dviljoen

A user-made collection of slides to assist in the learning of FET Mathematics taught in a South African school.

and

Interest or depreciation is calculated using the initial amount.

Interest or depreciation is calculated using the current value of the loan or investment.

Simple interest

Straight-line depreciation

Compound interest

Reducing-balance depreciatation

An interest rate which is compounded more than once a year

The interest rate which would affect the same change per year as a nominal interest rate

...for converting the nominal rate to the annual effective rate.

compounded

only compounded

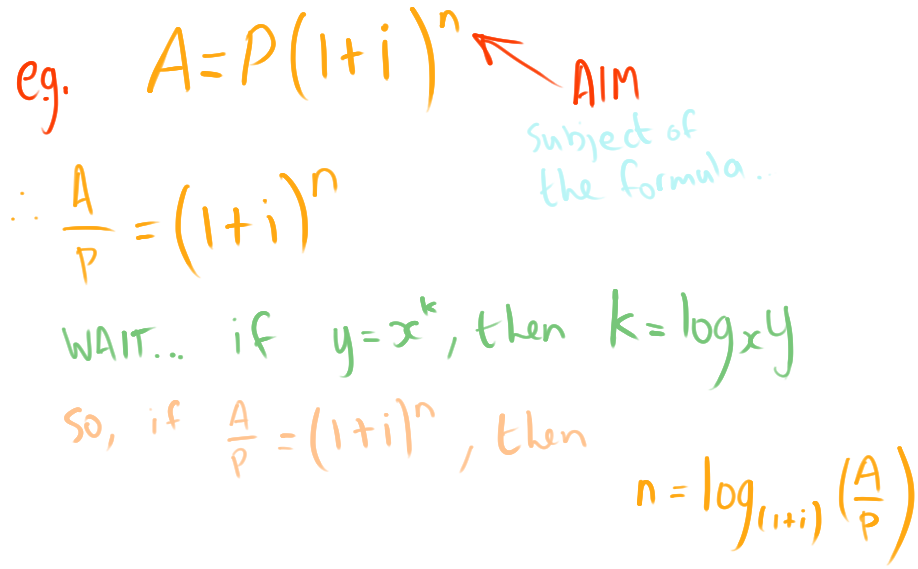

Using knowledge of logarithms, one is now able to solve for a particular time period of a loan or investment as follows:

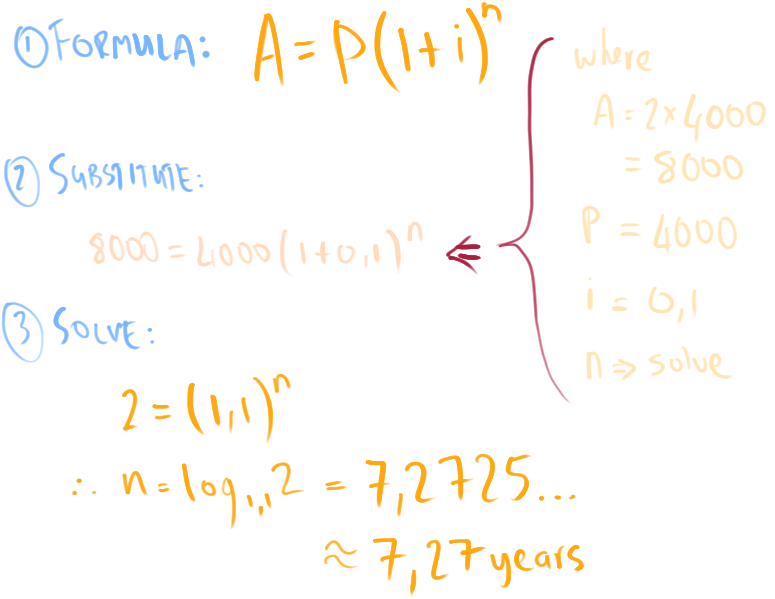

R4000 is deposited in a savings account paying 10% per annum compounded annually. How long will it take for the savings account to double?

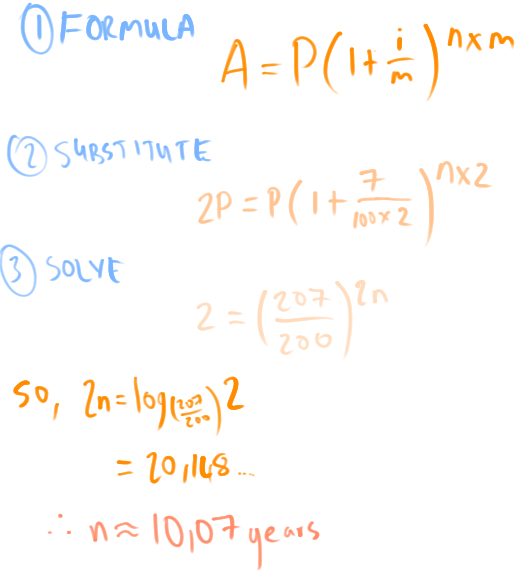

The interest rate for a loan is 7% compounded half-yearly. How many years will it take the loan amount to double?

