Content ITV PRO

This is Itvedant Content department

Impact of bank rates

Learning Outcome

5

Understand the impact of RBI policies on banks and consumers.

4

Differentiate between CRR and SLR.

3

Analyze the impact on loans and EMIs.

2

Learn how RBI controls inflation and growth.

1

Understand Repo Rate, Reverse Repo Rate, CRR, and SLR.

Repo Rate

The rate at which the RBI provides short-term funds to commercial banks. It is the RBI's primary tool to steer interest rates in the economy.

Impact on Repo Rate when it goes DOWN:

→ Banks get cheaper funds from RBI

→ Banks pass on lower rates to customers

→ Loans become cheaper → More borrowing → Economy grows faster

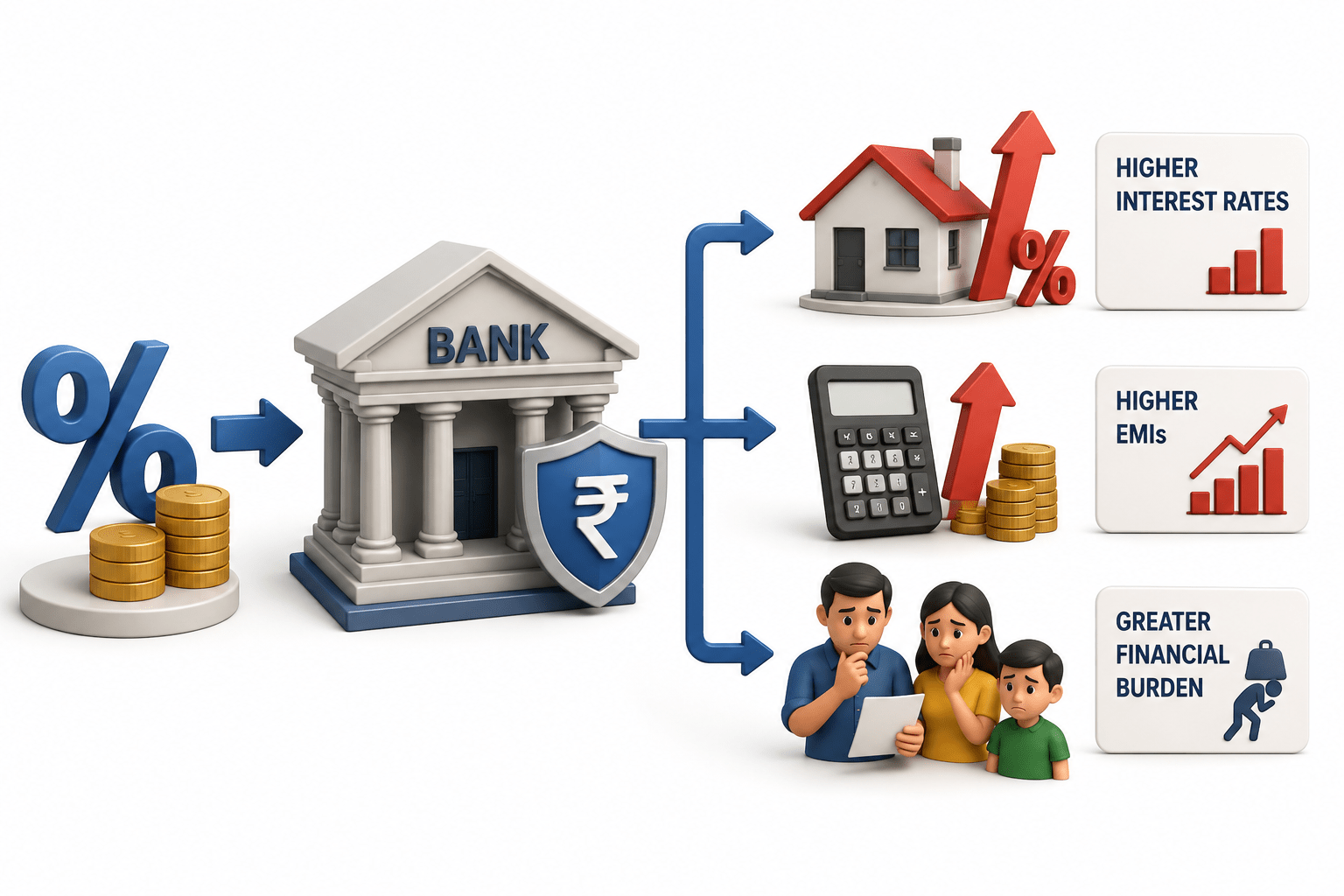

Impact on Repo Rate when it goes UP:

→ Banks borrow at a higher cost from RBI

→ Banks raise their own lending rates (MCLR rises)

→ Loans become expensive → Borrowing slows → Inflation cools down

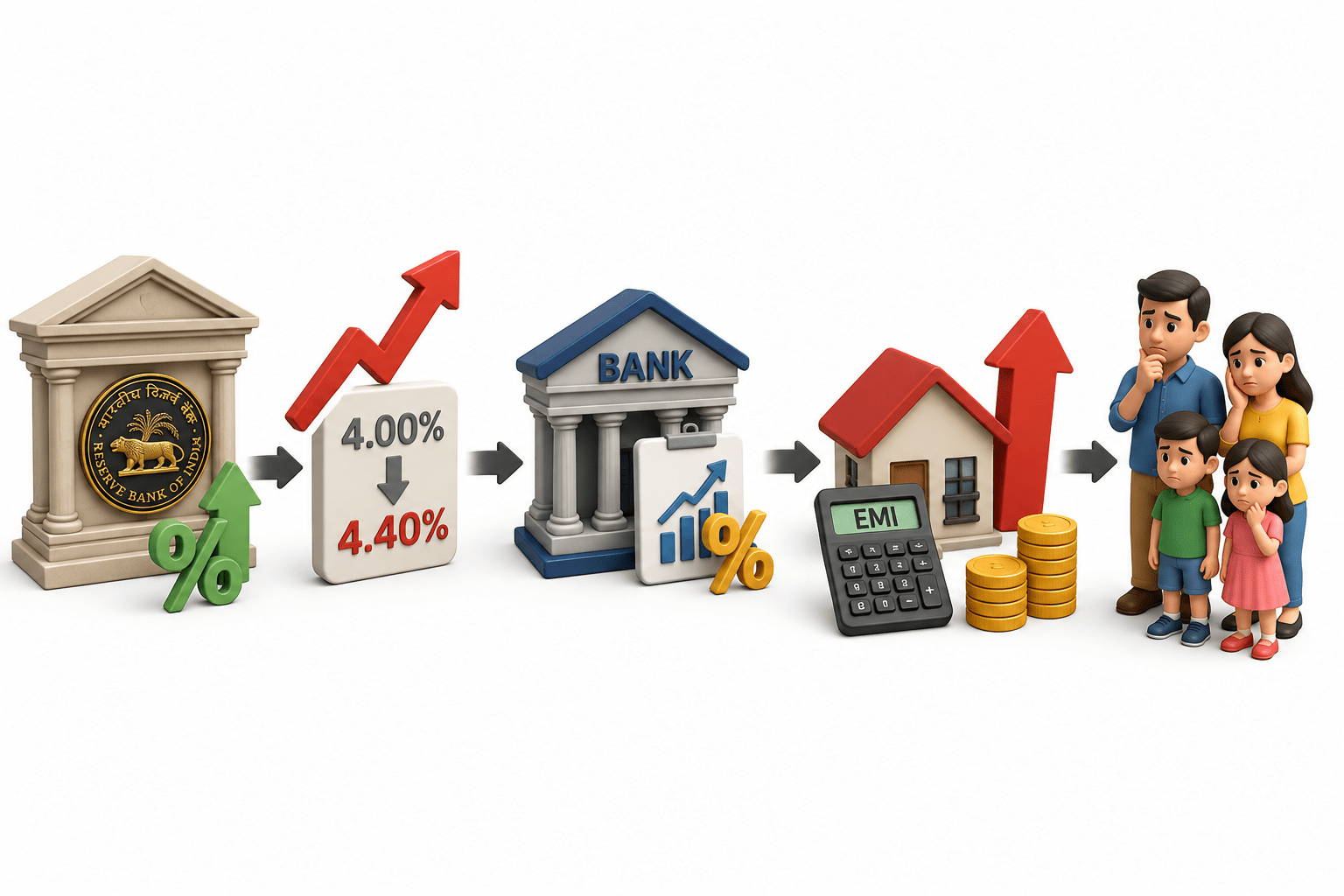

Real-Life Example:

In May 2022, RBI raised the Repo Rate from 4.00% to 4.40%.

Major banks increased home loan rates shortly after.

