qplum

Our dream is to make investing a science ... not a competition, but a truly inclusive process. The way we can come together to achieve this is to make investment management more (1) Thorough (2) Efficient (3) Transparent. Means: A.I and Tech

Information presented here is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and there are no guarantees of any kind. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed here in. Past performance is not indicative of future performance.

Hardik Patel

How does a typical quant pipeline look like?

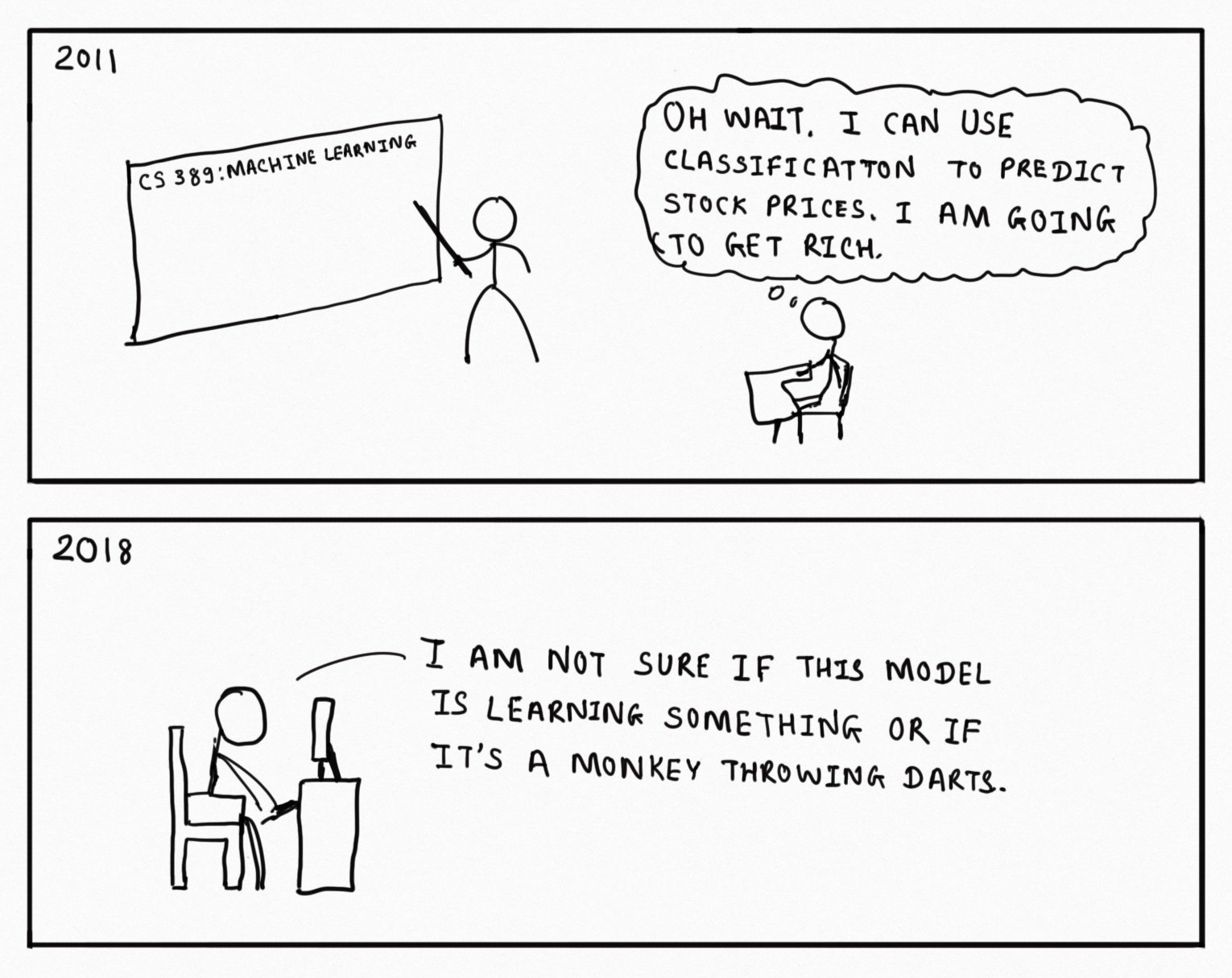

But, how does Machine Learning come into the picture?

