Phase-Type Models in

Life Insurance

Dr Patrick J. Laub @ IME, München

Université Lyon 1

Motivating theory

Stochastic Models (2019), 34(4), 1-12.

Can read on https://arxiv.org/pdf/1803.00273.pdf

\tau

S_t

t

Guaranteed Minimum Death Benefit

S_\tau

\text{Payoff} = \max( S_{\tau}, K )

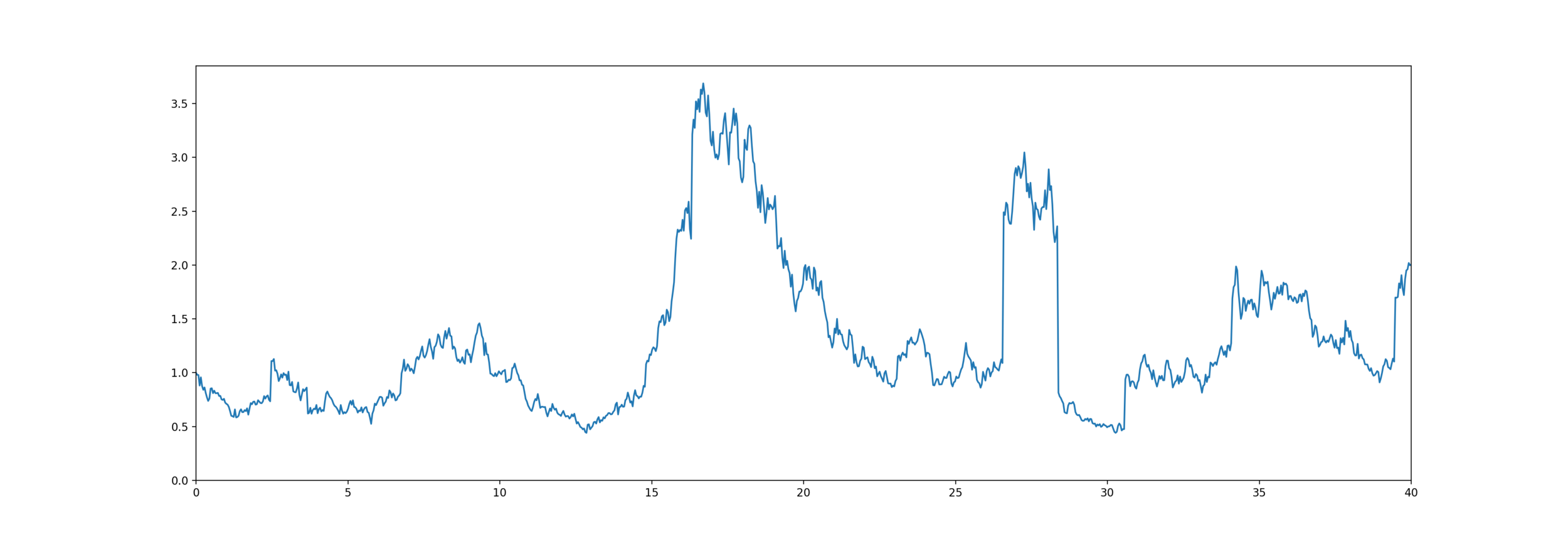

Equity-linked life insurance

\tau

t

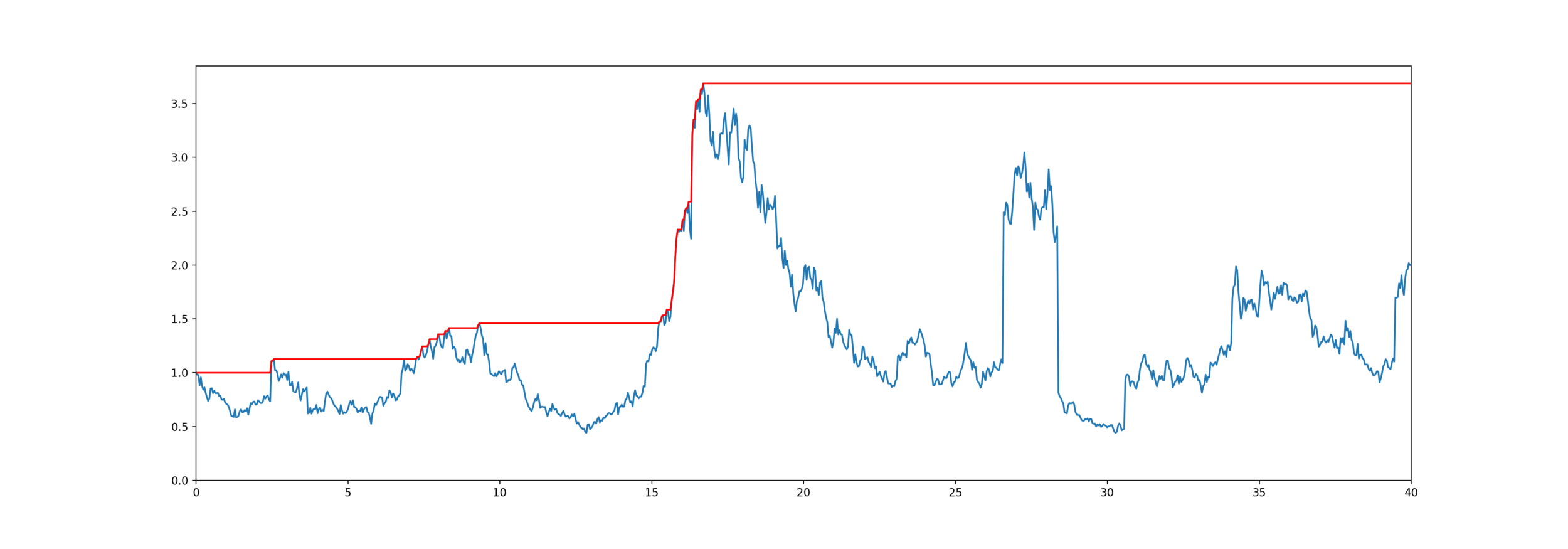

High Water Death Benefit

\text{Payoff} = \overline{S}_{\tau}

Equity-linked life insurance

\overline{S}_\tau

\overline{S}_t = \max_{s \le t} S_s

Model for mortality and equity

The customer lives for years,

\tau

\tau \sim \text{PhaseType}(\boldsymbol{\alpha}, \boldsymbol{T})

