German Health Insurance: GKV vs PKV

A Comprehensive Analysis for Informed Decision-Making

Introduction

- Agenda: Deep dive into GKV and PKV

- Focus: Unpacking the complexities and subtle nuances

- Audience: Tailored for informed decision-makers and expats with a keen interest in German healthcare system

Advanced Benefits of GKV

- Collective Risk Management: GKV's solidarity principle means risk is shared among all insured, stabilizing costs.

-

Regulatory Protection: GKV is heavily regulated, ensuring consistent coverage across all Krankenkassen, on flipside lots of paperwork

- Example: A freelance writer with a chronic condition doesn't have to worry about coverage denial or premium hikes.

-

Social Security Integration: GKV is well integrated into other social benefits. GKV + Harz -> GKV + ALG 1 -> GKV + Work

- Example: A photographer on parental leave continues to receive healthcare coverage without additional paperwork or costs.

Advanced Benefits of PKV

- Customized Premiums and Coverage: PKV offers tailored plans based on individual health risks and preferences.

- Superior Service and Amenities: Access to better facilities, shorter waiting times, and more comprehensive services.

-

Long-term Financial Planning: High-income individuals can leverage PKV for potentially lower lifetime costs.

- Example: Each PKV has Altersrucklage - it saves up part of costs into personal fund, which will be used when you get older.

Drawbacks and Risks of GKV

-

Limited Coverage Scope: GKV may not cover certain treatments and medications.

- Example: A freelance journalist needs specific non-standard mental health therapy not covered by GKV.

-

Less Flexibility in Provider Choice: Limited ability to choose healthcare providers or specialists.

- Example: An expat artist struggles to find English-speaking doctors within the GKV network.

-

Potential for Service Delays: Longer waiting times for appointments and treatments.

- Example: A graphic designer waits months for a non-urgent MRI scan under GKV.

Drawbacks and Risks of PKV

-

Age and Health-Related Premium Increases: Premiums rise with age and changing health conditions.

- Example: A middle-aged photographer faces steep premium increases after a diabetes diagnosis.

-

Complexity in Policy Selection and Management: PKV plans can be intricate, requiring careful selection and understanding.

- Example: A software developer spends weeks comparing PKV plans to find the right balance of coverage and cost.

-

Potential Financial Burden for Families: Each family member needs a separate policy.

- Example: A novelist with three children finds the cumulative cost of individual PKV policies financially challenging.

PKV Premium Adjustments in Light of Health Changes

- Myth Buster: PKV premiums do not increase due to individual health changes or new diagnoses.

- Initial Risk Assessment: Premiums set based on health status at policy inception - it's your health "snapshot."

- Age and General Cost Factors: Premiums rise due to aging and overall healthcare cost increases

- No Individual Penalties for Illness: Developing a new condition or health deterioration doesn't trigger a personal premium hike.

- Beitragsanpassung Explained: Premium adjustments are due to collective factors like medical inflation, not individual health trajectories.

- Key Consideration: Long-term planning is crucial; switching plans later can be costlier due to age and current health.

Payments to Doctors - GOÄ

-

Higher Reimbursement Rates in PKV: Doctors earn more from PKV patients, potentially leading to prioritized treatment.

- Example: A freelance photographer notices quicker appointments and more attentive care compared to her GKV-covered peers.

-

Billing Flexibility and Transparency: PKV patients often have a clearer understanding of healthcare costs.

- Example: A graphic designer in PKV receives detailed billing for each service, understanding exactly what is paid for.

-

Impact on Medical Service Access: Preference for PKV patients can sometimes lead to indirect service disparities.

- Example: An expat teacher in GKV experiences longer wait times for specialist appointments compared to PKV counterparts.

Switching from PKV to GKV

-

Income Threshold Considerations: Dropping below the Jahresarbeitsentgeltgrenze enables a return to GKV.

- Example: A software engineer switches to a lower-paying job and becomes eligible to return to GKV.

-

Age-Related Restrictions: Under 55, switching is feasible; over 55, it becomes significantly harder.

- Example: A 56-year-old freelancer finds it nearly impossible to switch back to GKV after a health scare.

-

Employment Changes Impacting Eligibility: Job status changes can open a window to GKV.

- Example: Transitioning to part-time work allows a PKV-covered musician to opt back into GKV.

Additional Factors: Kur, Krankentagegeld, Beitragsanpassung

-

Kur (Rehabilitation) Coverage Differences: GKV typically covers rehabilitation measures, unlike some PKV plans.

- Example: An author with chronic back pain benefits from a Kur covered by GKV, which wouldn't be covered under her previous PKV plan.