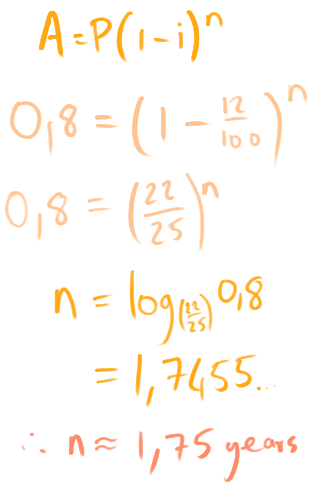

A motor car depreciates at 12% per annum using the reducing-balance method. After what length of time will the value of the car be 80% of the original selling price?

Money is invested at regular intervals such that all the payments - as well as the compound interest earned - contribute to the total value of the investment when it matures.

| Type | Example | Effective Rate |

|---|---|---|

| Short term | 5-year savings policy | ~9% p.a |

| Long term | Retirement Annuity | ~8% p.a |

If R500 is invested every month, with the account having an interest rate of 12% per annum compounded monthly, calculate the savings after 3 months.

| Time | Interest | Payment | Balance |

|---|---|---|---|

| 0 months | R0 | R500 | R500 |

| 1 months | R5 | R500 | R1005 |

| 2 months | R10.05 | R500 | R1515.05 |

| 3 months | R15.15 | R500 | R2030.20 |

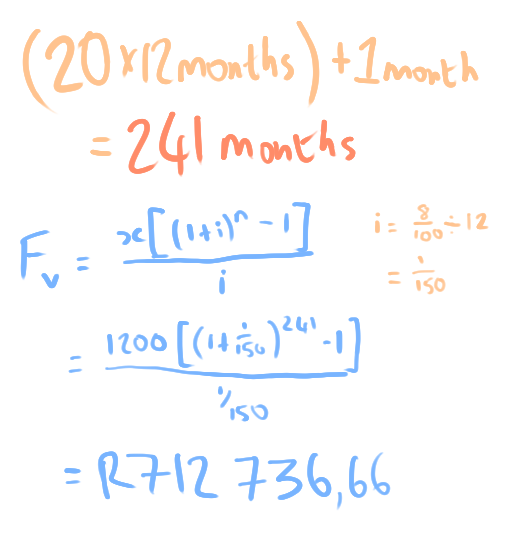

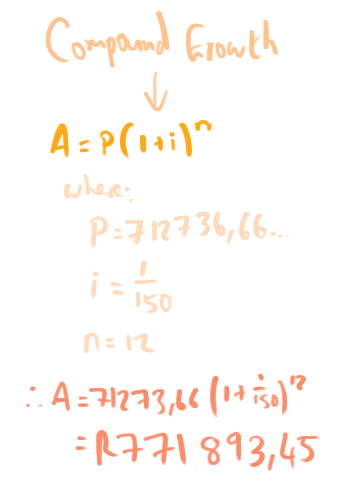

R1200 is deposited into a savings plan - while the monthly payments continue at the end of every month for the next 20 years. If the interest remains fixed at 8% per annum compounded monthly:

Instalments are made at regular intervals such that all the repayments contribute to the total repayment of the loan - as well as the interest charged during the term.