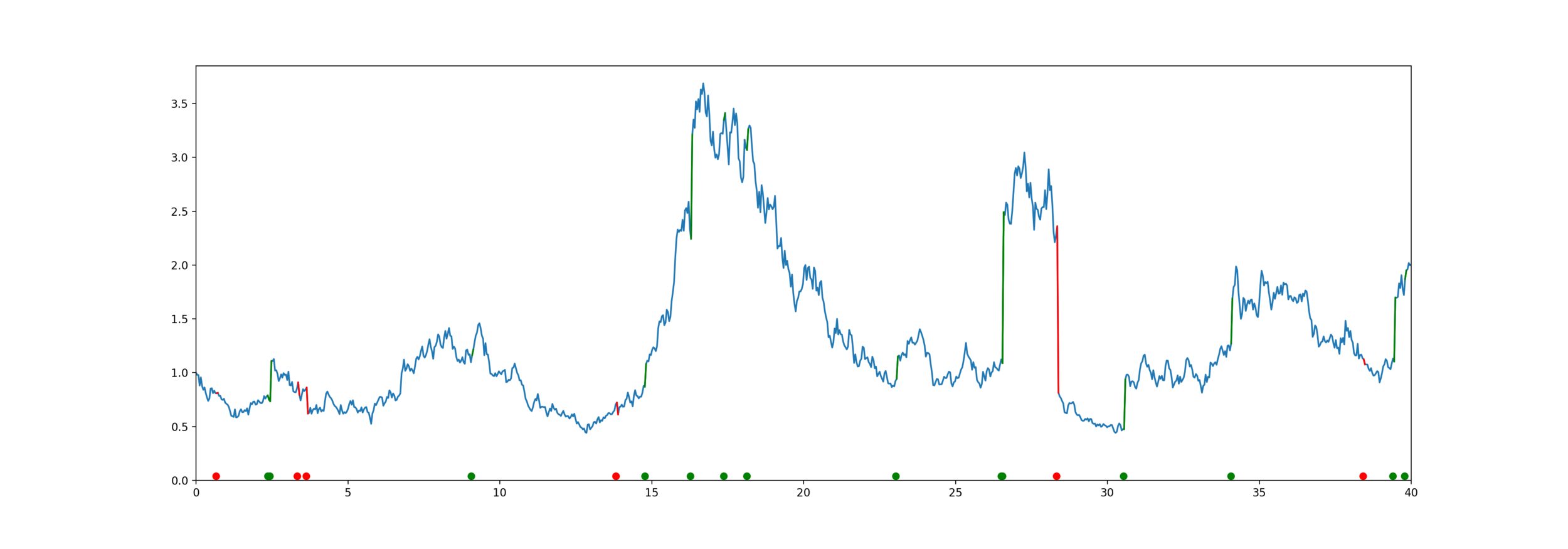

X_t \sim \text{Jump Diffusion}

S_t = S_0 \mathrm{e}^{X_t}

Equity is an exponential jump diffusion,

\text{Brownian Motion}(\mu, \sigma^2) + \text{Compound Poisson}(\lambda_1) + \text{Compound Poisson}(\lambda_2)

\text{Price} = \mathbb{E}[ \mathrm{e}^{-\delta \tau} \text{Payoff}( S_\tau, \overline{S}_\tau ) ]

S_t

t

Exponential PH-Jump Diffusion

\text{UpJumpSize}_i \overset{\mathrm{i.i.d.}}{\sim} \text{PhaseType}(\boldsymbol{\alpha}_1, \boldsymbol{T}_1)

\text{DownJumpSize}_i \overset{\mathrm{i.i.d.}}{\sim} \text{PhaseType}(\boldsymbol{\alpha}_2, \boldsymbol{T}_2)

\# \text{UpJumps}(0, t) \sim \mathrm{Poisson}(\lambda_1 t)

\# \text{DownJumps}(0, t) \sim \mathrm{Poisson}(\lambda_2 t)

Get some helpful matrices

\boldsymbol{U} = \boldsymbol{U}(\delta, \mu, \sigma^2, \boldsymbol{\alpha}, \boldsymbol{T}, \lambda_1, \boldsymbol{\alpha}_1, \boldsymbol{T}_1, \lambda_2, \boldsymbol{\alpha}_2, \boldsymbol{T}_2 )

\text{UpJumpSize}_i \overset{\mathrm{i.i.d.}}{\sim} \text{PhaseType}({ \color{red} \boldsymbol{\alpha}_1 }, { \color{red} \boldsymbol{T}_1 })

\text{DownJumpSize}_i \overset{\mathrm{i.i.d.}}{\sim} \text{PhaseType}( { \color{red} \boldsymbol{\alpha}_2 }, { \color{red} \boldsymbol{T}_2 })

\# \text{UpJumps}(0, t) \sim \mathrm{Poisson}({ \color{red} \lambda_1 } t)

\# \text{DownJumps}(0, t) \sim \mathrm{Poisson}({ \color{red} \lambda_2 } t)

