Differentiable

Agent-Based Models

Oxford, January 2024

Arnau Quera-Bofarull

www.arnau.ai

Modelling an epidemic

Two common approaches:

1. SIR models

\frac{dS}{dt} = -\frac{\beta S I}{N}

\frac{dI}{dt} = \frac{\beta SI}{N} - \gamma I

\frac{dR}{dt} = \gamma I

Pros:

"cheap",

simple,

...

Cons:

only models "averages",

...

Two common approaches:

2. ABM models

Pros:

individual agents,

individual interactions,

...

Cons:

computational cost,

calibration,

...

Modelling an epidemic

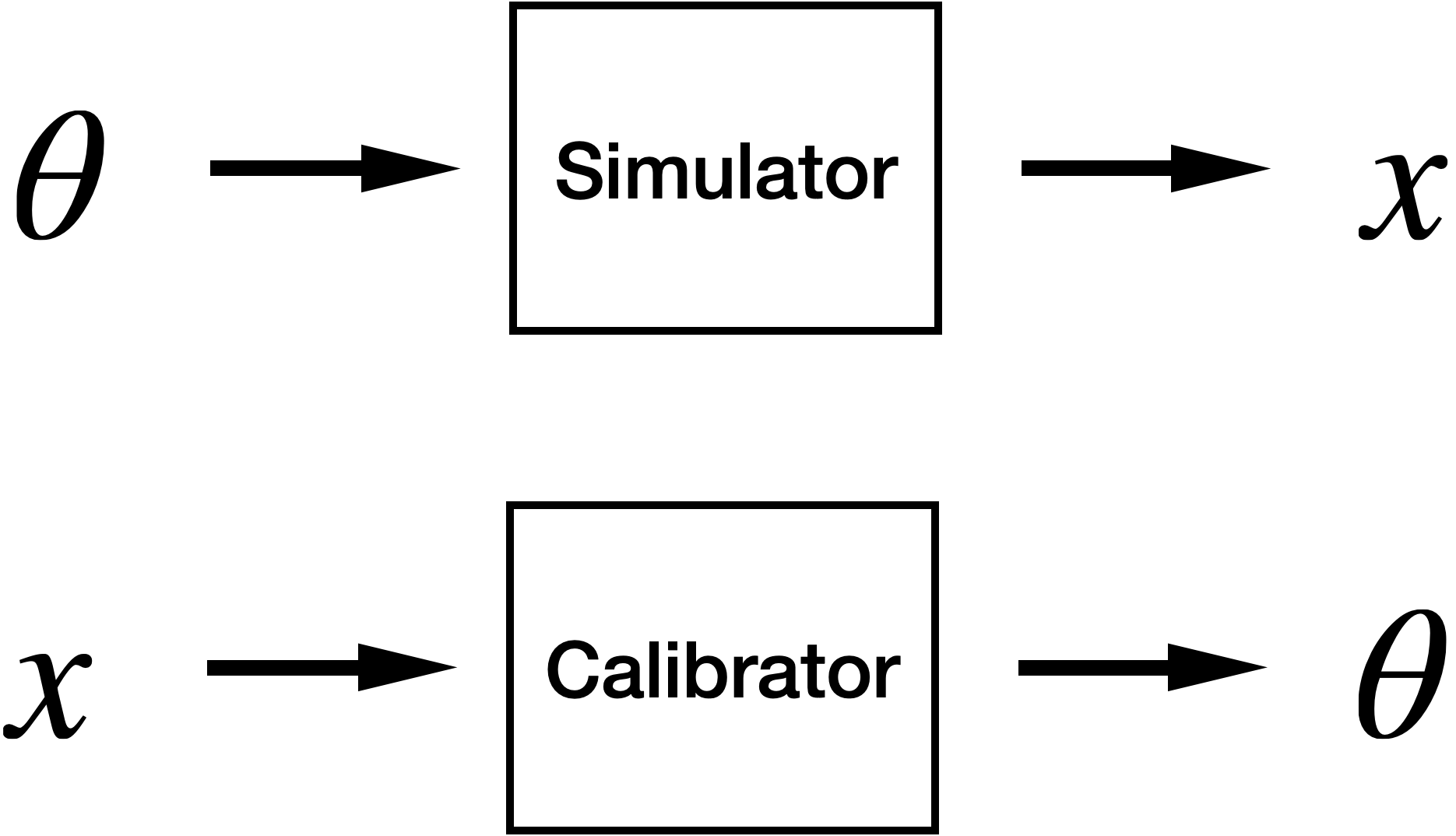

Calibration

Typically hard because

- No access to the likelihood.

- Simulator is slow to run.

- Large parameter space.

Variational Inference

- Assume posterior can be approximated by a parameterised distribution.

- Optimise for best parameters using gradient

(Generalized) Variational Inference

Knoblauch et al (2019)

\mathbf \theta

\mathbf y

ABM

\ell (\mathbf \theta, \mathbf y)

\pi(\mathbf \theta \mid \mathbf y) \propto e^{-\ell (\mathbf \theta, \mathbf y)}\pi(\mathbf\theta)

Prior

(Generalized) posterior

(Generalized) Variational Inference

\pi(\mathbf \theta \mid \mathbf y) \approx q^*(\mathbf \theta)

Optimization problem

Assume posterior approximated by variational family

q^*(\mathbf \theta) = \argmin_{q \in \mathcal Q}

q^*(\mathbf \theta) = \argmin_{q \in \mathcal Q} \left[ \mathbb E_{q(\mathbf \theta)} \ell(\mathbf \theta, \mathbf y) + D(q (\mathbf \theta) \mid \mid \pi(\mathbf \theta)) \right]

q^*(\mathbf \theta) = \argmin_{q \in \mathcal Q} \left[ \mathbb E_{q(\mathbf \theta)} \ell(\mathbf \theta, \mathbf y) \right .

