Andreas Park PRO

Professor of Finance at UofT

Blockchain and Decentralized Finance:

2024 Intro for MFRM

Presenter: Andreas Park

Some Technological Innovations throughout History

technological innovation removes barriers:

many innovations move power to do things from selected few to the masses

tech disrupts a group of people who built a living around a technological restriction and they disrupt government power exerted via these groups

technological innovation removes barriers:

What is a Blockchain?

What is a Cryptocurrency?

Conceptually, what is a blockchain?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

\(\approx\) 50% is bitcoin (but used to be 70%)

Smart contract accounts

Externally owned accounts

controlled by private keys

private

key

public

key

seed phrase

public

address

wallet = software to keep and use private keys

What makes DeFi different from TradFi

decentralized finance =

provision of financial service functionality without the necessary involvement of a traditional financial intermediary like a bank or broker-dealer*

digital media =

provision of information service functionality without the necessary involvement of a traditional information intermediary like a publisher, library, or newagency

*my take: applies to only commoditizable services

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

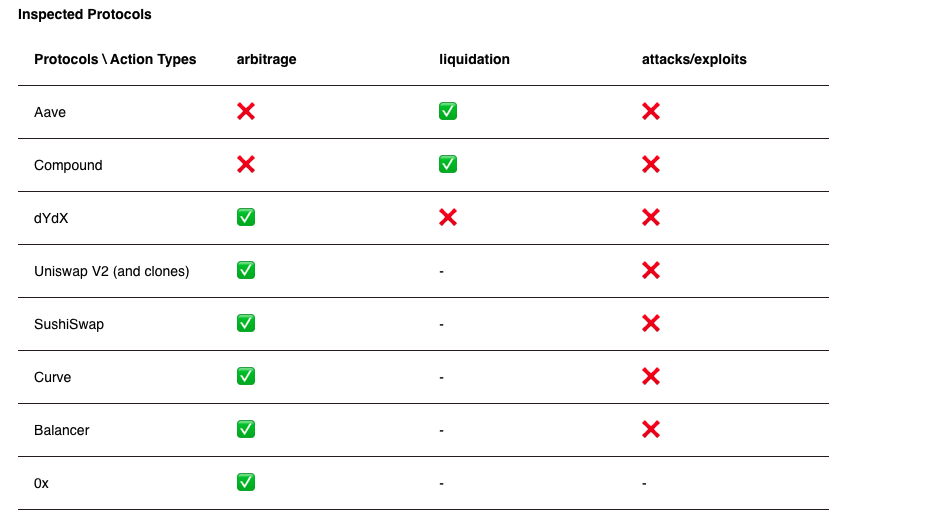

