qplum

Our dream is to make investing a science ... not a competition, but a truly inclusive process. The way we can come together to achieve this is to make investment management more (1) Thorough (2) Efficient (3) Transparent. Means: A.I and Tech

See important disclosures at the end of this presentation.

to connect the loose ends of this talk

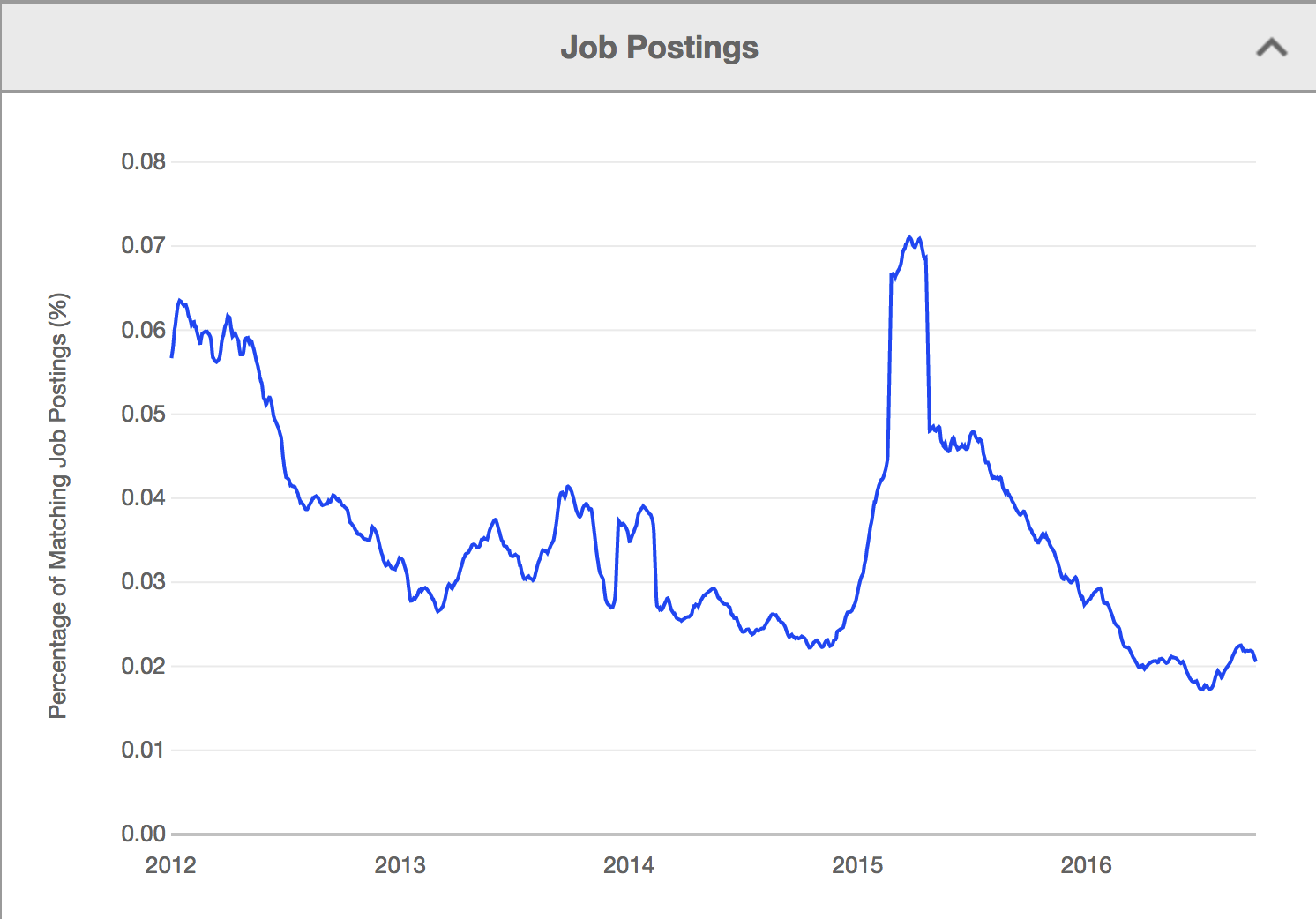

