Andreas Park PRO

Professor of Finance at UofT

Wannabe "Stablecoins"

Instructor: Andreas Park

GENIUS Act Stablecoins?

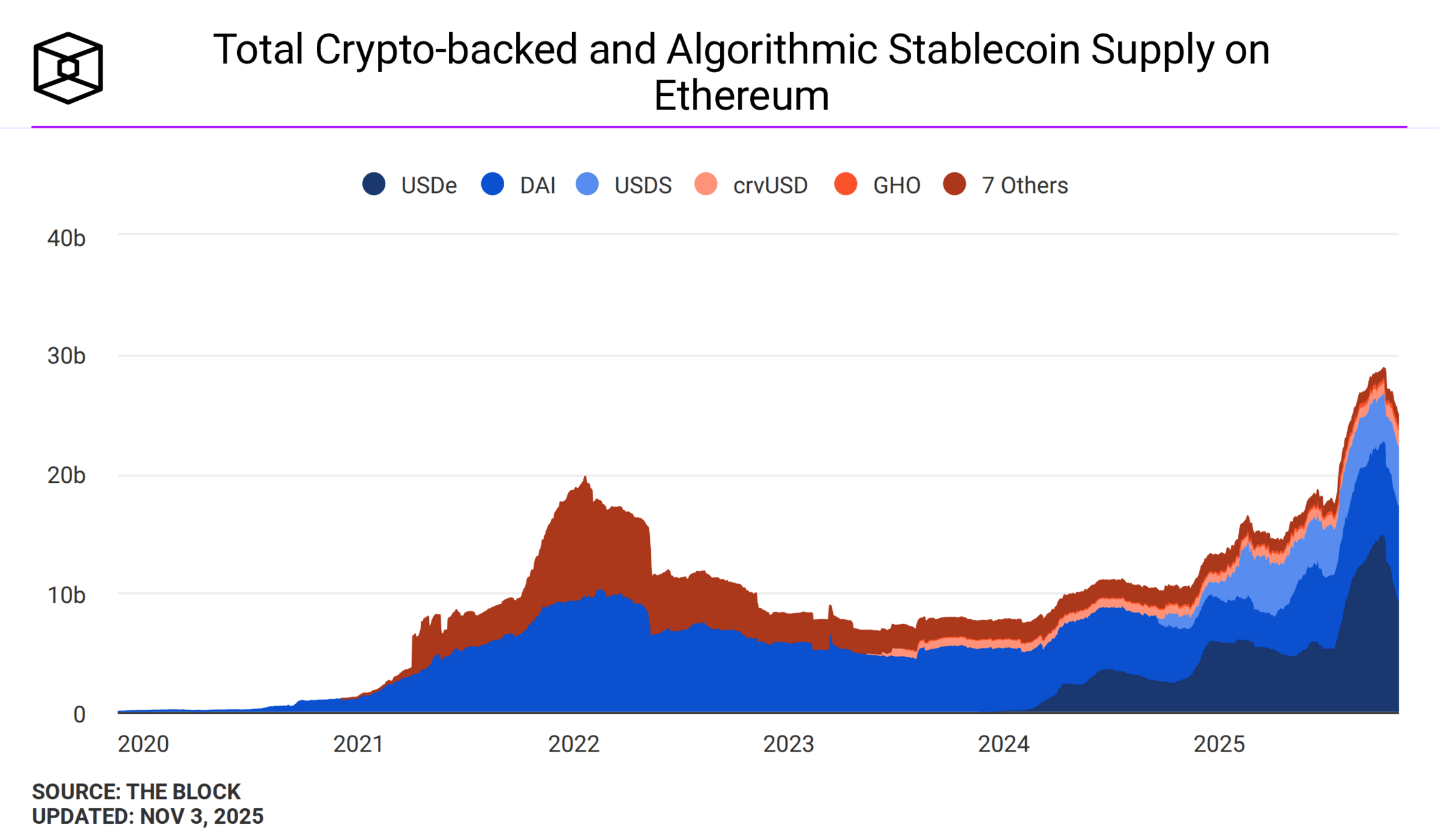

