“Uncertainty is an uncomfortable position.

- Voltaire

But certainty is an absurd one."

TMQR Exotic Beta and Commoditized Alpha Projects

Exotic Beta

TMQR has experience creating and managing exotic beta mandates featuring :

- risk limited single or multi commodity exposures.

- short volatility single or multi commodity exposures.

- yield enhancement / market neutral single and multi commodity exposures.

Exotic Beta

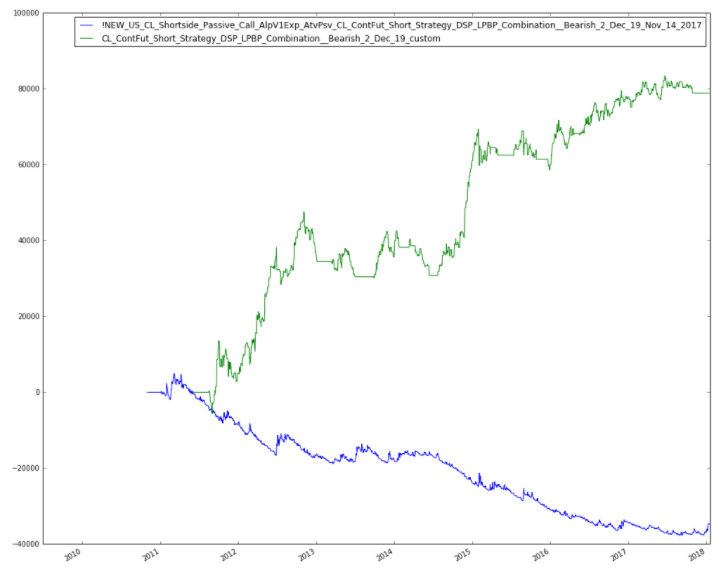

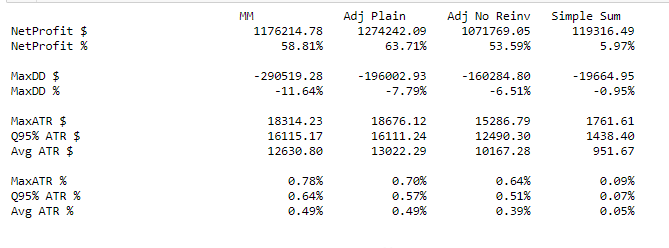

An example project specified 50% short and 50 % long crude oil to a bidirectional view of WTI. The final specification was that the exposure be risk limited at all times.

- Require a set of long alpha and short alphas.

- Predominantly a trend following strategy with some elements of yield enhancement plus a cap and floor on exposure.

task :

- construct a basket of long only WTI futures.

- construct a basket of short only WTI futures.

- devise a risk limited strategy to dampen trend following return stream.

- define a risk target/budget.

- Demo the proposed strategy.

Frame the solution:

What are we working with?

Quant Strategy development workflow :

- Data acquisition, data management and distribution.

- Strategy dev(alpha), testing, deployment and monitoring.

- Portfolio Management, risk targeting.

- Automated or semi-automated trade execution.

- Back office trade capture, reconciliation and return reporting.

The TMQR value proposition ...

- A pre existing set of institutional quality quant tools and deeply experienced personnel

aimed at reducing project risk,

speeding the development time,

and reduce the startup costs of rules based trading, investment and hedging systems.

TMQR Technology Services brings an expert team with ...

- Deep experience in quantitative risk management and trading strategy design and deployment.

- Data management solutions to meet the needs of, investment advisers, hedgers, fund sponsors or proprietary trading groups.

- Automated and semi-automated trade execution across asset classes.

Back to the Crude Oil mandate...

task :

- construct a basket of long only WTI,

make it risk limited with a dynamic risk reversal.

Back to the Crude Oil mandate...

task :

- construct a basket of short only WTI futures.

make it risk limited with a dynamic risk reversal.

- Require a set of long alpha and short alphas.

- Predominantly a trend following strategy with some elements of yield enhancement plus a cap and floor on exposure.

task :

- define a risk target/budget.

