Marius Zoican PRO

I am an Associate Professor of Finance and Canada Research Chair in Financial Technology at the University of Calgary’s Haskayne School of Business. My research sits at the intersection of technology and finance.

Michael Brolley and Marius Zoican

FMA 2020 October 22, 2020

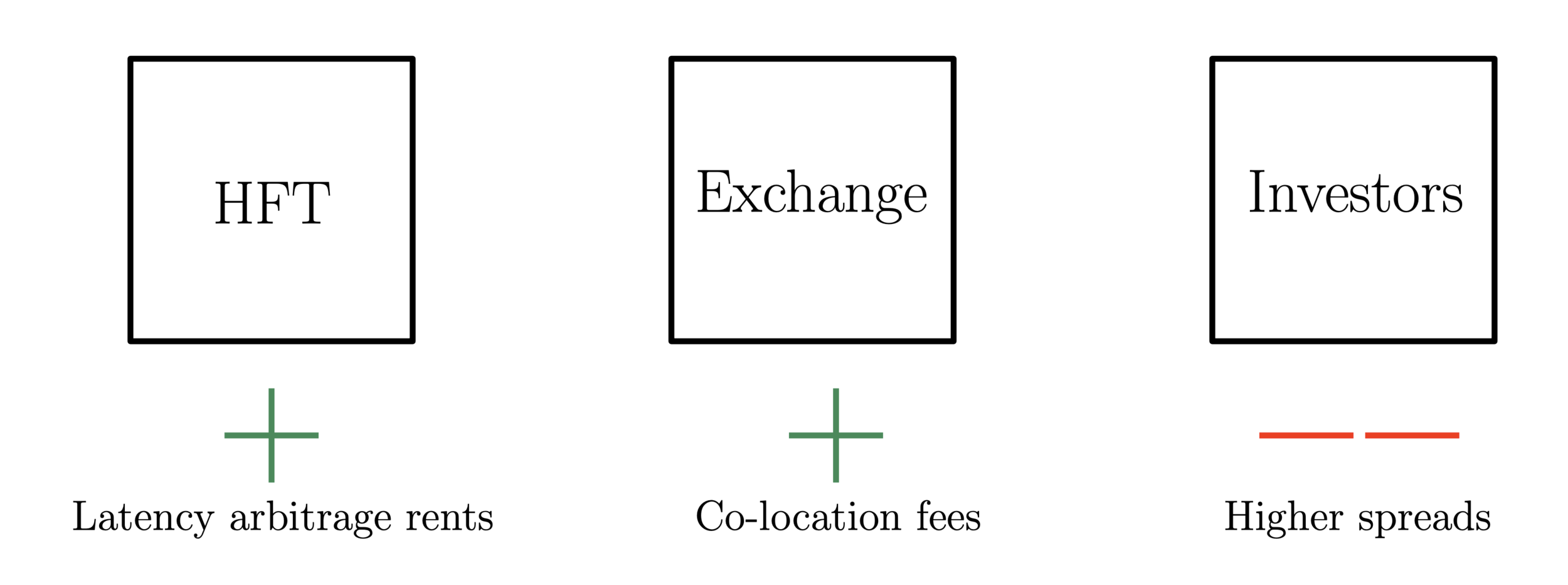

HFT races drive up exchange costs...

...but is that enough to stop them?