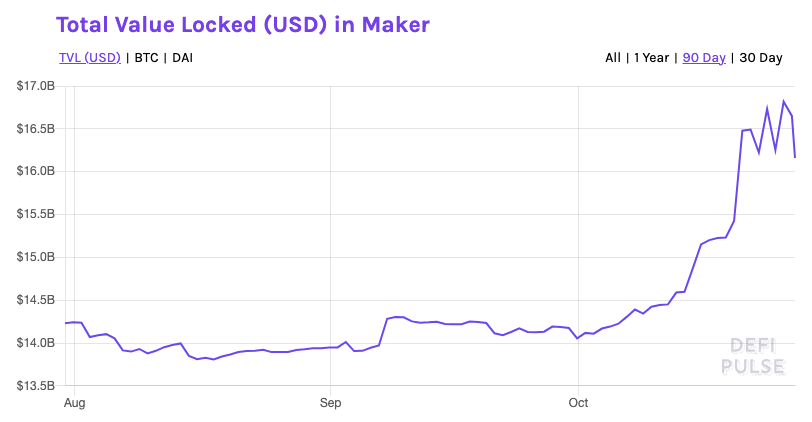

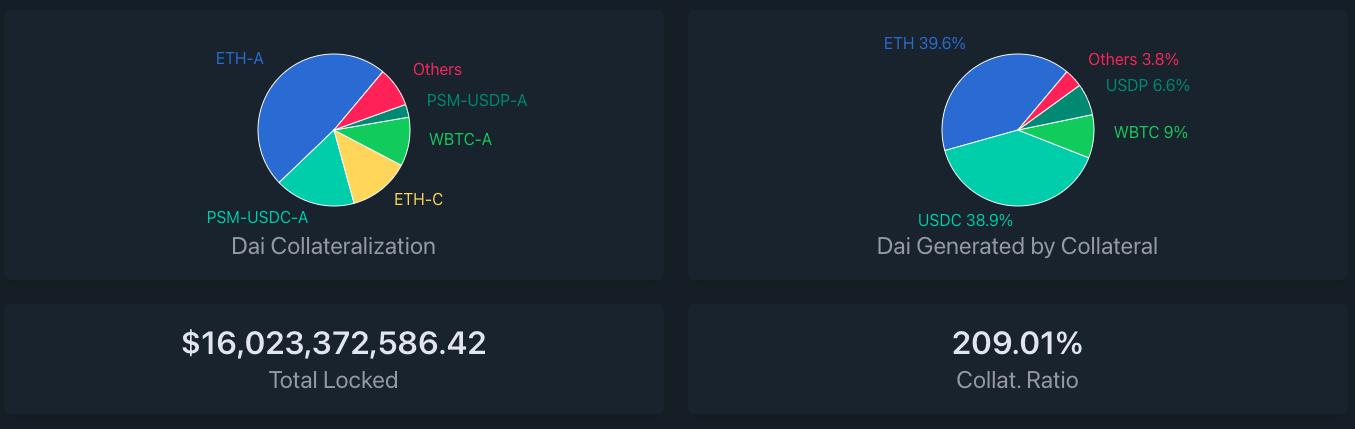

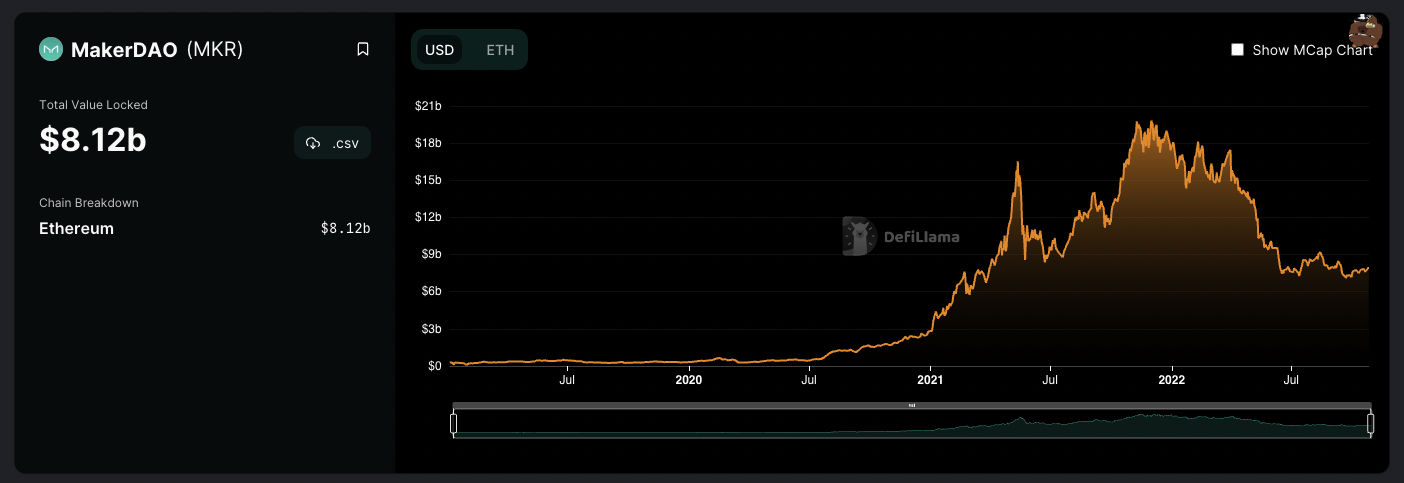

MakerDAO/Sky

based

Ethena Basis Trade

Terra-Luna