- Demo the proposed strategy.

Frame the solution:

- define a risk target/budget.

- Demo the proposed strategy.

Frame the solution:

The Birth of the McNugget

In the early 80's McDs wanted to offer a chicken based product but were concerned that rising chicken prices would force a choice between rising menu prices and squeezed margins .

There was no existing way to hedge chicken but chicken, from a financial point of view, is a combination of corn and soymeal since those are the feed ingredients of the chick.

The Birth of the McNugget

Both corn and soymeal are liquid, exchange traded derivatives products. So a consultant to McD's who specialized in risk consulting and concentrated on actively trading commodities, currencies and other markets suggested ....

the use of a synthetic future composed of corn and soymeal that would effectively hedge the producers exposure to price fluctations allowing them to quote a fixed price to McD's .

The synthetic future in the case above is what we call an EXO.

TMQR has been a pioneer in development of EXOs to solve risk challanges with a special concentration on exchange traded options

- EXOs or Exotic Beta indexes represent an exposure in a particular market. The index can be designed to be long, short or neutral..

- EXOs have been used create specialized benchmarks of unique mandates.

- “Commoditized Alphas” are a special class of active indexes designed to replicate a particular trading style.

Some example trading styles we have "commoditized" include

- momentum,

- mean reversion,

- seasonality or

- volatility harvesting.

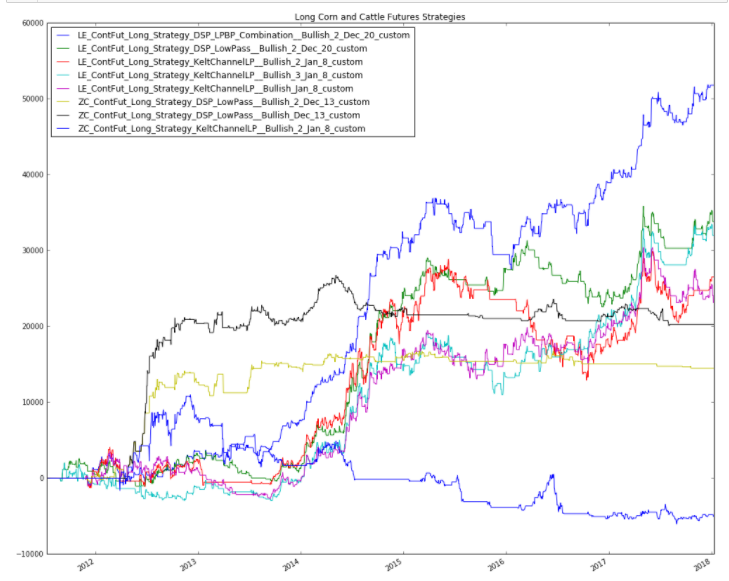

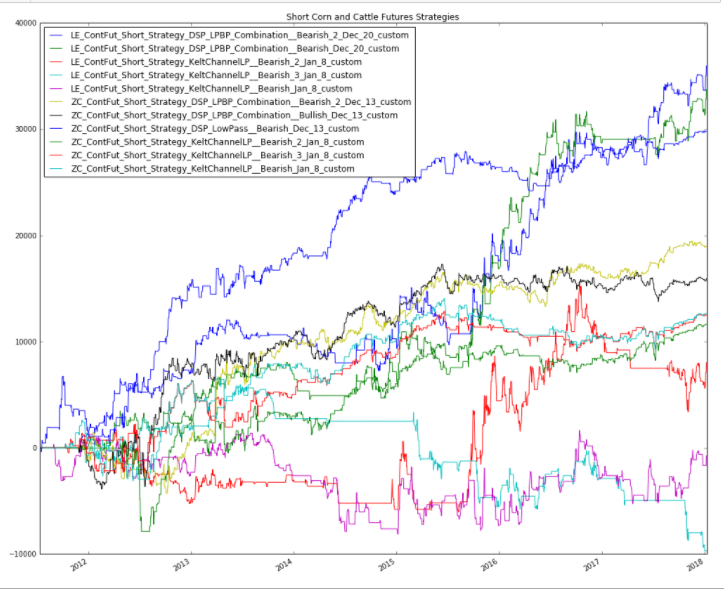

An EXO for the Cattle crush...

