Andreas Park PRO

Professor of Finance at UofT

Instructor: Andreas Park

Rotman – Master in Financial Risk Management

Financial Innovation

Application: Issuing and transferring money

store of value?

unit of account?

method of exchange?

\(\to\) does not require "double coincidence of wants"

\(\to\) don't have to price everything relative to each other

\(\to\) don't have to spend money immediately upon receiving it

Idea:

Sidebar: what is a DAO?

4 ETH

(1 ETH = $375)

(Oct 15, 2020)

\(\approx\) $1,500

\(\vdots\)

1,500 DAI

(1 DAI = $1)

formally: this smart contract is a collateralized debt position (CDP)

fractional collateral \(\to\) collateralization factor \(=\) 150%

total collateral = $1,500

maximum loan = $1000

overcollateralization = $500

actual loan (example) = $500

buffer = $500

ETH \(\nearrow\) $500

value of ETH collateral = $2,000

maximum loan = $2,000/150%=$1,333

total collateral = $2,000

maximum loan = $1,333

overcollateralization = $667

actual loan (example) = $500

buffer = $500

overcollateralization = $667

new loan capacity= $333

ETH \(\searrow\) $187.5

value of ETH collateral = $750

maximum loan = $750/150%=$500

total collateral = $750

maximum loan = $500

overcollateralization = $250

actual loan (example) = $500

buffer = $0

for reference: former value of collateral

ETH \(\searrow\) $150

value of ETH collateral = $600

maximum loan = $600/150%=$400

total collateral = $600

maximum loan = $400

required overcollateralization = $200

actual loan (example) = $500

buffer = -$100

for reference: former value of collateral

\(\Rightarrow\) liquidation possible by "keeper"

sell 3.33 ETH=$500=500 DAI

repay $500=500 DAI loan

retain incentive

return ETH remainder to pool

\(\Rightarrow\) all relies on behavioral assumptions

\(\Rightarrow\) But: there are also real incentives & mechanisms

borrowers of DAI need to pay interest \(\to\) stability fee

DSR paid on "locked" DAI

total amount of debt (or DAI) outstanding is limited

Sidebar: how is this decided?

\(\to\) special "governance" token MKR

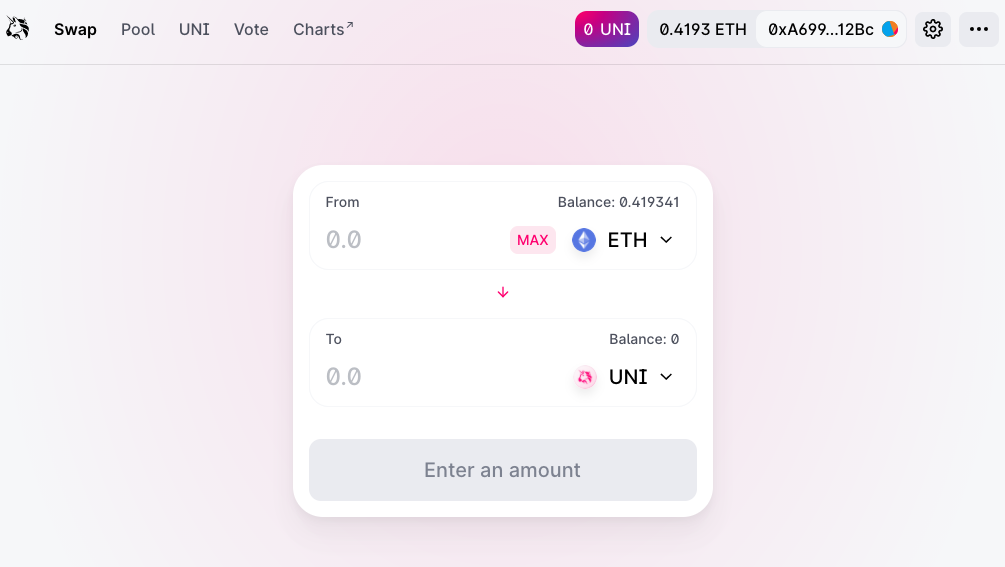

Application: asset trading

Note: we are covering trading in a separate set of slides; I am including them here for completeness