Application: Decentralized Borrowing & Lending

borrow

provide collateral

5. repay DAI

for loan

with health factor <1

liquidation

opportunity

1. flash-borrow DAI

2. repay loan

with DAI

3. claim

collateral ETH

4. convert ETH to DAI

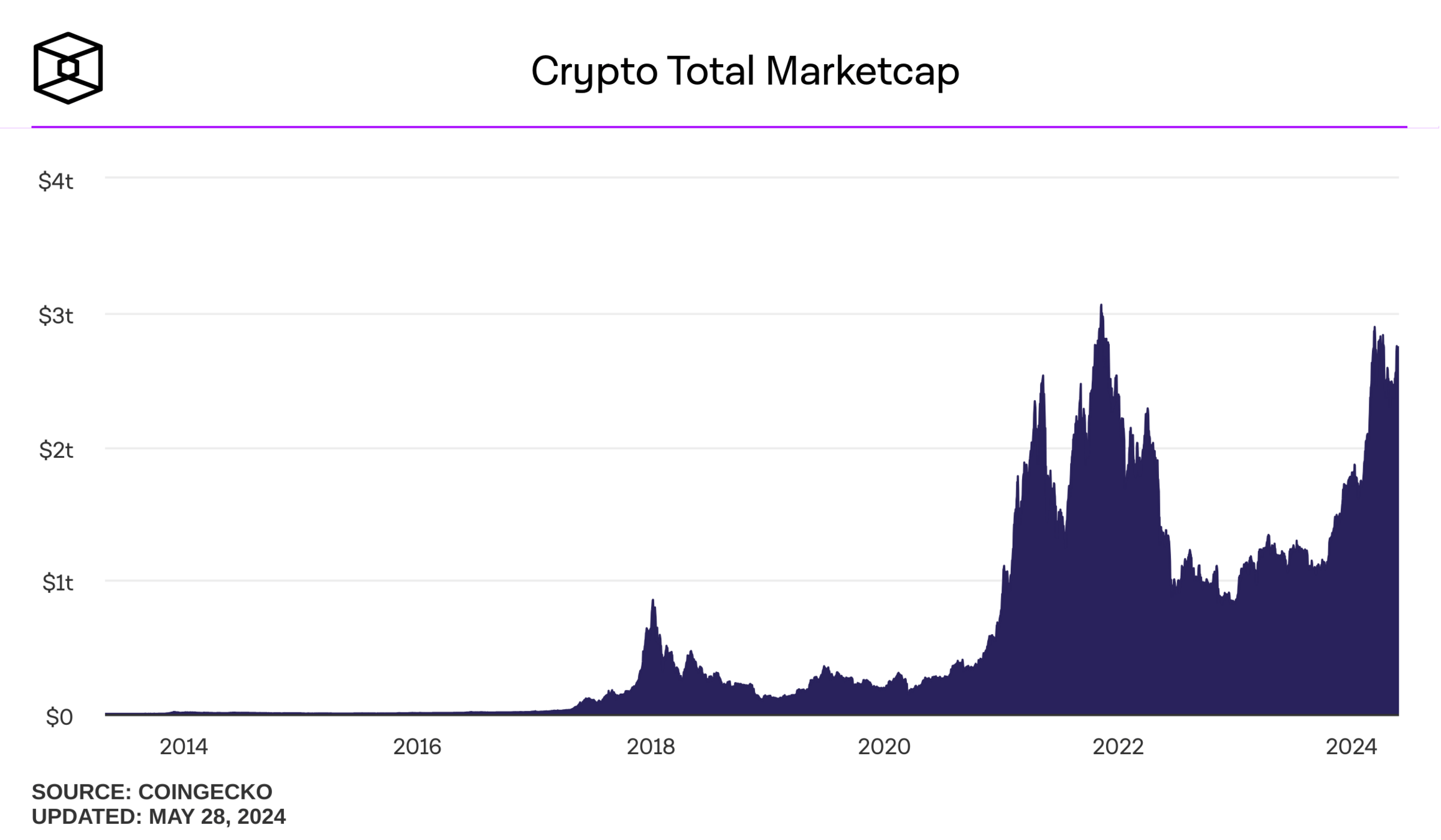

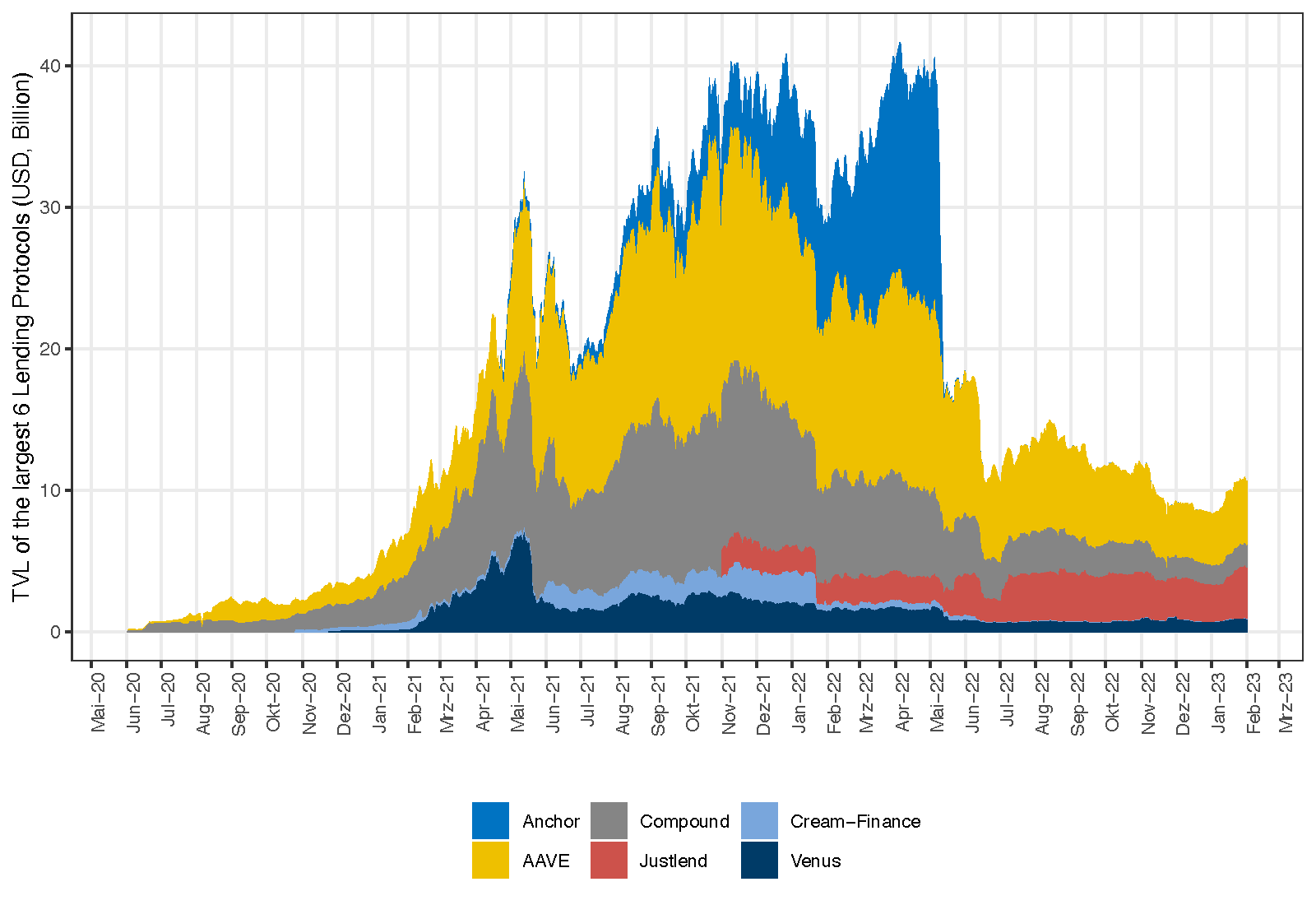

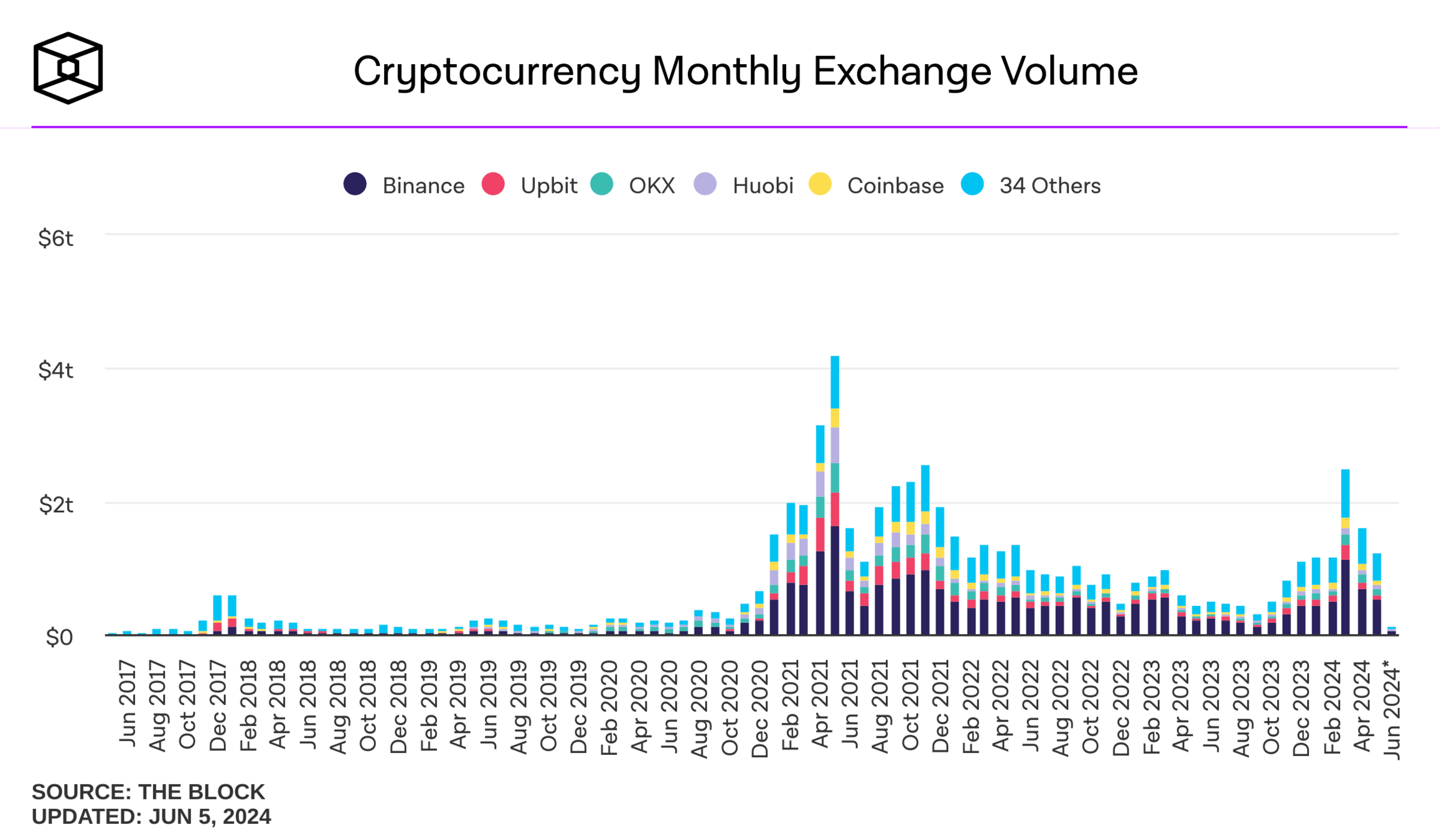

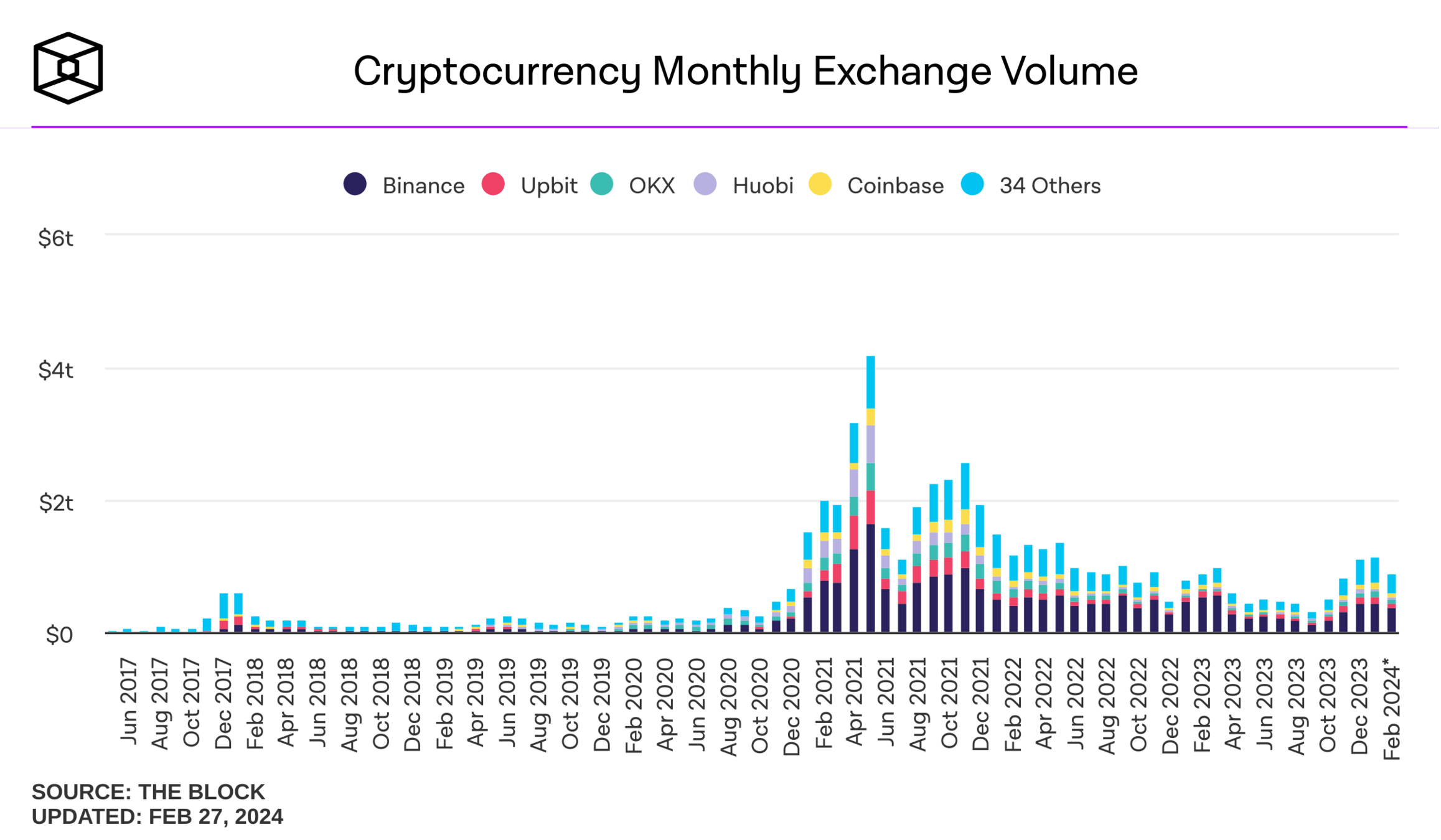

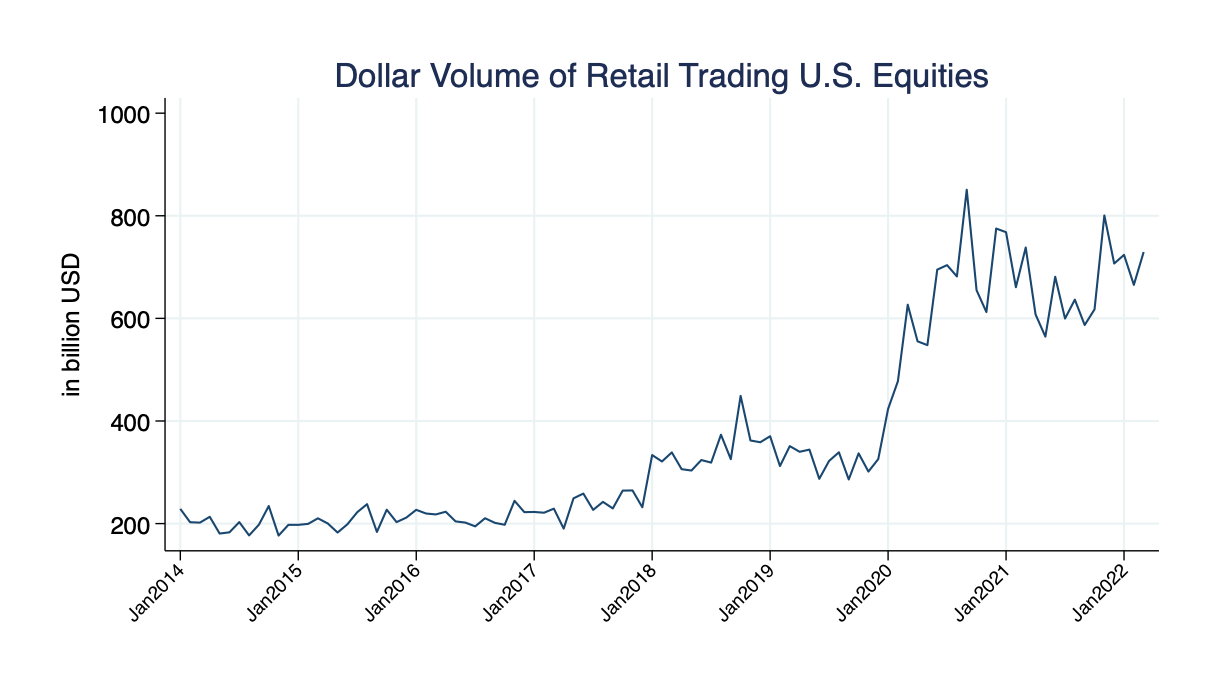

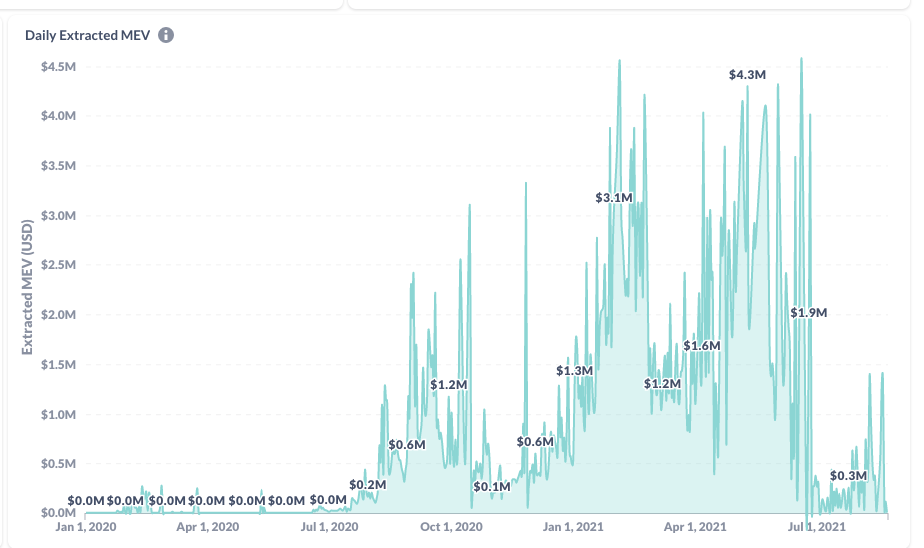

Some Data

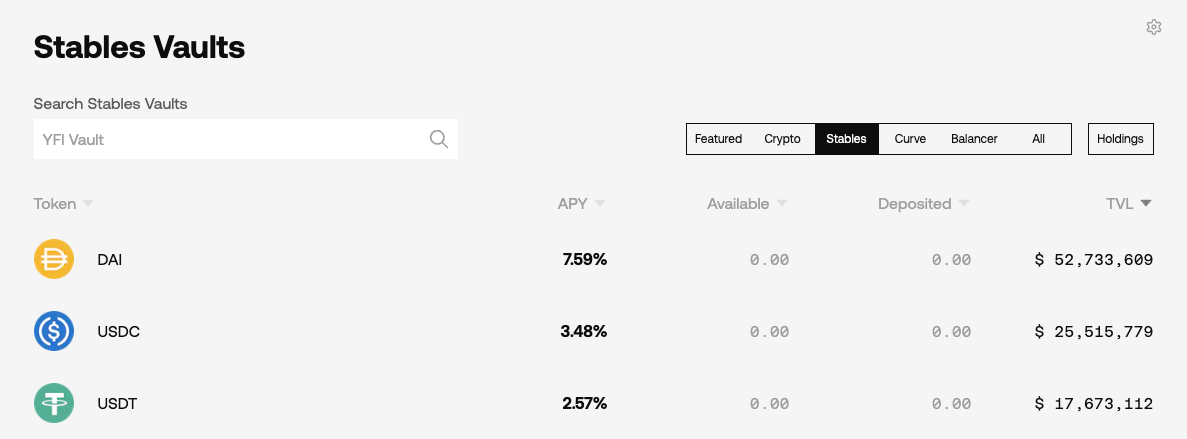

Obvious Smart Contract Application: Automate Investment Strategies

idea: create new mutual fund like asset

"yield aggregator:" push capital where rate of return is highest

What roles do tokens play?

What roles do tokens play?

recall the differences

\(\to\) key feature: no necessary intermediaries

Problems:

lesser problem because

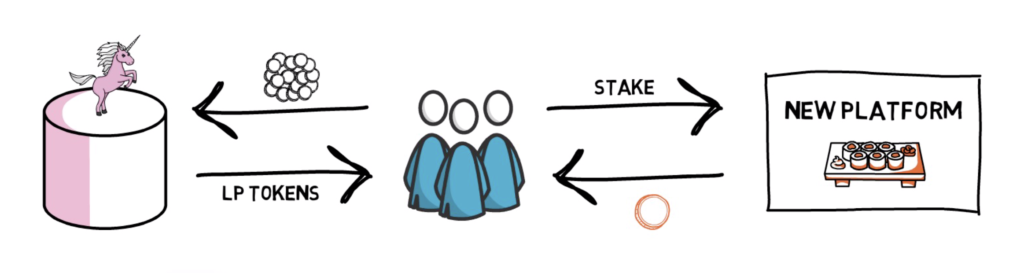

Common solution: create a reward token! Here's how this works

Step 4: users receive a reward token based on the time that they lock up the "receipt" token

Step 3: users lock up the "receipt" token in a smart contract

Step 2: users contribute liquidity and get a "receipt" token

Step 1: create reward tokens and deposit into a smart contract

borrow

provide collateral

Application: Pool-based borrowing and lending

Same problems as with trading:

But: in contrast to trading, here you need both!