Asset

Traders

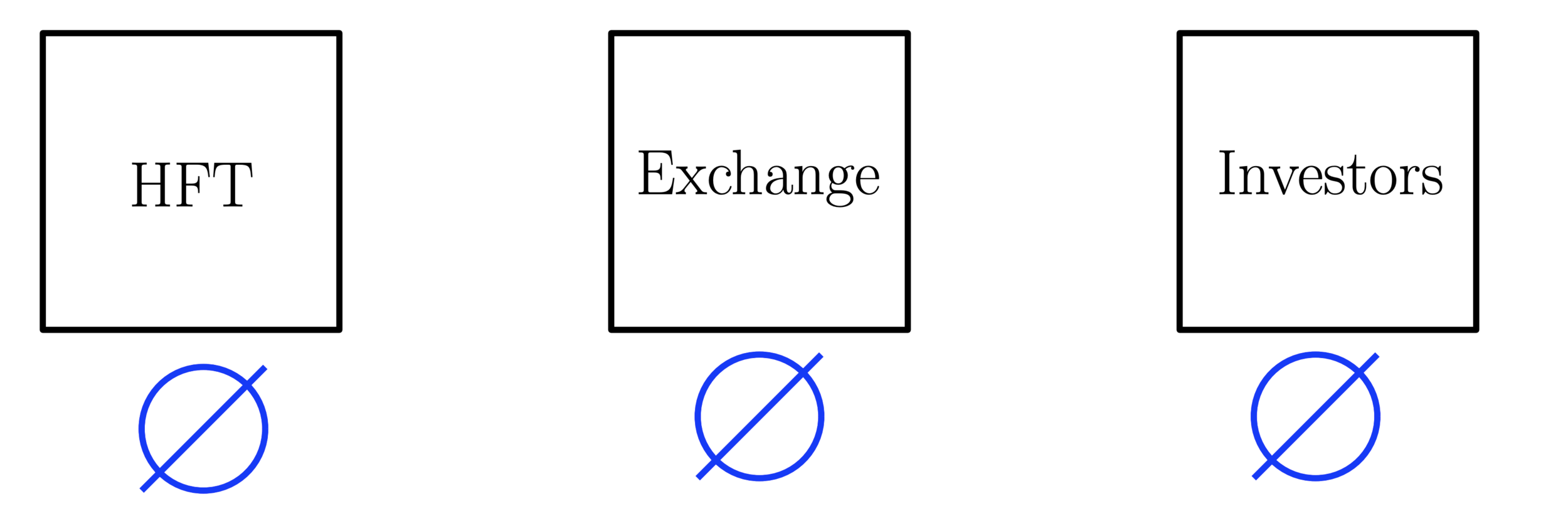

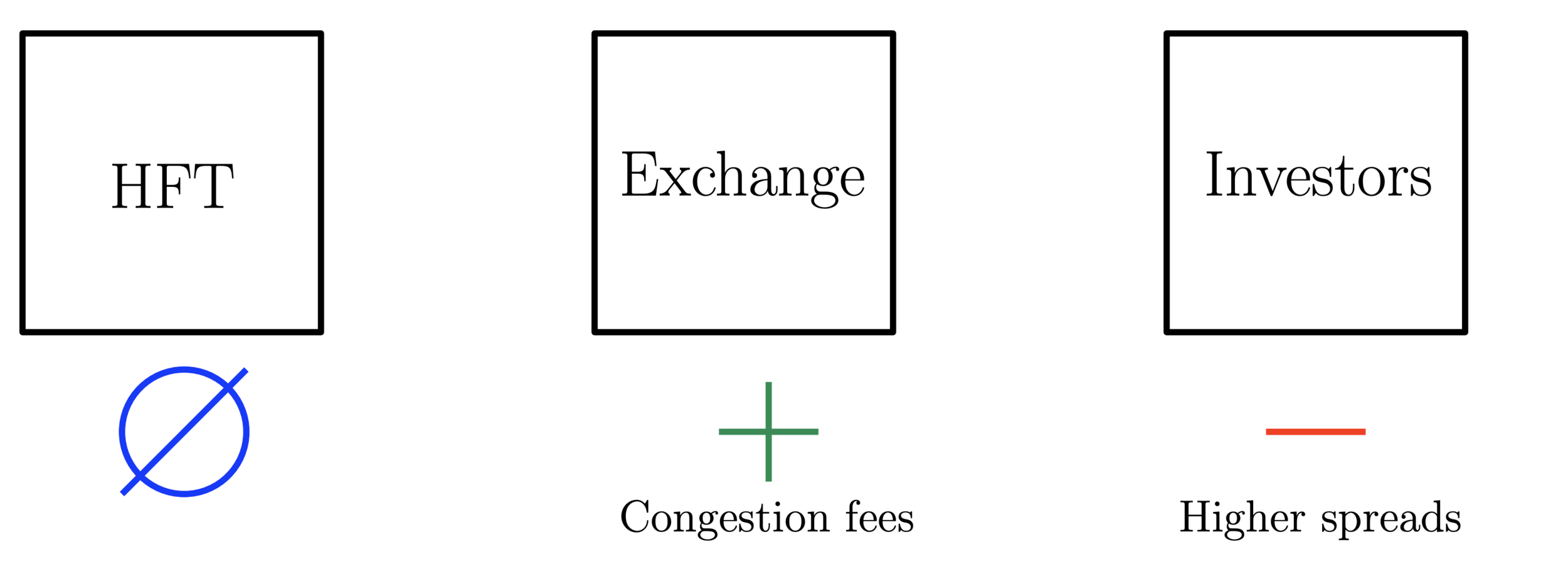

If HFT "snipers'' submit a marketable order simultaneously, each is charged a fee

