Andreas Park PRO

Professor of Finance at UofT

Blockchain and Decentralized Finance:

A 2024-25 Primer

Presenter: Andreas Park

What is a Blockchain?

What is a Cryptocurrency?

Conceptually, what is a blockchain?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

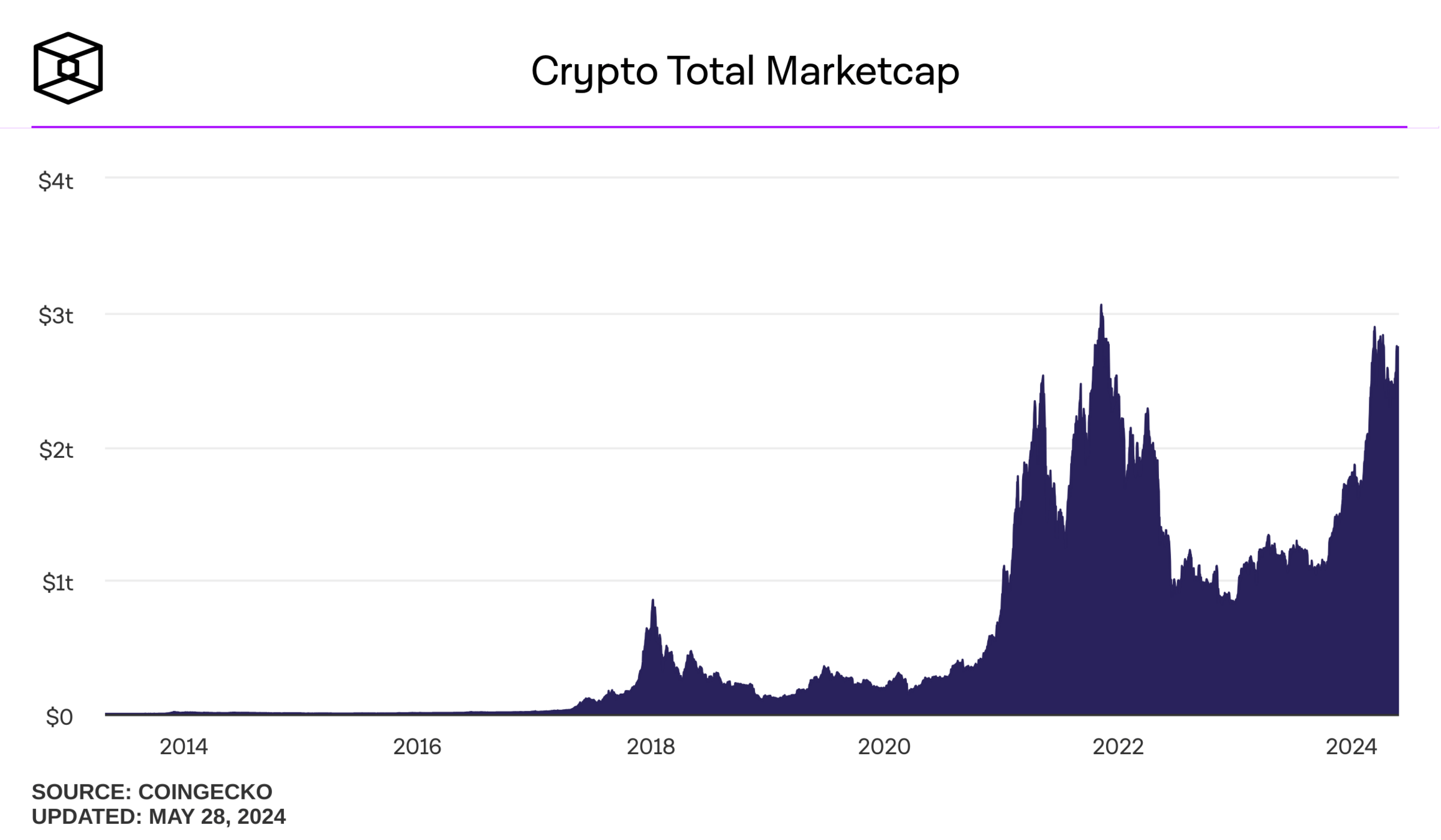

\(\approx\) 50% is bitcoin (but used to be 70%)

Smart contract accounts

Externally owned accounts

controlled by private keys

private

key

public

key

seed phrase

public

address

wallet = software to keep and use private keys

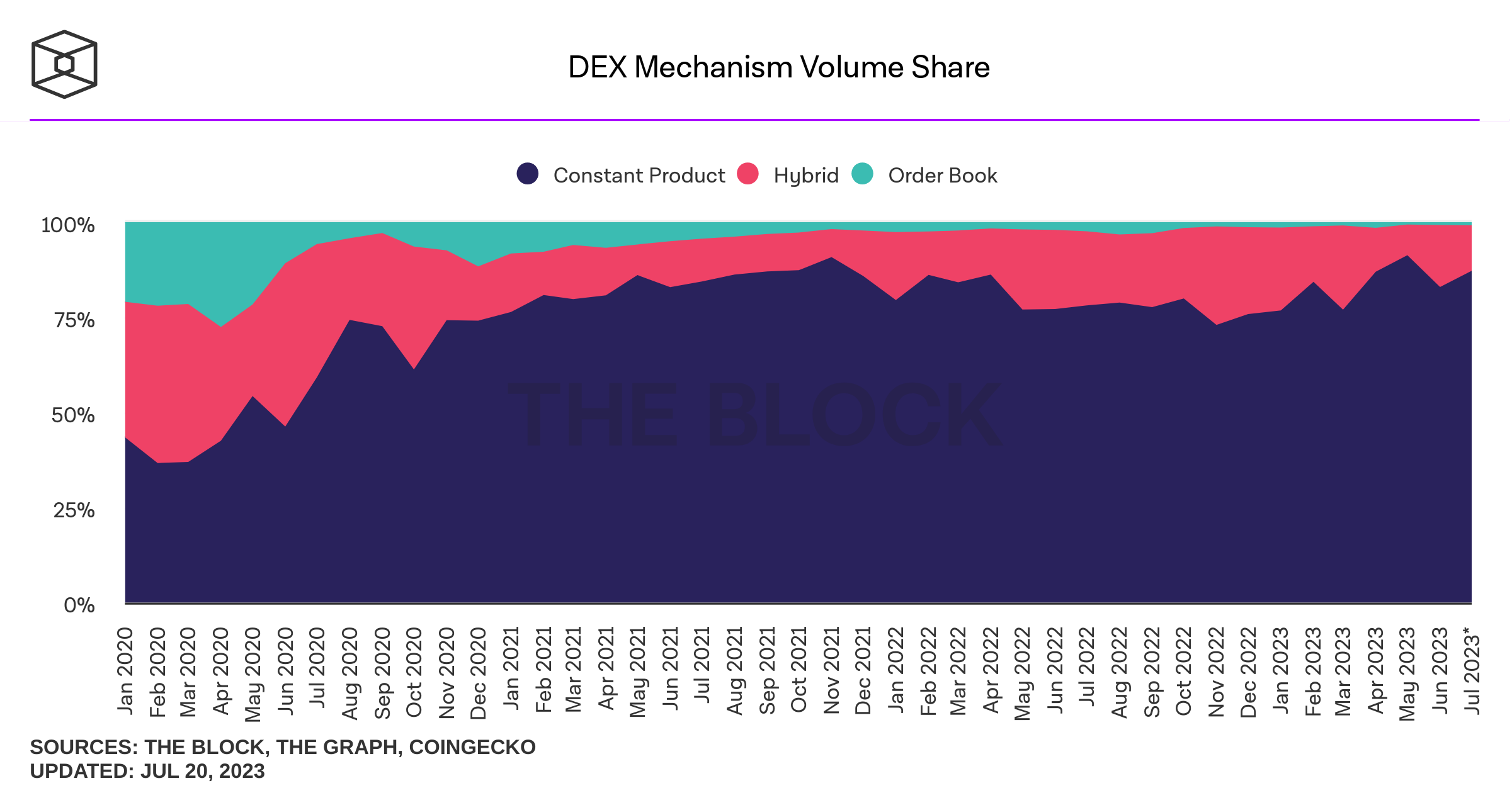

Decentralized Trading

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

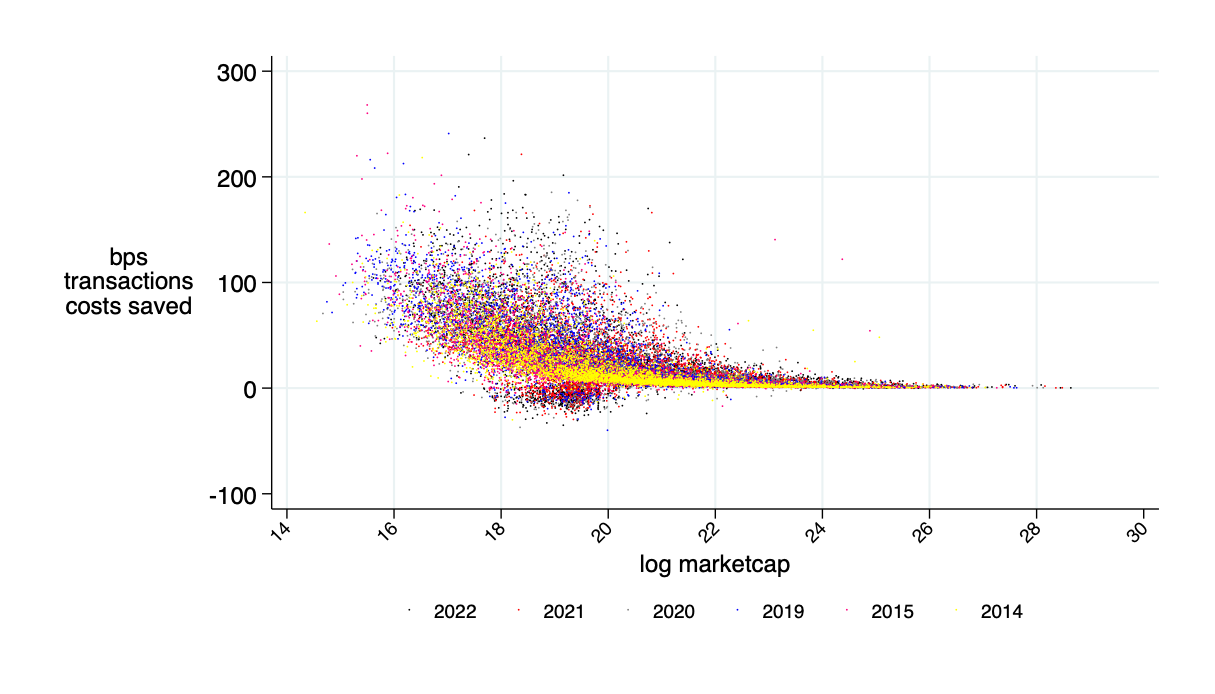

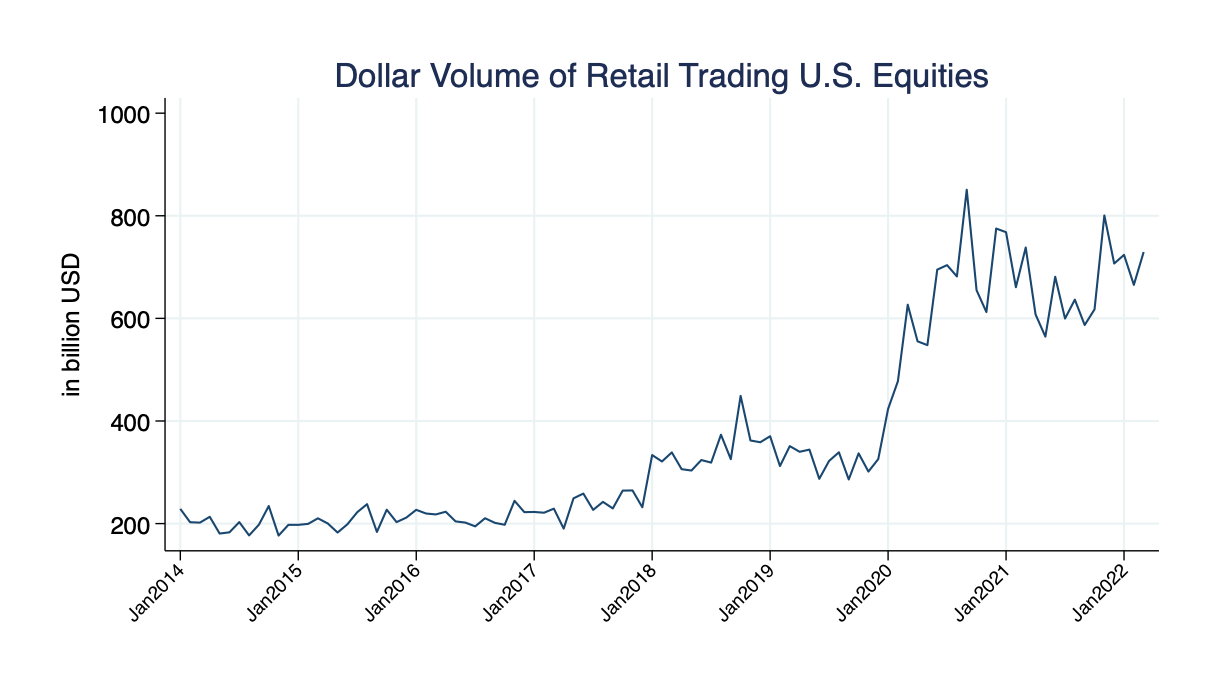

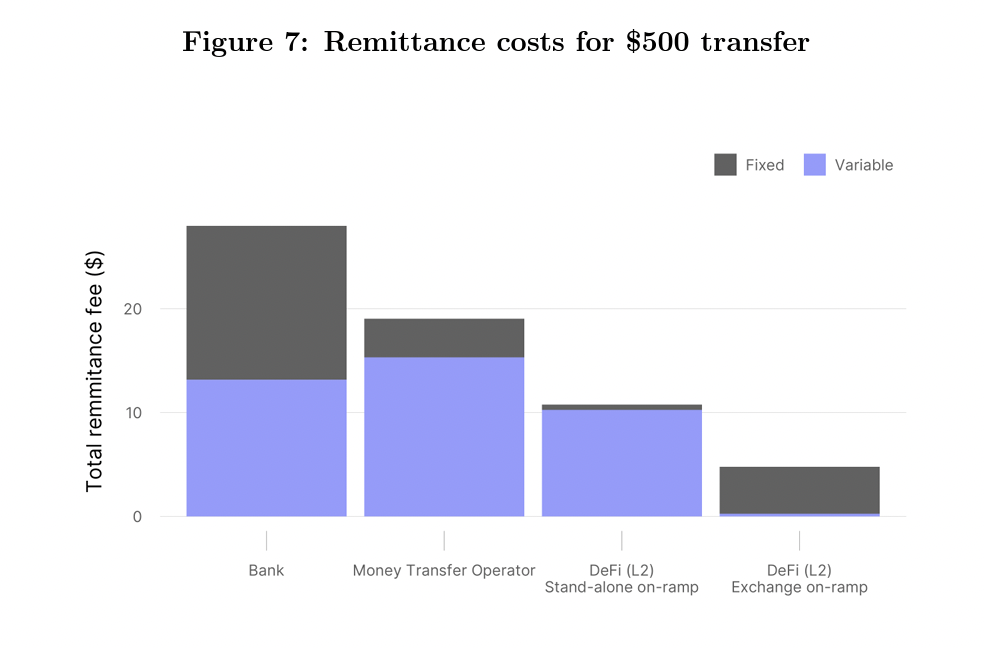

Source of savings:

Possible transaction cost savings when applied to equity trading: \(\approx\) 30%

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

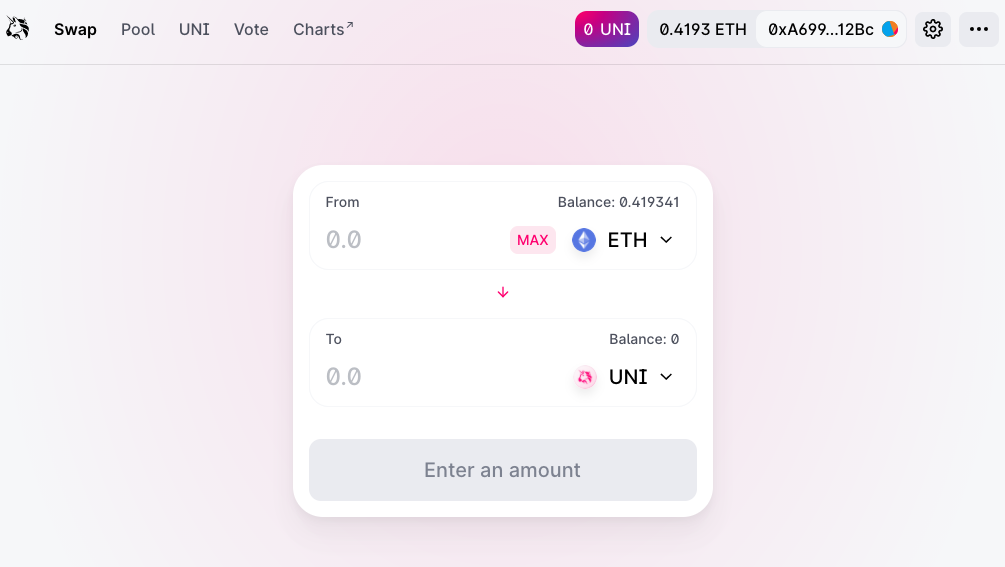

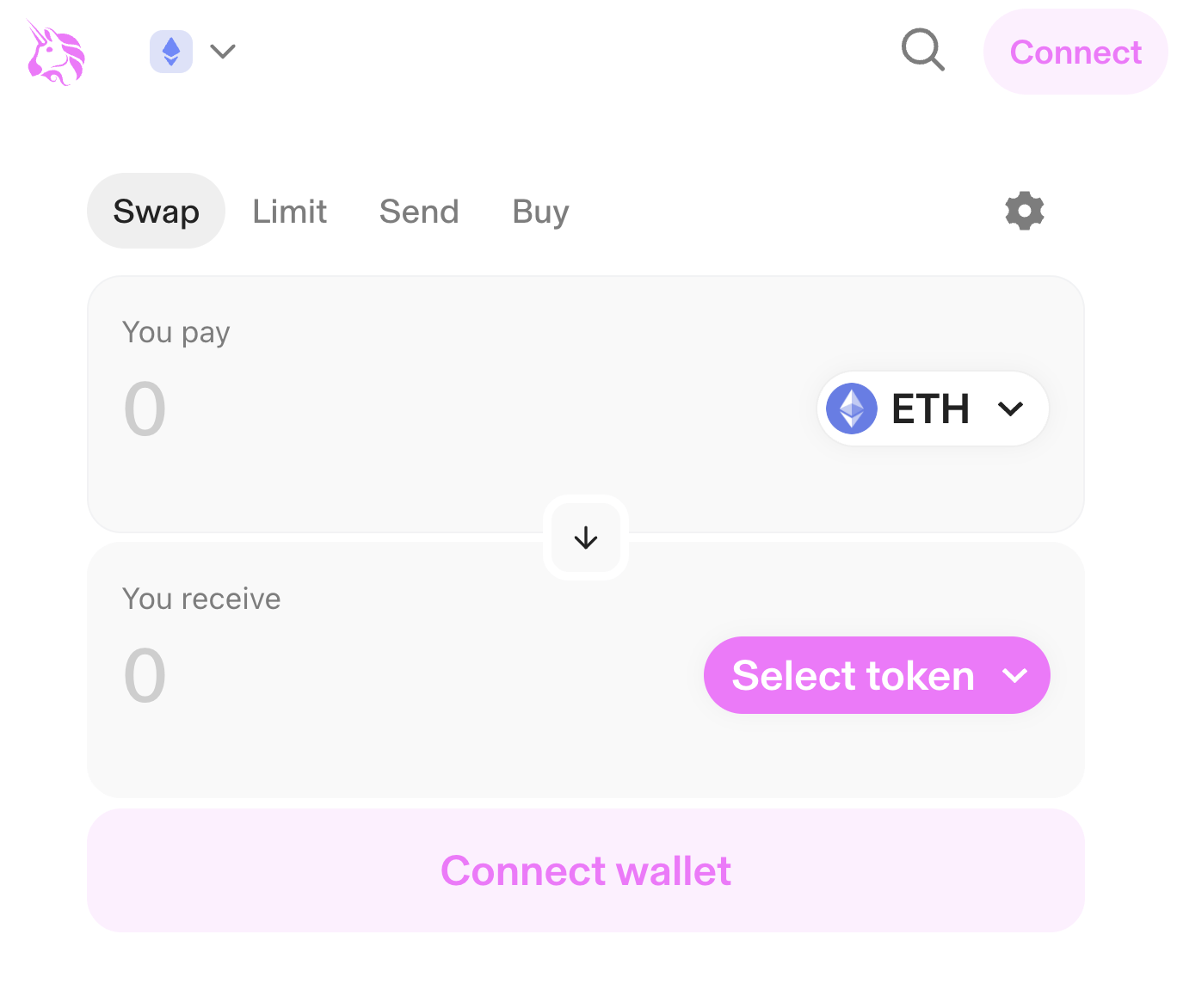

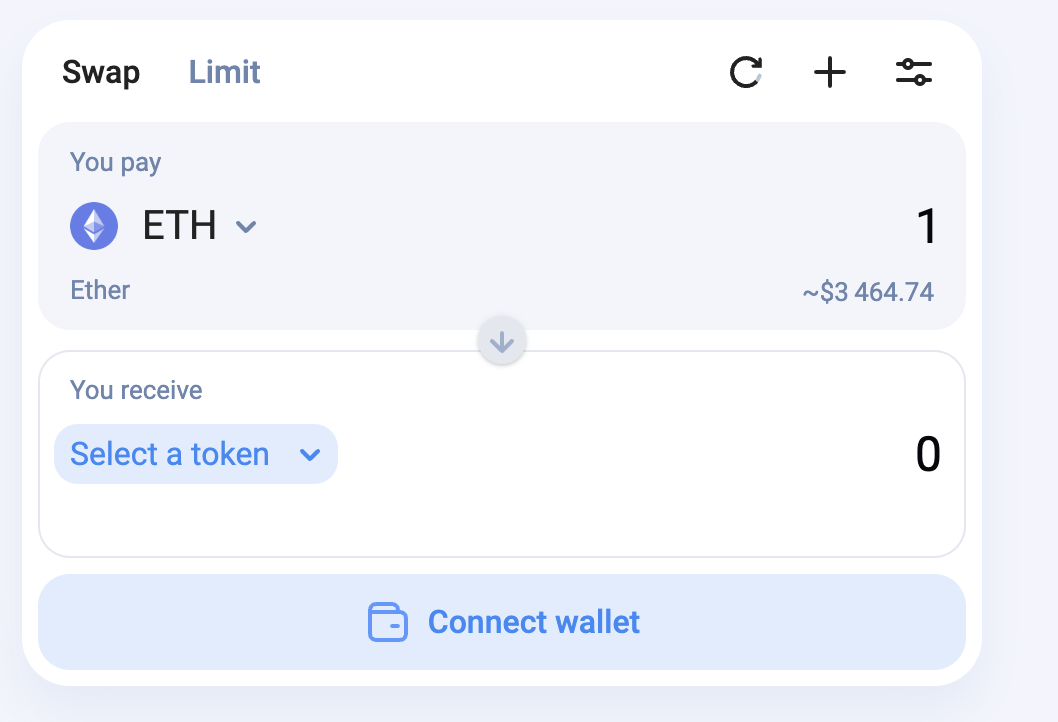

\(\to\) simply connect with MetaMask (or similar wallet)

How does this look in practice?

