Health Care Reform: The Affordable Care Act and Beyond

BE 608

States: How are they preventing death spirals, reducing adverse selection or improving moral hazard?

Goals of the ACA

•Expand insurance coverage

•Reduce the growth of health spending

•Strengthen quality incentives

Builds on the existing system of private insurance.

Outline

•Pre-ACA Insurance Coverage Patterns

•Overview of ACA Coverage Provisions

•Early Evidence on Coverage Gains

•Marketplace Performance

•Implications for Patients and Providers

•Implications for the Labor Market

•Looking Forward

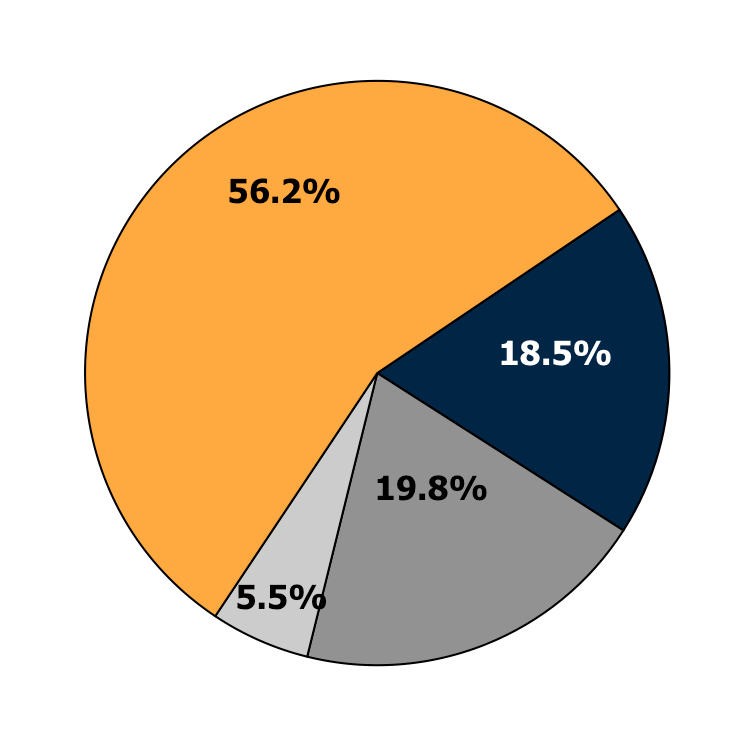

What was Coverage Like Before the ACA?

Employer-Sponsored

Health Insurance

Private Non-Group

Medicaid or other

public programs

Uninsured

Source: 2011 CPS ASEC, Non-Elderly Only

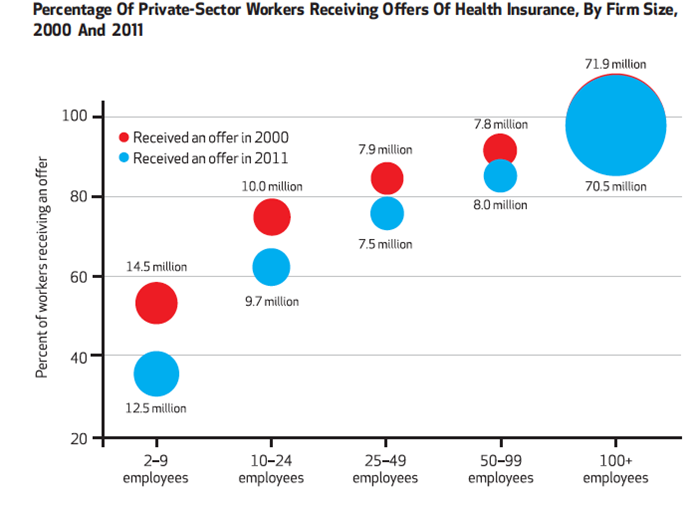

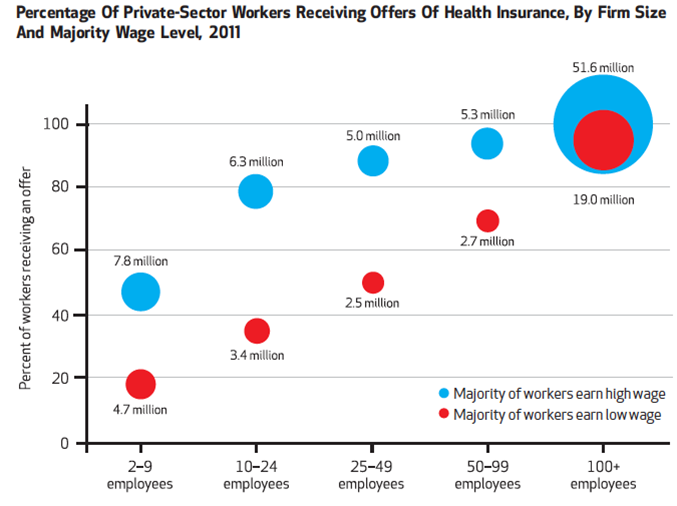

Why is employer sponsored health insurance so popular?

•Should ask: Why do (some) workers prefer to pay for ESI with reduced wages?

•Answer: ESI is a much better deal than individually-purchased coverage. There are three main reasons:

1.Efficient risk-pooling

2.Economies of scale in marketing and administration

3. Substantial tax subsidy

Advantages of ESI are the mirror image of the limitations of the existing individual market.

Employer Sponsored Health Insurance

Source: Buchmueller, Carey and Levy Health Affairs 2013

Employer Sponsored Health Insurance

Source: Buchmueller, Carey and Levy Health Affairs 2013

Employer Sponsored Health Insurance

Employer Health Insurance and the Labor Market

The link between health insurance and the workplace (and the lack of other affordable options) can distort worker behavior. The result is various types of “job-lock”:

- Job mobility

- Entrepreneurship

- Weekly hours

- Retirement

Broader labor market trends contributed to reduced access to ESI:

- Declining labor force participation

- Dislocation from technology and trade

- Declining unionization

- The “gig economy”

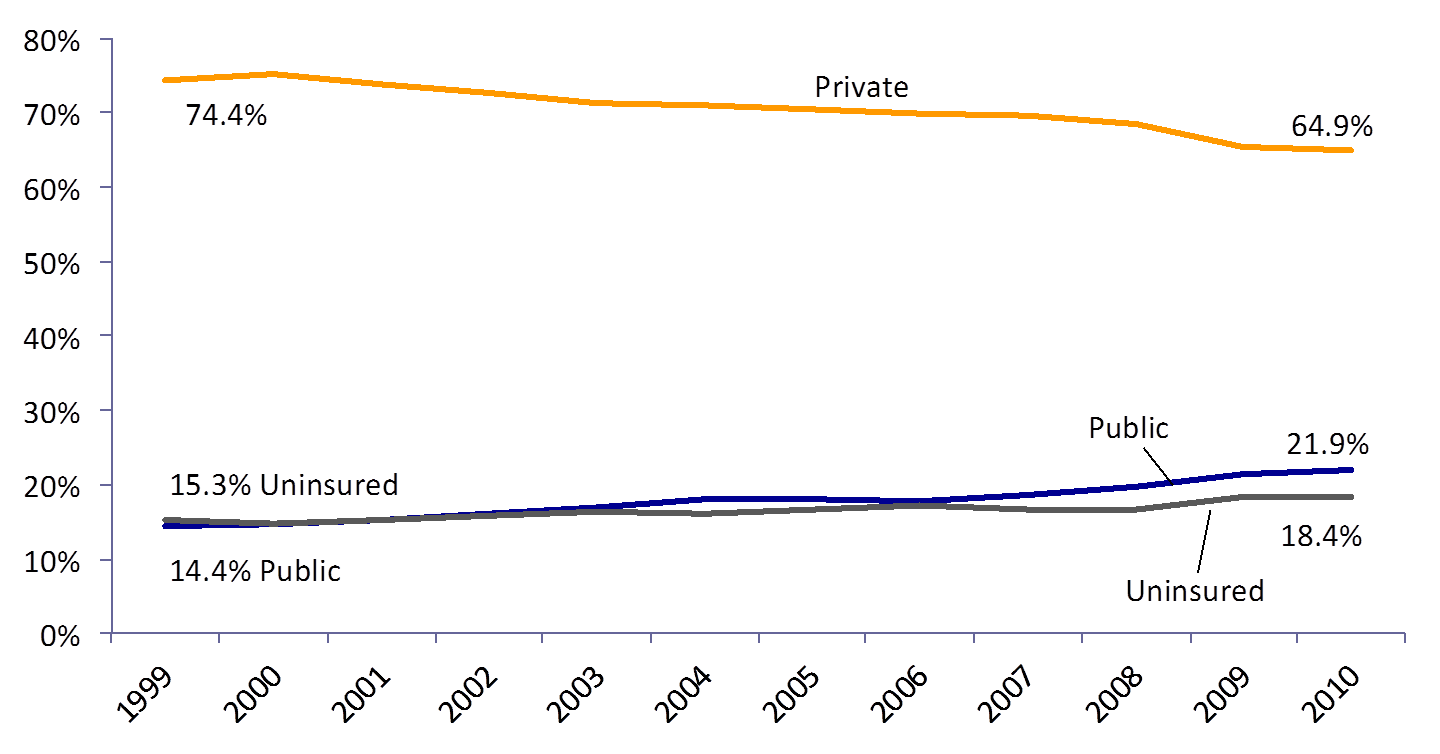

Declines in Coverage

Source: DeNavas-Walt et al. Income, Poverty and Health Insurance Coverage in the United States: 2011, US Census Bureau (2012)