\text{Brownian Motion}({ \color{red} \mu }, { \color{red} \sigma^2 })

\tau \sim \text{PhaseType}({ \color{red} \boldsymbol{\alpha} }, { \color{red} \boldsymbol{T} })

\text{Price} = \mathbb{E}[ \mathrm{e}^{-{\color{red} \delta} \tau} \text{Payoff}( S_\tau, \overline{S}_\tau ) ]

\boldsymbol{U}_{n+1} = f(\boldsymbol{U}_n)

Use fixed-point approximation

\boldsymbol{U}^* = \boldsymbol{U}^*(\delta, \mu, \sigma^2, \boldsymbol{\alpha}, \boldsymbol{T}, \lambda_1, \boldsymbol{\alpha}_1, \boldsymbol{T}_1, \lambda_2, \boldsymbol{\alpha}_2, \boldsymbol{T}_2 )

\boldsymbol{U}_{n+1}^* = f^*(\boldsymbol{U}_n^*)

Pricing these contracts

\text{Price} = \mathbb{E}[ \mathrm{e}^{-\delta \tau} \text{Payoff}( S_\tau, \overline{S}_\tau ) ]

\text{Price} =

\boldsymbol{\alpha}^\top \boldsymbol{F} \, \text{diag}(\boldsymbol{r}) \, \boldsymbol{G} \, \boldsymbol{\alpha}^*

\boldsymbol{G} = \boldsymbol{G}(g, \boldsymbol{U}^*)

\boldsymbol{F} = \boldsymbol{F}(f, \boldsymbol{U})

\text{Payoff}(S_\tau, \overline{S}_\tau) = f(S_\tau) g(\overline{S}_\tau)

\boldsymbol{r} = \boldsymbol{r}( \boldsymbol{U}, \boldsymbol{U}^* )

\boldsymbol{\alpha}^* = (-\boldsymbol{T} \boldsymbol{1}) ^{\top} \text{diag}(-\boldsymbol{\alpha} \boldsymbol{T})

Take home messages

- If you really care about the details, check out our paper

- What are phase-type distributions? Why are they interesting?