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

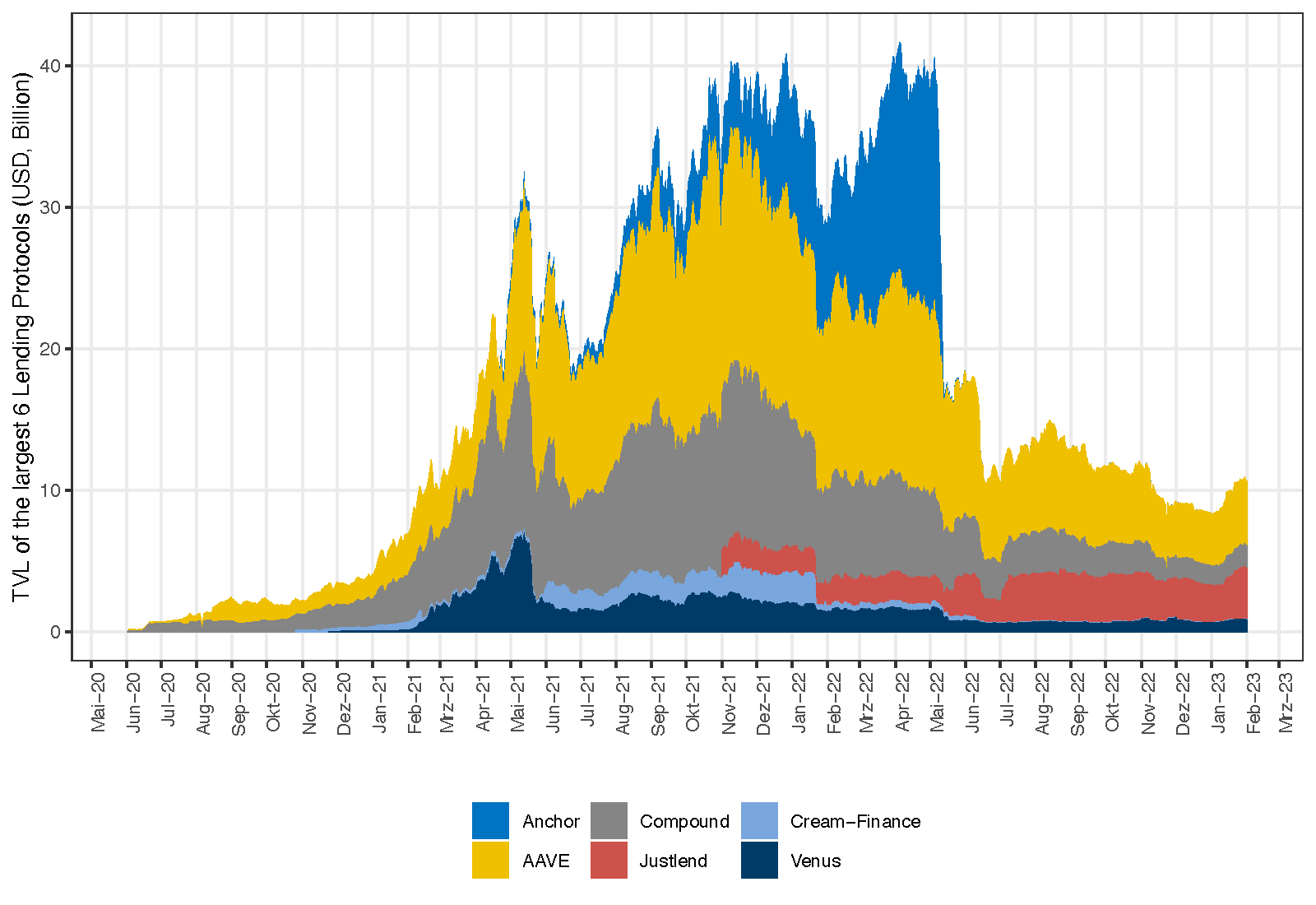

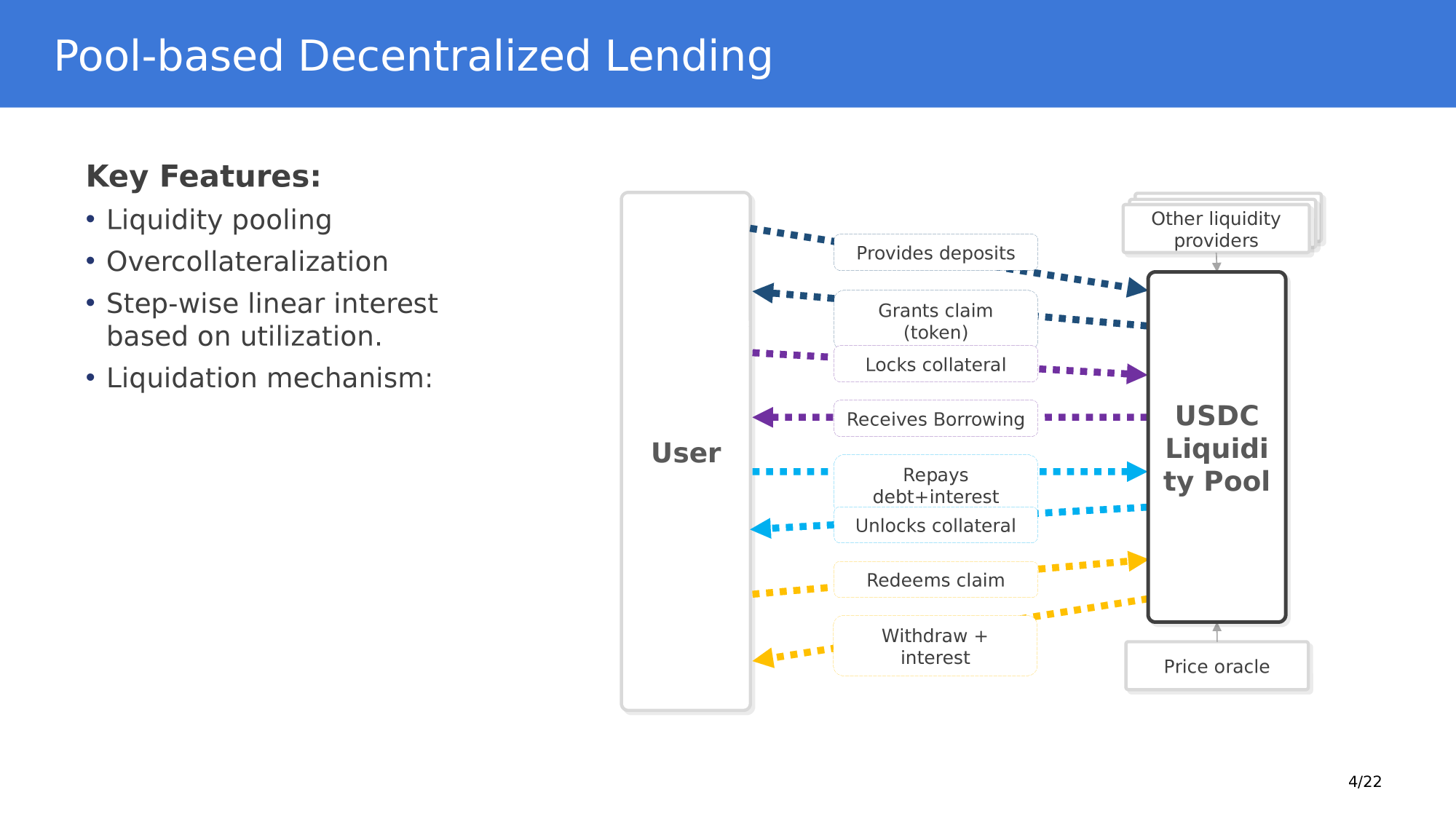

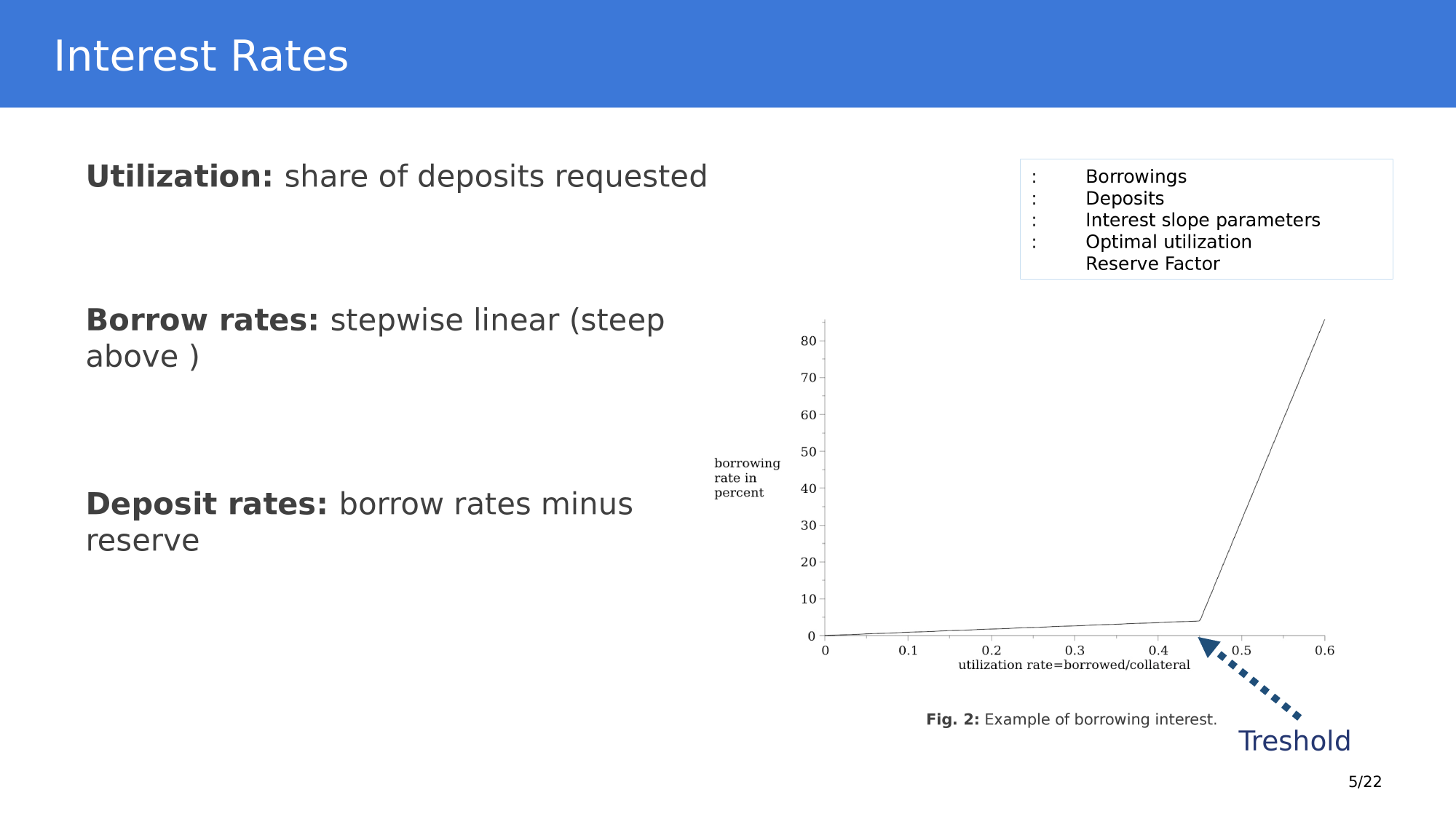

Pool-based lending principles

borrow

provide collateral

Application: Pool-based borrowing and lending

Application: Decentralized Borrowing & Lending

Obvious Smart Contract Application: Automate Investment Strategies

idea: create new mutual fund like asset

"yield aggregator:" push capital where rate of return is highest

Flash Loans

5. repay DAI

for loan

with health factor <1

liquidation

opportunity

1. flash-borrow DAI

2. repay loan

with DAI

3. claim

collateral ETH

4. convert ETH to DAI

What roles do tokens play?

What roles do tokens play?

recall the differences

\(\to\) key feature: no necessary intermediaries

Problems:

lesser problem because

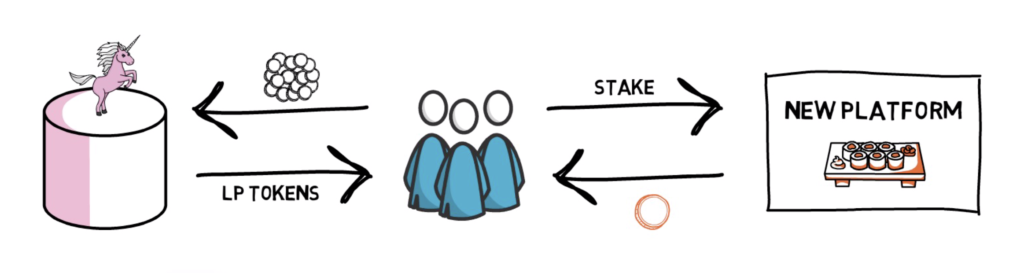

Common solution: create a reward token! Here's how this works

Step 4: users receive a reward token based on the time that they lock up the "receipt" token

Step 3: users lock up the "receipt" token in a smart contract

Step 2: users contribute liquidity and get a "receipt" token

Step 1: create reward tokens and deposit into a smart contract

borrow

provide collateral

Application: Pool-based borrowing and lending

Same problems as with trading:

But: in contrast to trading, here you need both!

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

Without intermediaries:

platform economics!

incentives for both?

What value do these tokens have?

Vampire Attacks and Other Shenanigans

Source: https://finematics.com/vampire-attack-sushiswap-explained/

another common trick:

Application 3: Oracle Nodes Ecosystems

Chainlink

https://market.link/overview

A Taxonomy of Tokens

What's a crypto-token and what's special about it?

Tokens by use

payments:

utility

stablecoins

governance

asset

derivatives

Disclaimer: this list in non-exhaustive, new ideas and concepts come up every day!

Asset Tokenization or

"The Creation of Asset-Linked Tokens"

Tokenization is coming

Tokenization of stocks is nothing new: American Depository Receipts

foreign investor/

issuer

domestic bank with foreign representation

ADR issuing bank handles

Is this a workable model for blockchain- tokenization of existing assets?

foreign representation of domestic bank/ its custodian

domestic depository bank

S.E.C.

registration with form F-4

domestic broker

issues and cancels ADRs

domestic investor

lets investors own and trade ADRs

domestic

market

deposits shares

Blockchain Tokenization has many options

existing investor/

issuer

token issuance platform

investor

wallet

instruct to create tokens

deposits shares

custodian bank

deposits shares

creates tokens and sells to investors

centralized or decentralized

market

S.E.C.

registration

Tokenization & DeFi Solutions

DEX Accounting is complicated

Some solutions exist

Tokenization FAQs

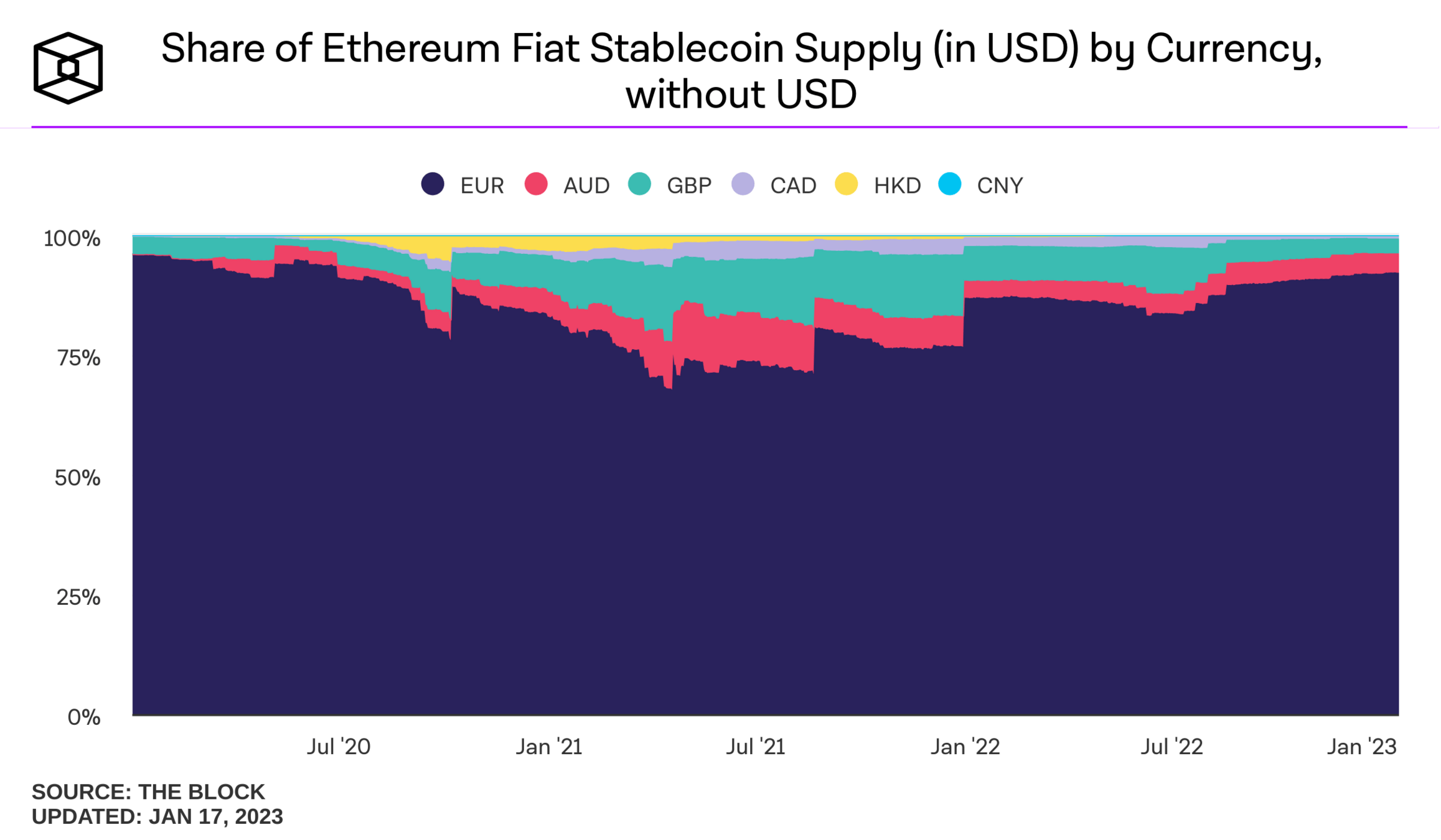

What is a stablecoin?

digital representation of a unit of a fiat currency on a blockchain

pulled from Nick Carter's talk on "Will stablecoins serve or subvert U.S. interests?"

