Presentations

Templates

Features

Teams

Pricing

Log in

Sign up

Log in

Sign up

Menu

Winter School in Political Economy

Lecture 3

Inequality

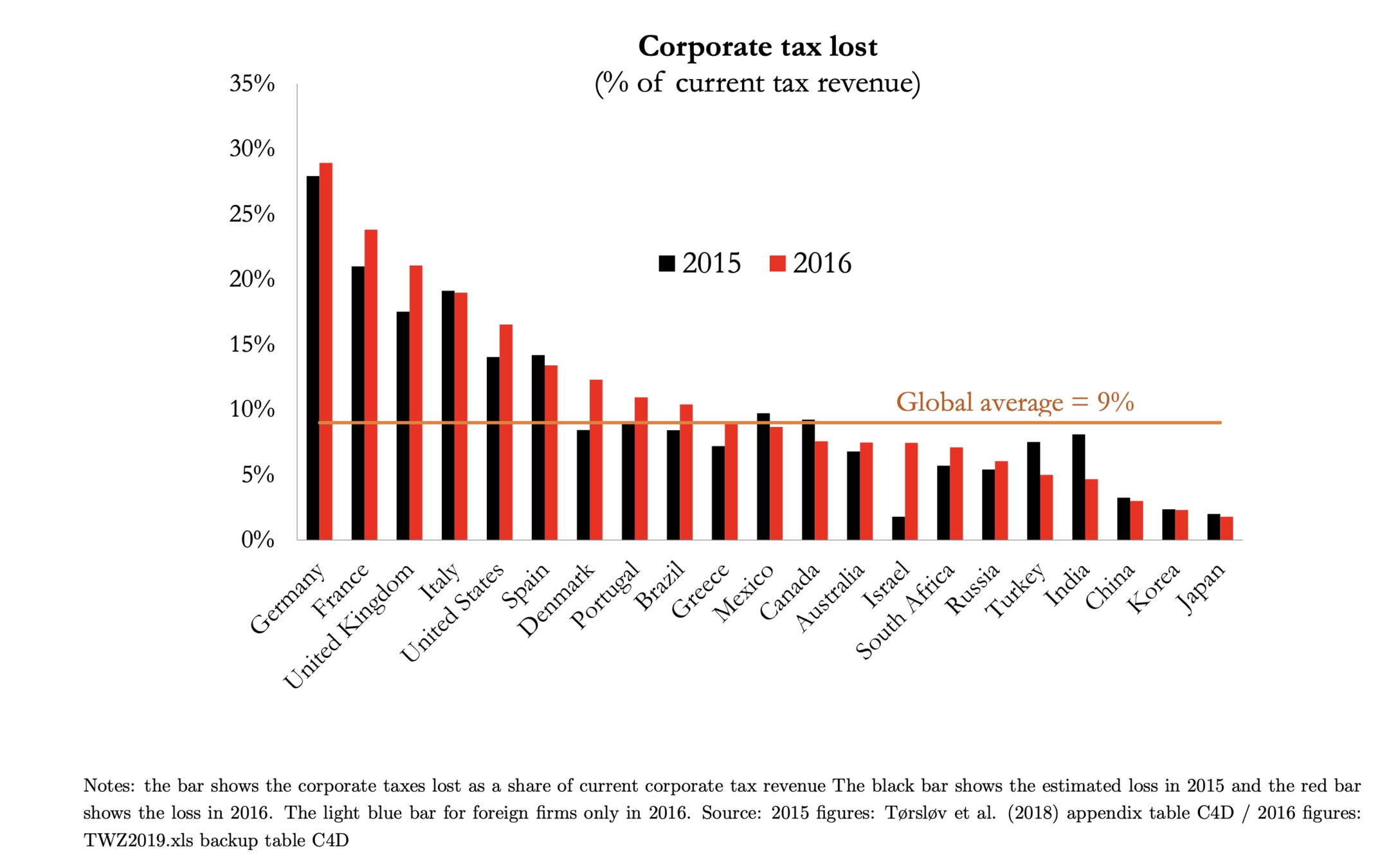

Where do we stand

1985 to 2019 decrease from 49% to 23% in the global average statutory corporate tax rate

Largely driven by tax competition – race to the bottom

Distinction between real and nominal tax rate

Distinction between optimisation and avoidance

Weak international efforts

Direction of change

Tax deficit

as if all profits were subject to min rate

min rate at 21% for foreign earning of US MNC

CIT in US at 28%

tax collector of last resort

Coordination through OECD and G20

moving ahead of BEPS

Unilateral actions against non-adopting tax havens

Thank you and see you in the Q&A

Winter School in Political Economy Lecture 3

By Dawid Walentek

Winter School in Political Economy Lecture 3

178

Dawid Walentek

post-doc @UGent

dawid_walentek

More from

Dawid Walentek