Distance between ABM output and data

Divergence posterior - prior

How to optimize q?

q_{\phi^*}(\mathbf \theta) = \argmin_{\phi \in \Phi} \left[ \mathbb E_{q_\phi(\mathbf \theta)} \ell(\mathbf \theta, \mathbf y) + D(q_\phi (\mathbf \theta) \mid \mid \pi(\mathbf \theta)) \right]

\phi' \longrightarrow \phi' - \eta \nabla_\phi \mathcal L(\phi')

Choose parametric family of distributions (e.g., Normal)

q(\mathbf \theta) = q_\phi (\mathbf \theta)

q_{\mathbf \phi} (\mathbf \theta) = \frac{1}{\mathbf\phi_2\sqrt{2\pi}} e^{-\frac{1}{2}\left(\frac{\mathbf\theta - \mathbf\phi_1}{\mathbf \phi_2}\right)^2}

How to optimize q?

\nabla_\phi \mathbb E_{\theta \sim q_\phi(\mathbf \theta)} \ell(\mathbf \theta, \mathbf y)

Need to compute the gradient

\mathbb E_{\theta \sim q_\phi(\mathbf \theta)} \left[\nabla_\phi \log q_\phi(\mathbf\theta) \cdot \ell(\mathbf\theta, \mathbf y)\right]

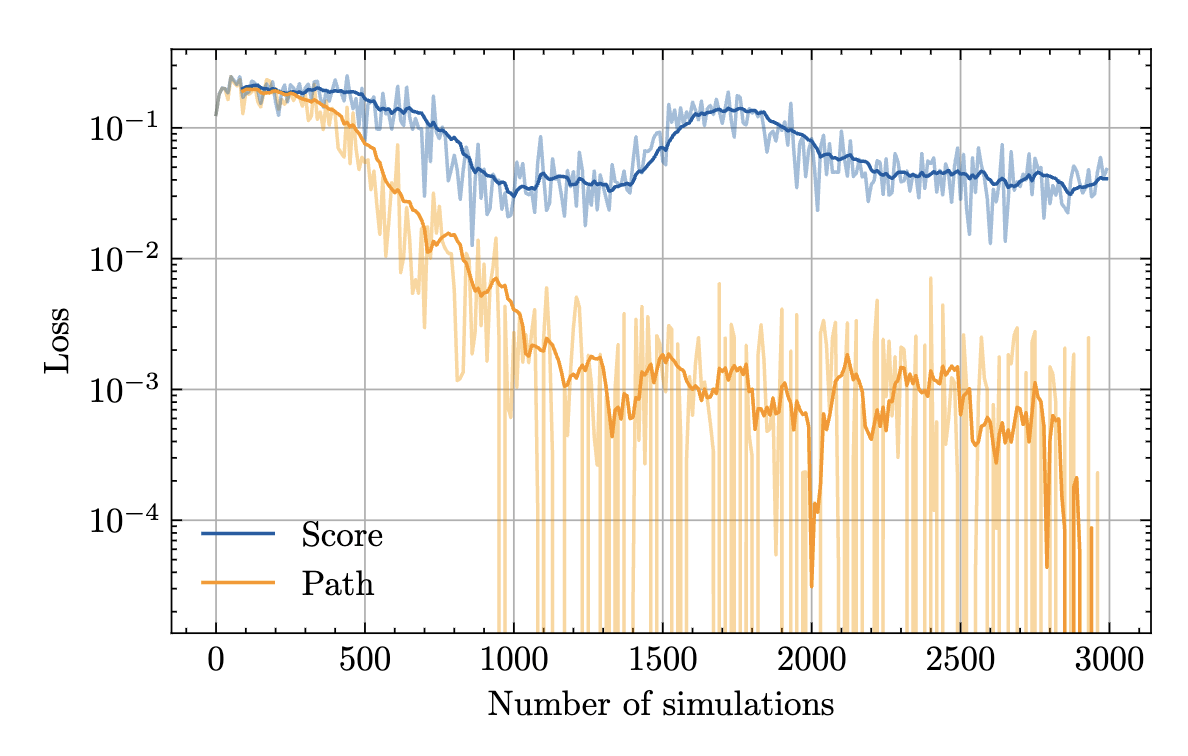

Score function estimator

Monte Carlo

gradient estimation

Mohamed et al (2020)

\mathbb E_{\epsilon \sim q_\phi(\epsilon)} \left[\nabla_\phi \ell(f(\epsilon; \mathbf\theta, \mathbf y))\right]

Path-wise estimator

Reparameterization

Score function estimator

Path-wise estimator

- Unbiased

- Typically high variance

- Does not require differentiable simulator

- Unbiased*

- Low(er) variance

- Requires differentiable simulator

"Gradient assisted calibration of financial agent-based models" Dyer et al. (2023)

How to build differentiable

Agent-Based Models

Differentiable simulators

f: \mathbb R^m \longrightarrow \mathbb R^n

(J_f)_{ij} = \frac{\partial f_i}{\partial x_j}

Numerical differentiation

\frac{\partial f}{\partial x} = \lim_{\epsilon \to 0}\frac{f(x+\epsilon) - f(x)}{\epsilon}

