Andreas Park PRO

Professor of Finance at UofT

Andreas Park

Lecture 1: 30,000 ft overview

Lecture 2: Drilling down

Lecture 3: Finance Applications

Lecture 4: Smart contracts

Objectives

Objectives

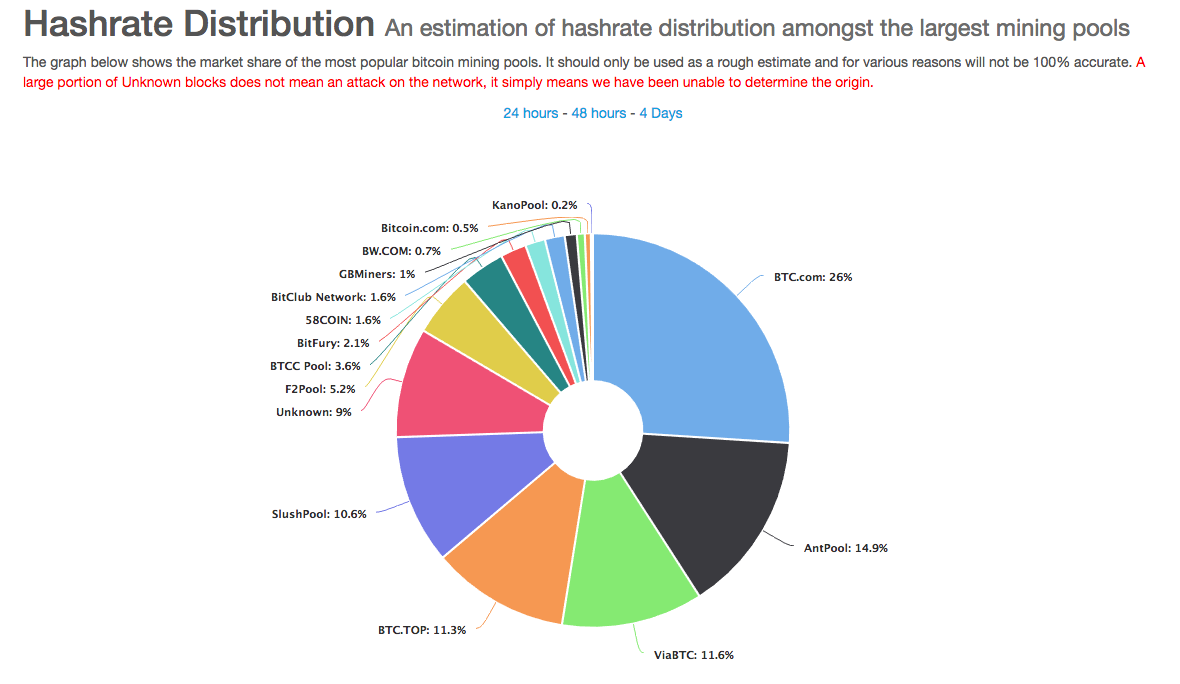

Source: blockchain.info 25/02/2018

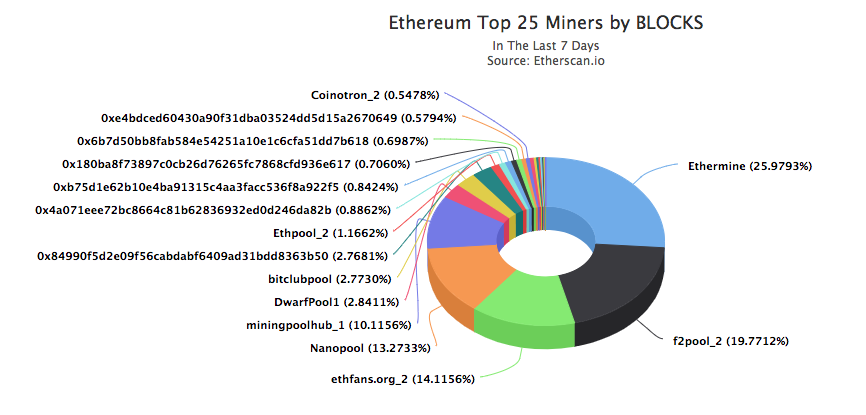

Source: etherscan.io 25/02/2018

Miners

have a huge say over changes in the protocol, and

