David Stancel

Cryptocurrency Expert, Advisor, Lecturer, Author, & exCTO @ Fumbi

Workshop

David Stancel

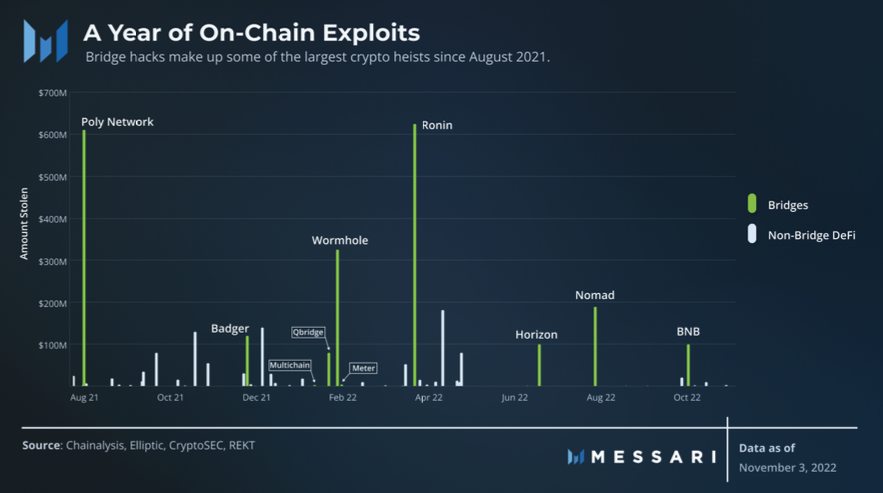

THREE ARROWS CAPITAL

VOYAGER DIGITAL

CELSIUS NETWORK

FTX

BlockFI

Core SCientific

Genesis Global Capital

Great Source on Scams in Crypto:

https://www.youtube.com/@Coffeezilla

Text

Text

Text

Text

Text

Text

Text

Text

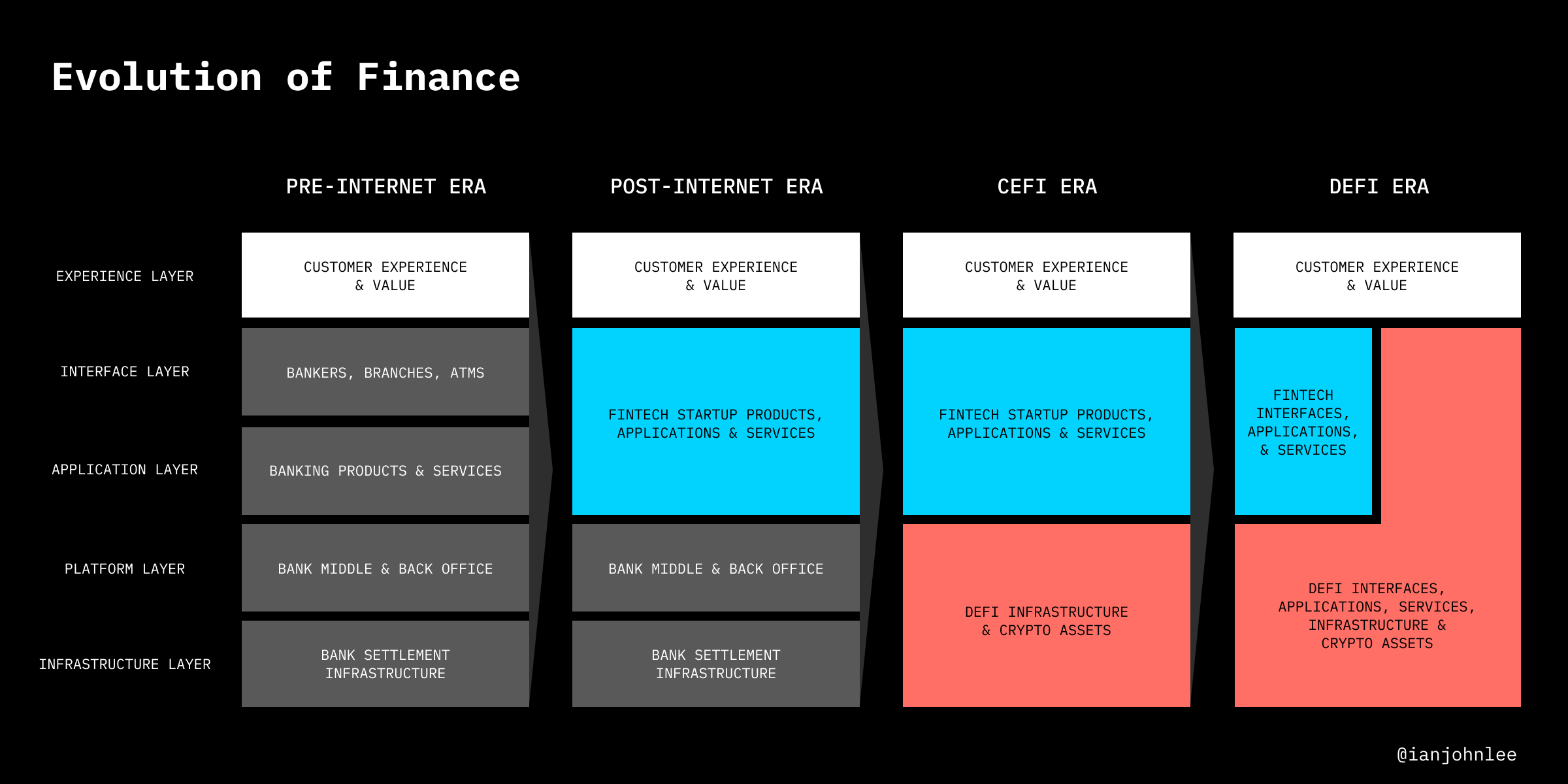

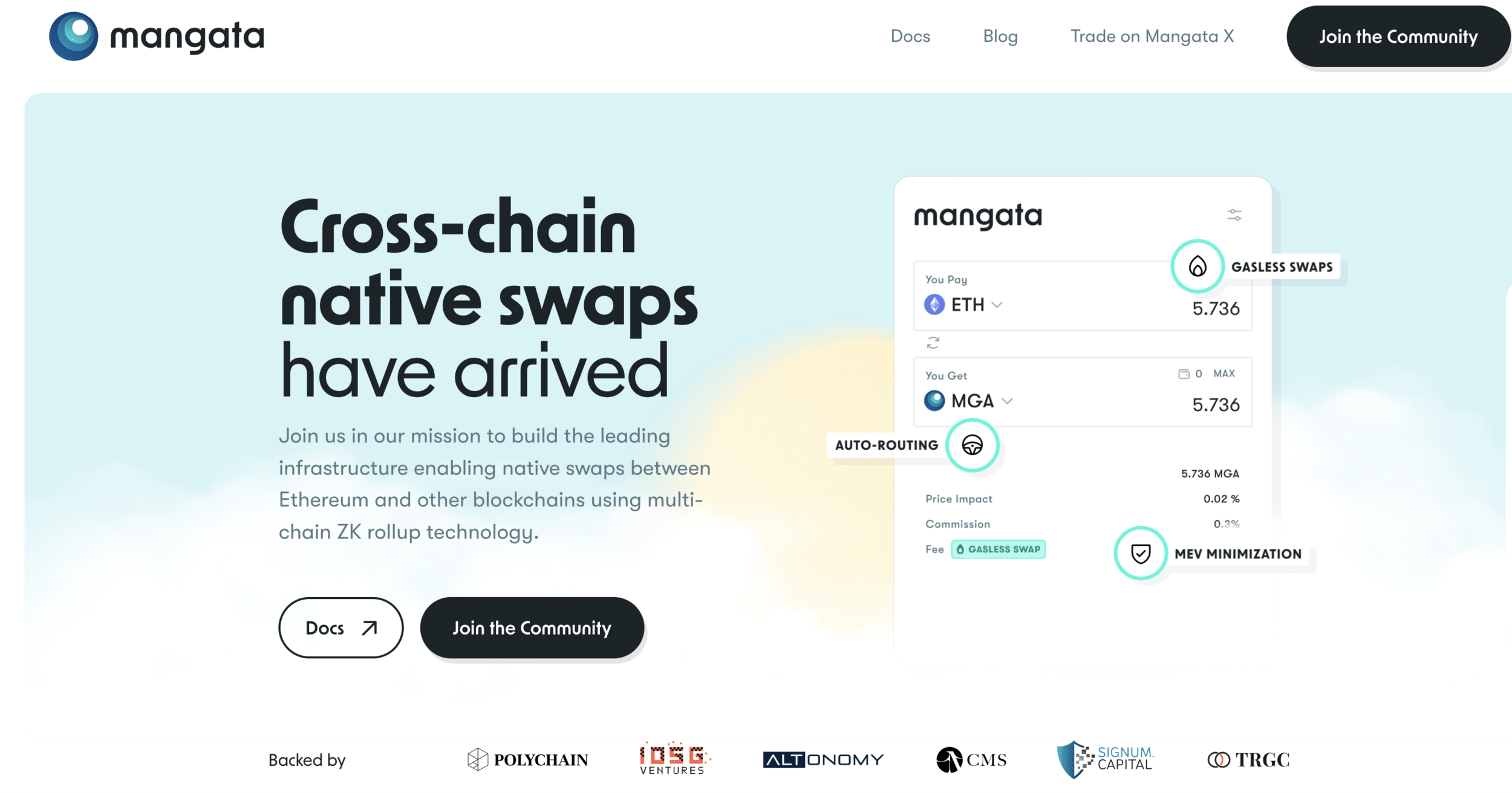

Restaking enables staked ETH to be used as cryptoeconomic security for protocols other than Ethereum, in exchange for protocol fees and rewards.

Restaking is available for both natively staked ETH and liquid staked tokens like stETH, rETH, cbETH, and LsETH.

Completely Transparent

Blockchain

Open-Source

Eliminates Middlemen

Trust-minimizing

Open and permissionless

Composable

Allows unprecedented automatization

algorithmic finance

programmable money

Allows things that have not been possible before

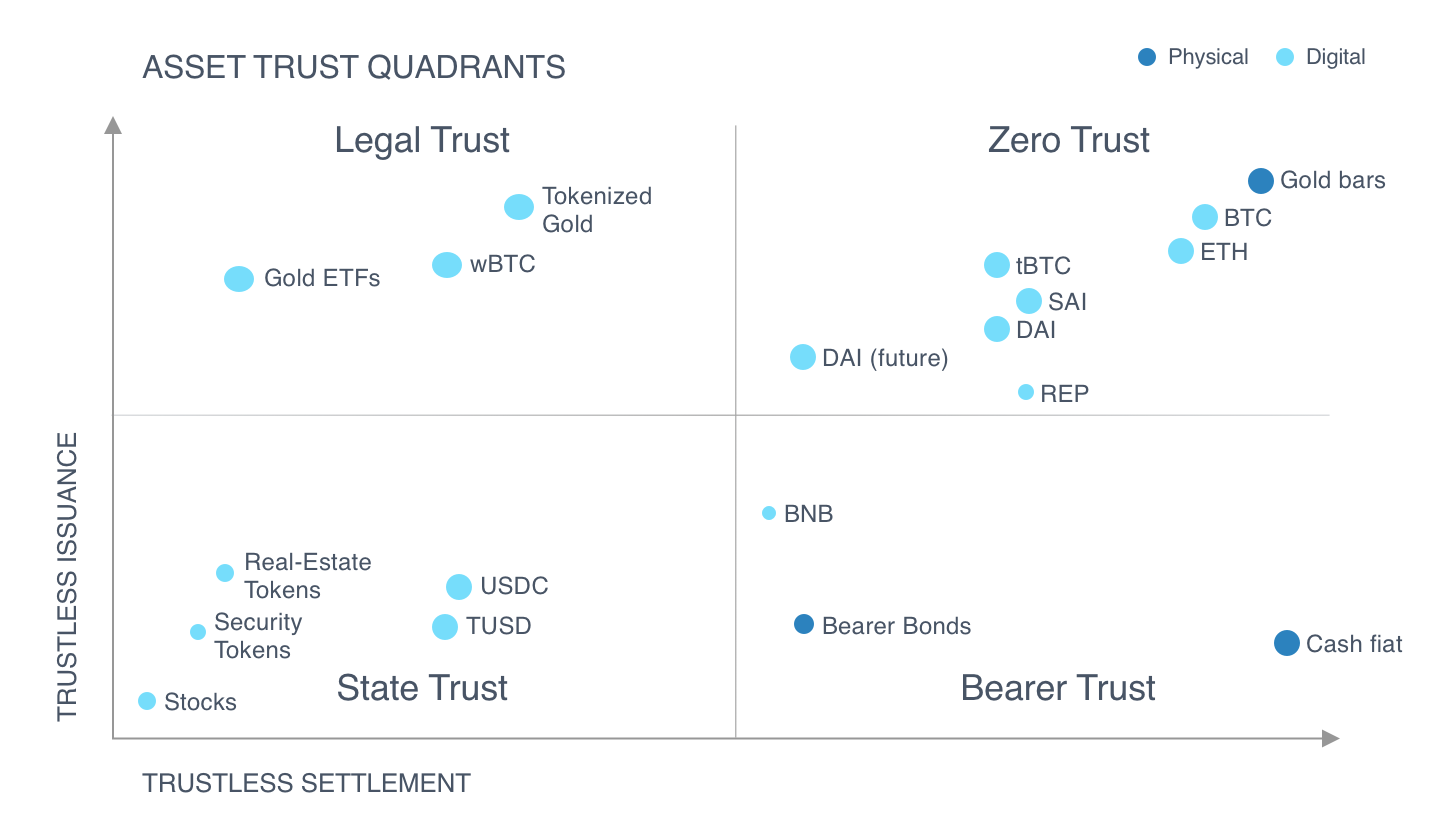

Stablecoin with no counterparty risk

Flash loans

Uniswap, Lido, and OpenSea (the three largest Ethereum-based apps) now generate more monthly fees, on a combined basis, larger than the entire Ethereum L1

Real-world assets account for 57% of MakerDAO’s total protocol revenue, up from less than 10% in July