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

Without intermediaries:

platform economics!

incentives for both?

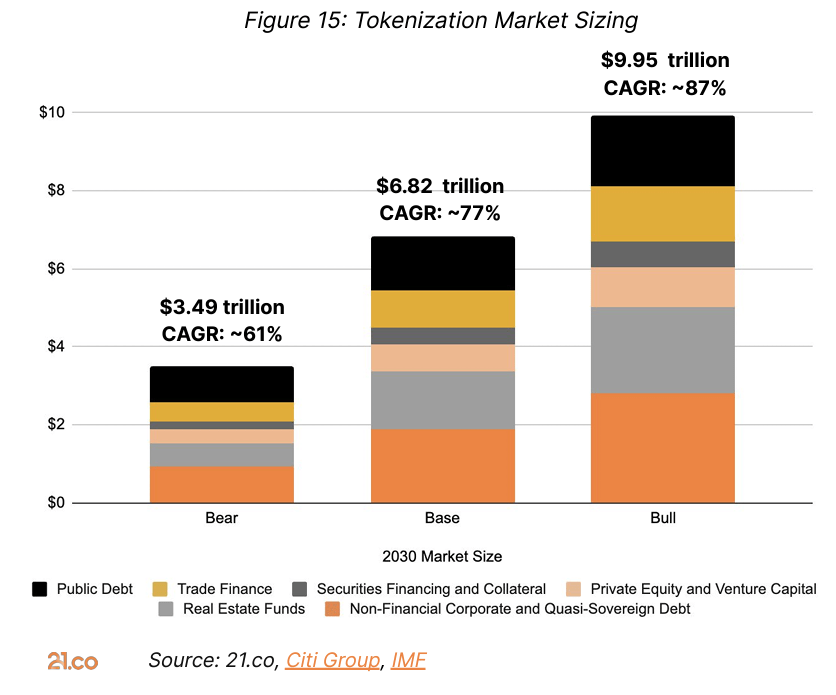

Asset Tokenization or

"The Creation of Asset-Linked Tokens"

Tokenization is coming

Challenges

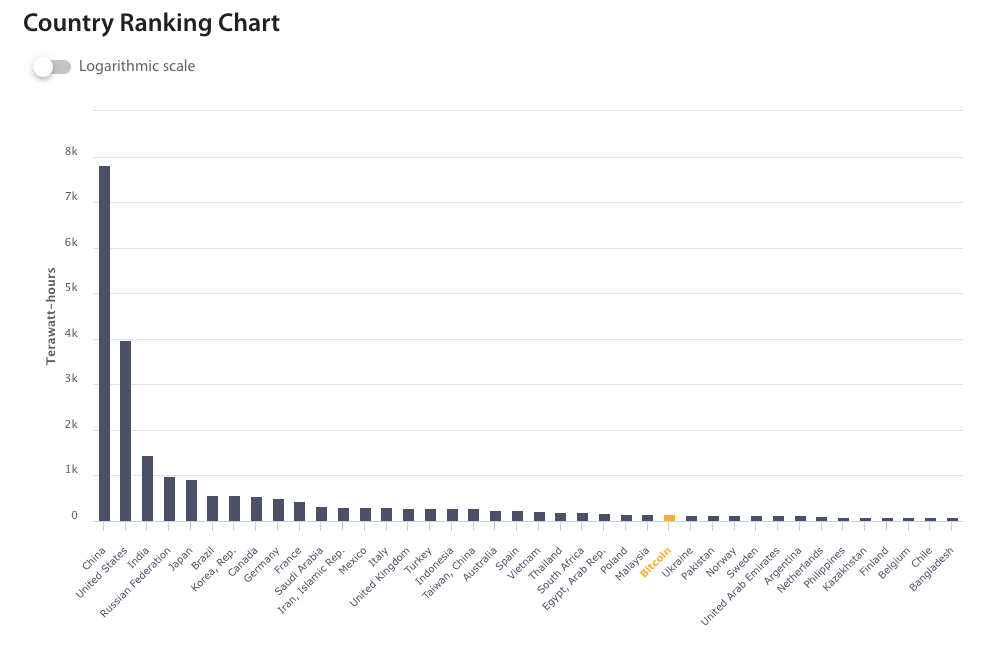

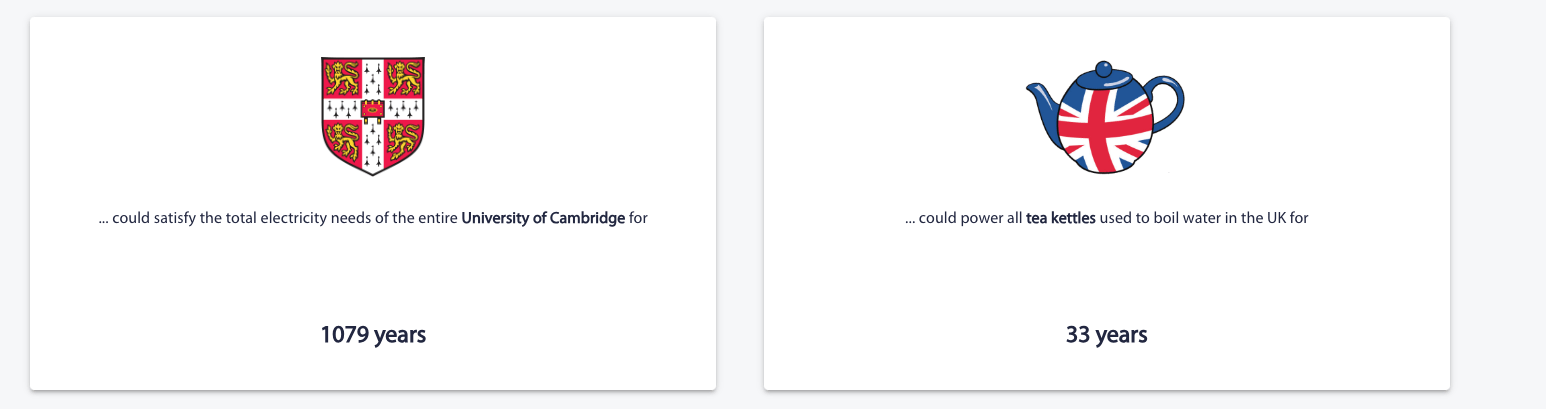

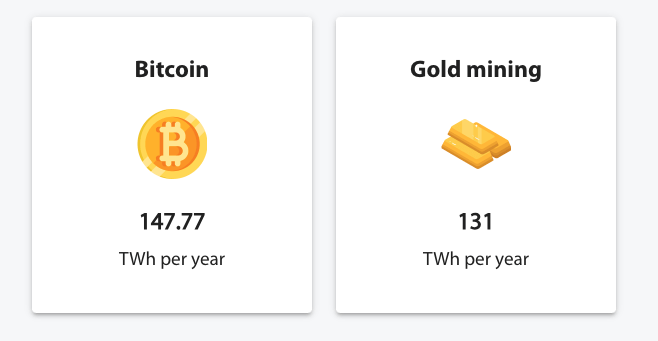

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

Challenge 1: Energy Consumption

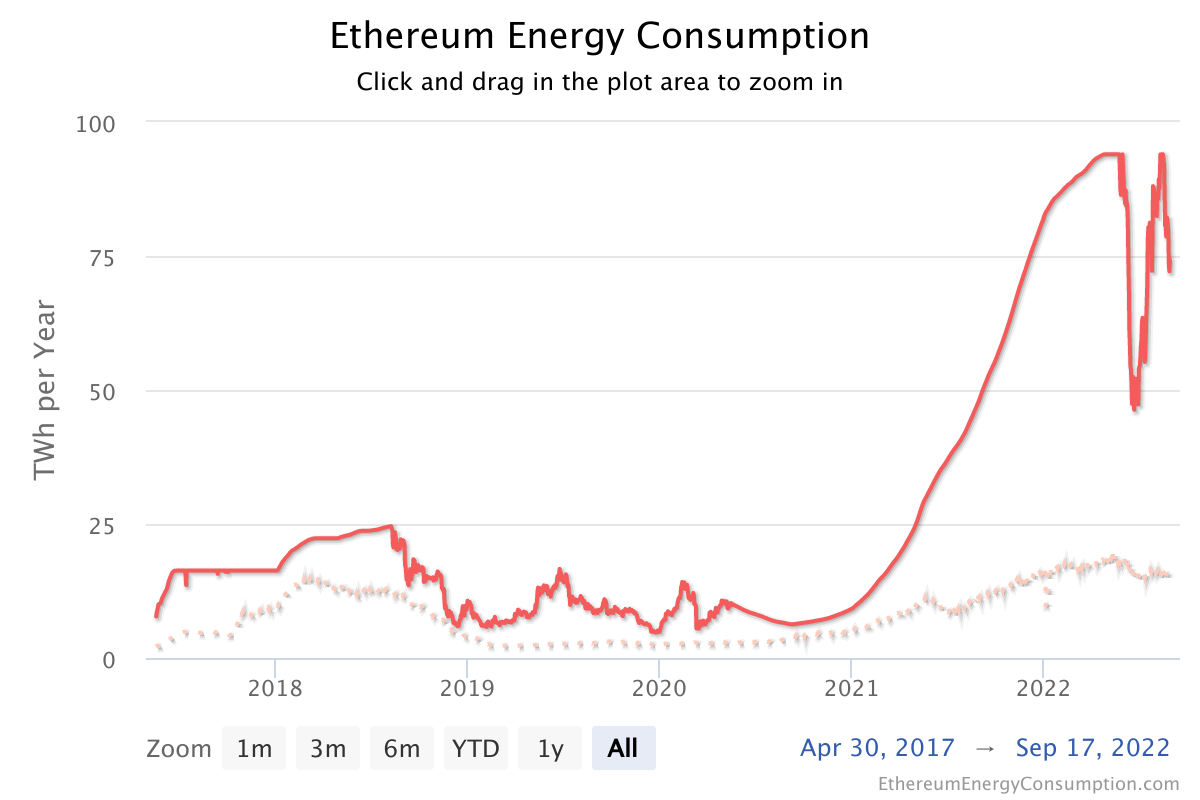

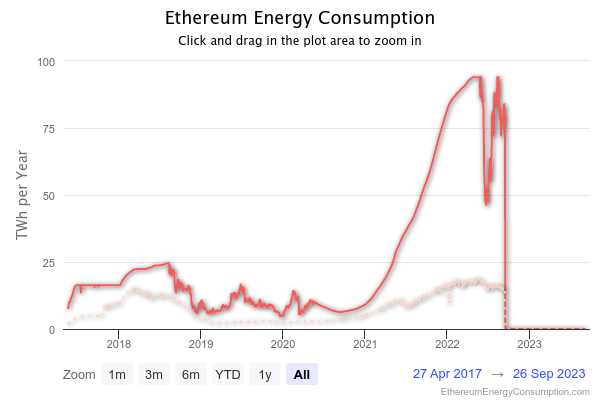

Ethereum Challenge 1: Environment

problem solved

| transactions per second | T per 12 hours (business day) | |

|---|---|---|

| Bitcoin | 7 | 302,400 |

| Ethereum | 30 | 1,296,000 |

| Algorand | 2000 | 86,400,000 |

| Conflux | 4000 | 172,800,000 |

| Athereum | 5000 | 216,000,000 |

| Payments Canada ACSS | 648 | 28,000,000 |

| US retail | 7639 | 330,000,000 |

| Canada number of equity trades | 46 | 2,000,000 |

| Orders on Canadian equity markets | 3588 | 155,000,000 |

Tweaks: lighting network (BTC) or side chains, SegWit, blocksize possible, but there are limits

microtransactions, IoT, and other smart contract use cases place very high demands