they can collectively block changes, force forks, etc., and

have incentives that may run counter to the common good

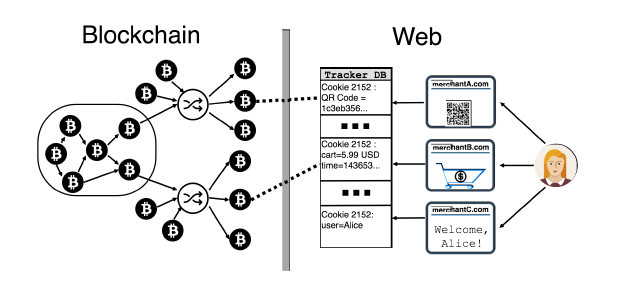

Root Problem

Solutions

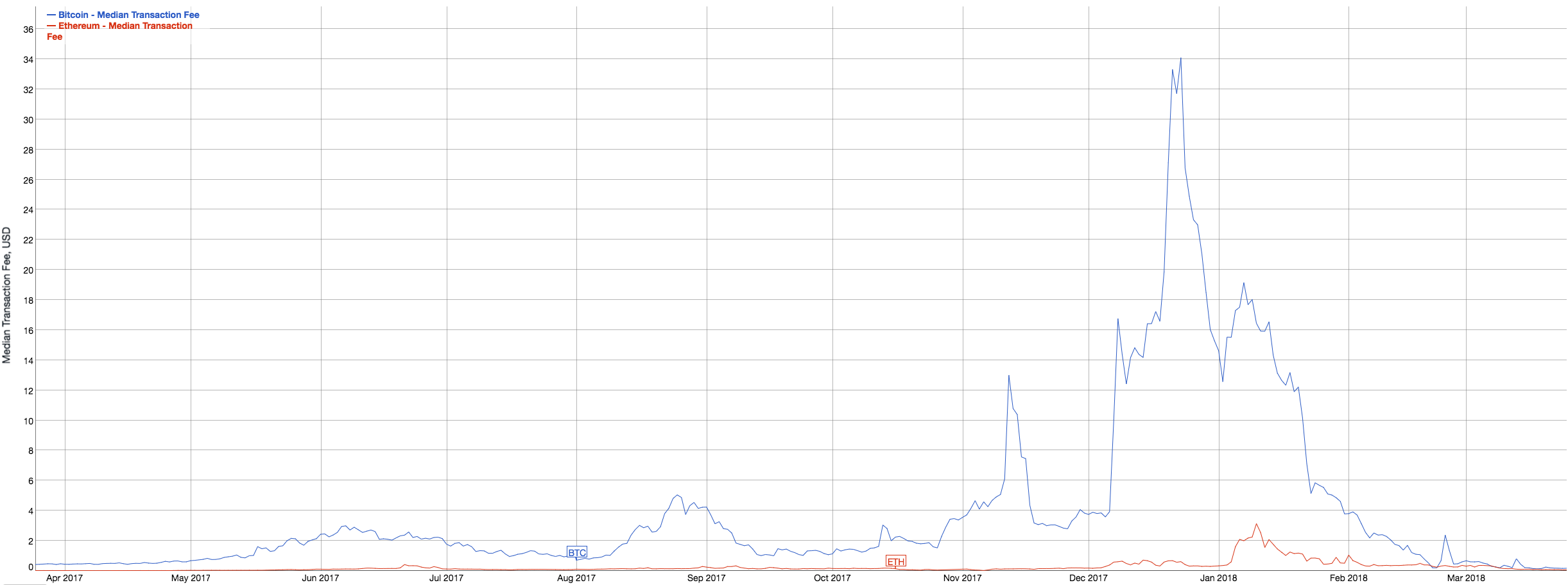

Source: bitinfocharts

S=1M

S'=8M

p

p'

demand=supply

revenue maximizing S*:

Empirical question:

1M vs 8M: which has higher revenue?

