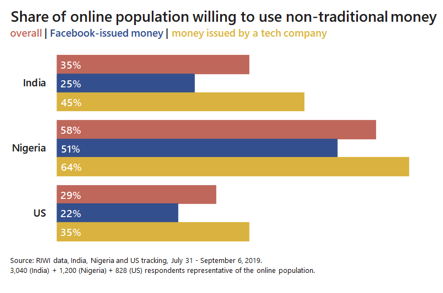

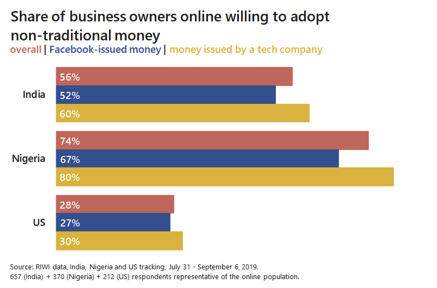

Would you use Libra/Money issue by Tech Firm?

If we ask explicitly for Facebook vs Tech Firm

Scaled to yes/maybe/no. About 20% say: "Need more info"

Source: Will Libra Succeed? Results of a Global Randomized Survey Experiment; by Danielle Goldfarb and yours truly

They have ZERO interest in becoming a financial institution/bank

\(\rightarrow\) no expertise

\(\rightarrow\) competitive market

\(\rightarrow\) one of the most regulated business environments

They are trying to deal with frictions that impede their business

They aim to collect data which will vastly improve their business

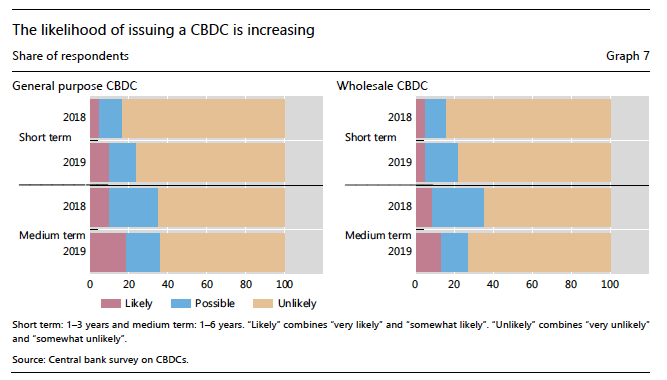

Related Development: Central Bank-Issued Digital Currencies

Source: BIS Quarterly Review, March 2020

BoC analysis (August 2020):

Would a CBDC improve the efficiency of its currency function?

Would CBDC improve the efficiency and safety of both retail and large-value payment systems?

Is CBDC an appropriate policy response to payment innovations such as privately issued e-money and digital currency to achieve its monetary policy goals and to implement policies promoting financial stability?

"Central Bank Digital Currencies: A Framework for Assessing Why and How " Fung and Hallaburda 2016, BoC Working Paper

Contingency Planning for a Central Bank Digital Currency (BoC website)