| Type | Example | Effective Rate |

|---|---|---|

| Short term | Unsecured Loan | 30-60% p.a |

| Long Term | Home Loan | ~10.5% p.a |

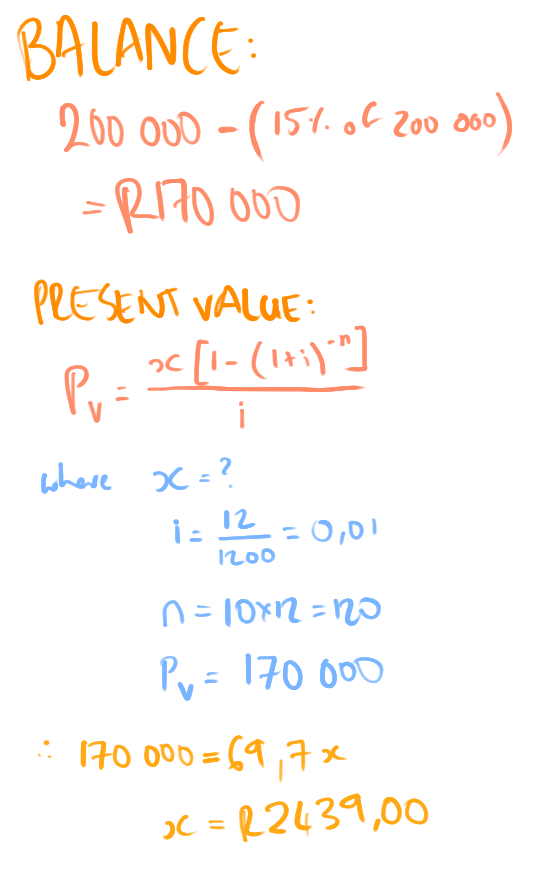

A loan is taken out to the value of R200 000. A 15% deposit is paid, and the balance is settled through fixed monthly instalments for the next 10 years. The interest rate is 12% per annum compounded monthly.

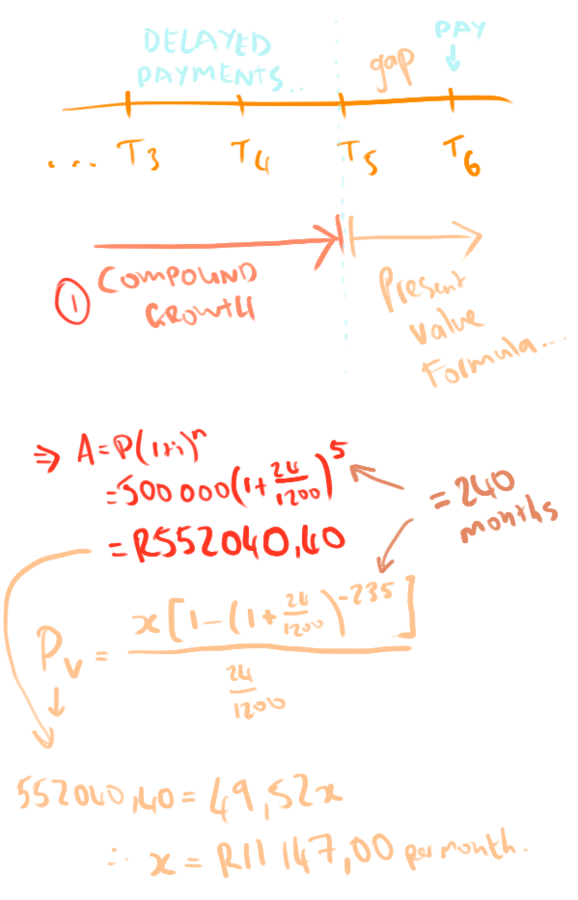

A business takes out a 20 year loan of R500 000. The loan is repaid by means of equal monthly repayments, starting 6 months after granting the loan. The interest rate is 24% per annum compounded monthly.