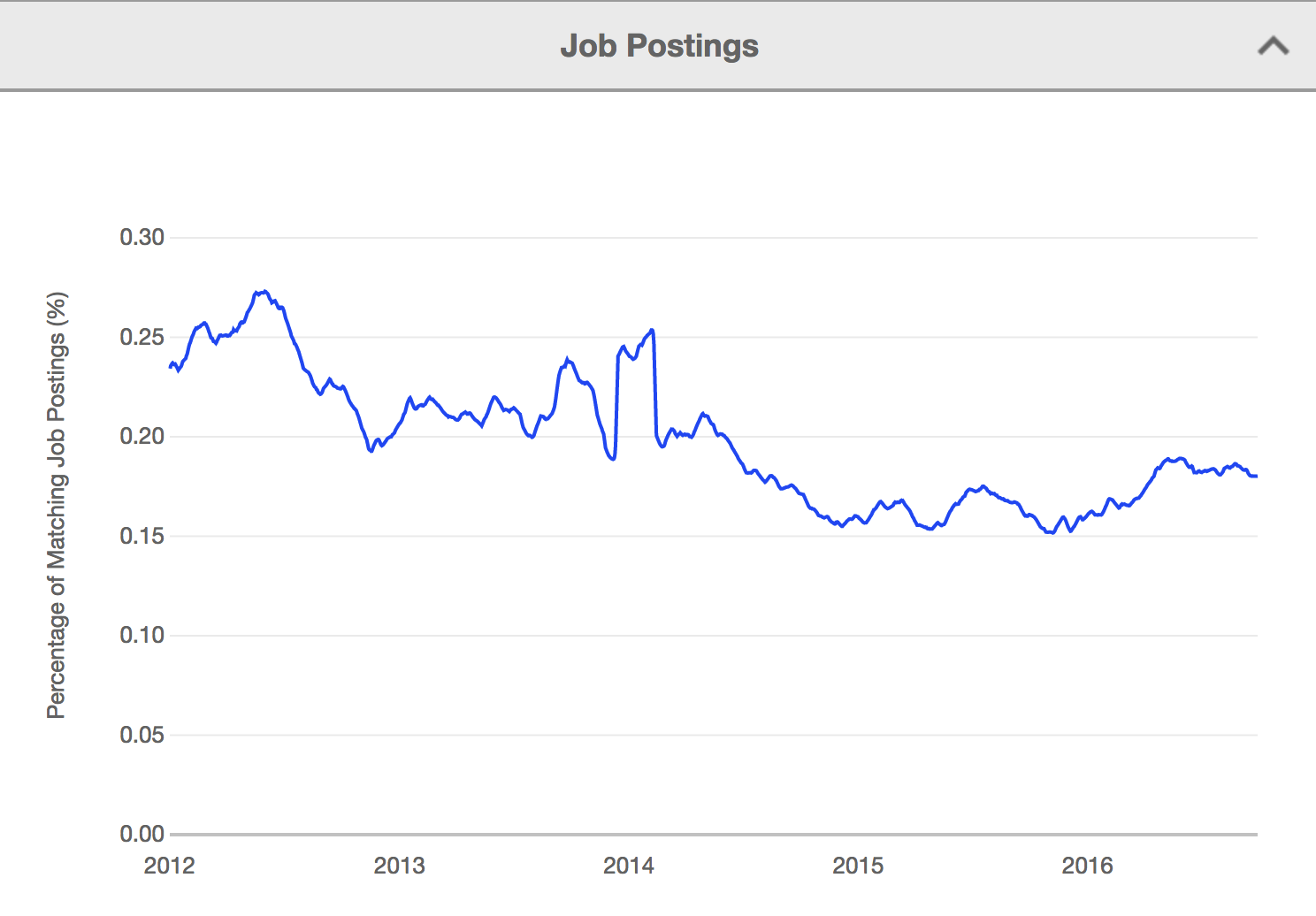

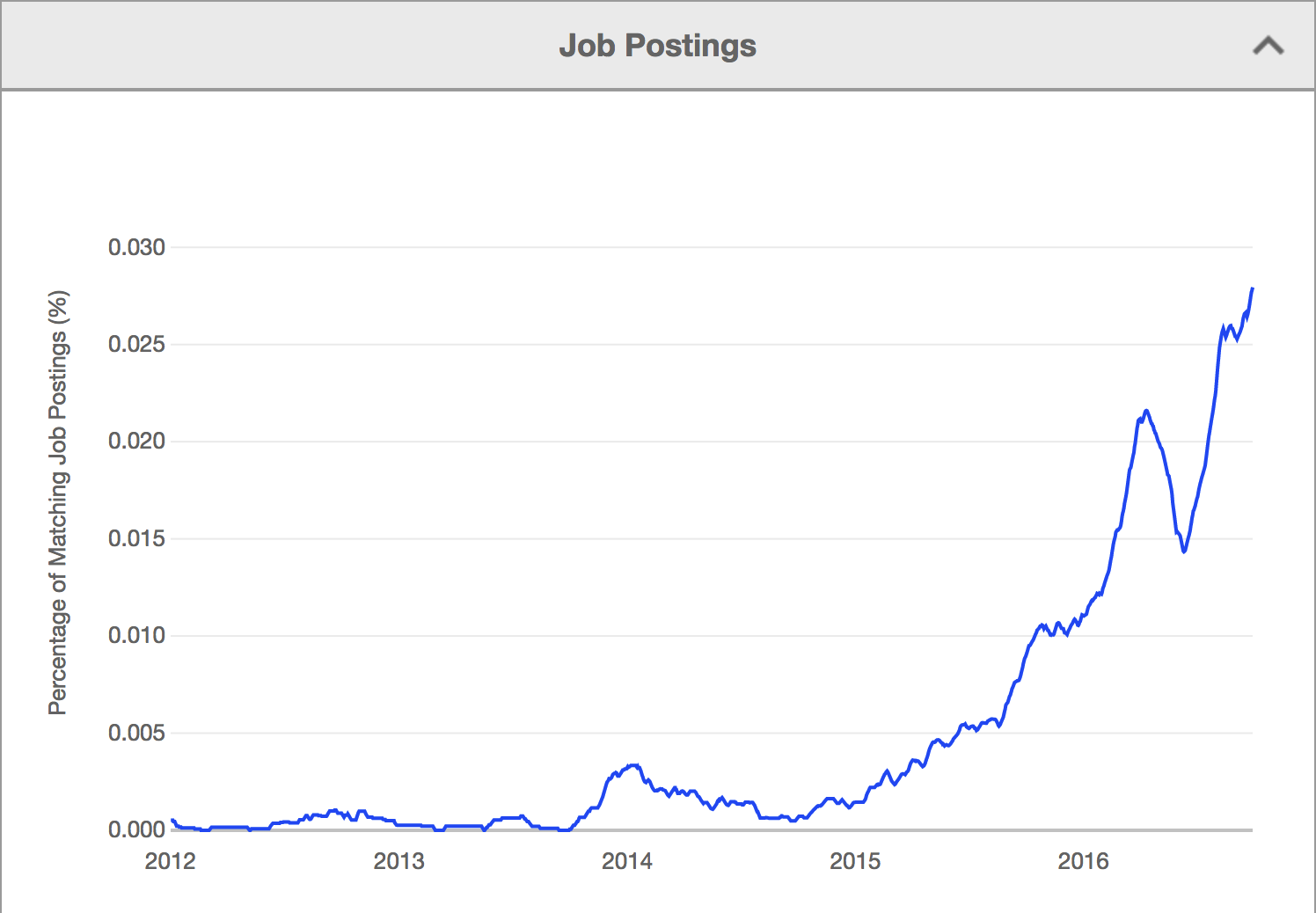