- I have a package to fit them in the Julia language.

If you've never tried Julia, go for it.

\dagger

1

3

2

\overline{\boldsymbol{T}} = \left( \begin{matrix}

-6 & 4 & 2 & 0 \\

1 & -1 & 0 & 0 \\

0 & 5 & -5.5 & 0.5 \\

0 & 0 & 0 & 0

\end{matrix} \right)

\boldsymbol{\alpha} = ( \frac13, \frac13, \frac13, 0 )^\top

2

4

1

0.5

5

What are phase-type distributions?

Markov chain State space

( X_t )_{t \ge 0}

\{1, ..., p, \dagger \}

Phase-type definition

Markov chain State space

- Initial distribution

- Sub-transition matrix

- Exit rates

\boldsymbol{\alpha}

\boldsymbol{T}

\boldsymbol{t} = -\boldsymbol{T} 1

\boldsymbol{t}

\tau = \inf_t \{ X_t = \dagger \}

( X_t )_{t \ge 0}

\{1, ..., p, \dagger \}

\Leftrightarrow \tau \sim \mathrm{PhaseType}(\boldsymbol{\alpha}, \boldsymbol{T})

\overline{\boldsymbol{T}} = \left( \begin{matrix}

\boldsymbol{T} & \boldsymbol{t} \\

0 & 0

\end{matrix} \right)

Two ways to view the phases

As meaningless mathematical artefacts

Choose number of phases to balance accuracy and over-fitting

As states which reflect some part of reality

Choose number of phases to match reality

X.S. Lin & X. Liu (2007) Markov aging process and phase-type law of mortality.

N. Amer. Act J. 11, pp. 92-109

M. Govorun, G. Latouche, & S. Loisel (2015). Phase-type aging modeling for health dependent costs. Insurance: Mathematics and Economics, 62, pp. 173-183.

Phase-type properties

Matrix exponential

Density and tail

Moments

Laplace transform

f_\tau(s) = \boldsymbol{\alpha}^\top \mathrm{e}^{\boldsymbol{T} s} \boldsymbol{t}

\mathrm{e}^{\boldsymbol{T} s} = \sum_{i=0}^\infty \frac{(\boldsymbol{T} s)^i}{i!}

\tau \sim \mathrm{PhaseType}(\boldsymbol{\alpha}, \boldsymbol{T})

\overline{F}_\tau(s) = \boldsymbol{\alpha}^\top \mathrm{e}^{\boldsymbol{T} s} 1

\mathbb{E}[\tau] = {-}\boldsymbol{\alpha}^\top \boldsymbol{T}^{-1} \boldsymbol{1}

\mathbb{E}[\tau^n] = (-1)^n n! \,\, \boldsymbol{\alpha}^\top \boldsymbol{T}^{-n} \boldsymbol{1}

\mathbb{E}[\mathrm{e}^{-s\tau}] = \boldsymbol{\alpha}^\top (s \boldsymbol{I} - \boldsymbol{T})^{-1} \boldsymbol{t}

Class of phase-types is dense

S. Asmussen (2003), Applied Probability and Queues, 2nd Edition, Springer

Phase-type generalises...

- Exponential distribution

- Sums of exponentials (Erlang distribution)

- Mixtures of exponentials (hyperexponential distribution)

\boldsymbol{\alpha} = \left( 1 \right), \boldsymbol{T} = \left( -\lambda \right), \boldsymbol{t} = \left( \lambda \right)

\boldsymbol{\alpha} = \left( \begin{matrix}

1 \\

0 \\

0

\end{matrix} \right) ,

\boldsymbol{T} = \left( \begin{matrix}

-\lambda_1 & \lambda_1 & 0 \\

0 & -\lambda_2 & \lambda_2 \\

0 & 0 & -\lambda_3

\end{matrix} \right)