Inaccurate

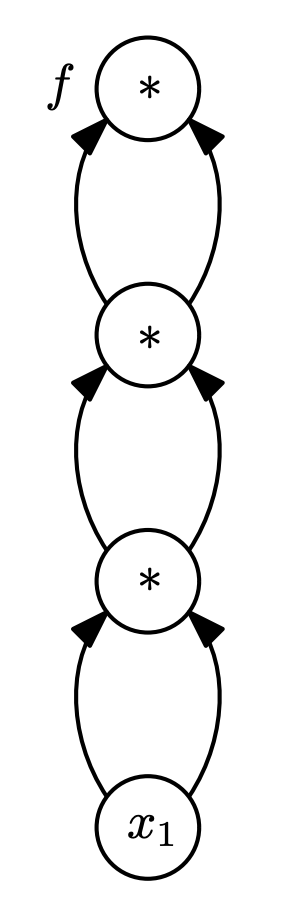

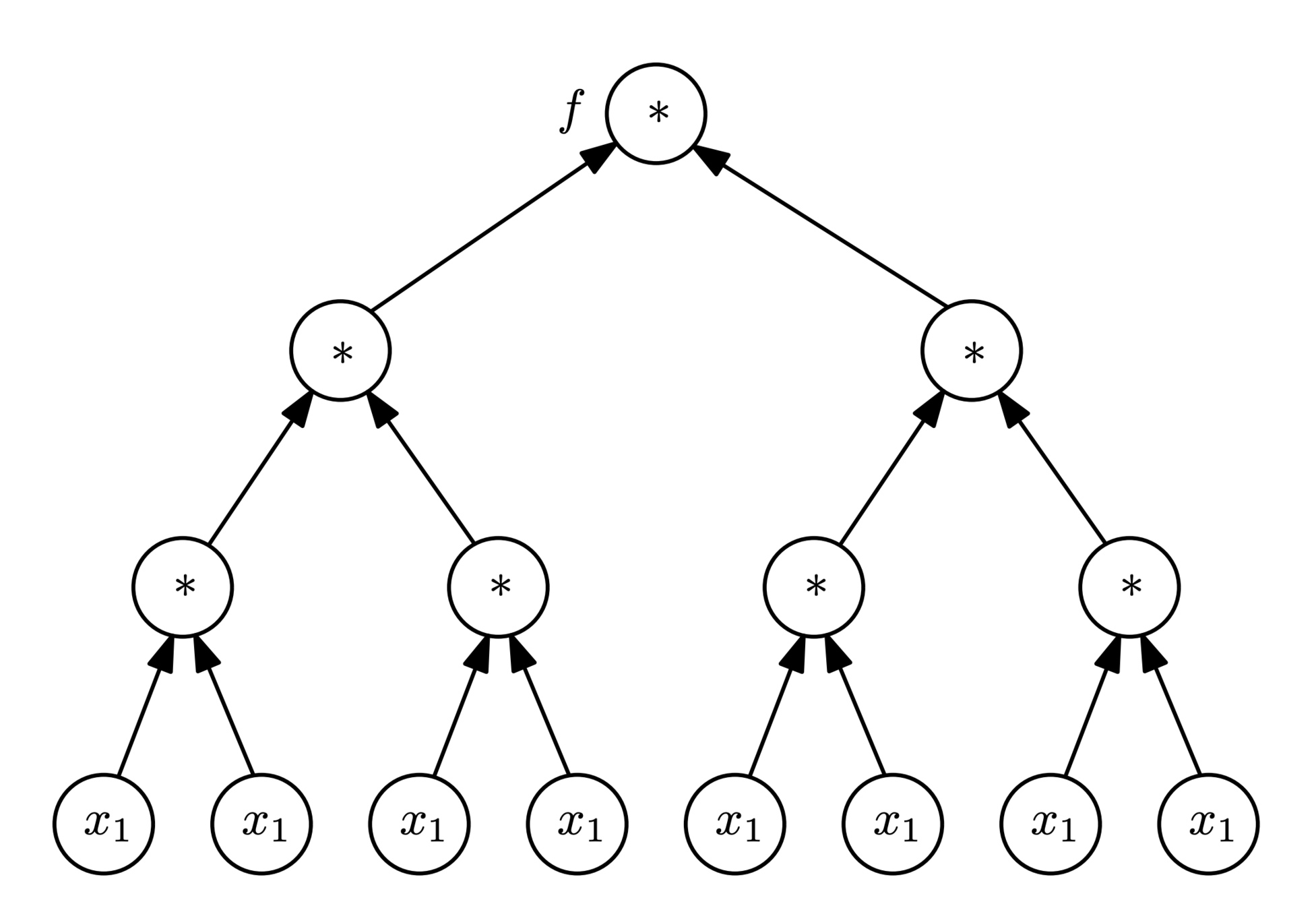

Automatic differentiation

def f(x1)

t1 = x1 * x1

t2 = t1 * t1

return t2 * t2t_1

t_2

2

4

16

256

\frac{\partial f}{\partial t_2} = 2 t_2 = 2 \cdot 16 = 32

f

x_1

\frac{\partial t_2}{\partial t_1} = 2 t_1 = 2 \cdot 4 = 8

\frac{\partial t_1}{\partial x_1} = 2 x_1 = 2 \cdot 2 = 4

\frac{\partial f}{\partial f} = 1

f'(x) = 8x^7 = 8\cdot 2^7 = 1024 = 32 \cdot 8 \cdot 4

Idea:

Decompose program into basic operations that we can differentiate

Automatic differentiation

Reverse mode AD

t_1

t_2

2

4

16

256

\frac{\partial f}{\partial t_2} = 32

f

x_1

\frac{\partial t_2}{\partial t_1} = 8

\frac{\partial t_1}{\partial x_1} = 4

Forward mode AD

\frac{\partial x_1}{\partial x_1} = 1

t_1

t_2

2

4

16

256

\frac{\partial f}{\partial t_2} = 32

f

x_1

\frac{\partial t_2}{\partial t_1} = 8

\frac{\partial t_1}{\partial x_1} = 4

\frac{\partial f}{\partial f} = 1

Automatic differentiation

Reverse mode AD

t_1

t_2

2

4

16

256

\frac{\partial f}{\partial t_2} = 32

f

x_1

\frac{\partial t_2}{\partial t_1} = 8

\frac{\partial t_1}{\partial x_1} = 4

Forward mode AD

\frac{\partial x_1}{\partial x_1} = 1

t_1

t_2

2

4

16

256

\frac{\partial f}{\partial t_2} = 32

f

x_1

\frac{\partial t_2}{\partial t_1} = 8

\frac{\partial t_1}{\partial x_1} = 4

\frac{\partial f}{\partial f} = 1

Forward vs Reverse

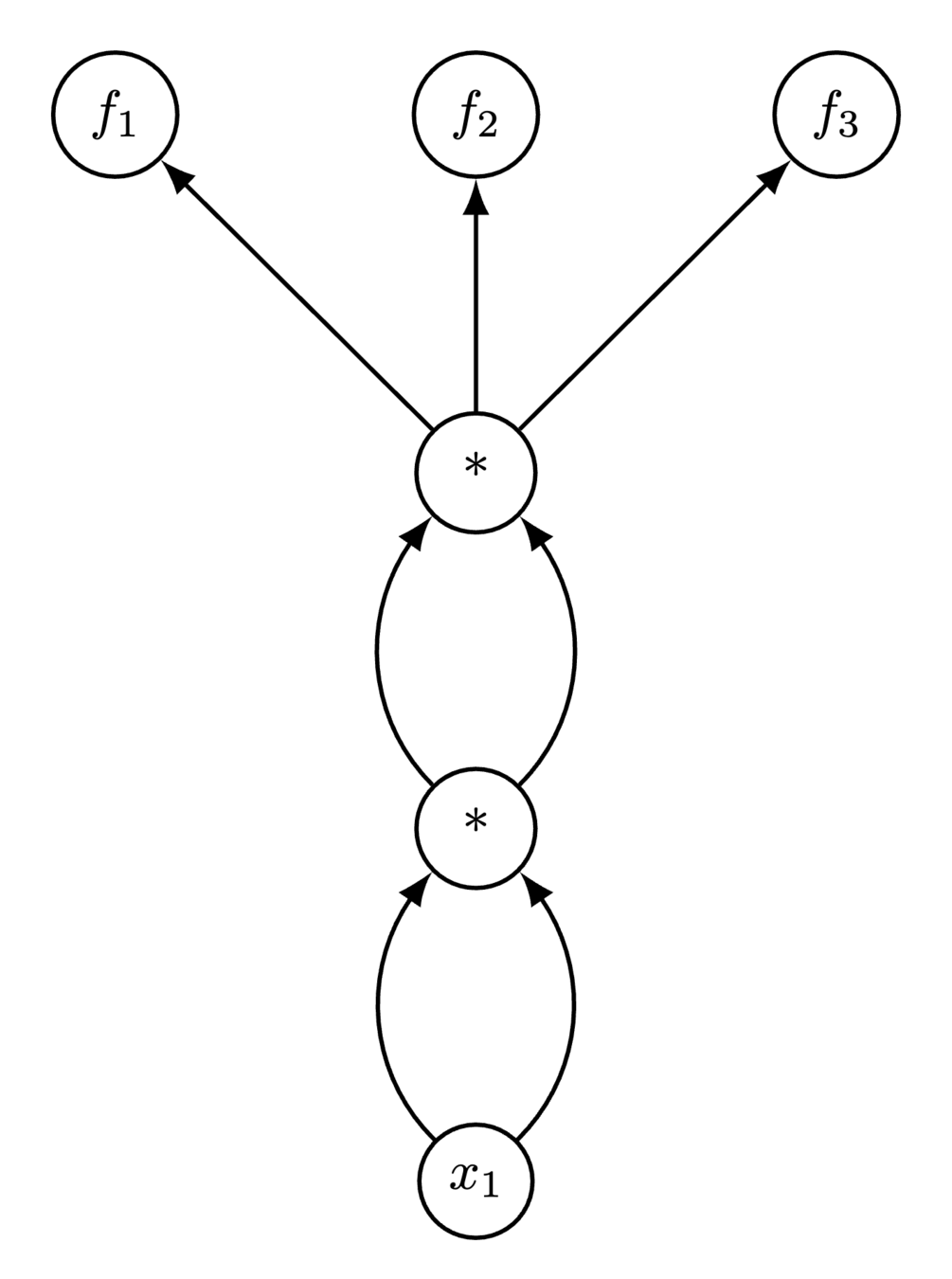

Multiple outputs

def f(x1)

t1 = x1 * x1

t2 = t1 * t1

return [t2, t2, t2]Reverse needs 3 full model evaluations!

