Building your algo setup in a day

By: Sumit Raj

About Me:

- Techie | Author | Trainer | Mentor | Startups

- Working as Principal Engineer at Unacademy

- Authored internationally published book "Building Chatbots with Python", translated in Portuguese, Korean & Chinese.

- Avid Quora writer: Over 1.6 million views so far.

- Still learning to trade.

Problem

- Not being able to take quick action

- Emotions play

- Strategies needs more time

- Seamless execution

- Cost and Productivity

Challenge

- I know the strategy

- I have manually backtested it or got it backtested.

- I can write the pseudo code, may be using Chartink or TradingView using an interface

- But I don't know how to automate or I can't sit all day in front of the system

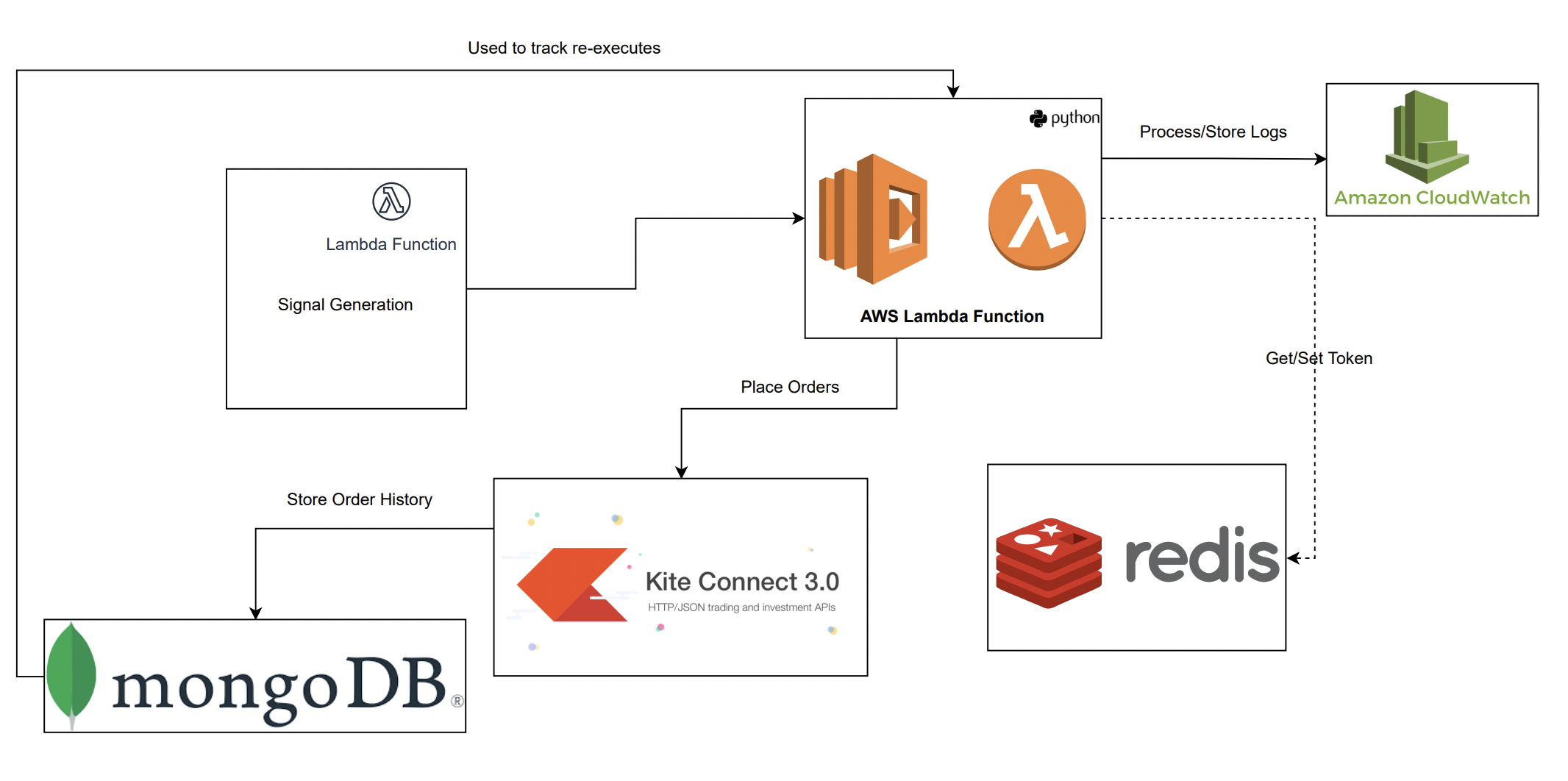

Serverless Solution

What is serverless?

