Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

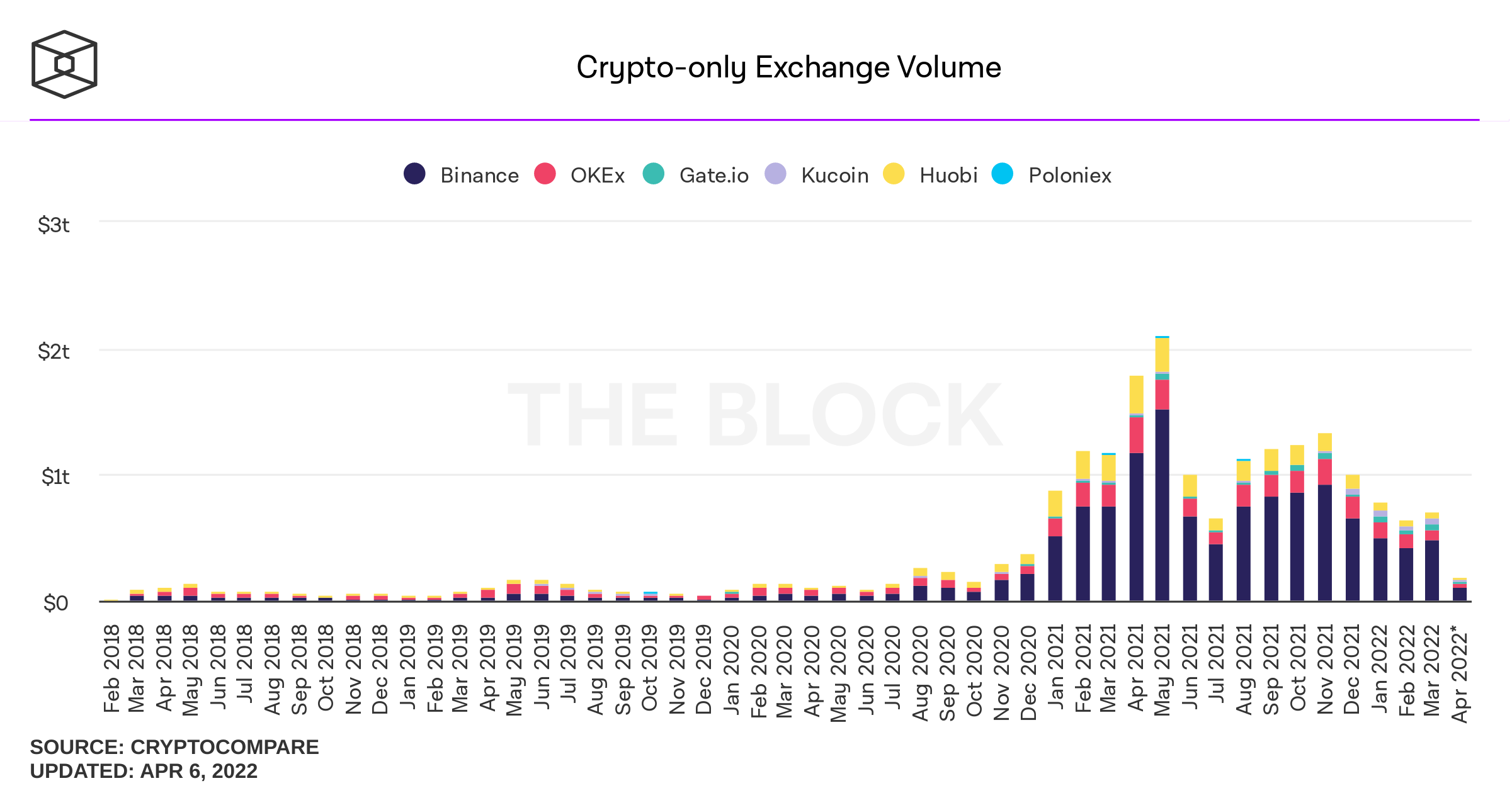

(307 CEX, rest DEX)

approx:

400B p.m.

approx:

700B p.m.