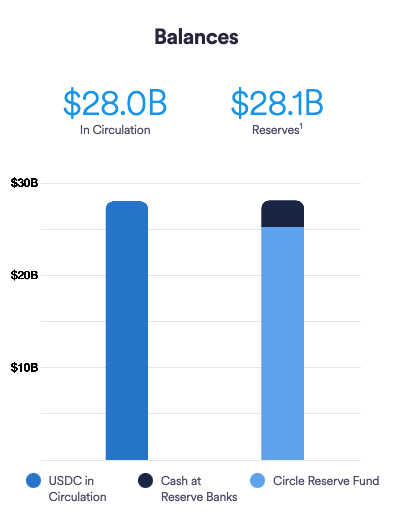

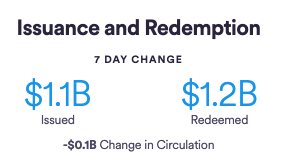

Collateral Backed Stablecoins: USDT & USDC

\(\Rightarrow\) 5% over-collateralized

primary market acces: 6 entities only

Collateral Backed Stablecoins: USDT & USDC

primary market acces: 560+ entities

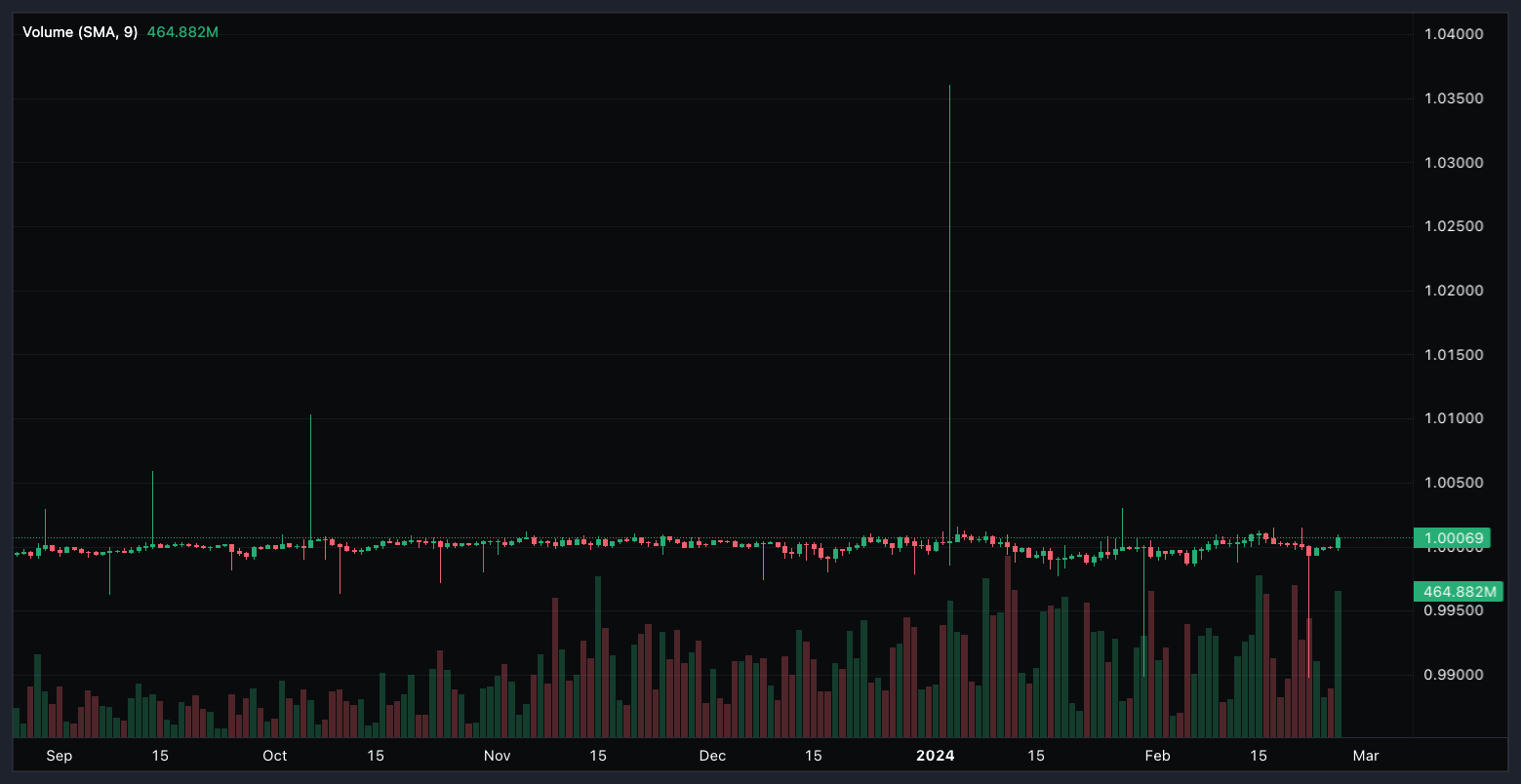

What makes a Stablecoin stable?

USD-USDT (6 months)

\(\Rightarrow\) need a primary/reference market mechanism to allow for forces of arbitrage to align prices

Arbitrage when price(stablecoin)>$1

collateralized stablecoin

arbitrageur

issuer/ primary market

secondary market

collateralized stablecoin

arbitrageur

Arbitrage when price(stablecoin)<$1

issuer/ primary market

secondary market

Stablecoin use cases

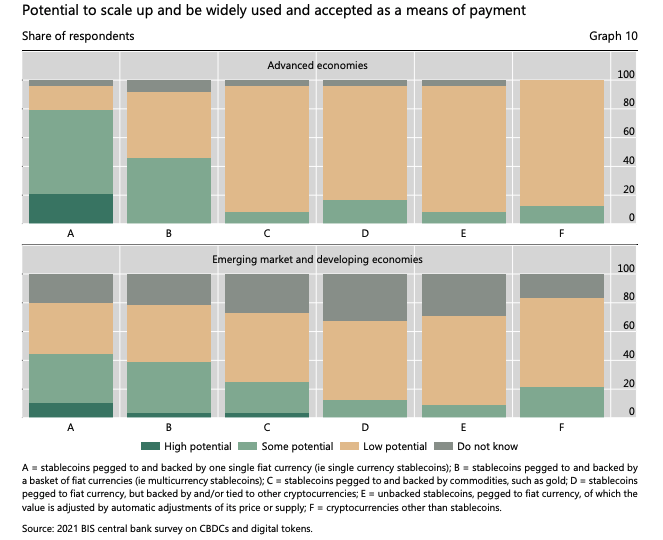

What do central bankers think about stablecoins?

BIS Survey of Central Banks:

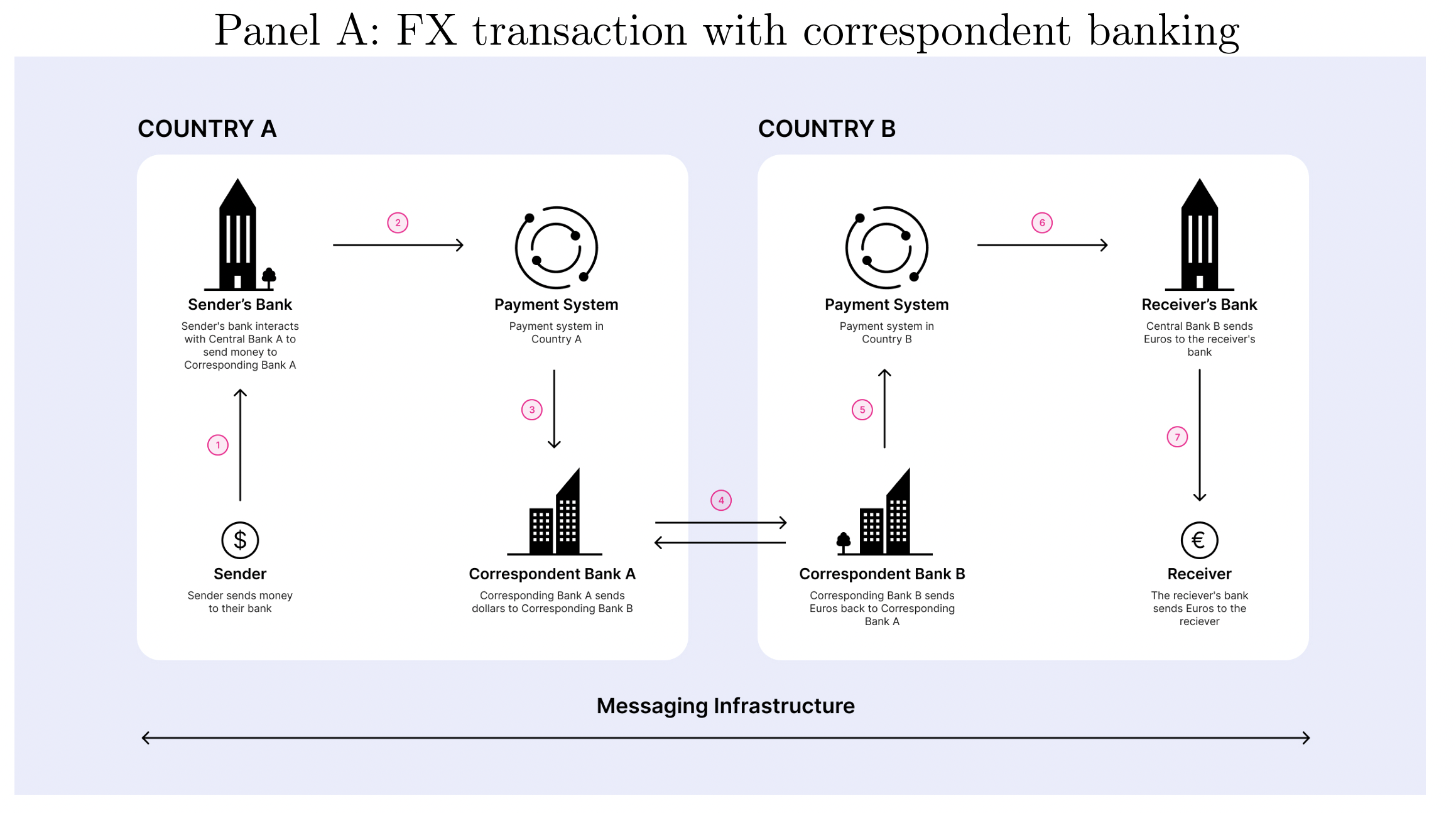

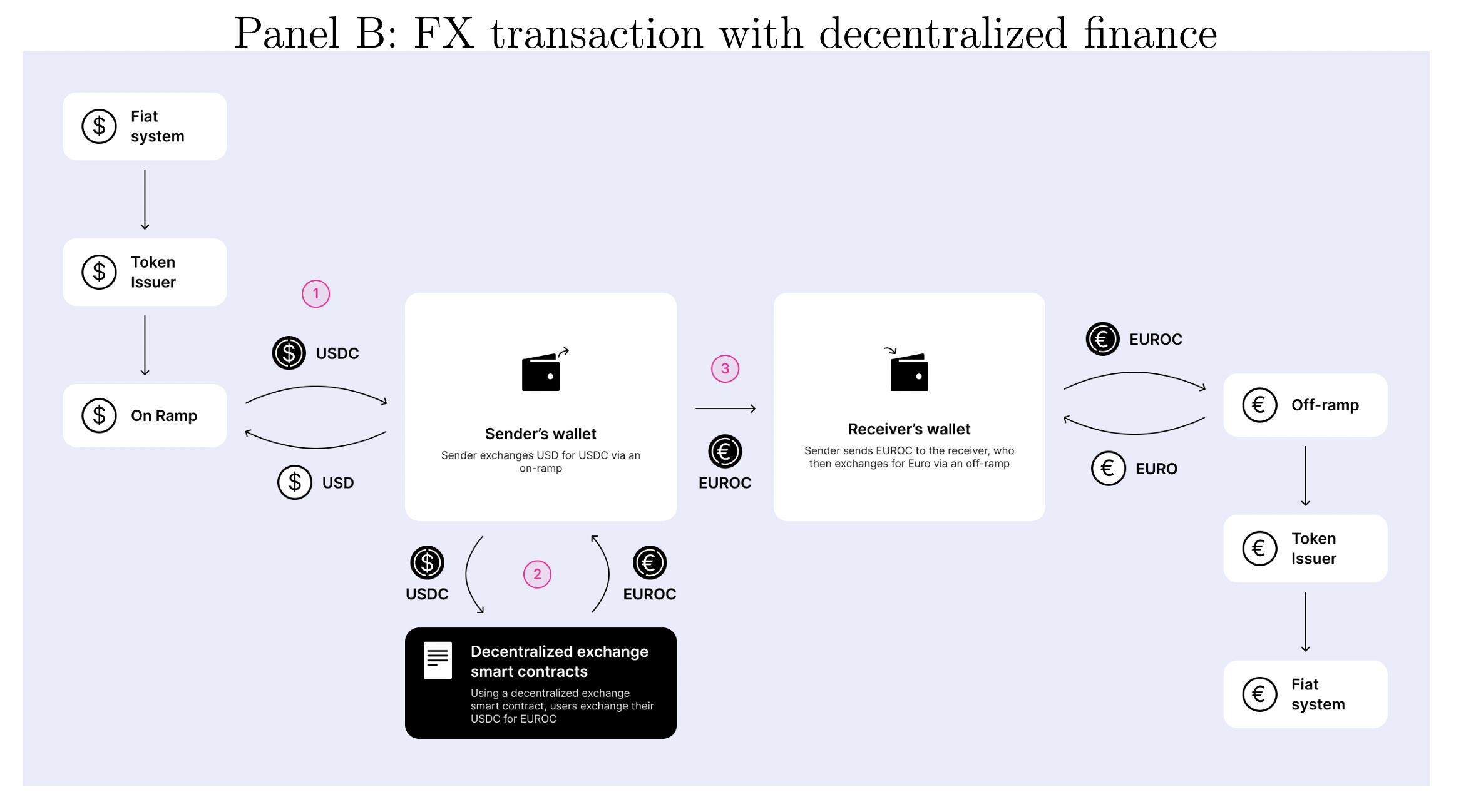

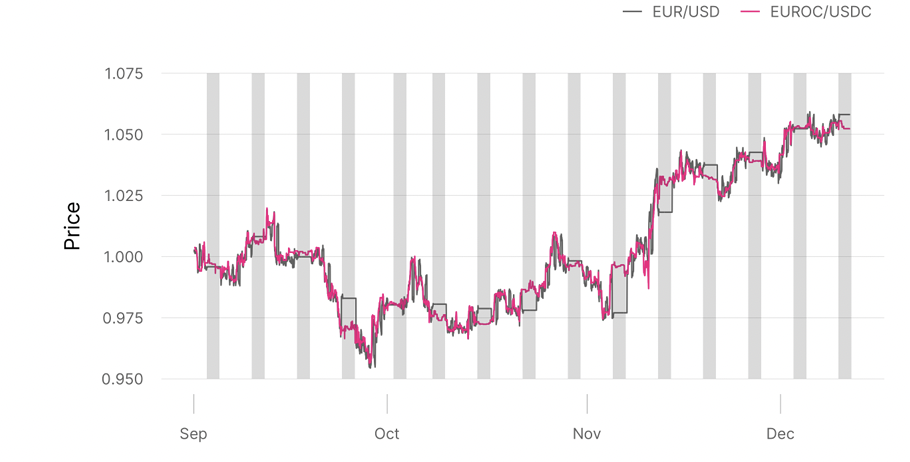

Source: On-chain Foreign Exchange and Cross-border Payments by Austin Adams, Mary-Catherine Lader, Gordon Liao, David Puth, Xin Wan (2023) [team from UniSwap Labs]