- Serverless architectures doesn't mean there are no servers.

- 3rd-party "Backend as a Service" (BaaS) services or "Functions as a Service" (FaaS) platform

- Removes the need for a traditional always-on server like EC2 or VMs.

- No out of memory error unless you already know how much you needed.

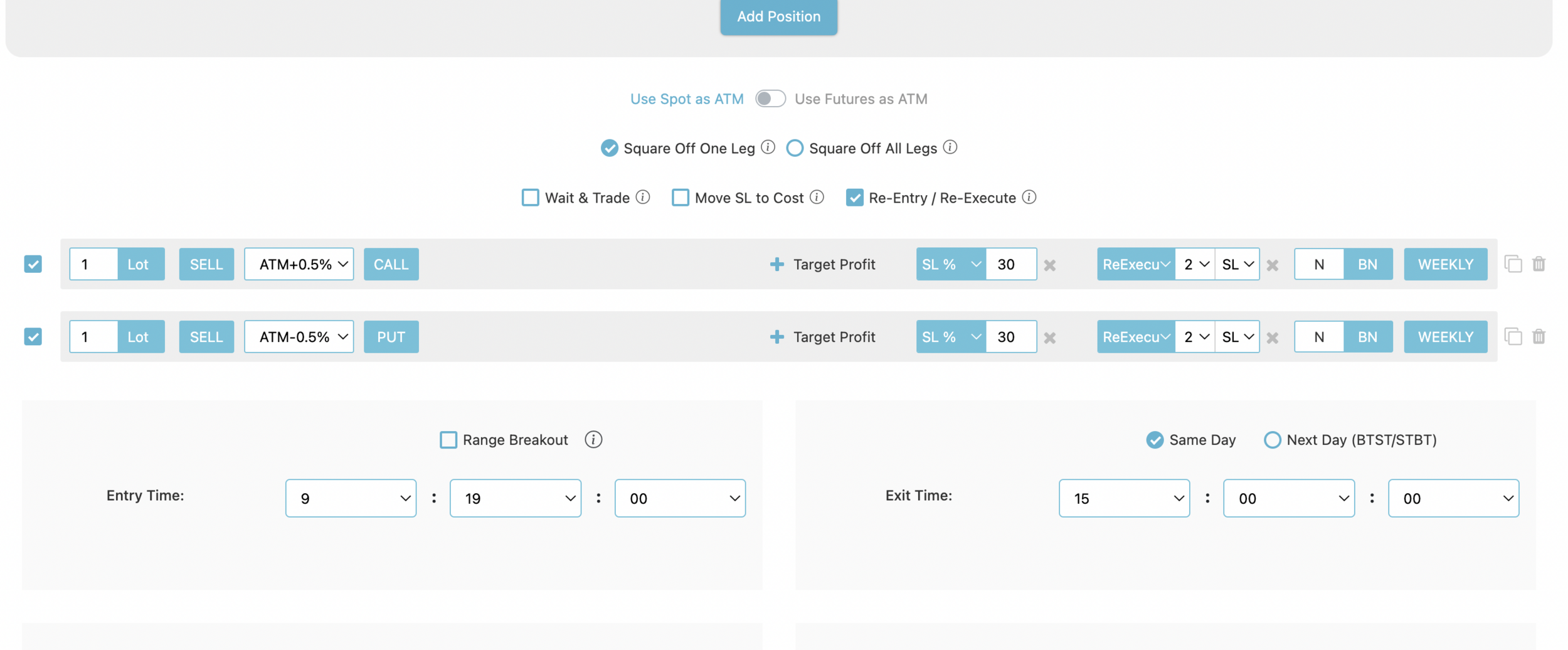

The Strategy

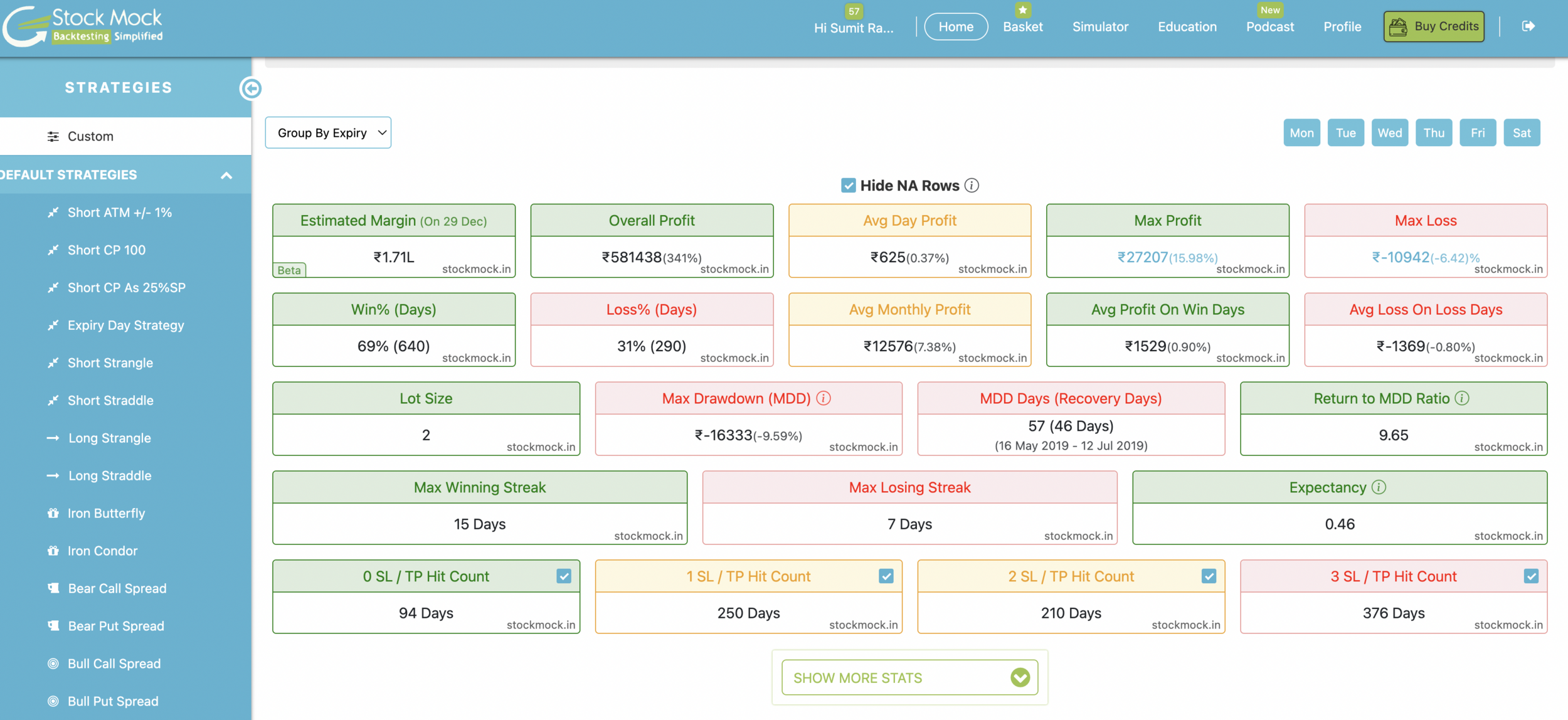

Backtested results on StockMock

Rule 1:

Short ( ATM + 0.5 % CE and ATM - 0.5 % PE ) with 30% SL

Rule 2:

Entry at 9:19 AM and exit at 15:00pm

Rule 3:

If SL triggers for anyone of the leg (CE or PE) THEN

For that particular leg (CE or PE) re-execute logic ( i.e short ATM + 0.5 % CE or ATM - 0.5 %PE ) the next minute.

Re-execute can be done max for 2 times each leg (CE or PE ) if SL Triggers.

