Andreas Park PRO

Professor of Finance at UofT

Sniping in Fragmented Markets

Katya Malinova (DeGroote School of Business)

Andreas Park (University of Toronto)

Western Finance Association 2020

1,000

Shares at Canadian Offer

300

400

investor sends buy order to broker

buy 1,500 shares

for trader: no-trade-through regulation => broker must split among three venues

Shares

1-tick off

400

100

2,000

Many questions in microstructure relate to multi-markets, for instance,

buy 1,500 shares

buy 400 shares

buy 1,000 shares

buy 100 shares

fundamental problem for researcher:

how can we string together trades across many venues?

fundamental advantage that we have:

we can string together trades and we can differentiate (somewhat) what comes first and what follows

Note: NBBO depth (and depth at the largest market) is usually larger than 100 shares

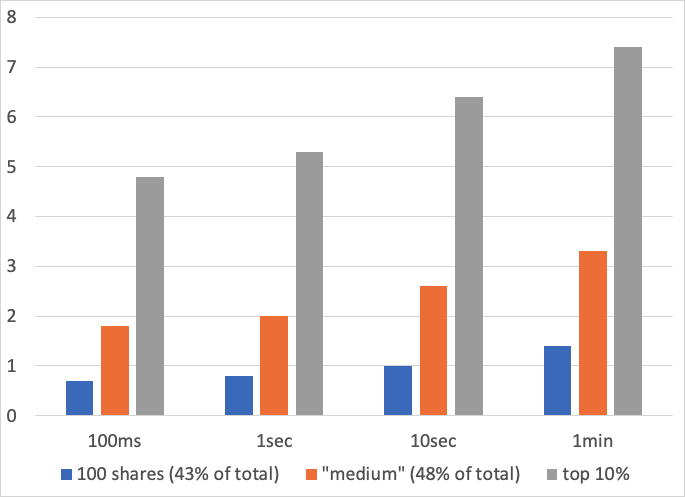

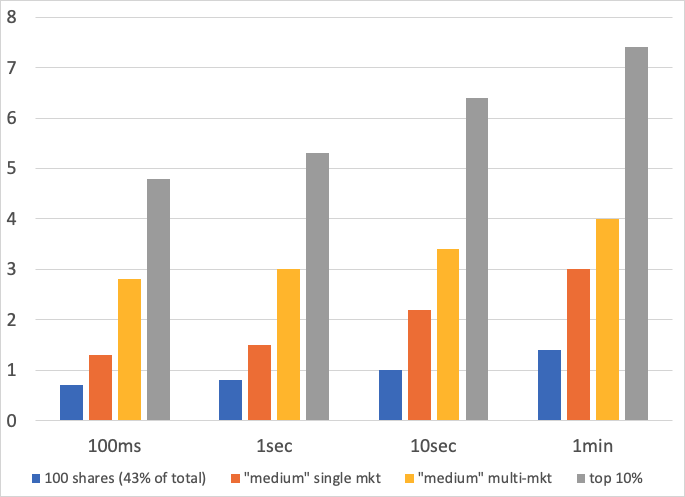

Use the same classification as Comerton-Forde, Malinova, Park (JFE 2019), loosely:

Fun Fact: retail trades are on average larger than institutional trades

medium:

Fun Facts:

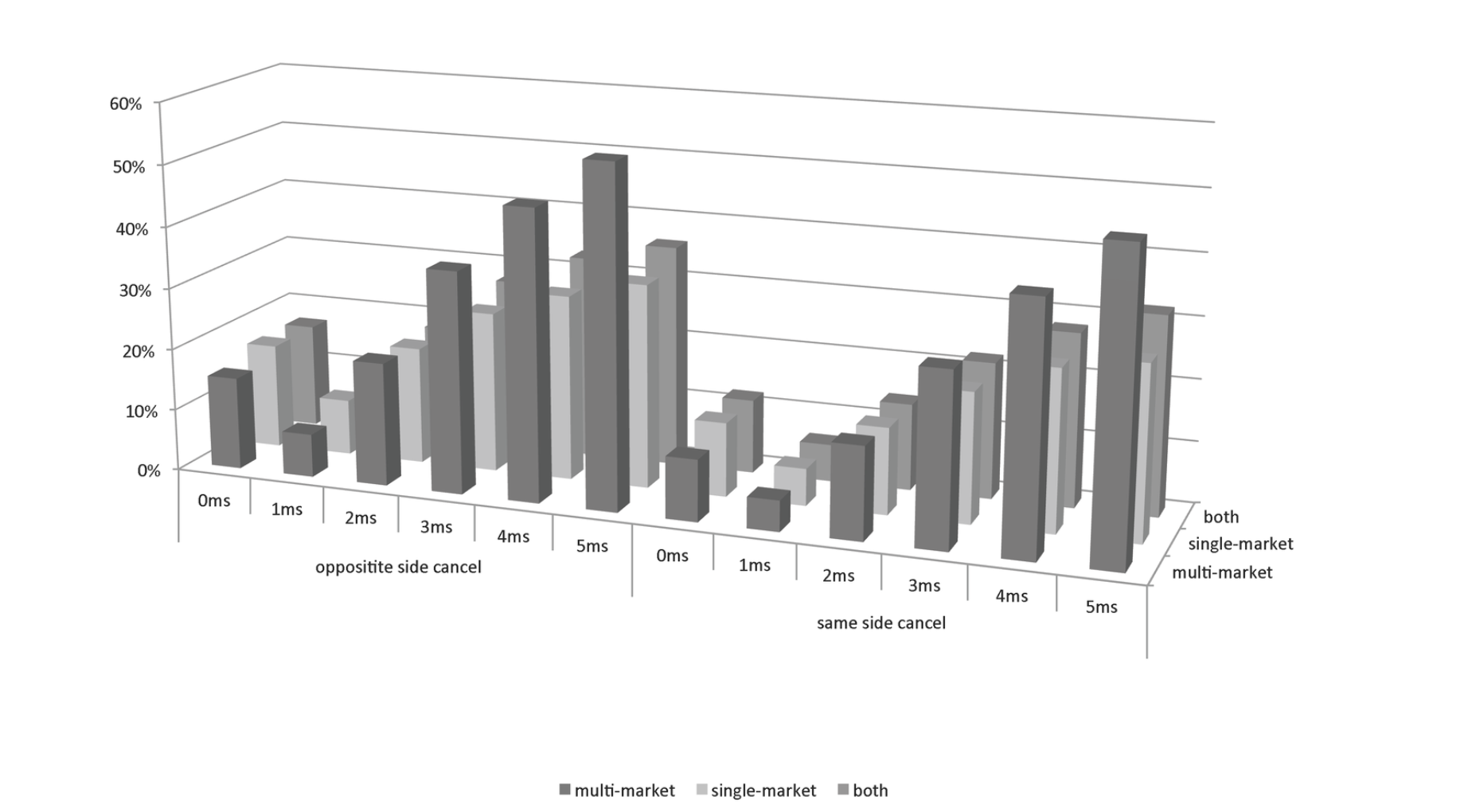

1. Flurry of cancellations

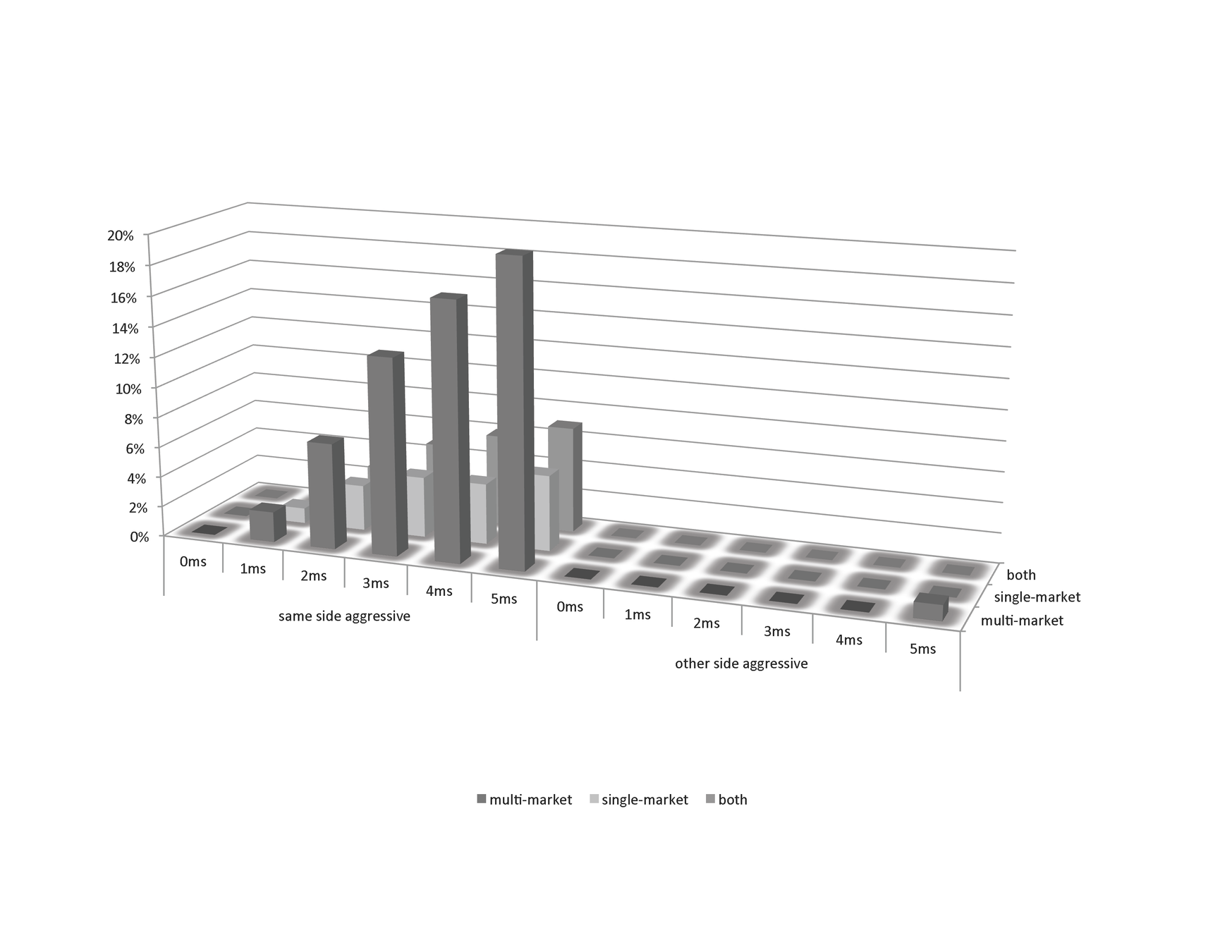

2. Flurry of aggressive orders

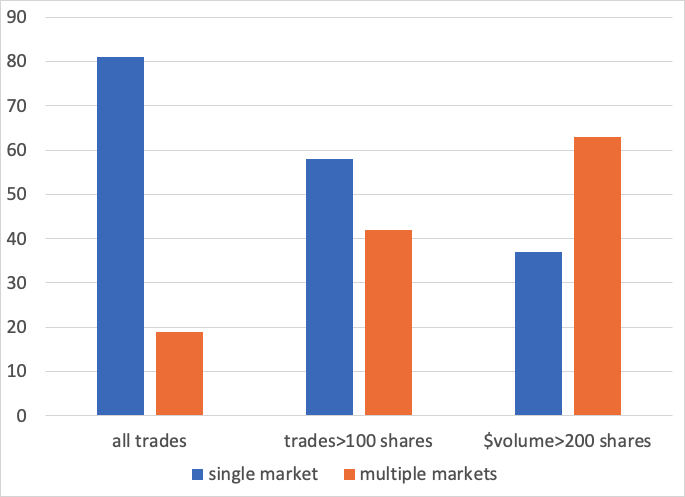

60%

10%

25%

5%