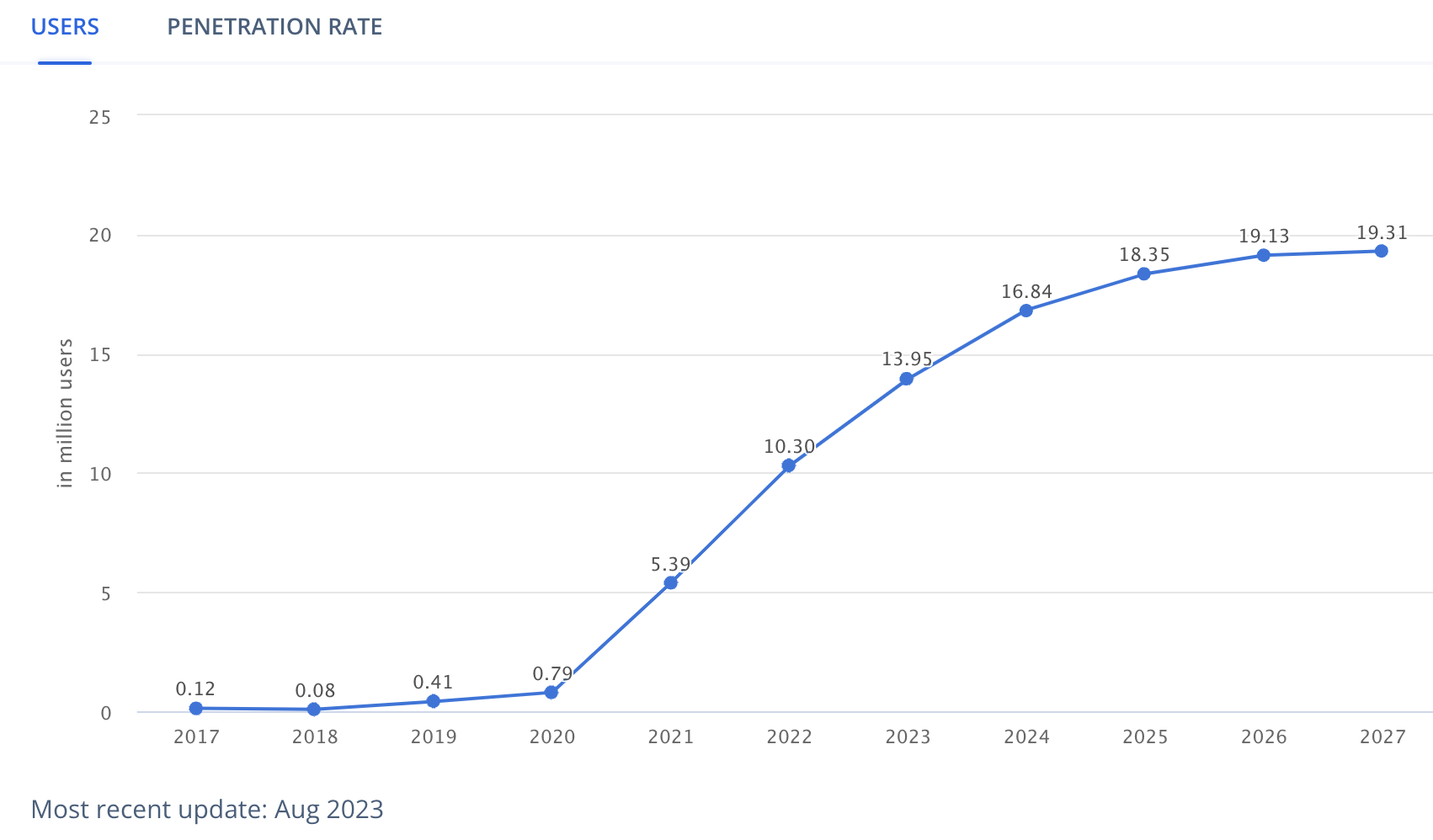

●5M active daily users - 40x growth in the last 2 years

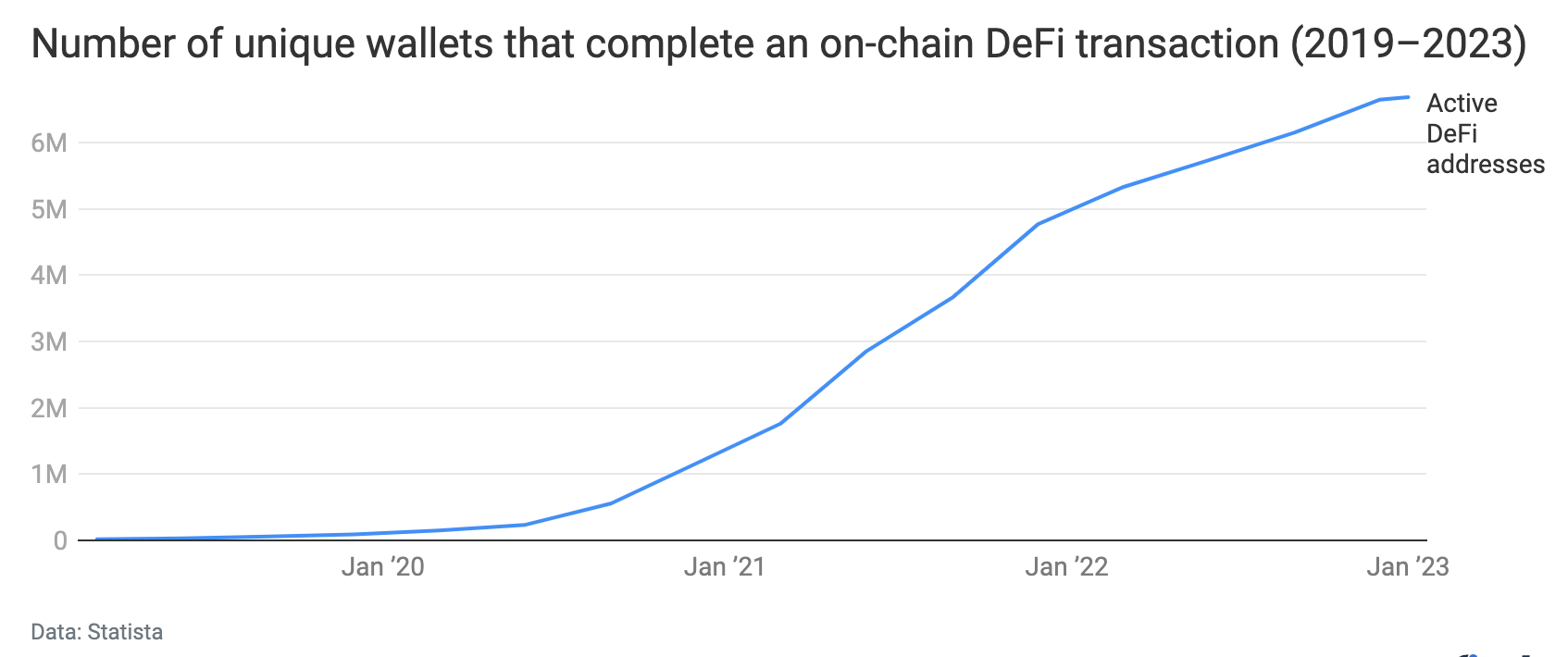

●100M users have self-hosted wallets

●TVL 5X growth in the last 2 years, despite the market meltdown

●Expected to 10X in the next 4 years, 20X in the next 10 years

●Partnerships like Paypal and Metamask will just further foster the adoption

●MiCA will “normalize” crypto assets from late 2024 and include them into the traditional financial services