Forward can amortize

Forward vs Reverse

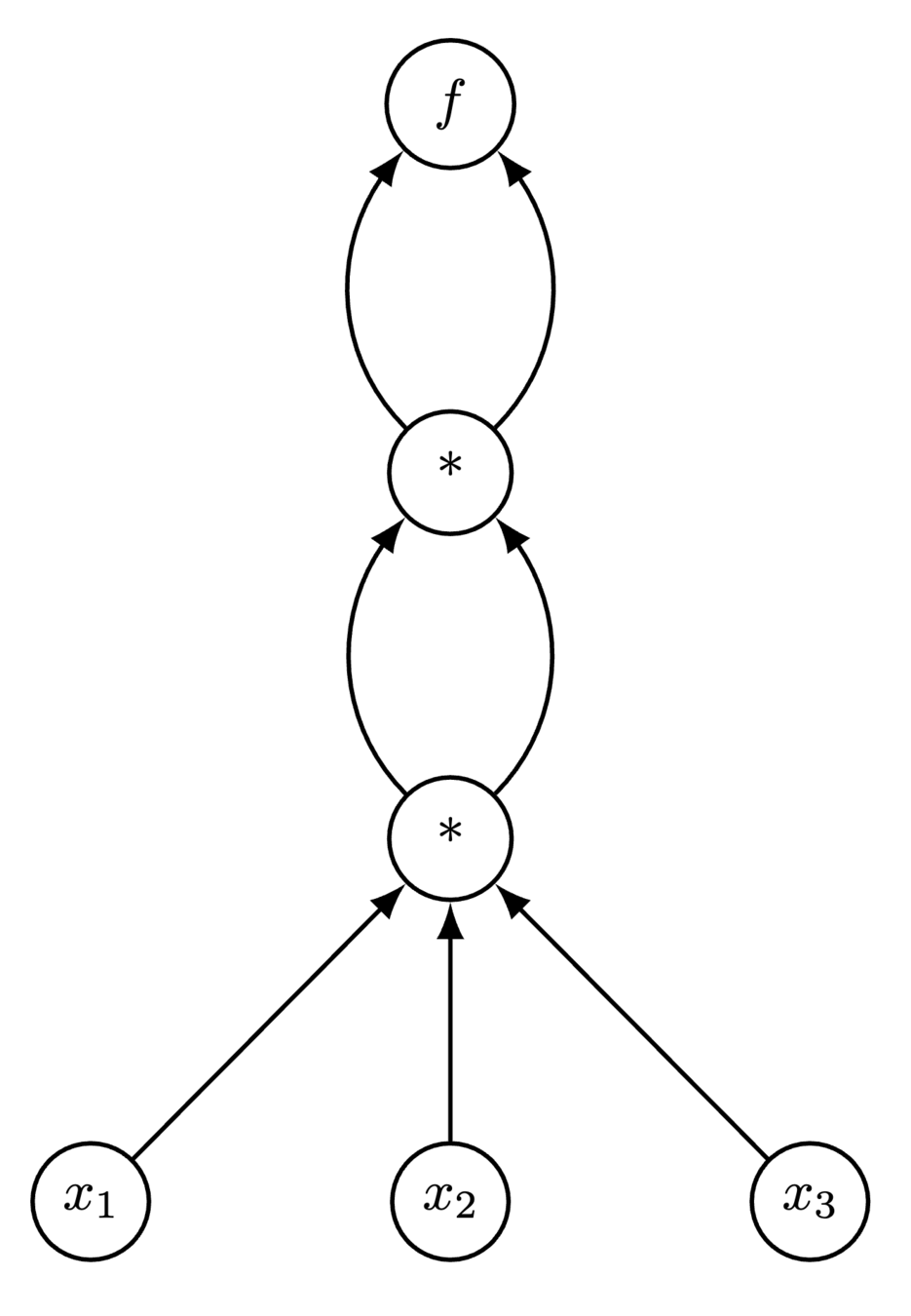

Multiple inputs

def f(x1, x2, x3)

t1 = x1 * x2 * x3

t2 = t1 * t1

return t2 * t2

Forward needs 3 full model evaluations!

Reverse can amortize

Forward vs Reverse

f: \mathbb R^m \longrightarrow \mathbb R^n

Reverse mode preferred for deep learning

m \gg n

However

Quera-Bofarull et al. "Some challenges of calibrating differentiable agent-based models"