EMIs on home loans rose significantly.

Borrowers across the country felt the impact directly.

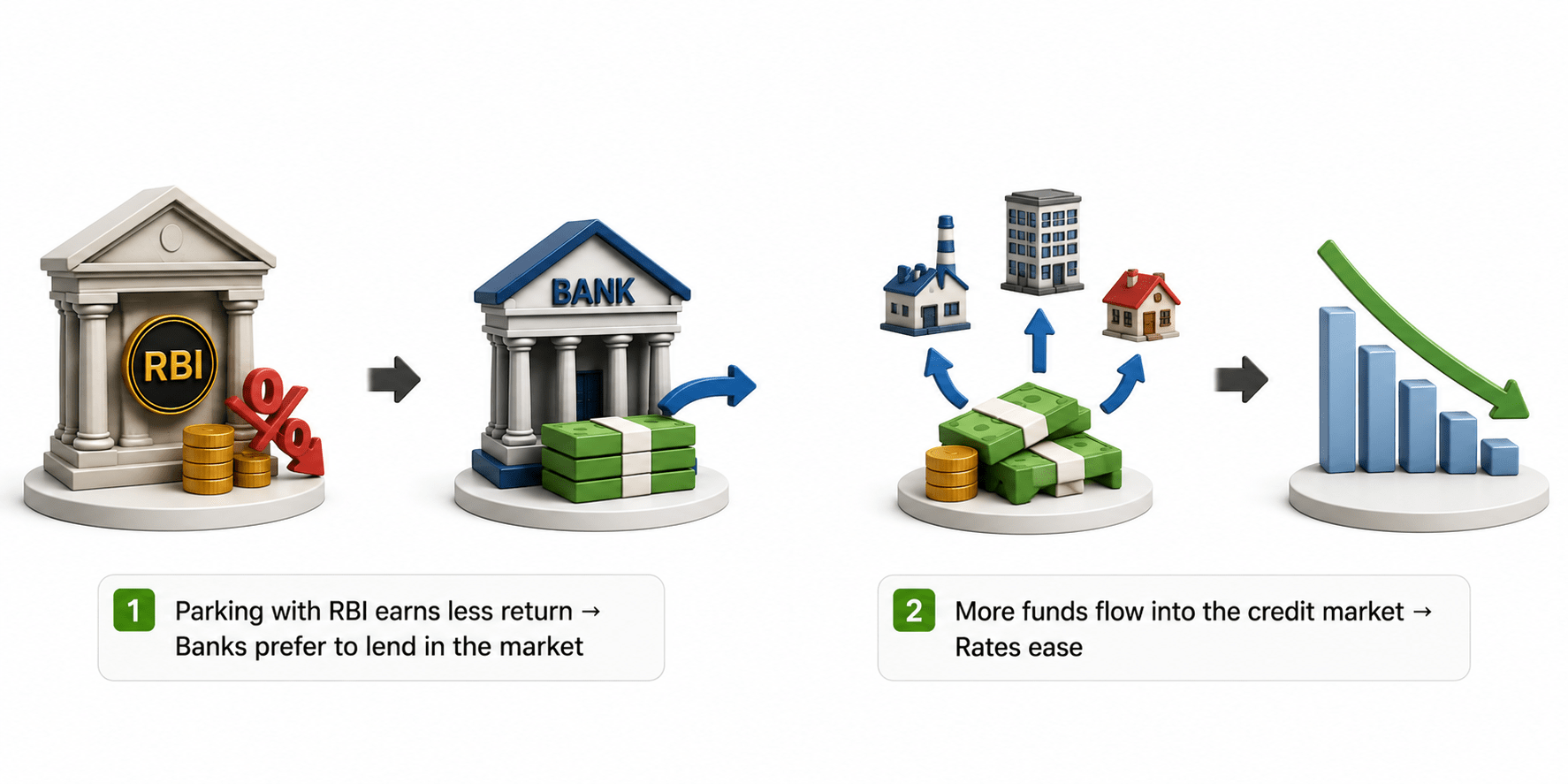

Reverse Repo Rate → Controls the Floor of Rates

The rate at which the RBI borrows money from commercial banks. When banks have surplus cash, they park it with the RBI at this rate.