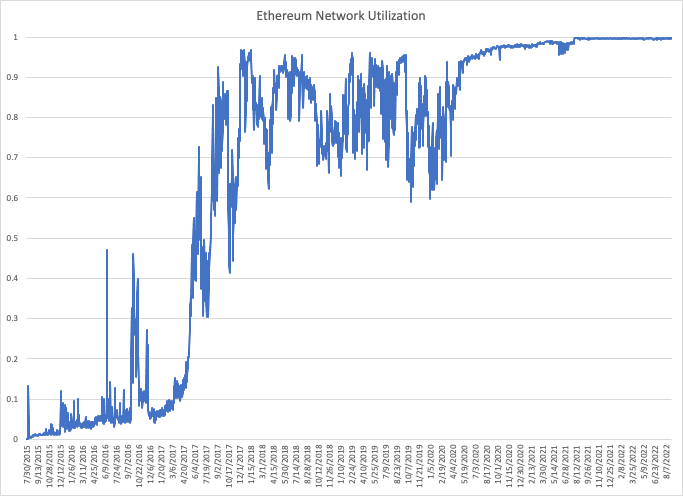

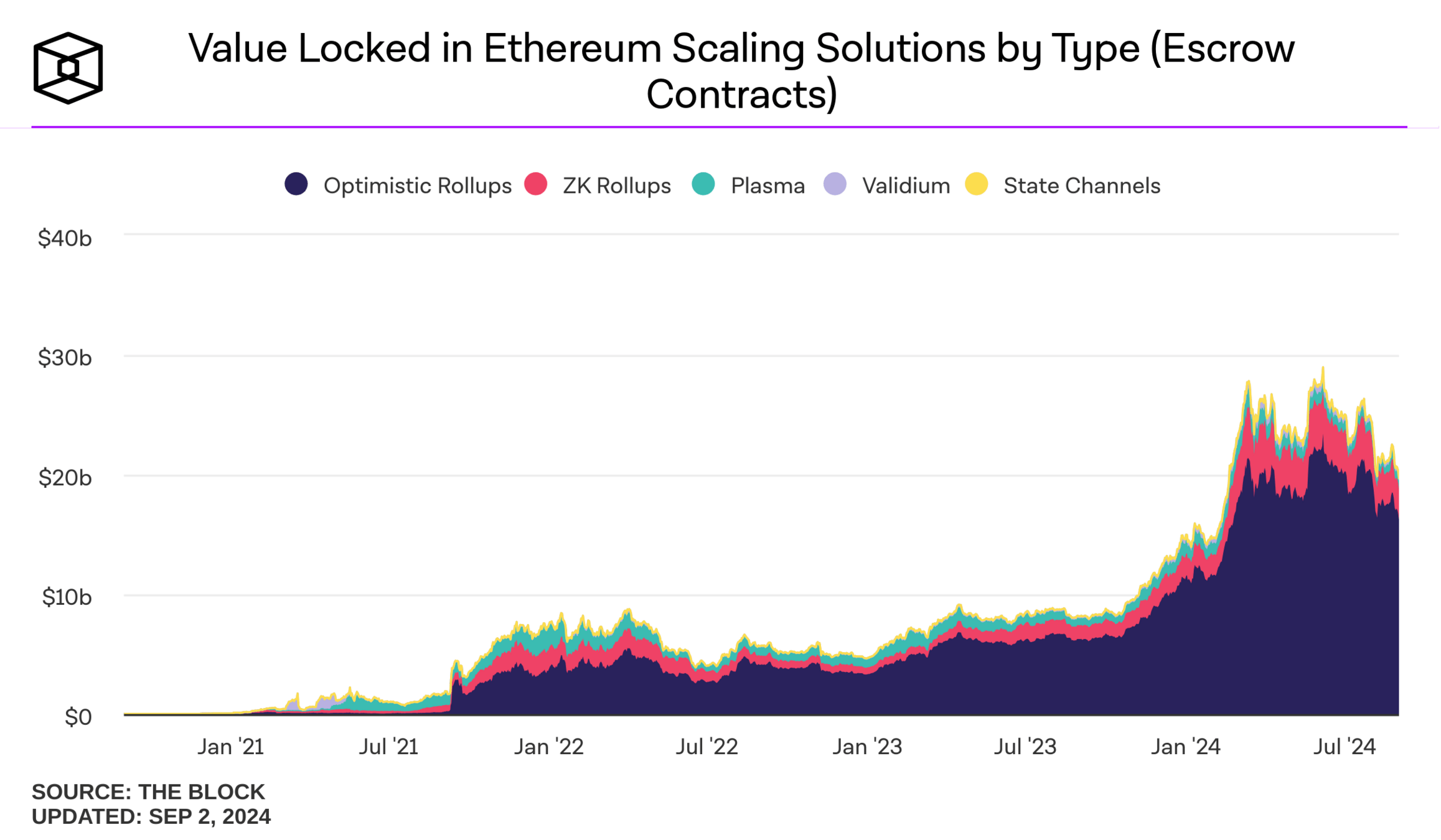

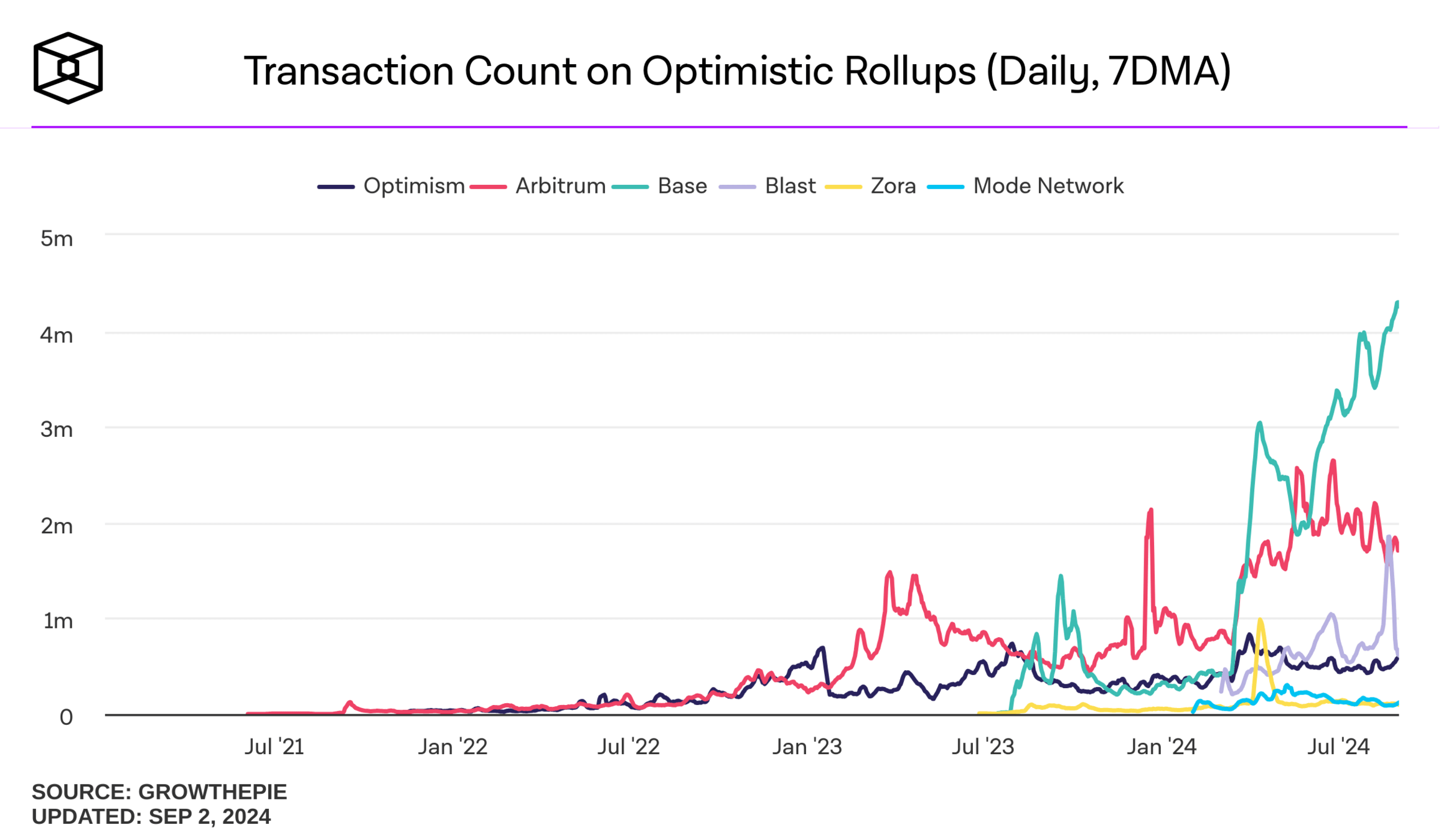

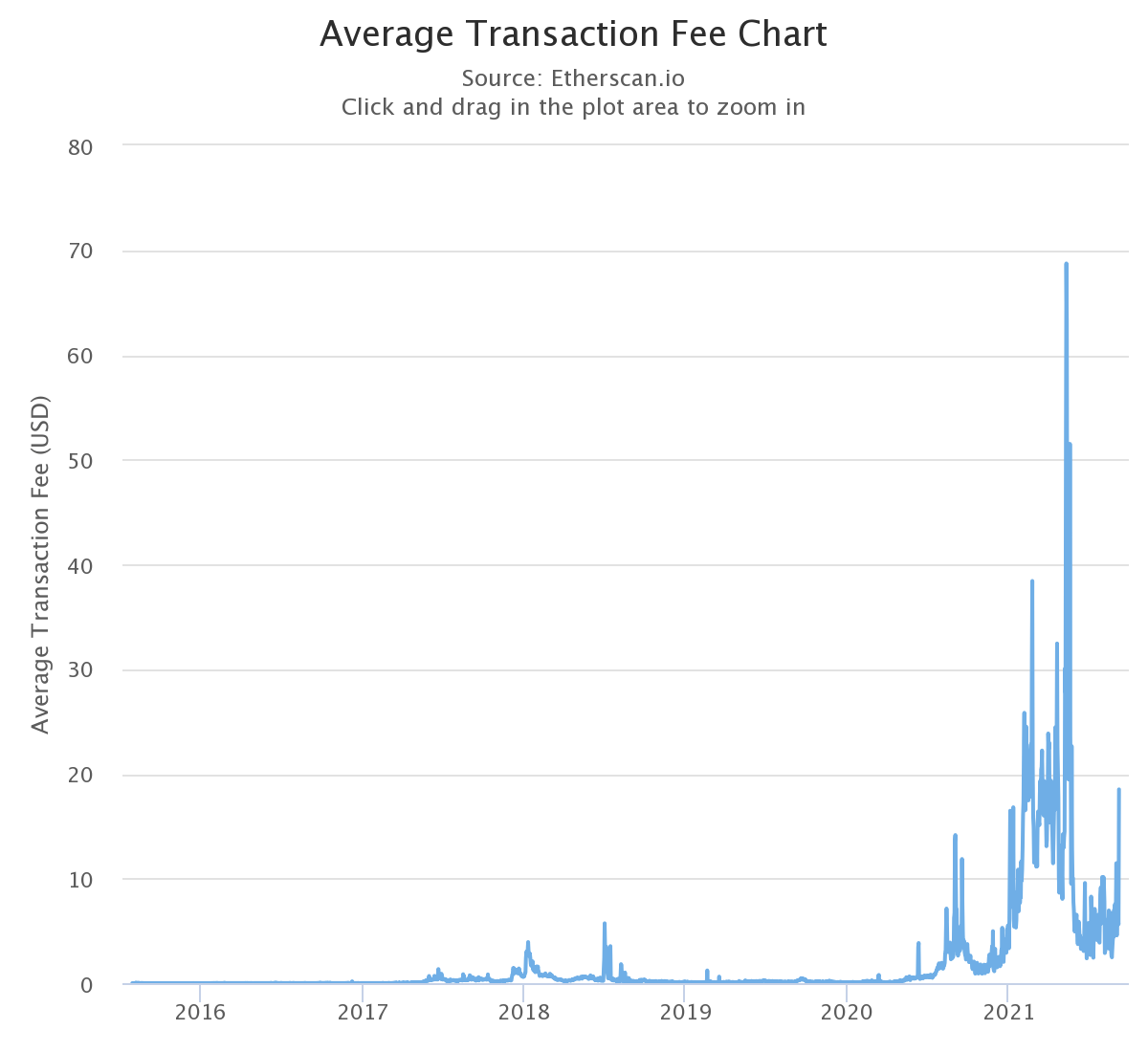

Ethereum Challenge 2: Throughput

Ethereum Challenge 2: Throughput

Source: Etherscan w re-scaling

Ethereum Throughput Solution: L2s/Rollups