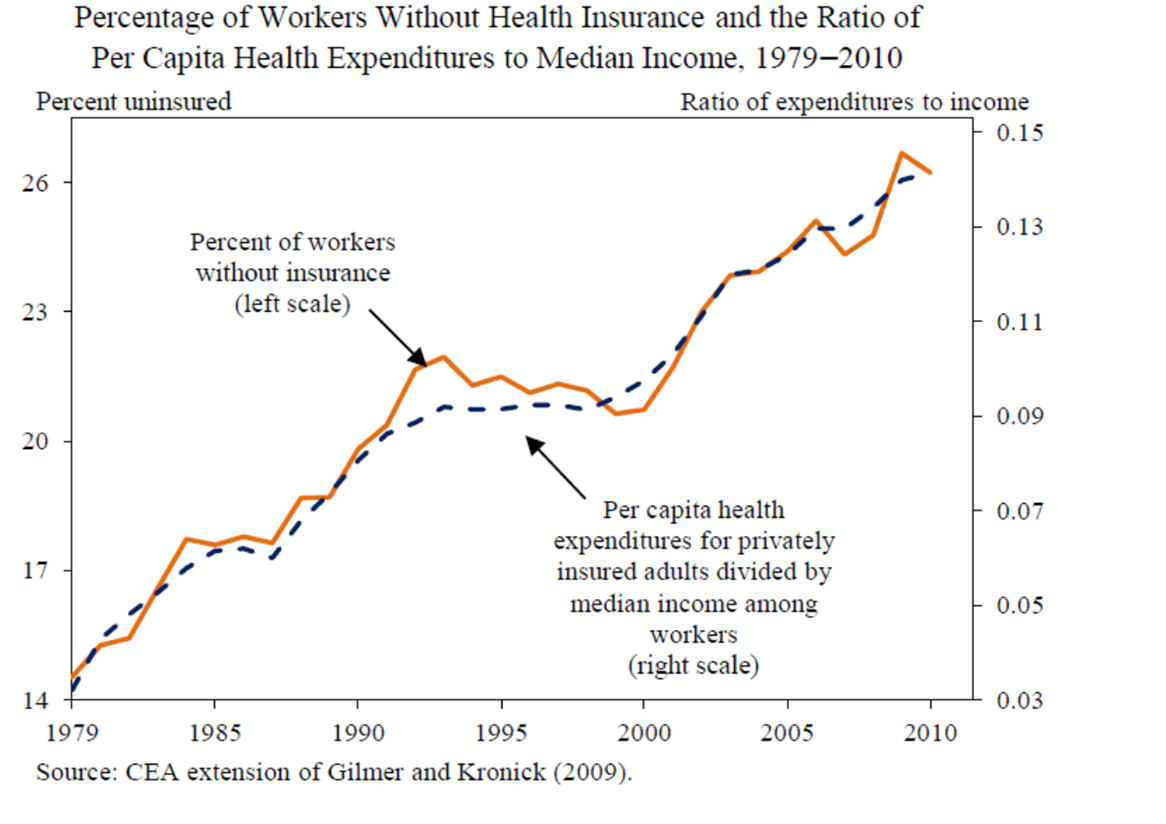

Cost Growth Drove Declines in Coverage

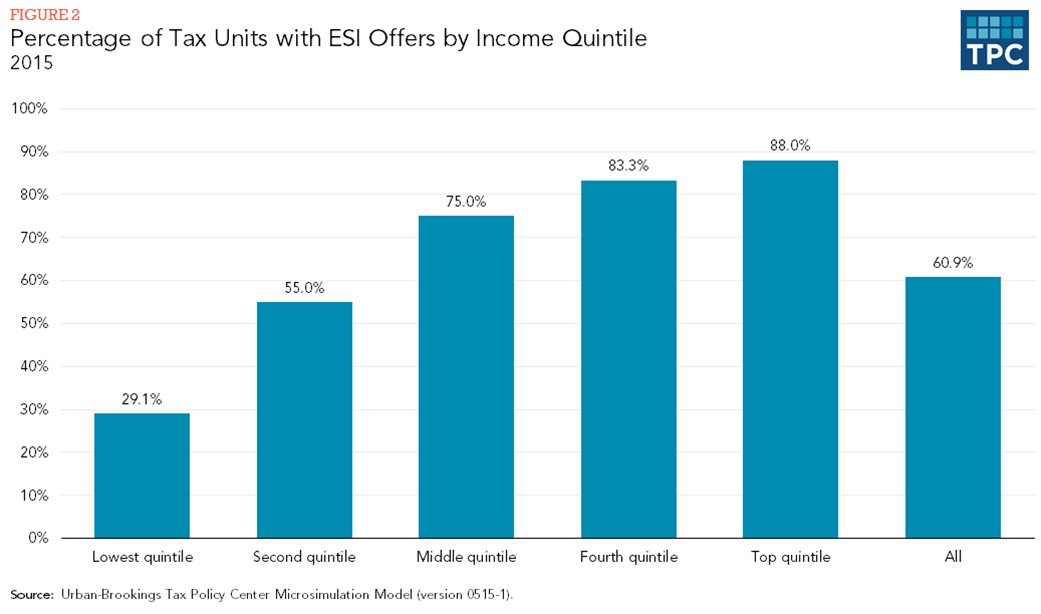

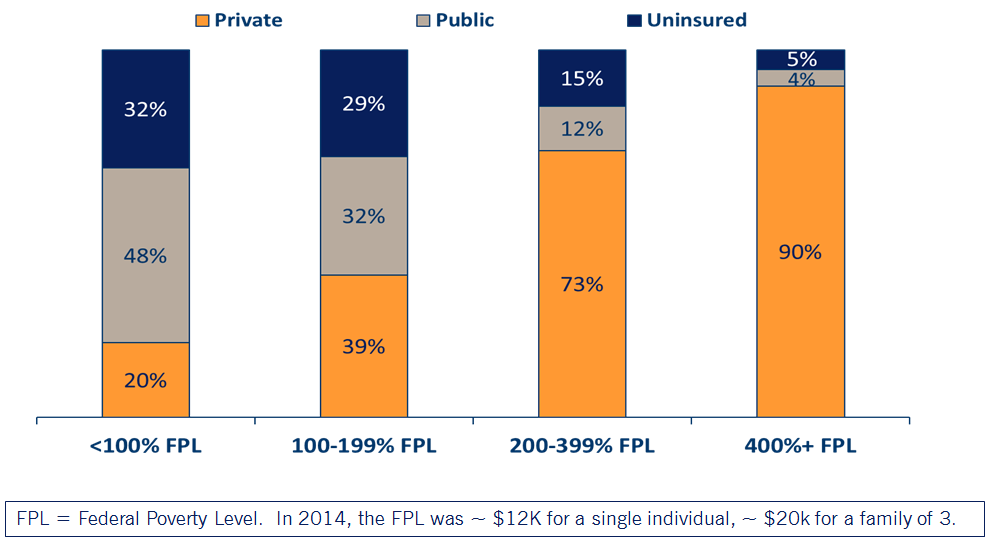

Health Insurance by Income Level

ACA Coverage Provisions

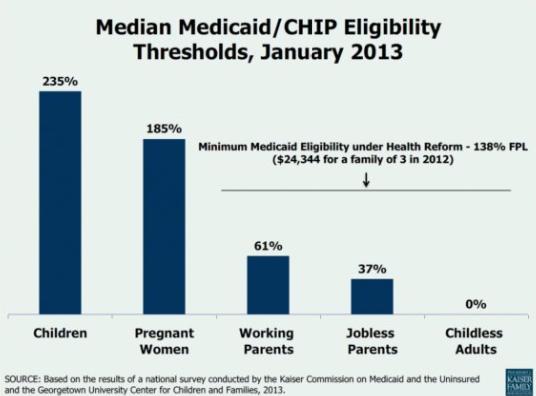

Poverty Line Cheat Sheet

| # in Family | 100% | 138% | 250% | 400% |

|---|---|---|---|---|

| 1 | $12,060 | $16,643 | $30,150 | $48,240 |

| 2 | $16,240 | $22,411 | $40,600 | $64,960 |

| 3 | $20,420 | $28,180 | $51,050 | $81,680 |

| 4 | $24,600 | $33,948 | $61,500 | $94,400 |

ACA Expanded Coverage in 3 Ways

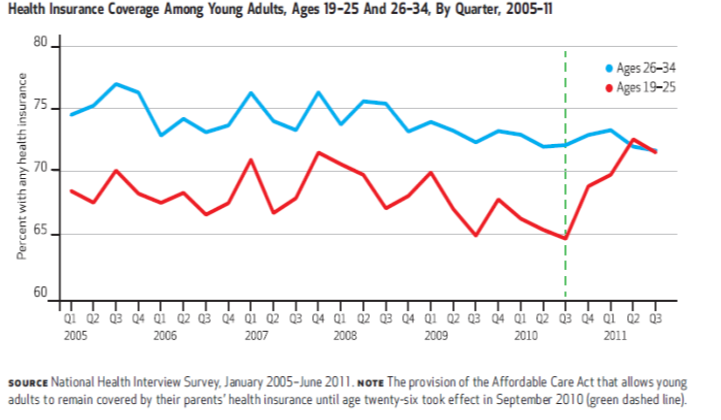

1.Young adults allowed to stay on their parents’ private insurance until age 26 (effective September 2010)

2.Eligibility for Medicaid extended to everyone with incomes below 138% of the Federal Poverty Level (effective Jan 2014*)

3.New tax credits for private insurance for families between 100 and 400% of the Federal Poverty Level (effective Jan 2014)

* Several states elected to expand Medicaid at different times, or not at all!

Medicaid Expansion

Medicaid Expansion

How does the government plan to expand Medicaid?

- Federal match assistance percentage (FMAP): States were historically guaranteed at least a 1-to-1 match from federal government.

- Higher match rate for lower income states (highest is MS, 2.8 to 1 in 2015)

- Under ACA, federal government pays 100% of additional costs during 2014-2016, then phases down to 90% by 2020.

- Under the original law, states have to expand Medicaid or risk losing all of their funding

NFIB v Sibelius 2012

High profile supreme court case challenging constitutionality of the ACA:

SCOTUS ruled the threat of losing all Medicaid funding was unconstitutionally coercive, a "gun tot he head" as Roberts wrote in his majority opinion.

Because of this ruling, states could opt not to expand Medicaid without risking losing additional funding.

Also gave states some negotiating power to expand on their terms.