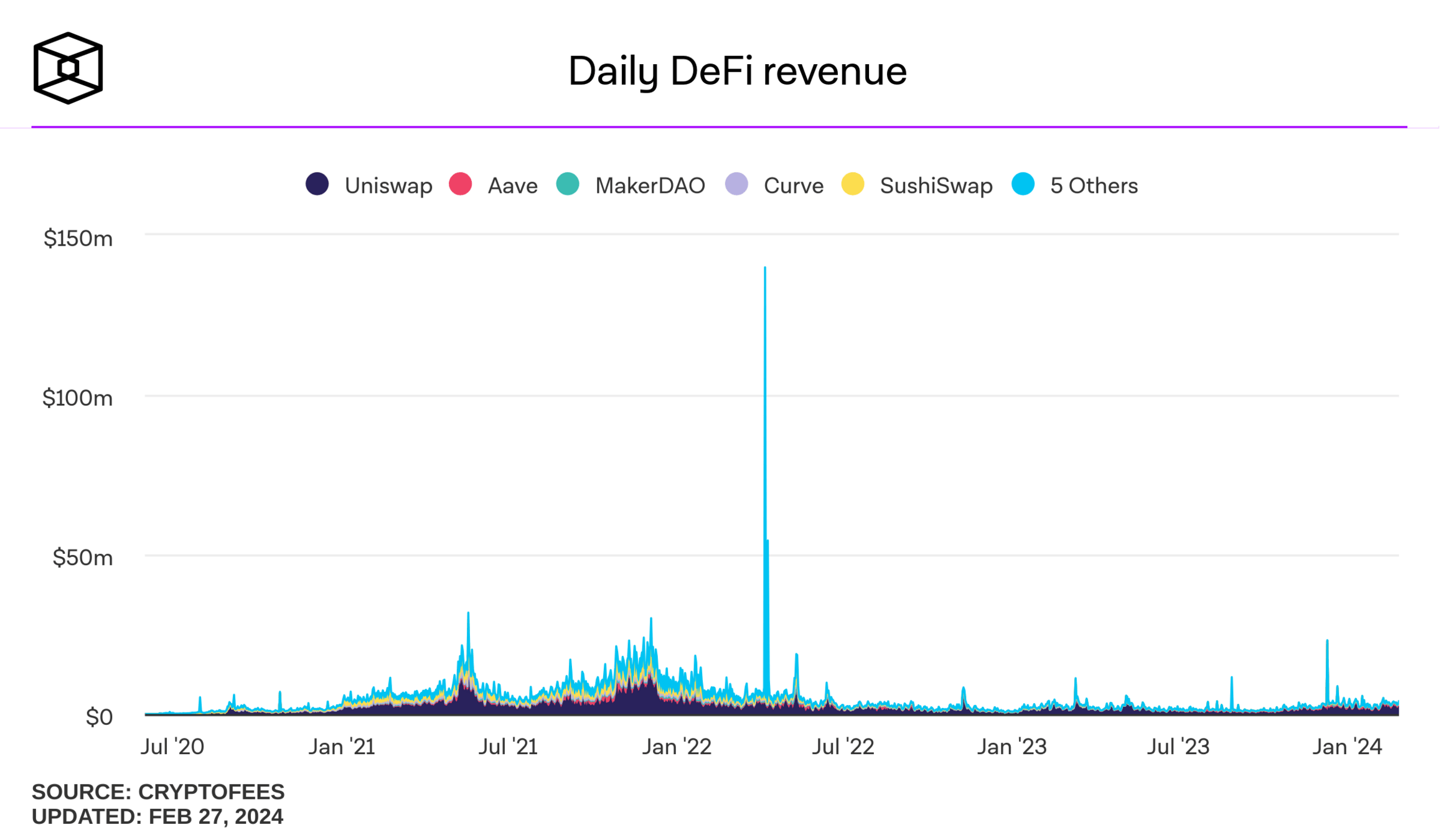

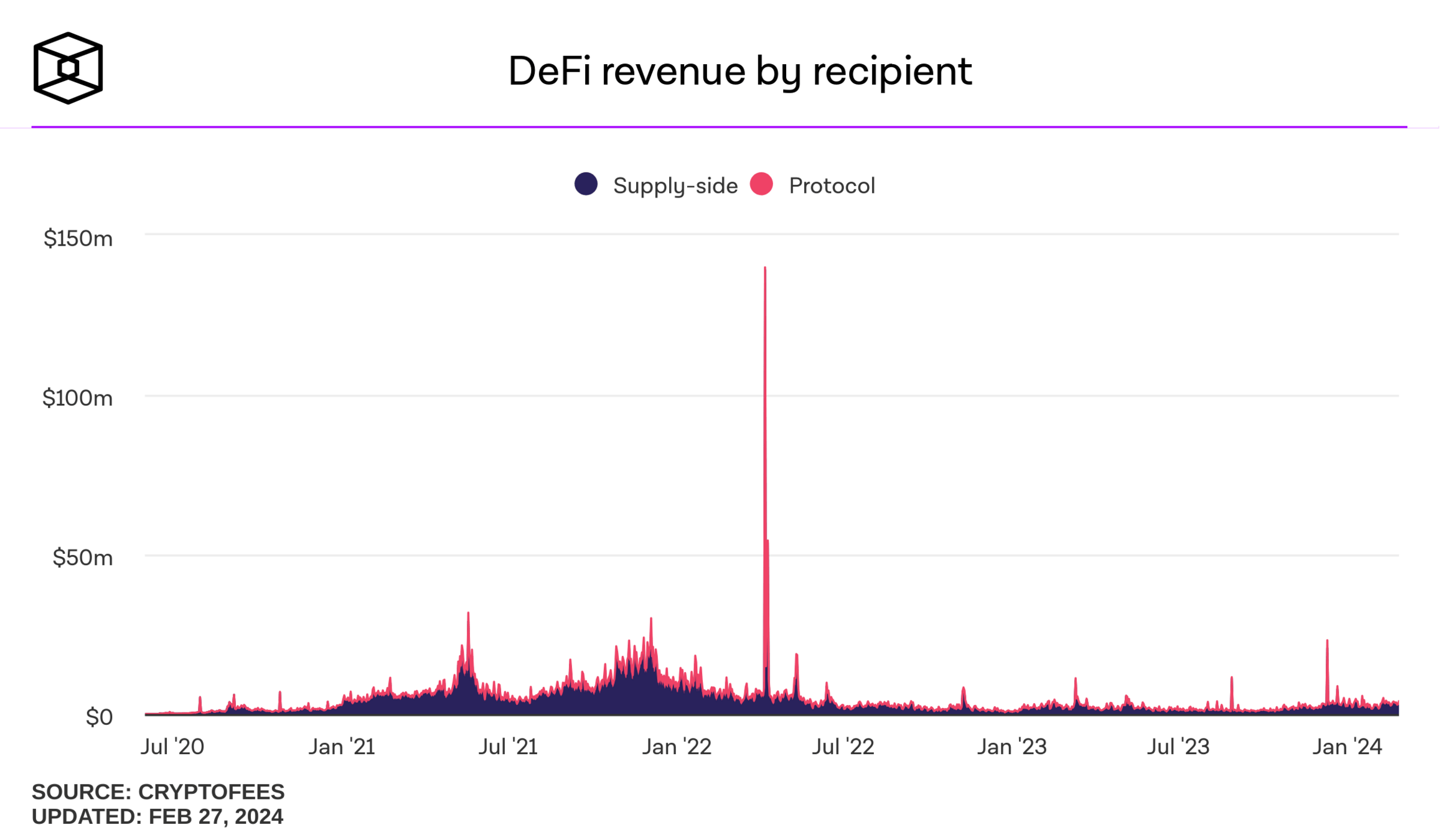

DeFi fees:

Run Risks

Stablecoin Run Risks

The "U.S. President's Working Group on Stablecoins" would essentially make issuers narrow banks (deposits largely backed only by reserves)