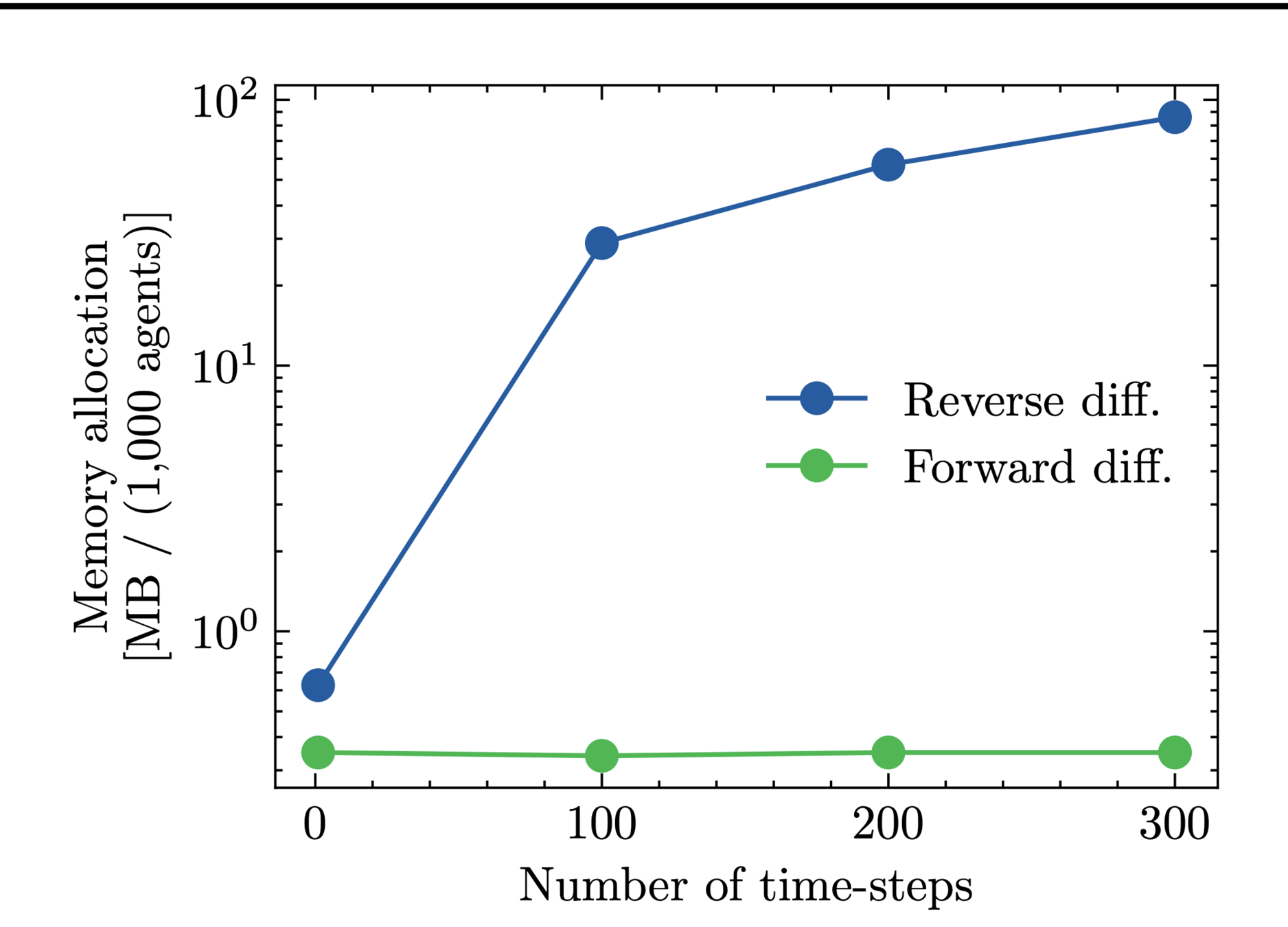

Reverse mode needs to store computational graph!

Can blow up in memory

Differentiating through randomness

x \sim \mathcal N(\mu, \sigma^2)

\epsilon \sim \mathcal N(0, 1)

x = \mu + \epsilon \sigma

\frac{\mathrm{d} x}{\mathrm{d} \mu} = 1

\frac{\mathrm{d} x}{\mathrm{d} \sigma} = \epsilon

What about discrete distributions?

x \sim \mathrm{Categorical}(\mathbf p)

Option 1: Straight-Through

Just assign a gradient of 1.

Works if program is linear

Bengio et al. (2013)

x \sim \mathrm{Categorical}(\mathbf p)