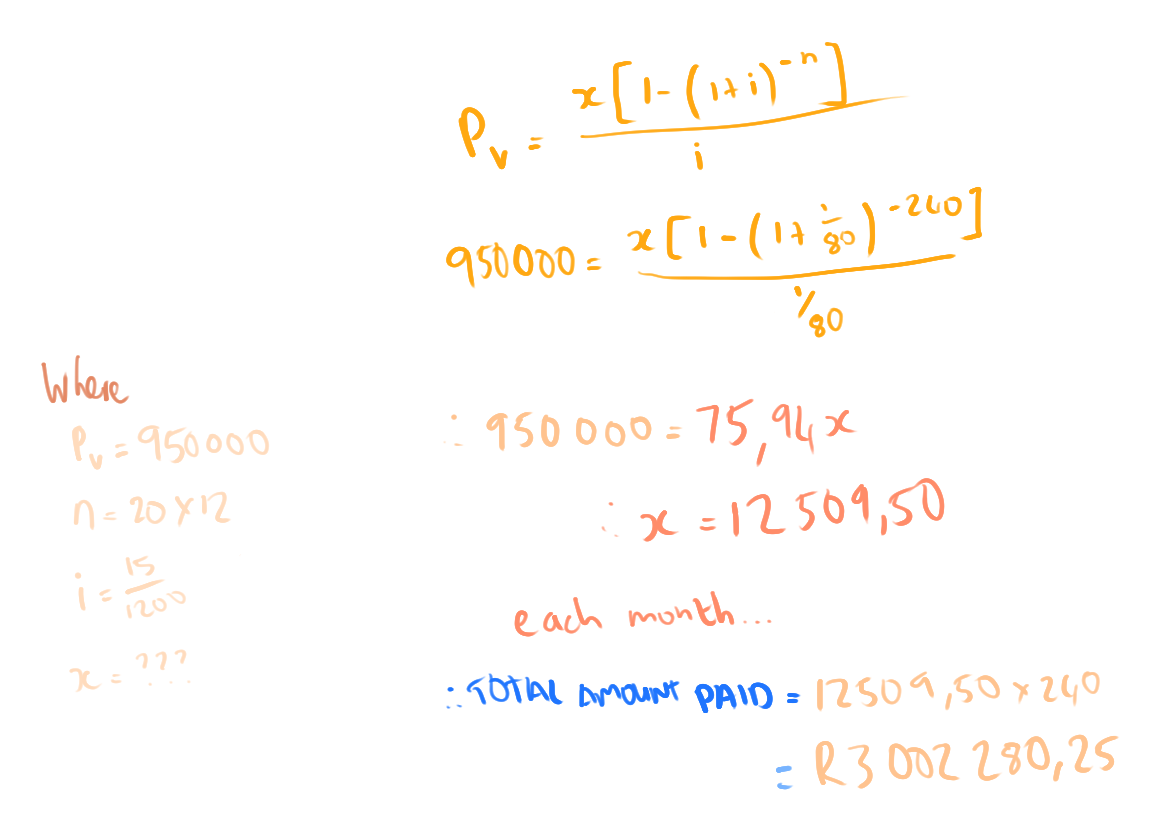

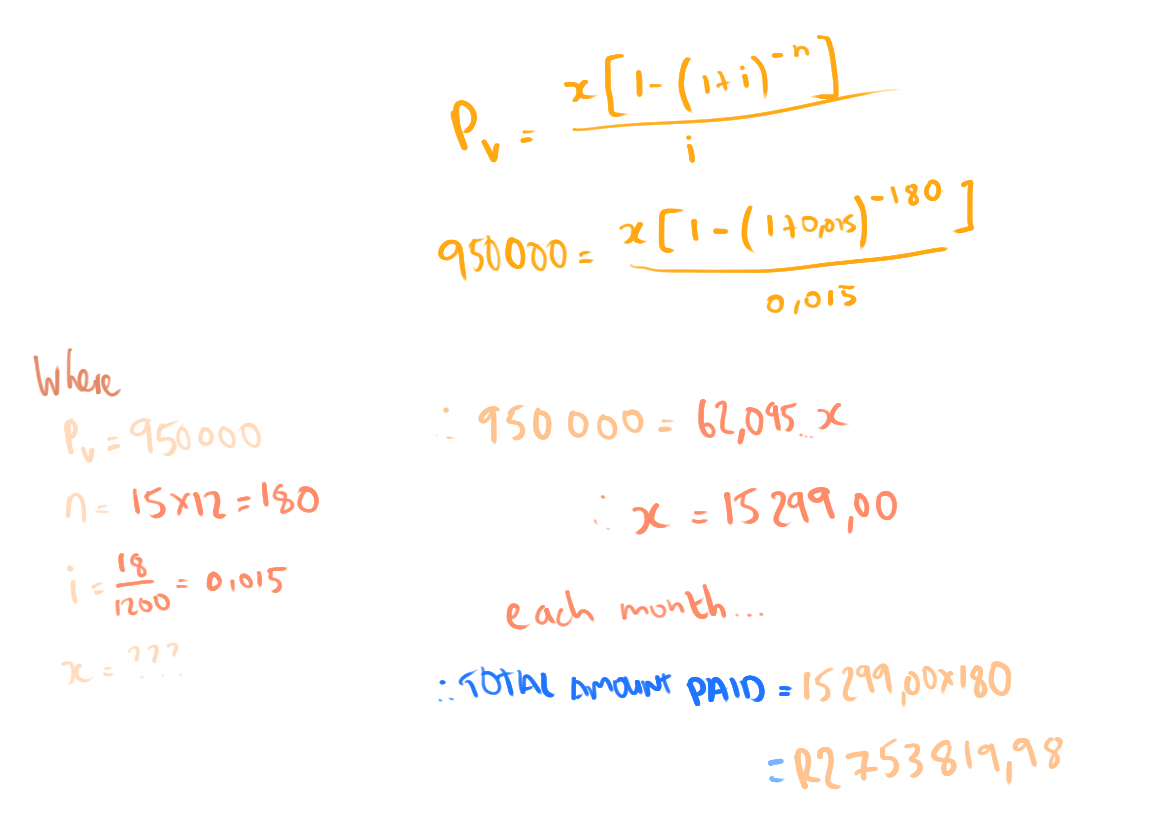

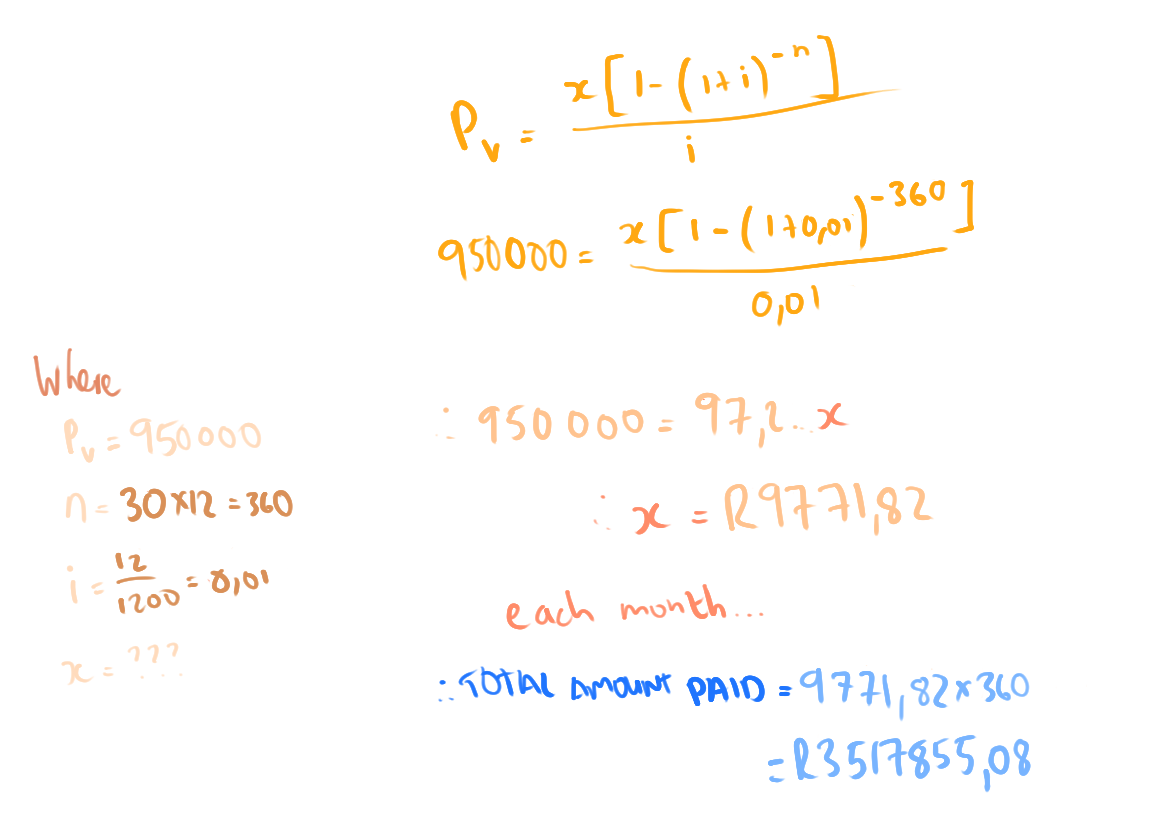

A customer is searching for the most affordable home loan for R950 000. He receives the following offers from 3 different banks shown below:

| Bank | Term | Interest |

|---|---|---|

| Option A | 20 years | 15% |

| Option B | 15 years | 18% |

| Option C | 30 years | 12% |

(Interest is calculated per annum, compounded monthly)

A customer is searching for the most affordable home loan for R950 000.

| Term | Interest |

|---|---|

| 20 years | 15% |

(Interest is calculated per annum, compounded monthly)

A customer is searching for the most affordable home loan for R950 000.

| Term | Interest |

|---|---|

| 15 years | 18% |

(Interest is calculated per annum, compounded monthly)

A customer is searching for the most affordable home loan for R950 000.

| Term | Interest |

|---|---|

| 30 years | 12% |

(Interest is calculated per annum, compounded monthly)

A customer is searching for the most affordable home loan for R950 000. He receives the following offers from 3 different banks shown below:

| Bank | Term | Interest | Monthly Repayments | Total Amount |

|---|---|---|---|---|

| Option A | 20 yrs | 15% | R12 509.50 | R3 002 208.25 |

| Option B | 15 yrs | 18% | R15 299.00 | R2 753 819.98 |

| Option C | 30 yrs | 12% | R9 771.82 | R3 517 855.08 |

(Interest is calculated per annum, compounded monthly)

NOTE: Option C has the lowest monthly repayment amount, so while it may be easier from a month-to-month basis, it also generates the largest total amount paid by the end of the term.