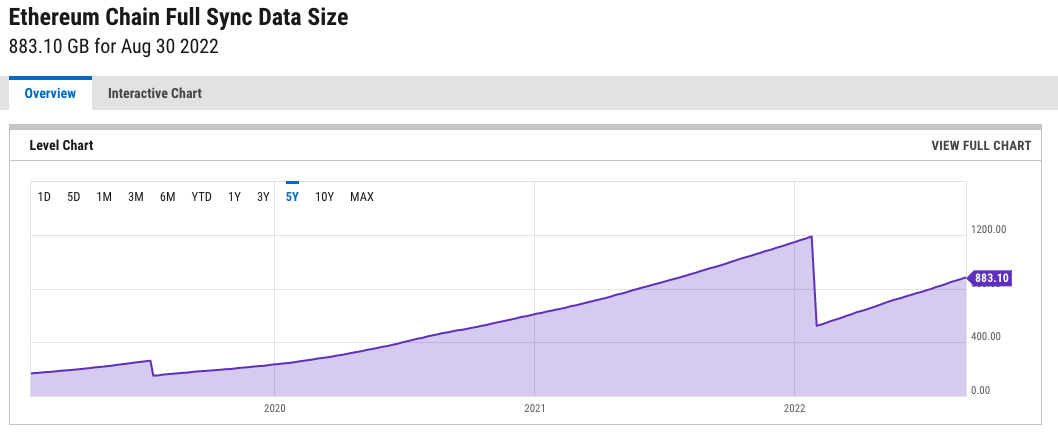

Ethereum Challenge 3: State Size

Source: Ycharts

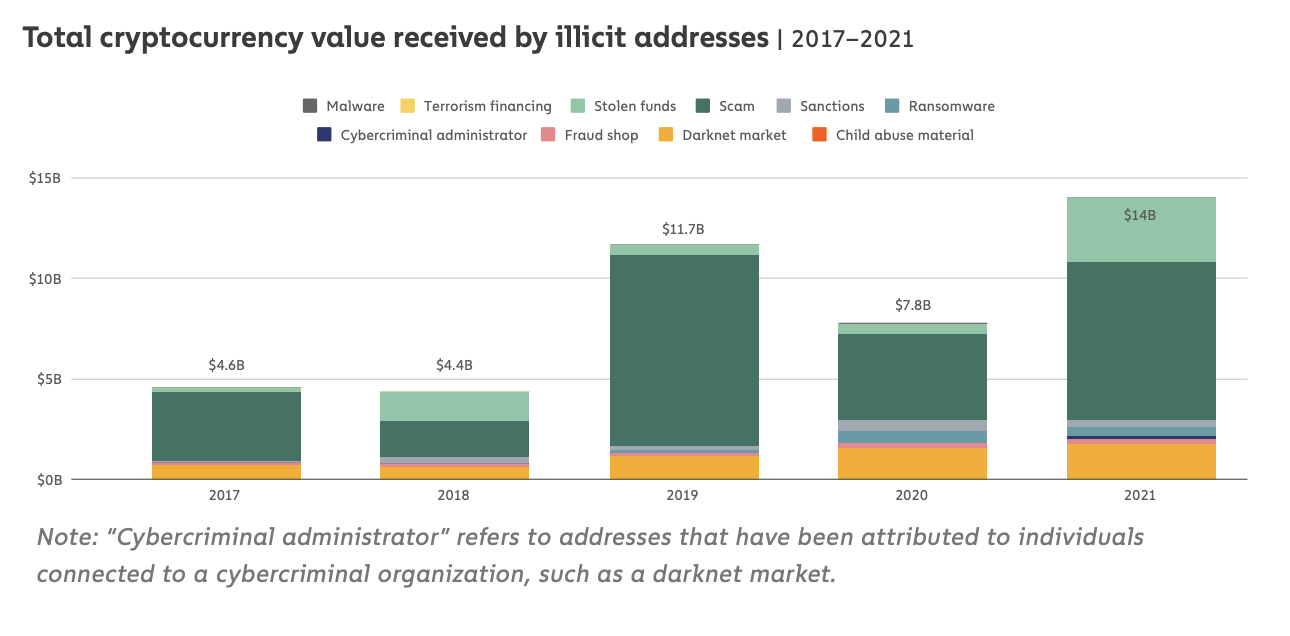

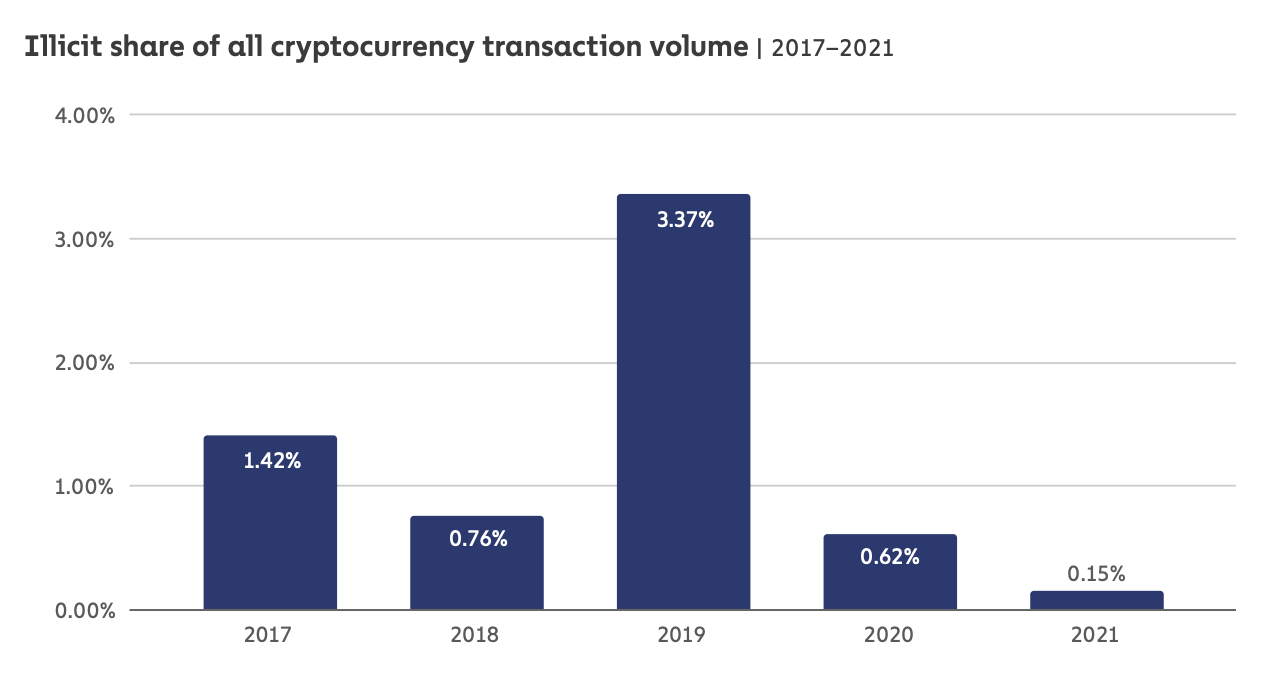

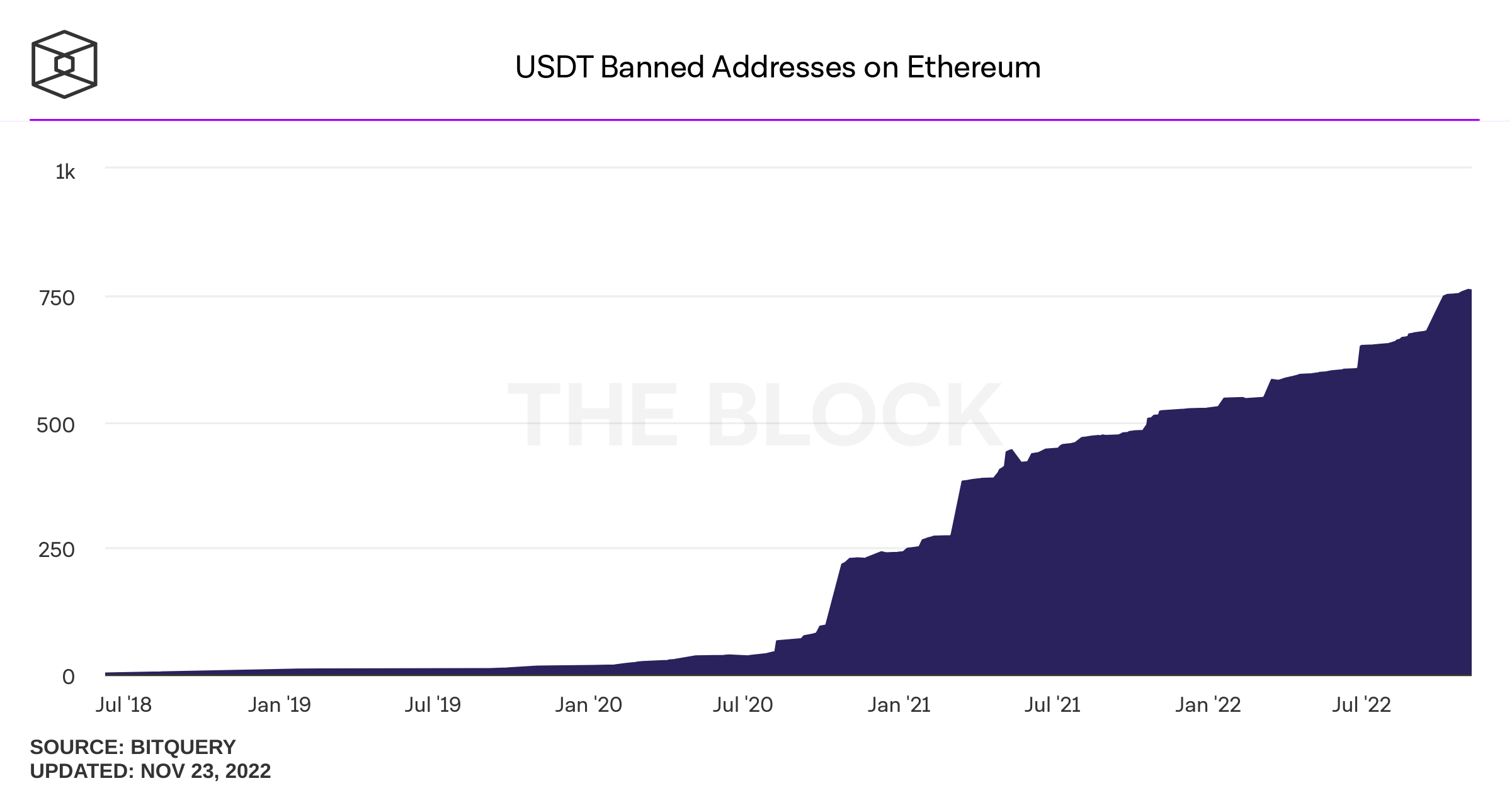

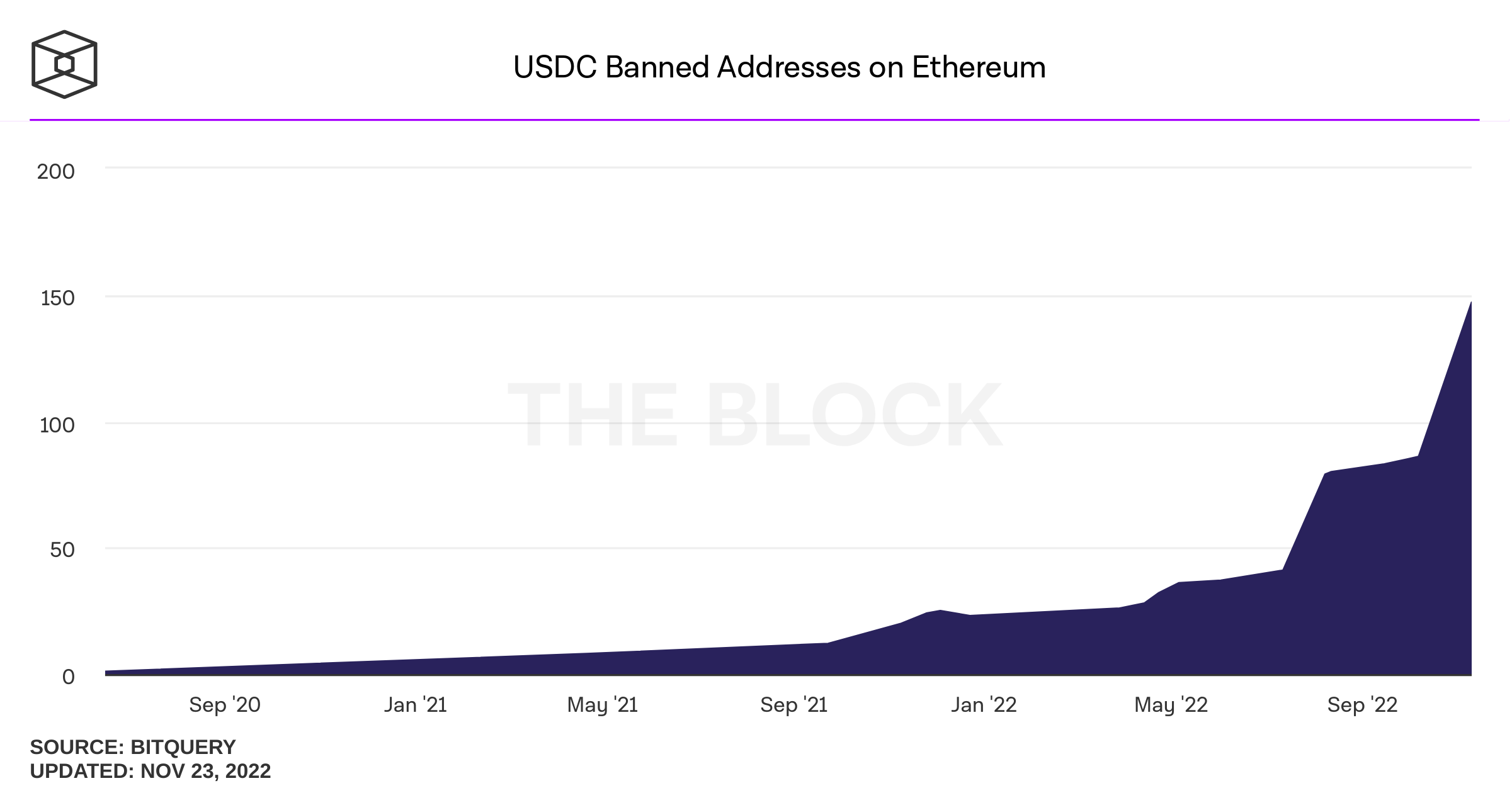

Money Laundering and Crime

extra info:

criminals don't use USDC - why are we so worried?