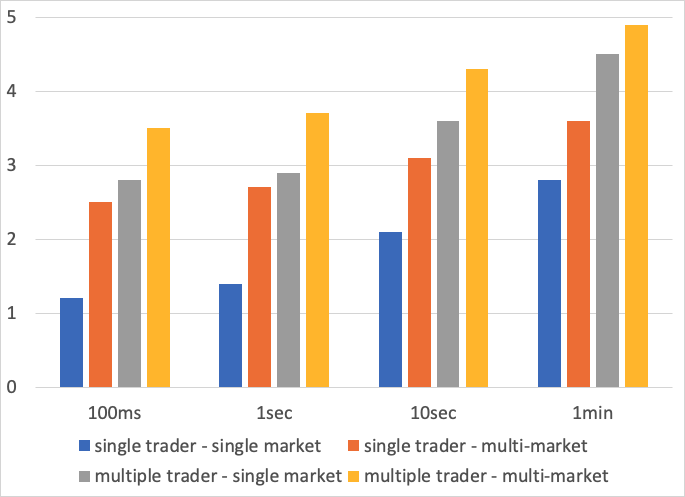

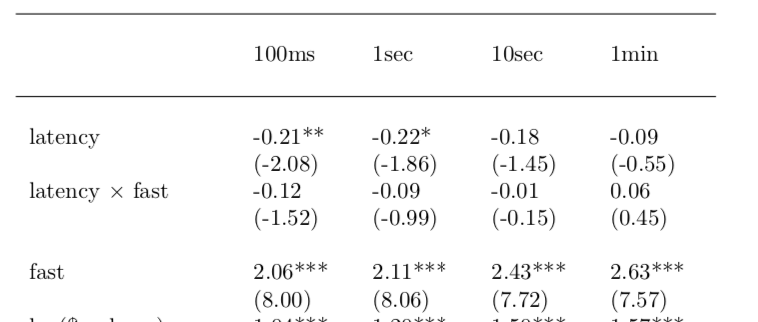

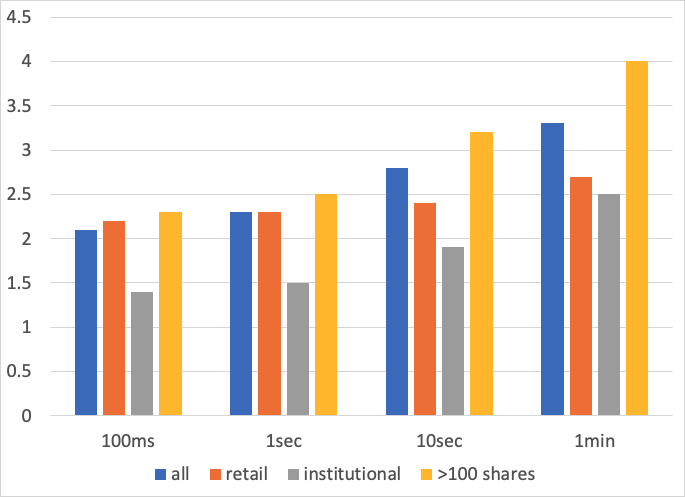

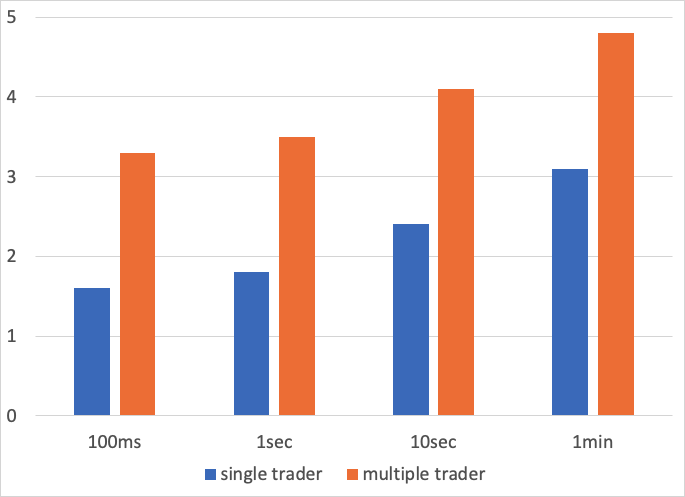

Big question: how do we interpret the last point?

fast traders create the appearance of a more informed trade and generate a larger price impact

fast traders are better at predicting that a trade is more informative and act while they can