-

Krankentagegeld (Sick Pay) in PKV: PKV often includes compensation for income loss during long-term illness.

- Example: A freelance consultant relies on Krankentagegeld from PKV during a prolonged illness.

-

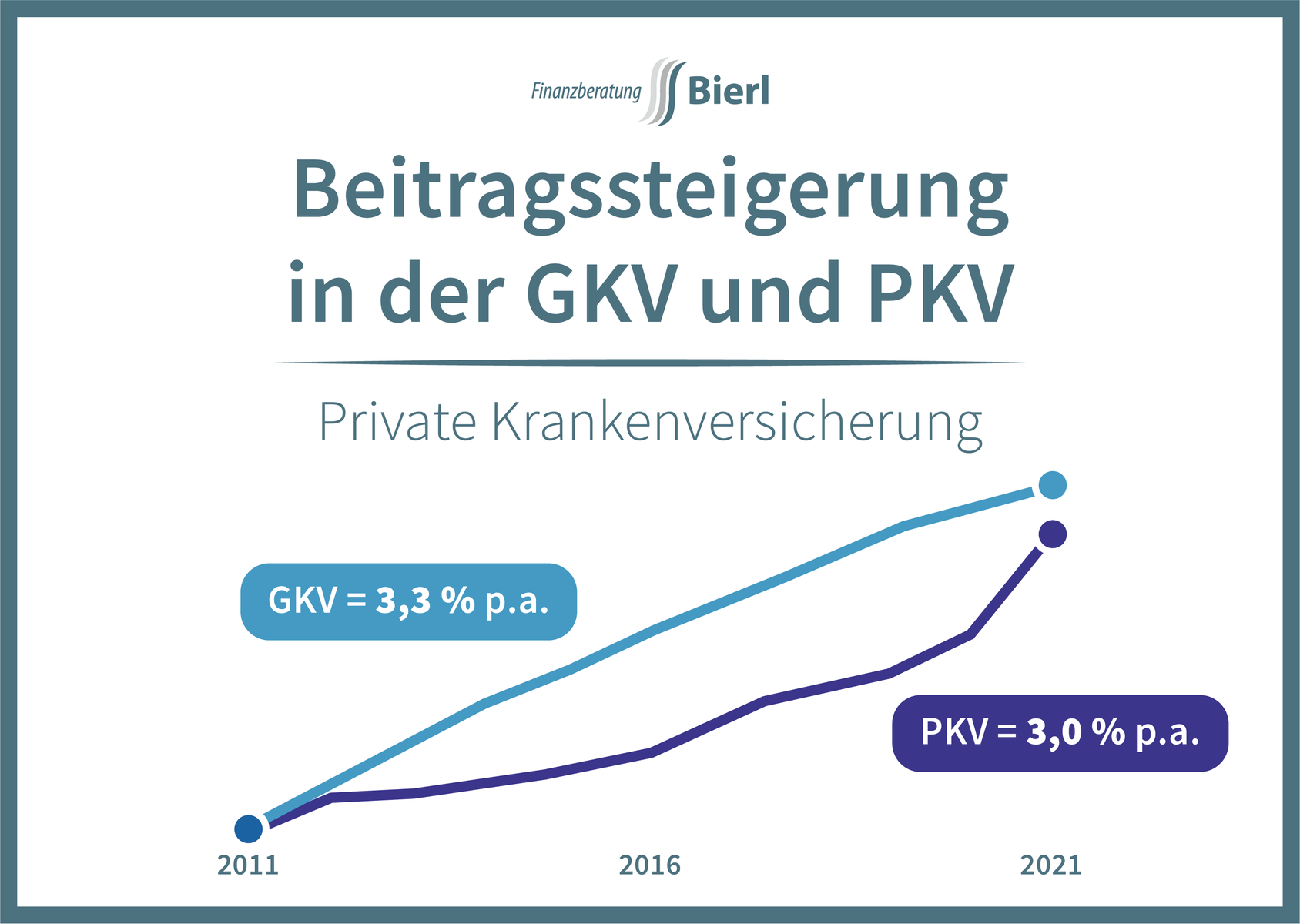

Beitragsanpassung Dynamics: PKV premiums adjust based on various factors, leading to potential increases.

- Example: An expat engineer experiences a significant Beitragsanpassung due to aging and changes in the health insurance market.

Conclusion

- Decision Making: Choosing between GKV and PKV depends on personal circumstances, health status, and long-term plans.

- Expert Advice: Consider consulting a Versicherungsberater for personalized advice tailored to your specific situation.

- Stay Informed: Regularly review and adjust your health insurance plan to align with your changing life and health circumstances.

German Health Insurance: GKV vs PKV

By Tim Zadorozhniy