Investor

Broker

Venue

Settlement

Exchange

Wholeseller

Darkpool

Internalizer

Venue

Settlement

Investor

On chain

Idea:

Price mechanism:

Prices

invariant \(k=4\times4=16\)

Instantaneous exchange rate:

1 = 1

Contract deposit:

sell 4 DAI for USDC

what price will therefore be quoted?

how many USDC?

Problem: large "slippage" (or price impact)

establish and sell a new token

front-running

transactions enter mem-pool

\(\to\) all visible there

arbitrageur make instant-swap trade at higher gas price

\(\to\) trade instead of original trade

\(to\) reverse to gain slippage from earlier trader

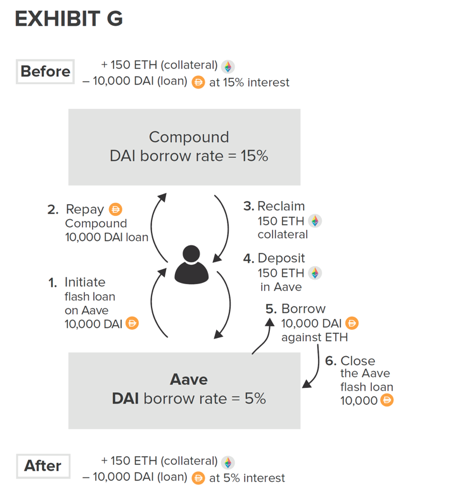

take three pairs (ignore that BTC is not directly on Ethereum)

BTC-DAI

ETH-BTC

ETH-DAI

\(\to\) simply connect with MetaMask (or similar wallet)