only 20-25% of trades move the price

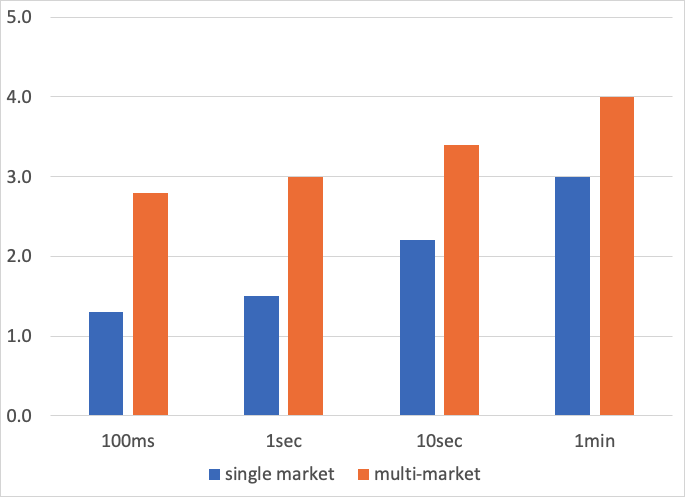

multi-market trades have larger price impact

but: seems that multi-trader (!) is key

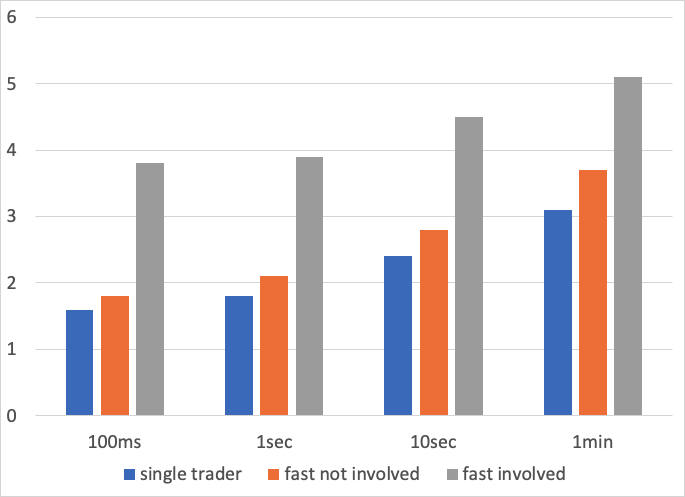

trades that involve the fast traders (snipers?) have the largest price impact

\(\Rightarrow\) Ideally: experiment such that trade information content not affected but fast traders' sniping ability curtailed (or improved)

Market A and B move to the same data centre: April 29, 2013

Our Premise

Disclaimer:

three other concurrent changes

Did it become easier to hit both markets?

same ms before: 22% same ms after: 31%

single-trader, multi-market \(\nearrow\) 2%

Did liquidity decline?

bid-ask spread: No.

quoted depth: Yes

(+ went down on the lower-rebate venue)

Are "snipers" less active?

Yes. Decline 1-2%

investors unlikely to know about or mind the system change:

\(\Rightarrow\) no change to intrinsic price impact

if "snipers" move the price too much

\(\Rightarrow\) price impact without "snipers" should decline

Findings

investors

routers

brokers

trading venues

desk

execution algorithm

HFT-MM detect informative trade and move the price before they get run over: HFT-MM contribute to price discovery with limit orders

fast (sniping) traders run over the HFT-MMs are better at predicting when a trade is more informative and act while they can

MMs get run over by informative investor trades

bid-ask spread is MM compensation

bid-ask spreads can be low but quotes move fast

bid-ask spreads are slightly higher because of snipers

Kyle 1985/Glosten-Milgrom

Brogaard, Hendershott, Riordan (2020)

Budish, Crampton, Shin (2016)

fast (sniping) traders react quickly on the possibility of a future price movement and create noisier prices

not clear how this affects spreads and risk/returns

Social Cost

Literature

Yang & Zhu (2018) ("Backrunning")

traditional view

premise

HFT-MM are better MMs

HFT-MM and HFT-snipers interactions

HFT-snipers interactions with the market

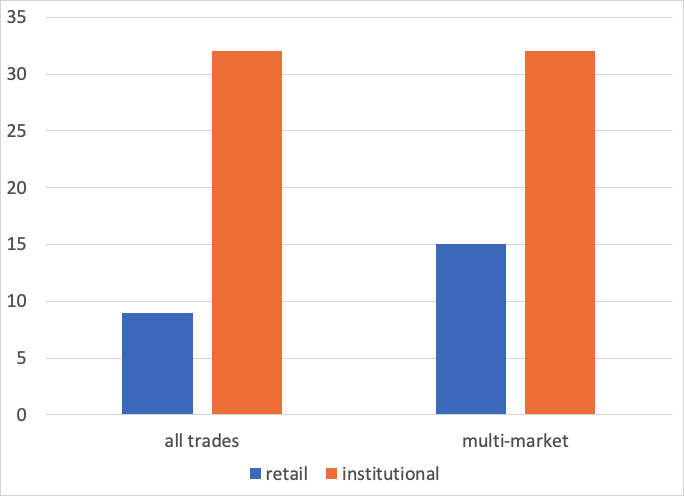

Fun Facts:

64%

36%

85%

15%

By Andreas Park

Presentation for the 2020 WFA in San Francisco (held virtually, of course).