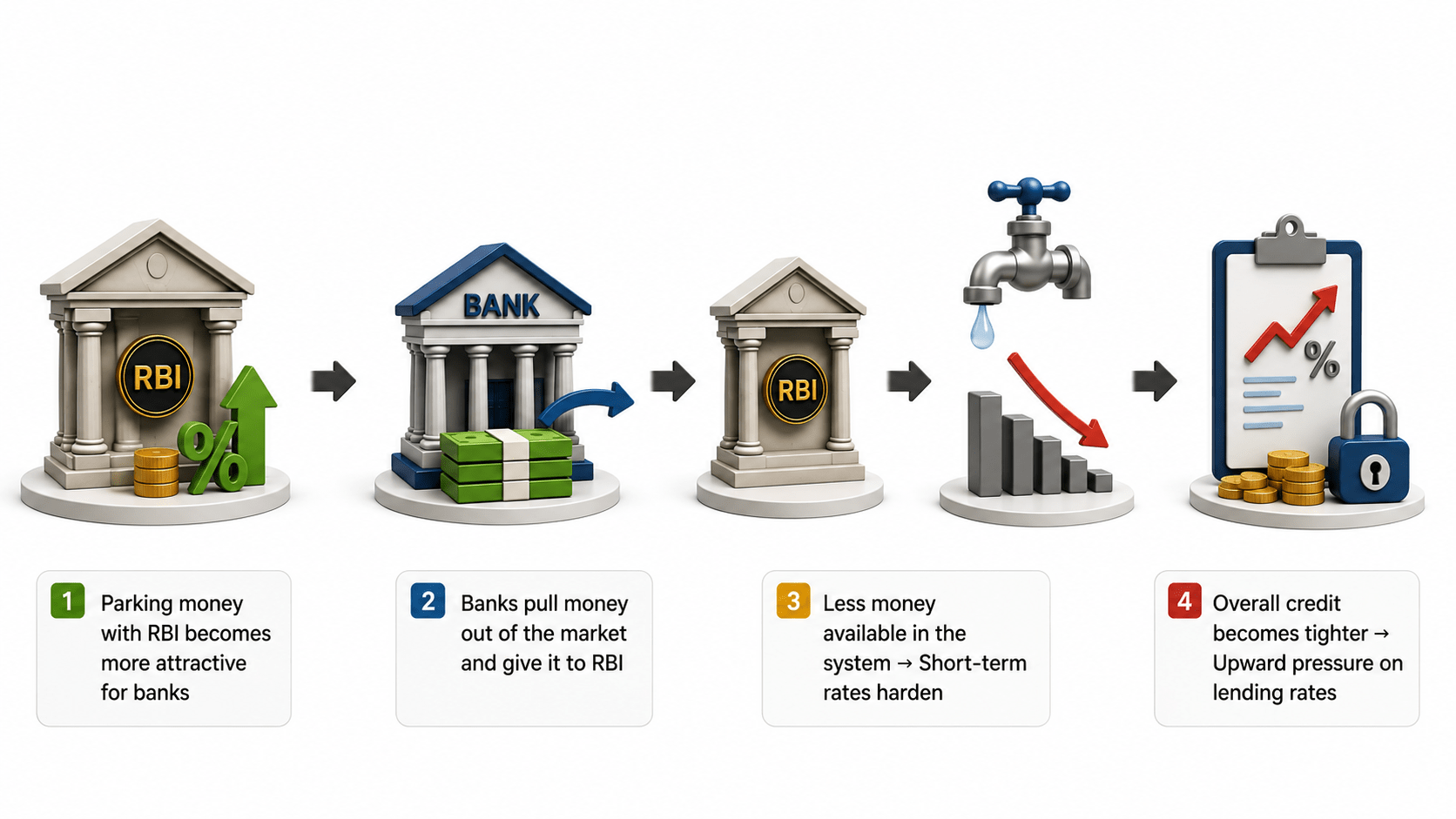

Impact on Reverse Repo Rate when it goes UP:

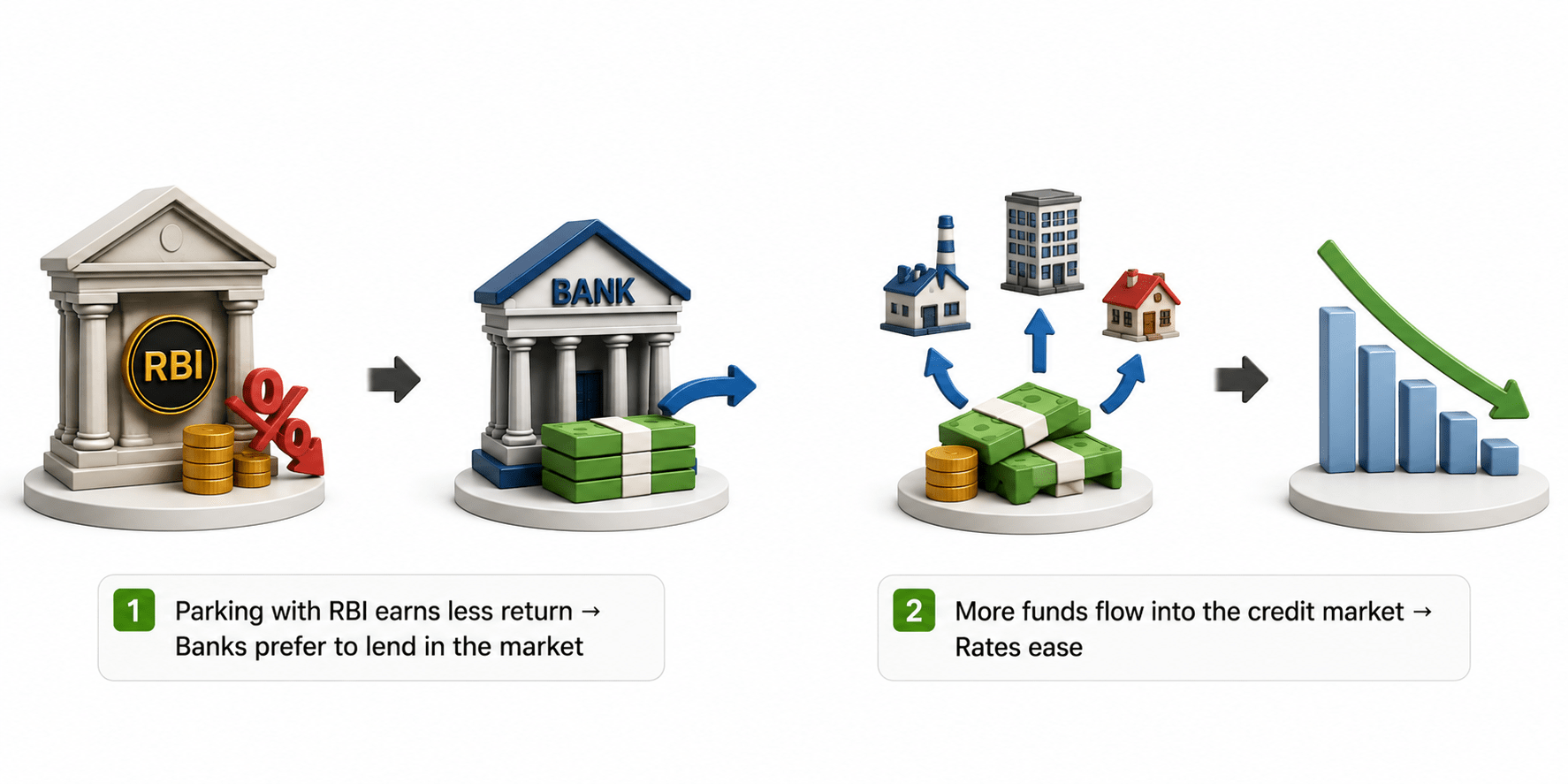

Impact on Reverse Repo Rate when it goes DOWN:

Real-Life Example:

During COVID (2020), RBI slashed Reverse Repo Rate from 4.00% to 3.35% to push banks to stop "lazy banking" — i.e., parking money with RBI instead of lending it to businesses. Banks were nudged to lend more to MSMEs and individuals to revive the economy.

Note: Reverse Repo Rate does not change the Bank Rate directly. It sets the floor for market interest rates.

CRR (Cash Reserve Ratio) → Locks Bank Money, Raises Rates

Every bank must keep a fixed percentage of its total deposits as cash with the RBI. This money earns no interest and cannot be used for lending.