Root Problem

Solutions

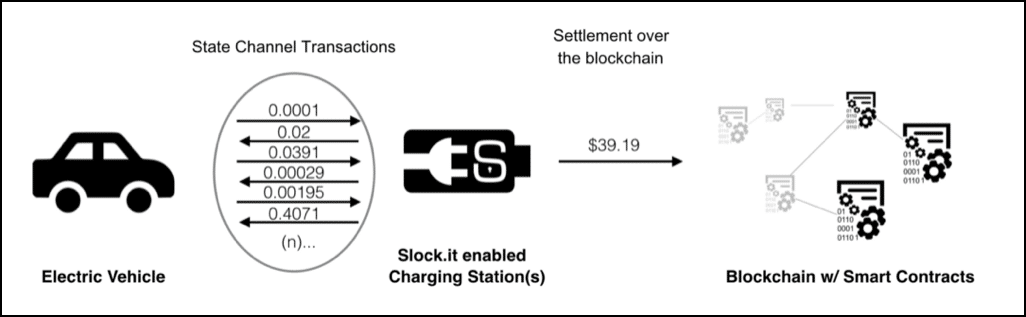

https://blog.stephantual.com/what-are-state-channels-32a81f7accab

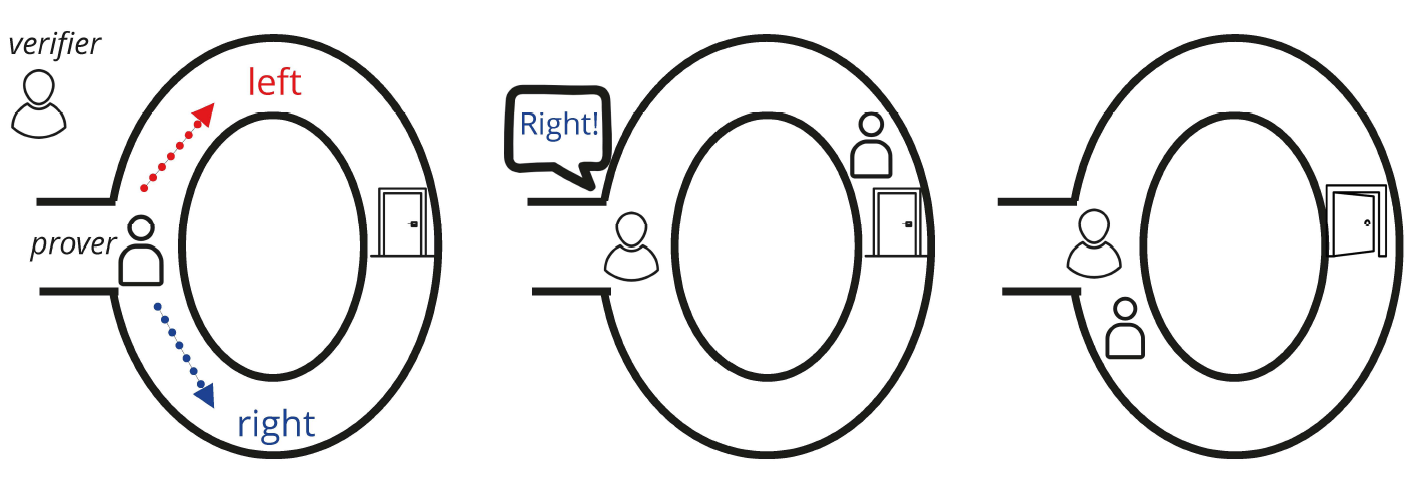

Root Problem

Solution

Where to add a new block B7?

My personal problem: I have not yet seen a convincing theoretical model of PoS

Root problem

Solutions

Terminology

Let's discuss it!

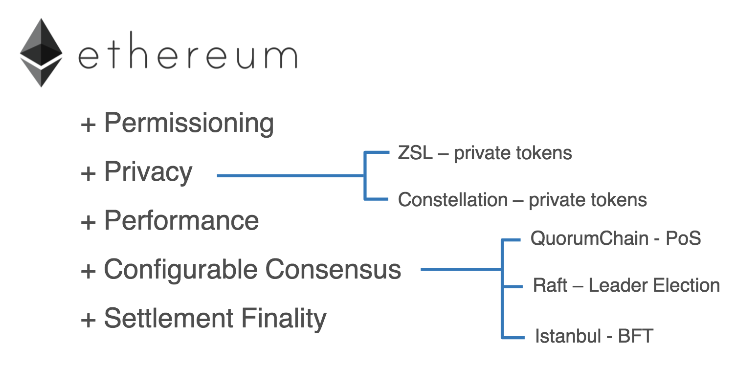

Common Idea:

Advantages

Description Idea:

Basic idea

Features

Premise

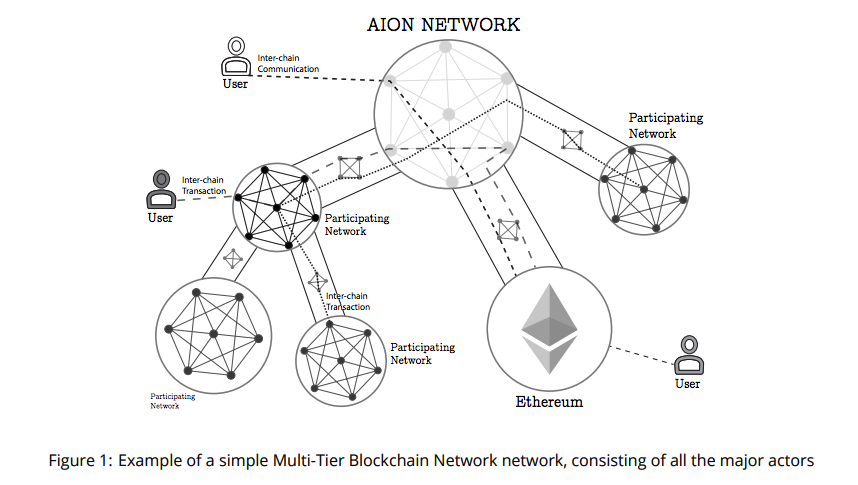

transaction bridge supported by validator votes

votes ("signatures") get stored on Ethereum

transaction bridge supported by validator votes; get paid in AION tokens

Special Features:

What is Hyperledger?

What is Sawtooth?

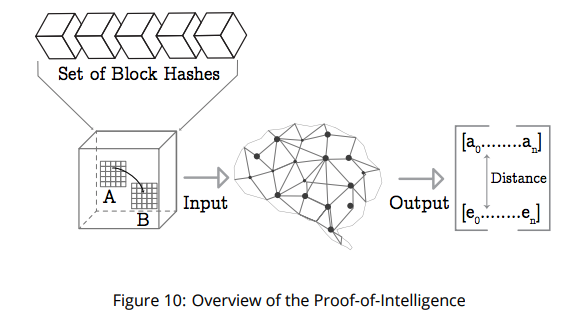

What is PoET?

My understanding (vastly simplistic)

Key roles

Key feature

My take:

Recently permitted by the SEC in the US and the CSA in Canada; restrictions (among others)

Limits for investors (per firm and total portfolio value)