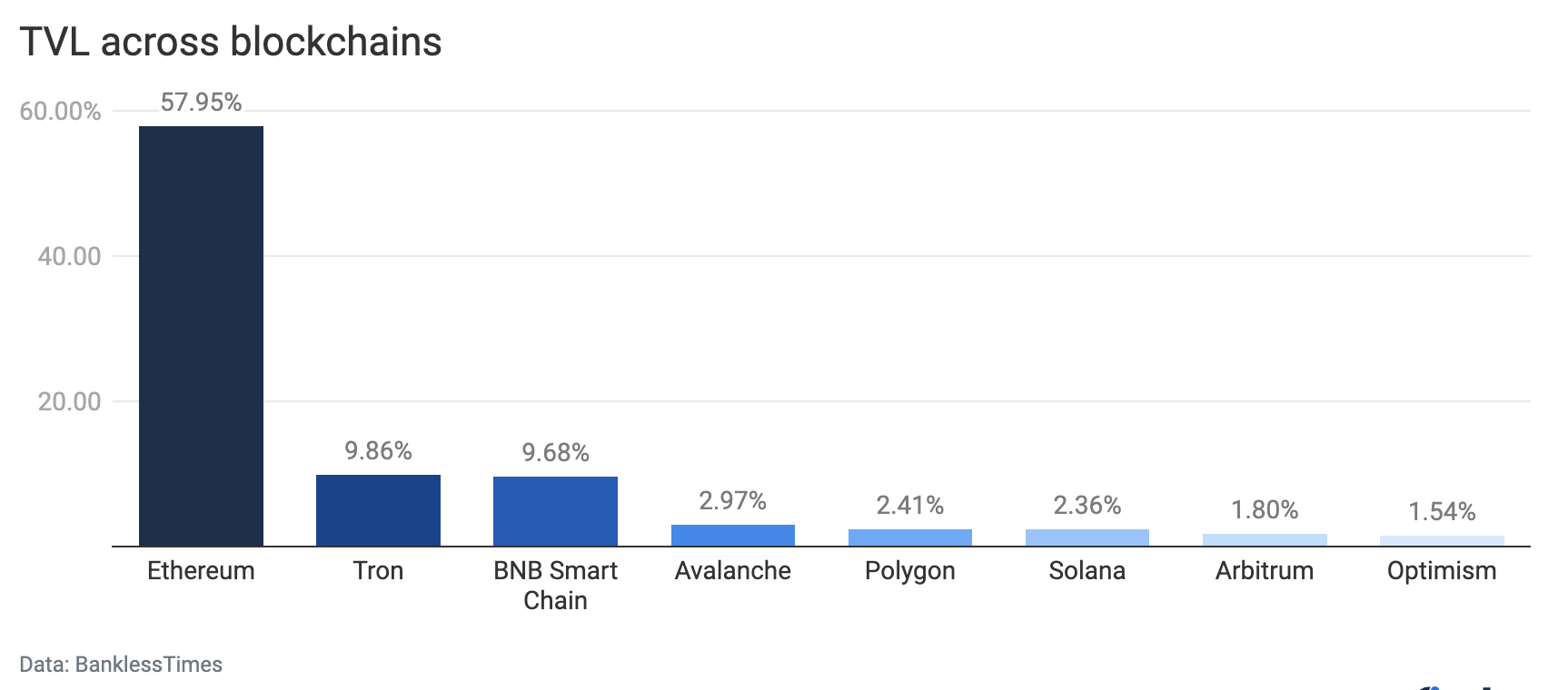

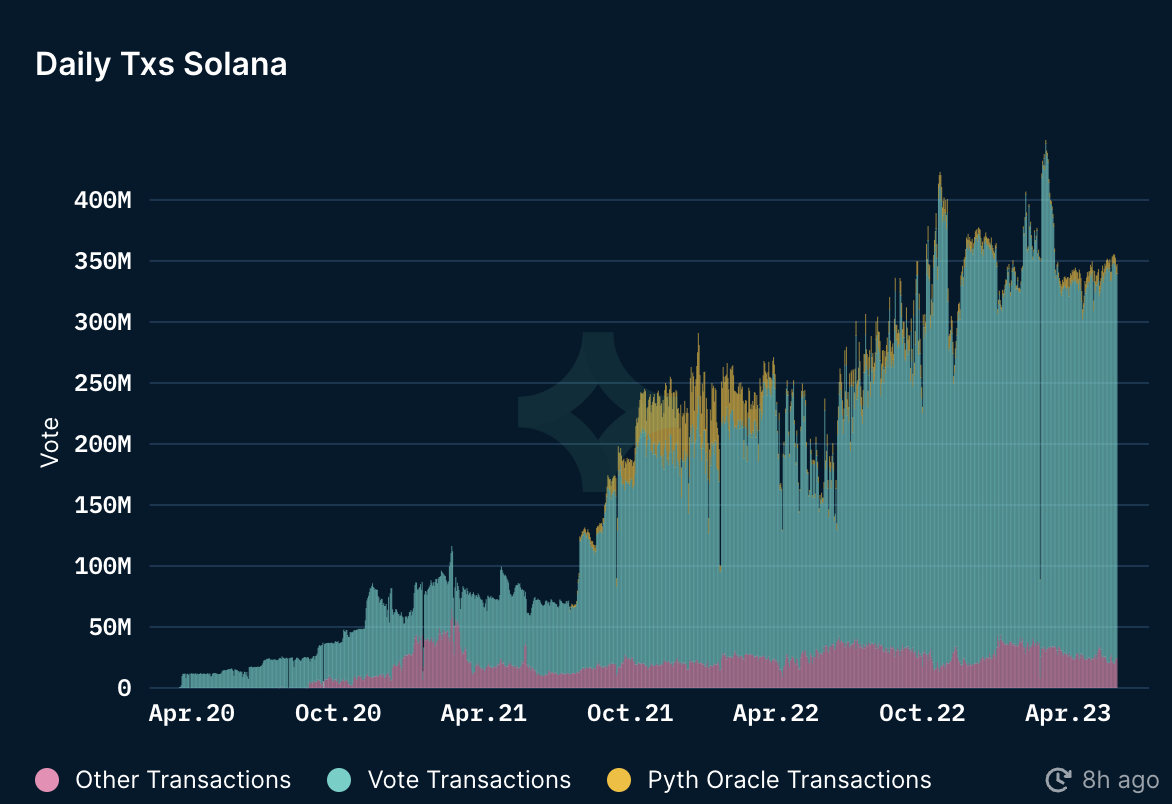

Solana lost the most TVL throughout 2022: Solana’s ecosystem lost 96% of its TVL in dollar terms in 2022. It started the year with $6.68 billion in its ecosystem and ended with $290 million.

The collapse of Alameda Research/FTX played a significant role in the collapse of the ecosystem due to how closely tied Sam Bankman-Fried was to it.

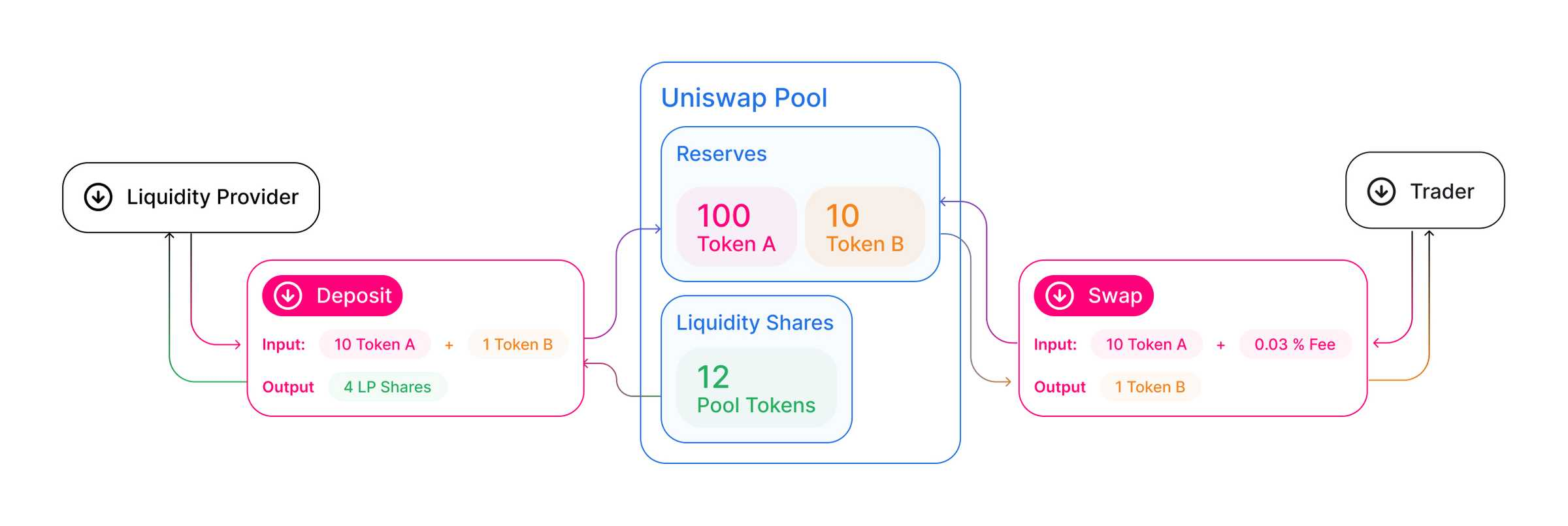

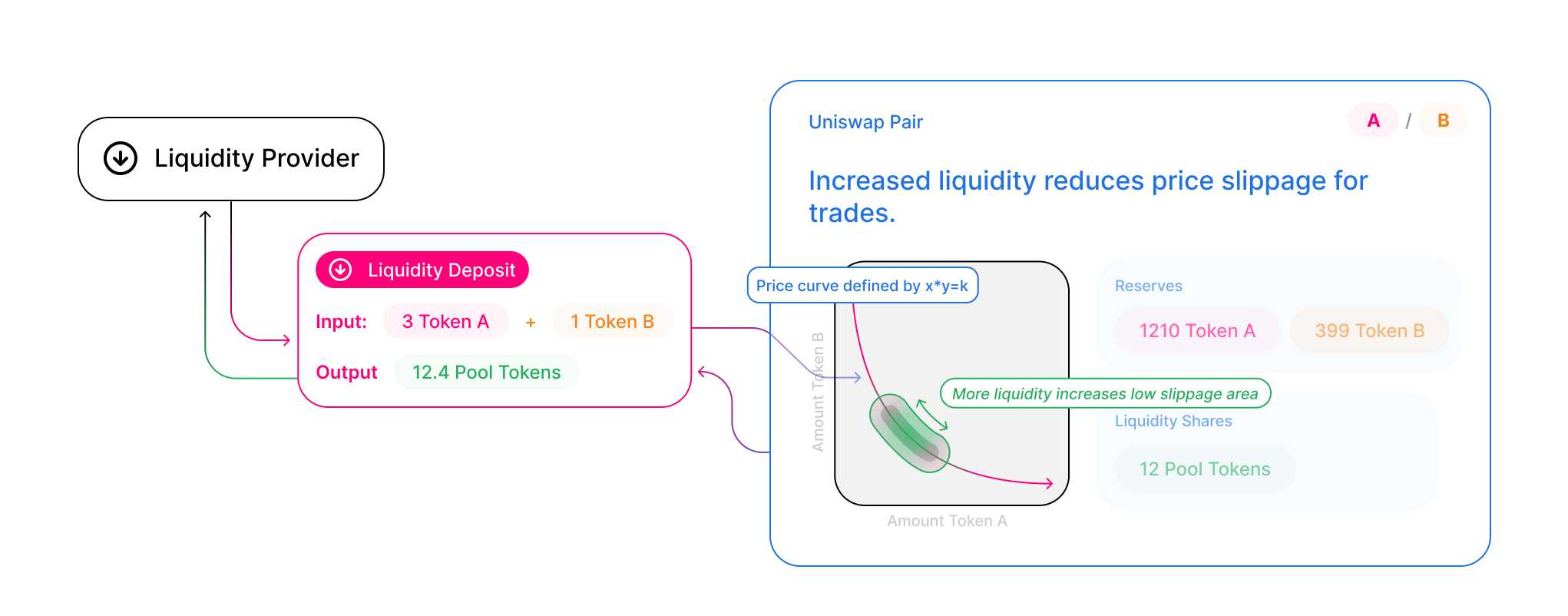

Uniswap is a fully decentralized on-chain protocol for token exchange on Ethereum that uses liquidity pools (AMM) instead of order books. Anyone can quickly swap between ETH and any ERC20 token or earn fees by supplying any amount of liquidity. And anyone can create a market (i.e., liquidity pool) by supplying an equal value of ETH and an ERC20 token.