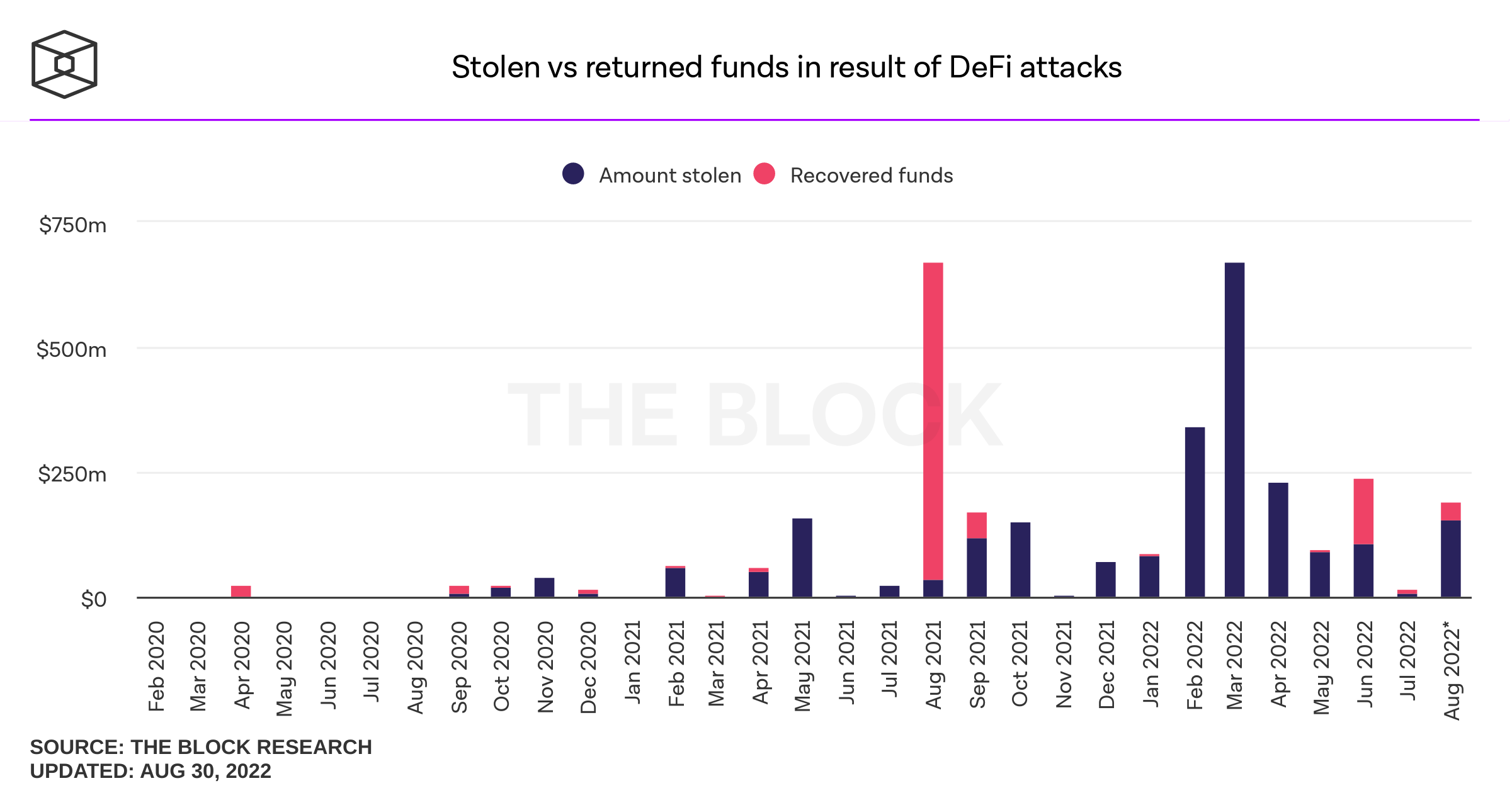

Hacks, Thefts, and Exploits

Common Reasons: hacks, faulty code, tricking a protocol

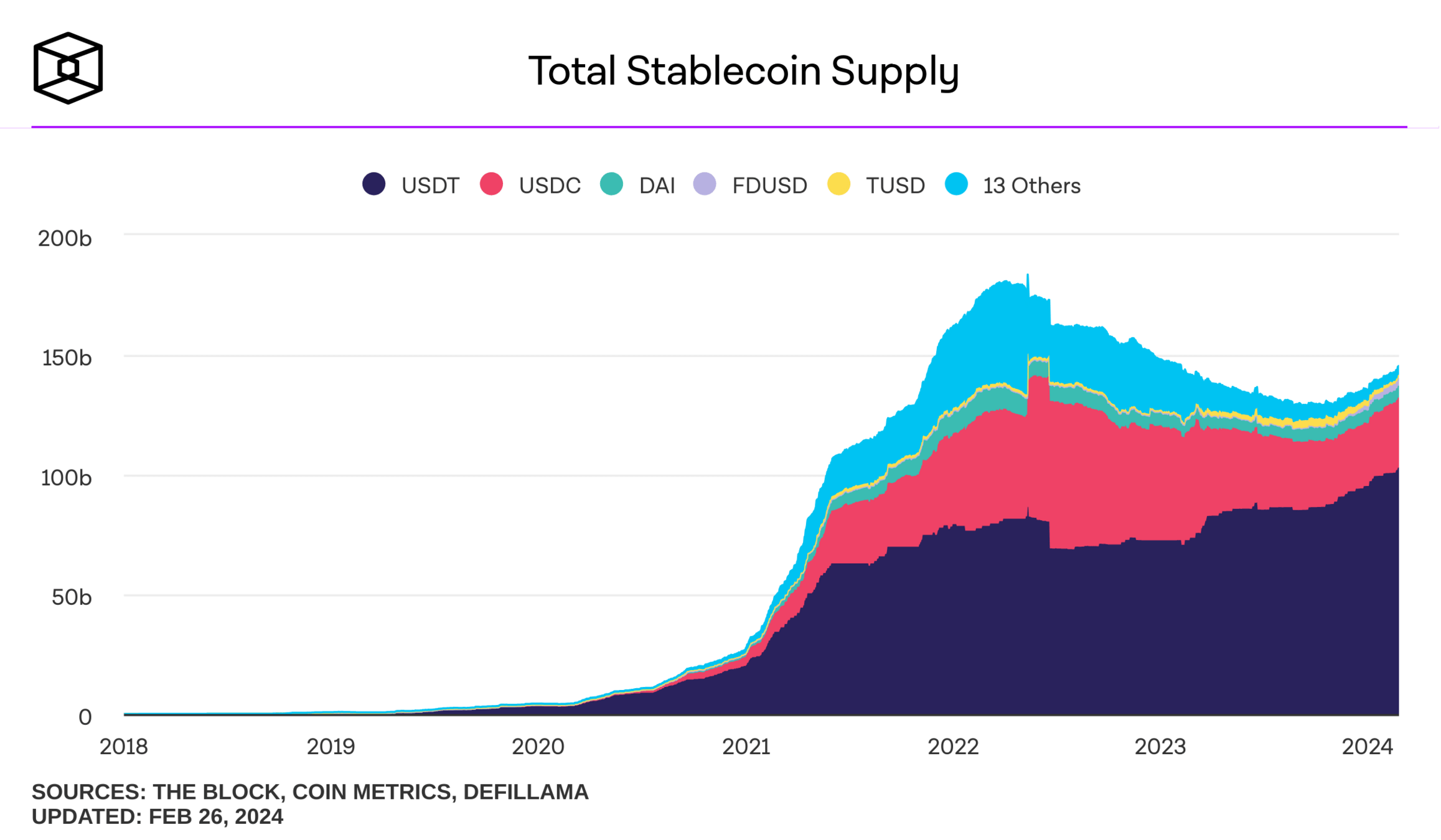

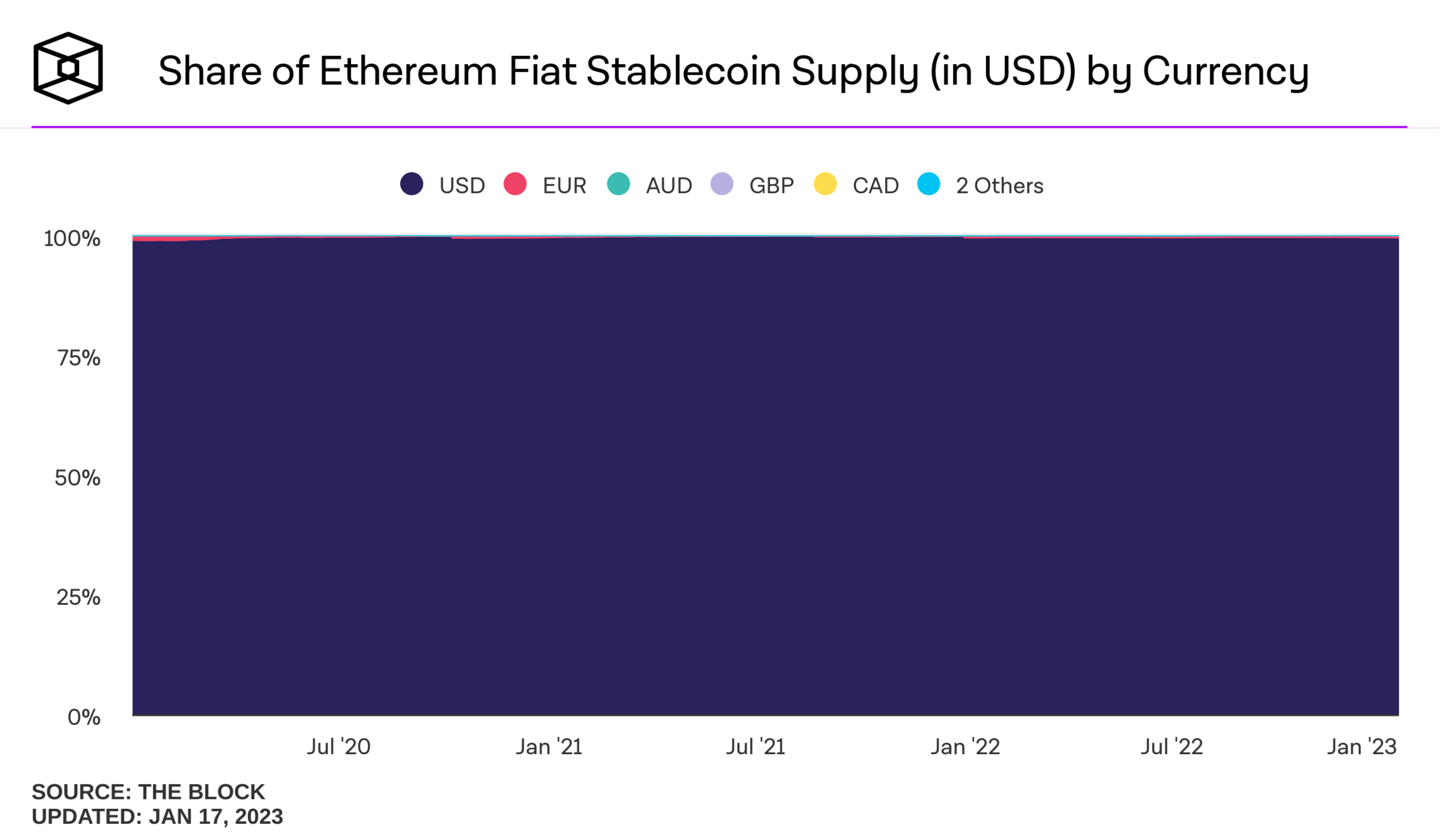

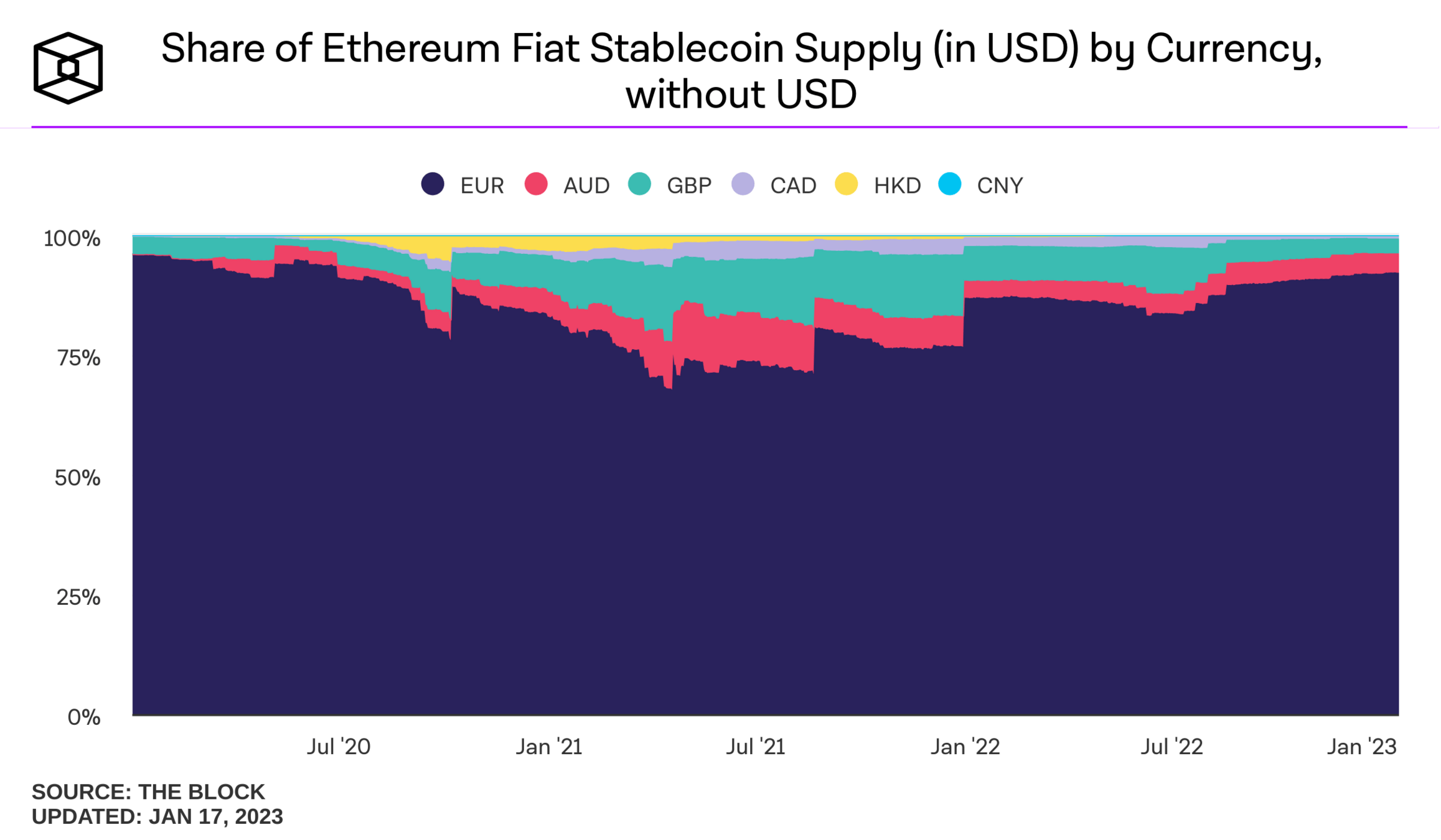

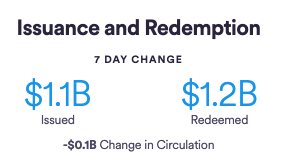

What is a stablecoin?

digital representation of a unit of a fiat currency on a blockchain

pulled from Nick Carter's talk on "Will stablecoins serve or subvert U.S. interests?"

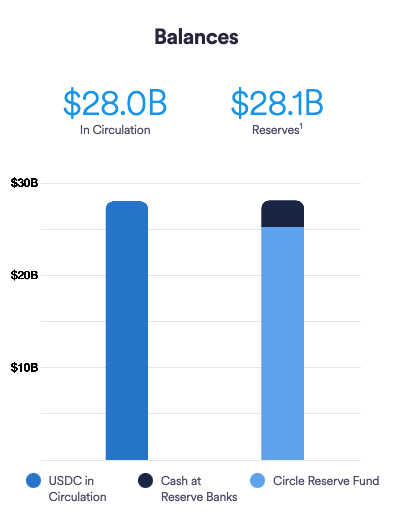

Collateral Backed Stablecoins: USDT & USDC

