“Uncertainty is an uncomfortable position.

- Voltaire

But certainty is an absurd one."

TMQR

Commoditized Alpha and

Exotic Beta

TMQR has been a pioneer in development of EXOs to solve risk challanges with a special concentration on exchange traded options

- EXOs or Exotic Beta indexes represent an exposure in a particular market. The index can be designed to be long, short or neutral..

- EXOs have been used create specialized benchmarks of unique mandates.

- “Commoditized Alphas” are a special class of active indexes designed to replicate a particular trading style.

Some example trading styles we have "commoditized" include

- momentum,

- mean reversion,

- seasonality or

- volatility harvesting.

Commoditized Alpha

The Commoditized Alpha concept is an attempt to solve some of the inherent constraints in manager selection and strategy calibration.

- define the manager or trader process you would like to access.

- identify the algorithm that expresses the manager or trader process ( trend, following, mean reversion, seasonality, vol harvesting etc.

- create a swarm of simulated traders following the defined strategy through hyper parameterization.

- select from swarm respecting the principles of walk forward efficiency and momentum.

- re-balance periodically to maintain exposure to high momentum swarm members.

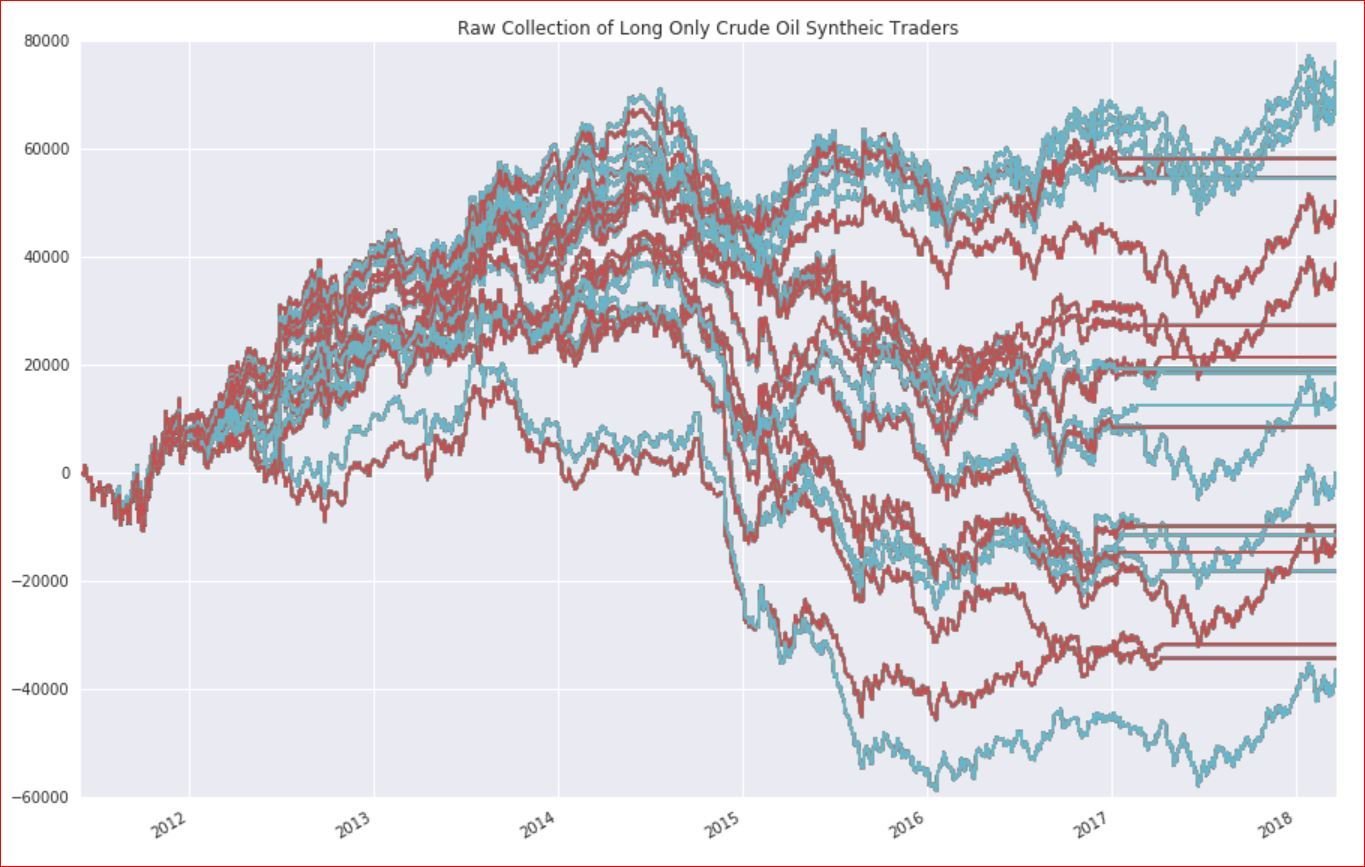

Sample Trend Following Swarm on Crude Oil

Sample Long Only Trend Following Commoditized Alpha on Crude Oil

Exotic Beta

Commoditized Alpha Indexes :

- can switch composition without manager lock ups, lowering cost and potentially improving performance.

- internalize manager selection in an effort to reduce the cost of due diligence.