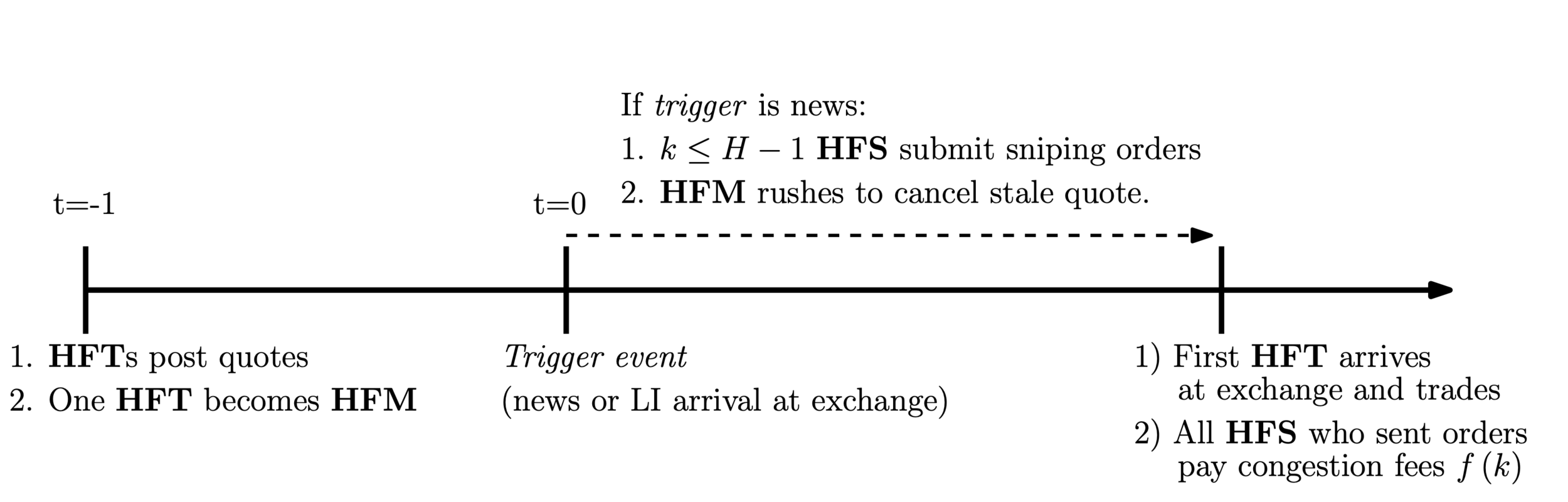

HFTs post quotes at t=0.

Afterwards, nothing happens until a "trigger event:''

HFTs determine:

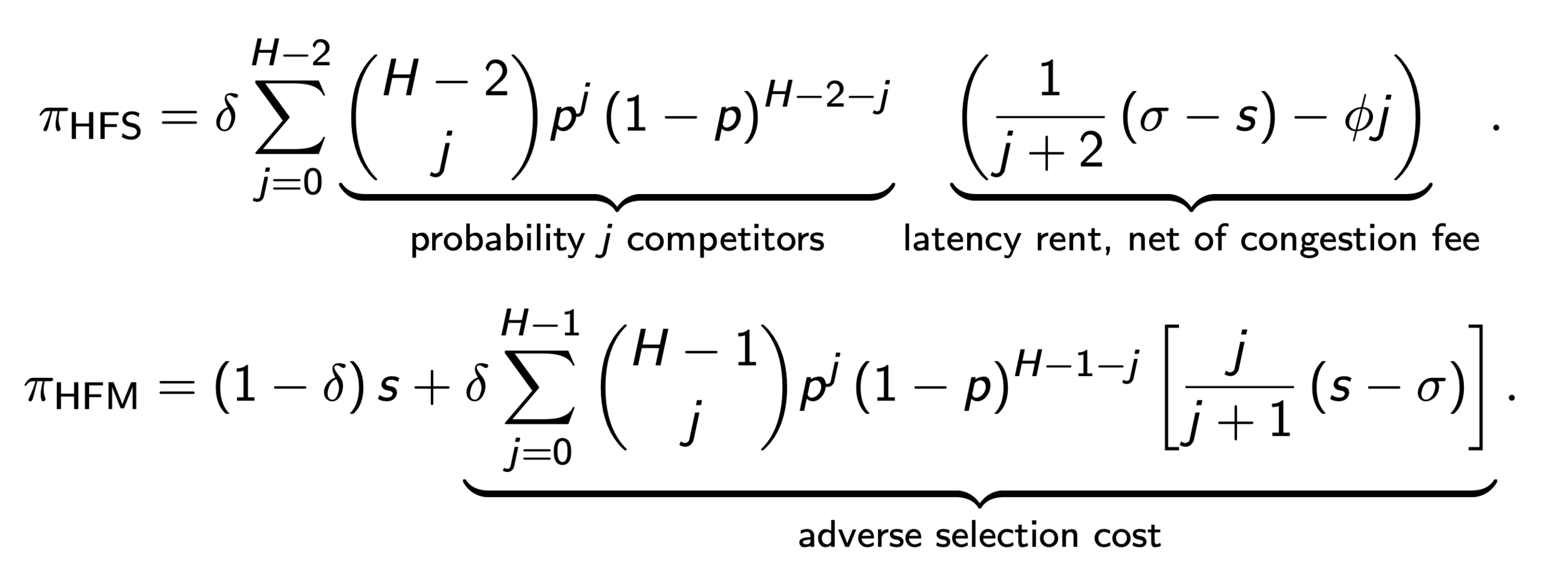

HFT expected profits (sum over random # of competitors in the race)