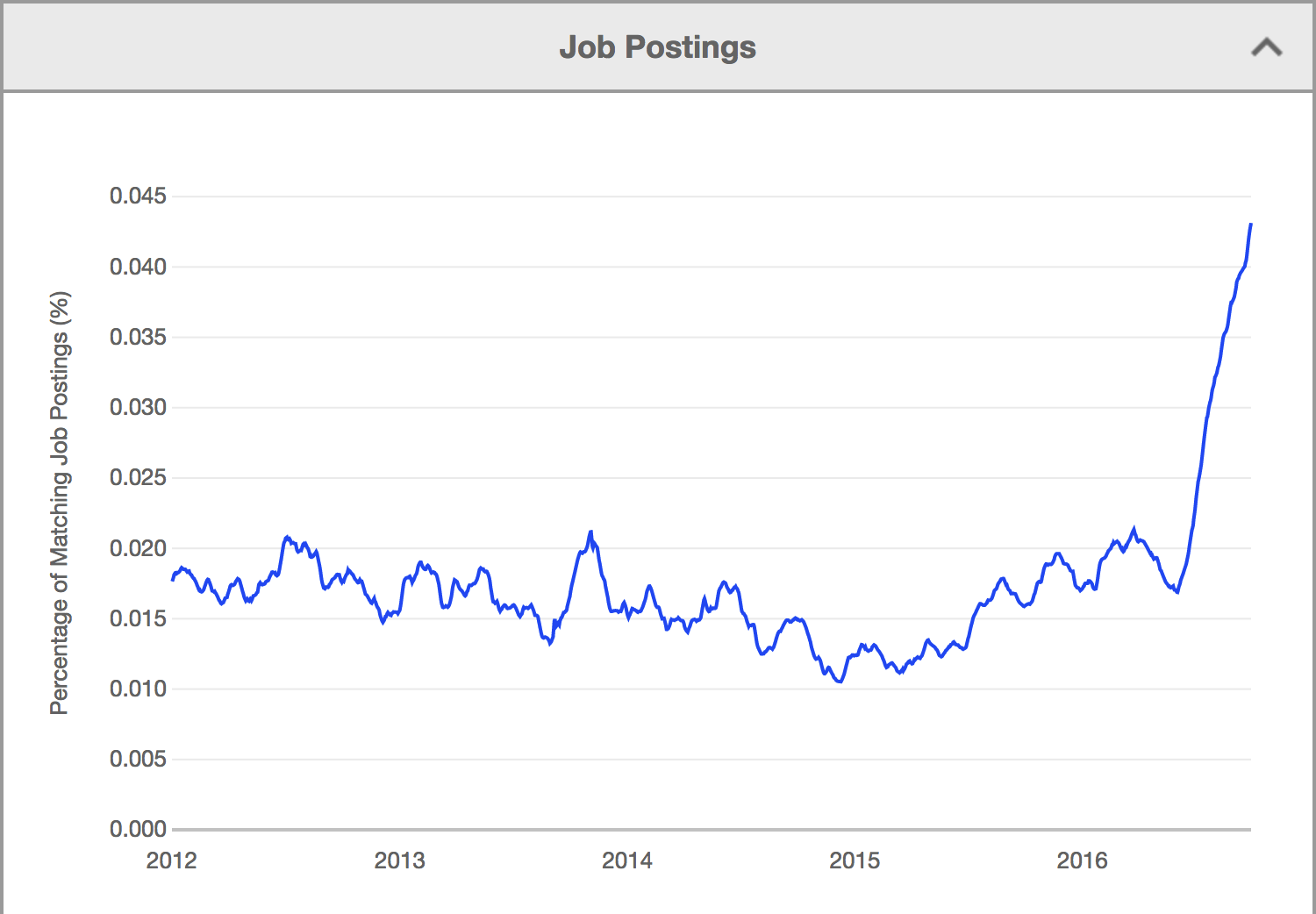

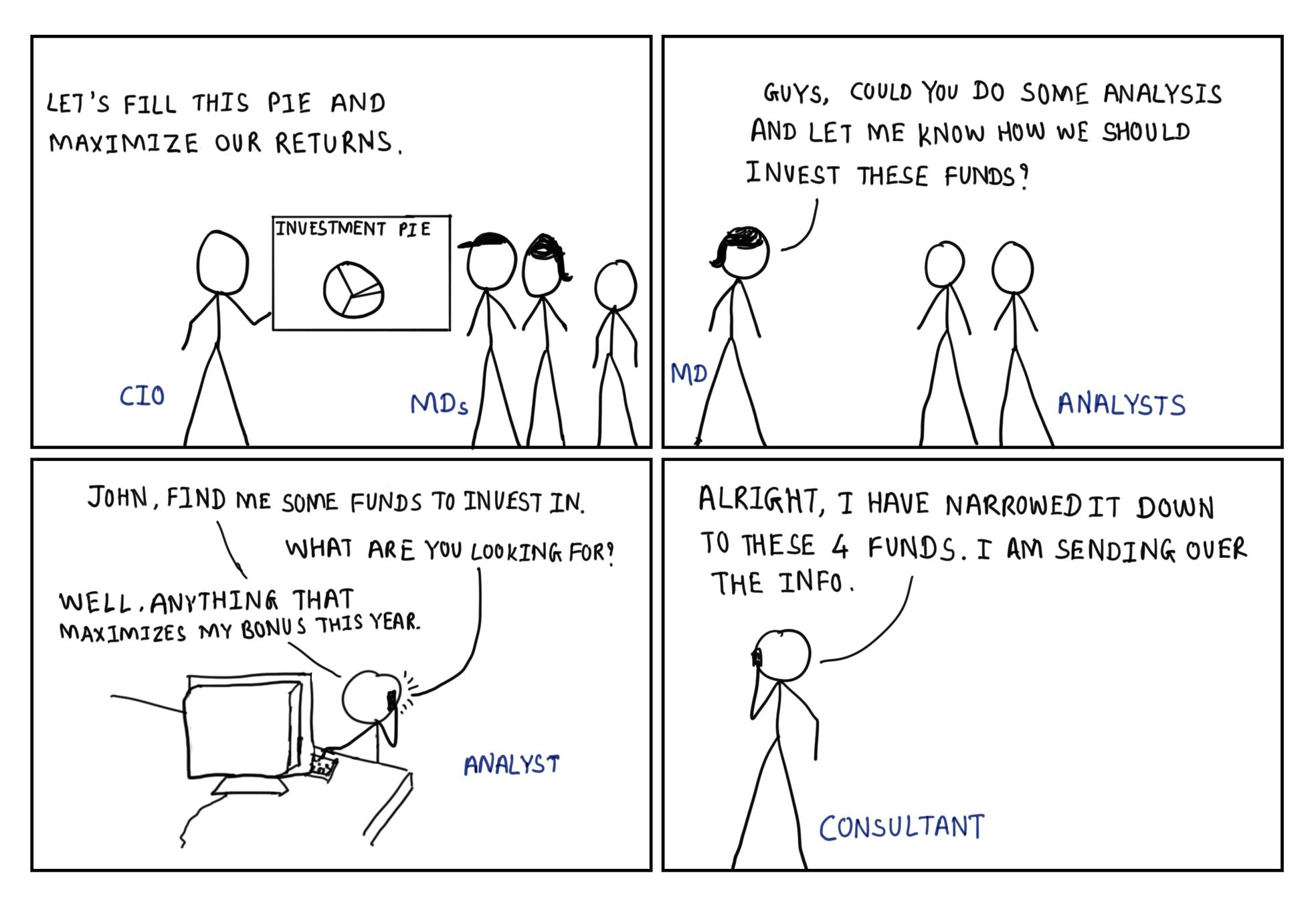

Nationwide job postings - traders, quants, FinTech, A.I.