- only hold representative swarm members when the style displays momentum.

- yield enhancement / market neutral single and multi commodity exposures.

Connection to the leveraged and inverse ETF Space... using the following components.

- dedicated long only commoditized alpha indexes with EXO bullish risk reversal overlay.

- plus

- dedicated short only commoditized alpha indexes EXO bearish risk reversal overlay.

- plus

- static outright futures/outright exposure.

We have a framework to offer high conviction risk limited leveraged and inverse exposures to single commodities, currencies, indexes and interest rate markets.

- Require a set of long alpha and short Commoditized Alpha Indexes.

- Predominantly a trend following strategy with some elements of yield enhancement plus a cap and floor on exposure.

task :

- construct a basket of long only WTI futures.

- construct a basket of short only WTI futures.

- devise a risk limited strategy to dampen trend following return stream.

- define a risk target/budget.

- Demo the proposed strategy.

Frame the solution:

TMQR brings an expert team with...

- Deep experience in quantitative risk management and trading strategy design and deployment.

- Data management solutions to meet the needs of investment advisers, hedgers, fund sponsors or proprietary trading groups.

- Automated and semi-automated trade execution across asset classes.

Back to the Crude Oil mandate...

task :

- construct a Long only Commoditized Alpha Index.

- Overlay a dynamic put index which targets a -5% to -15% delta to engineer a more asymmetric payoff profile.

Back to the Crude Oil mandate...Long Commoditized Alpha and Put overlay

Back to the Crude Oil mandate...

