Marius Zoican PRO

I am an Associate Professor of Finance and Canada Research Chair in Financial Technology at the University of Calgary’s Haskayne School of Business. My research sits at the intersection of technology and finance.

Michael Brolley

Marius Zoican

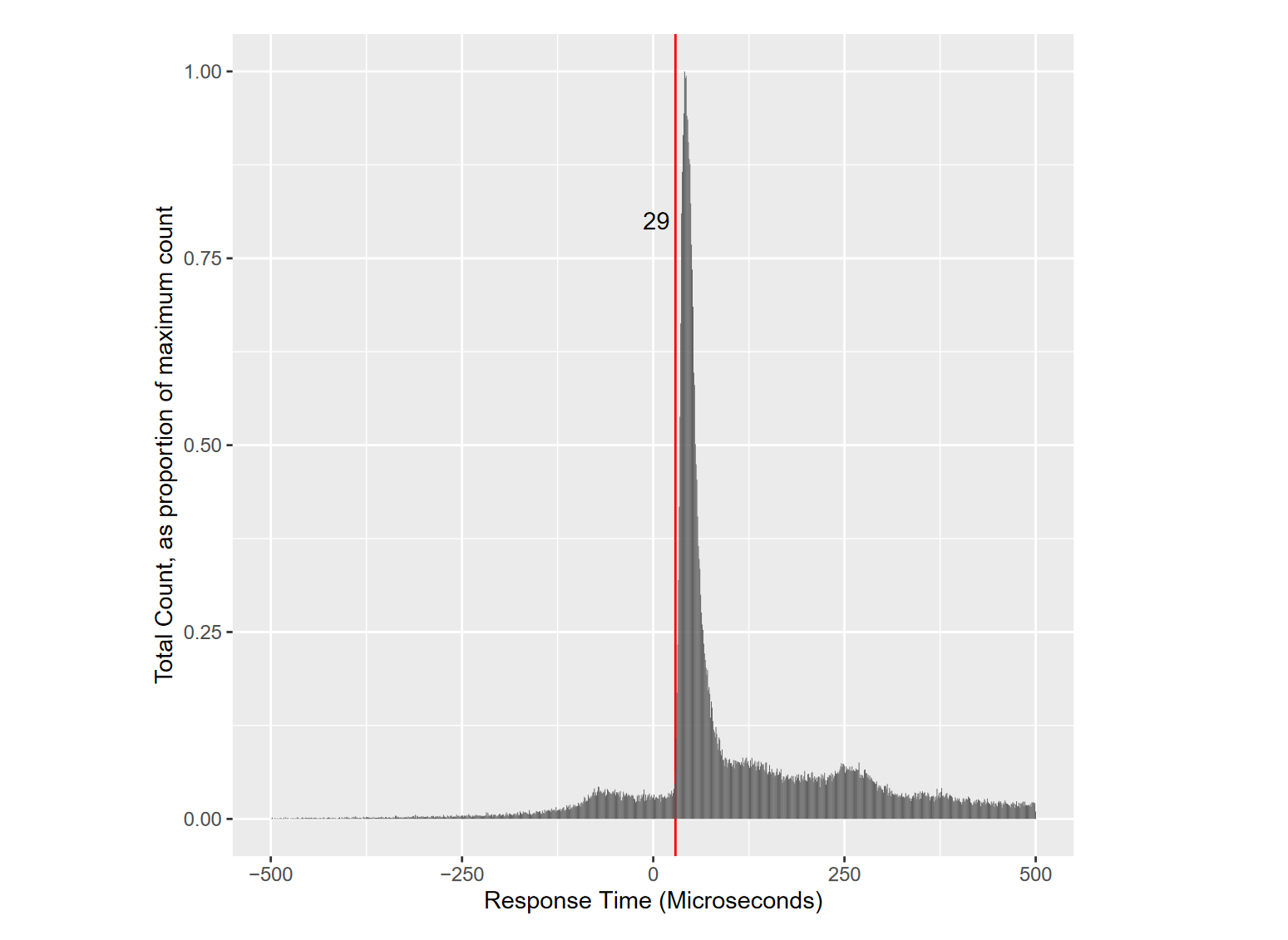

U.K.-based evidence (Aquilina, Budish, O'Neill, 2020) shows that latency arbitrage races are:

| Speed bumps | Batch auctions | |

|---|---|---|

| Liquidity | 😃😃 | 😃😃 |

| Exchange revenue | 😞 | 😞😞 |

| Implementation difficulty | 😐 | 😞😞 |

| Regulatory challenges | 😐 | 😞 |

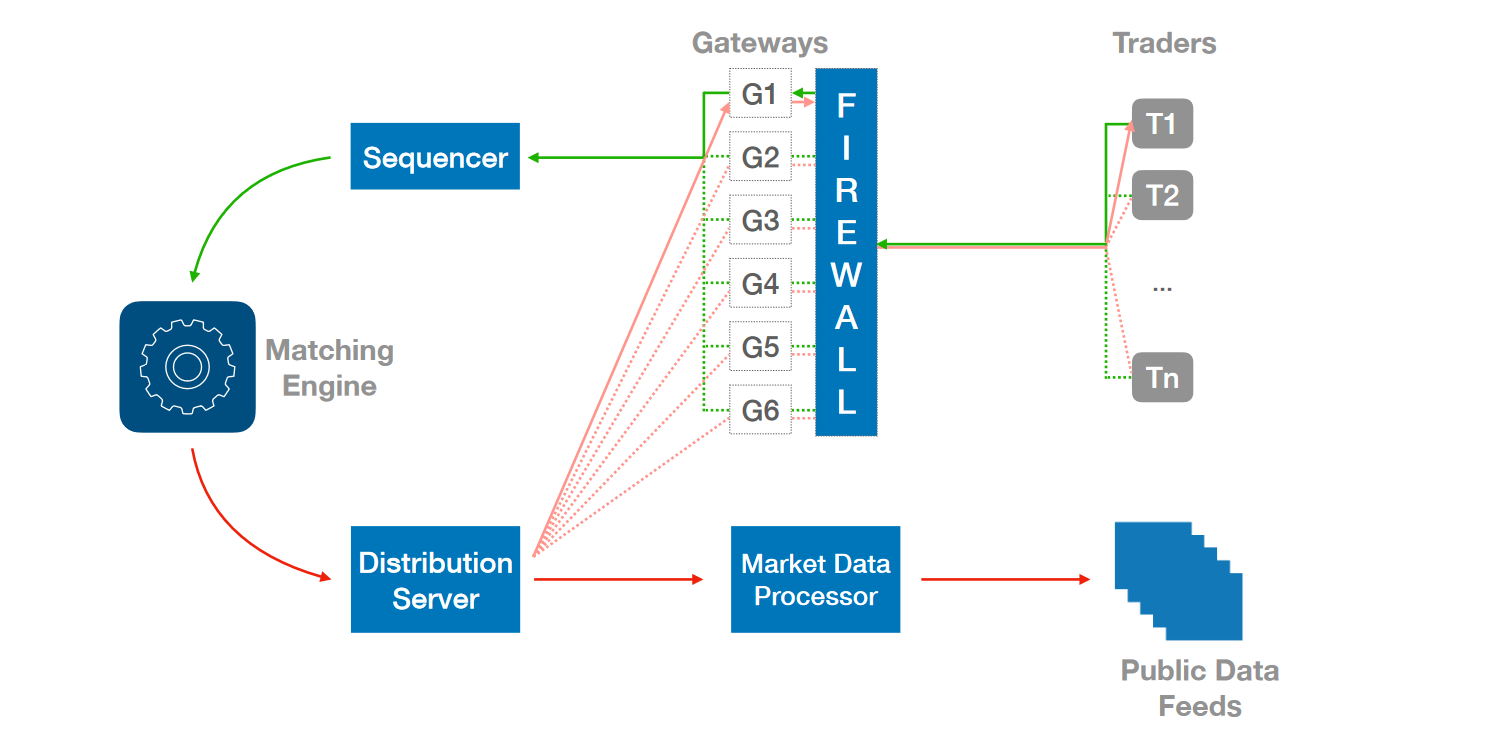

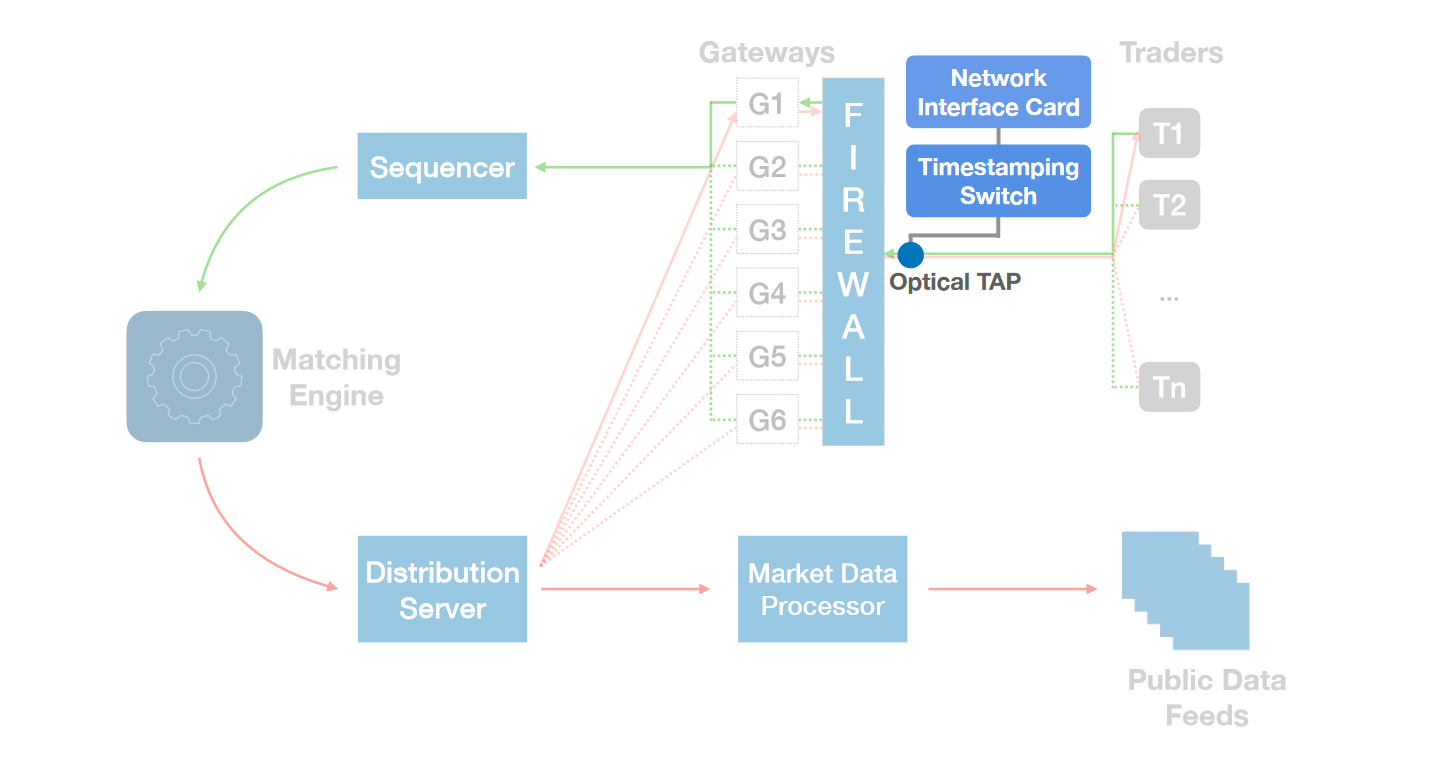

Two parameters:

M1 and M2 arrive at same time if:

M2 Inbound < M1 Inbound + AEL + MRT

Two important outcomes:

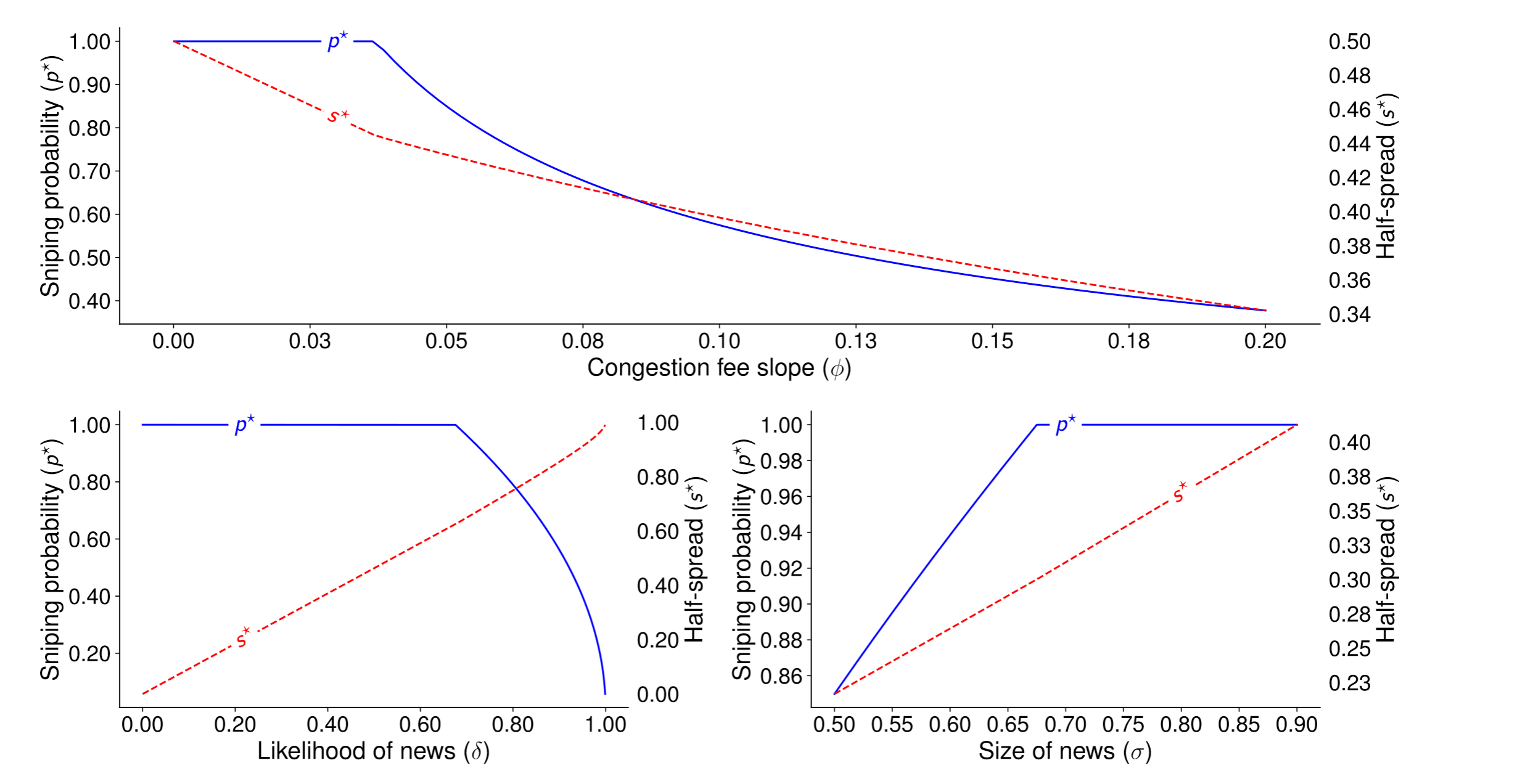

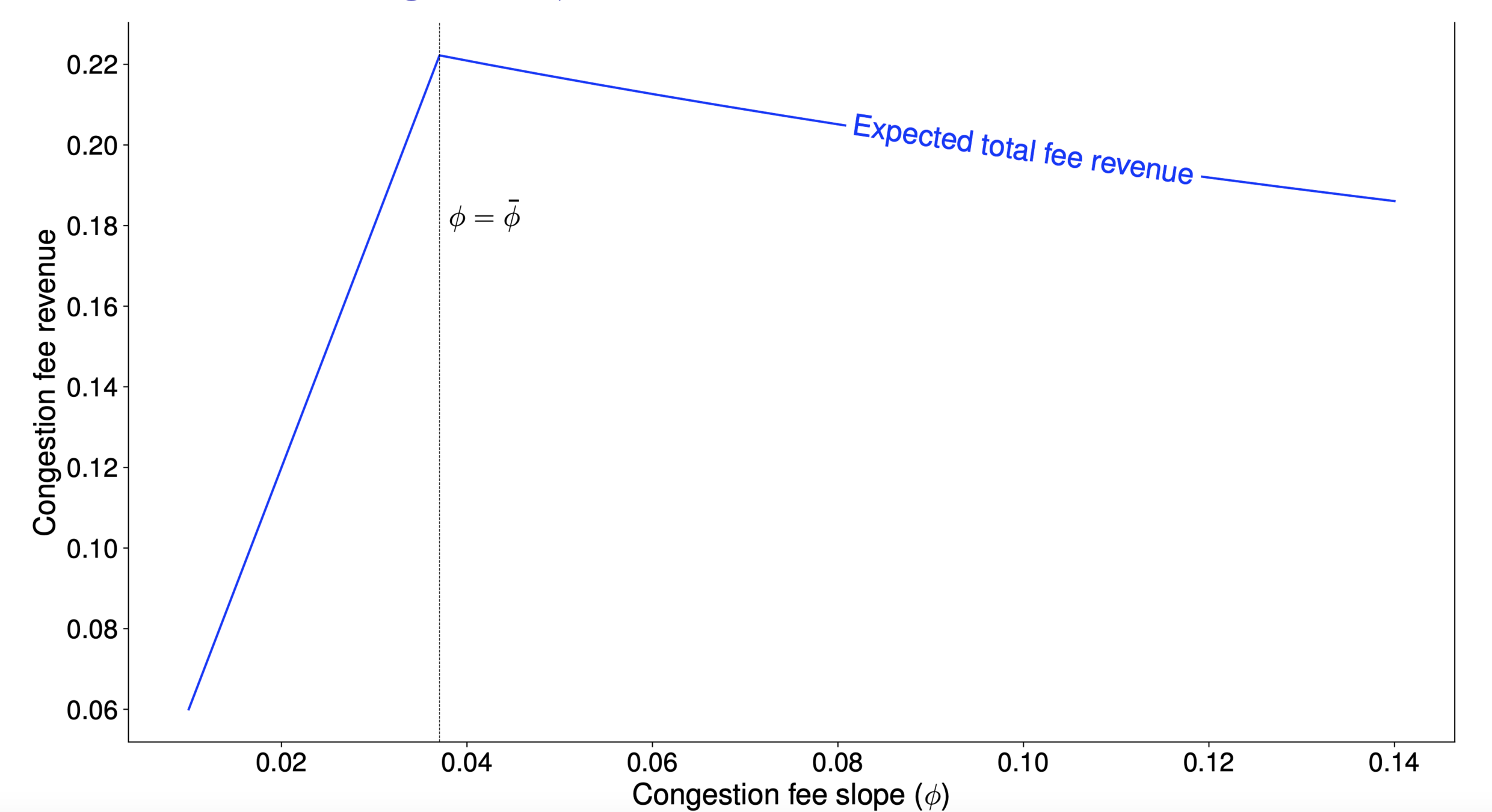

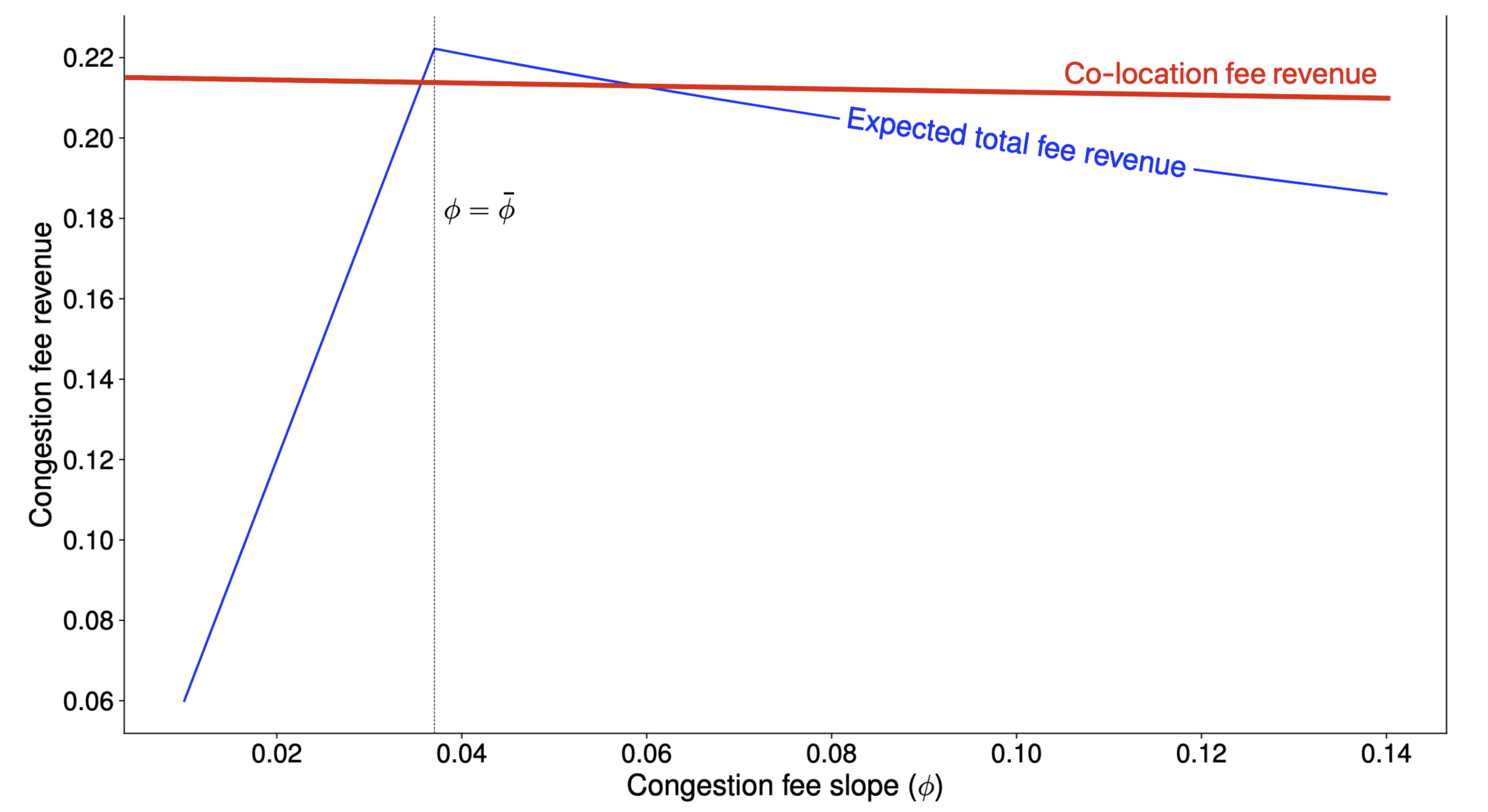

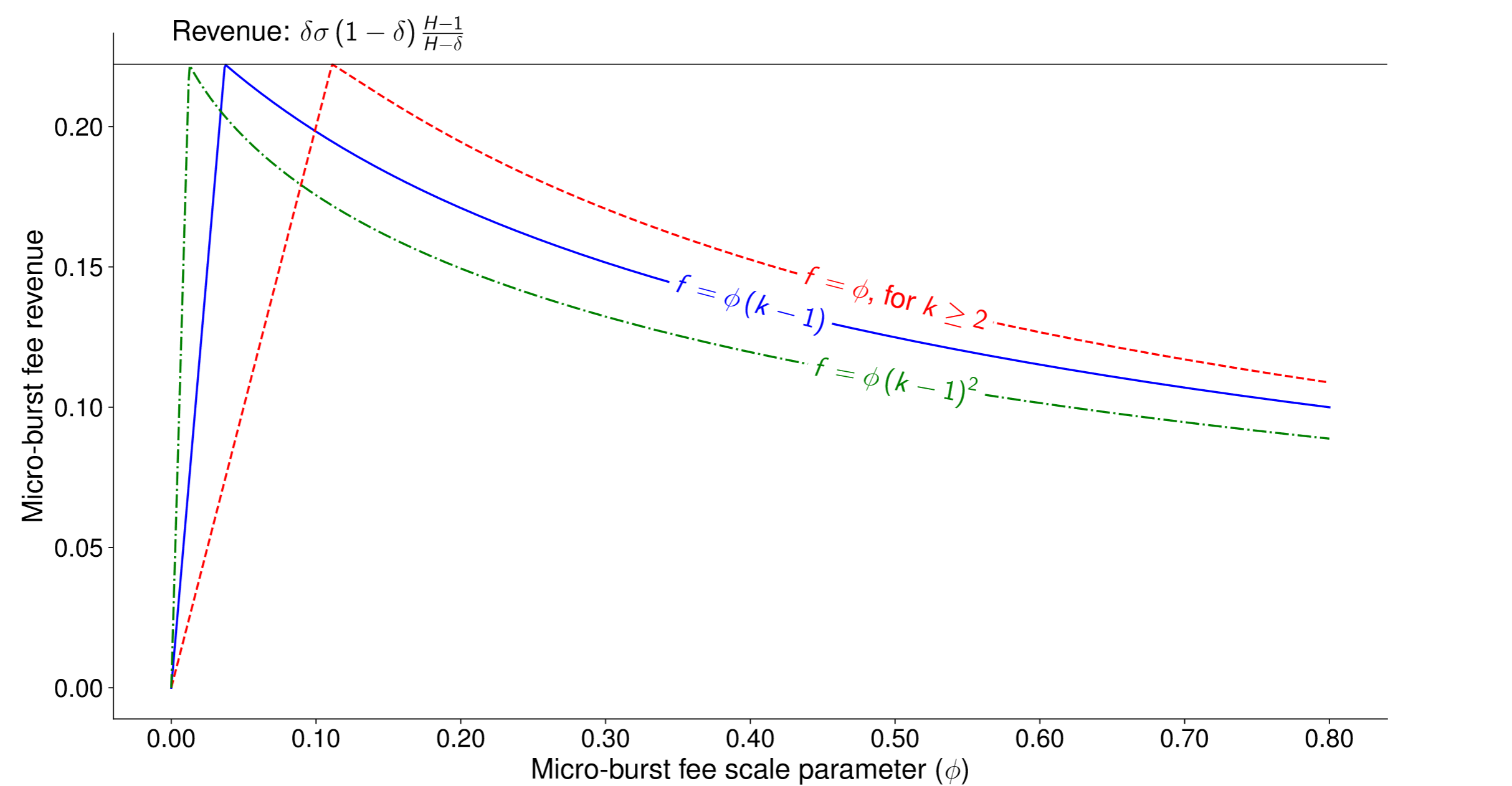