Source: Indeed.com

Narv Narvekar

HMC

David Swensen

Yale

Warren Buffett

Berkshire

Ken Griffin

Citadel

Images may be subject to copyright

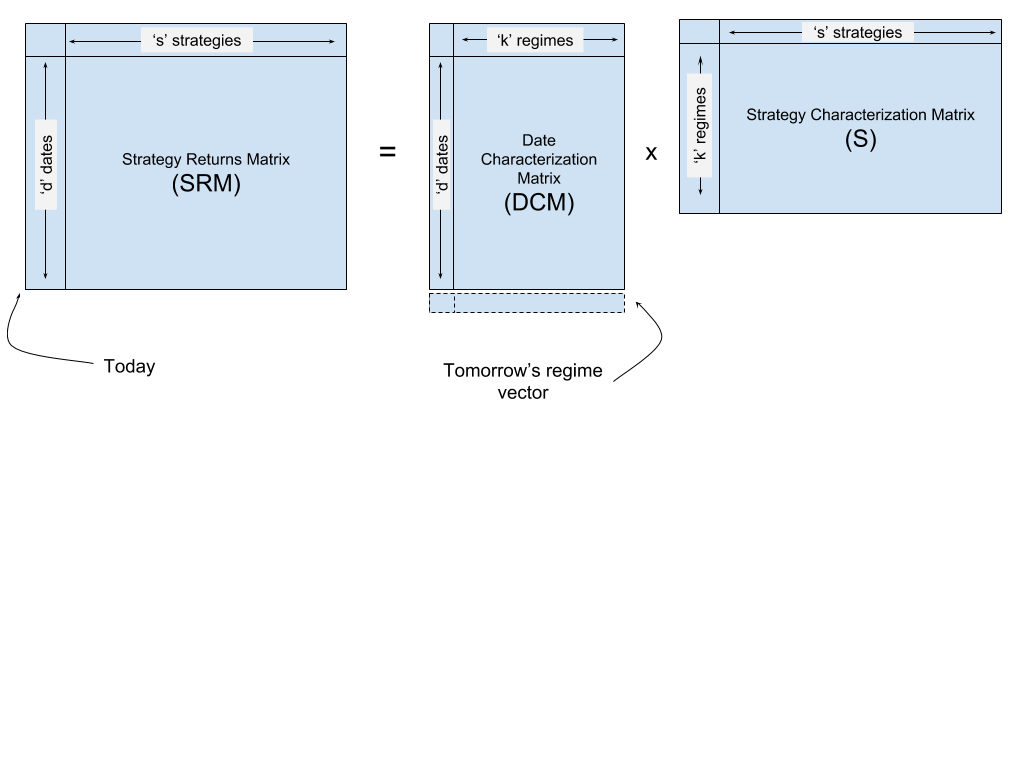

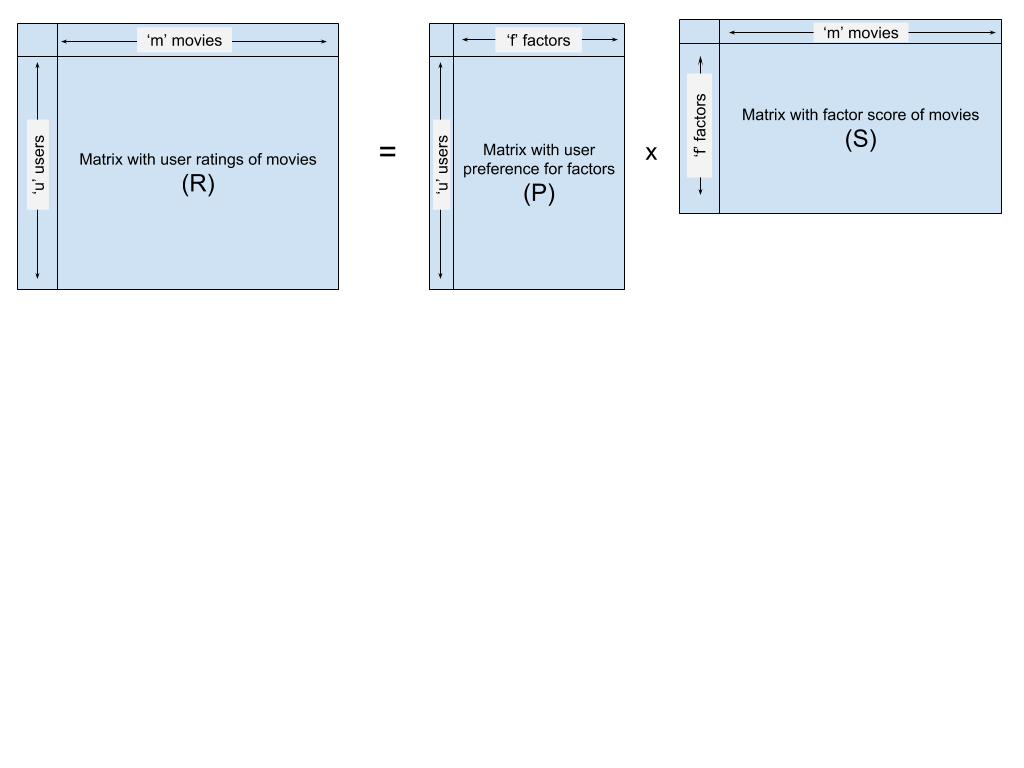

It turns out that allocating to investment strategies is very similar to recommender systems

Visualization of matrix factorization based collaborative filtering

"Unsupervised learning had a catalytic effect in reviving interest in deep learning, but has since been overshadowed by the successes of purely supervised learning. Although we have not focused on it in this Review, we expect unsupervised learning to become far more important in the longer term." - Geoffrey Hinton et. al., Nature, Deep Learning

- Investment strategies that learn by themselves (article)

"security analysis may begin--modestly, but hopefully--to refer to itself as a scientific discipline "

Imagining investing with a "trustworthy tool" and not experts!