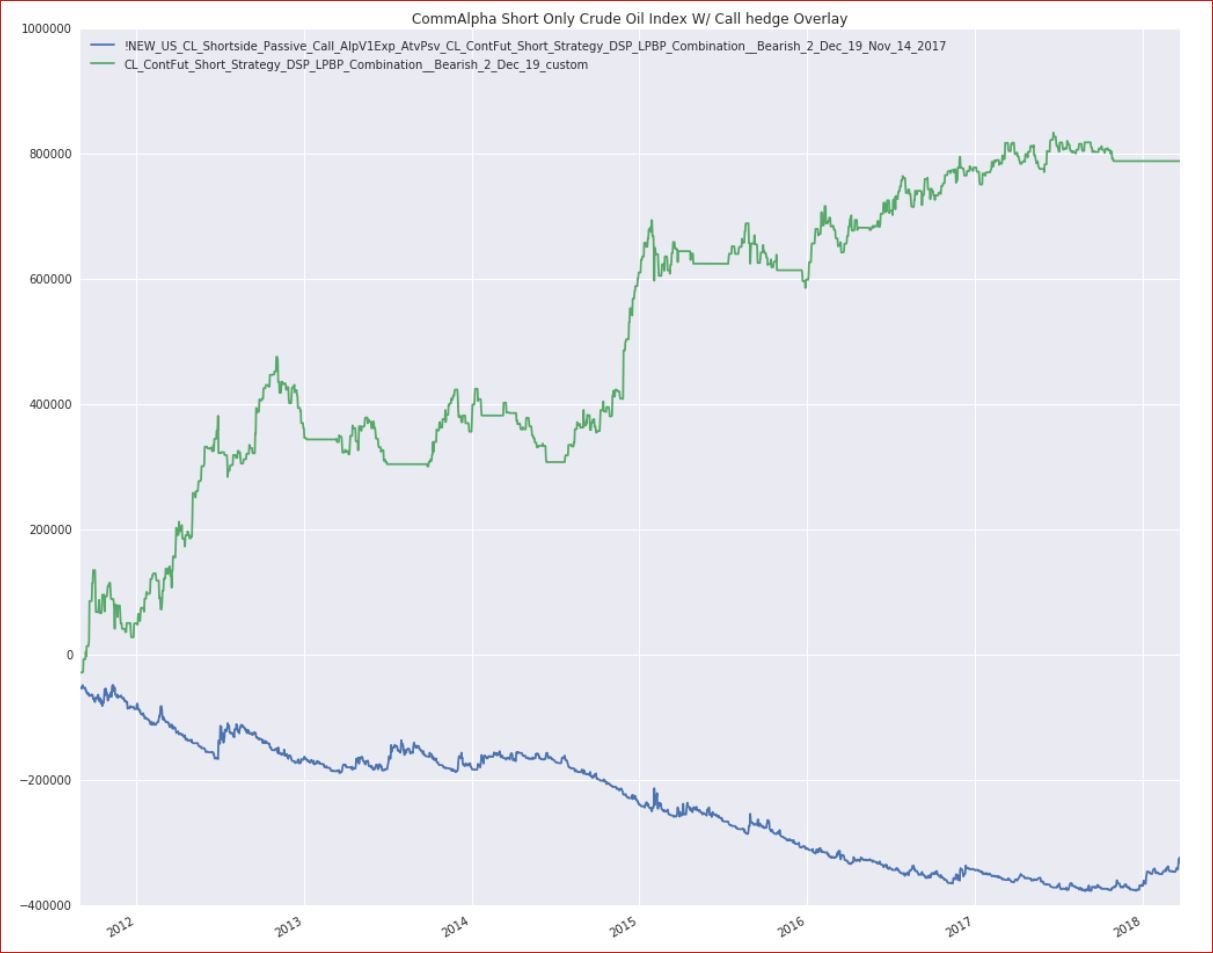

task :

- construct a Short only Commoditized Alpha Index.

- Overlay a dynamic call index which targets a 5% to 15% delta to engineer a more asymmetric payoff profile.