Uniswap allows only one market per ERC20 token. The market creator sets the exchange rate, which shifts through trading due to Uniswap’s “constant product market maker” mechanism. When trading reduces one side of the pair’s liquidity relative to the other, the price changes. This creates arbitrage opportunities, encouraging more trading.

1. Deposit ETH to Metamask

2. Wrap ETH --> WETH (via Dai.makerdao.com)

3.Exchange it for PETH (pool eth), used for collateral

4. Create CDP (the loan)

5. Lock your PETH collateral

6. Mint new DAI (max. 60% of collateral)

7. Exchange DAI for ETH

8. Send ETH to any exchange and get EUR, BTC etc.

1. Get some ETH

2. Exchange it for DAI (which you owe) and MKR (for governance fee) on Oasis DEX

3. Return DAI to the smart contract and pay the fee in MKR

4. You cancel CDP smart contract

5. Unlock your PETH

6. Exchange PETH for WETH

7. Unwrap WETH --> ETH

8. You have your ETH back

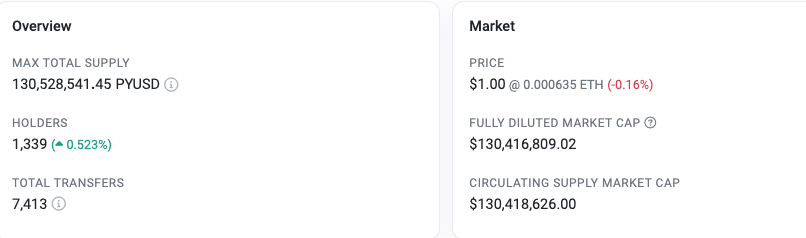

https://etherscan.io/token/0x6c3ea9036406852006290770bedfcaba0e23a0e8

1. https://delphidigital.io/

2. https://messari.io/

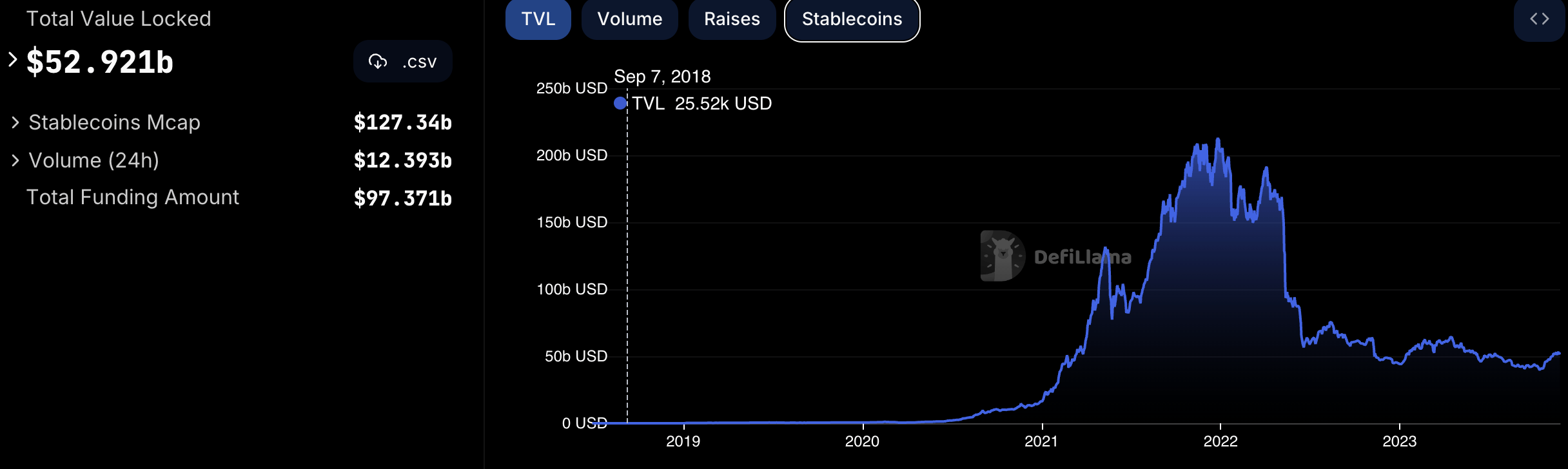

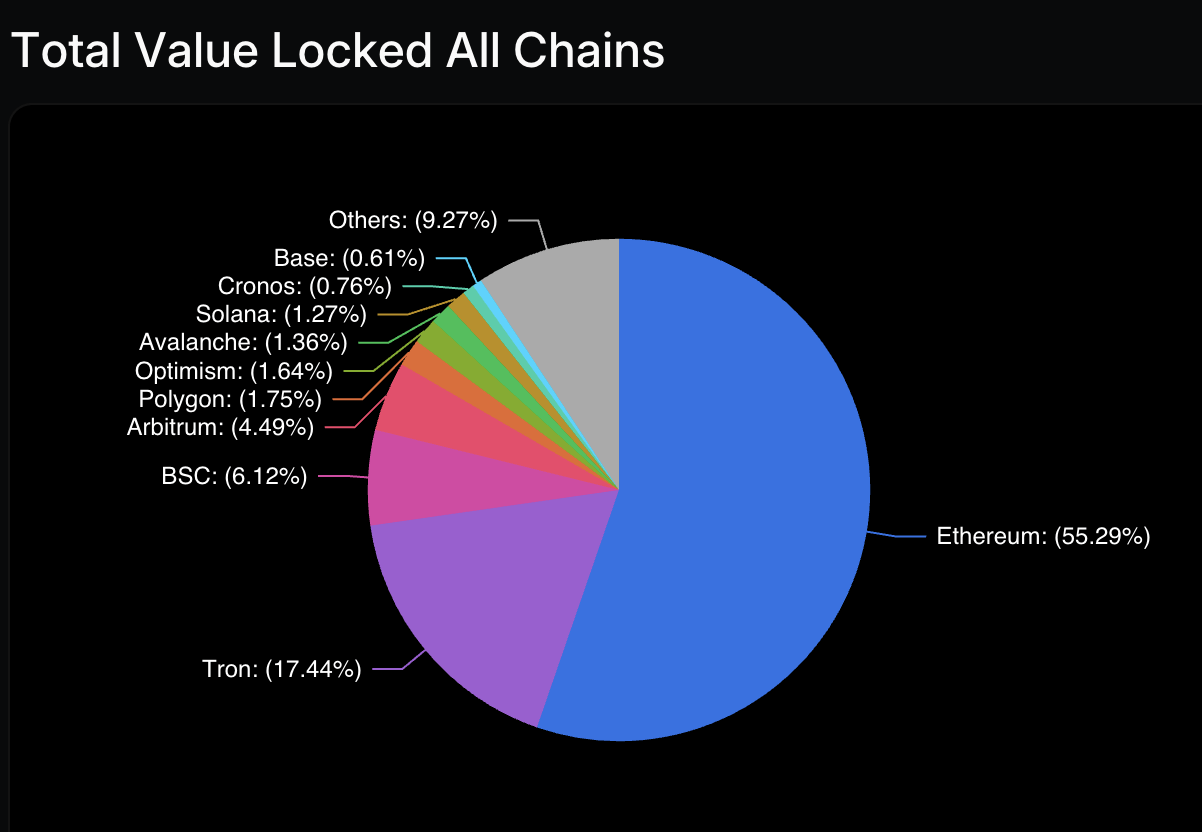

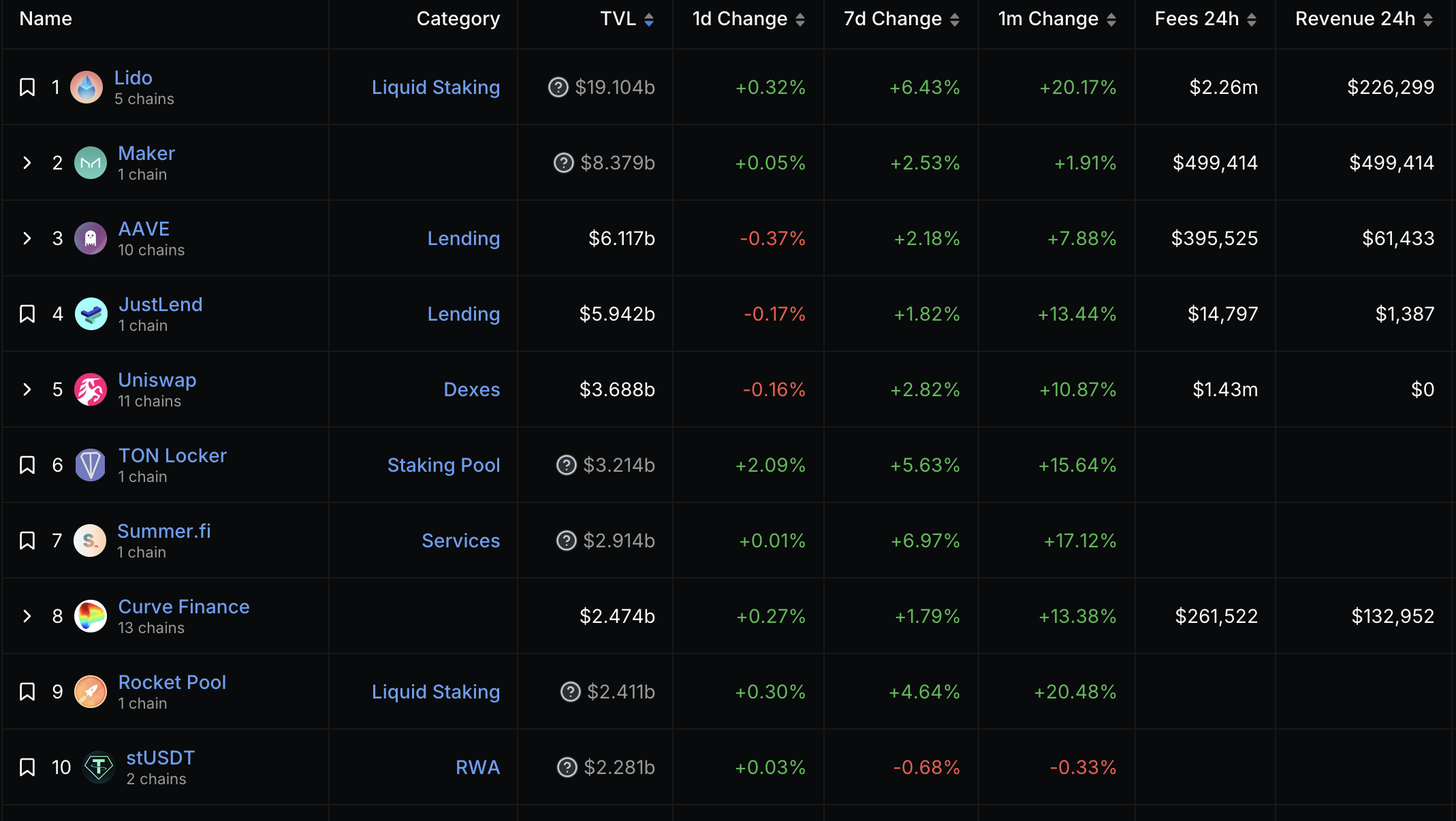

Key Data Sources for DeFi

3. https://defillama.com/

except for gas

Text

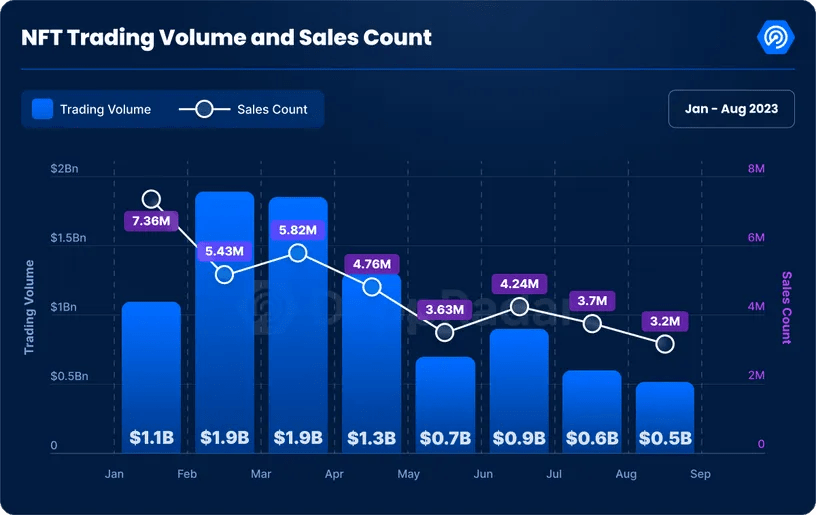

Bitcoin ordinals were launched in February and gained momentum in Q2, generating over $400 million in trading volume in May with a total sale count of 832,648. However, the hype seems to have subsided, with monthly volumes shrinking to less than $5 million as of mid August 2023.