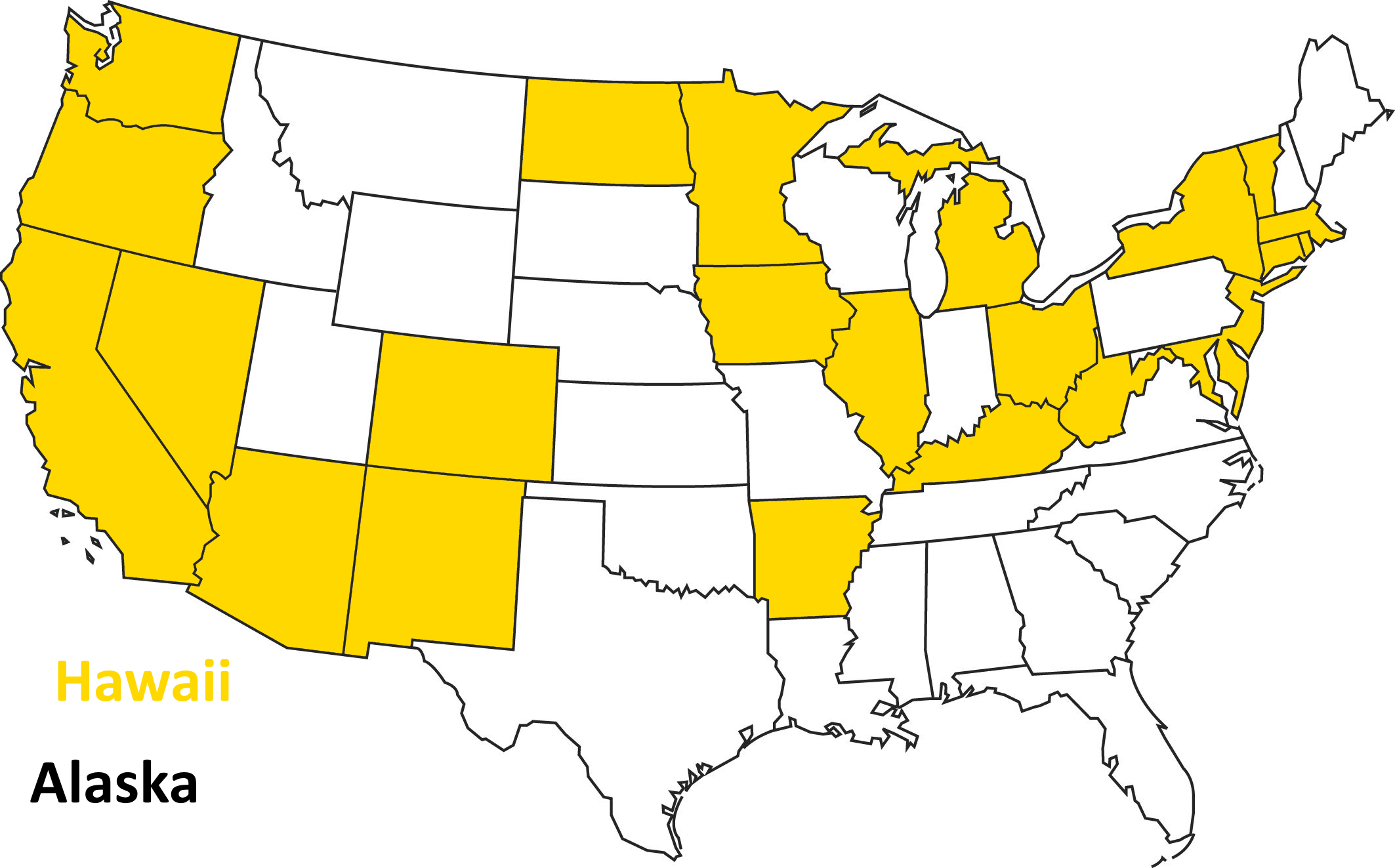

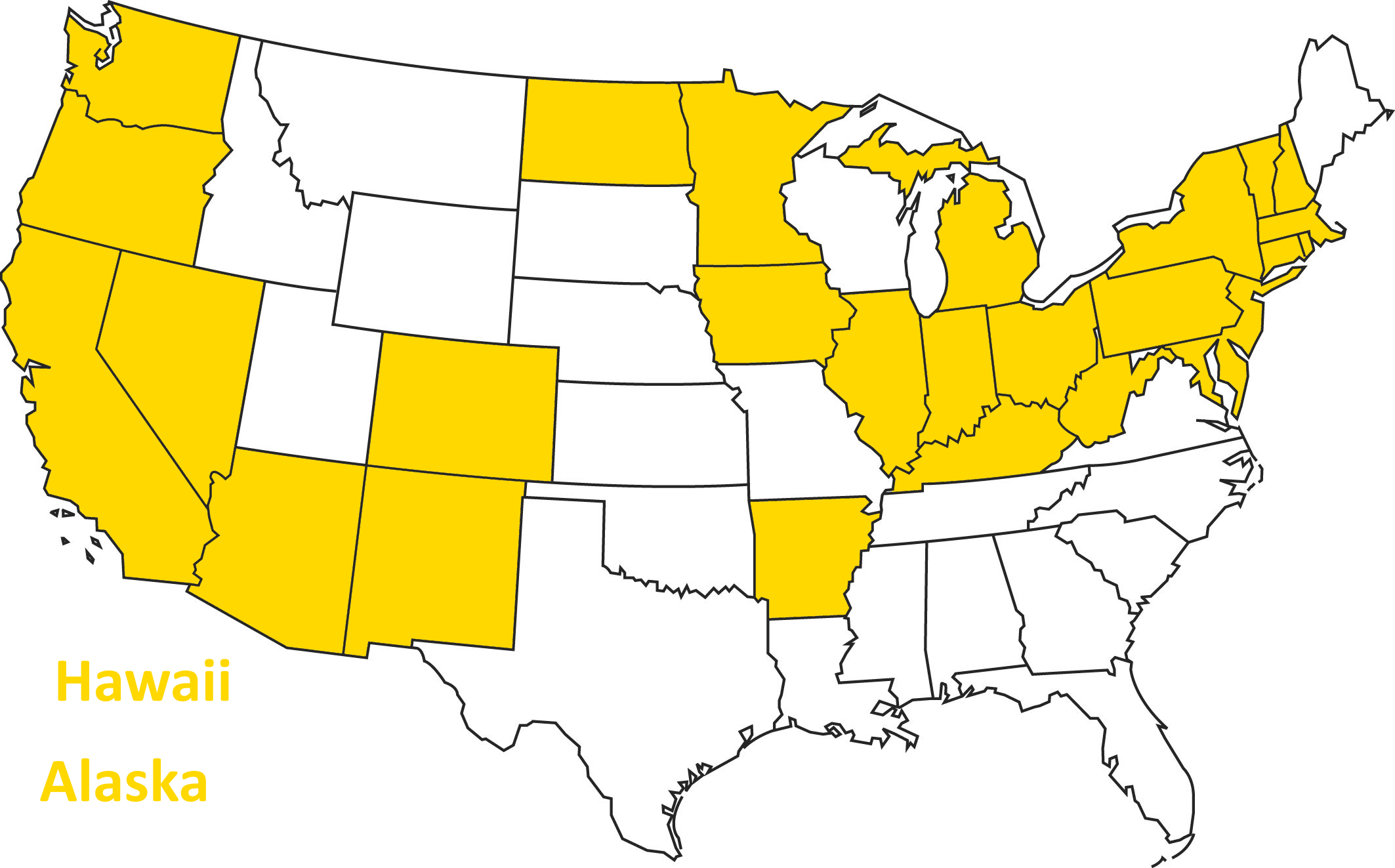

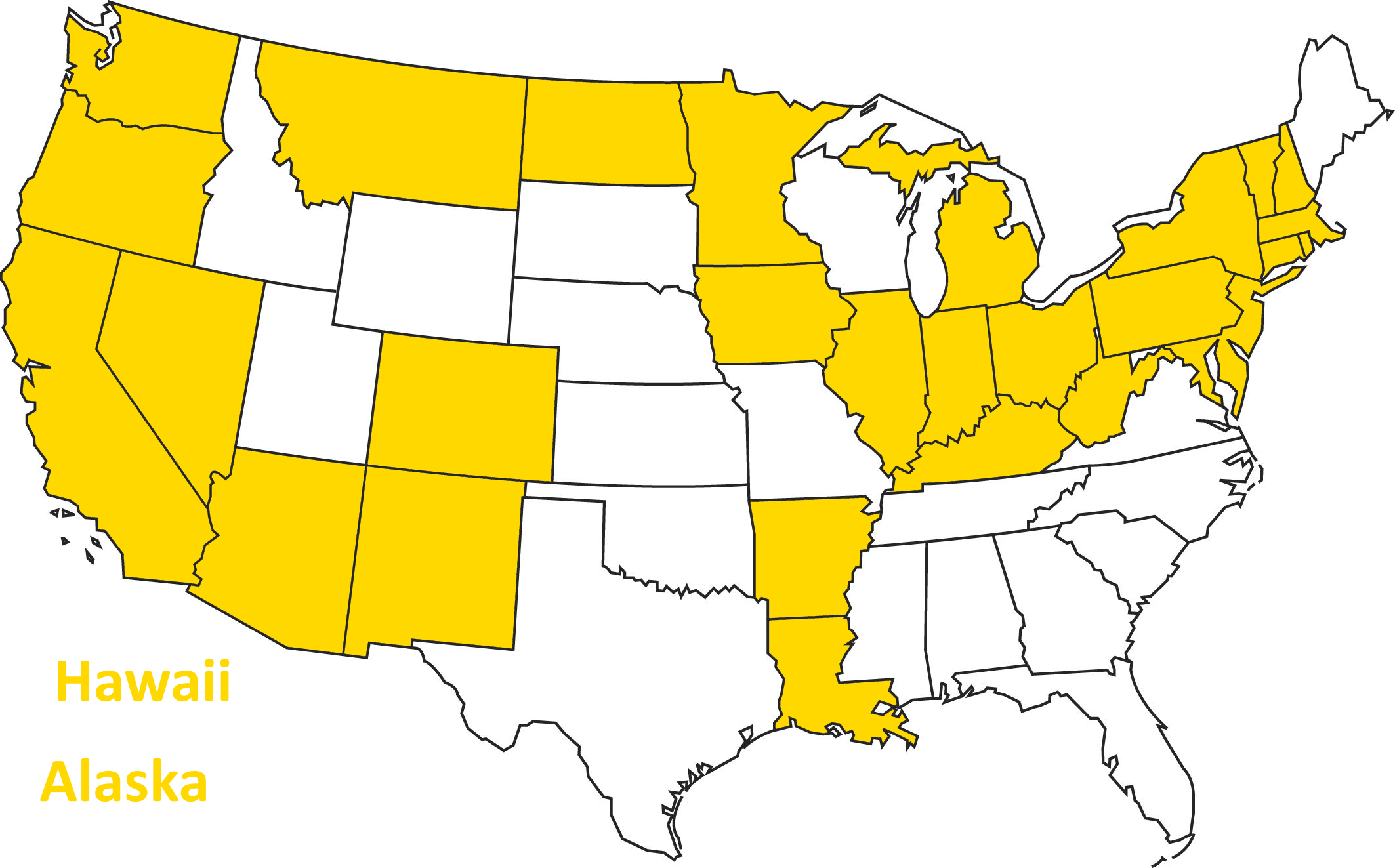

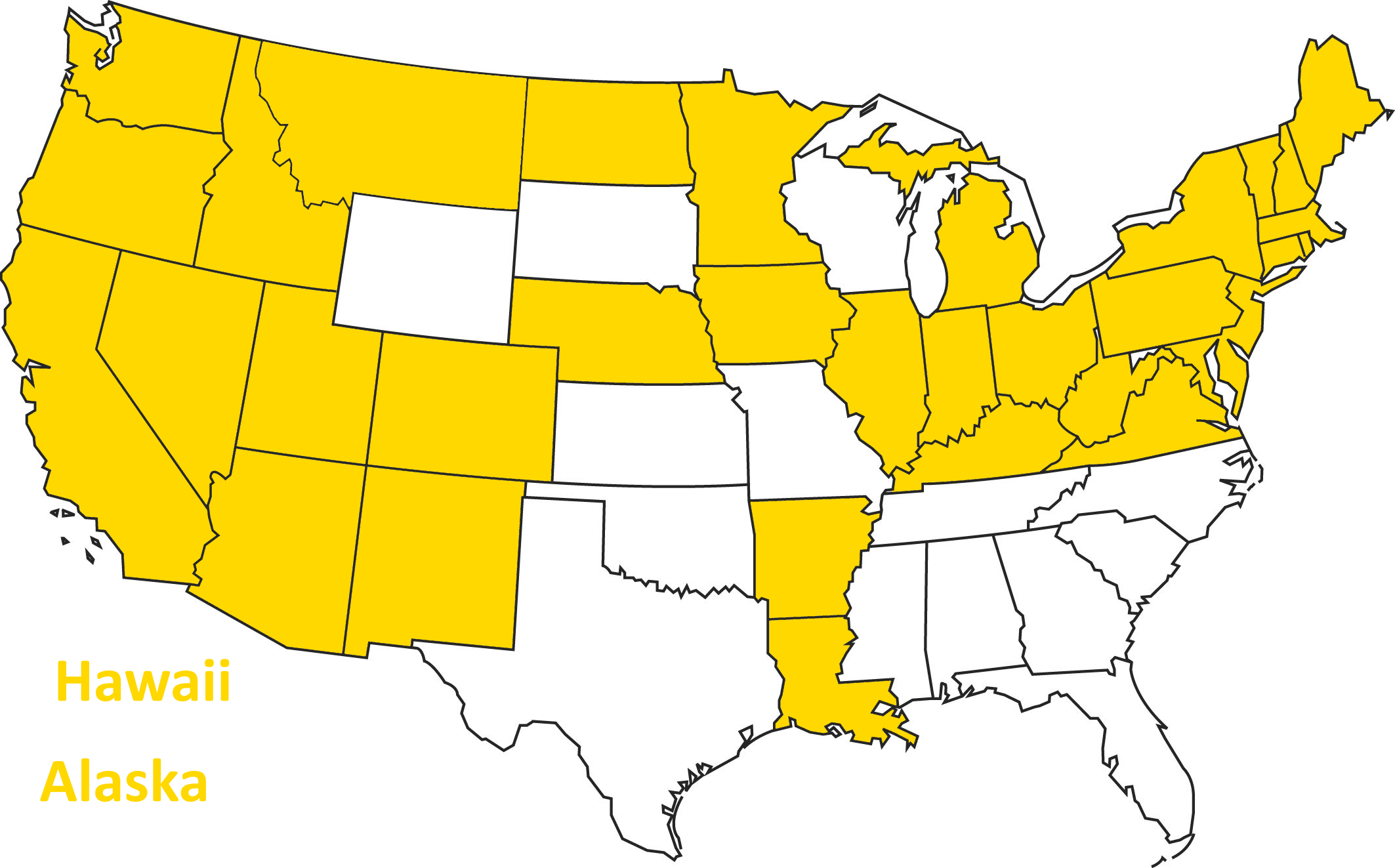

Opted to Expand in 2014

As of 2015...

As of 2016...

Today

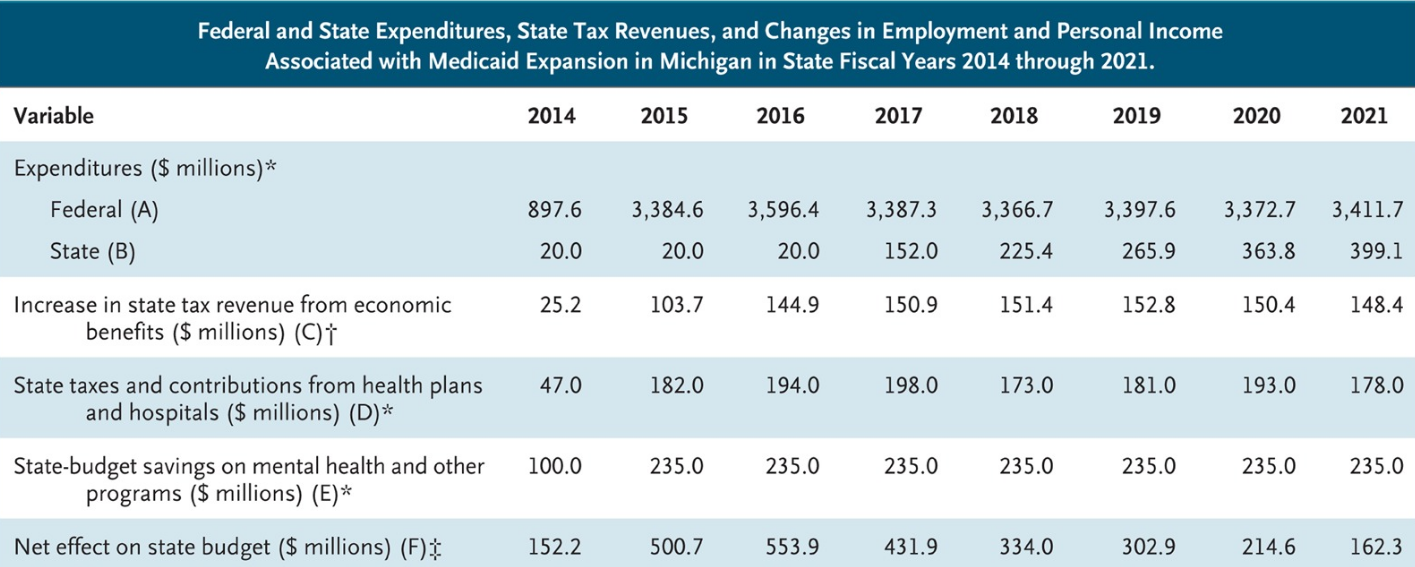

Can States Afford to Expand?

Medicaid is the single largest item in most state budgets.

- 10% of a big number is a big number

- Is expansion is a financial burden on states?

- In many states Medicaid reduces the need for other state-funded programs.

•UM analysis: over first 10 years the state of Michigan will save $1 billion.

Can States Afford to Expand?

Private Coverage Provisions

Underwriting reforms:

- "Guaranteed issue": no denials or exclusions for pre-existing conditions

•Adjusted community rating: premiums vary by age, smoking status

Individual mandate

Tax penalty for not having insurance

- 2014: max[$95 per adult, 1% of income]

- 2017: max[$695 per adult, 2.5% of income]

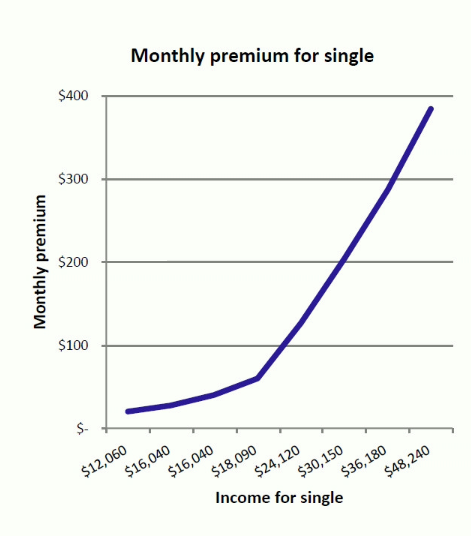

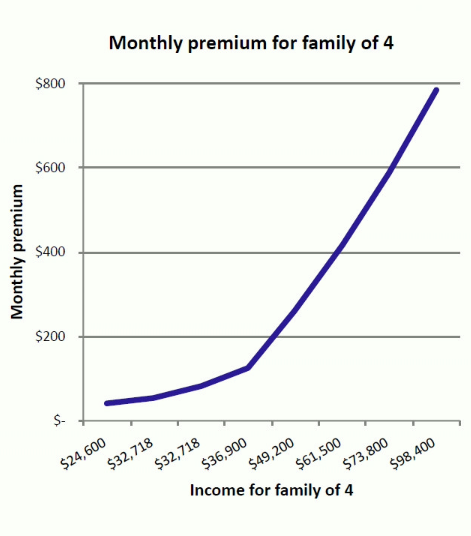

Premium Tax Credits

•Available between 100% and 400% of poverty

•Eligibility limited to people without access to affordable ESI

•Can only be used for coverage in newly established “marketplaces”

Health Insurance "Marketplaces"

The goal: make it easier to shop for health insurance if you don't have coverage through an employer

•Consumers choose from a menu of private plans

•All plans must offer 10 “essential health benefits” and conform to one of four actuarial value “metal levels.”

•Tax credits are based on consumer income and the premium for the 2nd lowest cost silver plan.

- 100-133 % of FPL: premiums are capped at 2% of income

- 300-400% of FPL: premiums are capped at 9.7% of income

•Low-income enrollees also qualify for cost-sharing reductions.

Health Insurance Marketplaces

Note: if a consumer gets a subsidy, then what the consumer actually pays doesn't actually depend on the price--it depends on the consumer's income.

When prices go up, the consumer doesn't necessarily pay more... (who does?)