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy BTC

sell BTC

move BTC to Kraken

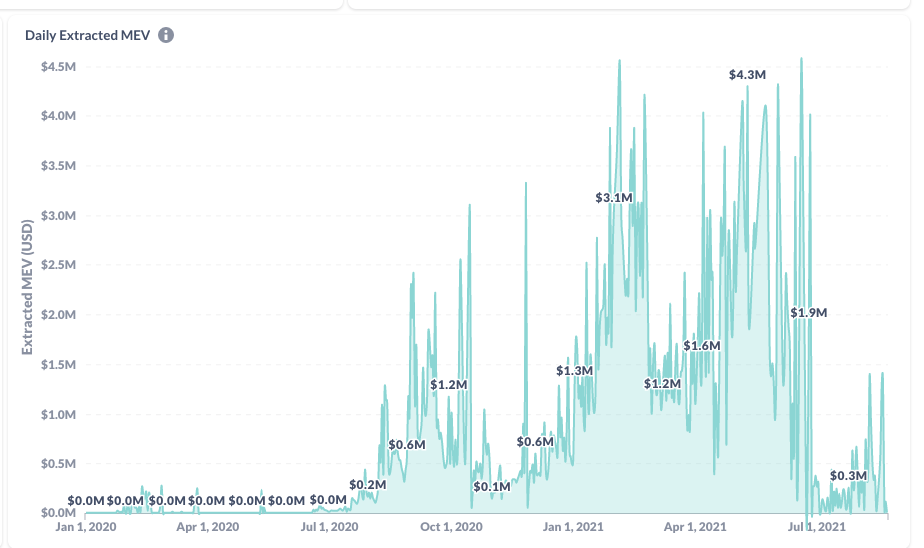

Crypto Wash Trading, Lin William Cong, Xi Li, Ke Tang, Yang Yang

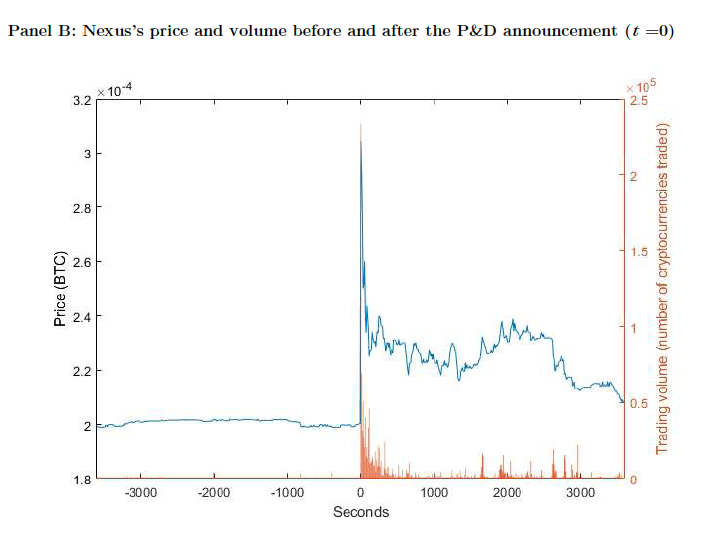

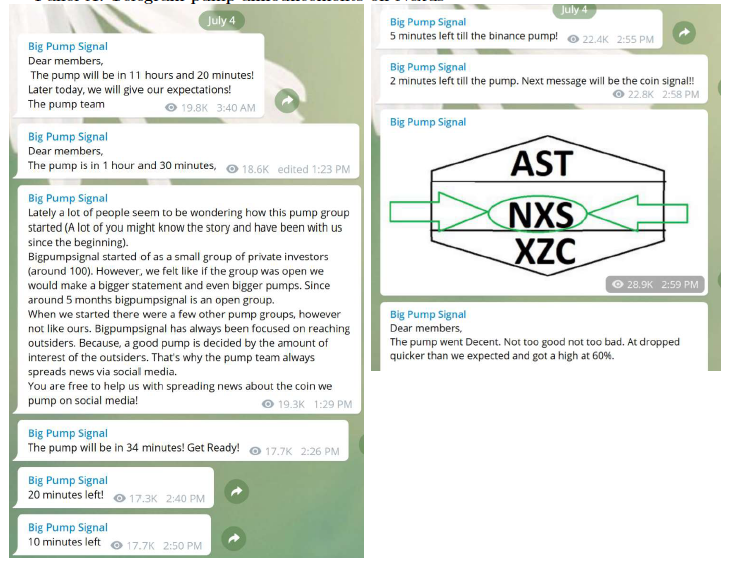

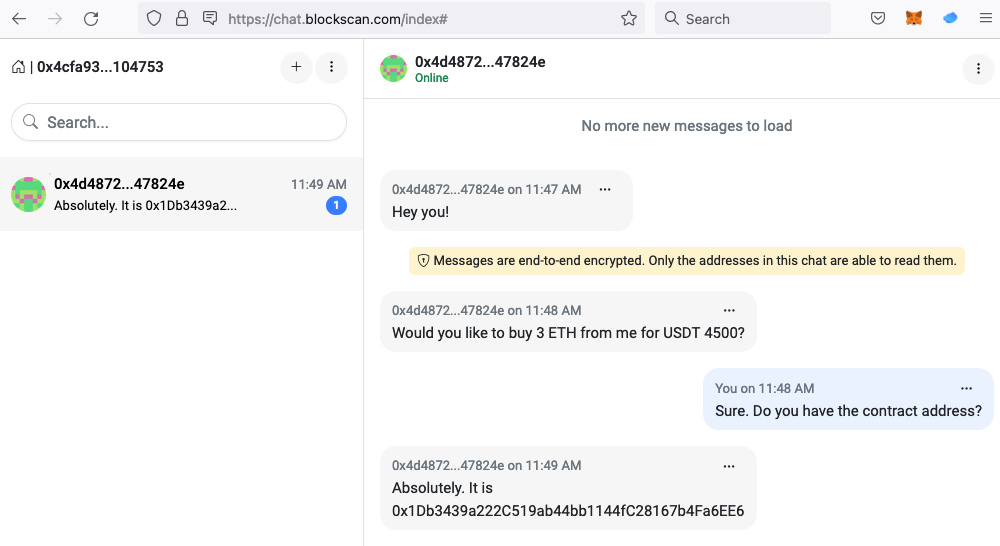

What is pump and dump?

arranged via Telegram Channels

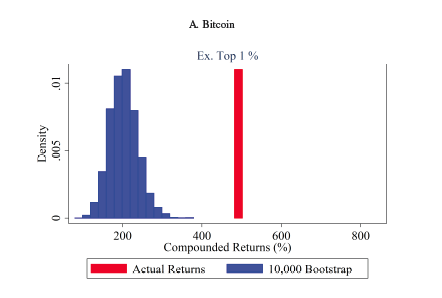

the 1% of hours with the strongest lagged Tether flow are associated with 58.8% of the Bitcoin buy-and-hold return over the period.

the "normal-times" returns

By yours truly, Dec 2017: "What really concerns me about the current craziness is the role of the cryptocurrency exchange platforms, such as Coinbase, Quadriga, or Bitfinex, which most people use to buy Bitcoins. These are like banks that hold deposits. For cryptocurrencies to succeed it is critical that these interfaces with the real world are financially robust. Are they? Do they have all the Bitcoins they sell? Can they always satisfy depositors’ demands?"

Source: https://vitalik.ca/general/2022/11/19/proof_of_solvency.html

seller

buyer

New institutions!

invariant \(k=4\times4=16\)

Instantaneous exchange rate:

1 = 1

Contract deposit:

sell 4 DAI for USDC

what price will therefore be quoted?

how many USDC?

Problem: large "slippage" (or price impact)

\(X-Q\)

\(X\)

\(Y+P(Q))\)

\(Y\)

\(c=X\cdot Y\)

Does it matter economically?

\(X-Q'\)

\(X\)

\(X-Q\)

\(X-Q'-Q\)

receive \(-P(-Q|X-Q'-Q)\)

pay \(P(Q)\)

\(P(Q'|X-Q)\)

\(Y\)

\(Y+P(Q)\)

\(Y+P(Q')\)

\(Y+P(Q)+P(Q'|X-Q)\)

\(P(Q')\)