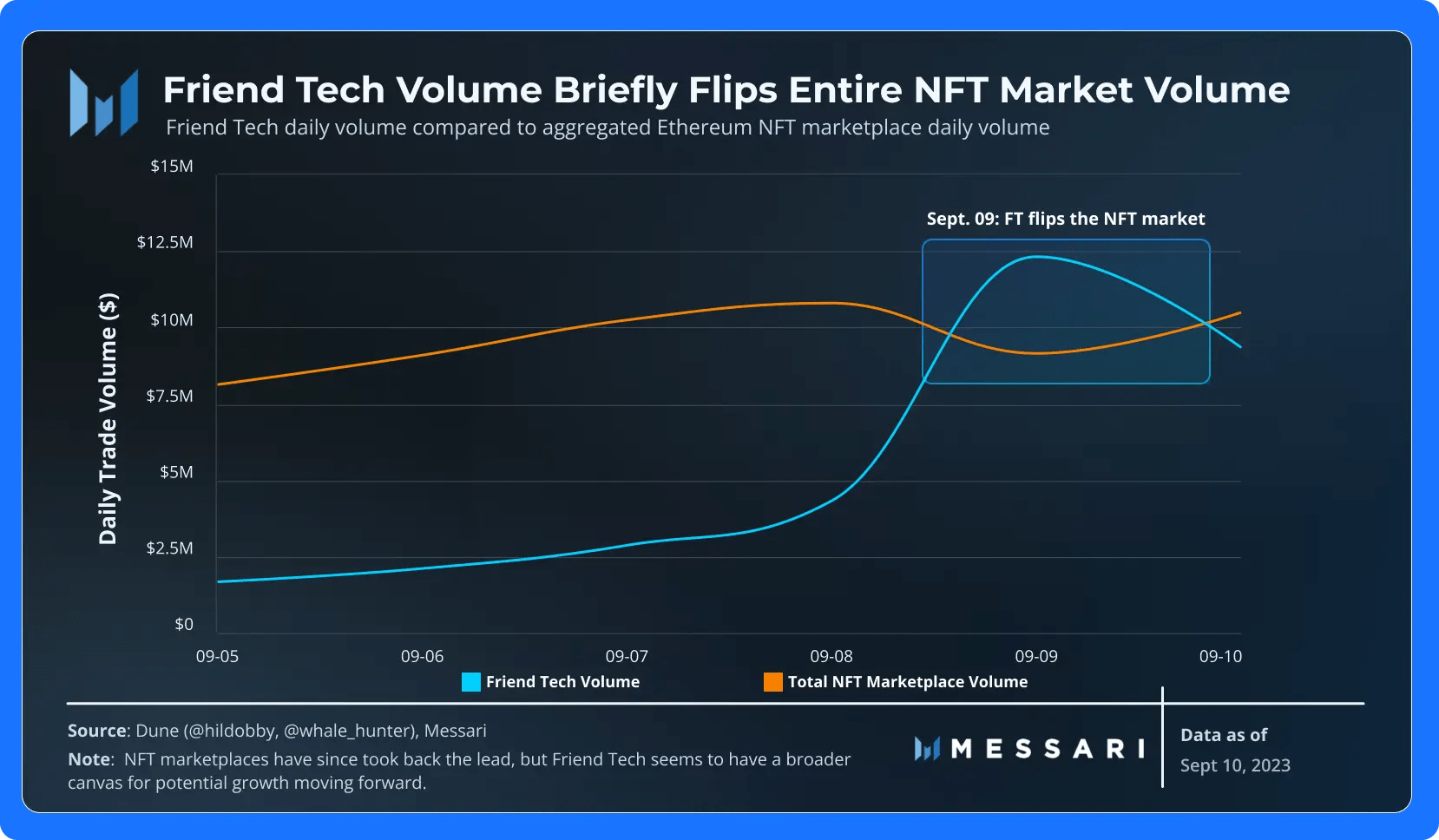

Friend.tech, an innovative social application, recently launched on Base, Coinbase's new Layer-2 solution. Friend.tech enables users to purchase shares of Twitter influencers, granting them exclusive access to private group chats with these social media personalities

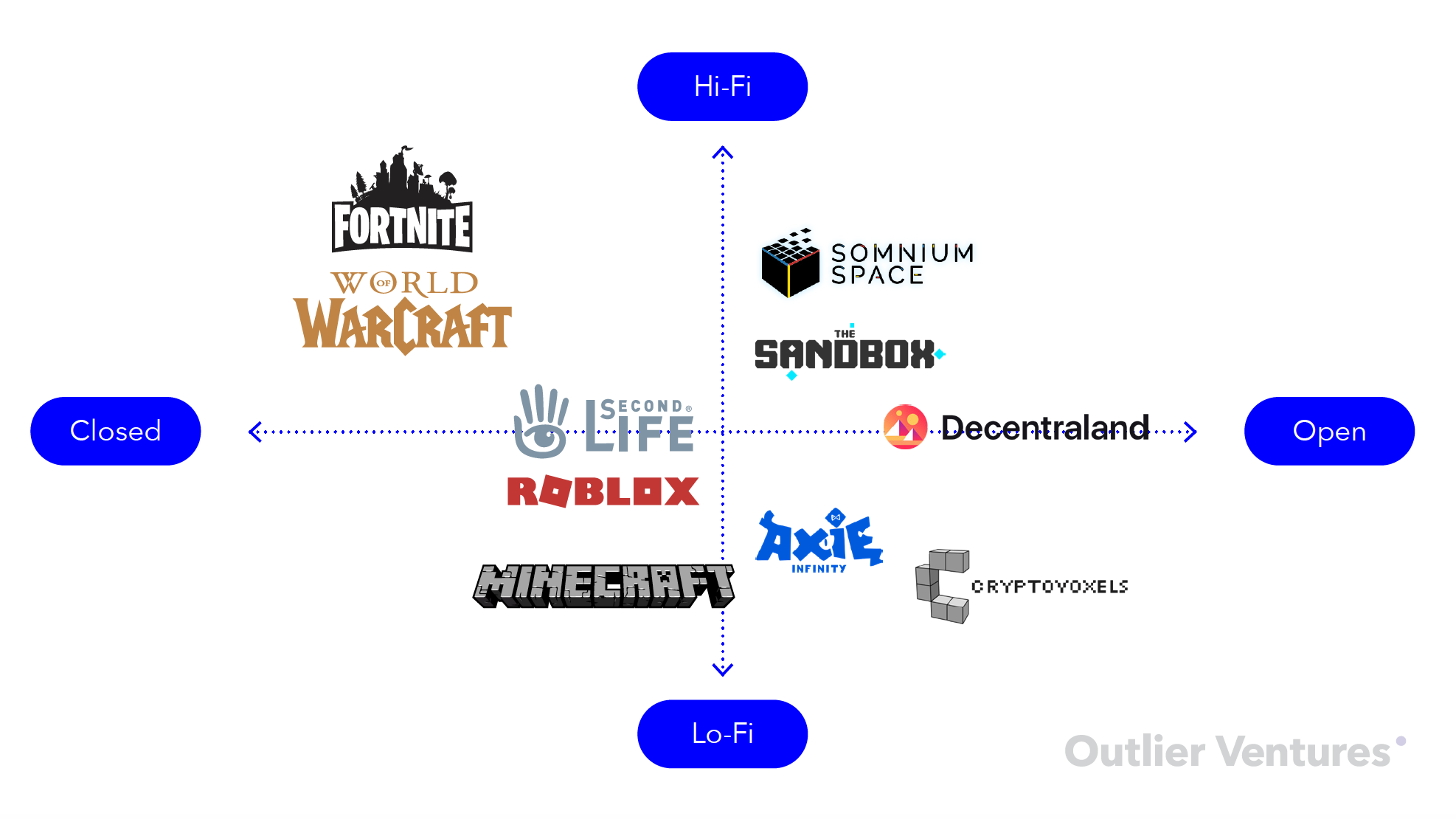

In the fourth quarter of 2020 and first quarter of 2021, the gaming industry had two of its largest-ever initial public offerings (IPOs) in Unity Technologies and Roblox Corporation, both of which wrapped their corporate histories and ambitions in Metaverse-related narratives.

Start in the 1970s with text-based virtual worlds known as Multi-User Dungeons. MUDs were effectively a software-based version of the role-playing game Dungeons & Dragons.

Using text-based commands that resembled human languages, players could interact with one another, explore a fictional world populated by non-playable characters and monsters, attain power-ups and knowledge, and eventually retrieve a magical chalice, defeat an evil wizard, or rescue a princess

Great leap came in 1986 with the release of the Commodore 64 online game Habitat, which was published by Lucasfilm, the production company founded by Star Wars creator George Lucas.

Habitat was described as “a multi-participant online virtual environment” and, in a reference to Gibson’s novel Neuromancer, “a cyberspace.”

“Citizens” of Habitat were in charge of the laws and expectations of their virtual world, and had to barter with each other for necessary resources and avoid being robbed or killed for their wares. This challenge led to periods of chaos, after which new rules, regulations, and authorities were established by the player community to maintain order

The 1990s saw no major “proto-Metaverse” games, but advances continued. That decade, millions of consumers took part in the first isometric 3D (also known as 2.5D) virtual worlds, which gave the illusion of three-dimensional space, but only allowed users to move across two axes.

Not long after, full 3D virtual worlds emerged. A number of games, such as 1994’s Web World and 1995’s Activeworlds, also empowered users to collaboratively build a visible virtual space in real time, rather than through asynchronous commands and votes

2007 - stock exchange was launched in Second Life

with the aim of helping Second Life–based companies raise capital using the platform’s Linden Dollars currency.

Throughout the 2010s, bands of users collaborated in Minecraft to build cities as large as Los Angeles—roughly 500 square miles.

One video game streamer, Aztter, constructed a stunning cyberpunk city out of an estimated 370 million Minecraft blocks, having worked an average of 16 hours per day for a year.

Fortnite’s social experiences -- its famous 2020 concert with Travis Scott. In that case, “players” converged on a much smaller portion of the map.

The title’s standard cap of 100 players per instance was halved, while many items and actions, such as building, are disabled, thereby further reducing the workload. While Epic Games can rightly say that more than 12.5 million people attended this live concert, these attendees were split across 250,000 separate copies (meaning, they watched 250,000 versions of Scott) of the event that didn’t even start at the same time.

EVE Online stands apart from games like World of Warcraft and Fortnite because all users are part of one singular and persistent realm.

Over the course of an average day in 2021, over 350 million people participated in a battle royale game—just one genre of high CCU game—and billions were able to do so. In 2016, only 350 million people in the world owned the equipment needed to render a rich 3D virtual world. At its peak in 2021, Roblox had 225 million monthly users

Roblox and Minecraft are among the most popular games in the world, their reach is modest when considered in the broadest terms. These two supposed titans have 30–55 million daily active users, a fraction of the global internet population of 4.5–5 billion. In effect, they are still at the ICQ stage of virtual words

Concurrency is one of the foundational problems for the Metaverse, and for a fundamental reason: it leads to exponential increases in how much data must be processed, rendered, and synchronized per unit of time.