Premium for Benchmark Plan

Source: 2018 KFF, note this is net of subsidy

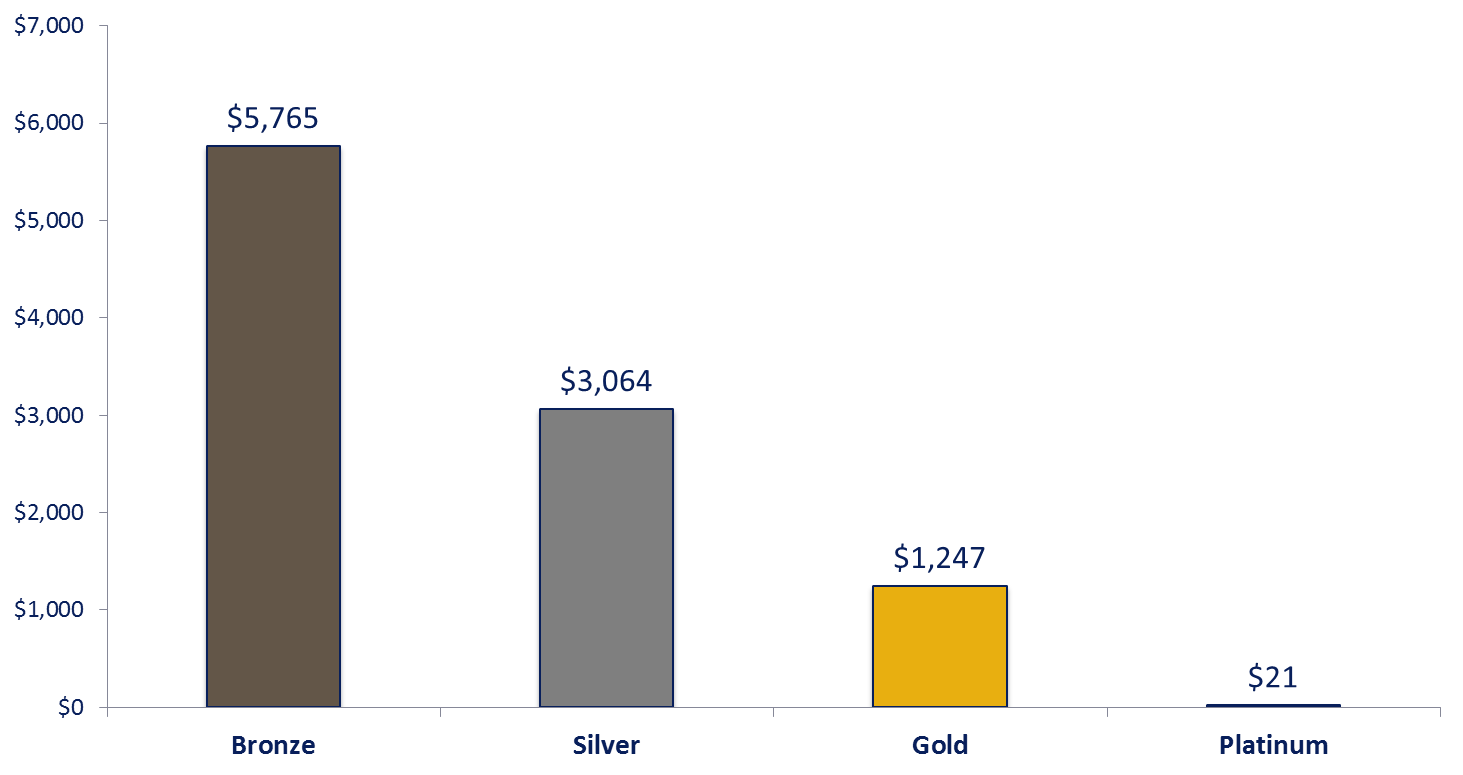

Typical Deductibles

Source: KFF

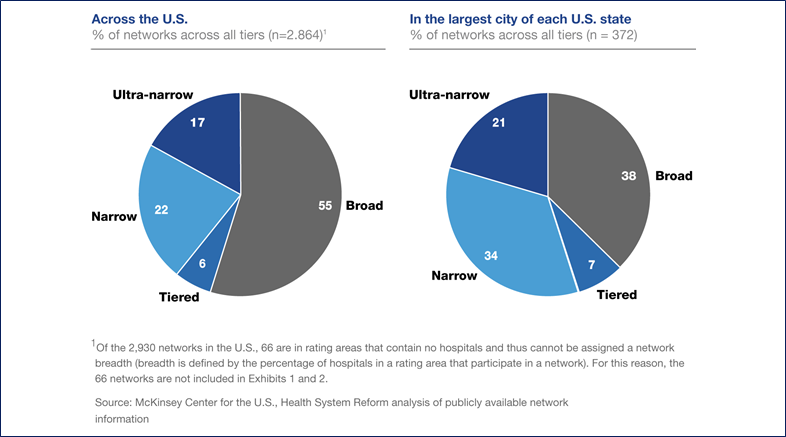

Rise of Narrow Network Plans

•Ultra narrow plans contract with < 30% of hospitals in the market

•Narrow plans contract 30% to 70% of hospitals in the market

•Broad plans contract with > 70% of hospitals in the market

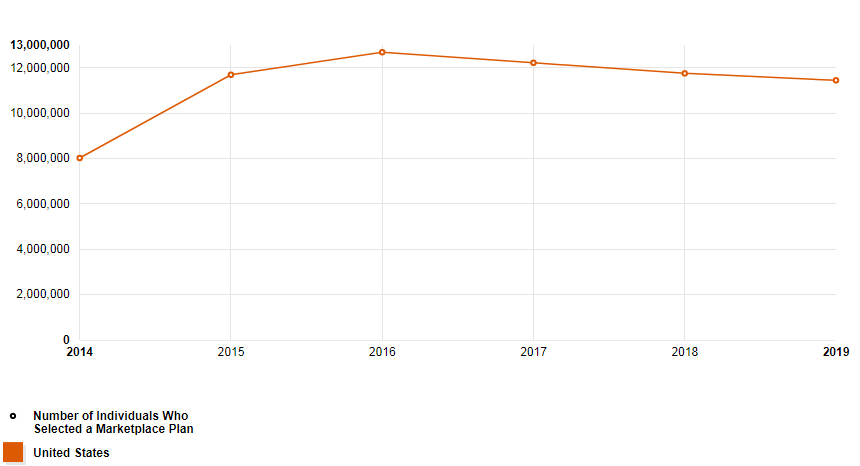

Marketplace Enrollments

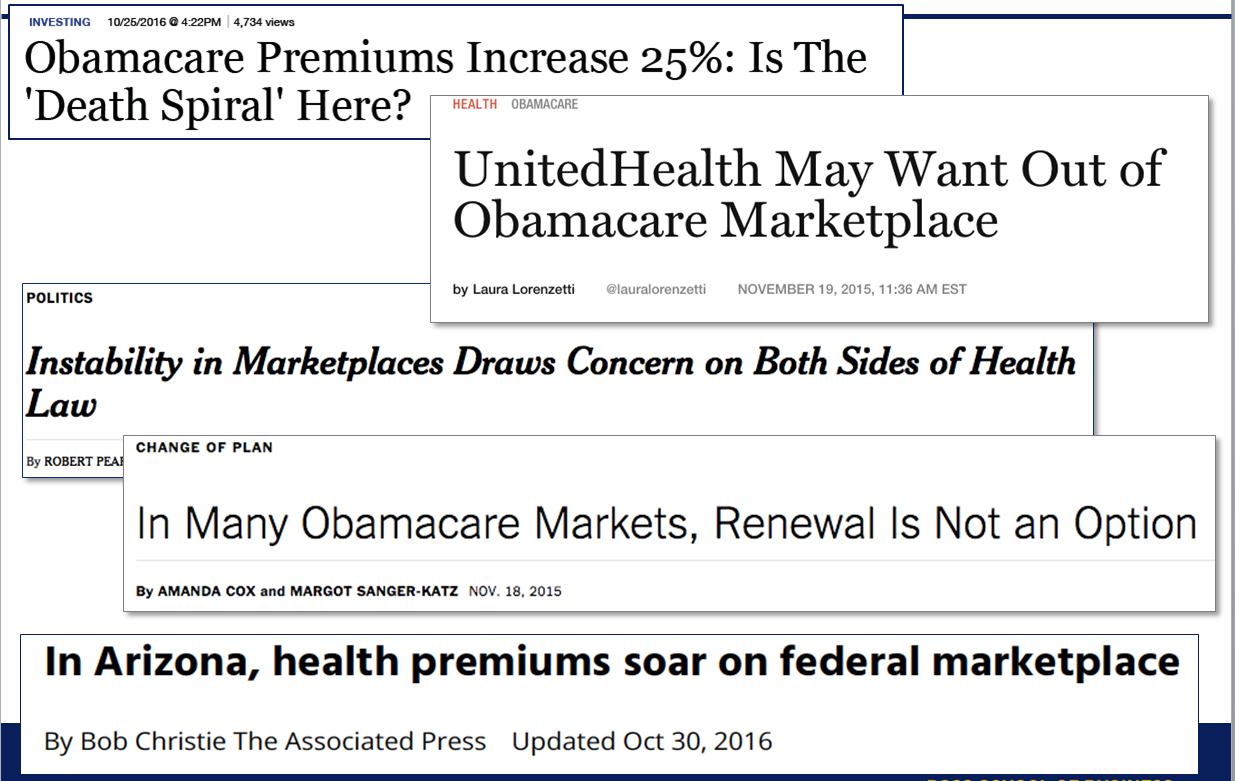

Withdrawal of "household name" insurers:

Exits 31 states in 2016/2017; remains partially active in New York, Nevada, and Virginia.

Withdraws entirely (from 13 states) in 2017/2018 transition.

Exits entirely (11 states) in 2017/2018 transition

Marketplace Enrollments

Success of plans with Medicaid managed care experience:

Narrow networks (e.g. So Cal plans exclude UCLA)

600k enrollees

Profitable

1.2 million marketplace enrollees

Low premium, high deductible, narrow network

Dependent Coverage

Dependents can remain on parents' coverage until age 26

- One of the most popular aspects of the bill

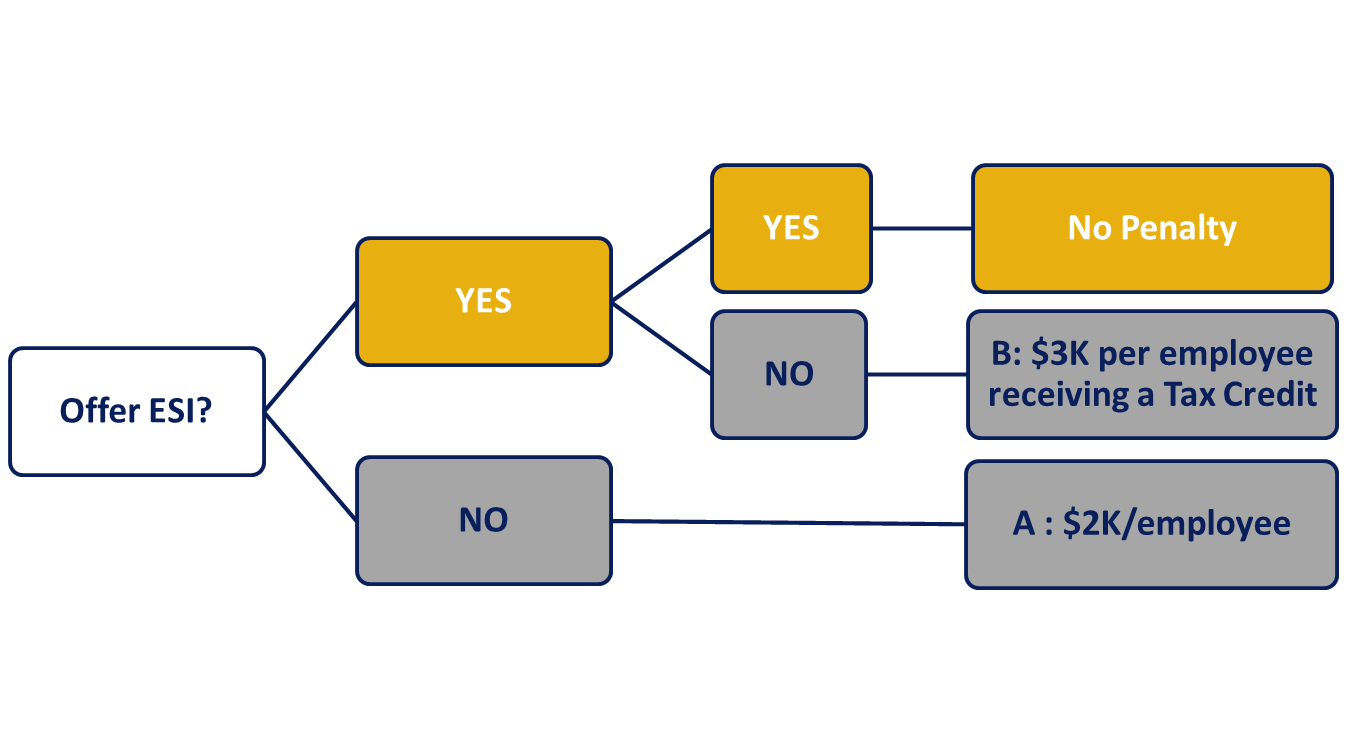

Employer Mandate (50+ FTEs)

•Penalties only apply if 1 or more full-time employee receives a premium tax credit in the exchange.

•Penalties do not apply to first 30 employees

•B penalty is capped at the amount of the A penalty (i.e., $2K/employee)

Early Evidence on Coverage Gains

About ~2 million gain coverage

through dependent mandate

Overall Coverage Gains

The number of people with insurance increased by 20 million between 2010 and 2015

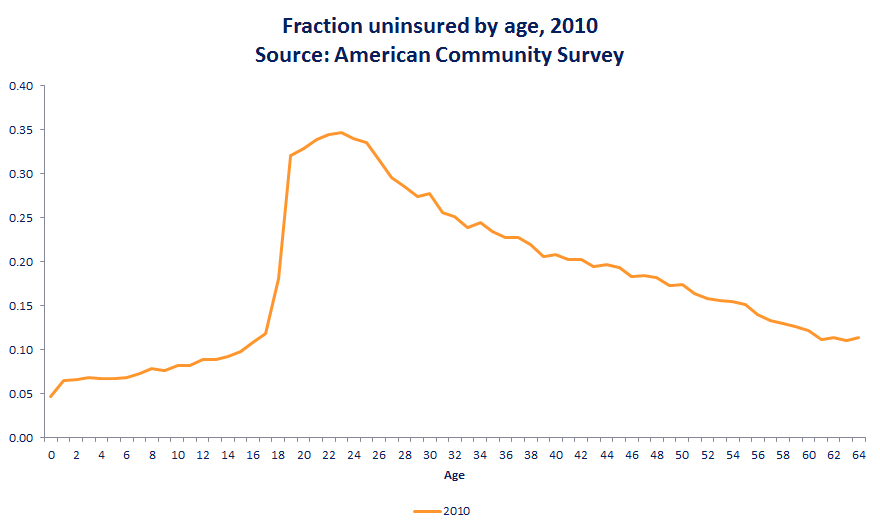

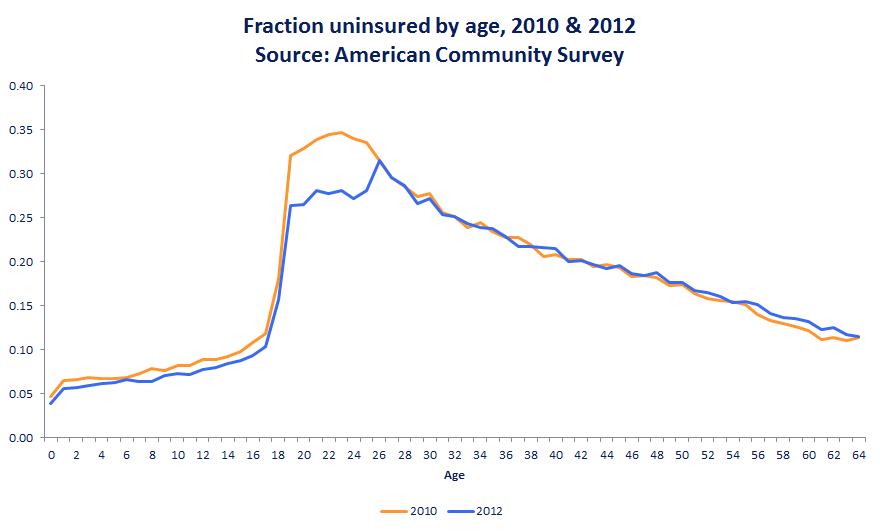

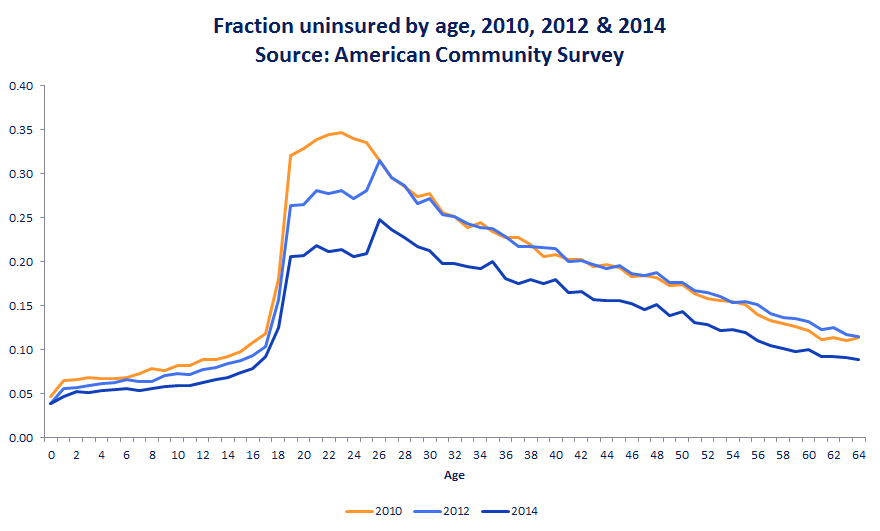

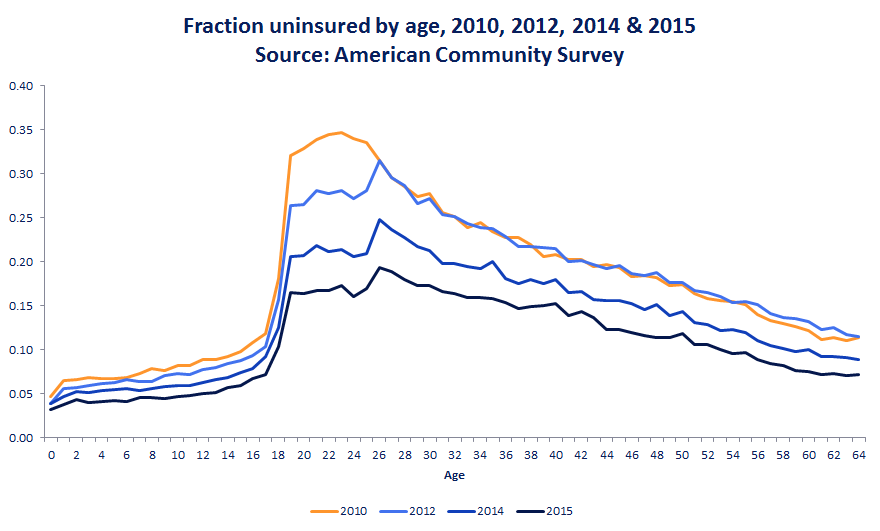

Coverage Gains by Age

Coverage Gains by Age

Coverage Gains by Age

Coverage Gains by Age

Coverage Gains Largest in states that expanded Medicaid

Sample among low income adults, Miller and Wherry 2016 New England Journal of Medicine