Must used registered platform

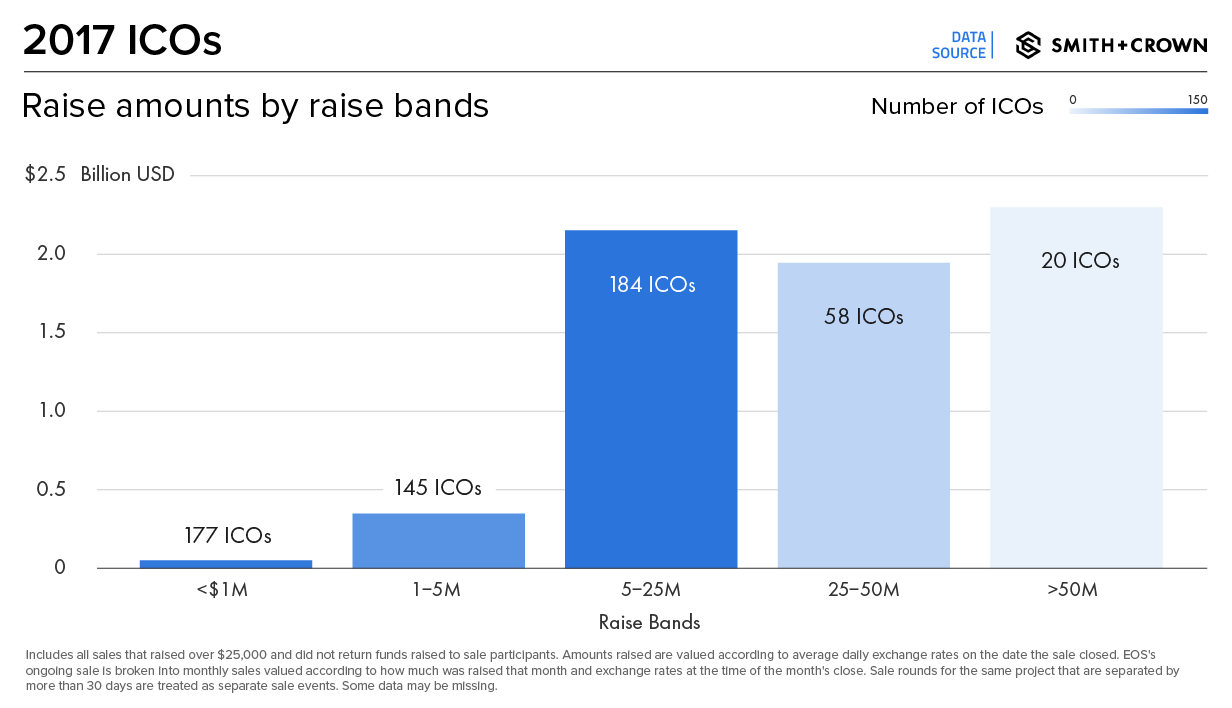

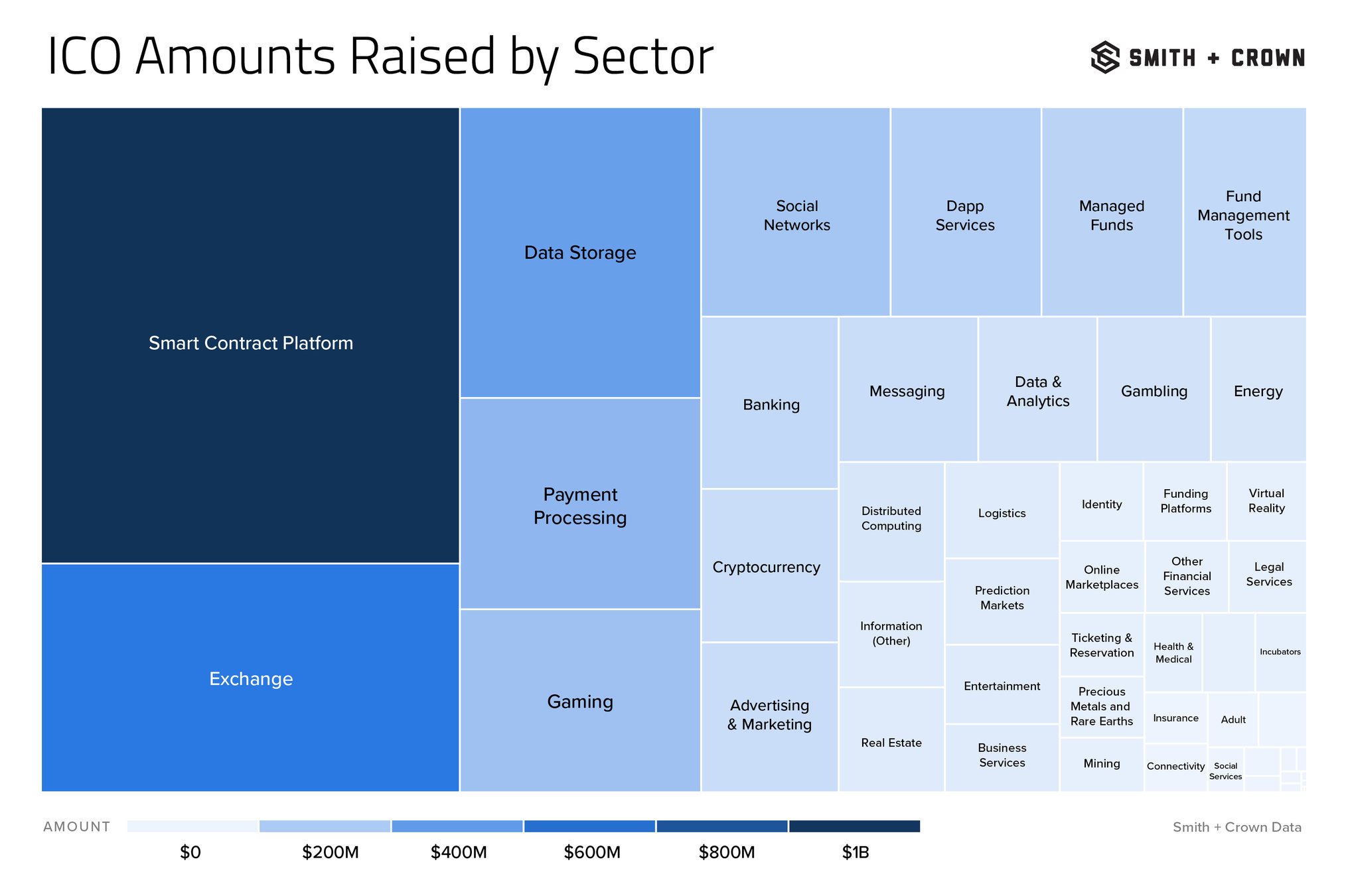

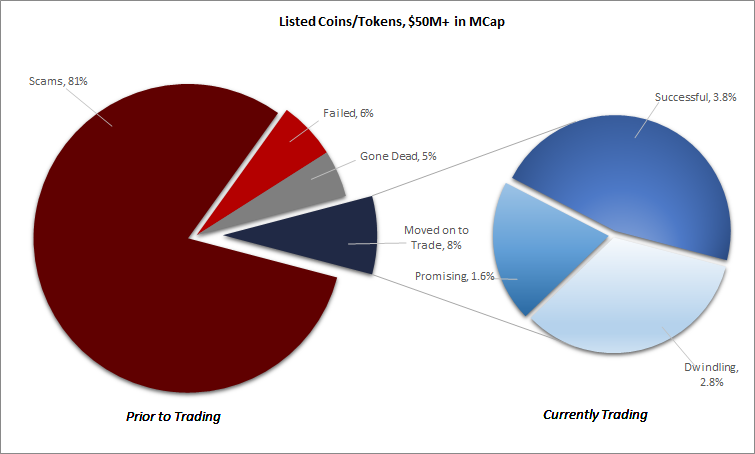

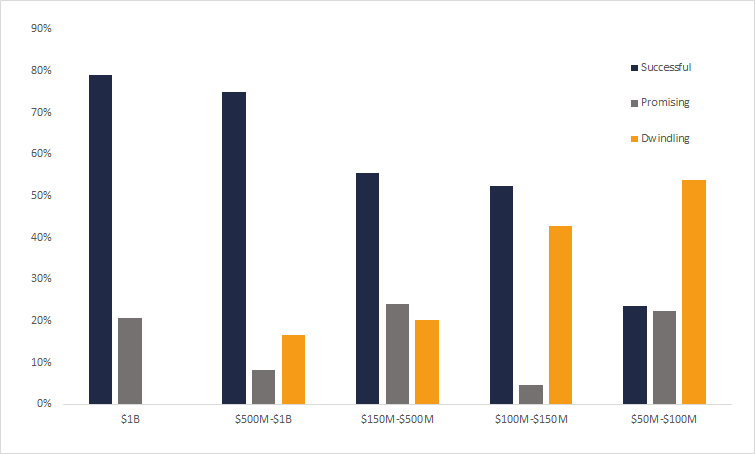

Classification (Source: Satis Group LLC)

Source: Satis Group LLC

Source: Satis Group LLC

“I believe every ICO I’ve seen is a security. … ICOs that are securities offerings, we should regulate them like we regulate securities offerings. End of story.”

Jay Clayton, Chairman, U.S. Securities and Exchange Commission, testimony before the United States Senate, February 6, 2018

“I have asked the SEC’s Division of Enforcement to continue to police this area vigorously and recommend enforcement actions against those that conduct initial coin offerings in violation of the federal securities laws”

Payment

Asset

Utility

in pre-financing and pre-sale phases of an ICO, tokens that confer claims to acquire tokens in the future

treated as securities

Payment

Asset

Utility

if additionally or only has an investment purpose at the point of issue:

=> treated as security

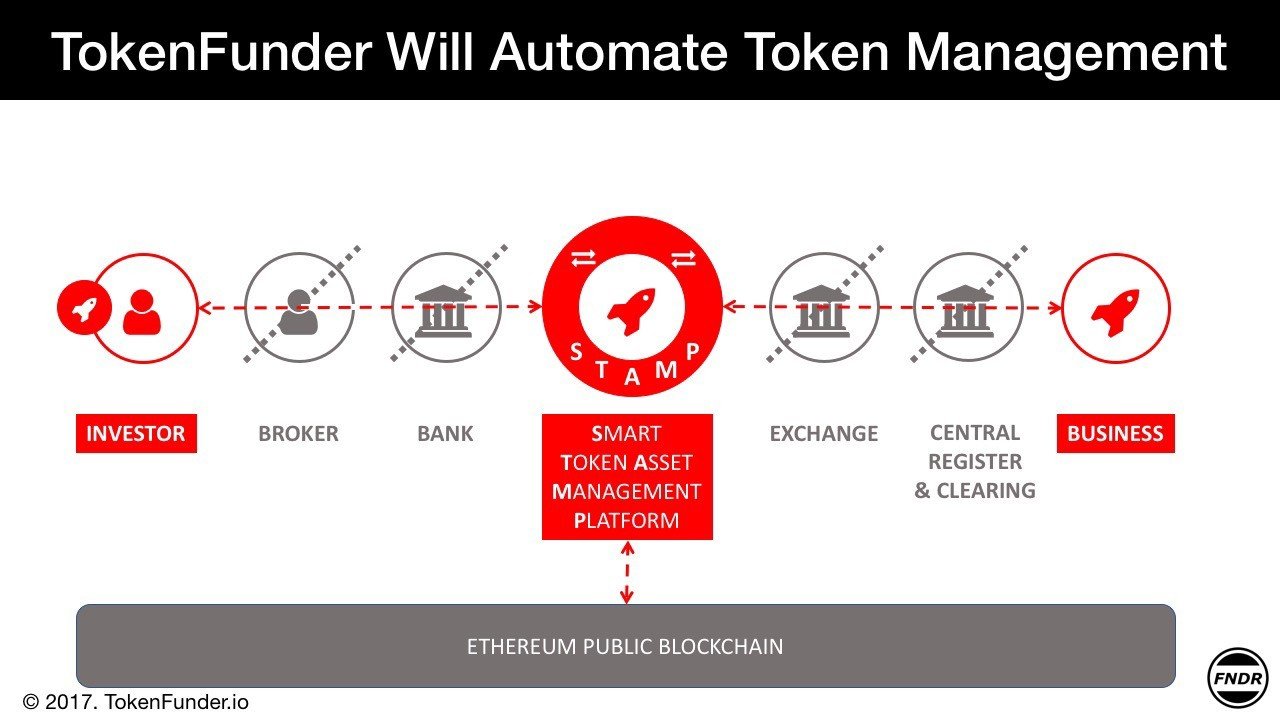

Source: Harbour (a tech firm)

Lower commissions with cryptocurrencies (no intermediaries to feed).

Small minimum investment amounts.

Global phenomenon, global investor base.

Tokens are readily tradable.

Can be pre-programmed to carry out the company’s incentive payouts — or returns — as set out in White Papers and Investor Prospectuses.

Contingent fundraising.

Milestone automation.

Retail

Institutional

Pro-Traders

Exchanges

Wholesellers

Dark pools

Broker Internalizations

Exchanges

Wholesellers

Dark pools

Broker Internalizations

(

(

Retail

Institutional

Pro-Traders

Rule: must send to exchange with best price

Exchange

Wholeseller

market order

limit order

In Europe: no best price obligation

Exchange

Dark pools

Type 2: "borrow" broker-dealer system

Type 1: licenced broker-dealer

risk control

You commonly don't access the market directly.

Brokers take many decisions but they are bound by regulations.

Critical: markets are formally linked by best-price rules.