, \boldsymbol{t} = \left( \begin{matrix}

0 \\

0 \\

\lambda_3

\end{matrix} \right)

\boldsymbol{\alpha} = \left( \begin{matrix}

\alpha_1 \\

\alpha_2 \\

\alpha_3

\end{matrix} \right) ,

\boldsymbol{T} = \left( \begin{matrix}

-\lambda_1 & 0 & 0 \\

0 & -\lambda_2 & 0 \\

0 & 0 & -\lambda_3

\end{matrix} \right)

, \boldsymbol{t} =

\left( \begin{matrix}

\lambda_1 \\

\lambda_2 \\

\lambda_3

\end{matrix} \right)

More cool properties

Closure under addition, minimum, maximum

(\tau \mid \tau > s) \sim \mathrm{PhaseType}(\boldsymbol{\alpha}_s, \boldsymbol{T})

\tau_i \sim \mathrm{PhaseType}(\boldsymbol{\alpha}_i, \boldsymbol{T}_i)

\Rightarrow \tau_1 + \tau_2 \sim \mathrm{PhaseType}(\dots, \dots)

\Rightarrow \min\{ \tau_1 , \tau_2 \} \sim \mathrm{PhaseType}(\dots, \dots)

... and under conditioning

\tau_n \sim \mathrm{Erlang}(n, n/T) \,, \quad \tau_n \approx T

Can make a phase-type look like a constant value

Contract over a limited horizon

\begin{aligned}

\tau \wedge T &\approx \tau \wedge \tau_n \\

&= \tau_n^* \sim \mathrm{PhaseType}(\dots, \dots)

\end{aligned}

\text{Price} \approx \mathbb{E}[ \mathrm{e}^{-\delta \tau_n^* } \text{Payoff}( S_{\tau_n^*}, \overline{S}_{\tau_n^*} ) ]

Payout occurs at death or after fixed duration T, whichever first

\text{Price} = \mathbb{E}[ \mathrm{e}^{-\delta (\tau \wedge T)} \text{Payoff}( S_{\tau \wedge T}, \overline{S}_{\tau \wedge T} ) ]

If it works for exponential distribution, try phase-type

Assume:

- is exponentially distributed

- where is a Brownian motion

Then and are independent and exponentially distributed with rates

\tau

S_t = \mathrm{e}^{X_t}

X_t

\overline{X}_\tau

\overline{X}_\tau - X_\tau

\lambda_{\pm} = \mp \frac{\mu}{\sigma^2} + \sqrt{ \frac{\mu^2}{\sigma^4} + \frac{2\lambda}{\sigma^2} }

\lambda

\mu, \sigma^2

Wiener-Hopf Factorisation

\mathbb{P}(\overline{X}_\tau \in \mathrm{d}x, X_\tau - \overline{X}_\tau \in \mathrm{d}y) = \mathbb{P}(\overline{X}_\tau \in \mathrm{d}x) \mathbb{P}(\underline{X}_\tau \in \mathrm{d}y)

X_t

-

is an exponential random variable

- is a Lévy process

\tau

Doesn't work for non-random time

\mathbb{P}(\overline{X}_t \in \mathrm{d}x, X_t - \overline{X}_t \in \mathrm{d}y \mid \overline{\sigma}_t = s)

= \mathbb{P}(\overline{X}_t \in \mathrm{d}x \mid \overline{\sigma}_t = s) \mathbb{P}(\underline{X}_t \in \mathrm{d}y \mid \underline{\sigma}_t = t - s)

How to fit them?

Traditionally, using EM algorithm

Bladt, M., Gonzalez, A. and Lauritzen, S. L. (2003), ‘The estimation of Phase-type related functionals using Markov chain Monte Carlo methods’, Scandinavian Actuarial Journal

Representation is not unique

\boldsymbol{\alpha} = ( 1, 0, 0 )^\top

\boldsymbol{T}_1 = \left( \begin{matrix}

-1 & 1 & 0 \\

0 & -2 & 2 \\

0 & 0 & -3

\end{matrix} \right)

\boldsymbol{T}_2 = \left( \begin{matrix}

-3 & 3 & 0 \\

0 & -2 & 2 \\

0 & 0 & -1

\end{matrix} \right)

\tau_1 \sim \mathrm{PhaseType}(\boldsymbol{\alpha}, \boldsymbol{T}_1)