\(\Rightarrow\) 5% over-collateralized

primary market acces: 6 entities only

Collateral Backed Stablecoins: USDT & USDC

primary market acces: 560+ entities

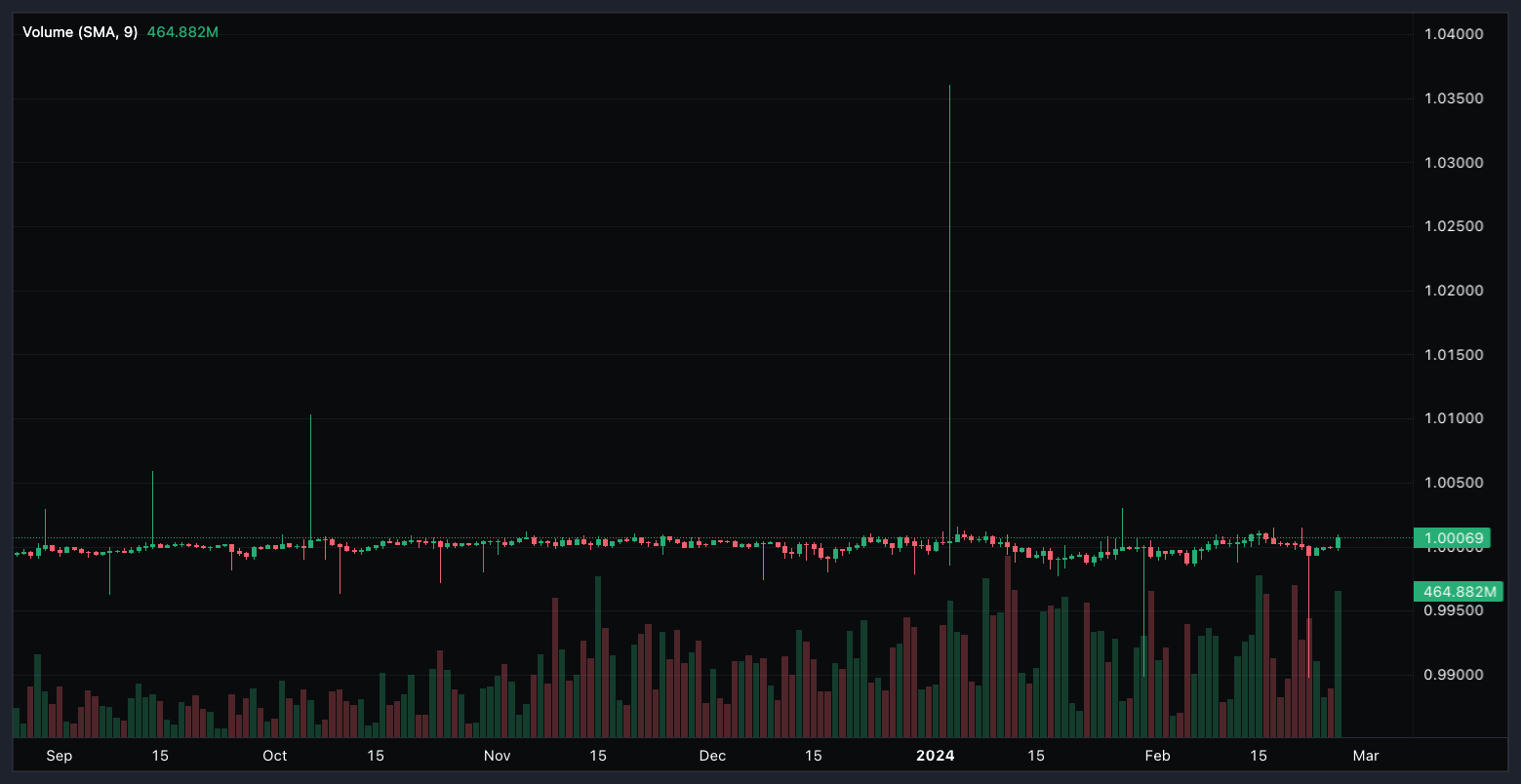

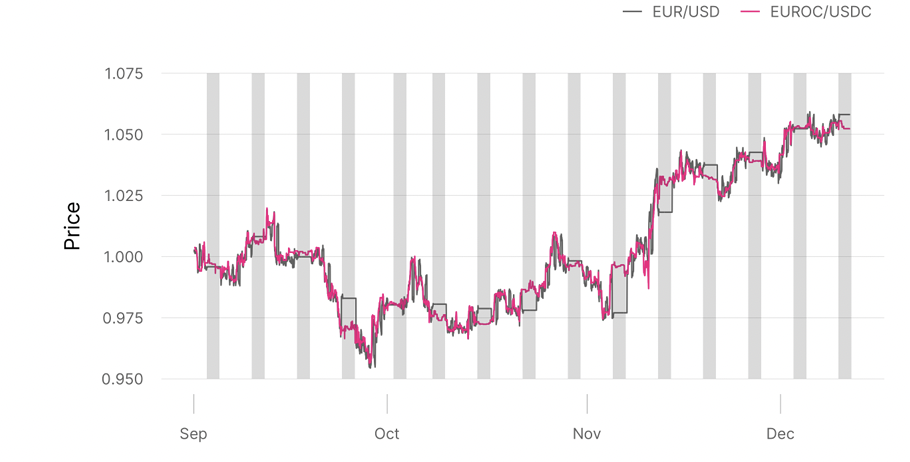

What makes a Stablecoin stable?

USD-USDT (6 months)

\(\Rightarrow\) need a primary/reference market mechanism to allow for forces of arbitrage to align prices

Stablecoin use cases

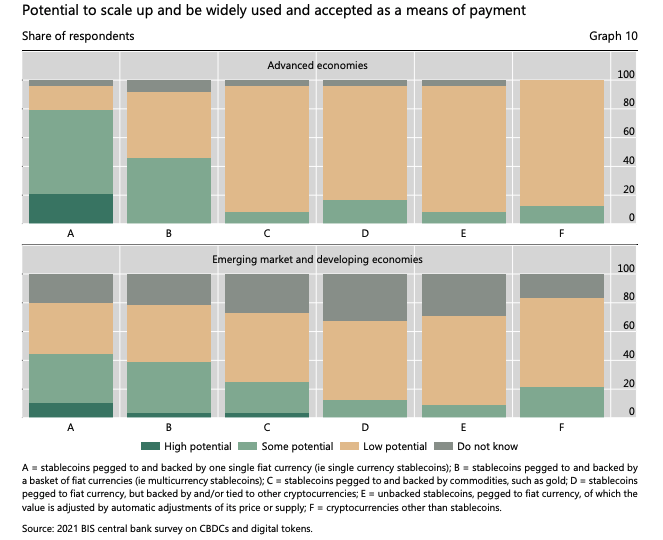

What do central bankers think about stablecoins?