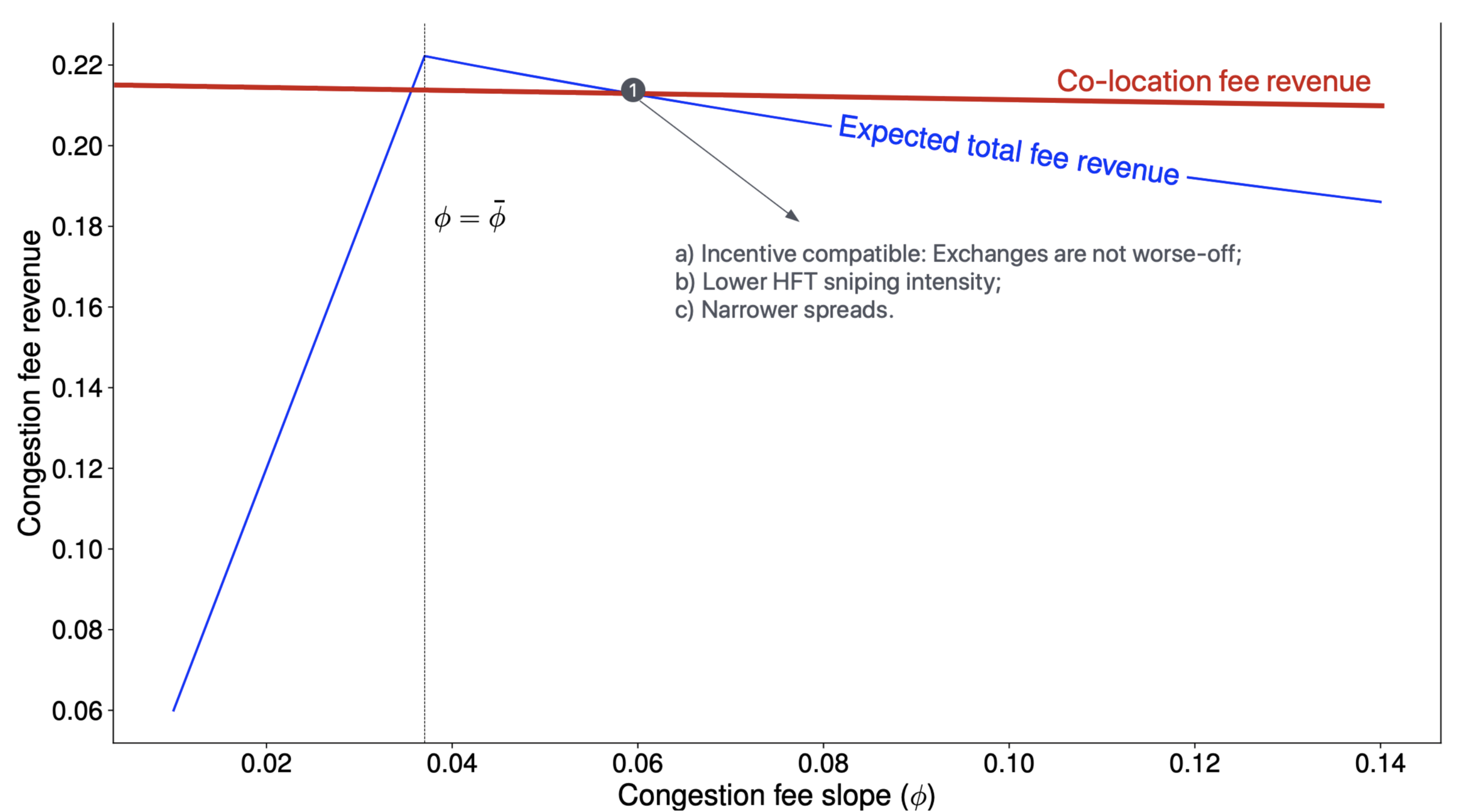

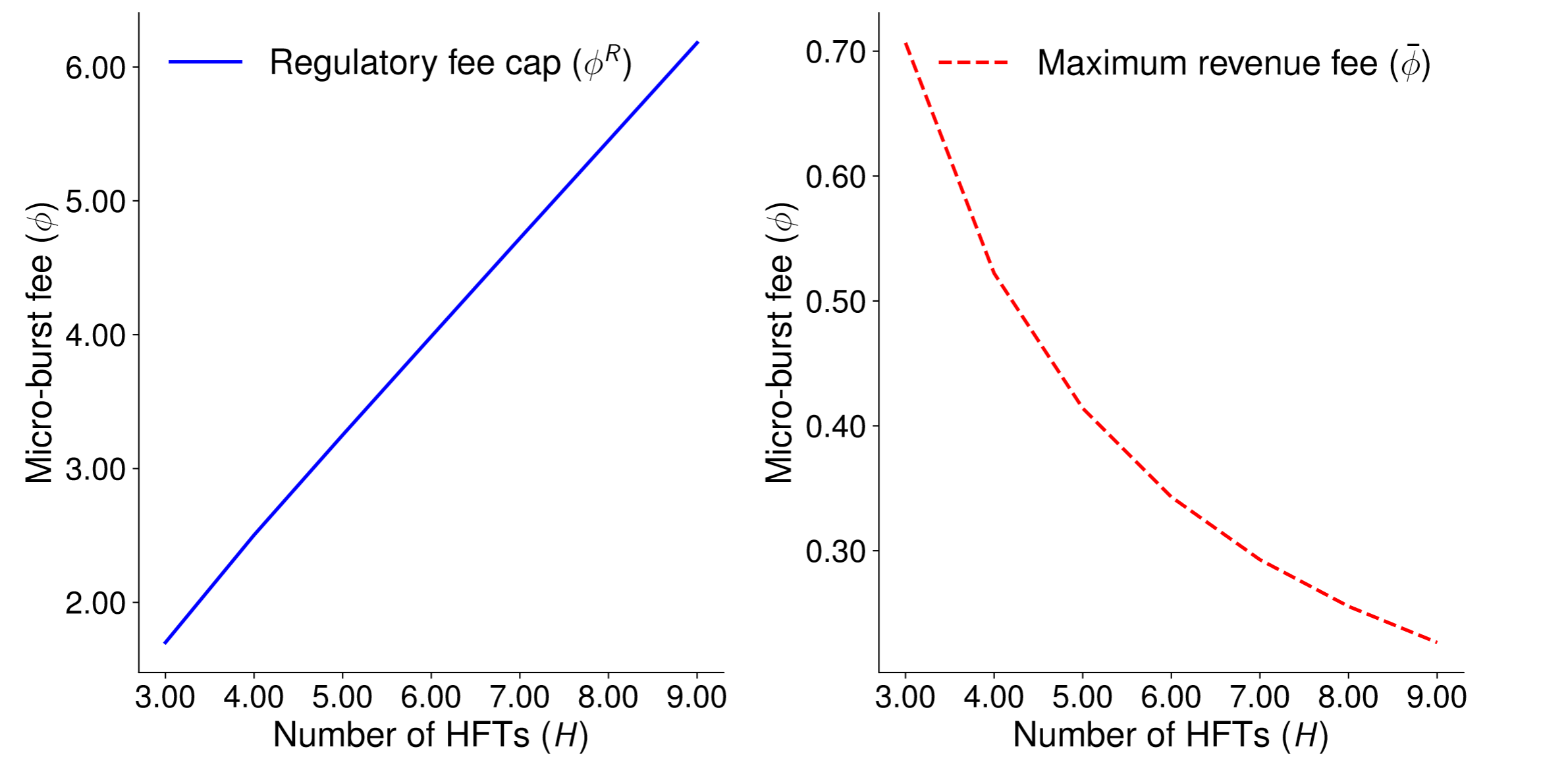

How does the fee magnitude impact revenues?