A glimpse of overall infrastructure

Sue wants to sell ABX

Bob wants to buy ABX

sell order

buy order

Clearing House

Stock Exchange

Broker

Broker

3rd party tech

custodian

custodian

record beneficial ownership

central bank for payment

Retail, Institutions, and Pro-Traders are indistiguishable

not clear whether and which institutions are active

Exchanges

Dark pools

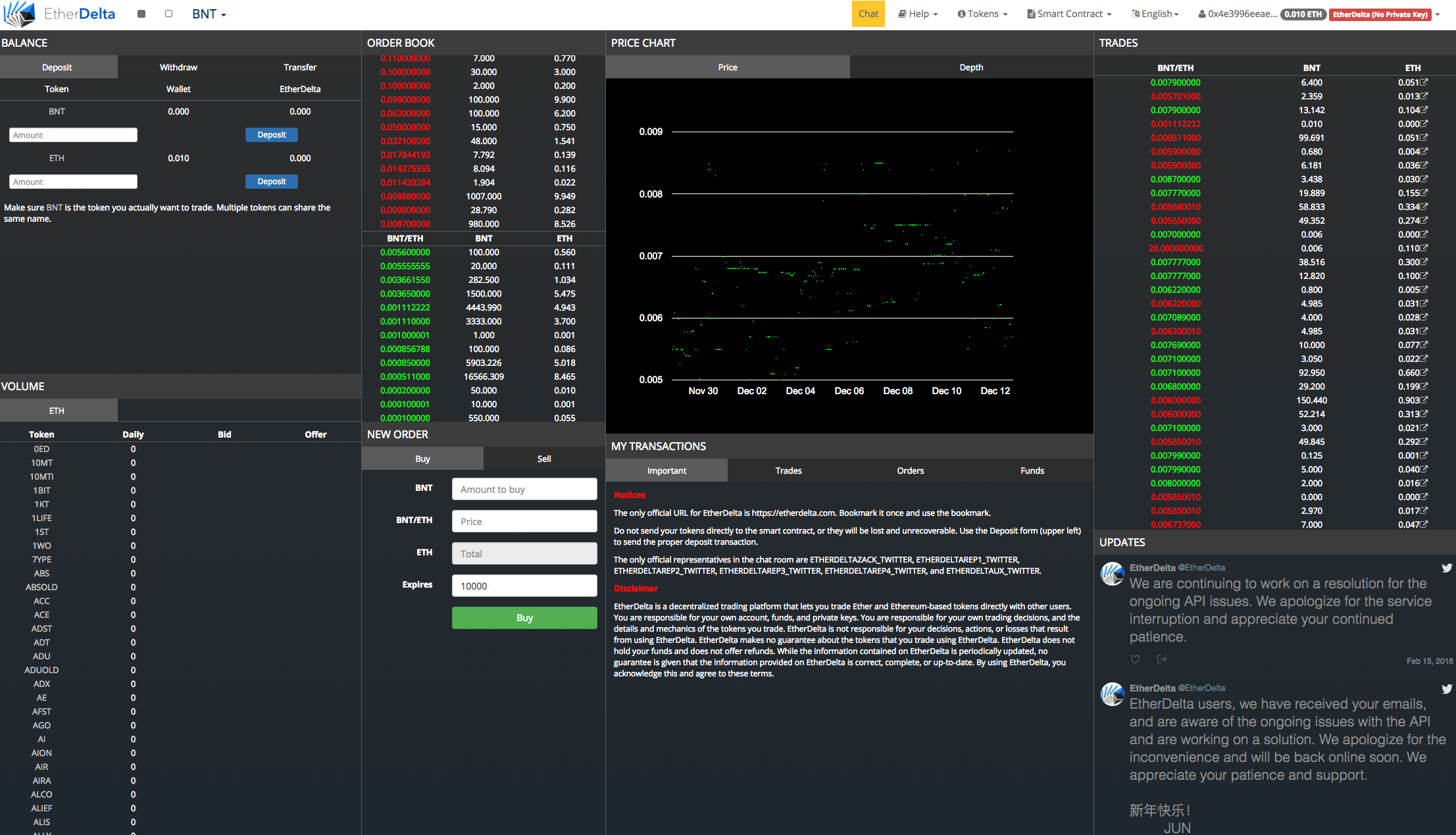

Smart On-chain contracts

Exchanges

Smart Contract

Order Driven

Market Maker

Exchanges

Smart On-chain contracts

Exchange

Internalizer

Wholeseller

Darkpool

Investor

Venue

Broker

Settlement

Investor

Venue

Settlement

On chain

(website)

e.g. AWS Ruby

(decentralized)

(call to smart contract)

By Andreas Park

This deck is for the third of four lectures on Blockchain technology in finance, taught at the Rotman School of Management, Spring 2018; for my 2018/19 classes, I will have split this class into multiple pieces, and this set of slides will become obsolete.