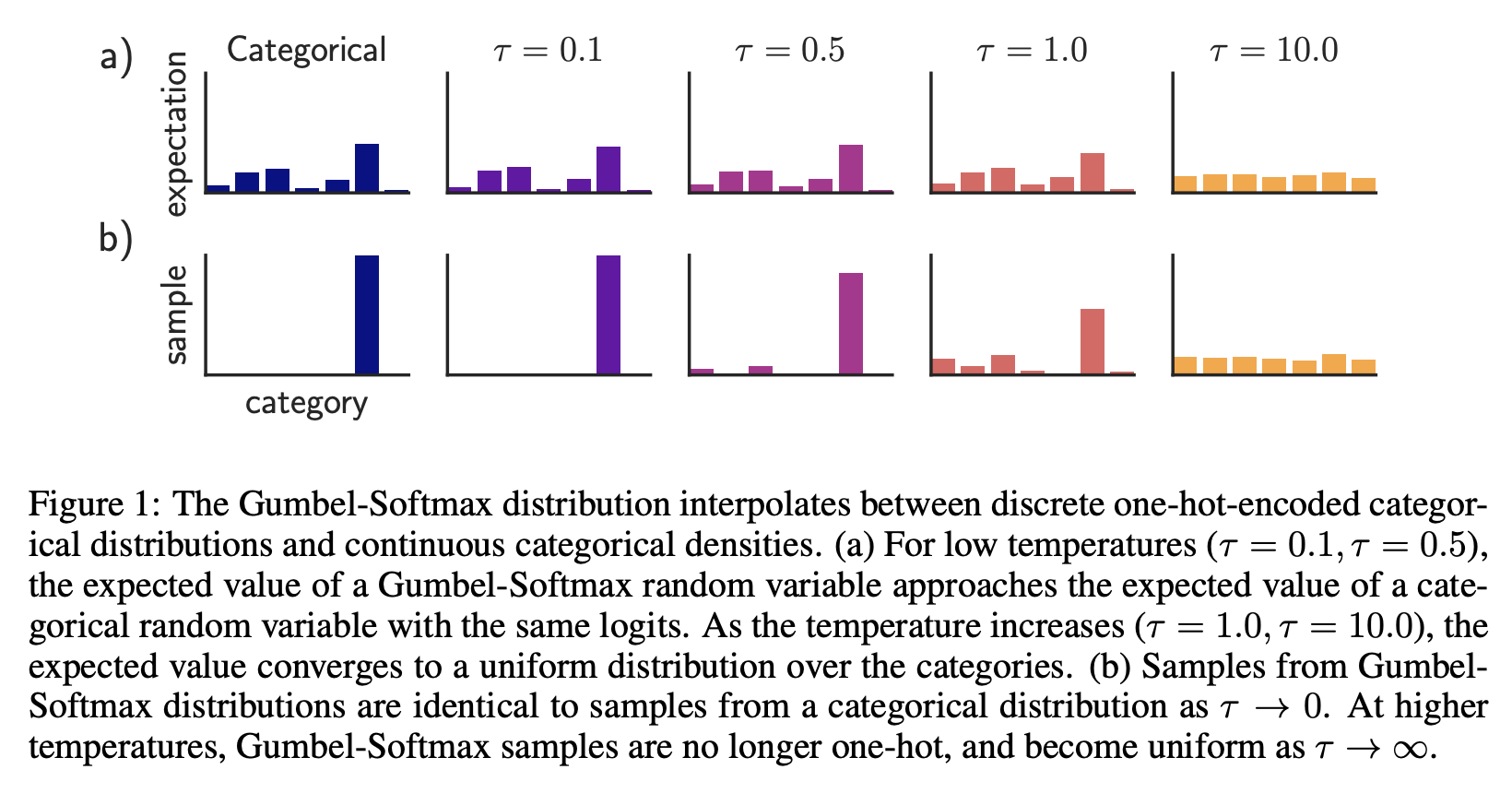

Option 2: Gumbel-Softmax

Jang et al. (2016)

Bias vs Variance tradeoff

x \sim \mathrm{Categorical}(\mathbf p)

Option 3: Smooth Perturbation analysis

StochaticAD.jl -- Arya et al. (2022)

Unbiased!

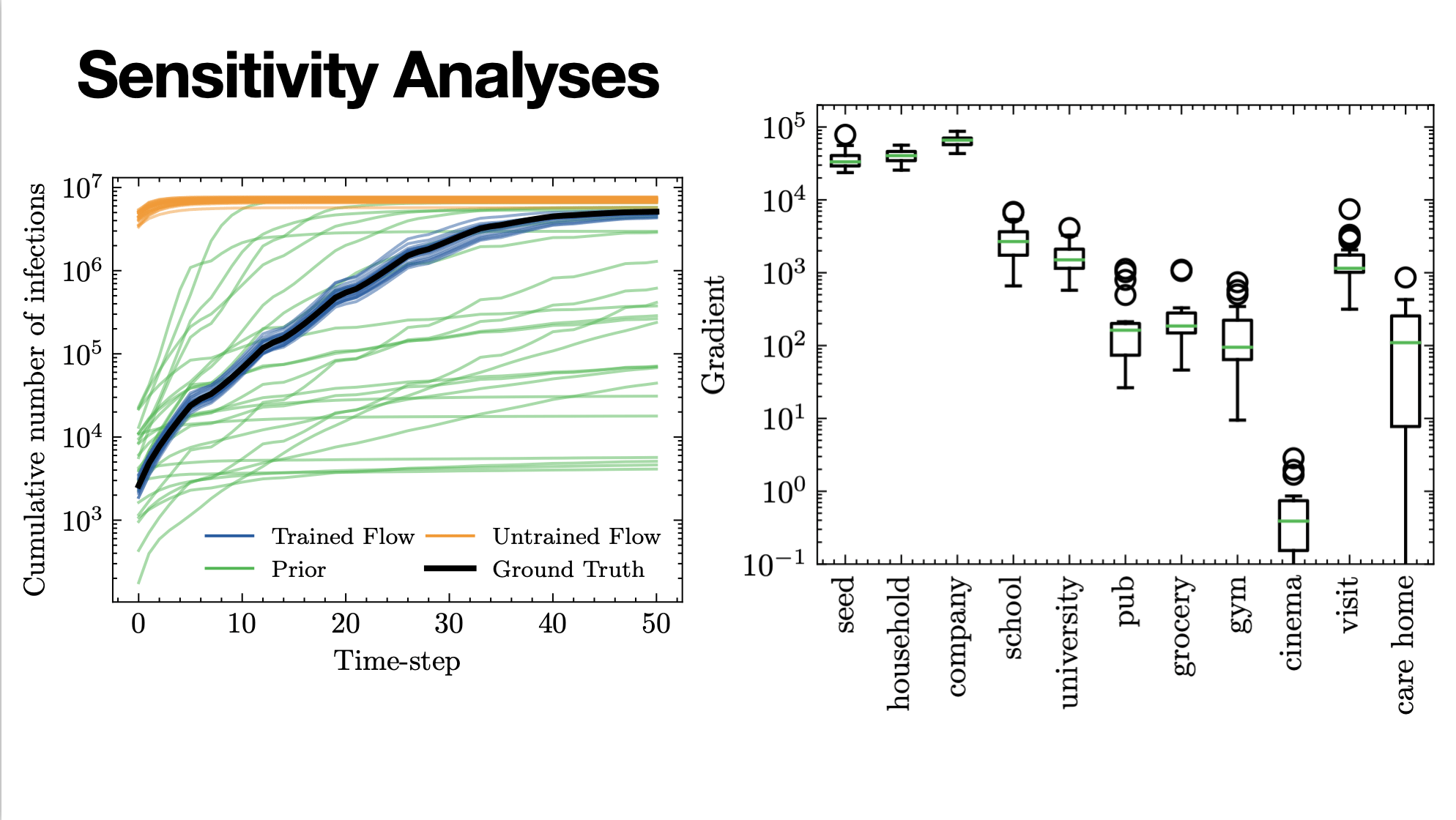

So does it work?