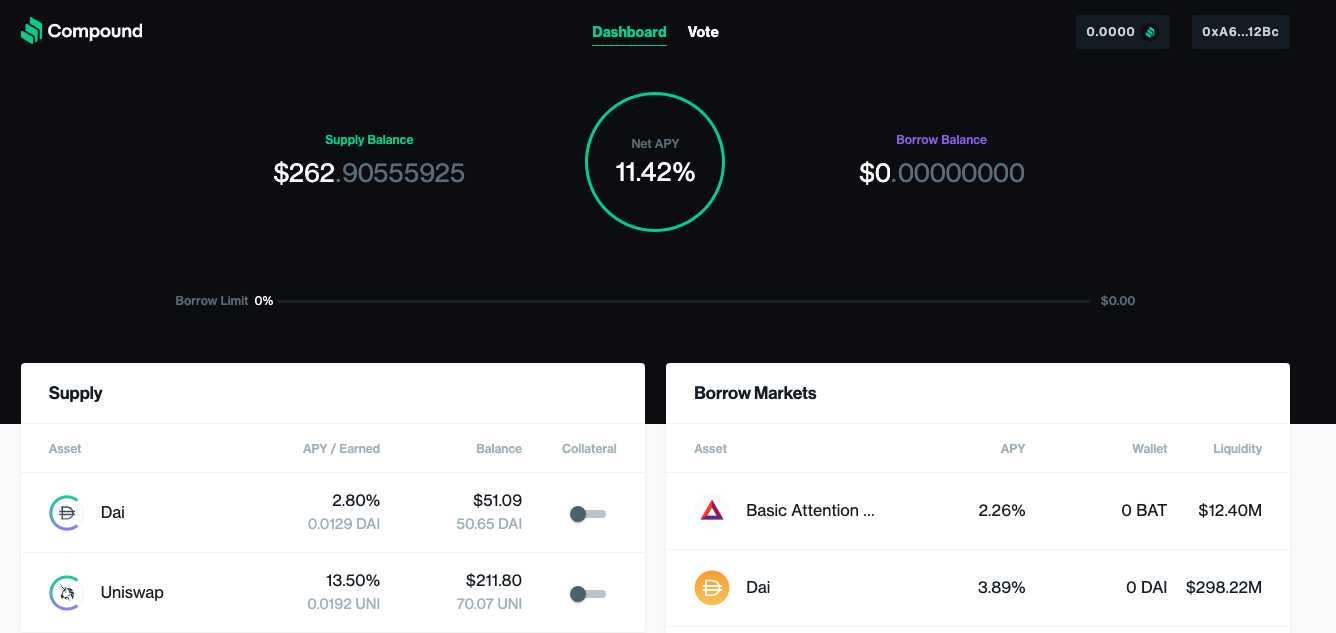

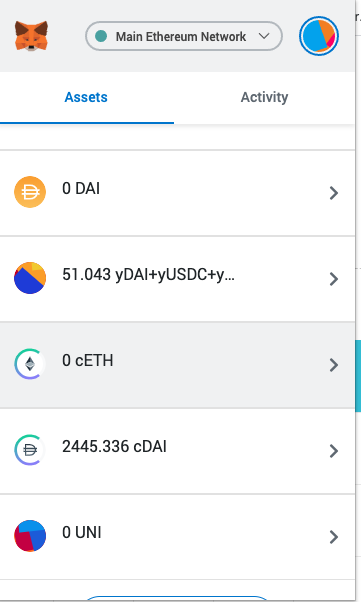

Application: Innovative Lending

Fundamentally, what does a bank do?

And how is this done?

on blockchain

Example 1

Example 2

Example 3

borrowing and lending rates compounded per block

100%

fraction of supplied that's been borrowed

base rate

borrow rate

common theme in DeFi: jumping between dApps

Source: Harvey, Ramachandran, and Santoro (2020)

Application: Derivatives

1 ETH = 300 DAI

collateralization ratio 125%

seller

buyer

supplies 1 ETH collateral today

mints (=borrows) 100 yDAI to be repaid in 1 year

y

receives 92 DAI today

pays 92 DAI today

y

receives 100 yDAI

repays loan with 100 DAI

deposits yDAI and receives 100 DAI

seller

buyer

Scenario 1: ETH \(\searrow\)100 DAI

keeper

closes undercollateralized position \(\to\) sells 0.8 ETH for 100 DAI

receives 100 DAI early

receives balance

of 0.2 ETH

seller

buyer

Scenario 2: ETH \(\ge\)125 DAI

deposits 100 yDAI

withdraws 100 DAI

receives balance of 1 ETH - 100 DAI

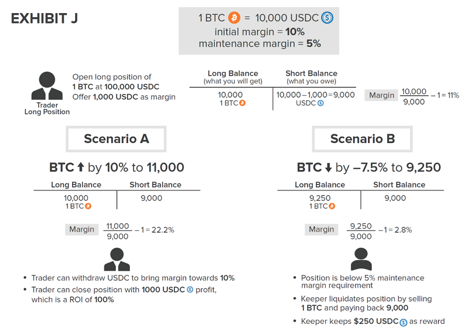

main product:

BTC perpetual futures contract

initial margin =

amount of collateral needed to be posted

maintenance margin =

amount of price movement after which collateral needs to be replenished

Source: Harvey, Ramachandran, and Santoro (2020)