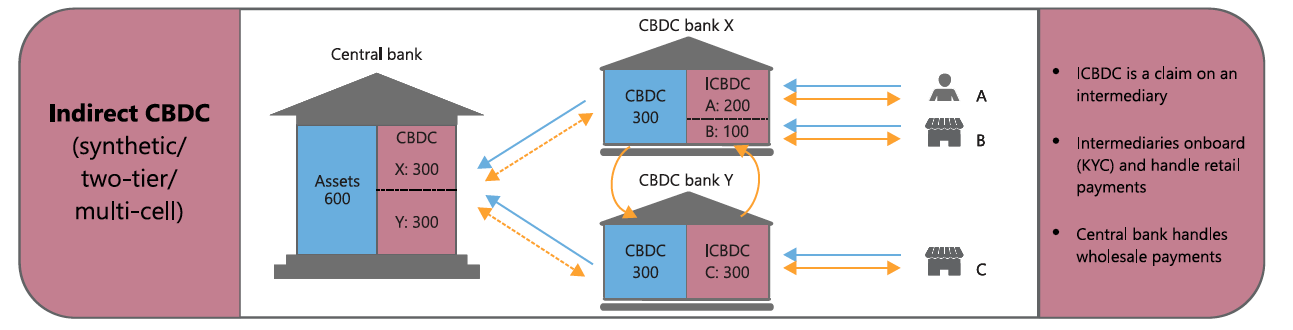

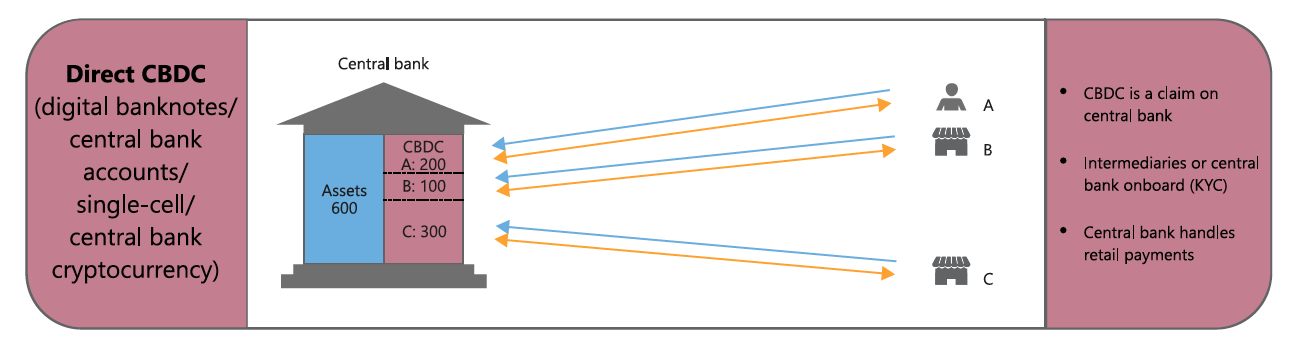

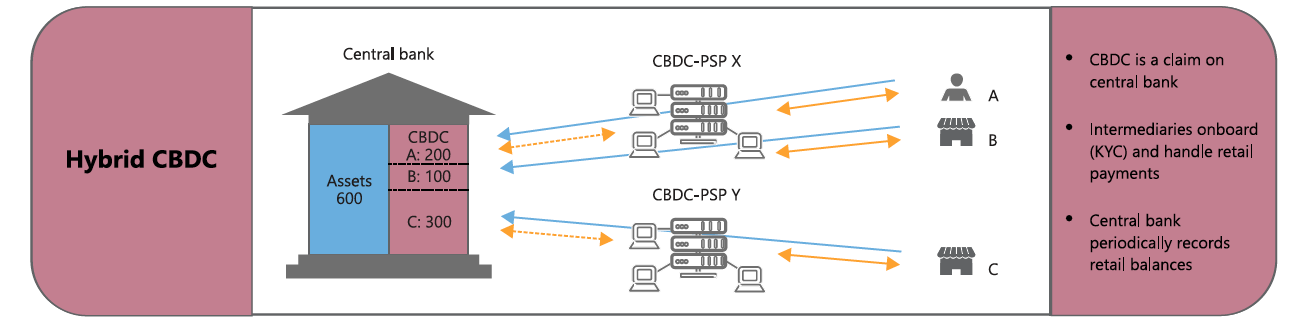

CBDC: Token vs Accounts

CBDC: Token vs Accounts

identification of the object being transferred as a means of payment

identification of the individual whose account is being debited

example: cash

example: ETH

Should the central bank issue e-money? Kahn, Rivadeneyra, Wong, Bank of Canada working paper 2019

A Taxonomy

Bech and Garratt (2017)

Prevailing view: account-based central bank e-money system is unlikely to be the preferred choice of policymakers

Tokens or Accounts?

Prevailing view: account-based central bank e-money system is unlikely to be the preferred choice of policymakers

Why not?

