Microcredit

Brandon Williams

Development Economics

October 17, 2024

Microcredit

Development Economics

October 17, 2024

Six Randomized Evaluations (2015)

In our careful assessment, meeting the credit needs of the poor is one of the most effective ways to fight exploitation and poverty.

I believe that this campaign will become one of the great humanitarian movements of history. This campaign will allow the world’s poorest people to free themselves from the bondage of poverty and deprivation to bloom to their fullest potentials to the benefit of all—rich and poor.”

- PM of Bangladesh, 1997

Microcredit

Development Economics

October 10, 2024

- Micro-credit hailed as a way to fix limited access to credit but what is the empirical evidence?

- Randomization is important

- Demand side: people who choose to borrow are different than those who do not

- Supply side: lenders may selectively choose where to lend

- And randomization technique may vary

- Community-level: only solicit or accept from treated markets

- Internalizes spillover and captures general equilibrium

- Loss of statistical power

- Individual: randomize from lendees at the margins

- Already interested in loans so take-up (and power) is high

- No control for spillover

- Community-level: only solicit or accept from treated markets

Six Randomized Evaluations (2015)

Microcredit

Development Economics

October 10, 2024

- Modest take-up among prospective micro-entrepreneurs

- Difficulty meeting the power needs of predicting take-up

- Lack of evidence of transformative effects on average borrower

- For example, no sizeable gains in income

- Modest but potentially meaningful effects (freedom of choice)

- Shifts to business instead of wage income

- Reductions in government aid or remittances

- Little support for the biggest drawbacks of microcredit

- Heterogeneous and segmented transformative effects

- Some good, some bad (reduction in schooling)

- Null results can hold a lot of economical significance!

Six Randomized Evaluations (2015)

Microcredit

Development Economics

October 10, 2024

Why such differing results?

Consider a model.

Six Randomized Evaluations (2015)

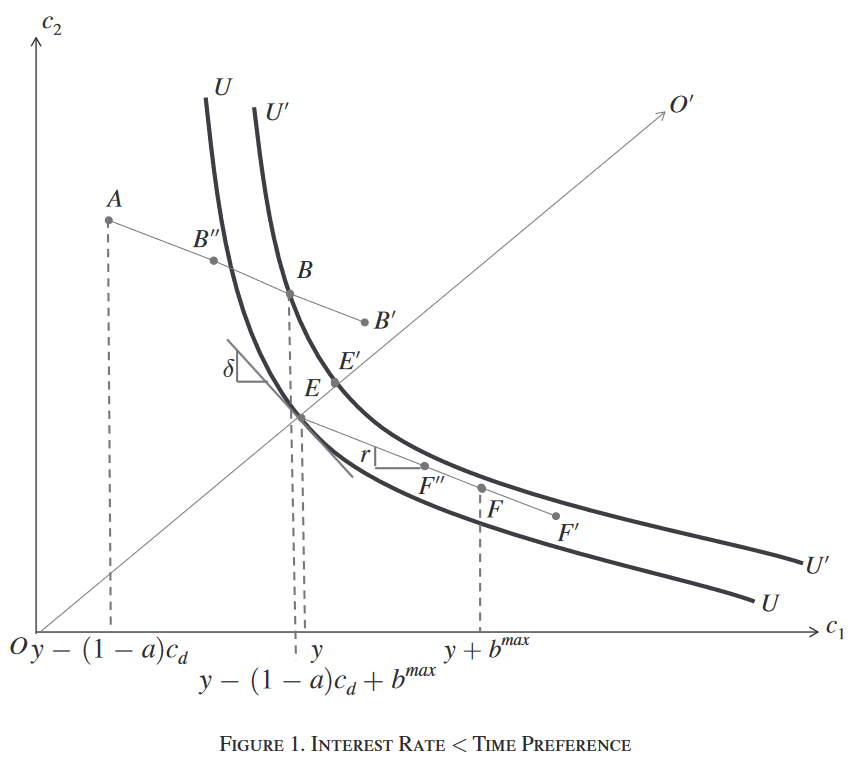

Indifference curves

Consumption in period 1

Period 2

Endowment given income y

Borrow in period 1 but do not buy the durable

Borrow in period 1 but do not buy the durable

Max loan size

Do not borrow and buy the durable

Borrow and buy the durable

What achieves the highest indifference curve?

What achieves the highest indifference curve?

What achieves the highest indifference curve?

But it requires less c1

What happens if more borrowing is available?

What happens if more borrowing is available?

What happens if more borrowing is available?

Higher utility with no c1 tradeoff

What about if less borrowing is available?

What about if less borrowing is available?

What about if less borrowing is available?

What about if less borrowing is available?

Borrow without buying

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Result 1: increasing access to credit means more likely to buy durable

(but may lower consumption)

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Result 3: this tradeoff holds for labor decision as well

increased access to credit reduces total consumption and increases labor

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Result 2:increased access to credit reduces the product of the project

shown by little a increasing

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Result 2:increased access to credit reduces the product of the project

shown by little a increasing

y+ac_d

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Result 2:increased access to credit reduces the product of the project

shown by little a increasing - an extremely productive return

y+ac_d

Do not borrow and buy the durable

Borrow and buy the durable

Borrow but do not buy the durable

Result 2:increased access to credit reduces the product of the project

shown by little a increasing - the opposite holds

y+ac_d

If there is any single lesson to come from the exciting recent proliferation of microfinance research, it is that microfinance is an extremely heterogeneous field: the design of microcredit contracts involves many degrees of freedom, and different kinds of borrowers are likely to value microfinance for very different reasons."

- VoxDevLit, "Microfinance", March 2023

Copy of Dev.Slides.10.17

By bjw95