Back to the Crude Oil mandate...Short Commoditized Alpha and Call overlay

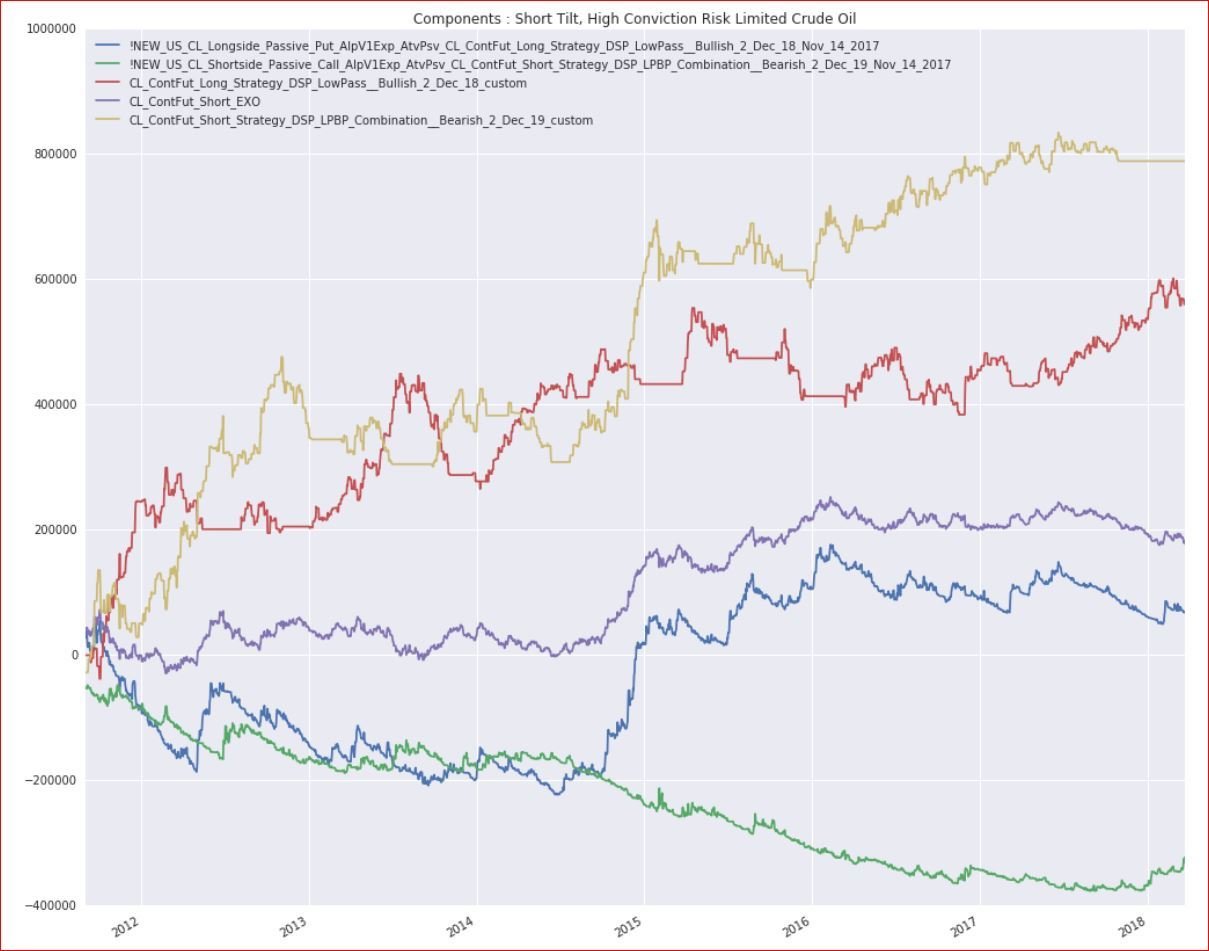

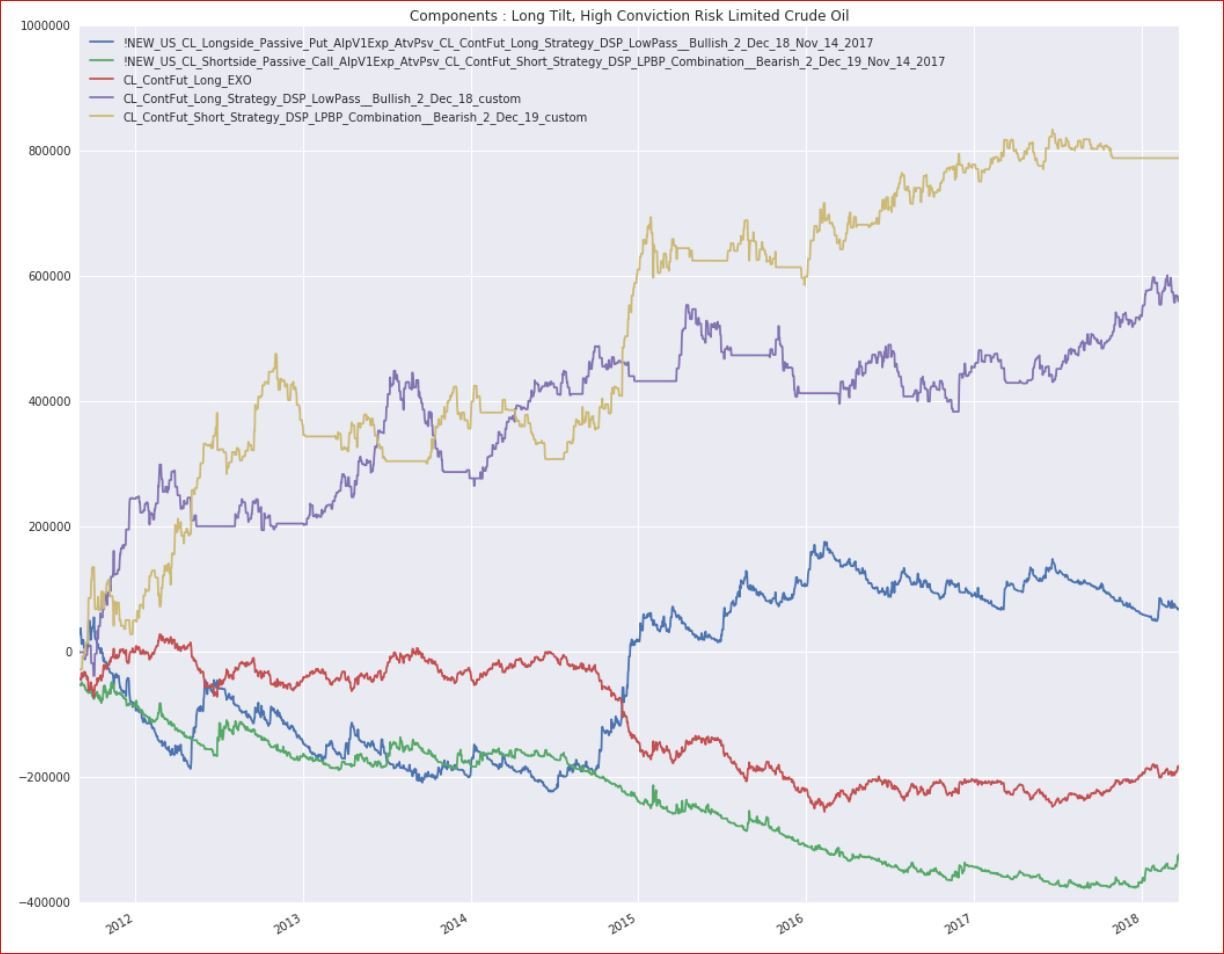

Back to the Crude Oil mandate...

task :

- When we add the 3 components together we get a high conviction risk limited exposure .

- The strength of the conviction can be controlled by the weighting or sizing of the static futures/ outright position.

- In the course of the last example we used 10 units of Long Alpha, 10 units of Short Alpha and 3 units of static futures.

Back to the Crude Oil mandate... Short Conviction Components

Back to the Crude Oil mandate... Long Conviction Components

Back to the Crude Oil mandate... Long and Short Conviction Compared

Other Product mandates... Gold Long and Short High Conviction Compared

Other Product mandates... US Interest Rates Long and Short High Conviction Compared

The High Conviction Risk Limited opportunity set for ETF sponsors

The process outlined for the previous Crude Oil example can be adapted to any products where there are liquid future/ equities and options available.

Commoditized Alpha can be adapted to accommodate any quantifiable investing style whether fundamental, technical, quantitative or discreationary.

Portfolios of high conviction risk limited exposures in different products could be constructed to focus risk exposures, exploit the non recourse leverage of options and deliver asymmetric return streams.

TMQR Key contact

Mr. Nikolas Joyce, head of research and trading, has twenty years experience trading financial markets and has worked as an associated person, registered investment advisor and Portfolio Manager for firms in both the futures and securities industry.

Mr. Joyce :

- co-managed funds in excess of $350,000,000 in equities.

- has for more than 10 years been an NFA member registered with the CFTC as a principal and registered CTA.

- holds a degree in Finance from the University of British Columbia - School of Commerce.

- As well as being a principal and director of Trend Management Limited.

najoyce@tml1.com

TMQR for Lev and Inverse ETFs

By nikolasjoyce

TMQR for Lev and Inverse ETFs

TMQR overview