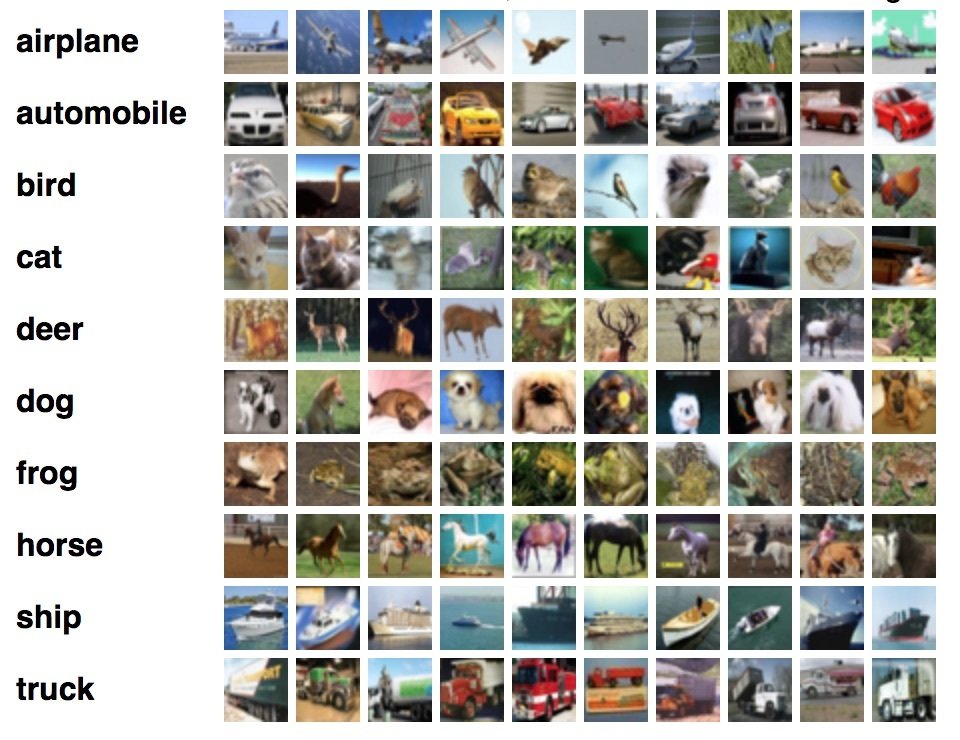

CIFAR10 is an image classification dataset

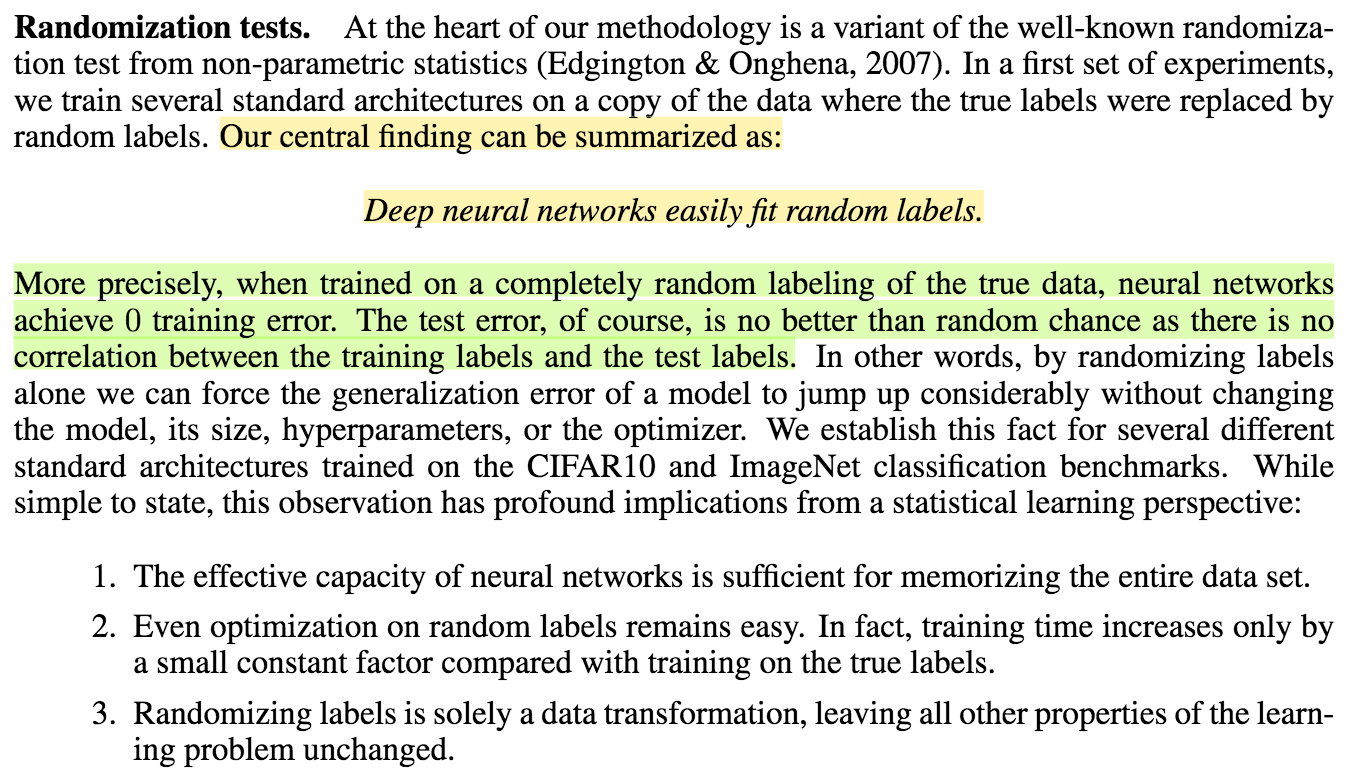

"Understanding deep learning requires rethinking generalization" paper from Google Brain

Is there a way to solve this generalization problem?

So, what can we do here?