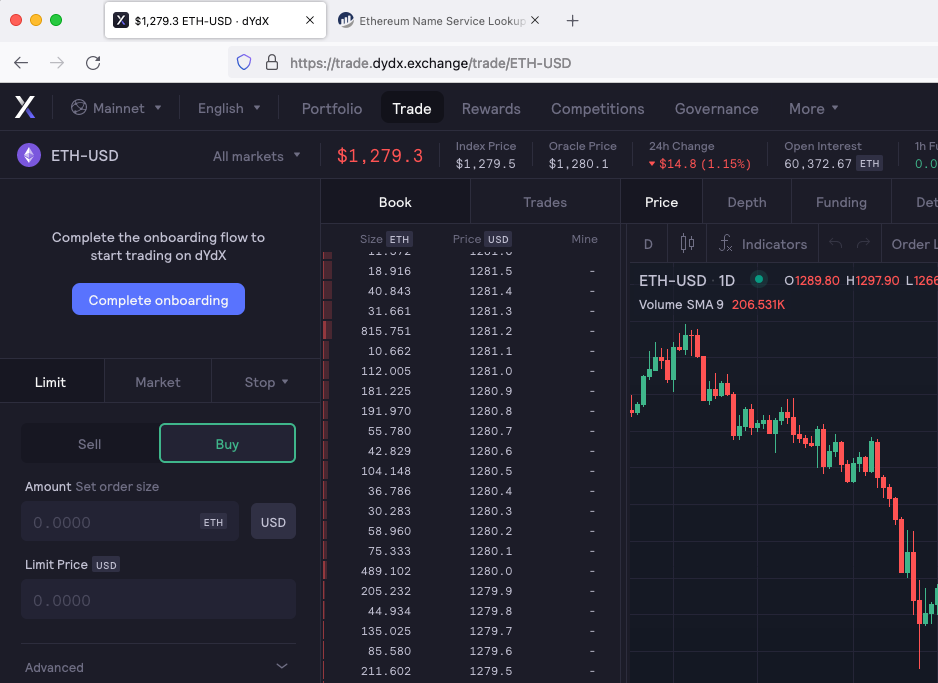

Example: Feb 2022, ETH-USDC trade

a

b

c

d

e

f

g

|

Option |

Exchange-side risk |

User-side risk |

|

Custodial exchange (eg.Coinbase today) |

User funds may be lost if there is a problem on the exchange side |

Exchange can help recover account |

|

Non-custodial exchange (e.g.Uniswap or dydx today) |

User can withdraw even if exchange acts maliciously |

User funds may be lost if userscrews up |

Source: https://vitalik.ca/general/2022/11/19/proof_of_solvency.html

\[\begin{array}{rcl} DL(P_0,P_1)&=&P_1(X_0-Q)+Y_0+P(Q)-(P_1X_0+Y_0)\\ &=& P(Q)-P_1\cdot Q \end{array}\]

quantity

price

\(Q\)

\(p(Q)\)

\(P^{\mathsf{dp}}(Q)=\int_0^Qp(q)~dq\)

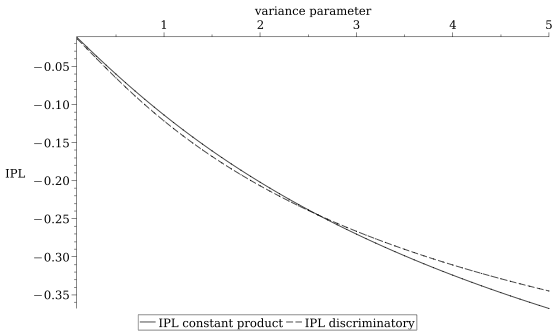

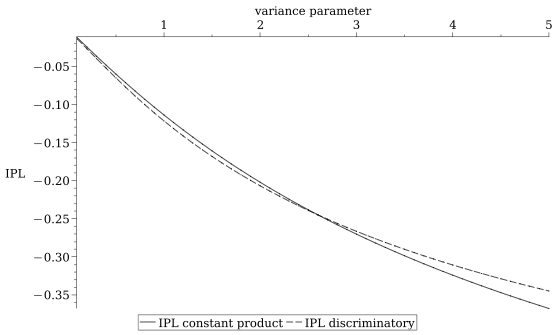

Gamma Distribution

Constant

product

worse

Constant

product

better

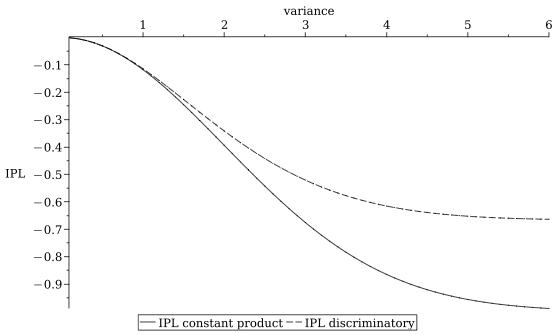

Log-Normal Distribution of Returns

Constant

product

is always worse

By Andreas Park