Andreas Park PRO

Professor of Finance at UofT

Katya Malinova

Andreas Park

Andriy Shkilko

2005

2009

2010

2011

2012

2013

2014

2015

2006

2007

2008

Source: RBCCM

don't try to do too many things or to be too nitty-gritty

must pay to adapt, no exceptions for venues

design, methodology, procedure

avoid biases and intrinsic noise

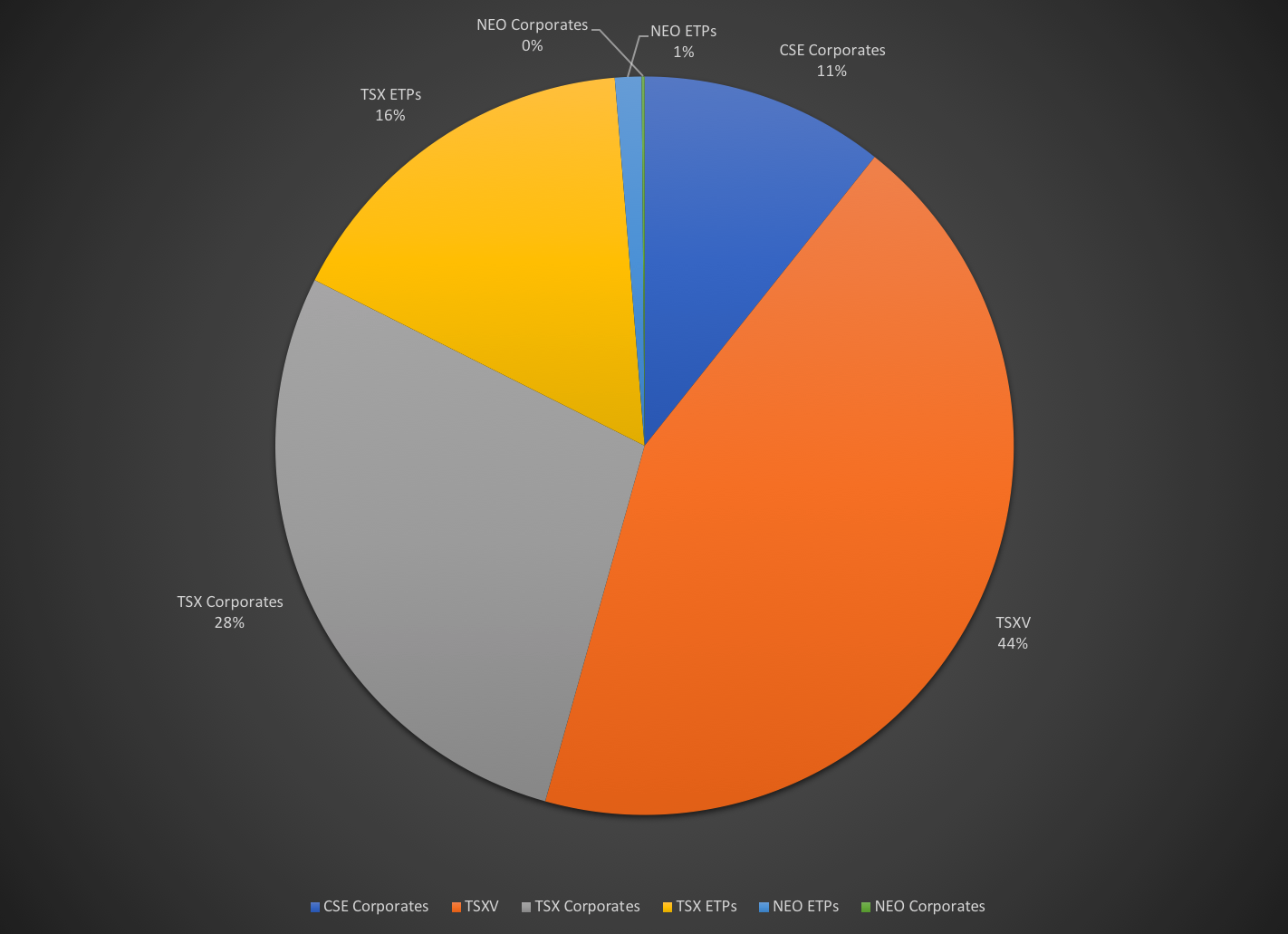

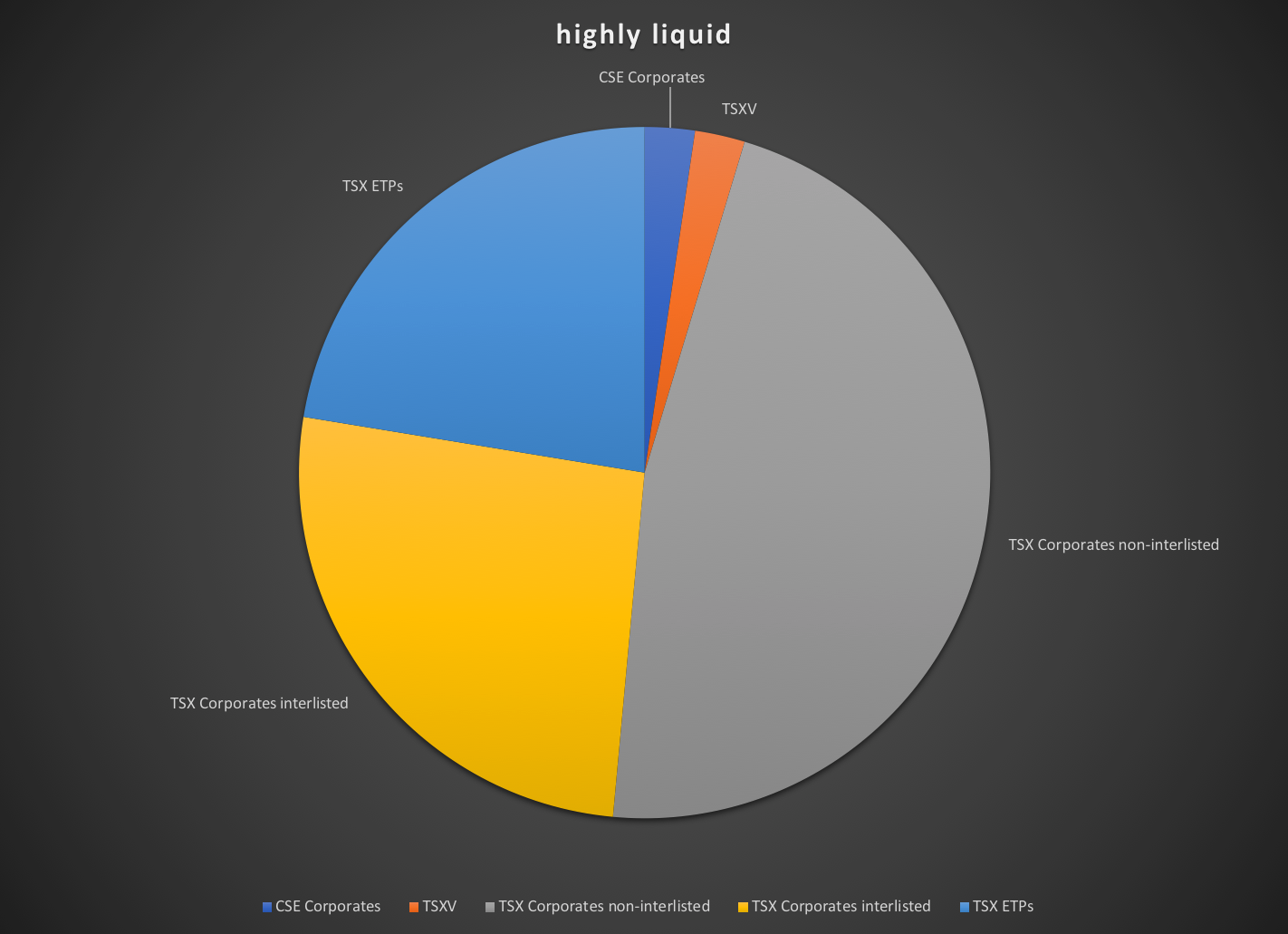

rebate prohibition for approximately 120-160 securities

prohibition group = approximately half of highly liquid, all venues (inverted, unprotected)