If you see a pattern in the dataset, it's more likely to be noise than signal

Model interpretability

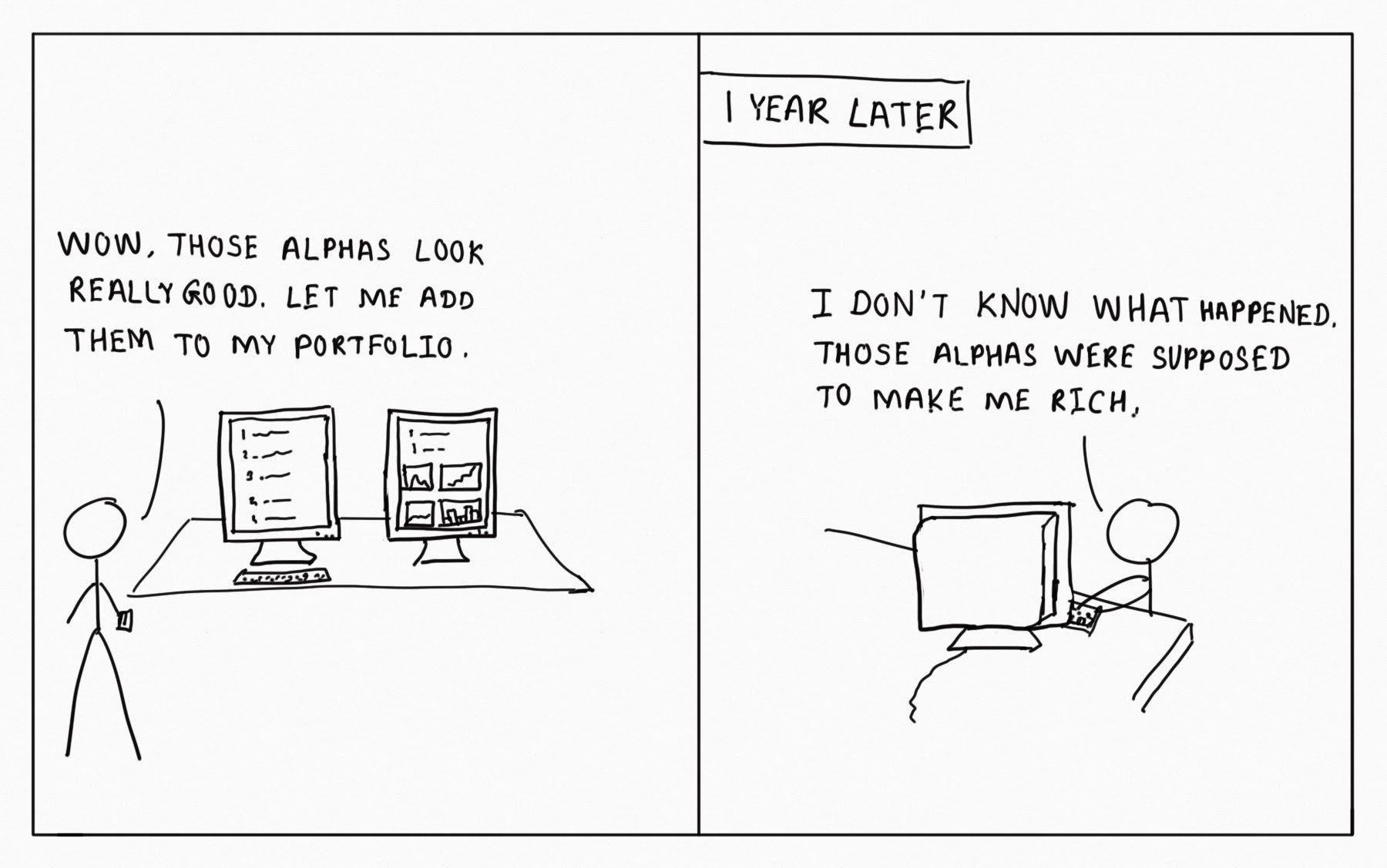

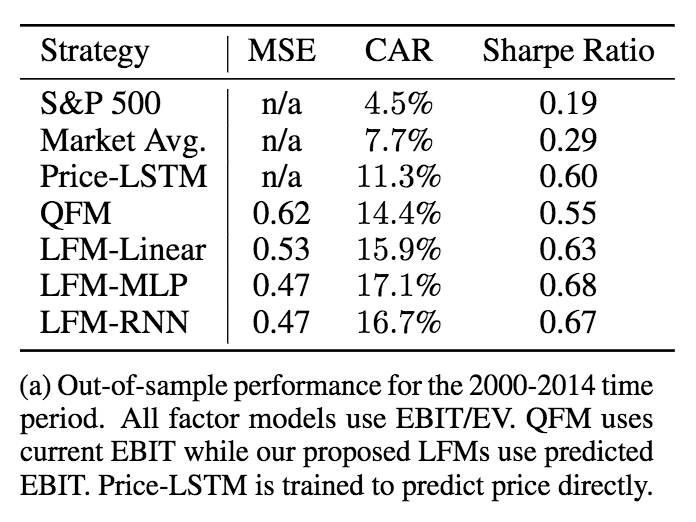

Model accuracy improvement might not lead to better portfolio returns

Wait, why can't we directly optimize the utility function?

Reinforcement Learning is another option to directly optimize the utility function

hardik@qplum.co

Information presented here is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and there are no guarantees of any kind. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed here in. Past performance is not indicative of future performance.

By qplum

Hardik Patel, presents four major pitfalls companies face when using machine learning methods in finance, and his advice on how to solve for them.