\tau_2 \sim \mathrm{PhaseType}(\boldsymbol{\alpha}, \boldsymbol{T}_2)

\tau_1 \overset{\mathscr{D}}{=} \tau_2

Also, not easy to tell if any parameters produce a valid distribution

Lots of parameters to fit

- General

- Coxian distribution

\boldsymbol{\alpha} = \left( \begin{matrix}

1 \\

0 \\

0

\end{matrix} \right) , \quad

\boldsymbol{T} = \left( \begin{matrix}

-\lambda_1 & \lambda_{12} & 0 \\

0 & -\lambda_2 & \lambda_{23} \\

0 & 0 & -\lambda_3

\end{matrix} \right)

\boldsymbol{\alpha} = \left( \begin{matrix}

\alpha_1 \\

\alpha_2 \\

\alpha_3

\end{matrix} \right) , \quad

\boldsymbol{T} = \left( \begin{matrix}

-\lambda_1 & \lambda_{12} & \lambda_{13} \\

\lambda_{21} & -\lambda_2 & \lambda_{23} \\

\lambda_{31} & \lambda_{32} & -\lambda_3

\end{matrix} \right)

p(p+1)-1

2p-1

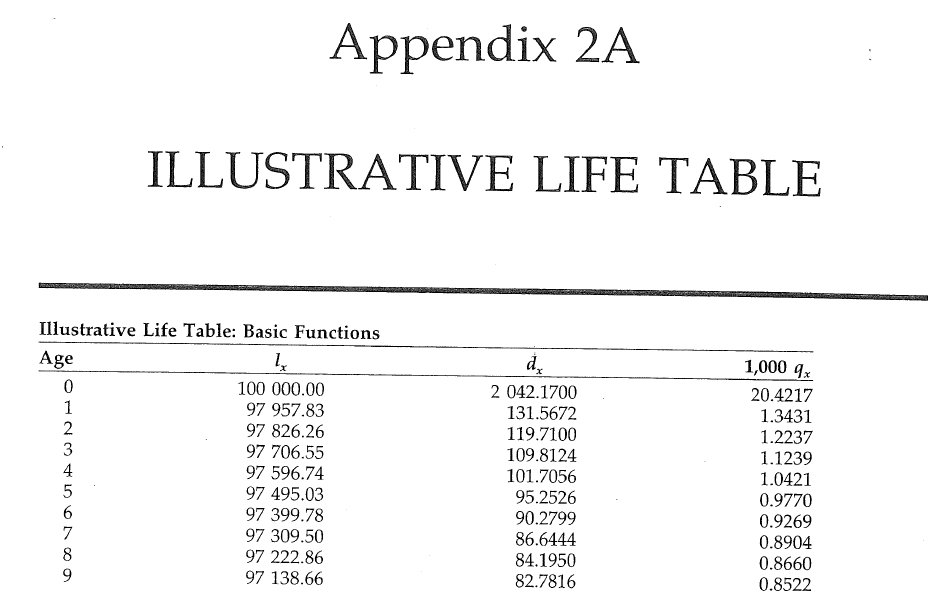

Problem: to model mortality via phase-type

Bowers et al (1997), Actuarial Mathematics, 2nd Edition

Fit General Phase-type with C

p = 5

p = 10

p = 20

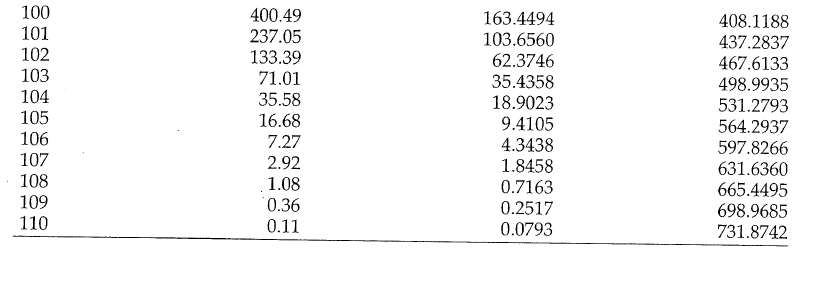

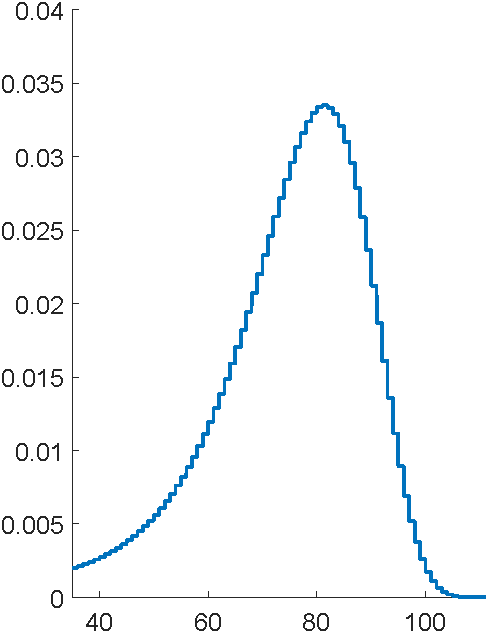

\text{Life Table}

Why's this so terrible?

\mathrm{e}^{\boldsymbol{T} s} = \sum_{i=0}^\infty \frac{(\boldsymbol{T} s)^i}{i!}

"E" step has a bazillion matrix exponential calculations

Fit Coxian distributions

p = 5

p = 10

p = 20

\text{Life Table}

General vs Coxian

Rewrite in Julia

void rungekutta(int p, double *avector, double *gvector, double *bvector,

double **cmatrix, double dt, double h, double **T, double *t,

double **ka, double **kg, double **kb, double ***kc)

{

int i, j, k, m;

double eps, h2, sum;

i = dt/h;

h2 = dt/(i+1);

init_matrix(ka, 4, p);

init_matrix(kb, 4, p);

init_3dimmatrix(kc, 4, p, p);

if (kg != NULL)

init_matrix(kg, 4, p);

...

for (i=0; i < p; i++) {