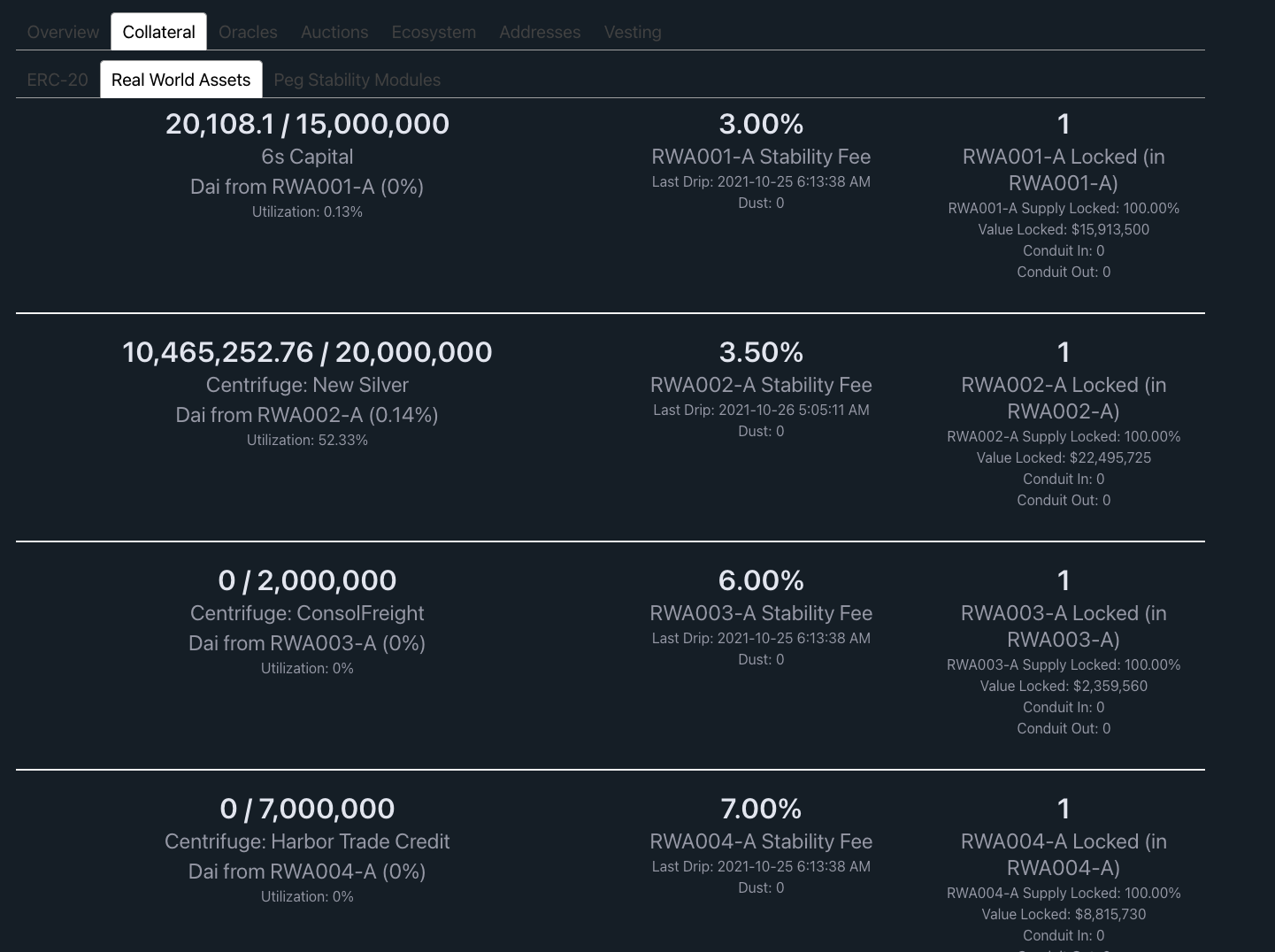

Type 1: Collateral-backed, smart contract created

MakerDAO's DAI/USDS

Basic Idea

4 ETH

(1 ETH = $375)

(Oct 15, 2020)

\(\approx\) $1,500

\(\vdots\)