- Benjamin Graham

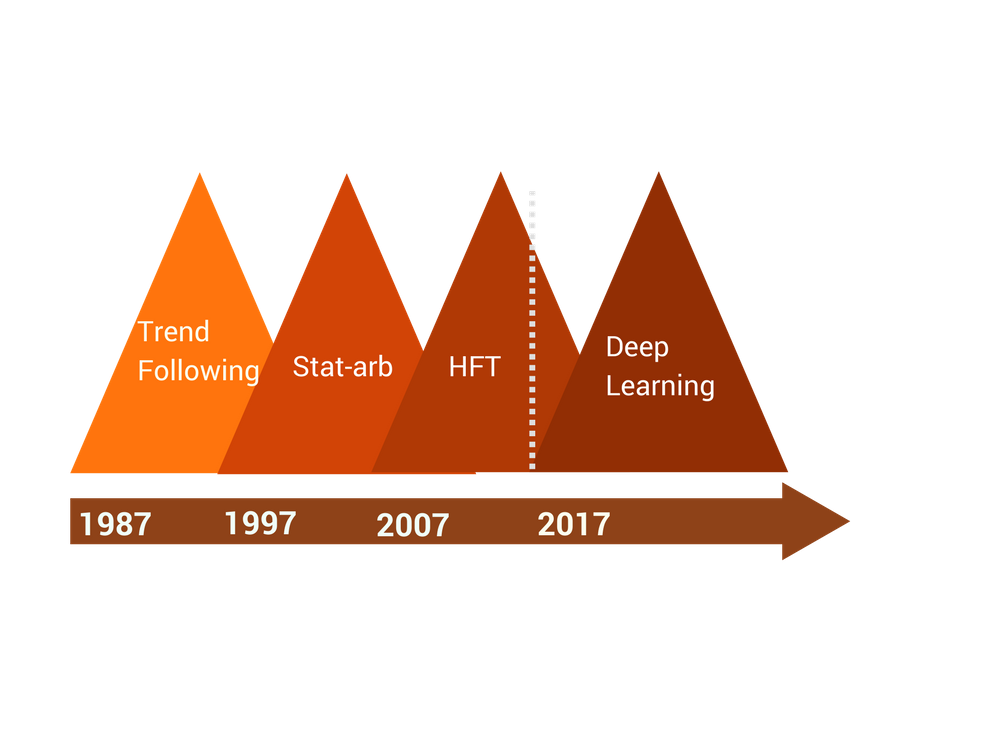

Asset management, a $160 trillion dollar industry is yet to be affected by A.I.

Time is ripe for the move to machine learning methods in institutional investing

(1) need to reduce costs

(2) find other sources of returns and

(3) use of systematic processes

You can make it happen!

Important Disclaimers: This presentation is the proprietary information of qplum Inc (“qplum”) and may not be disclosed or distributed to any other person without the prior consent of qplum. This information is presented for educational purposes only and does not constitute and offer to sell or a solicitation of an offer to buy any securities. The information does not constitute investment advice and does not constitute an investment management agreement or offering circular.

Certain information has been provided by third-party sources, and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. The information is furnished as of the date shown. No representation is made with respect to its completeness or timeliness. The information is not intended to be, nor shall it be construed as, investment advice or a recommendation of any kind. Past performance is not a guarantee of future results. Important information relating to qplum and its registration with the Securities and Exchange Commission (SEC), and the National Futures Association (NFA) is available here and here.