Challenges

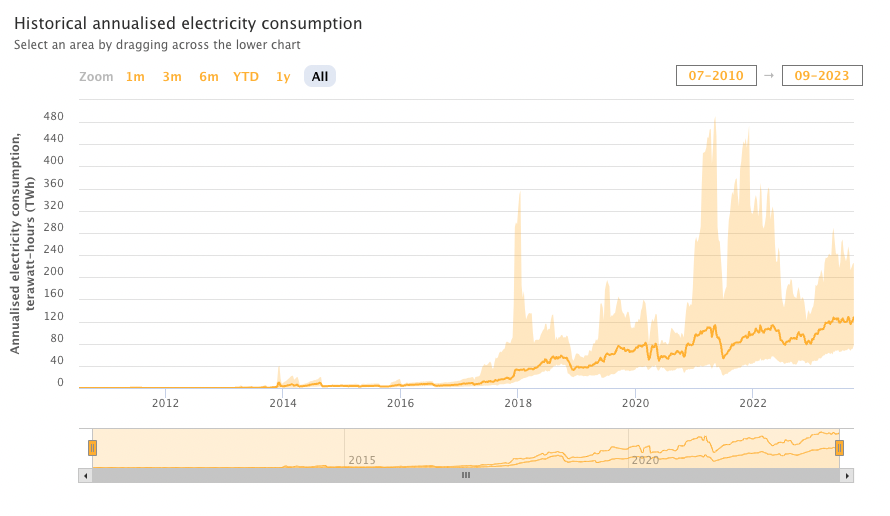

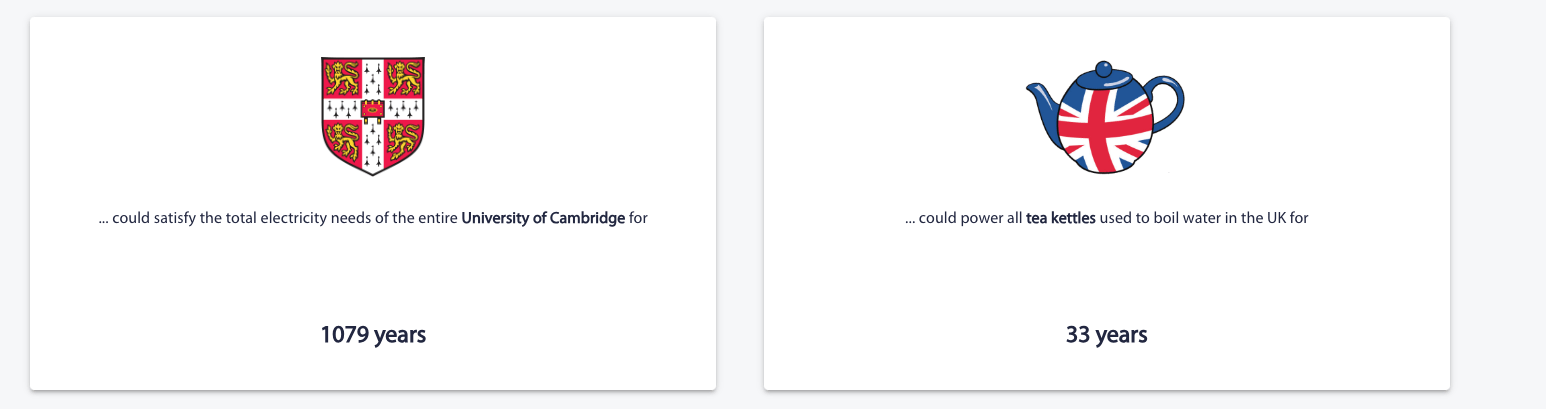

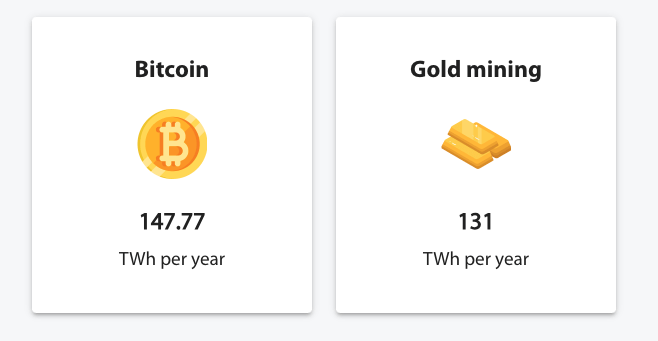

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

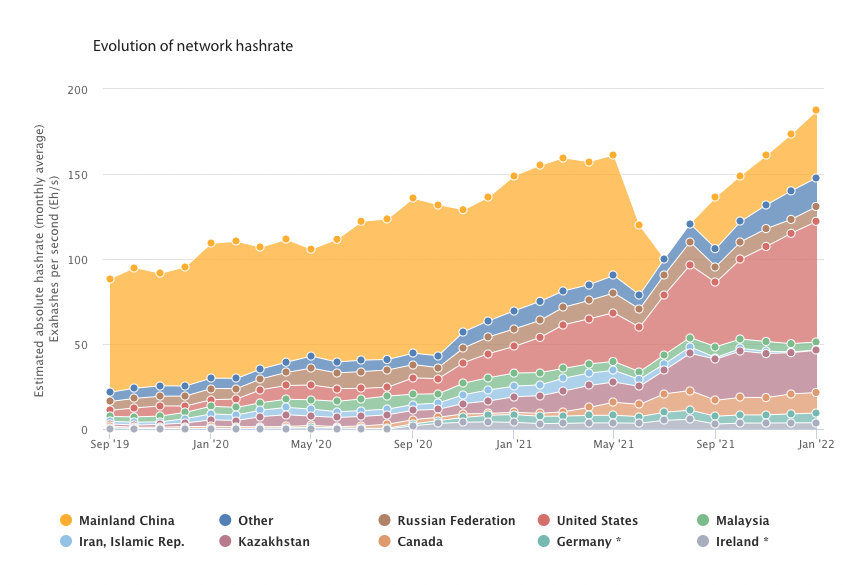

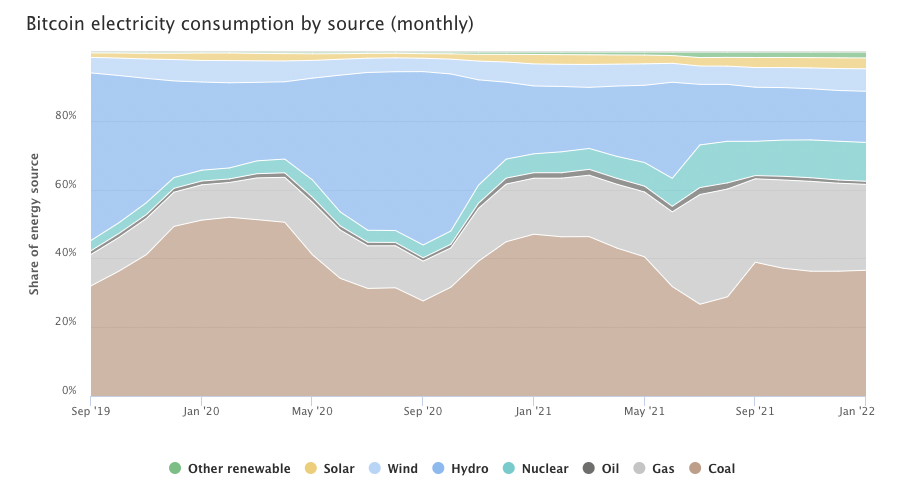

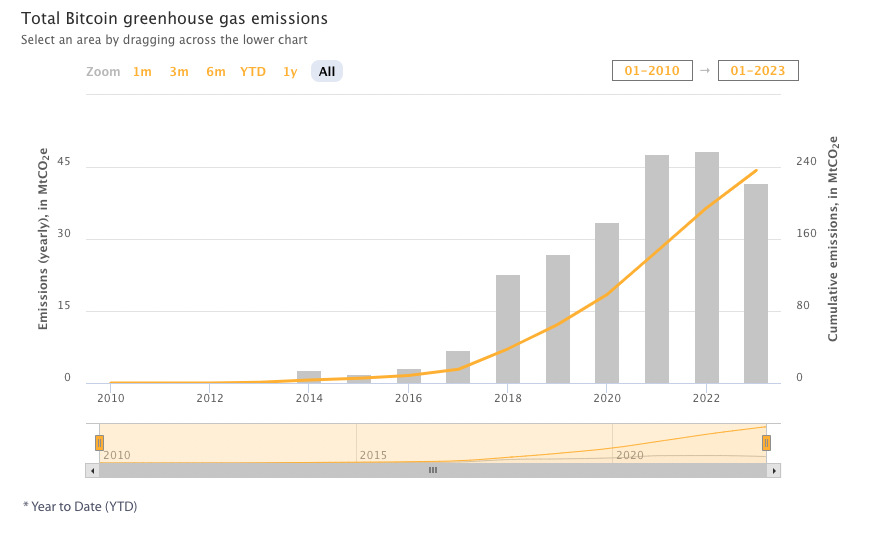

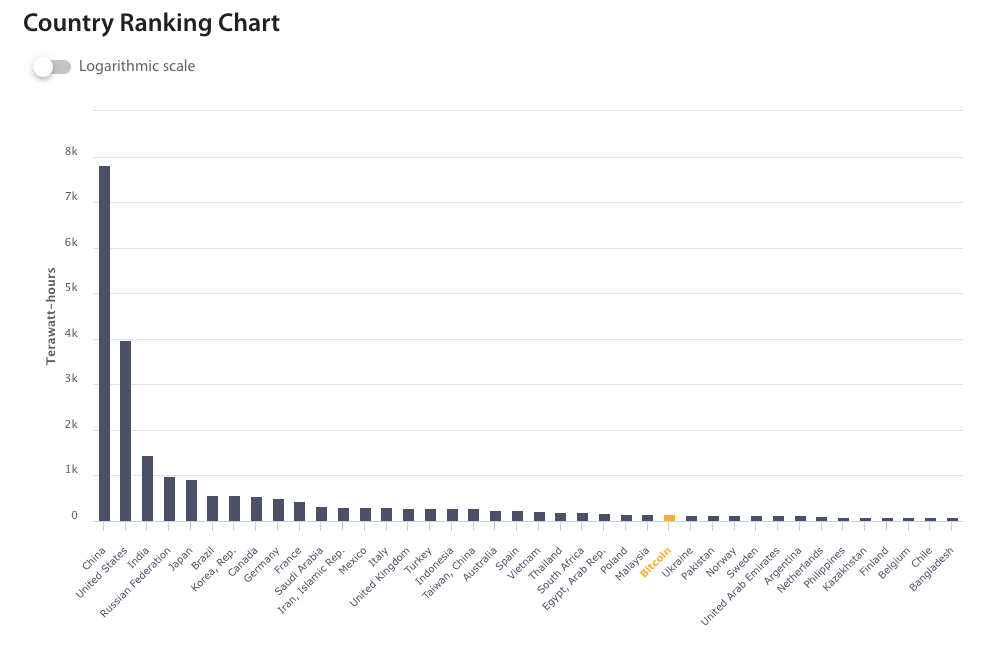

Challenge 1: Energy Consumption

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

Challenge 1: Energy Consumption

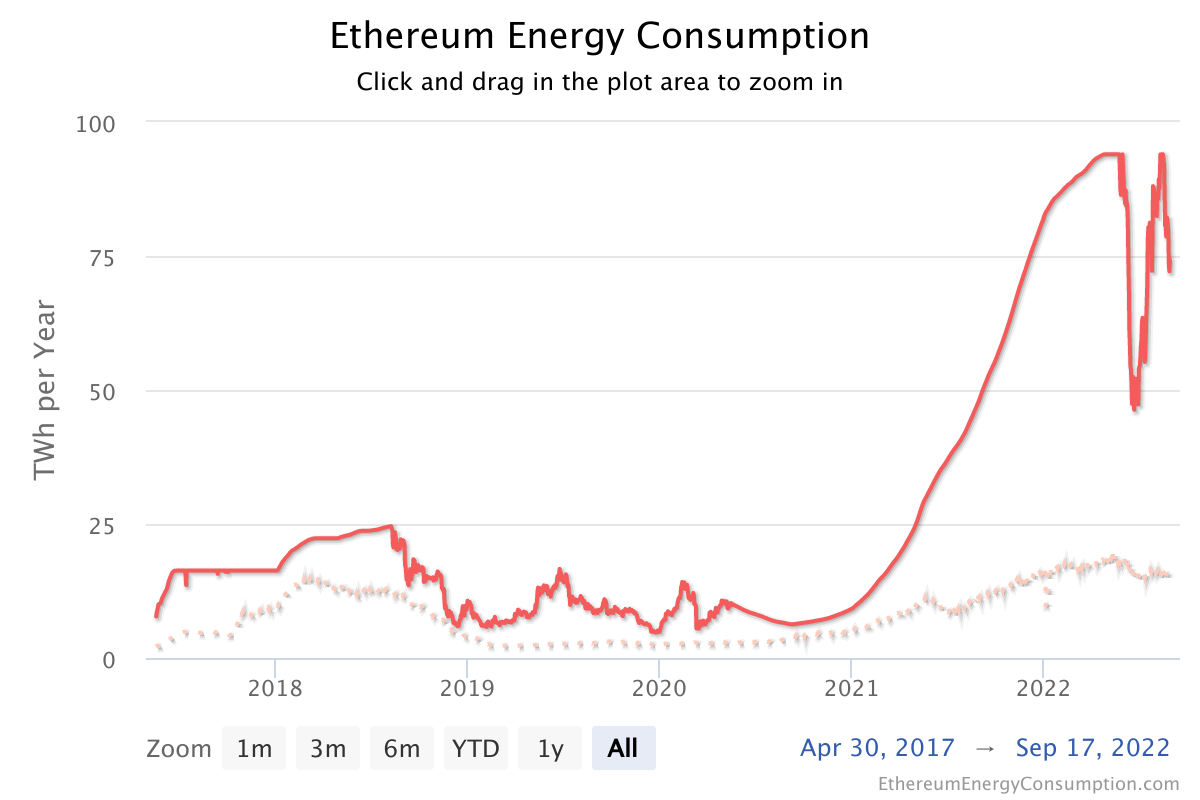

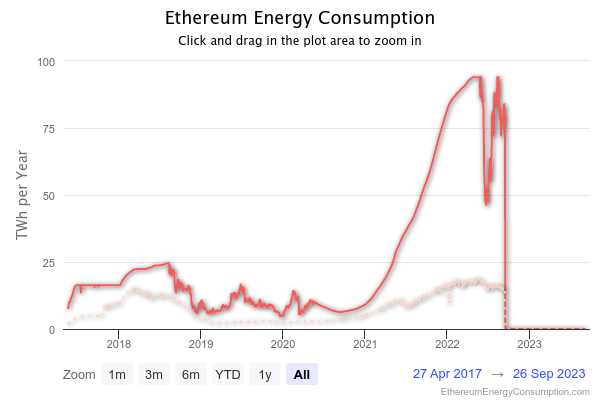

Ethereum Challenge 1: Environment

problem solved

| transactions per second | T per 12 hours (business day) | |

|---|---|---|

| Bitcoin | 7 | 302,400 |

| Ethereum | 30 | 1,296,000 |

| Algorand | 2000 | 86,400,000 |

| Conflux | 4000 | 172,800,000 |

| Athereum | 5000 | 216,000,000 |

| Payments Canada ACSS | 648 | 28,000,000 |

| US retail | 7639 | 330,000,000 |

| Canada number of equity trades | 46 | 2,000,000 |

| Orders on Canadian equity markets | 3588 | 155,000,000 |

Tweaks: lighting network (BTC) or side chains, SegWit, blocksize possible, but there are limits

microtransactions, IoT, and other smart contract use cases place very high demands