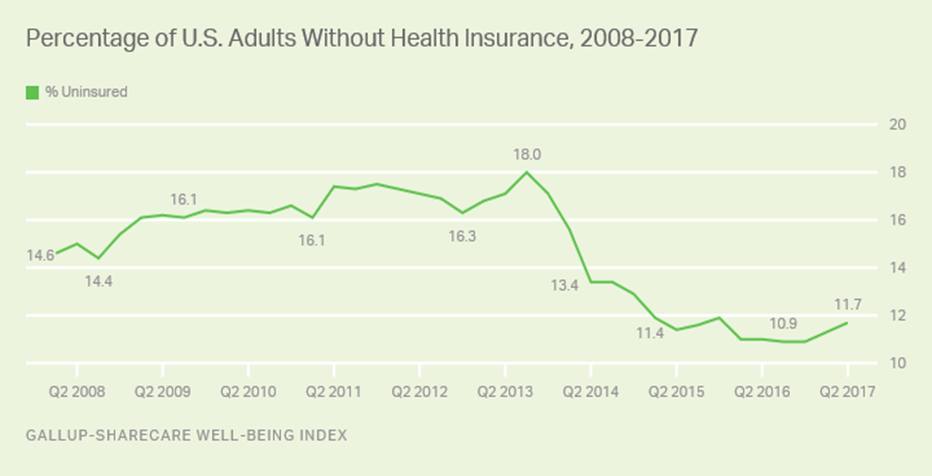

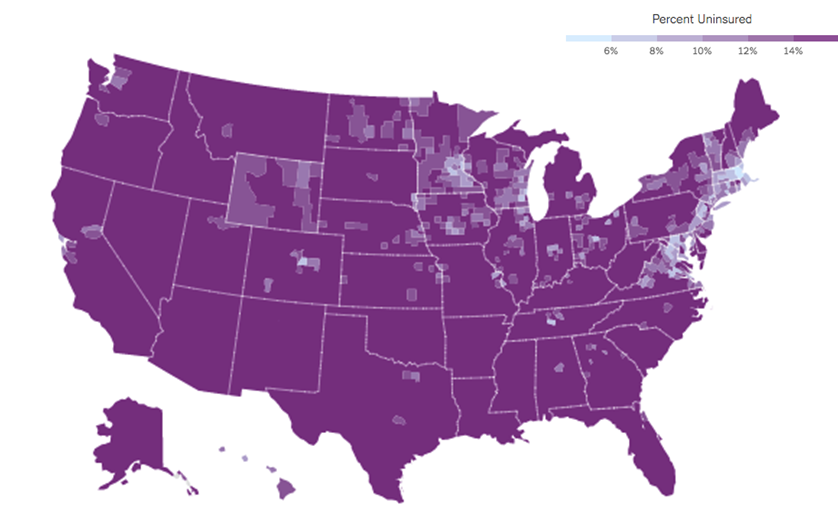

Percent Uninsured 2013

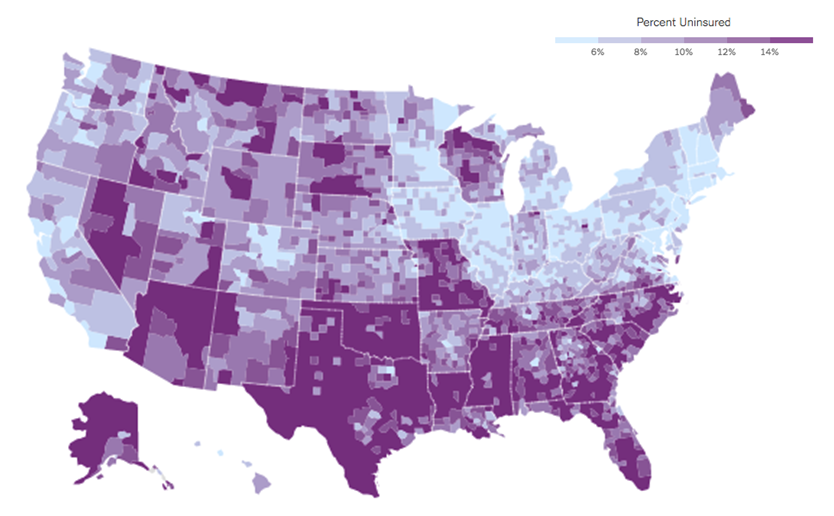

Percent Uninsured 2016

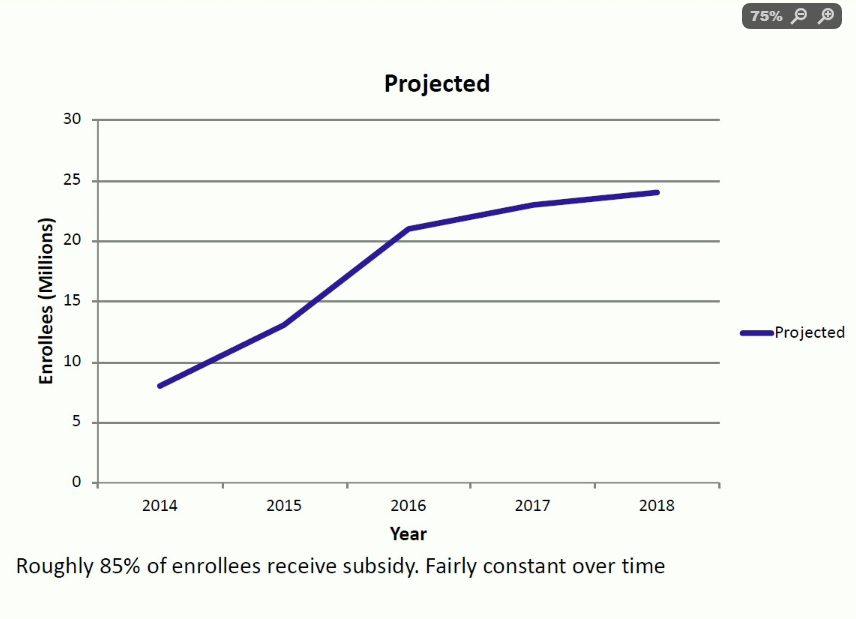

ACA Marketplaces

Marketplace Enrollments

Marketplace Enrollments

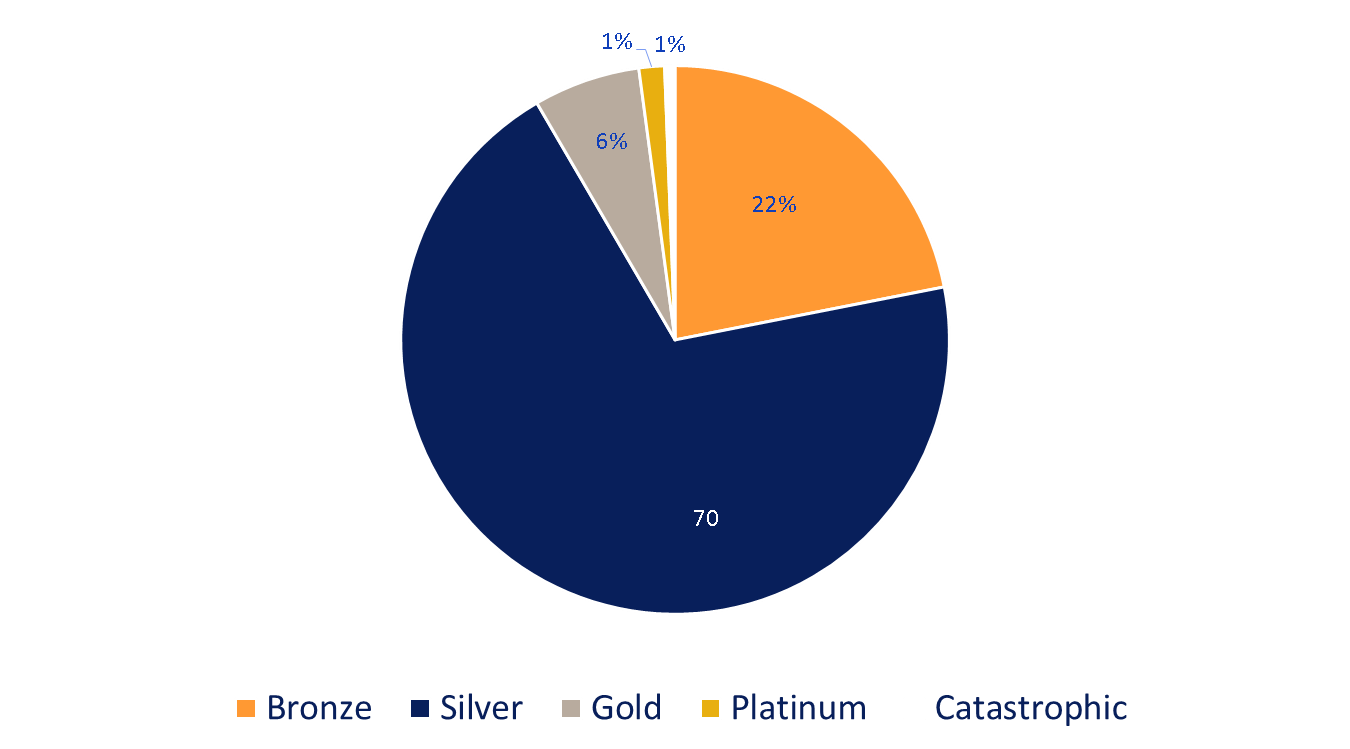

Enrollment by Plan Type

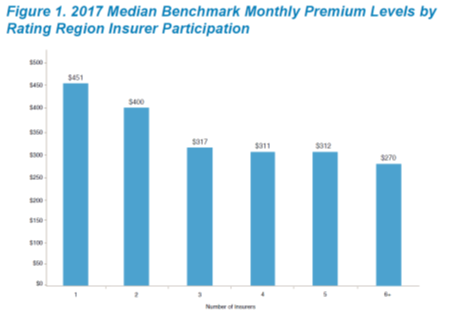

Significant Premium Volatility

Which price is relevant...?

Recall--the listed premium isn't relevant for 85% of enrollees who are receiving subsidies (capped as % of income).

- For these consumers, net of subsidy premium has declined.

Risk Selection in Marketplaces

•More evidence of adverse selection in non-expansion states (Peng 2017), especially “direct enforcement” states that most strongly resisted the ACA (Kowalski 2016) and states that permitted non-compliant plans to continue to be sold (Lucia and Corlette 2017).

Stabilizing effect of the tax credits--reduces death spiral tendencies.

But for "higher end" products (Platinum plans) death spiral appears to have happened.

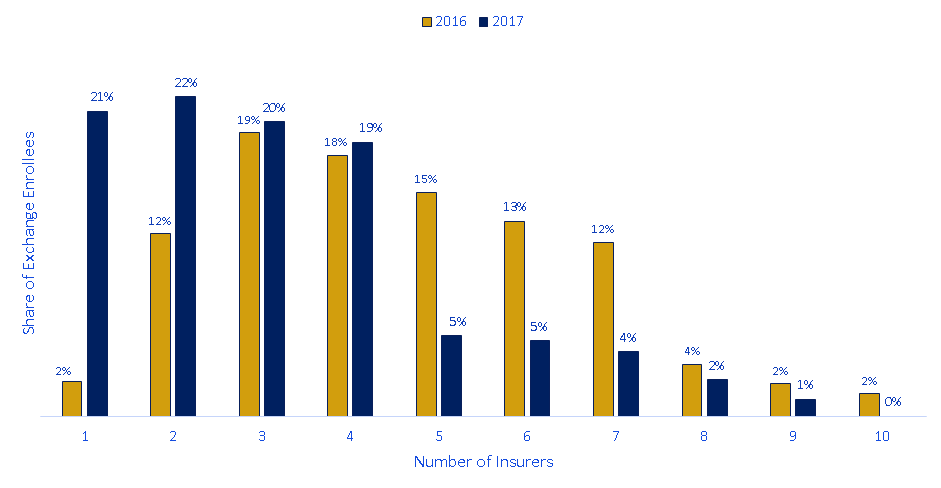

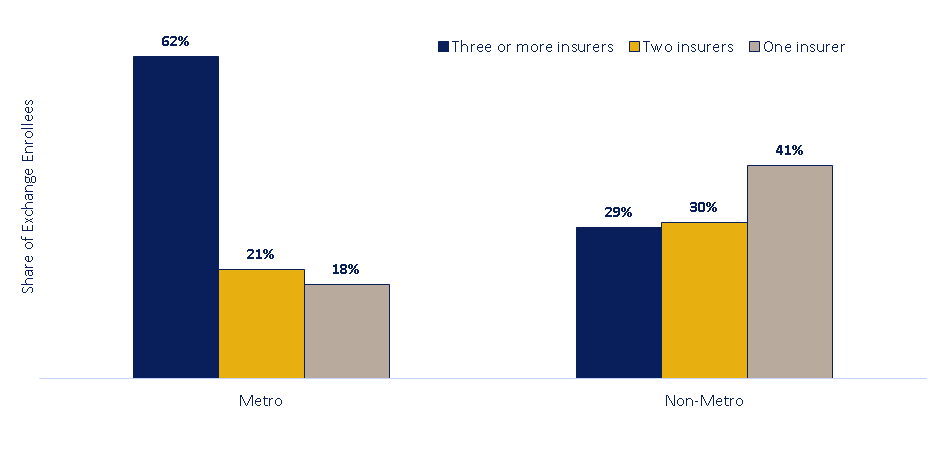

Competition on the Exchanges

About 20% of enrollees have only one insurance company offering plans--far from the "perfect competition" ideal