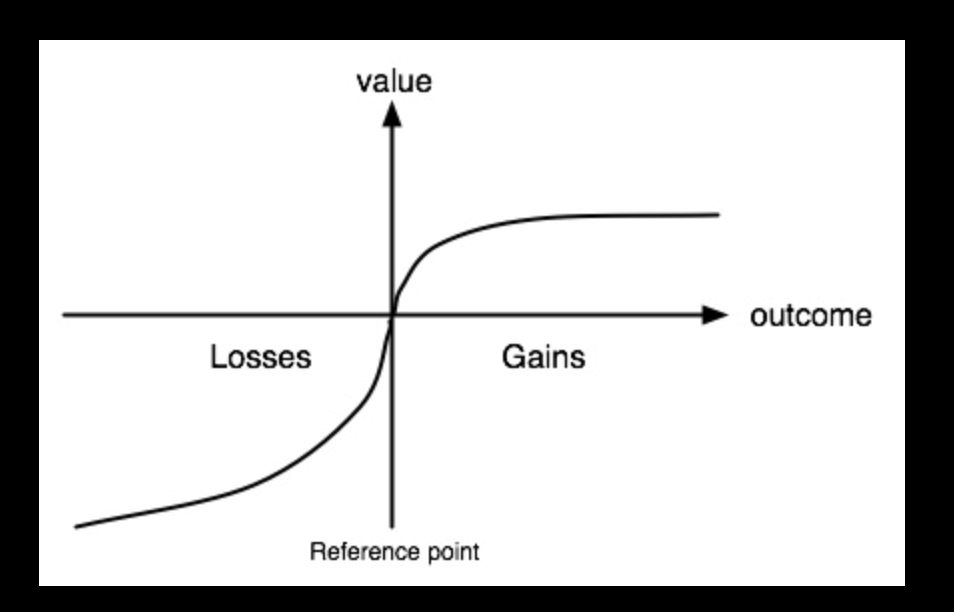

It is not always just about higher returns.

Utility function is not uniformly distributed.

Utility function is not the same.

Most pension funds have a nominal target yield.

Not meeting the target yield is a big deal compared to outperformance

III. Capacity:

Investments that have scale and capacity to get in and to get out

IV. Should work with illiquid assets:

Illiquid investments are a part of everyone's portfolio.

One cannot look at liquid investments without considering the illiquid assets that are a part of the portfolio already.

“By choosing to place asset allocation at the center of the investment process, investors ground the decision-making framework on the stable foundation of long-term policy actions.

Focus on asset allocation relegates market timing and security selection decisions to the background, reducing the degree to which investment results depend on mercurial, unreliable factors.

Selecting the asset classes for a portfolio constitutes a critically important set of decisions, contributing in large measure to a portfolio’s success or failure. Identifying appropriate asset classes requires focus on functional characteristics, considering potential to deliver returns and to mitigate portfolio risk. Commitment to an equity bias enhances returns, while pursuit of diversification reduces risks. Thoughtful, deliberate focus on asset allocation dominates the agenda of long-term investors.”

– David Swensen

(a) Target constant risk in the portfolio.

(b) Optimize portfolio for the specified utility function.

(c) Constrain any studies to a specified, systematic risk management threshold.

Important Disclaimers: This presentation is the proprietary information of qplum Inc (“qplum”) and may not be disclosed or distributed to any other person without the prior consent of qplum. This information is presented for educational purposes only and does not constitute and offer to sell or a solicitation of an offer to buy any securities. The information does not constitute investment advice and does not constitute an investment management agreement or offering circular.

Certain information has been provided by third-party sources, and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. The information is furnished as of the date shown. No representation is made with respect to its completeness or timeliness. The information is not intended to be, nor shall it be construed as, investment advice or a recommendation of any kind. Past performance is not a guarantee of future results. Important information relating to qplum and its registration with the Securities and Exchange Commission (SEC), and the National Futures Association (NFA) is available here and here.

By qplum

Gaurav Chakravorty explains how recommender systems can be utilized for investment management and details how AI and deep learning are used in trading today. Gaurav begins by diving into chief investment offices, which are growing their in-house machine learning teams to fine-tune their allocation, using both traditional and alternative strategies. Gaurav shares a novel approach to deciding asset and strategy allocations, inspired by research in recommender systems. Gaurav then explores the application of deep learning in trading, discussing useful techniques for AI-driven asset managers as well as the blind alleys they’ve gone down. With these cases as context, Gaurav addresses some of the technical and operational aspects of AI, such as key bottlenecks in training and inference, the software frameworks and hardware platforms that are most useful for those workloads, deployments, the scaling challenges, and the key drivers of the cost.