Option B has the lowest total amount required to be paid, and therefore should be the best option - as long as the monthly repayments are feasible according to the person's monthly budget.

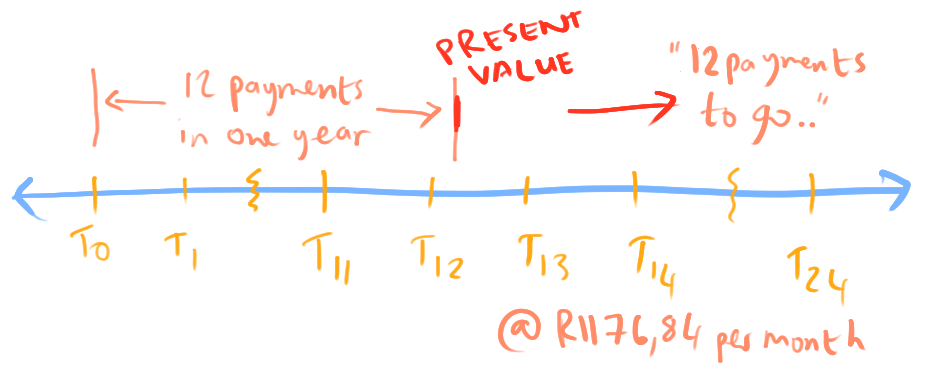

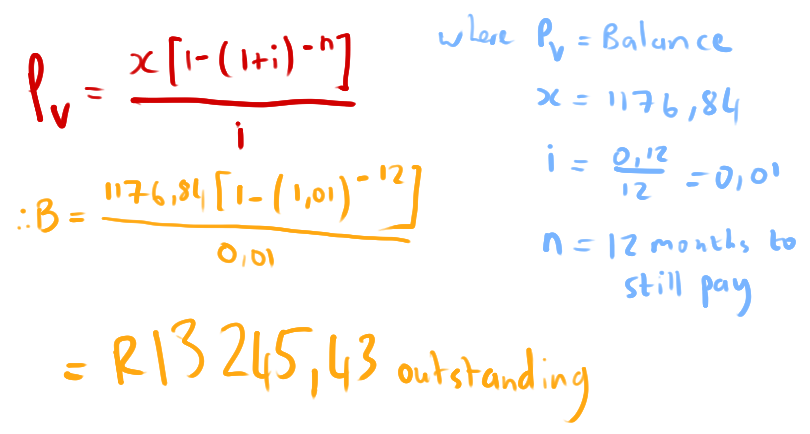

It is useful to be able to calculate the balance of a loan, and to know it at a specific time during the course of the loan.

A R25 000 loan for 2 years is paid back through monthly payments of R1 176.84 starting one month after the granting of the loan. If interest is calculated at 12% per annum compounded monthly:

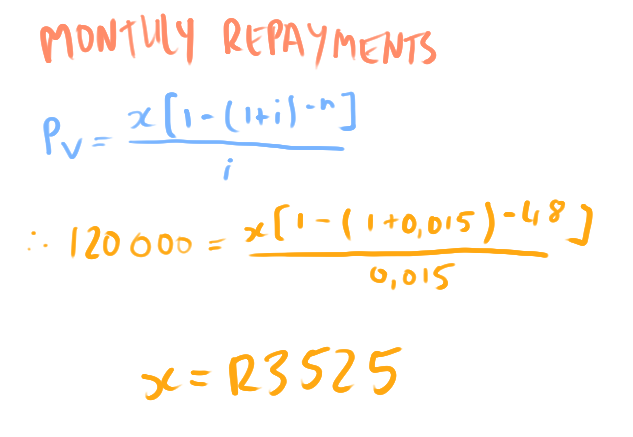

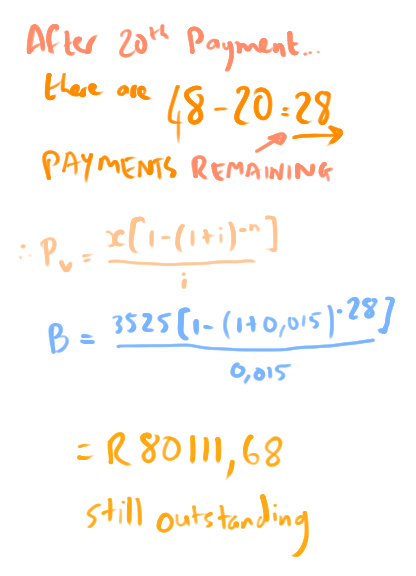

A R120 000 loan is granted over four years at an interest rate of 18% per annum compounded monthly.