For the purpose of this illustration we have created two types of indexes:

- a style index that represents the trading behavior of a large number of traders engaged in long only trend following style and a separate style index representing the behavior of short only trend following. The collection of "traders" is used to create a select group which represent the style. Periodically different members get included or excluded according to their performance.

- a style index representing a passive exposure to a short straddle which is paired with the trend following style above to express yield enhancement through premium collection.

What are we working with?

- Require a complimentary strategy or a replication strategy for a cattle crush exposure.

- Predominantly a trend following strategy with some elements of yield enhancement.

task :

- construct a basket of long only cattle and corn futures.

- construct a basket of short only cattle and corn futures.

- devise a yield enhancement strategy to dampen trend following return stream.

- define a risk target/budget.

- Demo the proposed strategy.

Frame the solution:

1. construct a basket of long only cattle and corn futures.

2 . construct a basket of short only cattle and corn futures.

3. devise a yield enhancement strategy to dampen trend following return stream.

- enhance long strategies with short ATM calls, short OTM puts.

- a new EXO was created to express a premium collection position which will be paired with a long futures signal. If a long strategy engages the following options position is deployed. If the long signal exits the following position is exited.

- the tail risk is hedged with deep OTM puts.

3. devise a yield enhancement strategy to dampen trend following return stream. (short side)

- enhance short strategies with short ATM puts, short OTM calls.

- a new EXO was created to express a premium collection position which will be paired with a short futures signal. If a short strategy engages the following options position is deployed. If the short signal exits the following position is exited.

- the tail risk is hedged with deep OTM calls.

task :

Define a risk target/budget.

Demo the proposed strategy.

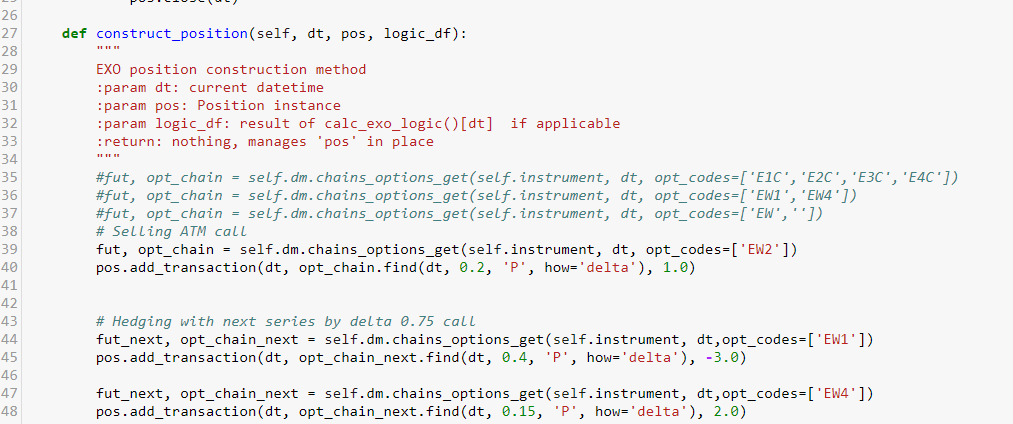

https://10.0.1.2:8888/notebooks/smart_campaign_generation/Top%20Select%20dashboards/LE_ZC_SmartCampaign_V5_YieldEnhance_Concept_Top_select_V5_Jan_8.ipynb

https://10.0.1.2:8888/notebooks/smart_campaign_generation/Top%20Select%20dashboards/LE_ZC_SmartCampaign_V5_Futures_Only_Concept_Top_select_V5_Jan_8.ipynb

Exotic Beta

An example project where the object was to build infrastructure to exploit the weekly options available on the S&P 500 Emini to express premium collection, short vol, long vol or another option based strategy using weekly options..