Impact on CRR when it goes UP:

More cash is locked with RBI → Banks have less money to lend

Less credit supply → Demand for loans stays same but supply shrinks

Banks raise lending rates to protect profit margins

Effective cost of borrowing rises

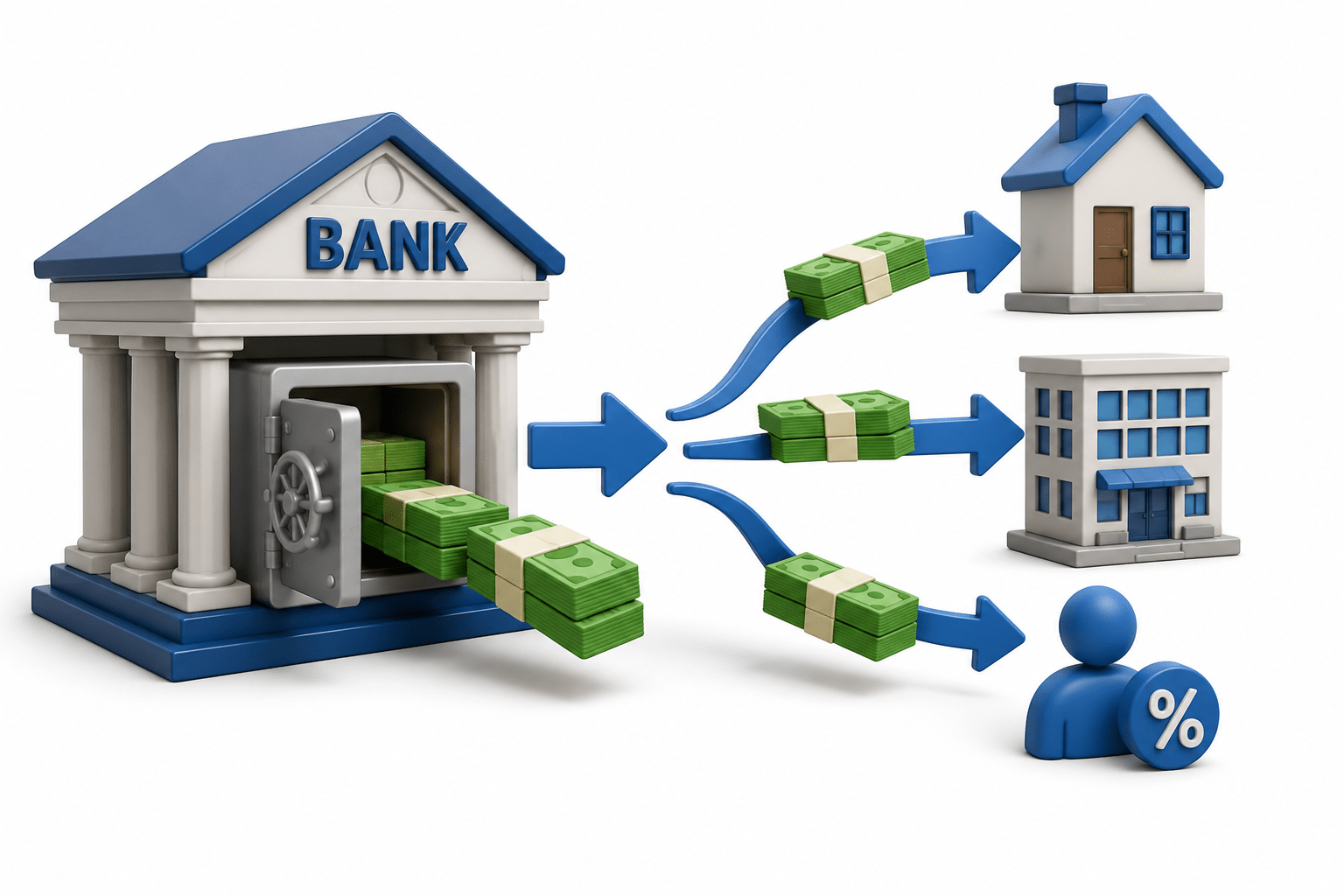

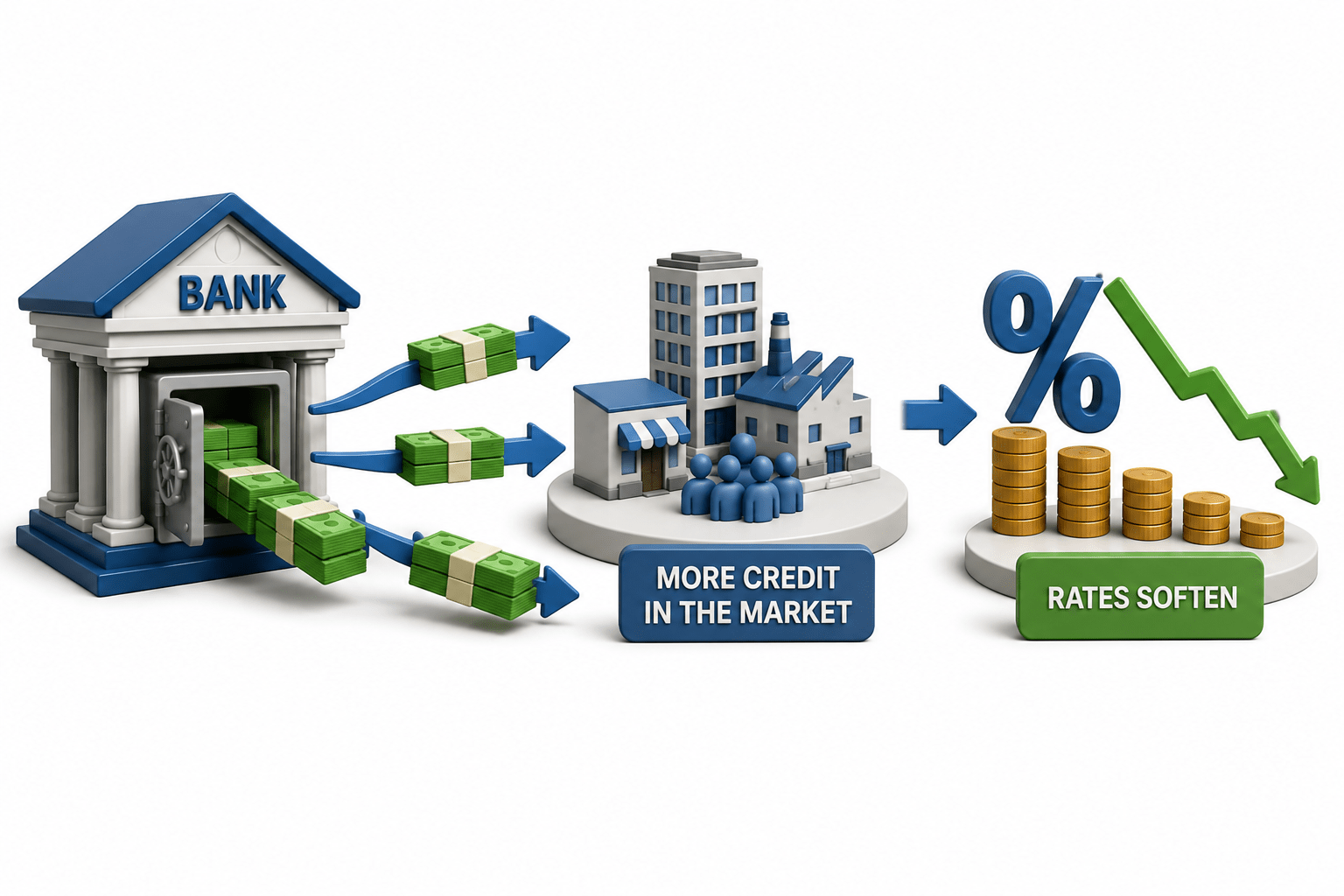

Impact on CRR when it goes DOWN:

Banks free up more cash for lending

More credit in the market → Rates soften

Real-Life Example:

In March 2020, RBI reduced CRR from 4% to 3%, releasing about ₹1.37 lakh crore into the banking system and boosting lending during the COVID-19 slowdown.

Simple Rule: CRR↑ = Less lendable money = Tighter credit = Higher effective rates