Competition on the Exchanges

This is worse in rural locations

Premiums are lower and more stable in markets with robust competition

Source: Holahan et al, Urban Institute Report, 2017

Effect of the ACA on patients and providers

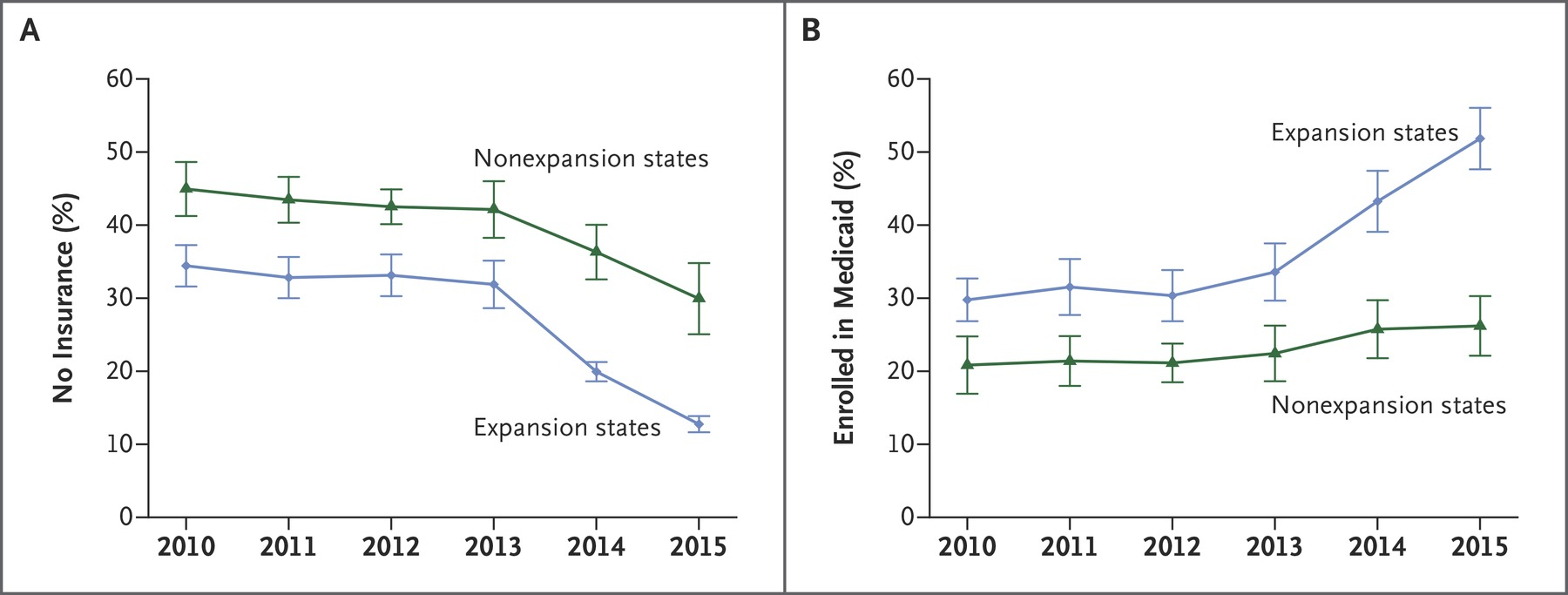

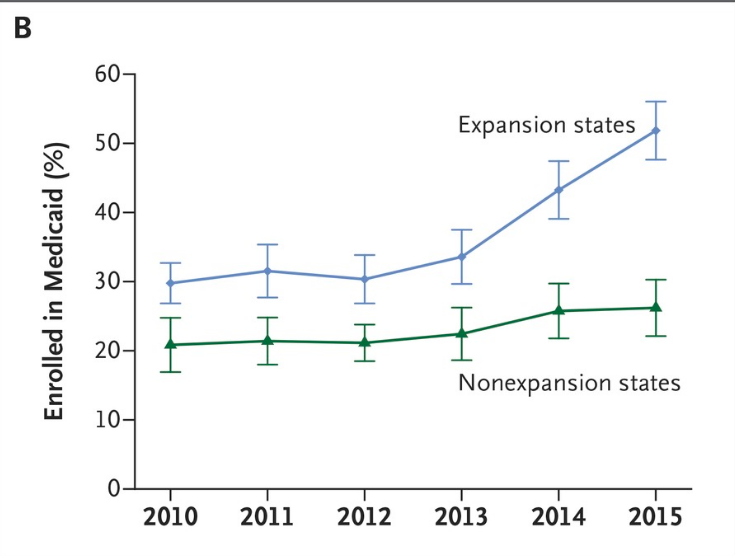

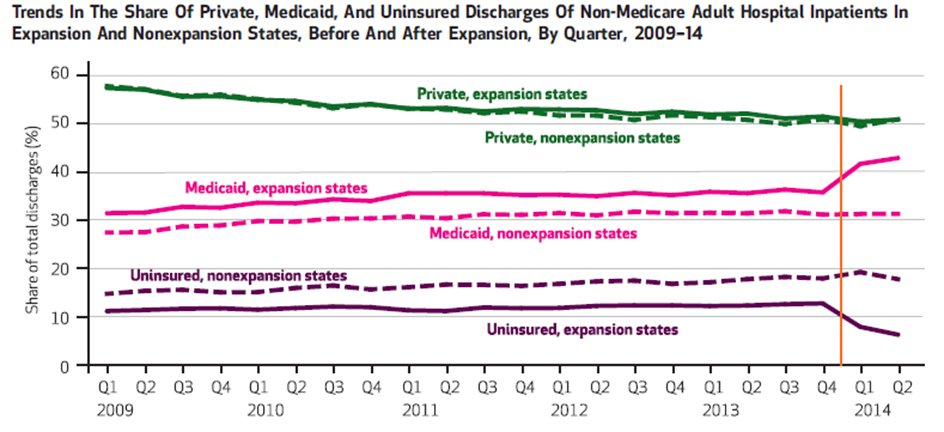

Medicaid Expansions

- Take advantage of non-universal adoption of the Medicaid expansion that resulted from the 2012 Supreme Court decision.

- Use a "difference in differences" quasi-experimental empirical design

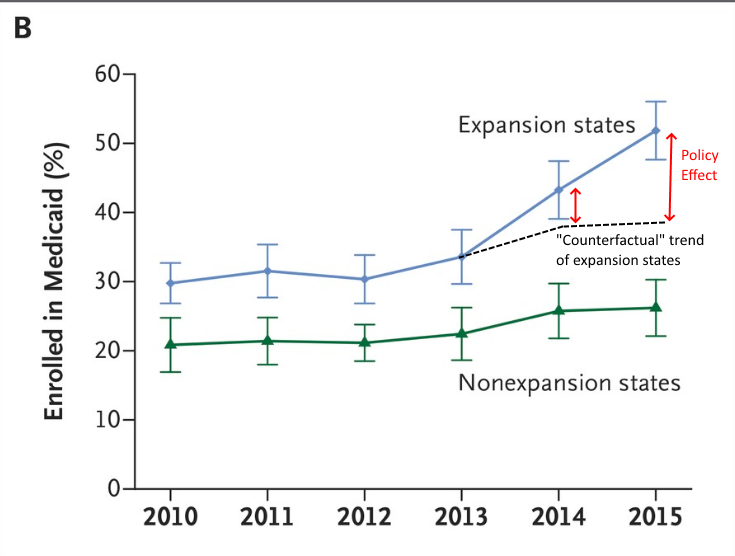

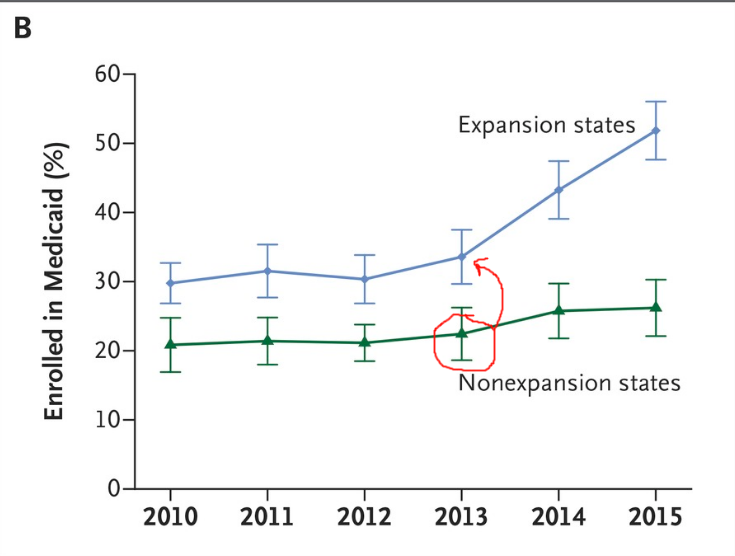

Compare changes in outcomes across expansion and non-expansion states.

Expansion states and non-expansion states might be at different levels, but are they on the same trajectory?

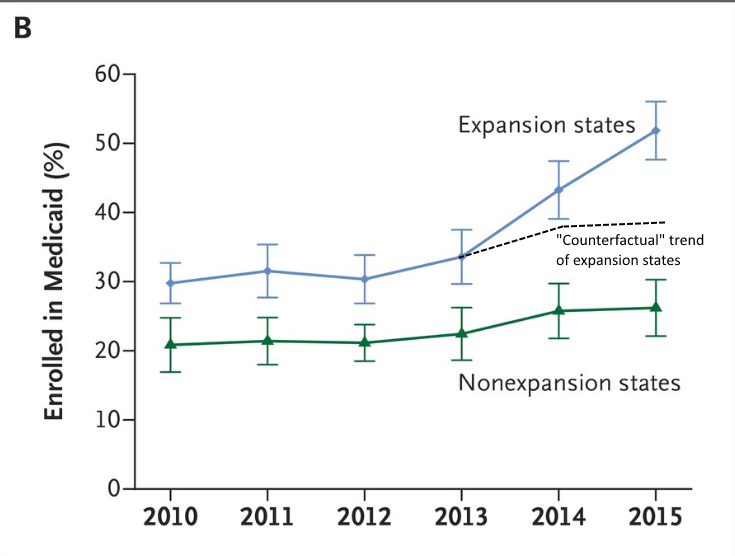

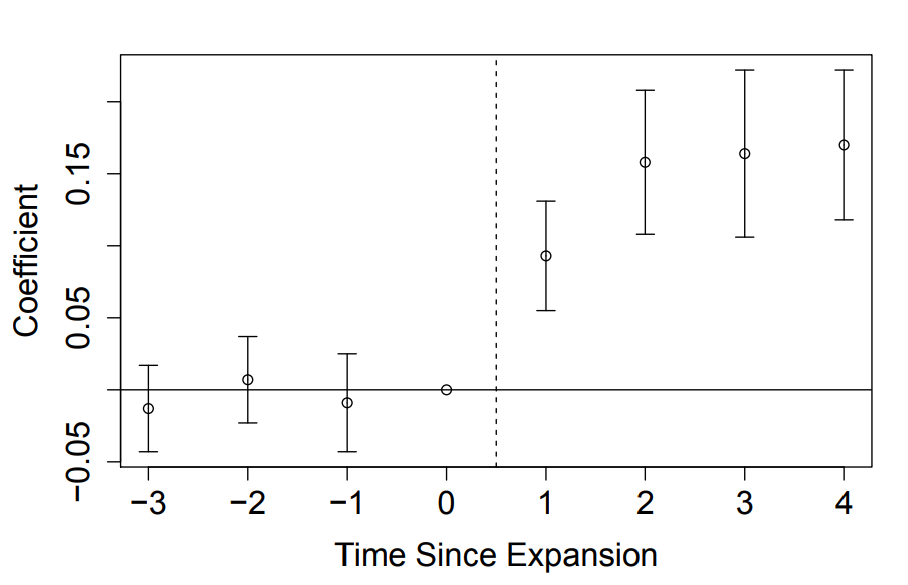

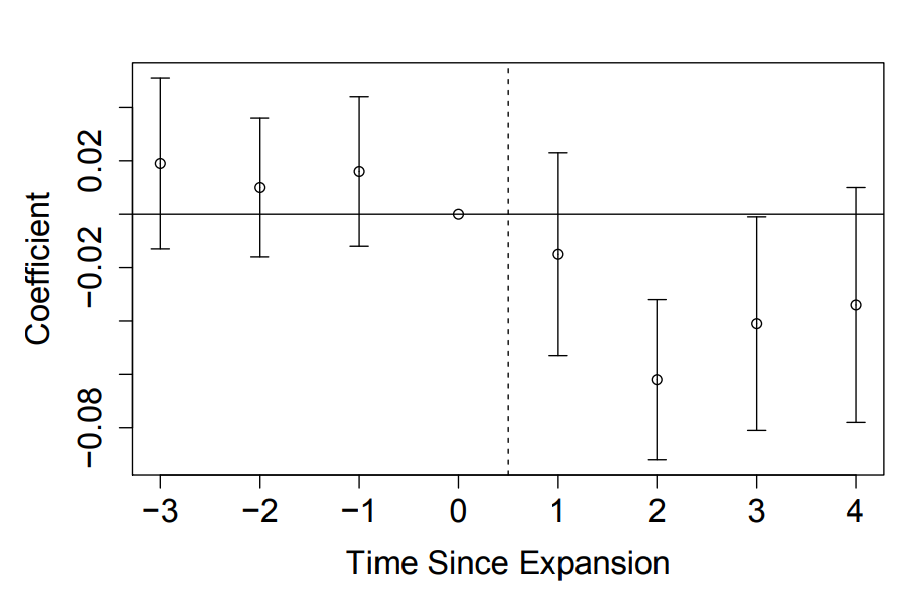

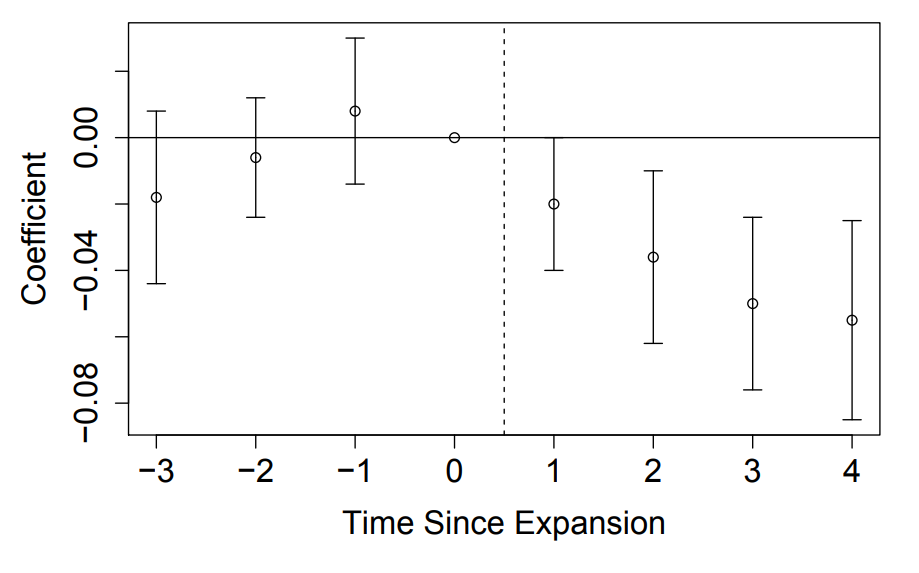

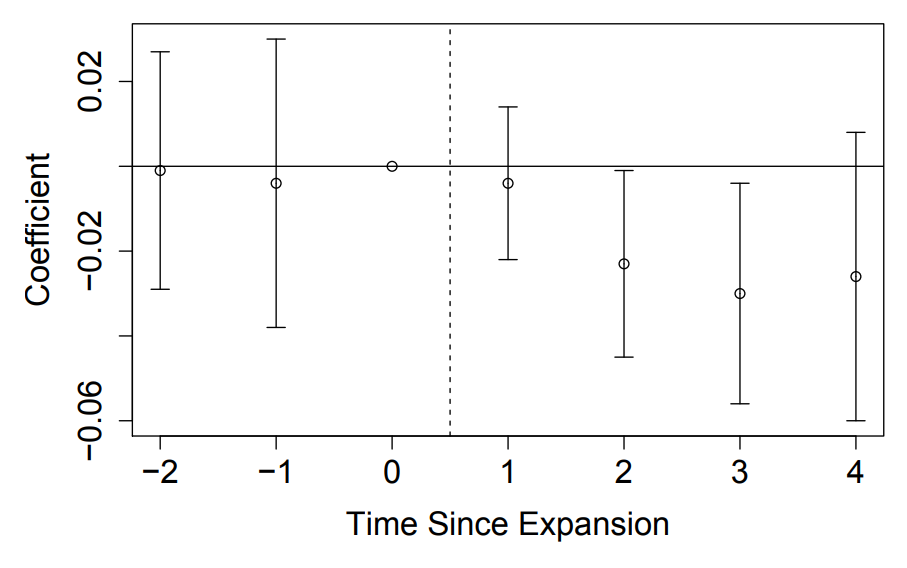

Difference in Differences

Let's go back to this figure:

Difference in Differences

Let's go back to this figure:

Difference in Differences

Let's go back to this figure:

Difference in Differences

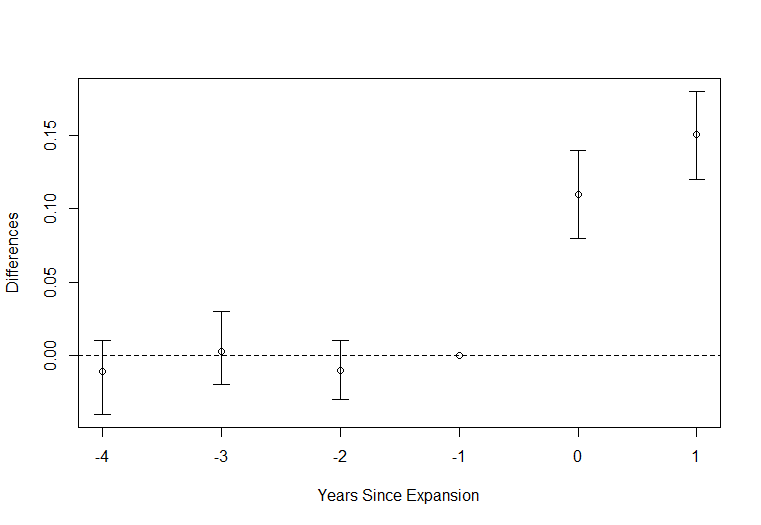

One way to represent this would be to subtract out the difference in one year (normalize to zero) and then plot the remaining difference.

Difference in Differences

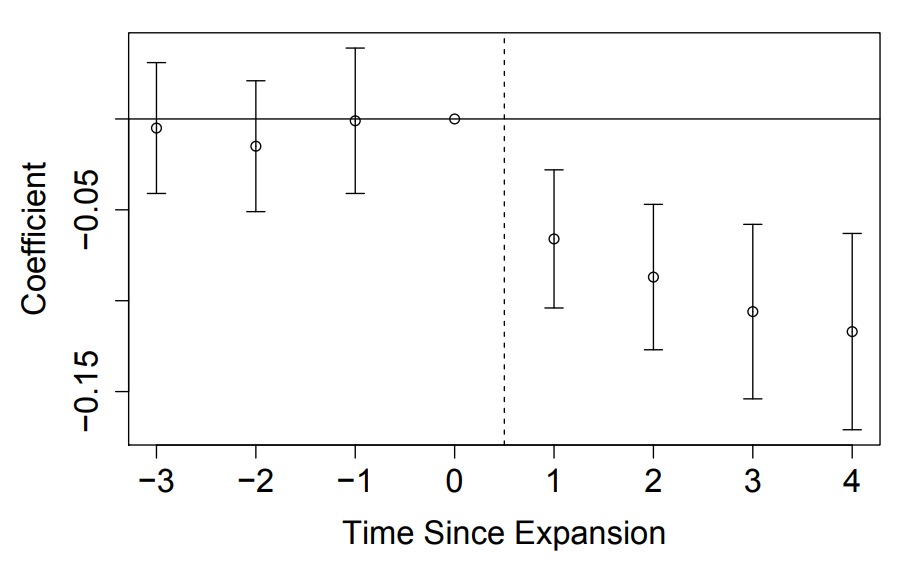

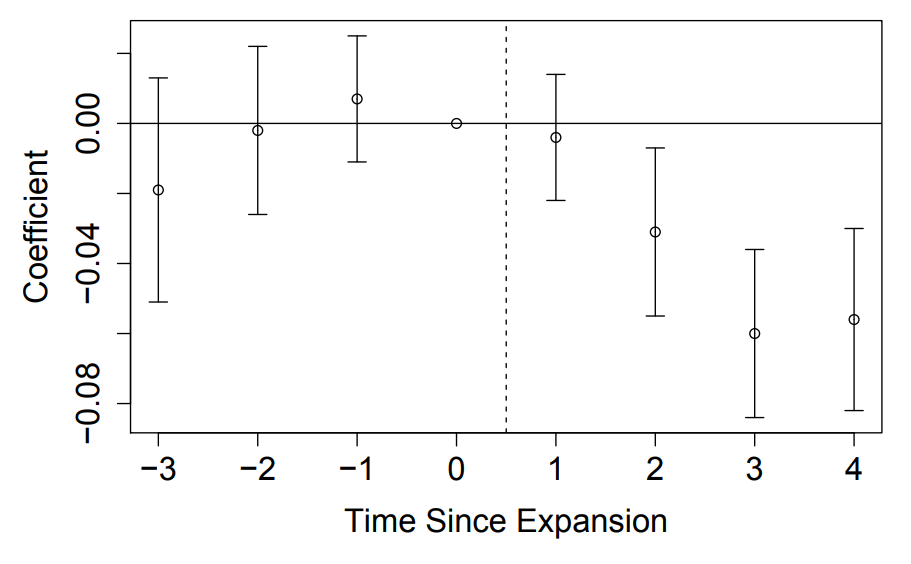

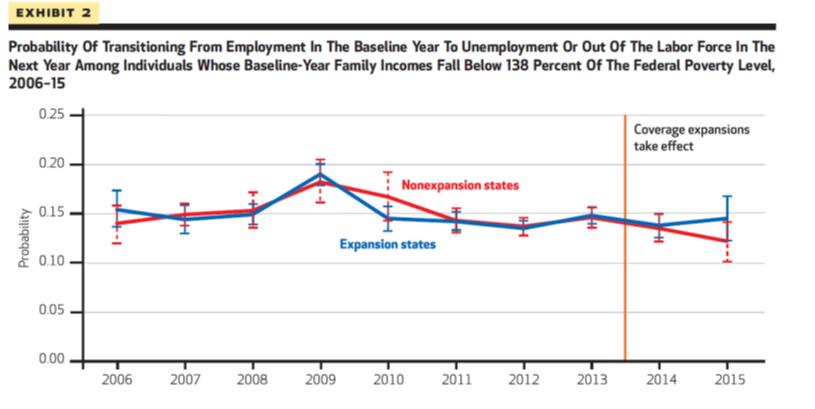

Uninsured

For low income adults--probability of being uninsured went up in expansion states

(Miller and Wherry 2019 AEA P&P)

On Medicaid

For low income adults--probability of being on Medicaid went up in expansion states

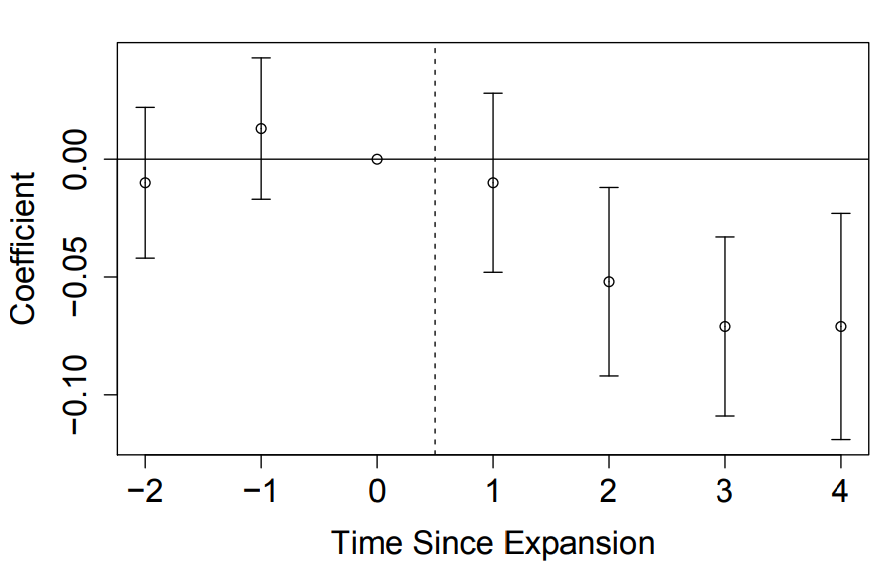

Privately Insured

For low income adults--probability of being privately insured went down in expansion states

Needed Care but Couldn't Afford it

Needed Specialty Care but Couldn't Afford it

Delayed Care due to Affordability

Problems Paying Bills

Financial effects important

This is a very disadvantaged group: average income, 38% FPL (~4400 for an individual), have about $2k of medical debt on credit reports on average

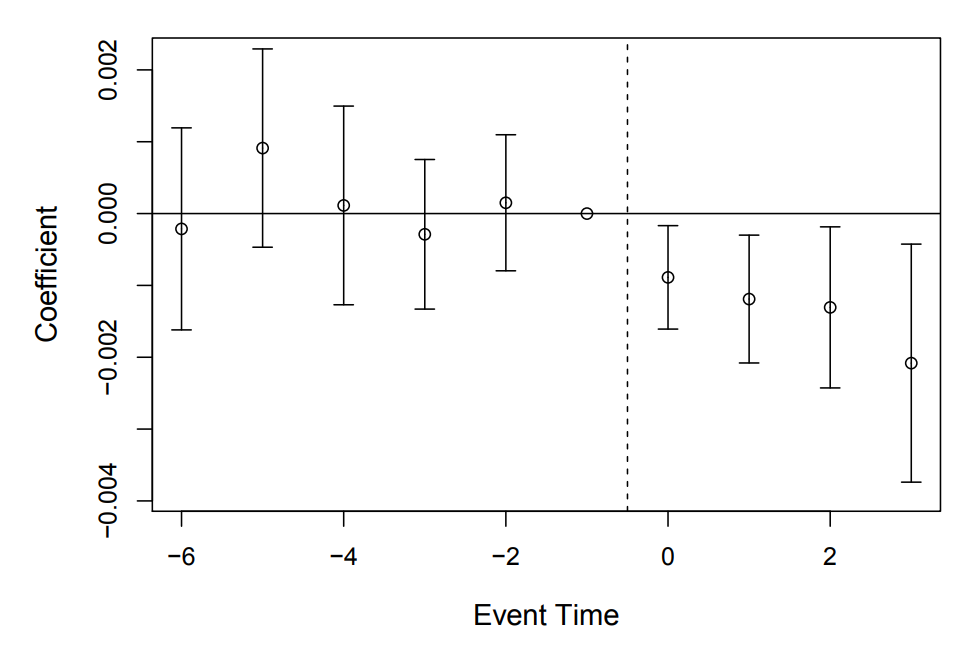

Mortality Effects

Reduction in mortality of about one tenth of a percentage point (about 9.4%). Implies 19,200 fewer deaths from 2014-2017 in expansion states.

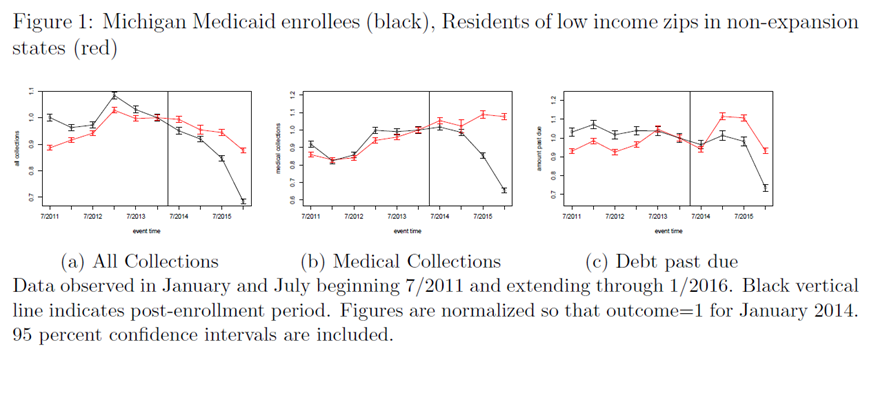

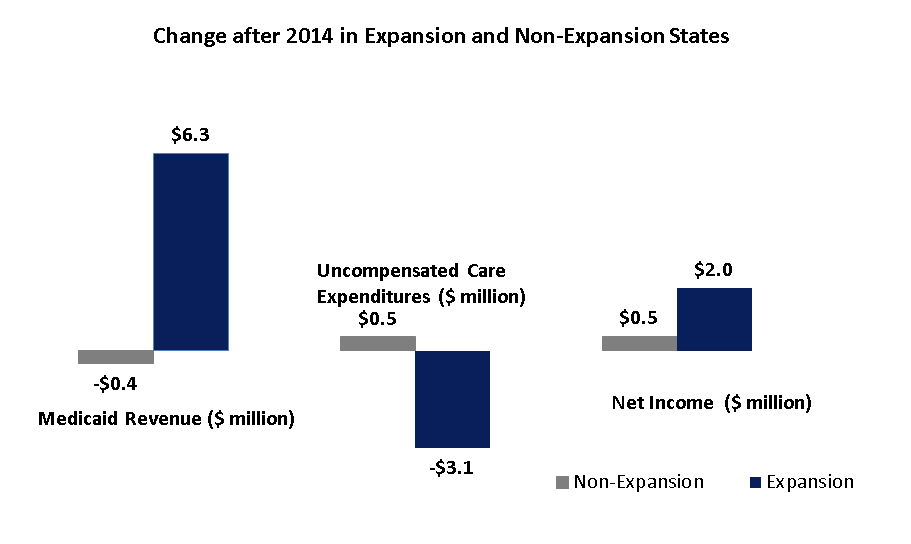

Effect on Providers

Because hospitals must accept all patients regardless of ability to pay, they are “insurers of last resort.”

- Each uninsured person generates an average of $900 in uncompensated care per year.

- 2013: hospitals provided ~$45 billion in uncompensated care

(~6% of expenditures)

Hospitals were advocates for reform and for continued Medicaid expansion.