Rule 4:

Let's dive into code

Rule 1: Part - I

def get_ltp(symbol):

url = f"https://api.kite.trade/quote/ltp?i={symbol}"

response = requests.request("GET", url, headers=headers, data={}).json()

ltp = response["data"][symbol]["last_price"]

return ltp

def get_atm_strikes(strike_list, symbol):

"""

Gets the ATM+0.5% strike for CE and ATM-0.5% strike for PE

"""

ltp = get_ltp(symbol)

atm_strike_ce = closest(strike_list, ltp * 1.005) #ATM + 0.5% for CE

atm_strike_pe = closest(strike_list, ltp * 0.995) #ATM + 0.5% for PE

data = [

{"strike_price": atm_strike_ce, "type": "CE"},

{"strike_price": atm_strike_pe, "type": "PE"}

]

return datasl = ltp * 1.3

#Place SL-M order

order_obj = place_order(tradingsymbol, qty, "BUY", order_type='SL-M',

trigger_price=sl)

order_id = order_obj['data']['order_id']

orders.append({'inst_type': inst_type, 'tradingsymbol': tradingsymbol, 'qty': qty,

'order_id': order_id, 'sl': sl, 'sl_hit': False})Rule 1: Part - II

Rule 2

if datetime.time(9, 19) < current_time.time() < datetime.time(15, 0): #Rule 2

Rule 3

def is_sl_hit(order_id):

# if order_id == "382270196720590":

# return True

# else:

# return False

return order_status(order_id) == 'COMPLETE'Rule 4

sl_hit_thresold = 2 #Rule 4

count_of_sl = len(get_data({"inst_type": it, "sl_hit": True}))

if count_of_sl < sl_hit_thresold:

sl_not_hit = get_data({"inst_type": it, "sl_hit": False}, {"order_id": 1})

order_id = sl_not_hit[0]['order_id']Utility Methods

def get_data(query={}, project={"_id": 0}):

data = db['tradelog'].find(query, project)

return list(data)

def update_data(query, data):

data.update({"modified_at": dt.now()})

newvalues = { "$set": data }

x = db['tradelog'].update_one(query, newvalues)

def insert_orders(orders):

print(orders, "orders list")

x = db['tradelog'].insert_many(orders)

return x.inserted_idsdef find_entry():

#Rule 1

inst = requests.get(instruments + '/NFO', headers=headers).text

df_fno = pd.read_csv(StringIO(inst))

df_options = df_fno[df_fno.segment == 'NFO-OPT']

df_bnf_only = df_options[(df_options.name.isin(['BANKNIFTY']))]

df_bnf_only = df_bnf_only[['instrument_token', 'tradingsymbol', 'expiry', 'strike',

'instrument_type', 'name']]

df = get_and_process_data(df_bnf_only, expiry_date)

atm_strikes_with_type = get_atm_strikes(df['strike'], f"NFO:{index_symbol}")

tradingsymbols = get_tradingsymbols(df, atm_strikes_with_type)

return tradingsymbolsdef exit_all_positions():

print("Exiting all positions at after cut off time")

sl_not_hit_by_3pm = get_data({"sl_hit": False}, {"order_id": 1,

"tradingsymbol": 1, "qty": 1})

for t in sl_not_hit_by_3pm:

print(t['tradingsymbol'], t['qty'], "BUY")

place_order(t['tradingsymbol'], t['qty'], "BUY")Utility Methods

def order_status(order_id):

url = f"https://api.kite.trade/orders/{order_id}"

payload={}

response = requests.request("GET", url, headers=headers, data=payload)

return response.json()['data']['status'] #list of ordersCost Perspective

- 1M free requests per month and 400,000 GB-seconds of compute time per month for AWS Lambda

| Price | |

|---|---|

| Requests | $0.20 per 1M requests |

| Duration | $0.0000166667 for every GB-second |

Average trading days: 21 * 6 hour/day = 126 hours

Average runtime: 800 ms ~1sec

126 hours= 126*3600 = 4,53,600 seconds

(126*3600*128)/1024 = 56,700 GB-seconds

56,700 GB-s - 400000 free tier GB-s = -343,300.00 GB-s

Lambda costs - With Free Tier (monthly): 0.00 USD

Let's do the maths

| Number of Requests (per month) | Price (per million) |

|---|---|

| First 300 million | $1.00 |

| 300+ million | $0.90 |

- Amazon API Gateway free tier includes one million API calls per month for up to 12 months.

- 5GB Data (ingestion, archive storage, and data scanned by Logs Insights queries)

- $1.00 per million events

Productivity and Maintenance

Perspective

- Setup cronjob with click of a button

- Logging is a piece of cake

- Search logs for history of your executions

- Stopping execution using Throttle

- Setup once and use forever

Why choose Serverless Lambda over EC2?

- Highly reduced operational cost

- Less complex to manage compared to VMs

- Faster development time and productivity

- Near zero maintenance

Questions?

Telegram:

Twitter:

Phone:

Email:

StockMock Podcast

By sumit12dec