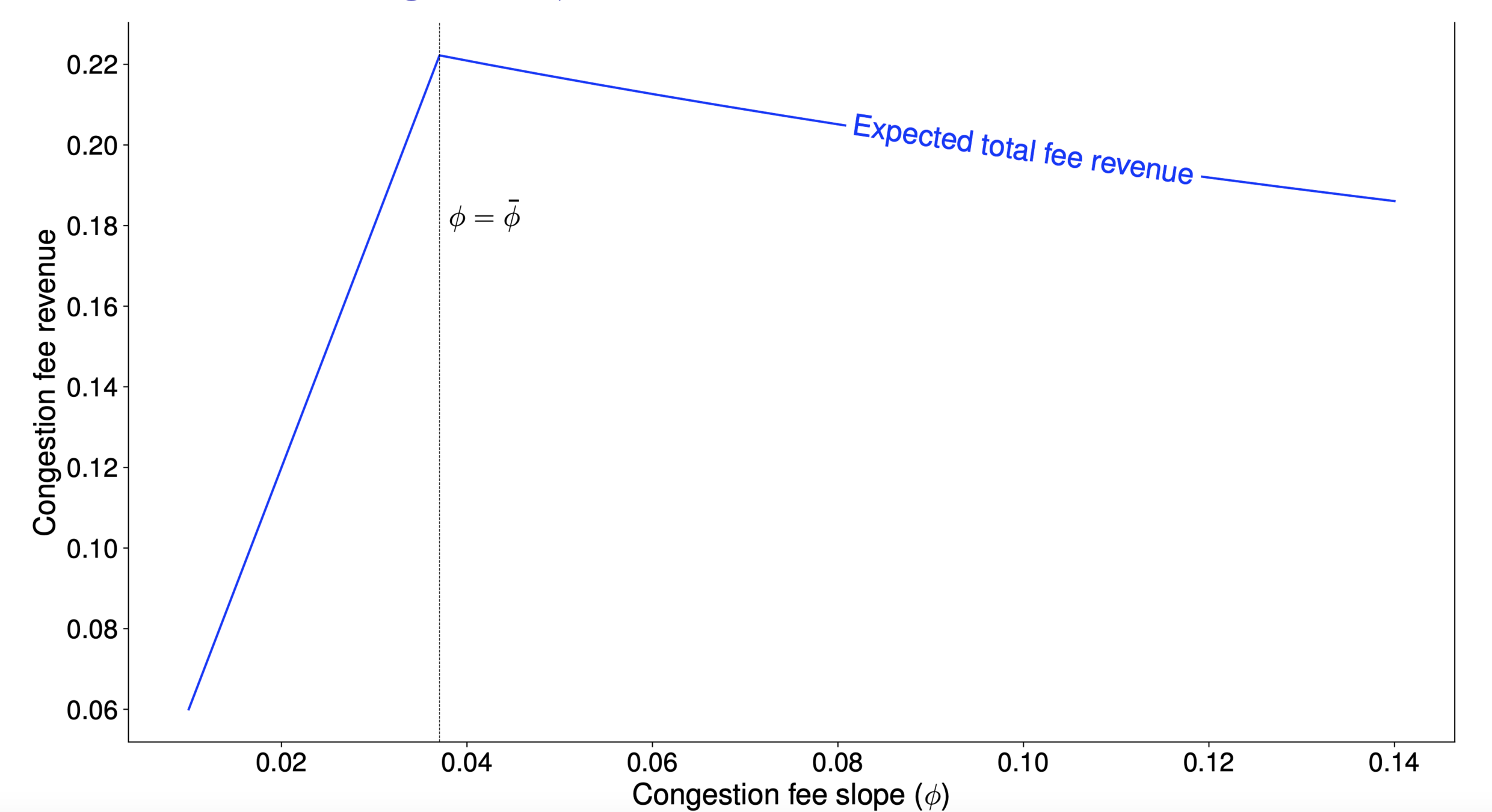

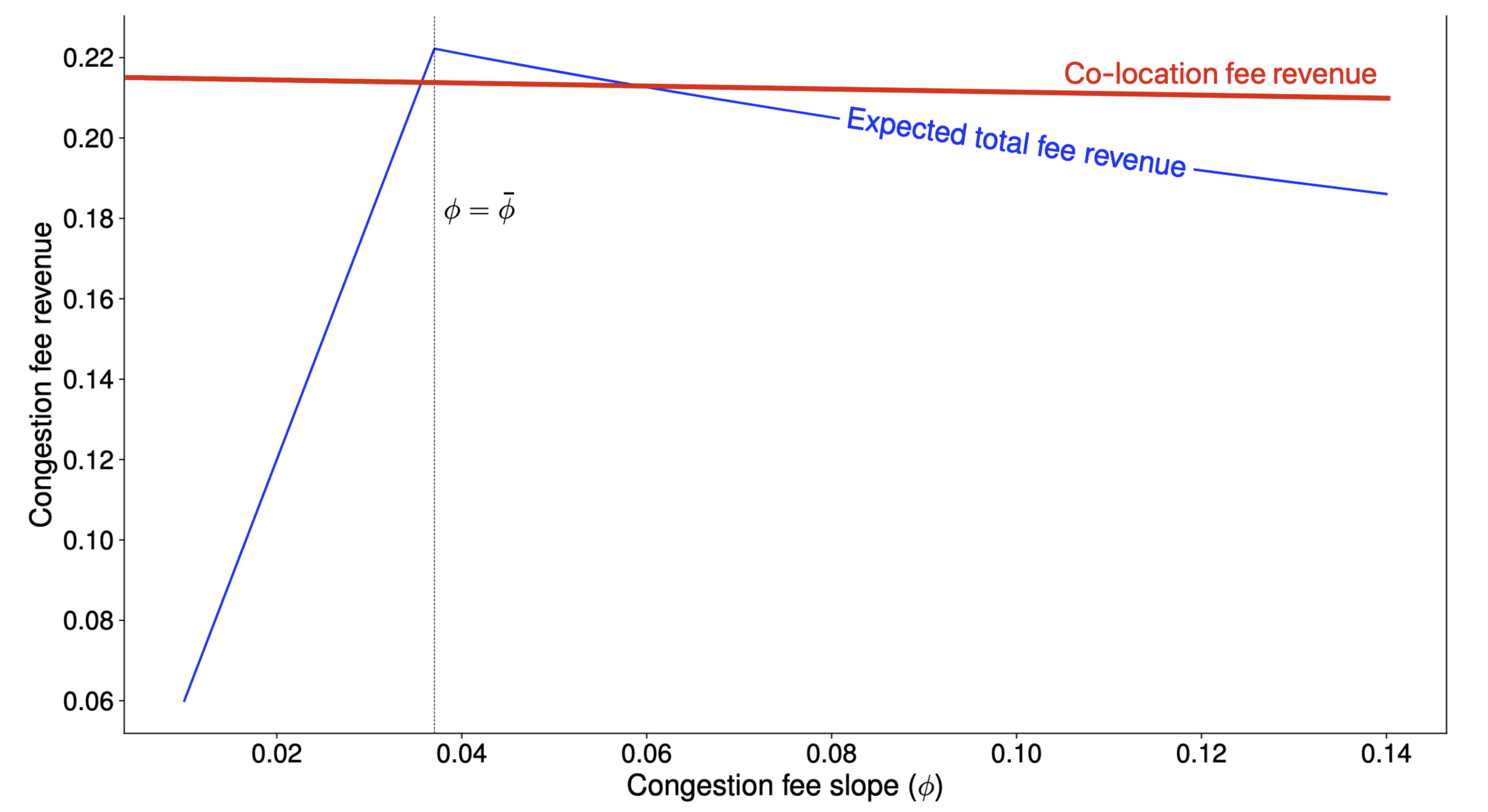

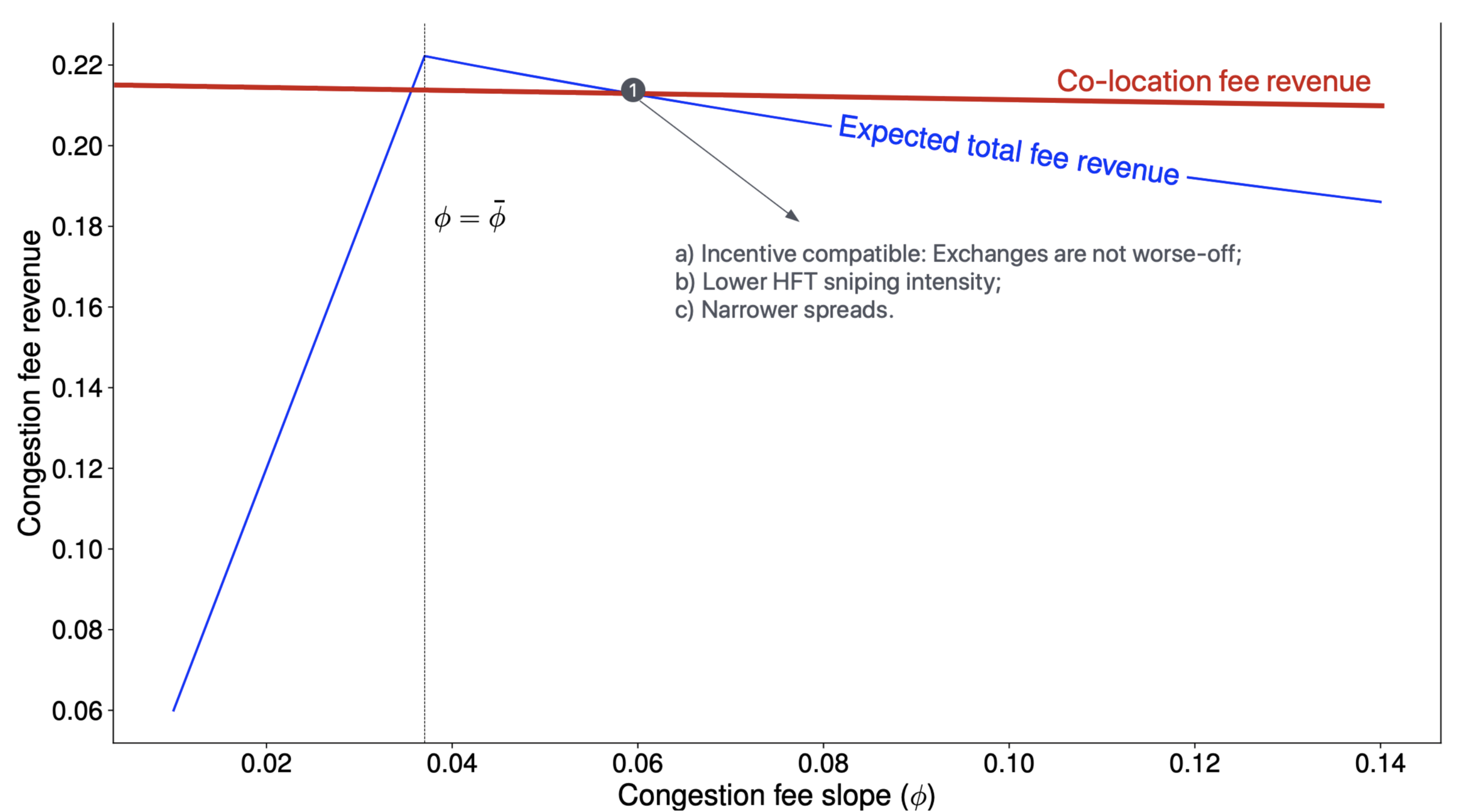

What about fee revenues?

By Marius Zoican

FMA conference presentation on October 22, 2020.