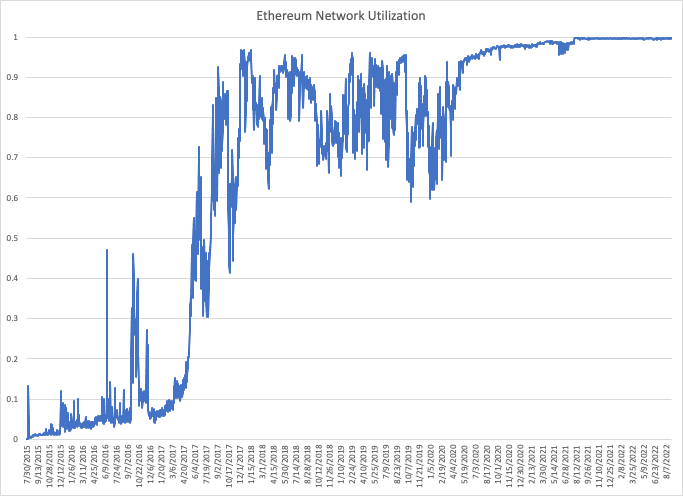

Ethereum Challenge 2: Throughput

Ethereum Challenge 2: Throughput

Source: Etherscan w re-scaling

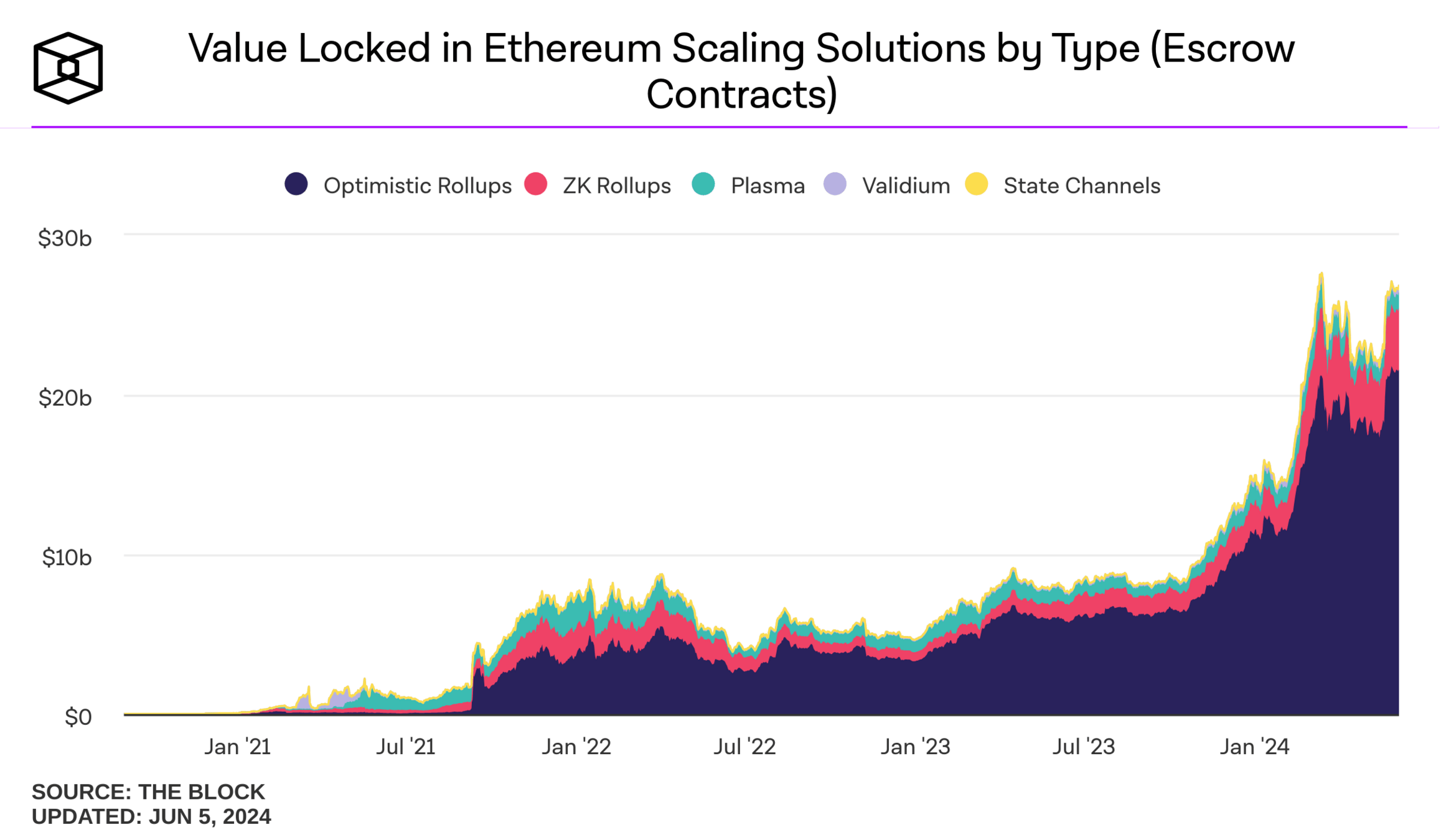

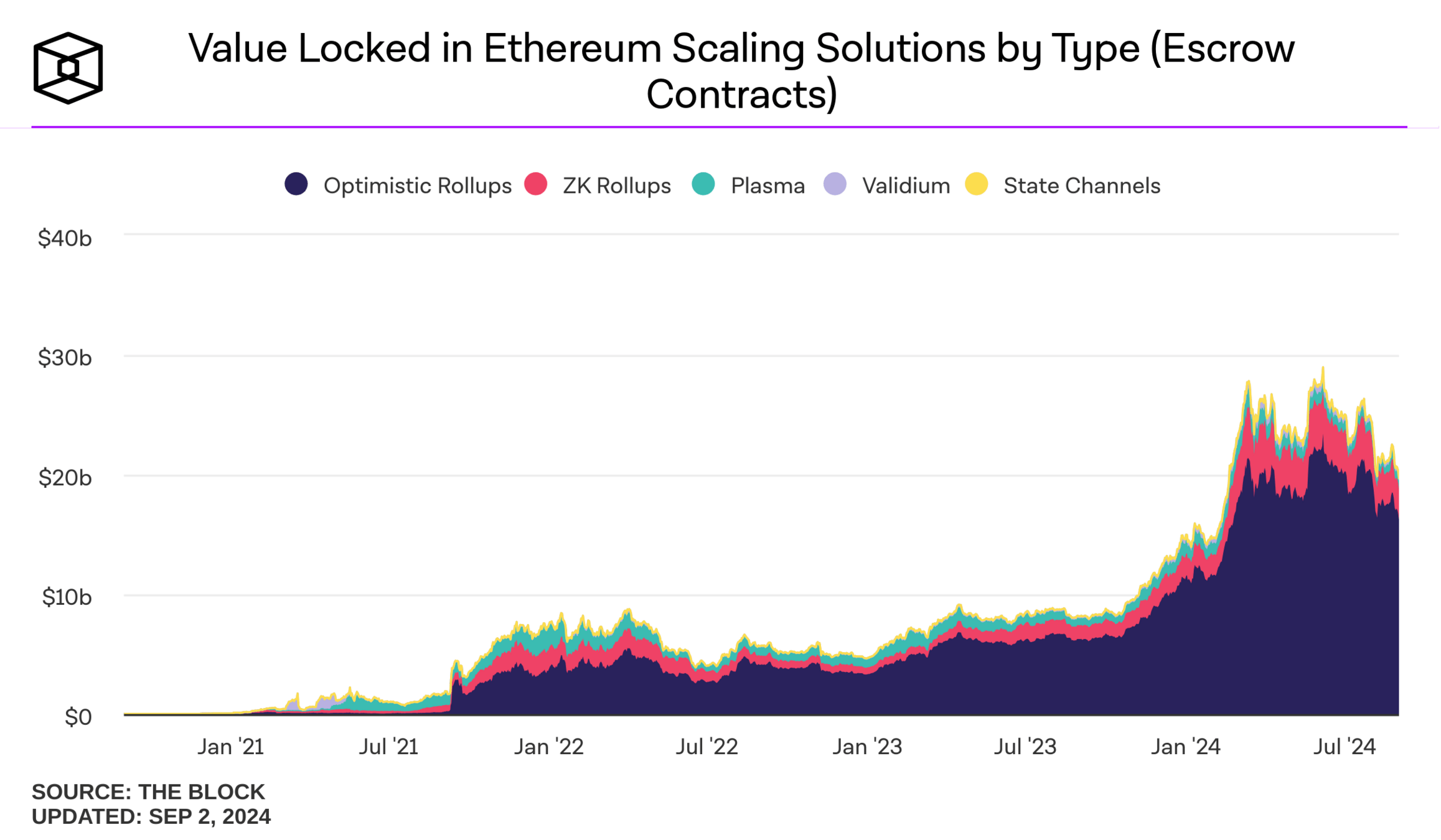

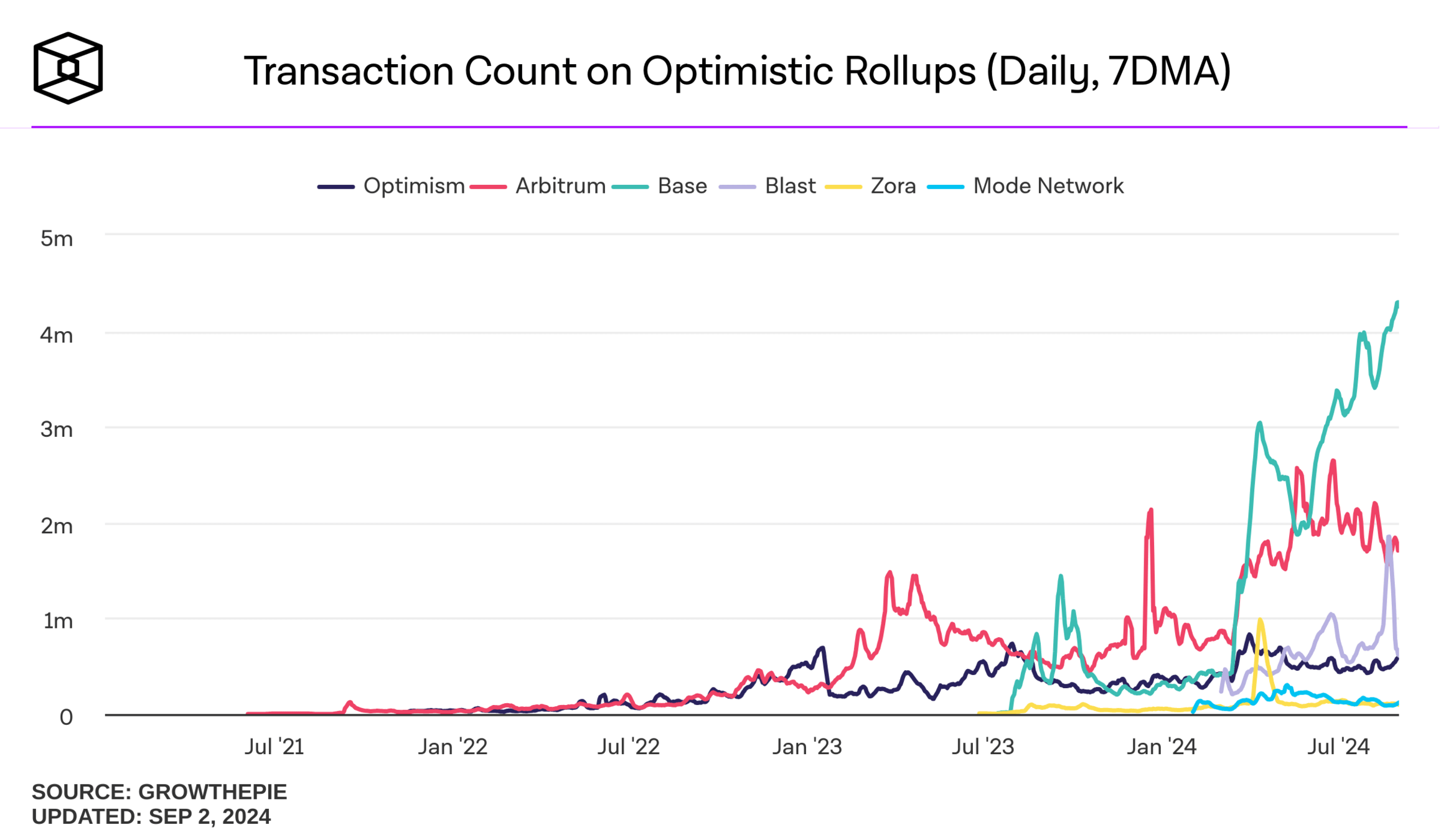

Ethereum Throughput Solution: L2s/Rollups

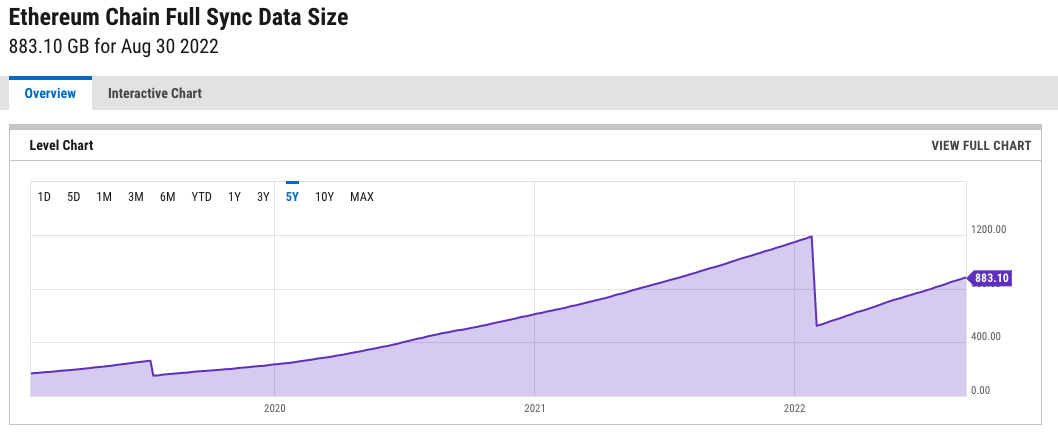

Ethereum Challenge 3: State Size

Source: Ycharts

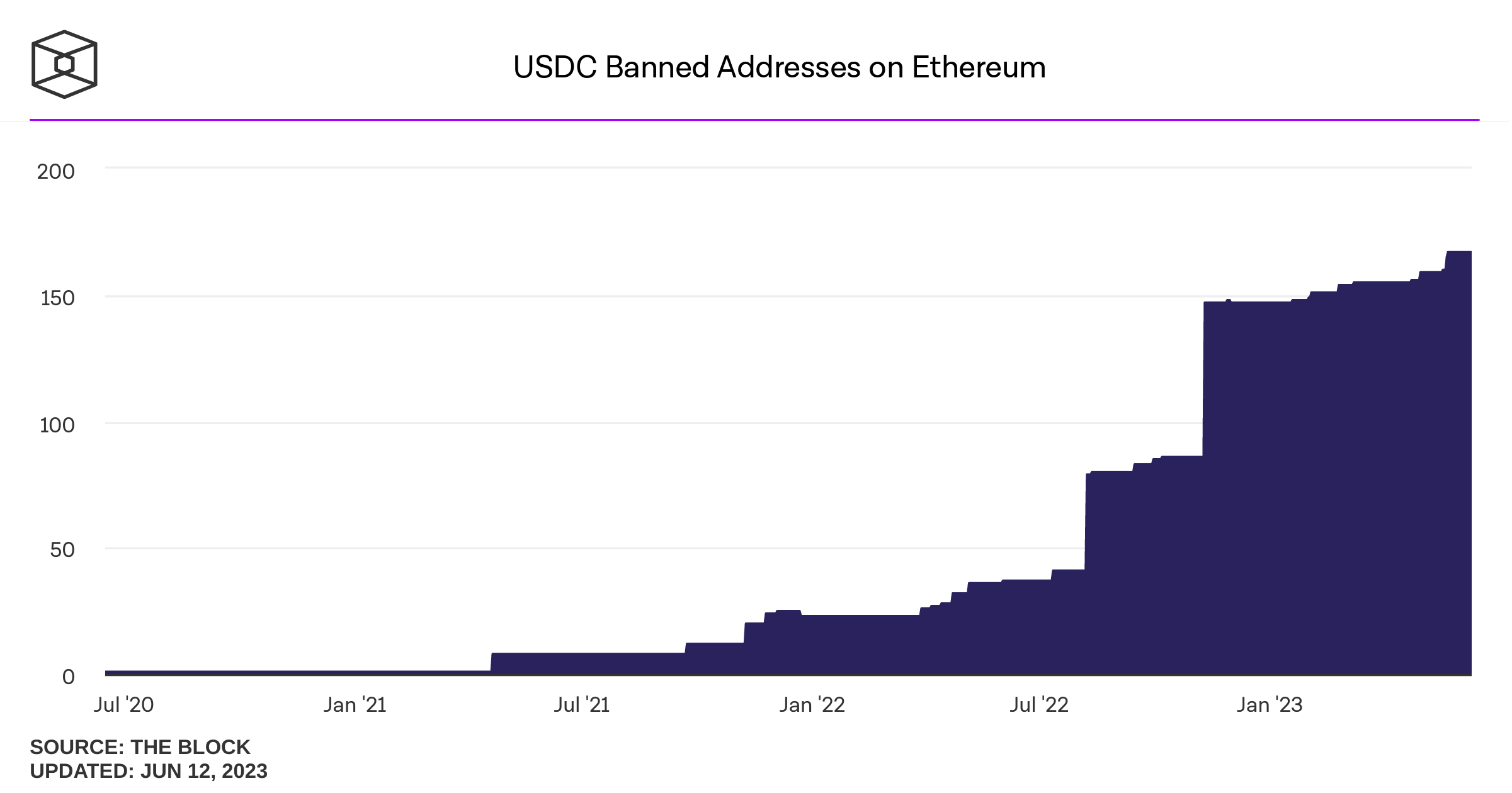

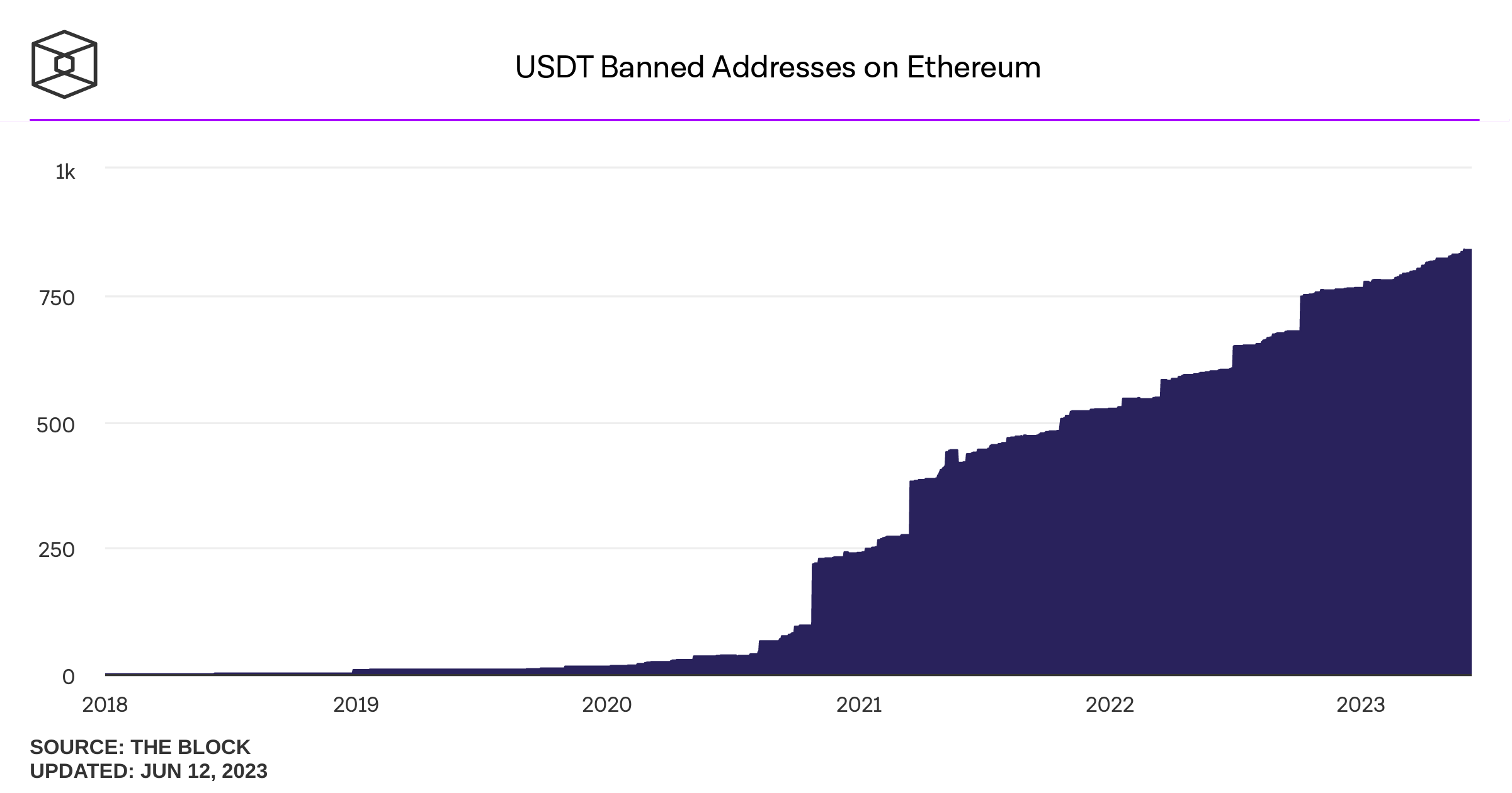

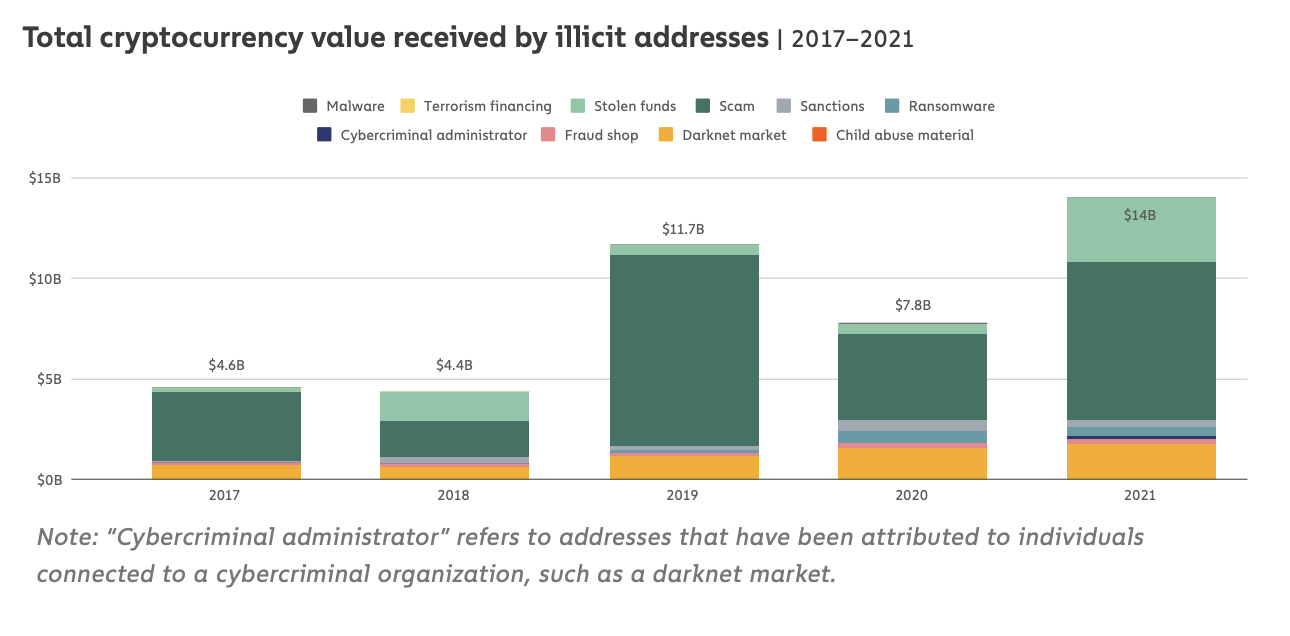

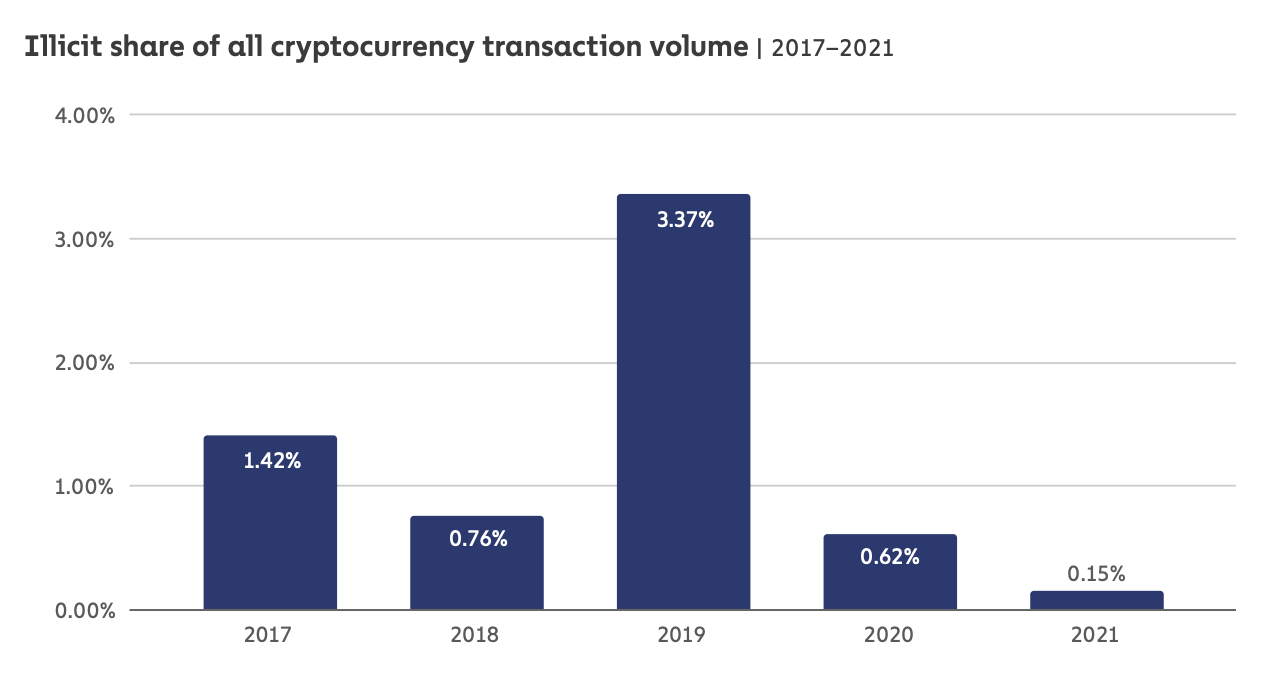

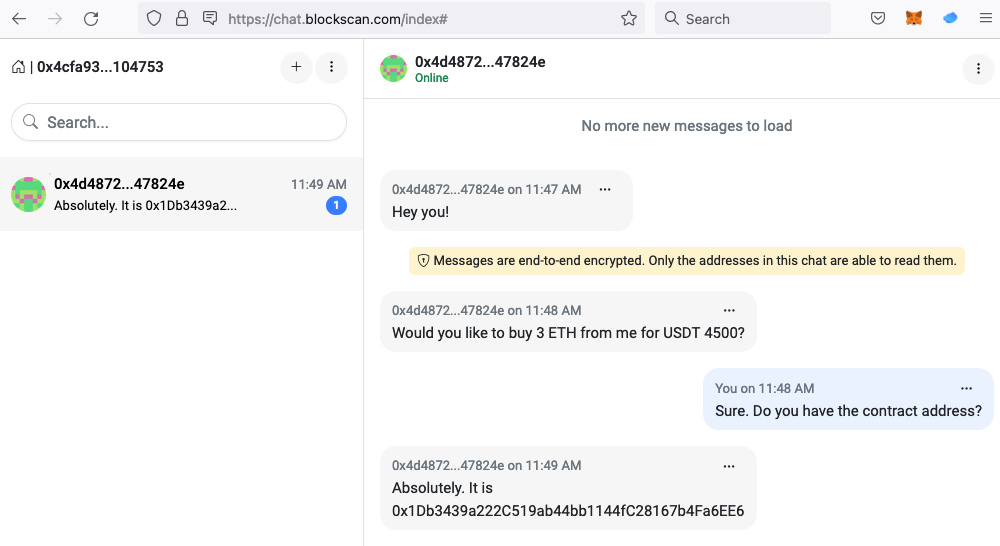

Money Laundering and Crime

What's special about crypto-crime?

criminals don't use USDC - why are we so worried?

extra info:

"The approximate amounts in USD received by wallets on the TRON blockchain associated with terrorist entities:

Source: https://inca.digital/intelligence/crypto-intelligence-alert-tron/inca_digital_crypto_intelligence_alert-TRON.pdf

Reality Part 2: The Stinky Stuff

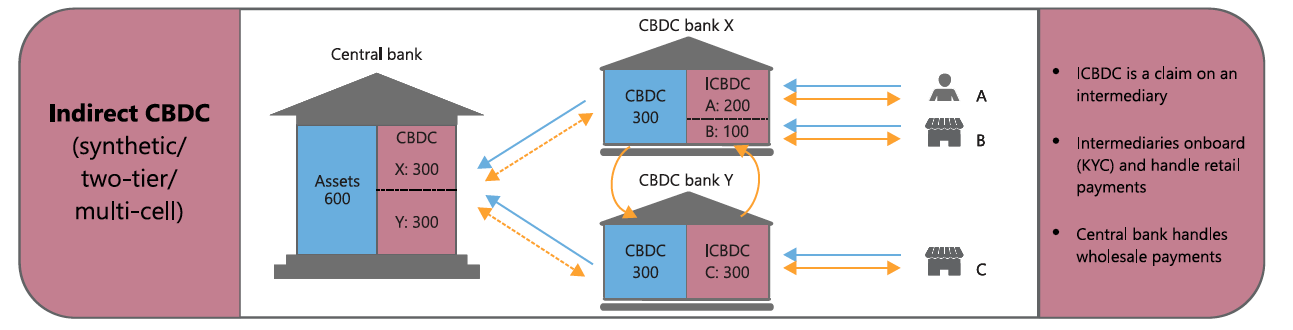

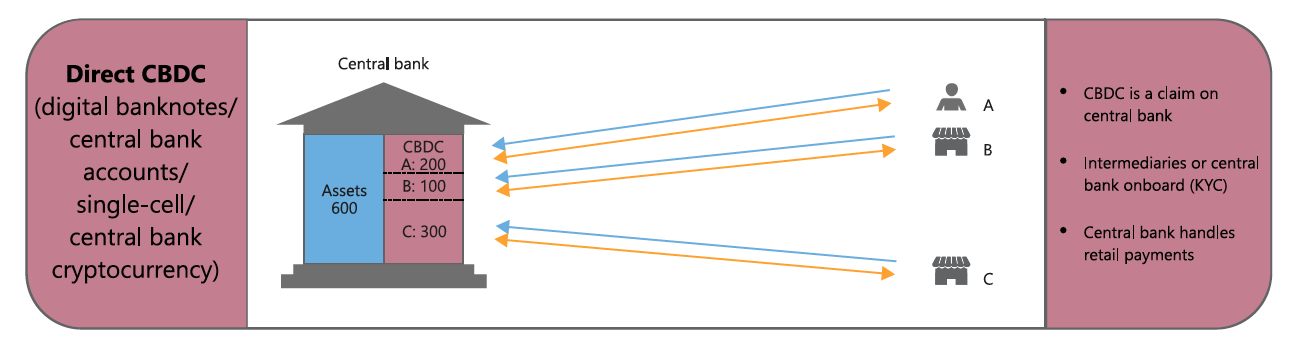

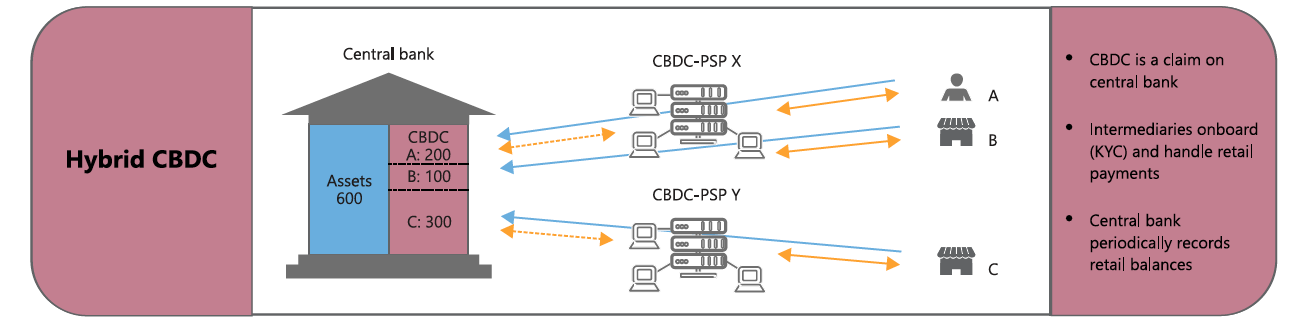

Central Bank-Issued Digital Currencies

Evolution

2008

2014/5

2019

2020

Source: BIS Quarterly Review, March 2020

How will you introduce and run it? Concerns

go alone

and do self

partner with banks \(=\)

use them for distribution and operation

The Year is 2008: what the Toronto a la cart program teaches us about CBDCs

Cautionary tales for central bank innovation

what people want

what we got

Features of Digital Money

fast money

CBDC run by

Central Bank

CBDC on new communually run system

bank-issued stablecoin on public blockchain

|

What? |

||||

|---|---|---|---|---|

| 24/7 instantaneous | ||||

| borderless | ||||

| programmable | ||||

| privacy | ||||

| p2p | ||||

| no commercial 3rd party | ||||

| nominal fee |

Taking a step back

Option 1a (existing cash):

Option 1b (convert cash to digital):

Option 2 (overcollateralized):

Option 3 (exotic):

What are Apple's options?

Thought experiment: Apple Inc. wants to issue a stablecoin

Options 1 a&b: Collateral Backed Stablecoins \(\to\) USDC

primary market acces: 560+ entities

\(\vdots\)

formally: this smart contract is a collateralized debt position (CDP)

The User's Perspective for a DAI Loan

Option 2 (reminder): Assets converted to cash: MakerDAO

Case 1:

stablecoin \(>\$1\)

arbitrageur

issuer

for fully decentralized algo/smart contract stablecoin: there is no dollar to give!

The Case of Luna-Terra

exchange LUNA for newly minted UST tokens at the prevailing $ market rate

secondary market

LUNA secondary market