design, sample selection & analysis codes publicly posted

focus on highly liquid securities, split into 3 subgroups

align with SEC pilot and coordinate on sample

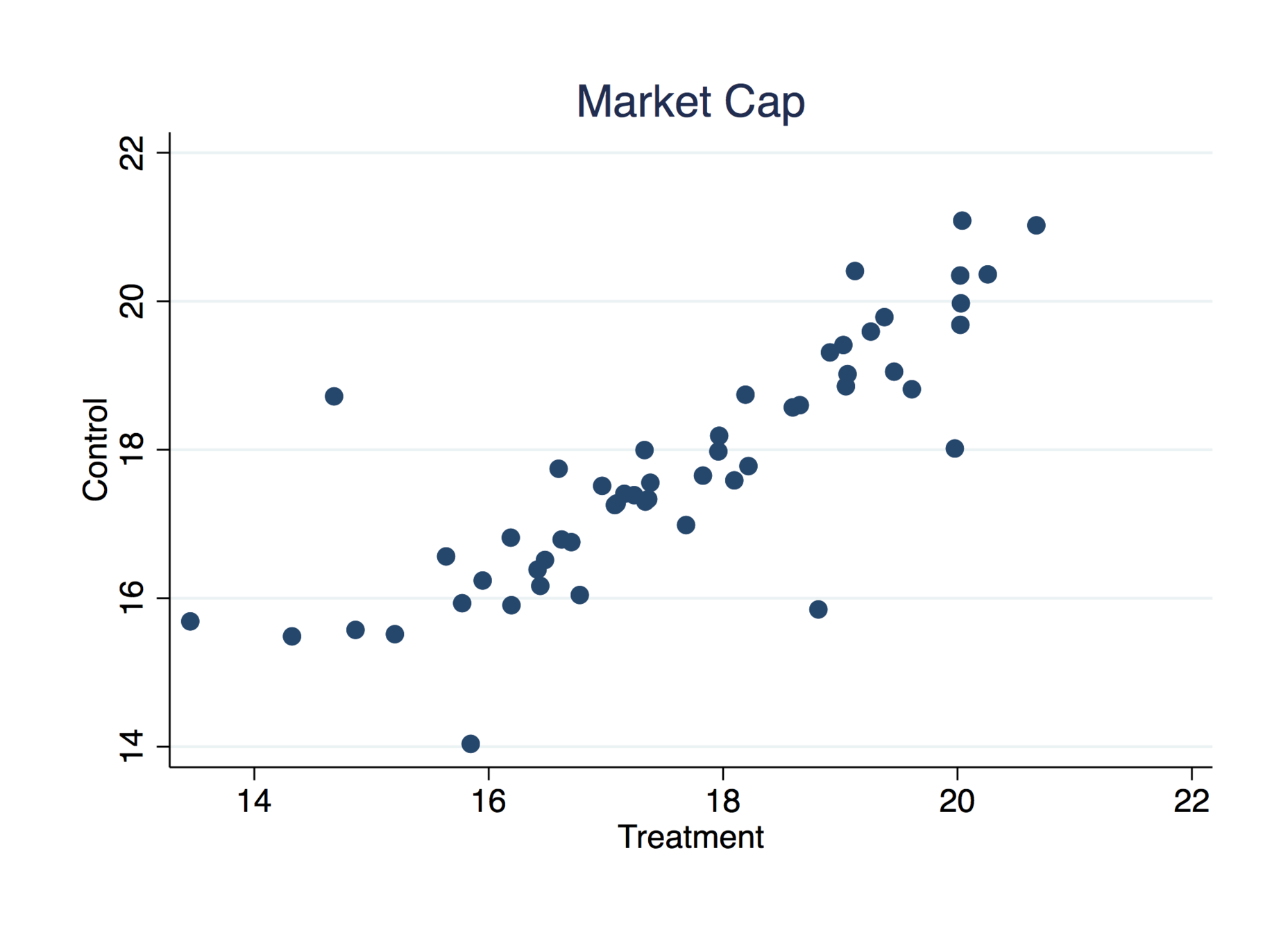

many securities almost never trade

low activity levels

large spreads/ single-sided quotes

=> noisy data

*based on IIROC definition

\(\sum_{k=1}^M \left( \frac{\textit{C}_{k}\!^i - \textit{C}_{k}\!^j}{\textit{C}_{k}\!^i +\textit{C}_{k}\!^{j}}\right)^2\)