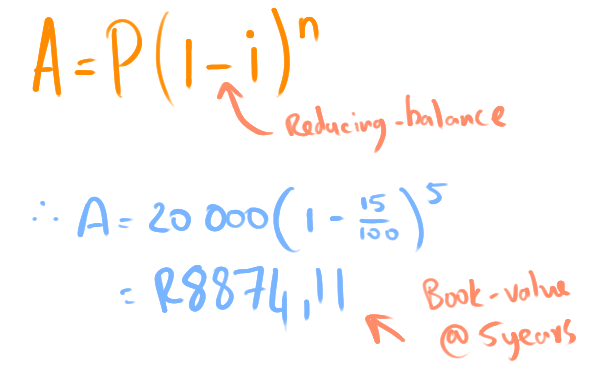

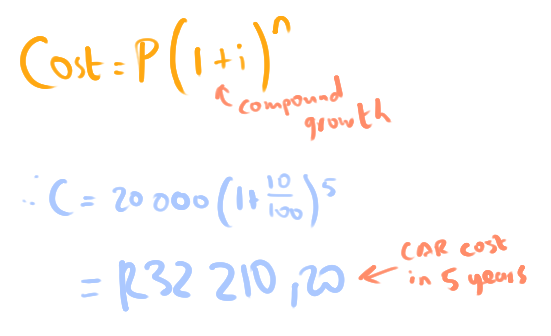

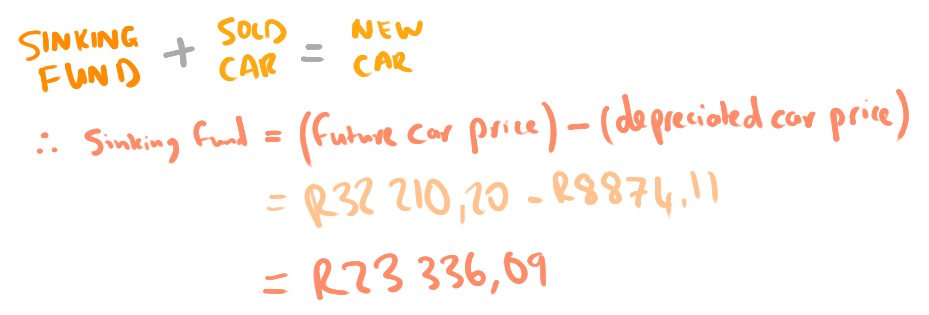

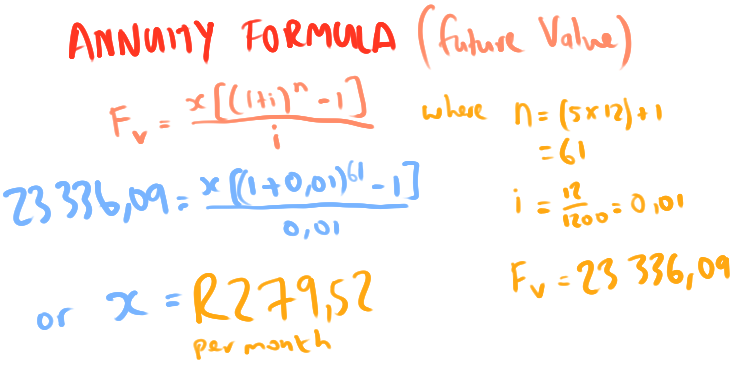

A R20 000 car is bought which depreciates in value at 15% per annum on a reducing-balance. A new car in 5 years time is estimated to have increased in value by 10% every year. The car will be sold at the end of the 5 years, so a sinking fund is set up in order to buy the new car. The sinking fund will grow at 12% per annum compounded monthly, with a first payment made immediately, and the final payment at the end of 5 years.

A company may purchase assets which will be used for a certain period of time and then sold or disposed of when new assets are purchased. A savings plan is often set up in order to prepare for this future, and this account is often known as a SINKING FUND.

A R20 000 car is bought which depreciates in value at 15% per annum on a reducing-balance. A new car in 5 years time is estimated to have increased in value by 10% every year. The car will be sold at the end of the 5 years, so a sinking fund is set up in order to buy the new car. The sinking fund will grow at 12% per annum compounded monthly, with a first payment made immediately, and the final payment at the end of 5 years.