1,500 DAI

(1 DAI = $1)

formally: this smart contract is a collateralized debt position (CDP)

fractional collateral \(\to\) collateralization factor \(=\) 150%

total collateral = $1,500

maximum loan = $1000

overcollateralization = $500

actual loan (example) = $500

buffer = $500

ETH \(\nearrow\) $500

value of ETH collateral = $2,000

maximum loan = $2,000/150%=$1,333

total collateral = $2,000

maximum loan = $1,333

overcollateralization = $667

actual loan (example) = $500

buffer = $500

overcollateralization = $667

new loan capacity= $333

ETH \(\searrow\) $187.5

value of ETH collateral = $750

maximum loan = $750/150%=$500

total collateral = $750

maximum loan = $500

overcollateralization = $250

actual loan (example) = $500

buffer = $0

for reference: former value of collateral

ETH \(\searrow\) $150

value of ETH collateral = $600

maximum loan = $600/150%=$400

total collateral = $600

maximum loan = $400

required overcollateralization = $200

actual loan (example) = $500

buffer = -$100

for reference: former value of collateral

\(\Rightarrow\) triggering of liquidation auction by "keeper"

sell 3.33 ETH=$500=500 DAI

repay $500=500 DAI loan

retain incentive

return remainding ETH to vault owner

borrowers of DAI need to pay interest \(\to\) stability fee

DSR paid on "locked" DAI

total amount of debt (or DAI) outstanding is limited

Sidebar: how is this decided?

\(\to\) special "governance" token MKR

MakerDAO has no "arbitrage" mechanism. It relies on markets to increase and decrease supply of DAI to bring the price close to $1.

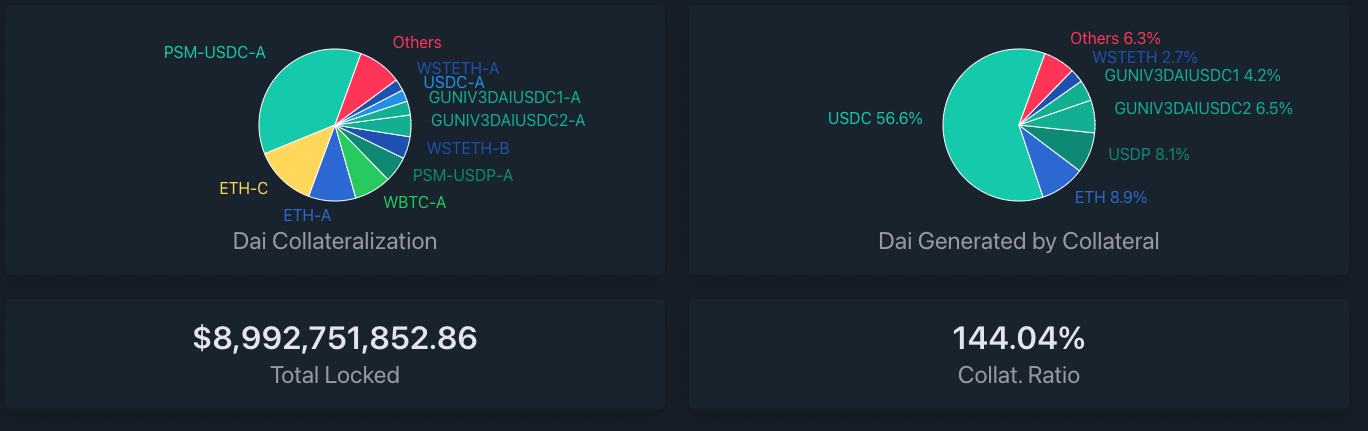

Source: daistats.com (Oct 27, 2021)

Source: daistats.com (Oct 26, 2022)

The Problem:

The Solution:

Note: In May 2021, ETH prices dropped again by >30% but no drama in DAI

Type 2:

Algorithmic Stablecoin

UST on Terra

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

under-collateralized stablecoin

arbitrageur

issuer

market

Case 1: price(1 SC) \(>\) 1 FU \(\to\) SC cheap

arbitrageur

issuer

The Case of Luna-Terra

exchange LUNA for newly minted UST tokens at the prevailing $ market rate

market

LUNA market

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

arbitrageur

issuer

The Case of Luna-Terra

exchange SC for newly minted LUNA tokens at the prevailing $ market rate

market

LUNA market

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

DISCUSSION

POTENTIAL PROBLEMS

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Type 3:

Basis Trade

USDe by Ethena

Basic Idea

Lifecycle

Does this work? Loose intuition

A bit more detail: let's start with a $100 in ETH position

Now add yields etc

What could go wrong?

Like Sky/MakerDAO, Ethena has no "arbitrage" mechanism. It relies on markets to increase and decrease supply of DAI to bring the price close to $1.

By Andreas Park

The deck covers "funky" stabelcoins that maybe don't quite deserve their name..