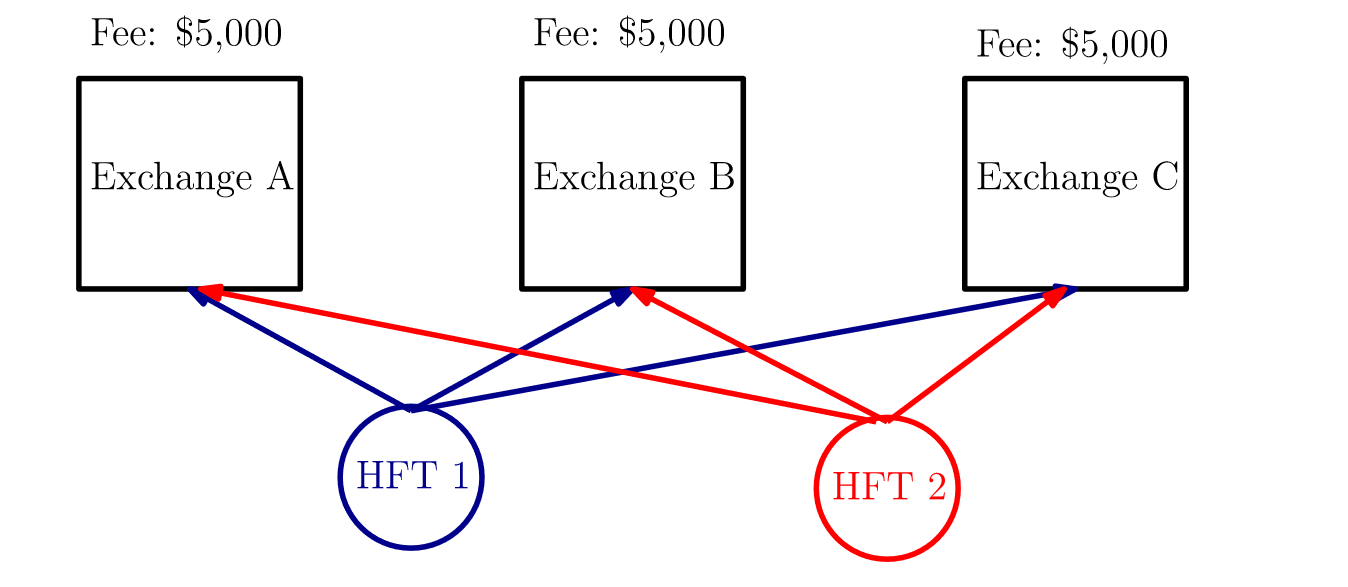

Co-location fees do not scale with trading activity and

they need to be paid in advance on all exchanges.

We calibrate caps on a constant fee structure:

| Speed bumps | Batch auctions | Micro-burst fees | |

|---|---|---|---|

| Liquidity | 😃😃 | 😃😃 | 😃 |

| Exchange revenue | 😞 | 😞😞 | 😃 |

| Implementation diff. | 😐 | 😞😞 | 😐/😃 |

| Regulatory hurdle | 😐 | 😞 | 😐/😃 |

By Marius Zoican

TMX Group presentation on May 19, 2021