A R20 000 car is bought which depreciates in value at 15% per annum on a reducing-balance. A new car in 5 years time is estimated to have increased in value by 10% every year. The car will be sold at the end of the 5 years, so a sinking fund is set up in order to buy the new car. The sinking fund will grow at 12% per annum compounded monthly, with a first payment made immediately, and the final payment at the end of 5 years.

A R20 000 car is bought which depreciates in value at 15% per annum on a reducing-balance. A new car in 5 years time is estimated to have increased in value by 10% every year. The car will be sold at the end of the 5 years, so a sinking fund is set up in order to buy the new car. The sinking fund will grow at 12% per annum compounded monthly, with a first payment made immediately, and the final payment at the end of 5 years.

The sinking fund will grow at 12% per annum compounded monthly, with a first payment made immediately, and the final payment at the end of 5 years.

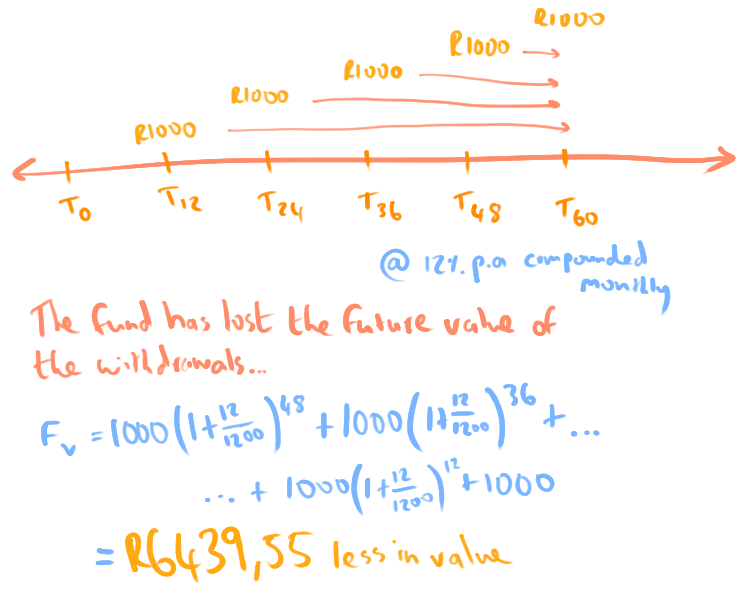

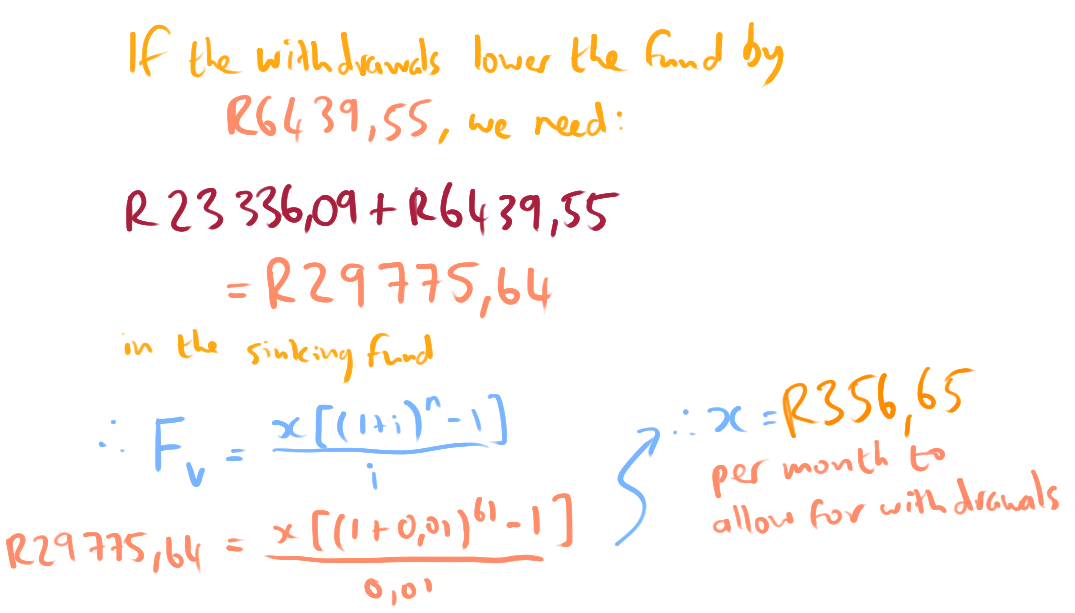

If the business decides to withdraw R1 000 from the account at the end of each year to pay for a car service...

Calculate the adjusted monthly repayments to allow for these withdrawals...

or

or

By dviljoen

A summary of the key concepts for students following the South African CAPS (FET) Mathematics curriculum.