Medicaid and Hospital Finances

Buchmueller et al. 2019, in preparation

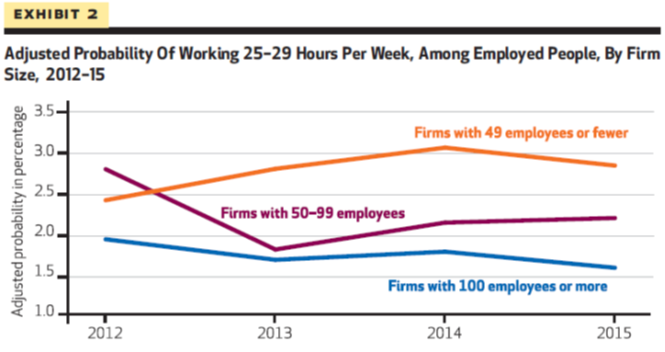

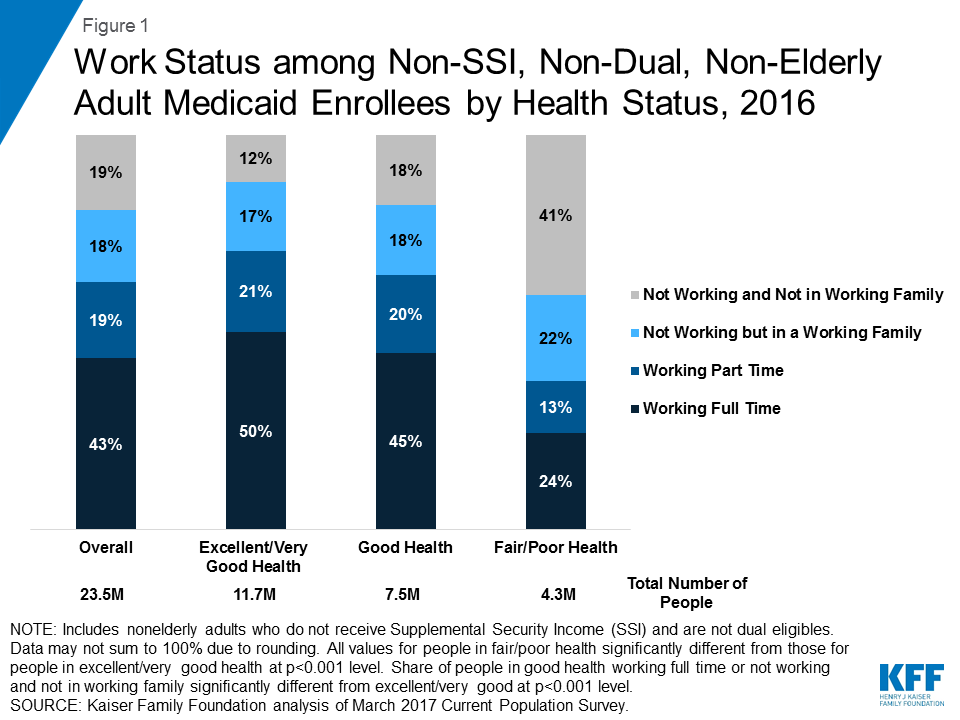

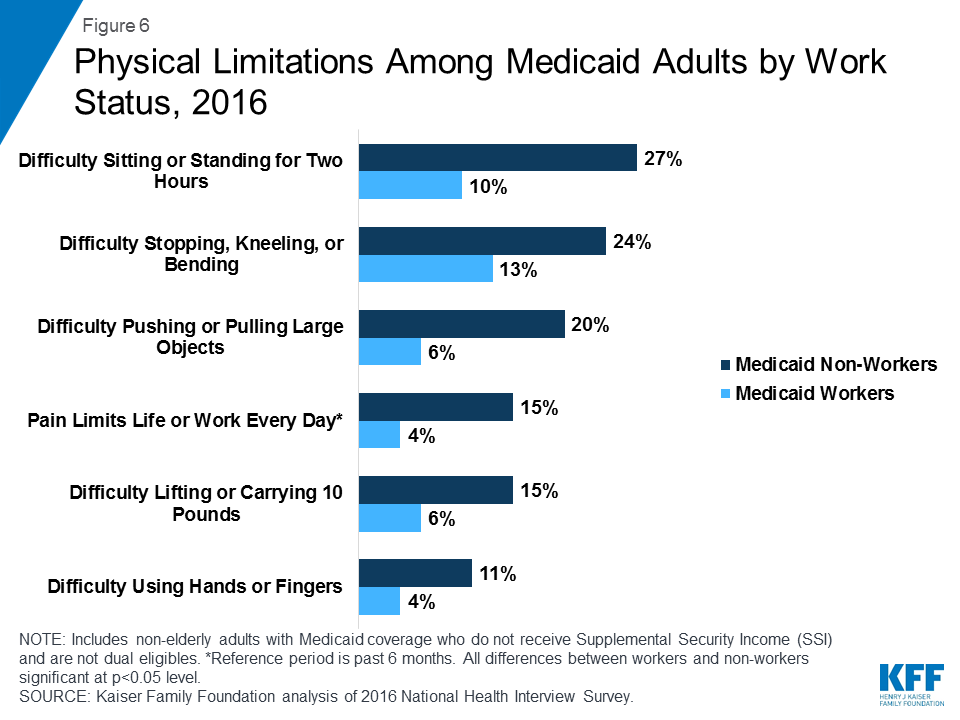

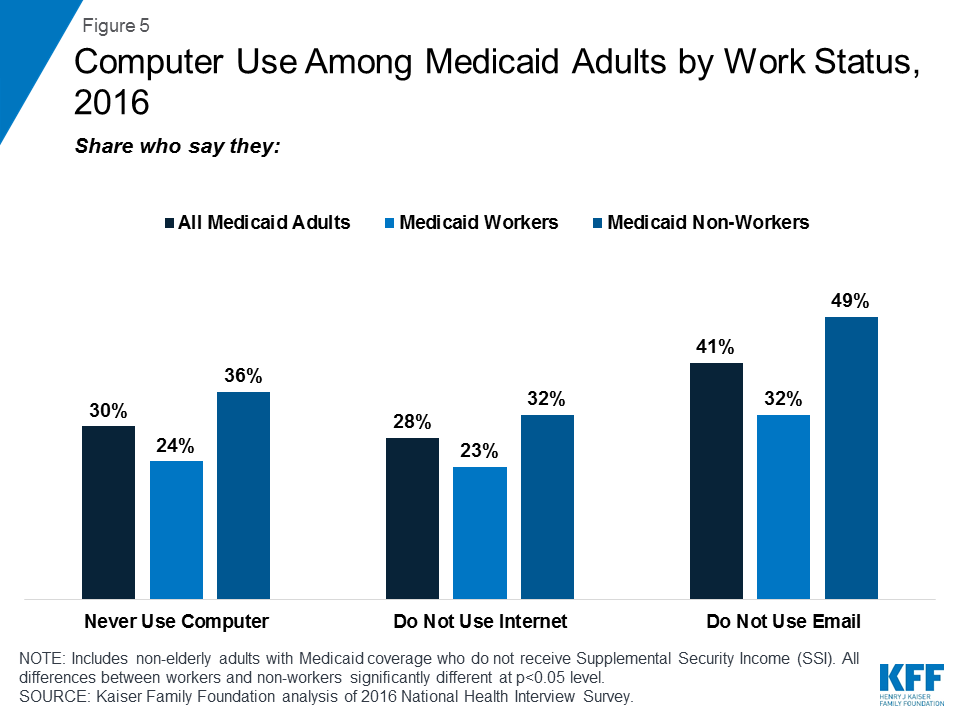

Labor Market Effects of the ACA

Potential Labor Market Effects

•The CBO projected that the ACA would reduce labor supply by roughly 2%. The largest effect was on retirement.

•Effects on labor supply could represent an improvement in labor market efficiency as job-lock is eased.

•Effects on labor demand may be inefficient if employers are distorting hiring to avoid cost of coverage (especially employers with 50 FTE+ who might get hit with a penalty).

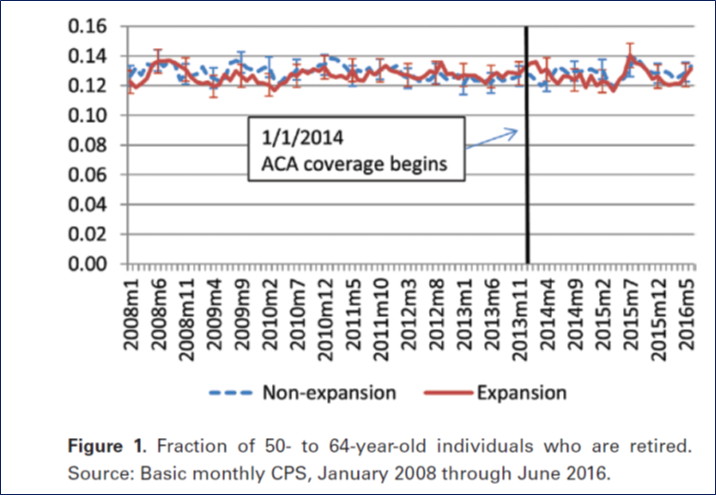

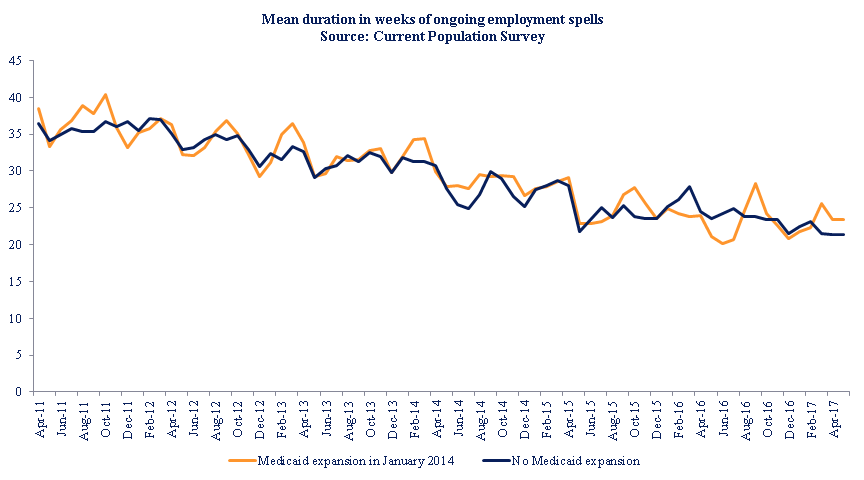

So far, there is little evidence of effects on either supply or demand--this was a surprise to most economists.

Nothing going on with early retirement...

(Levy et al 2017)

Length of unemployment spells... no obvious effect

Change to the ACA under the Trump Administration

Continued growth in Medicaid coverage

- Since the 2016 election, 5 states (VA, ID, LA, NE, UT and ME) have elected to expand Medicaid.

- Work requirements for Medicaid have been permitted:

- For example, in Michigan, new bill will require Medicaid recipients to work 29 hours per week; several categories such as pregnant women, full-time students, and disabled are excluded.

- Similar requirements put in place in Virginia, Arkansas (already dropped about 5,000 recipients), Kentucky (blocked); several other states considering them.

- Challenges to legality of waivers.

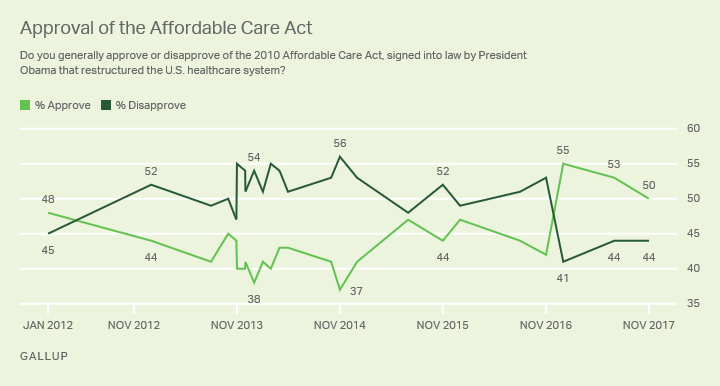

Make Obamacare Great Again?

Ironically, more people seem to like the Affordable Care Act after President Trump's election...

Relatively Steady Enrollment

Mandate Repeal

To reduce adverse selection, the ACA included an individual mandate to purchase insurance with a penalty if you did not purchase it. This was repealed for tax year 2017.

Could be a small effect (but no one knows for sure):

- Relatively few tax filers paid the penalty: about 12m were "exempted," 6.7 paid penalty

- Some confusion about whether mandate was repealed (about 40% did not know in latest Gallup poll)

- Many enrollees are subsidized, which is larger than the penalty

Short-term plans

A "loop hole" to allow insurance companies to not cover pre-existing conditions or all essential health benefits (e.g., maternity coverage) is to let them offer "short term" plans which are exempt from this regulation.

- Only permitted to cover for 3 months under Obama admin; Trump admin allows them to cover 364 days, renewable 3 years.

- Much cheaper than exchange plans--about 1/3 the cost--but cover less and don't cover pre-existing conditions.

- There is a concern they will pulling healthy people off of the exchanges, setting off a "death spiral."

Proposed solutions?

"Reinsurance"--encourage more insurance companies to offer exchange plans by having the government step in and cover the costs for patients who end up being particularly expensive.

AK, ME, MN, NJ, OR and WI all have applied to start such a program.

Government covers some fraction (e.g., 80%) of claims above some threshold (e.g., $50k)

Not cheap--Alaska has spent $55million on only 17k individuals, and expected costs to scale nationally are estimated to be about $38 billion.

Proposed solutions?

"Public option"/Medicare Buy-In:

Allow enrollees to "buy in" to Medicare at premiums that cover cost.

Medicare pays about 60% of what employer-sponsored insurance pays.

Forces plans to compete with Medicare

- on the plus side, lowers premiums (7-8% according to CBO in 2013)

- on the negative side, may drive some plans from the market and decrease choice.

Proposed solutions?

"Public" Medicare-for-All

Eliminate private insurance and replace it with Medicare.

- People like Medicare when they get it.

- Market based solutions (ACA) haven't been as popular as drafters hoped.

- Private insurance is expensive, we could reduce costs by switching to public plan.

Proposed solutions?

"Private" Medicare-for-All

Eliminate individual or employer sponsored private insurance and replace it with regulated private plans paid for by the government.

- Could cover everyone.

- Greater choice than "Public" Medicare for all (although potentially still less choice than current system).

Proposed solutions?

Market based approaches:

- Roll back regulations from ACA and allow market to provide greater range of products.

- Roll back Medicaid expansion and focus Medicaid coverage on the very needy or those with high health needs: pregnant women, poor children, disabled, elderly in nursing homes.

- Fewer people might choose to get covered, but those who got covered would have more options--"skimpier" but cheaper plans available might induce some currently uninsured to buy in.

- Pursue other (non-coverage related) policies like tort reform, reducing regulations and restrictions that could potentially lower costs.

Questions?

Copy of Lecture 3

By umich