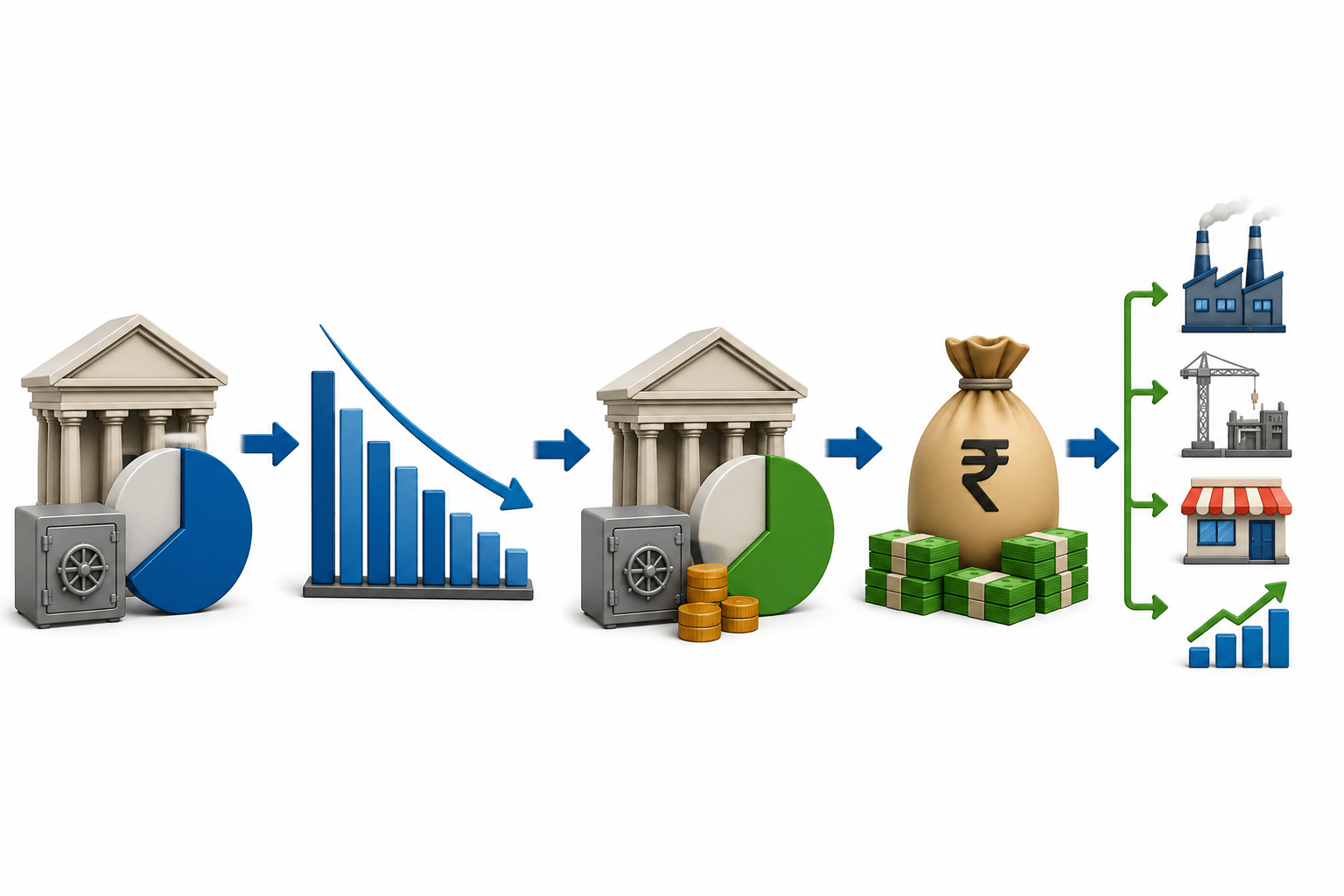

SLR (Statutory Liquidity Ratio) → Ties Up Bank Funds in Safe Assets

Banks must keep a portion of deposits in safe assets like government securities, treasury bills, or gold. Unlike CRR, these assets earn interest.

Impact on SLR when it goes UP:

→ More of the bank's funds are tied up in government bonds

→ Less money is available for commercial loans

→ Reduced credit supply → Upward pressure on lending rates

Impact on SLR when it goes DOWN:

→ Banks can deploy more funds into the credit market

→ Greater credit availability → Lending rates ease

Real-Life Example:

SLR has fallen from 38.5% in 1990 to 18% today, freeing more bank funds for lending and supporting economic growth.

CRR vs SLR in one line:

CRR → Cash held with RBI, earns nothing

SLR → G-Secs / gold held by bank, earns a small yield — but both reduce credit supply

Summary

5

SLR requires banks to hold safe assets.

4

CRR affects banks' lending capacity.

3

Reverse Repo Rate manages excess liquidity.

2

Repo Rate controls bank borrowing from RBI.

1

Bank Rate and Repo Rate affect borrowing costs.

Quiz

What happens when the Repo Rate increases?

A. Loans become cheaper

B. Banks lend more money

C. Borrowing becomes expensive

D. Inflation increases immediately

Quiz-Answer

What happens when the Repo Rate increases?

A. Loans become cheaper

B. Banks lend more money

C. Borrowing becomes expensive

D. Inflation increases immediately

By Content ITV