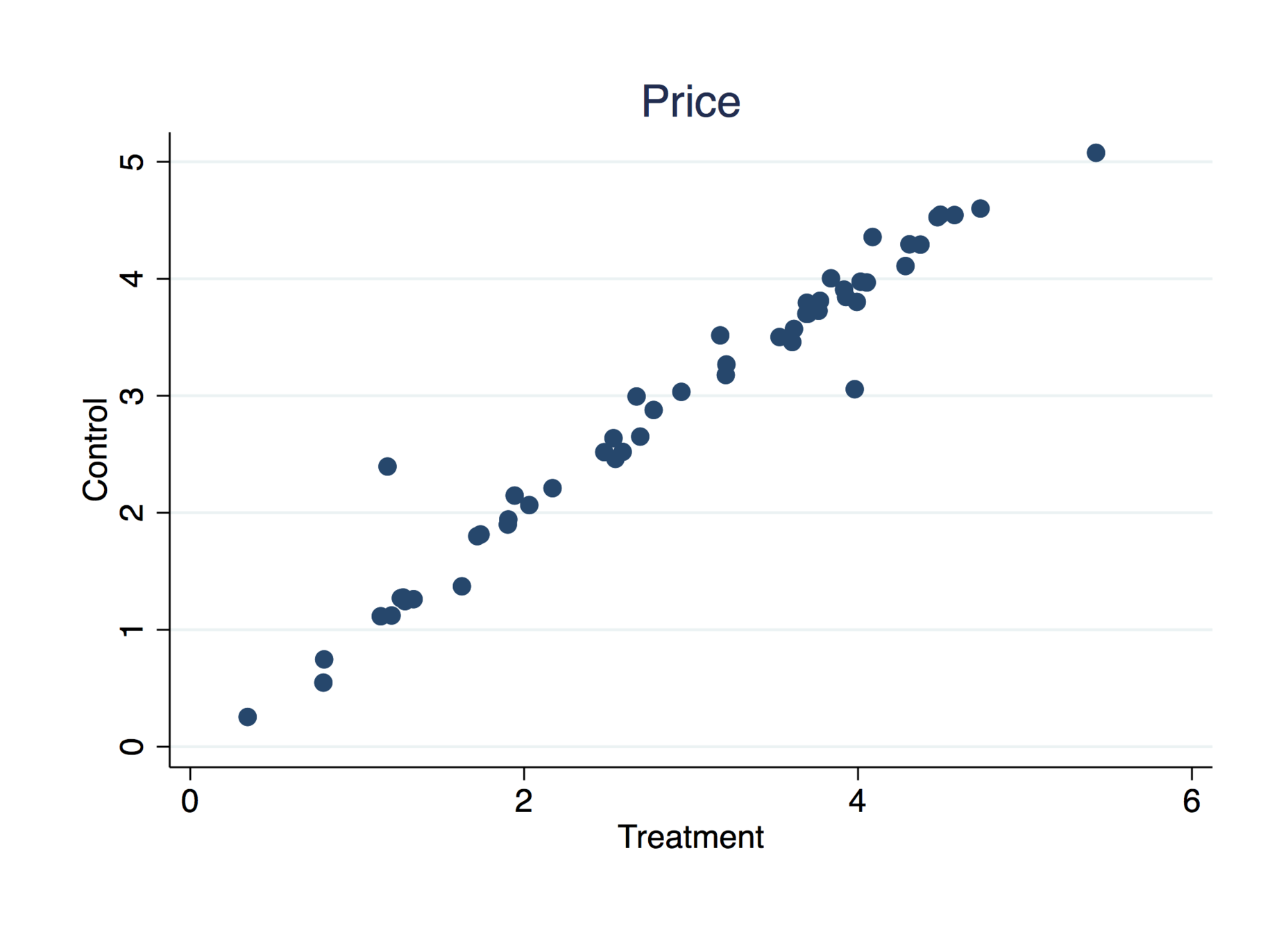

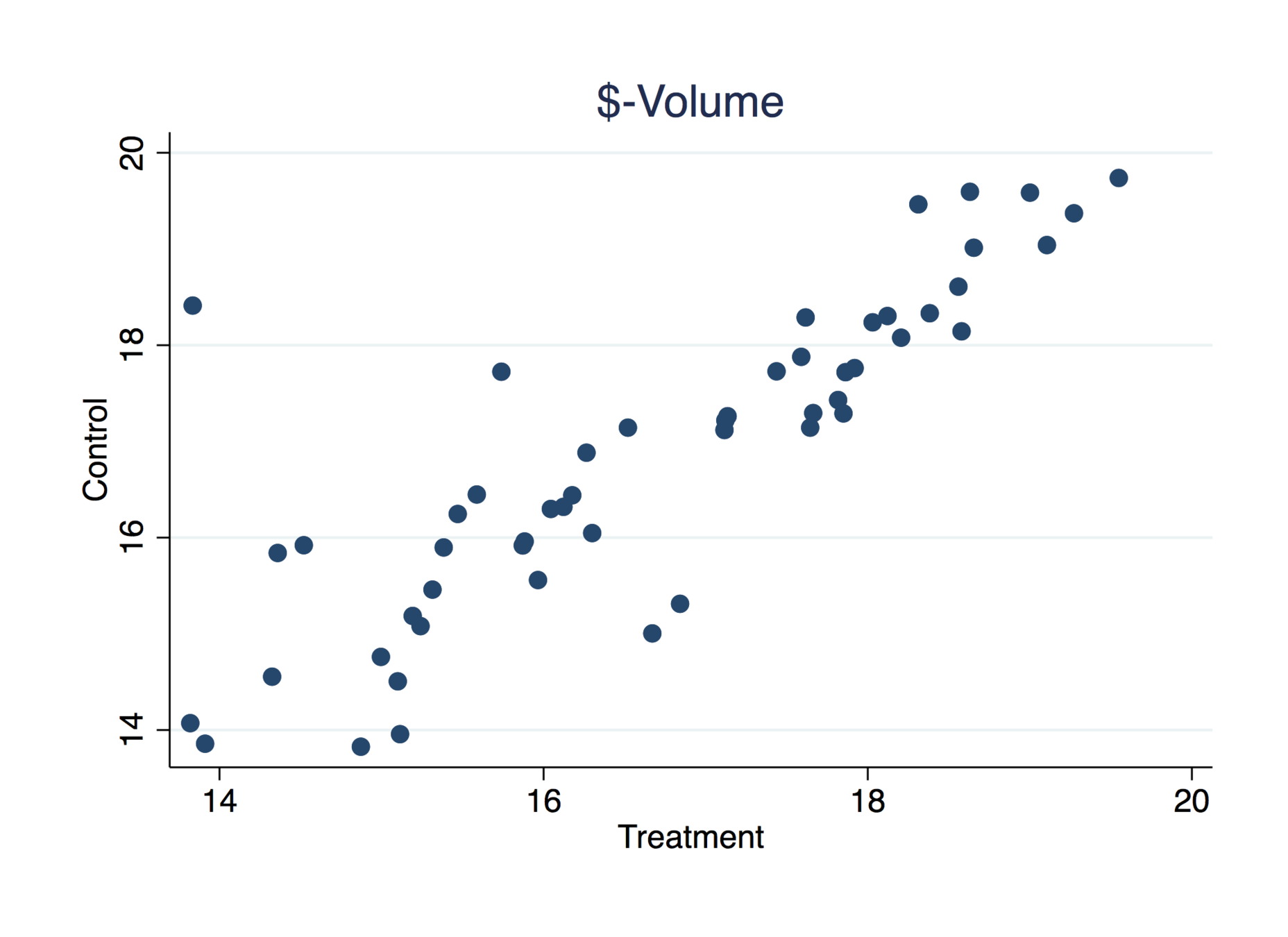

Visual: this is what we are looking for

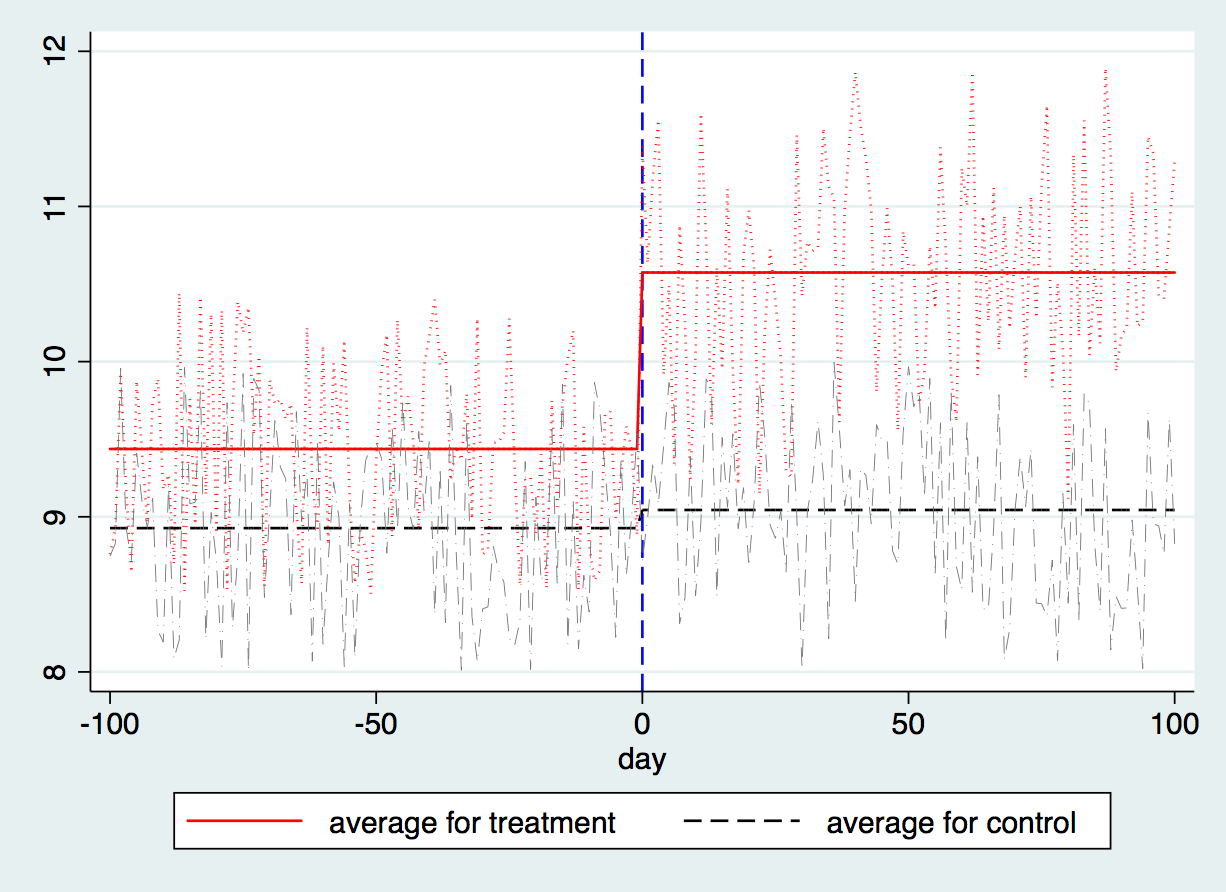

Mathematically: we estimate

\[\Delta{DV}_{it}=\alpha\cdot \textit{pilot}_{t} +{\textit{other } \atop \textit{variables}_{t}}+\delta_i+\epsilon_{it}\]

and ask: is \(\hat{\alpha}\not=0\)?

Question to industry:

Question to industry:

Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University

Associate Professor of Finance at the University of Toronto Mississauga and the Rotman School of Management, and Research Director at the Rotman FinHub

Associate Professor of Finance and Canada Research Chair in Financial Markets at Wilfrid Laurier University’s Lazaridis School of Business and Economics

By Andreas Park

The deck used at the September 12 CMI event at the Rotman School of Management.