David Stancel

Cryptocurrency Expert, Advisor, Lecturer, Author, & exCTO @ Fumbi

David Stancel, MSc.

Contact:

stanceldavid.sk

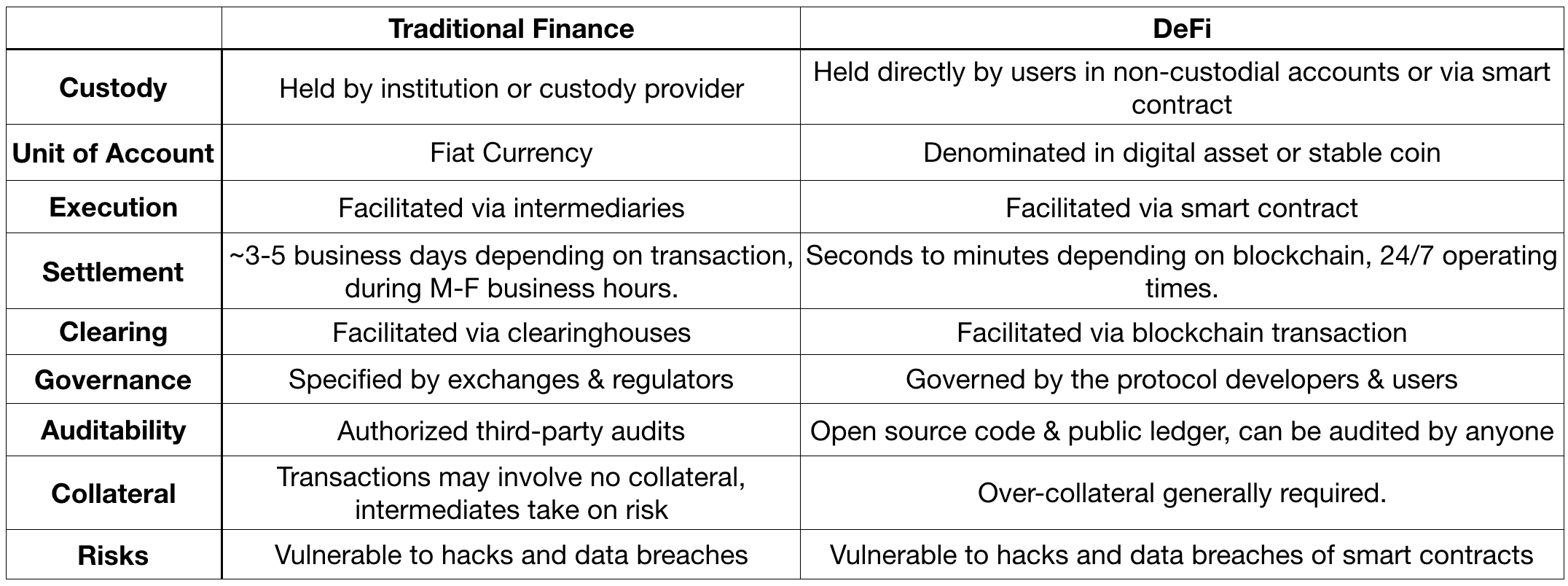

Completely Transparent

Blockchain

Open-Source

Eliminates Middlemen

Trust-minimizing

Open and permissionless

Composable

Allows unprecedented automatization

algorithmic finance

programmable money

Allows things that have not been possible before

Stablecoin with no counterparty risk

Flash loans

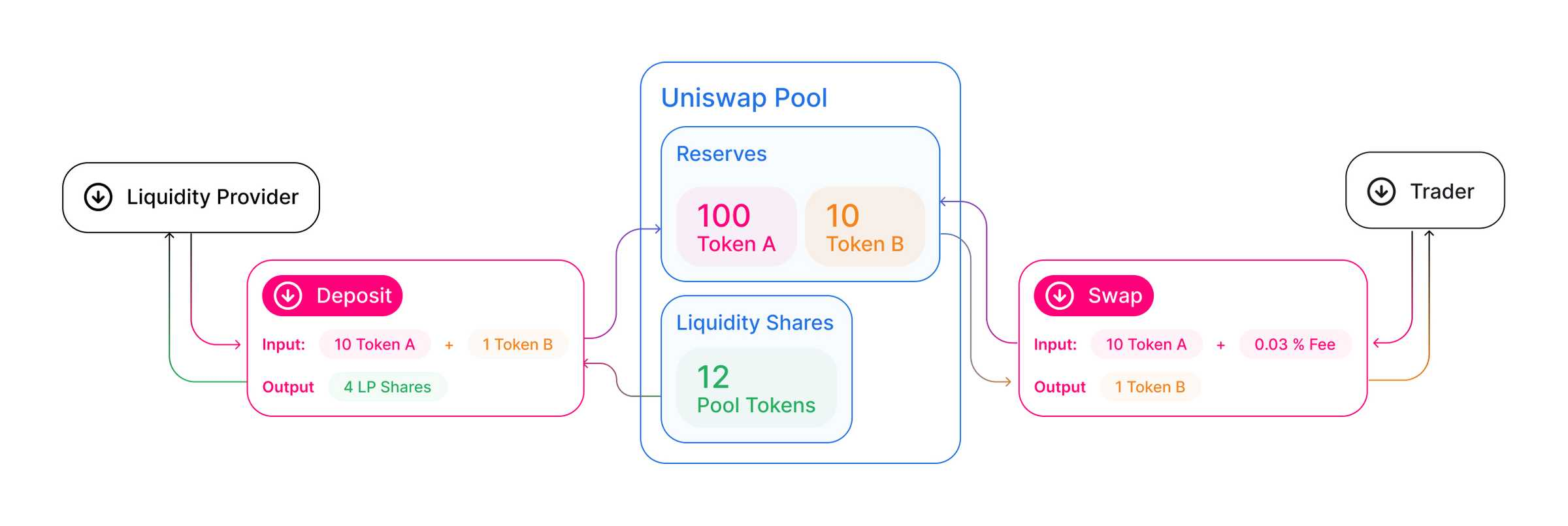

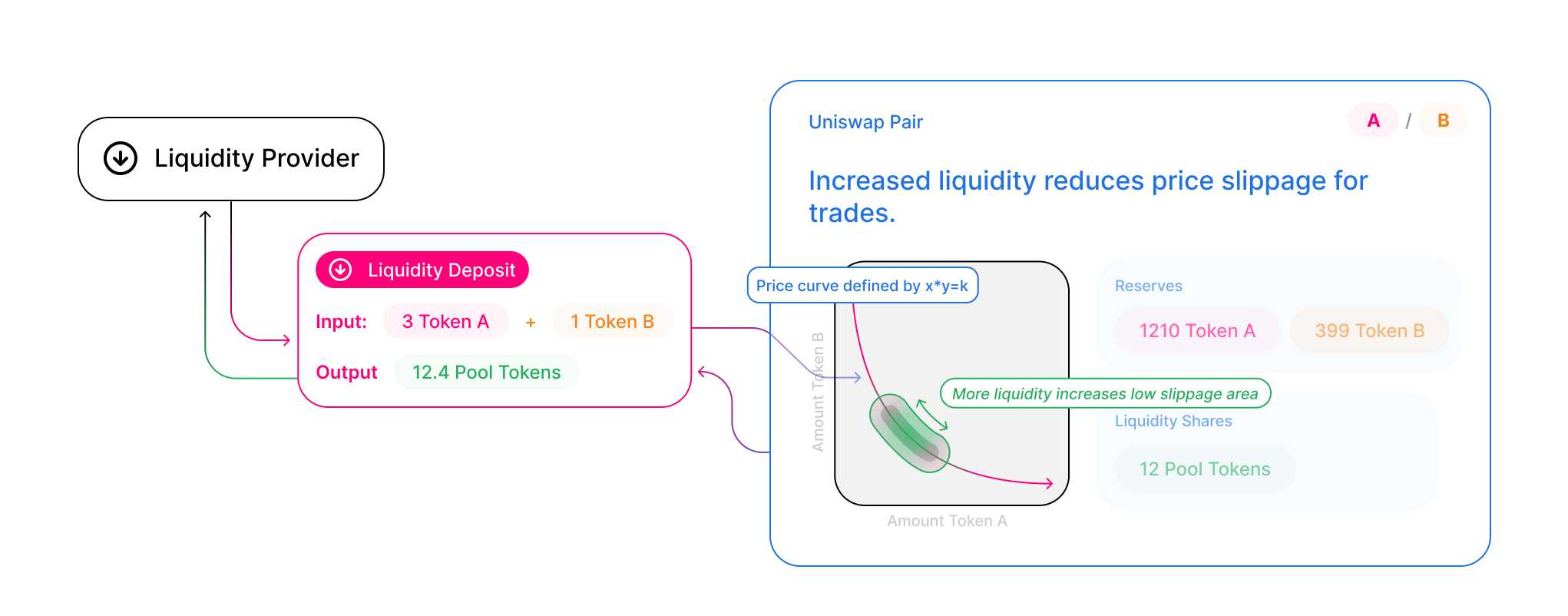

Uniswap is a fully decentralized on-chain protocol for token exchange on Ethereum that uses liquidity pools (AMM) instead of order books. Anyone can quickly swap between ETH and any ERC20 token or earn fees by supplying any amount of liquidity. And anyone can create a market (i.e., liquidity pool) by supplying an equal value of ETH and an ERC20 token.

Uniswap allows only one market per ERC20 token. The market creator sets the exchange rate, which shifts through trading due to Uniswap’s “constant product market maker” mechanism. When trading reduces one side of the pair’s liquidity relative to the other, the price changes. This creates arbitrage opportunities, encouraging more trading.

1. Deposit ETH to Metamask

2. Wrap ETH --> WETH (via Dai.makerdao.com)

3.Exchange it for PETH (pool eth), used for collateral

4. Create CDP (the loan)

5. Lock your PETH collateral

6. Mint new DAI (max. 60% of collateral)

7. Exchange DAI for ETH

8. Send ETH to any exchange and get EUR, BTC etc.

1. Get some ETH

2. Exchange it for DAI (which you owe) and MKR (for governance fee) on Oasis DEX

3. Return DAI to the smart contract and pay the fee in MKR

4. You cancel CDP smart contract

5. Unlock your PETH

6. Exchange PETH for WETH

7. Unwrap WETH --> ETH

8. You have your ETH back

https://etherscan.io/token/0x6c3ea9036406852006290770bedfcaba0e23a0e8

By David Stancel

DeFi