BIS Survey of Central Banks:

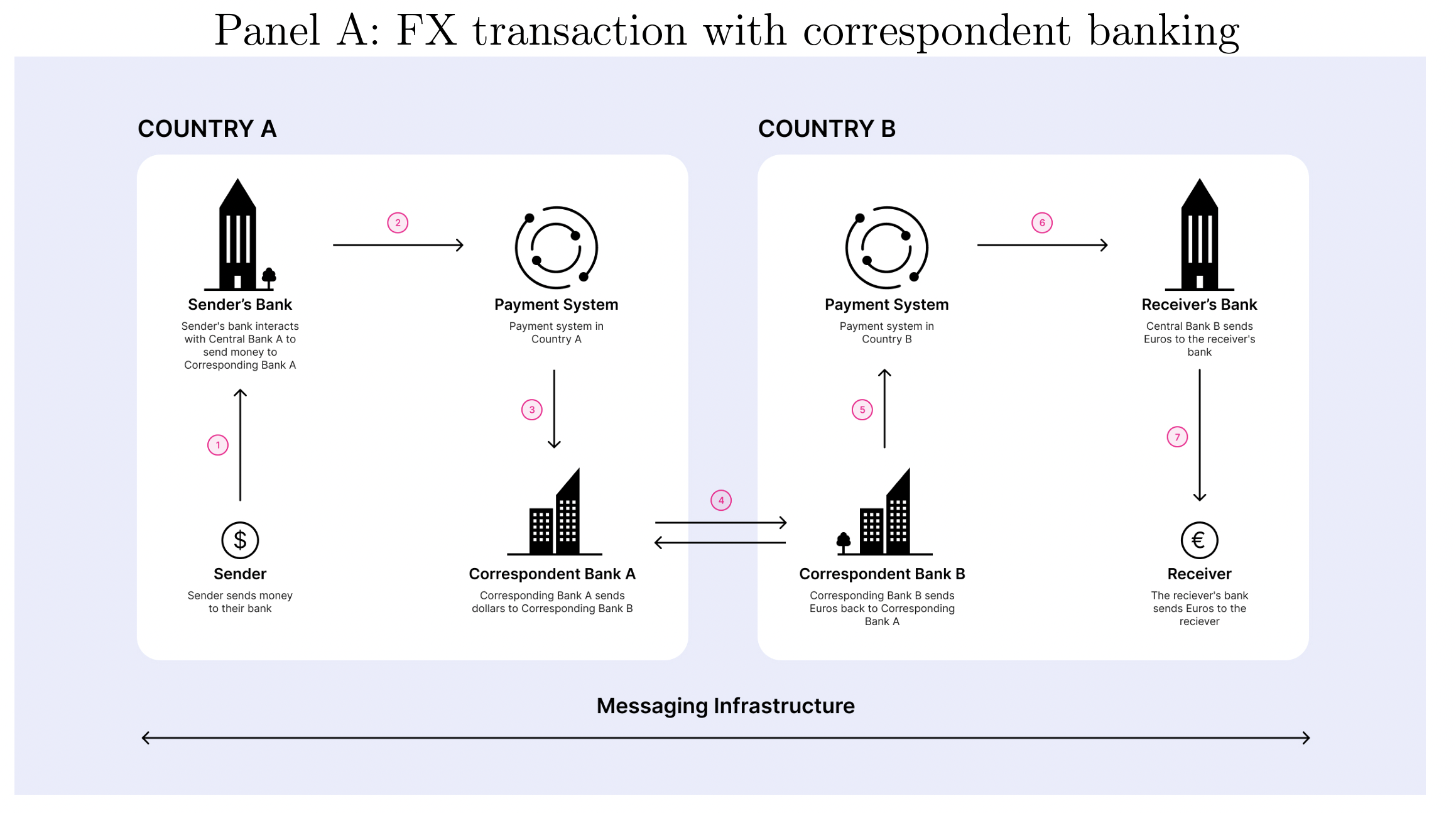

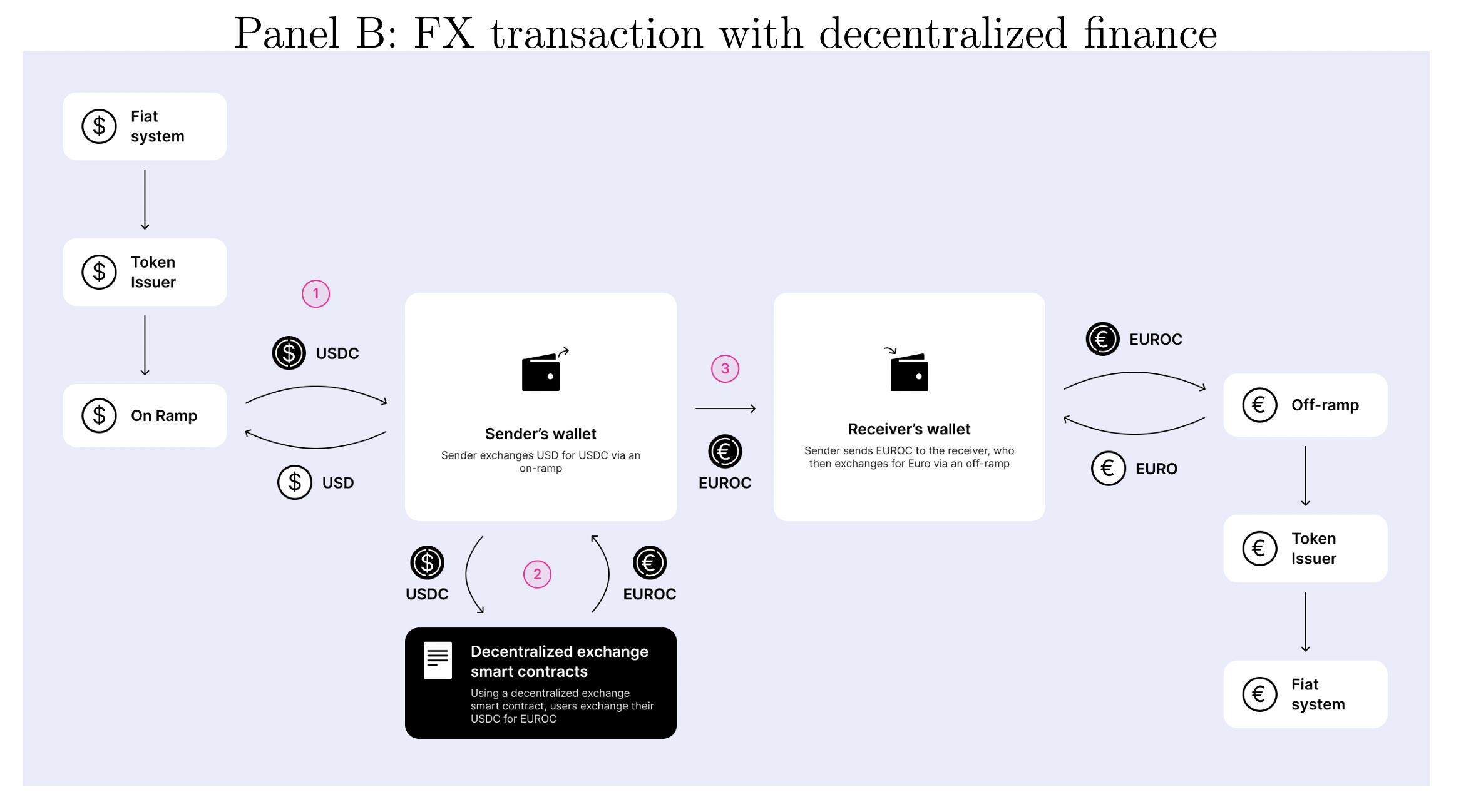

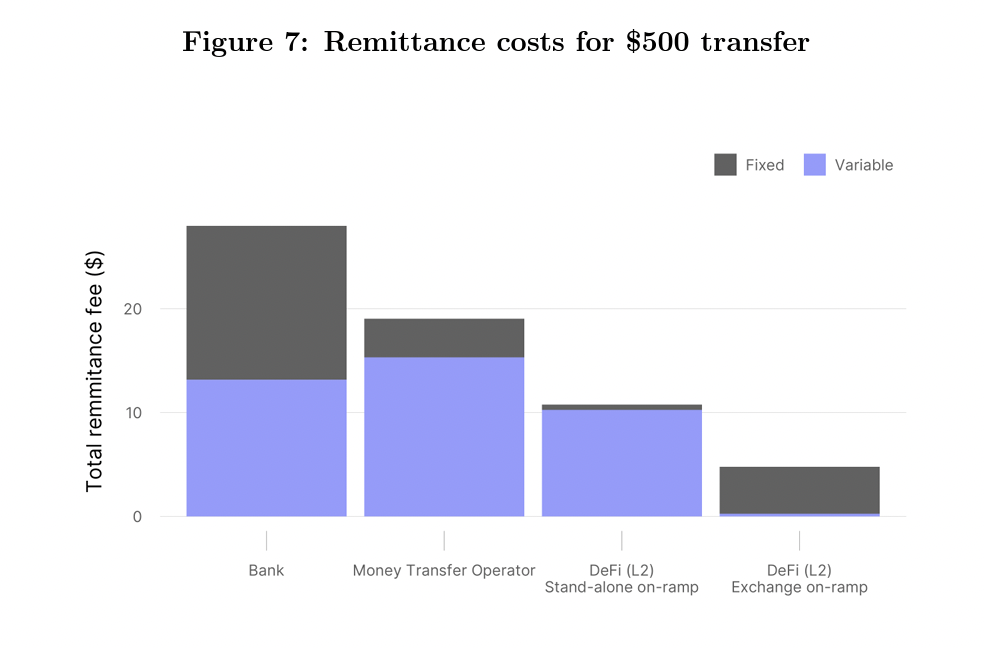

Source: On-chain Foreign Exchange and Cross-border Payments by Austin Adams, Mary-Catherine Lader, Gordon Liao, David Puth, Xin Wan (2023) [team from UniSwap Labs]

DeFi fees:

Central Bank-Issued Digital Currencies

Evolution

2008

2014/5

2019

2020

The Year is 2008: what the Toronto a la cart program teaches us about CBDCs

Cautionary tales for central bank innovation

what people want

what we got

Features of Digital Money

fast money

CBDC run by

Central Bank

CBDC on new communually run system

bank-issued stablecoin on public blockchain

|

What? |

||||

|---|---|---|---|---|

| 24/7 instantaneous | ||||

| borderless | ||||

| programmable | ||||

| privacy | ||||

| p2p | ||||

| no commercial 3rd party | ||||

| nominal fee |

Why are Blockchains challenging for current regulation?

What is blockchain=crypto? Some basic facts

anyone can use it

a open, general-purpose

digital value management tool

that maintains digital scarcity

ownership & control is direct and not intermediated

it's a protocol, not a thing

it does not belong to anyone

practically impossible to prevent the creation of code

borderless and digital

does not require high tech, a laptop is enough

requires use of tokens

What is blockchain=crypto? Some basic facts

anyone can use it

a open, general-purpose

digital value management tool

that maintains digital scarcity

ownership & control is direct and not intermediated

it's a protocol, not a thing

it does not belong to anyone

practically impossible to prevent the creation of code

borderless and digital

does not require high tech, a laptop is enough

requires use of tokens

The Investment Process

issuers

investors

services

needed & provided

A general purpose value management infrastructure:

intermediaries

separate institutions

The blockchain reality:

new institutions

emerged that do all three

tokens are often not intended to be investments!

... and that brought us ...

Regulators' Focus

MiCA

What is a security and why does it matter?

"What's the big deal \(\to\) just download a form from our website and register!"

\(\Rightarrow\) people (may) buy token with investment motive

\(\Rightarrow\) require protection from securities law

What is a security and why does it matter?

So what's the problem here?

But this has happened before!

When alternative trading systems emerged in the late 1990s, they were illegal exchanges under securities law because they were not broker-owned!

The S.E.C. approached the problem with no action letters and eventual changes in outdated rules

The Regulator's Dilemma

The Regulator's Dilemma

benign

crypto-assets

non-benign crypto-assets or crypto-assets that look like securities but are unregistered

crypto-assets that look like securities and are registered

crypto-assets that regulators feel comfortable to be traded on a platform under their supervision

The Regulator's Dilemma

The Reality of Markets

benign

crypto-assets

non-benign crypto-assets or crypto-assets that look like securities but are unregistered

crypto-assets that look like securities and are registered

crypto-assets that you feel comfortable to be traded on a platform under your supervision

The Dilemma

Final Thoughts

Some Final Thoughts

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

Slide deck 1