Microsfot Flight Simulator -the most realistic and expansive consumer-grade simulation in history. Its map is over 500,000,000 square kilometers—just like the “real” planet earth—and includes two trillion uniquely rendered trees (not two trillion copy-and-pasted trees, or two trillion trees made up of a few dozen varieties), 1.5 billion buildings, and nearly every road, mountain, city, and airport across the world.

Microsfot Flight Simulator -the most realistic and expansive consumer-grade simulation in history. Its map is over 500,000,000 square kilometers—just like the “real” planet earth—and includes two trillion uniquely rendered trees (not two trillion copy-and-pasted trees, or two trillion trees made up of a few dozen varieties), 1.5 billion buildings, and nearly every road, mountain, city, and airport across the world.

Microsoft Flight Simulator aspires for every town to not just differ from one another, but to exist as they do in real life. And it doesn’t want to store 100 types of clouds and then tell a device which cloud to render and with what coloring; rather, it wants to say exactly what that cloud should look like.

By the end of 2021, Adopt Me!’s virtual world had been visited more than 30 billion times—more than fifteen times the average number of global tourism visits in 2019.

Furthermore, developers on Roblox, many of whom are also small teams with fewer than 30 members, have received more than $1 billion in payments from the platform.

By the end of 2021, Roblox had become the most valuable gaming company outside of China, worth nearly 50% more than storied gaming giants Activision Blizzard and Nintendo.

1. The Streaming Book by Matthew Ball, freely online

2. The Metaverse Book, and Blog by Matthew Ball

3. Virtual Economy by L'Atelier

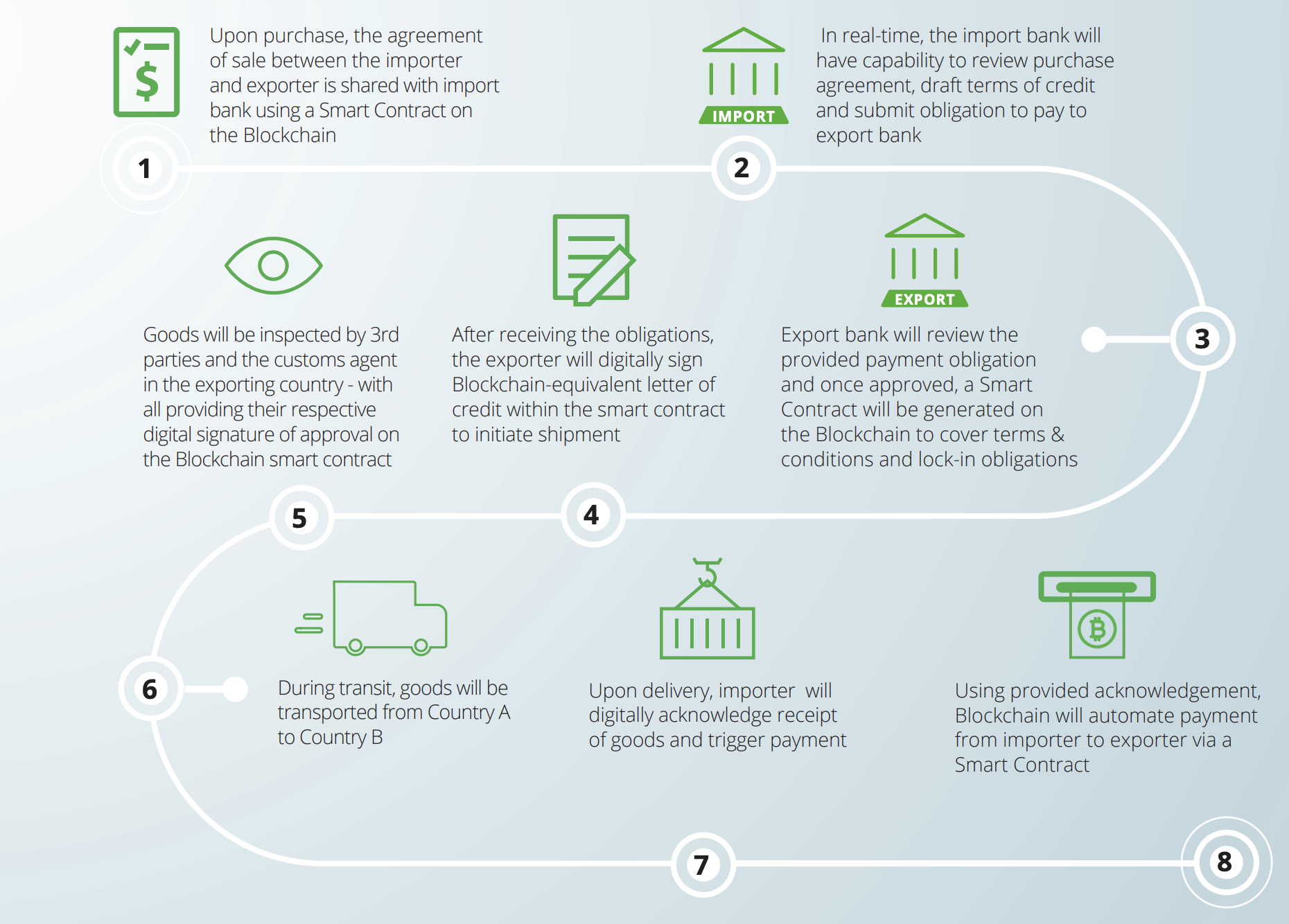

In March 2017 a group of 30 enterprises announced formation of Ethereum Enterprise Alliance, which has recently grown to more than 200 members, making it probably the largest blockchain consortium today.

EEA’s focus in bringing Ethereum to the enterprise environment, meaning moving from a public, permissionless to a private, permissioned setting, which means it will be easier to provide better support for privacy and performance. There are some plans to support anchoring on the public Ethereum network as a way to securely timestamp the chain state.

https://etherisc.com/

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/grid/trade-finance-placemat.pdf

September 2018, fifteen of the world’s largest banking and commodity companies announced the formation of komgo - a global blockchain-based trade financing platform.

Collaboration between: ABN AMRO, BNP Paribas, Citi, Crédit Agricole Group, Gunvor, ING, Koch Supply & Trading, Macquarie, Mercuria, MUFG Bank, Natixis, Rabobank, Shell, SGS and Société Génerale

While using ETHEREUM, it will launch with two initial products: a KYC process and a Letters of Credit product.

https://media.consensys.net/enterprise-blockchain-for-trade-financing-c005ec8fa079

Fraudsters contact investors in BTC investment schemes. As part of the scam, the so-called investment managers claim to have made millions of dollars investing in Bitcoin and promise their victims that they will profit as well.

To get started, the scammers want a charge. The Scammers then steal the upfront payments instead of making money. Scammers may also ask for personal identity information under the guise of transferring or depositing payments and gaining access to a person's crypto. Another sort of crypto scam is the use of phony celebrity endorsements.

Scammers offer to equal or multiply the cryptocurrency transferred to them. Their messages can create a sense of legitimacy and urgency. This seemingly 'once-in-a-lifetime chance may entice people to send assets immediately in hopes of a quick return.

They often use impersonation techniques and fake Social Media Accounts (Twitter, FB, Youtube, IG) of companies or Famous Personalities

This method includes sending links to files containing virus to the victims which get their PCs locked afterwards.

The attackers demand ransom to send decrypting keys.

Other ransomware may include keyloggers that log passwords of the victims when they sign into different crypto services, or that just replace crypto addresses of the victims with the ones of the attacker.

Crypto phishing scams have been around for a while and are still prevalent. In order to collect personal information, scammers send emails containing harmful links to phony websites.

Victims sing transactions that give permissions to the fraudulent smart contracts to transfer their crypto, e.g. ERC20 tokens.

Involve investment in a new project, NFTs, or coin in order to obtain money. Scammers steal money and then vanish with it. Because the code for these investments prevents customers from selling Bitcoin after they purchase it, they are left with a useless investment.

Sometimes hard to recognize as it may appear that developers just left the project (and new ones will maybe take over).

Similar like Rug Pull. The attackers create a new project with a liquid coin, commission a market maker, or coordinate with some entities with bigger capital to pump the price of the coin on some low liquidity exchange. When the investors start to buy in, the creator sell all their stash and leave.

otázky?

stanceldavid.sk

By David Stancel

NBS