Option 3: Algorithmic Stablecoin like UST on Terra

arbitrageur

issuer

exchange UST for newly minted LUNA tokens at the prevailing $ market rate

market

LUNA market

Case 2:

stablecoin \(<\$1\)

Option 3: Algorithmic Stablecoin like UST on Terra

Sadly, we know how this has always ended

UST Stablecoin

LUNA (cryptocurrency of the TERRA network)

But: there is no theoretical result that shows that collapse is inevitable

JPM coin

USDC

USDT

UST, Basis, Neutrino

DAI, FEI

Final Thoughts

Some Final Thoughts

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

Why are Blockchains challenging for current regulation?

UniSwap Lab supports development

a website app accesses the code

token holders control contact features

don't own the code

operation = decentral

control = decentral

anyone can use the baseline code

core code runs on the blockchain

tokens used as rewards

Illustration of the Challenges: The UniSwap Token

Questions around Regulation & Compliance

present vs future

Challenge 1: How do you get data onto a blockchain?

The Oracle Problem

<standings: 7,3,8,4,2,1,6,5> + digital signatures

Disagreement?

Majority Vote

1 ETH = $4780

1 ETH = $4789

1 ETH = $4781

DEXes can be used as on-chain price oracles

Time-Weighted Average Price (TWAP)

The Oracle Problem

Oracle nodes form their own ecosystem

staked LINK can be slashed

Chainlink

Same follow-on challenge for builders: how can you fit staking, rewards, and inevitable speculation into securities law?

Challenge 2: the settlement layer has a mind of its own

a

b

c

d

e

f

g

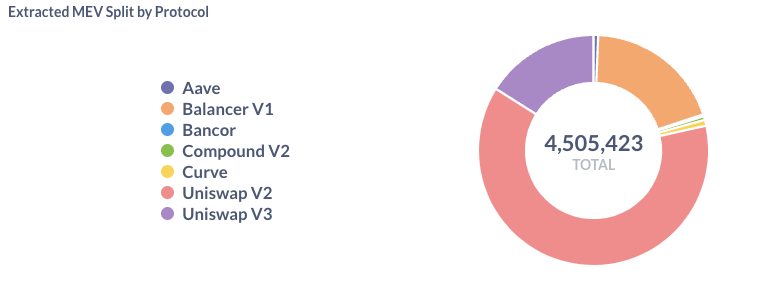

Problem: Public Mempools allow Sandwich (MEV) Attacks

A brief look under the hood: the workflow

liquidity pool

blockchain

user

website

router

liquidity pool

blockchain

user

A brief look under the hood: the workflow

aggregator protocol

router

pool 1

blockchain

user

pool 2

multiple

pools

A brief look under the hood: the workflow

back to UniSwap

pool 1

blockchain

user

pool 2

A brief look under the hood: the workflow

back to UniSwap

pool 1

blockchain

user

pool 2

just-in-time

liquidity bots

A brief look under the hood: the workflow

back to UniSwap

pool 1

blockchain

user

pool 2

just-in-time

liquidity bots

in the settlement layer ("MEV")

Are Tokens Securities and What Safeguards Should There Be?

Provocative Thoughts

- End of Theory -

Some Developments

seller

buyer

What is a Blockchain?

The Premise of the

Internet & Blockchain

Peer to Peer Communication

Peer to Peer Value

!

?

?

Sidebar: What is digitize-able value?

The challenge: how do you ensure digital scarcity?

By Andreas Park