Andreas Park PRO

Professor of Finance at UofT

New symbols?

What's notable about the security?

Calls for SAC

What do you have to do?

you wrote the call \(\to\) you are the market maker and have to hedge your position

Anything special?

dig deep into your options knowledge and recall what delta-hedging is

\(uS\)

\(dS\)

Task: find \(H\) and \(B\) such that you match the payoffs of the call!

\[H\cdot u\cdot S+B\cdot R_f = C_u\]

\[H\cdot d\cdot S+B\cdot R_f = C_d\]

\[H=\frac{C_u-C_d}{(u-d)S},~~B=\frac{uC_d-dC_u}{(u-d)R_f}.\]

The Solution:

risk free investment \[B= \frac{uC_d-dC_u}{(u-d)R_f}.\]

\(H=\text{the Delta}=\text{change in call values per change in underlying stock}.\)

\[C=HS+B=\frac{C_u-C_d}{(u-d)S}\cdot S +\frac{uC_d-dC_u}{(u-d)R_f}\]

Knowledge piece:

Idea: if \(q\) would be the true probability of \(u\), then investors behave as if they are risk-neutral.

After simplifications:

\(C=\frac{1}{R_f}\left(q\cdot C_u+(1-q)\cdot C_d\right)\) where \(q=\frac{R_f-d}{u-d}.\)

Price can go to

\(u^2S\)

\(d^2S\)

\(udS=duS\)

\(u^2S\)

\(d^2S\)

\(udS\)

That looks like a binomial formula!

\[u =\exp(\sigma\sqrt{\Delta t}),\]

\[d =\exp(-\sigma\sqrt{\Delta t}).\]

\[C=\frac{1}{{R_f}^2}\sum^N_{j=0}\underbrace{\left(N \atop j\right)q^j(1-q)^{N-j}}_{\text{prob of \(j\)ups}\atop \text{in \(N\)rounds}}\cdot \underbrace{\max(0,u^jd^{N-j}S-X)}_{\text{option payoff of \(j\)ups}\atop \text{and \(N-j\)downs}}.\]

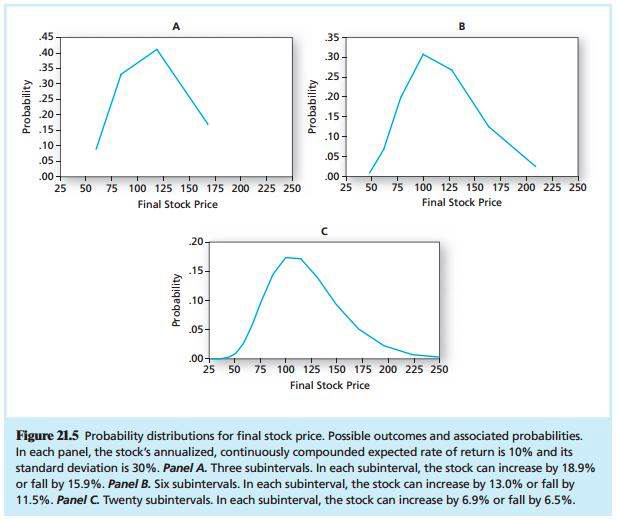

With more rounds/periods, the probability distribution of the final stock prices looks smoother and smoother.

Price of a European call:

\[C=S\cdot N(d_{1})-X\cdot e^{-rT}\cdot N(d_{2})\]

\(C=\)Current call option value

\(S=\)Current stock price

\(N(d)\)= probability that a random draw from a normal distribution will be less than \(d\),

\(X =\)Exercise price

\(r=\)Risk-free interest rate (annualized, continuously compounded with the same maturity as the option)

\(T =\)time to maturity of the option in years

\(\sigma = \)Standard deviation of the stock.

where

\(d_{1} = \frac{ \ln\left( \frac{S}{X}\right) + T\left(r + \frac{ \sigma^2}{2}\right)}{ \sigma \sqrt{T}}, \)

\(d_{2} = d_{1} - \sigma \sqrt{T}.\)

Initial replicating portfolio:

Black-Scholes "hugs" the curve of the payoff at maturity and gets closer has \(t\to\) maturity

steep slope = high hedge ratio

flat slope = low hedge ratio

Unobservable input: volatility.

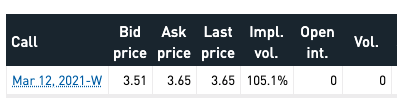

XIU Options from the Montreal Exchange

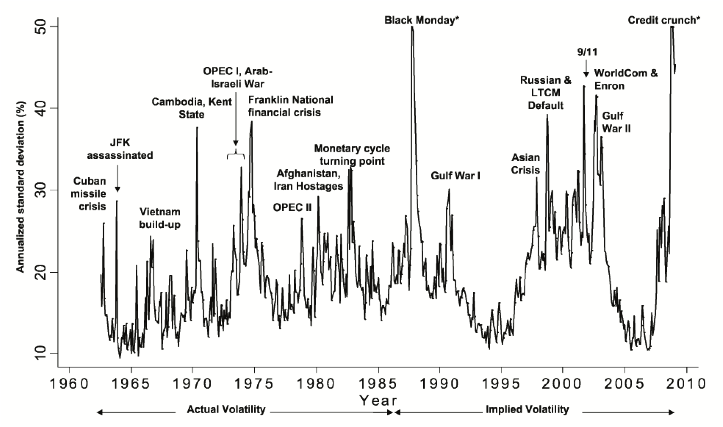

Source: Bloom (2009). The Impact of Uncertainty Shocks. Econometrica 77(3), 623-685.

when things go bad, you want your investment loss limited,

but you also want to benefit from the upside

slightly (but crucially) imprecise because the plot ignores the cost for the option \(\to\) insurance isn't free!

\(S\)

secure \(S\)

benefit from upside

\(S\)

\(S\)

\(S\)

secure \(S\)

benefit from upside

\(S\)

\(S\)

Cost of strategy 1: stock + put = \(S+P\)

Cost of strategy 2: bond + call = \(PV(S)+C\)

BUT: they provide the same payoff profile at maturity

\(\Rightarrow\) The Law of One Price applies

bond + call = stock + put

\(\Leftrightarrow\) \(S+P = PV(S)+C\)

Please note: this doesn't tell you the right price for a call, it tells you the relationship between put and call prices.

What do you have to do?

you wrote the call \(\to\) you are the market maker and have to hedge your position

Anything special?

By Andreas Park