avector[i] += (ka[0][i]+2*ka[1][i]+2*ka[2][i]+ka[3][i])/6;

bvector[i] += (kb[0][i]+2*kb[1][i]+2*kb[2][i]+kb[3][i])/6;

for (j=0; j < p; j++)

cmatrix[i][j] +=(kc[0][i][j]+2*kc[1][i][j]+2*kc[2][i][j]+kc[3][i][j])/6;

}

}

}

This function: 116 lines of C, built-in to Julia

Whole program: 1700 lines of C, 300 lines of Julia

# Run the ODE solver.

u0 = zeros(p*p)

pf = ParameterizedFunction(ode_observations!, fit)

prob = ODEProblem(pf, u0, (0.0, maximum(s.obs)))

sol = solve(prob, OwrenZen5())https://github.com/Pat-Laub/EMpht.jl

DE solver going negative

# Run the ODE solver.

u0 = zeros(p*p)

pf = ParameterizedFunction(ode_observations!, fit)

prob = ODEProblem(pf, u0, (0.0, maximum(s.obs)))

sol = solve(prob, OwrenZen5())

...

u = sol(s.obs[k])

C = reshape(u, p, p)

if minimum(C) < 0

(C,err) = hquadrature(p*p, (x,v) -> c_integrand(x, v, fit, s.obs[k]),

0, s.obs[k], reltol=1e-1, maxevals=500)

C = reshape(C, p, p)

end

Swap to quadrature in Julia

Fit Coxian with more phases

p = 50

p = 75

p = 100

\text{Life Table}

Coxian: Small p vs Big p

Uniformization magic

Coxian with uniformization

p = 50

p = 75

p = 100

\text{Life Table}

ODE vs Uniformization

A twist on the Coxian form

Canonical form 1

\boldsymbol{\alpha} = \left( \begin{matrix}

\alpha_1 \\

\alpha_2 \\

\alpha_3

\end{matrix} \right) , \quad

\boldsymbol{T} = \left( \begin{matrix}

-\lambda_1 & \lambda_1 & 0 \\

0 & -\lambda_2 & \lambda_2 \\

0 & 0 & -\lambda_3

\end{matrix} \right)

\lambda_1 < \lambda_2 < \dots < \lambda_p

Et voilà

p = 200

\text{Life Table}

using Pkg; Pkg.add("EMpht")

using EMpht

lt = EMpht.parse_settings("life_table.json")[1]

phCF200 = empht(lt, p=200, ph_structure="CanonicalForm1")Julia Package Published

Remember to try Julia

Thanks for listening!

IME Talk

By plaub