arnau.ai/blackbirds

Multiple examples of differentiable ABMs in PyTorch and Julia

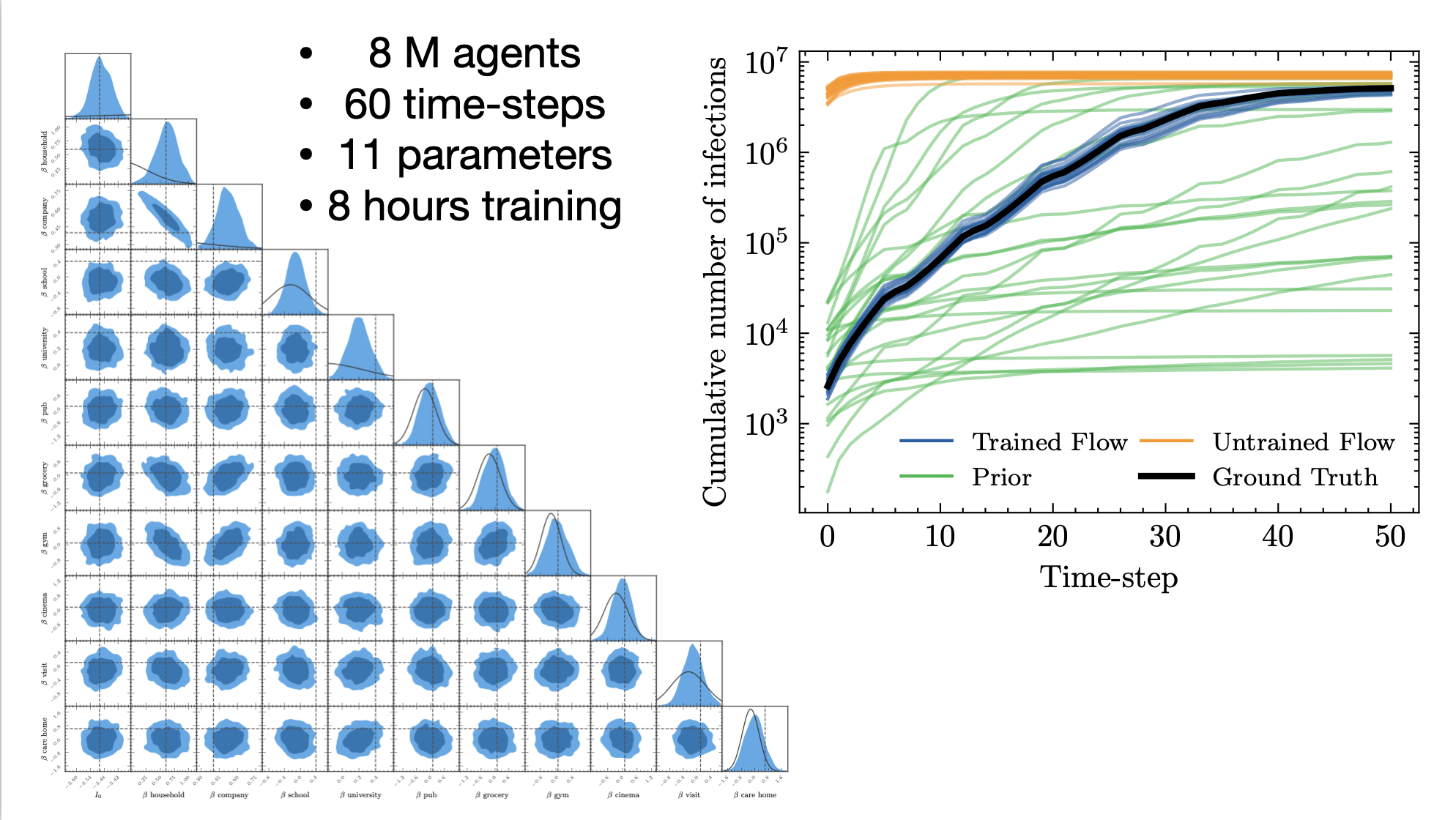

JUNE epidemiological model

Reverse-mode gives us senstivity analysis for free

Summary

-

Generalized Variational Inference promising route to calibrate differentiable ABMs.

-

Differentiable ABMs can be built using Automatic Differentiation

-

Automatic Differentiation provides O(1) sensitivity analysis.

Slides and papers:

www.arnau.ai/talks

Diff ABM examples:

www.arnau.ai/blackbirds

Backup slides

Symbolic differentiation

function f(x1)

t1 = x1 * x1

t2 = t1 * t1

return t2 * t2

end

f(x) = x^8

Symbolic differentiation

Hard-code calculus 101 derivatives

\begin{align*}

x' &= 1\\

(f+g)' &= f' + g'\\

(fg)' &= f'g + fg'\\

\end{align*}

Recurrently go down the tree via chain rule

Inefficient representation

Exact result

Automatic differentiation

DifferentiableAgent-Based Models

By arnauqb