Some history on private money

CBDC: Impact of "Global" Money

CBDC: Impact of "Global" Money

Cryptocurrencies, Currency Competition and the Impossible Trinity

Benigno, Schilling, Uhlig (2020)

Old: impossible trinity

New: with free capital and global currency, equalization of national policy interest rates

\(\to\) less of a point of national currency

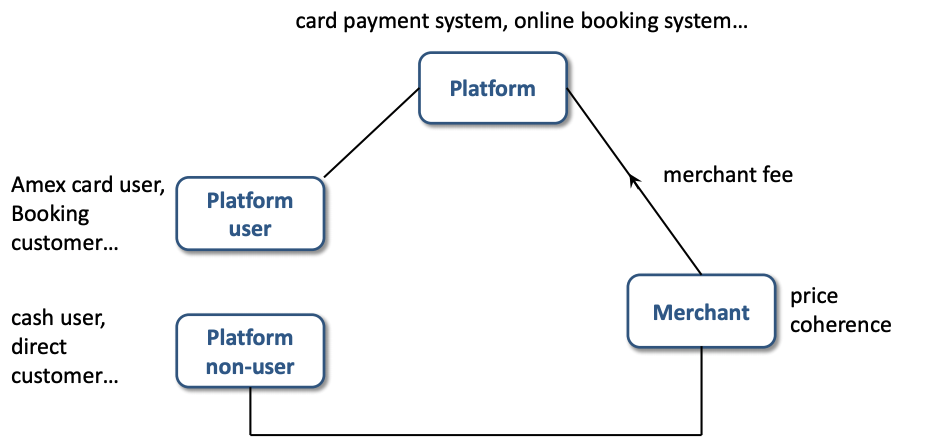

Platform Economics

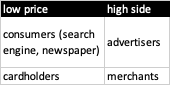

Examples of platform markets

gamers

users

“eyeballs”

cardholders

videogame platform

operating system

portals, newspapers, TV

debit & credit cards

game developers

application developers

advertisers

merchants

buyer

platform

seller

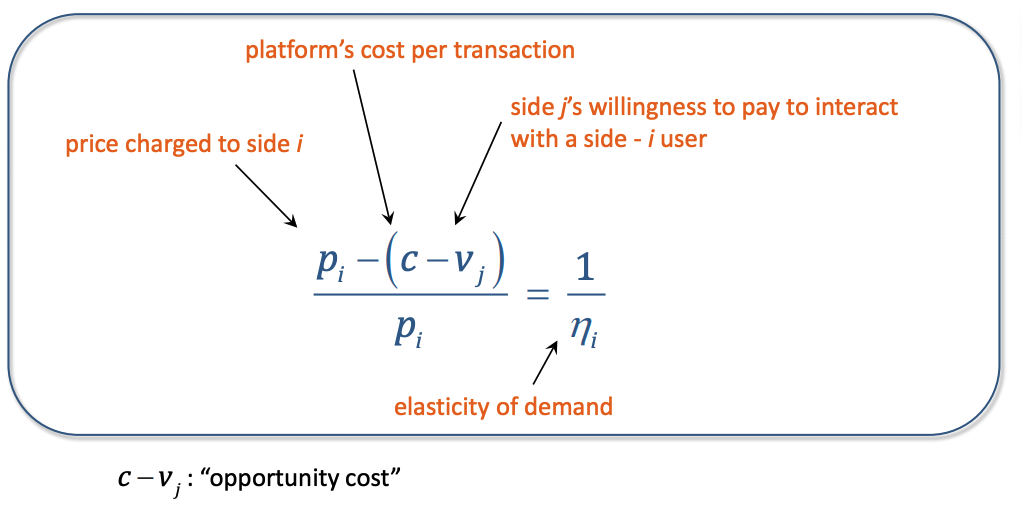

Platform pricing

Source: Jean Tirole's Nobel Lecture

Implications for the platform business model

Source: Jean Tirole's Nobel Lecture

Simple Example: heterosexual clubbing

assumption: people go clubbing to meet the opposite gender

common problem: imbalance of people from each gender

common solution: differential pricing (including free entry) for one side of the market

Regulation?

Question: is it a must-use arrangement or do people have alternatives?

By Andreas Park