- Require database of available weekly and monthly S&P options.

- functionality to quickly explore different exposures and assess the potential edge in the position.

task :

- construct a MongoDB of available options.

- construct a tool to express different positions.

- Pair options strategy with outright futures.

- define a risk target/budget.

- Demo the proposed strategy.

Frame the solution:

- Require database of available weekly and monthly S&P options.

- functionality to quickly explore different exposures and assess the potential edge in the position.

task :

- construct a MongoDB of available options.

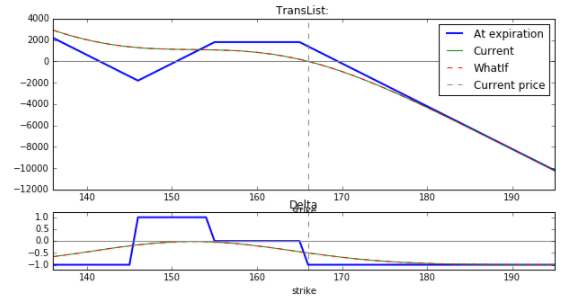

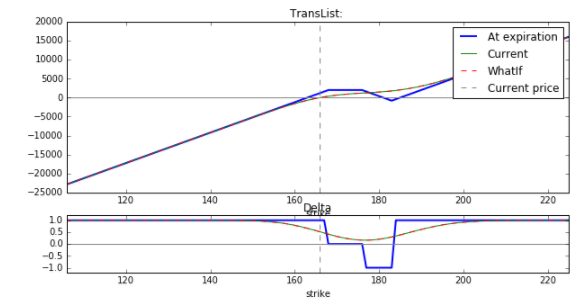

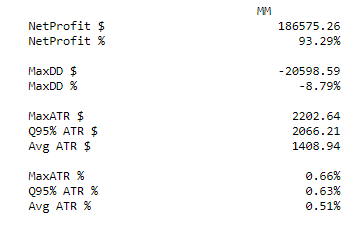

- construct a tool to express different positions. Discover some edge...

Frame the solution:

task :

- construct a MongoDB of available options.

- construct a tool to express different positions. Discover some edge...

Frame the solution:

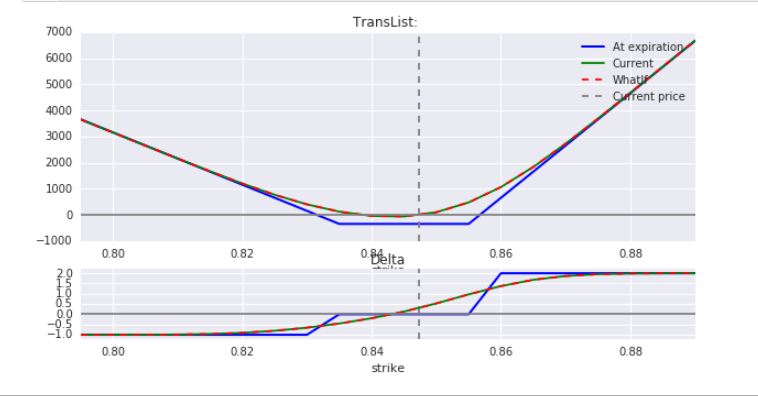

- construct a tool to express different positions. Discover some edge... An inexpensive hedge for long S&P positions.

Frame the solution:

TMQR Key contact

Mr. Nikolas Joyce, head of research and trading, has twenty years experience trading financial markets and has worked as an associated person, registered investment advisor and Portfolio Manager for firms in both the futures and securities industry.

Mr. Joyce :

- co-managed funds in excess of $350,000,000 in equities.

- has for more than 10 years been an NFA member registered with the CFTC as a principal and registered CTA.

- holds a degree in Finance from the University of British Columbia - School of Commerce.

- As well as being a principal and director of Trend Management Limited.

najoyce@tml1.com

Copy of TMQR portfolio mandates

By nikolasjoyce

Copy of TMQR portfolio mandates

TMQR overview