Application: Innovative Financing Tools

Data: coinschedule

for comparison: total size of

Toronto Stock Exchange: $2,200B

Toronto Venture Exchange: $41B

can finance projects that otherwise would find no debt or equity funding

enable network effects and new business opportunities

allows entrepreneurs to extract more surplus

can finance projects that otherwise would find no debt or equity funding

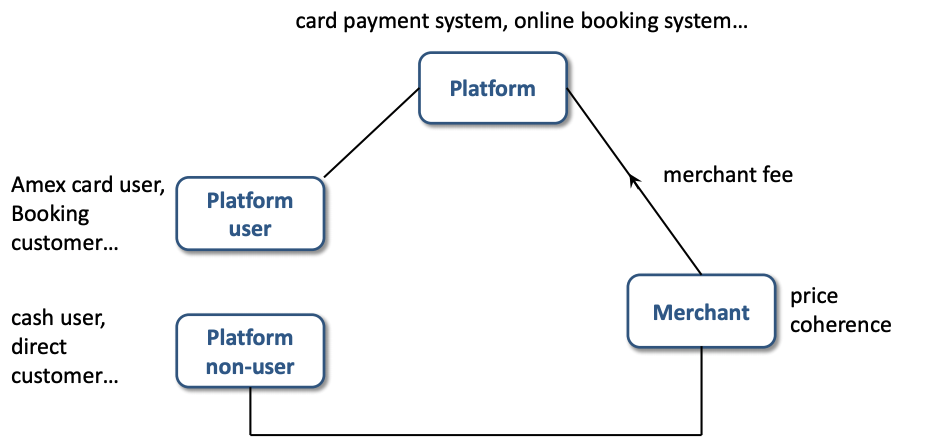

Platform Economics

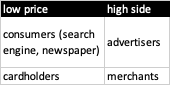

Examples of platform markets

gamers

users

“eyeballs”

cardholders

videogame platform

operating system

portals, newspapers, TV

debit & credit cards

game developers

application developers

advertisers

merchants

buyer

platform

seller

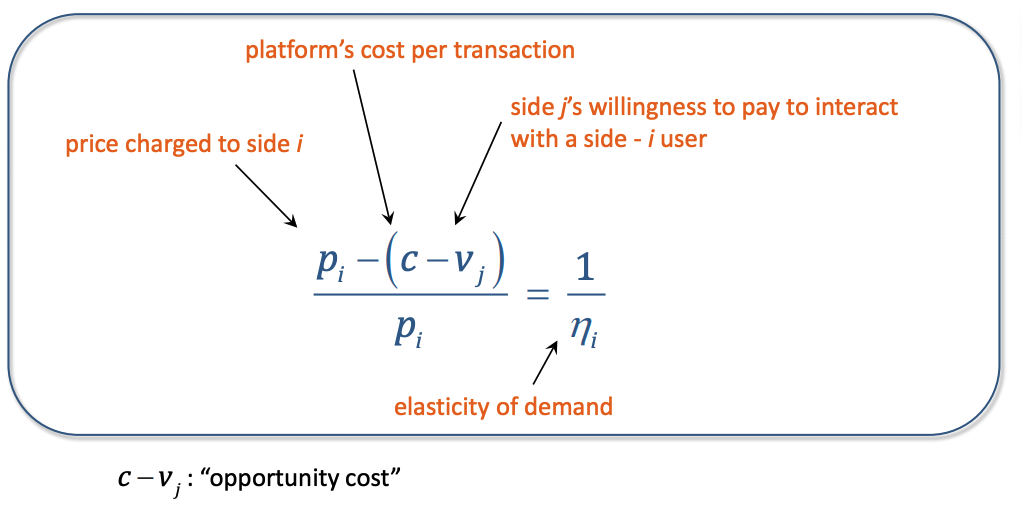

Platform pricing

Source: Jean Tirole's Nobel Lecture

Implications for the platform business model

Source: Jean Tirole's Nobel Lecture

Simple Example: heterosexual clubbing

assumption: people go clubbing to meet the opposite gender

common problem: imbalance of people from each gender

common solution: differential pricing (including free entry) for one side of the market

Regulation?

Question: is it a must-use arrangement or do people have alternatives?

By Andreas Park

This slide deck briefly discusses and reviews popular DeFi applications for MFRM RSM6313.